Enterprise Resource Planning Integration Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.45 Billion |

| Market Size (2031) | USD 24.25 Billion |

| Growth Rate (2026 - 2031) | 10.92% CAGR |

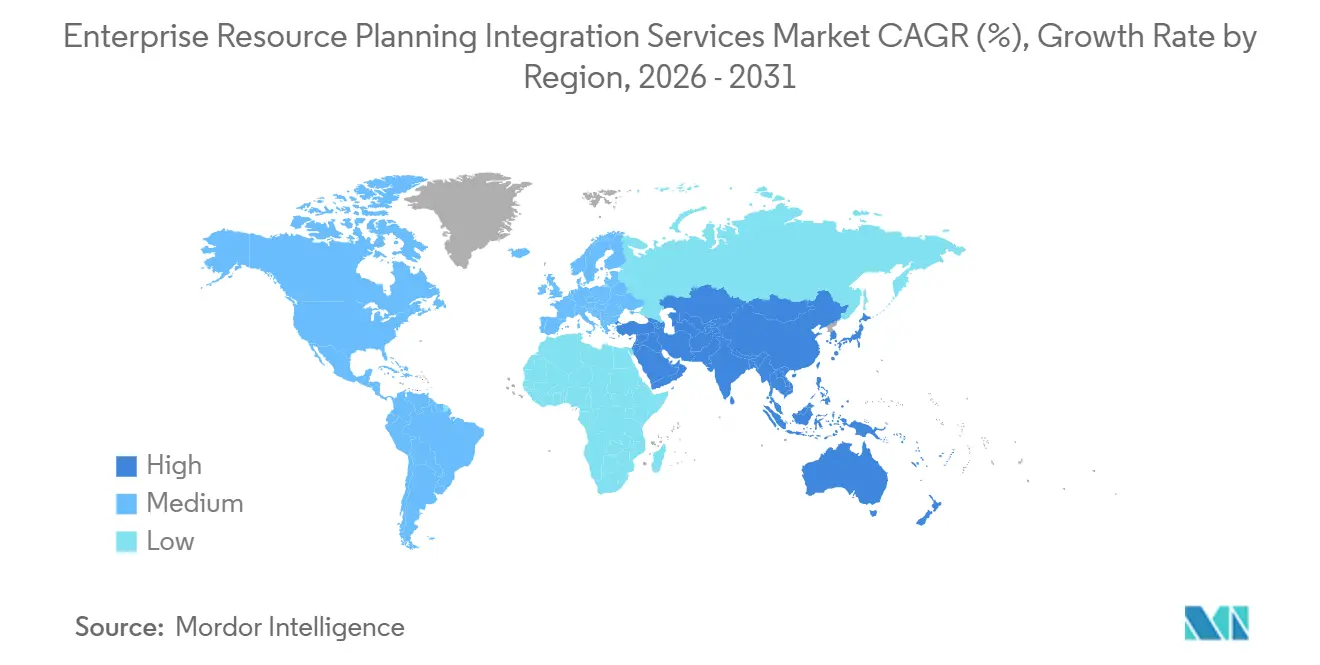

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

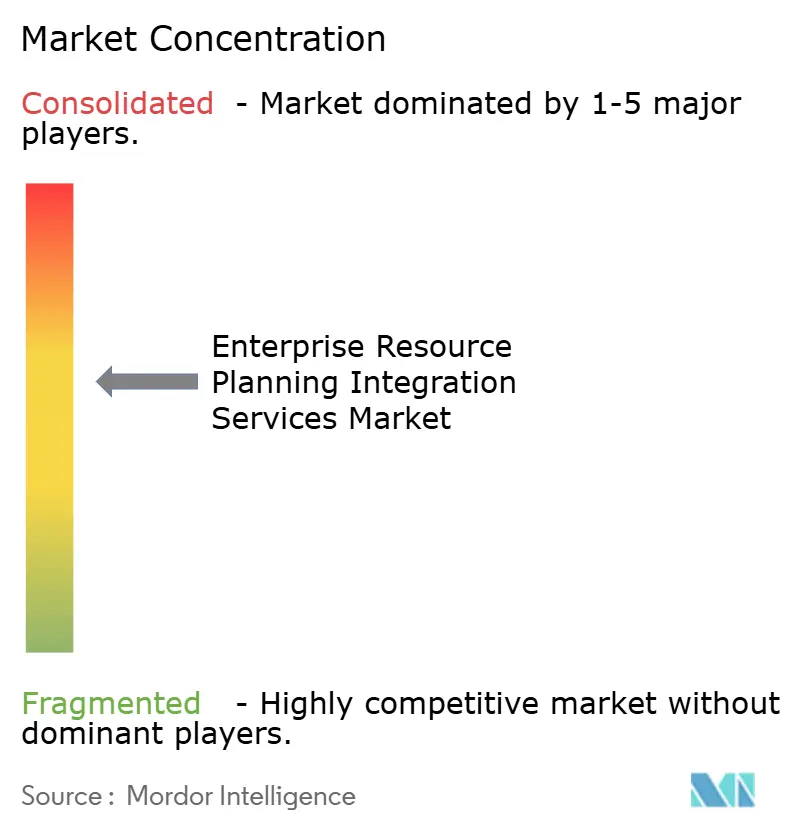

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Resource Planning Integration Services Market Analysis by Mordor Intelligence

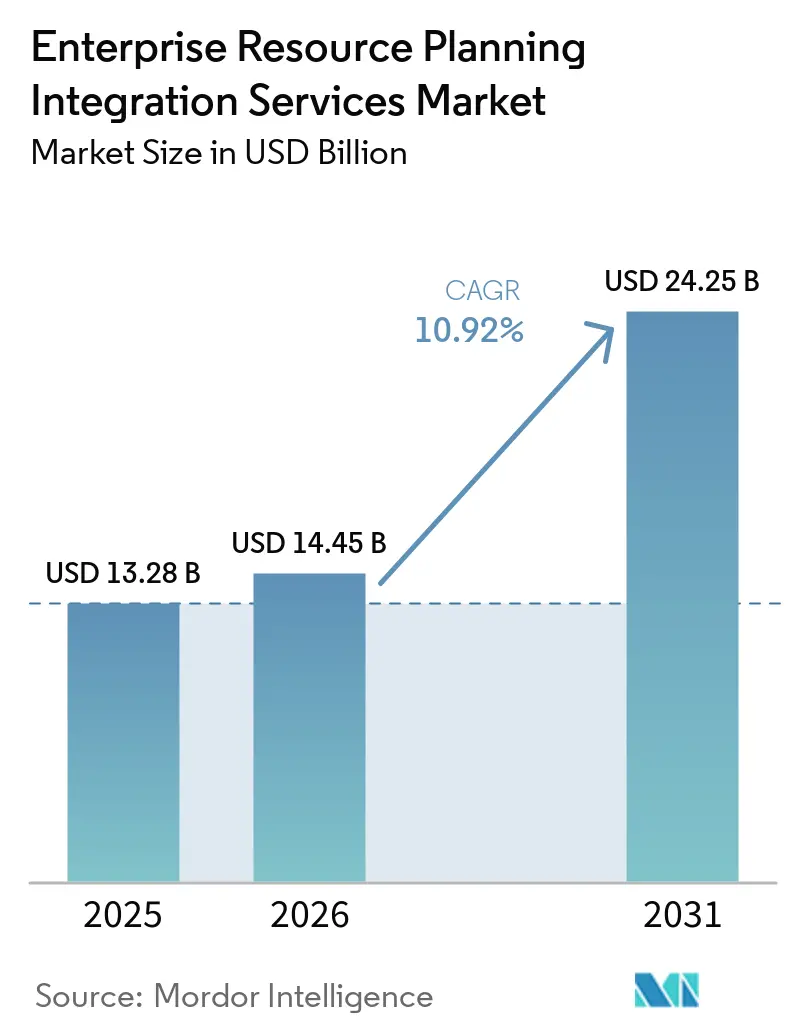

The ERP integration services market size is projected to be USD 13.28 billion in 2025, USD 14.45 billion in 2026, and reach USD 24.25 billion by 2031, growing at a CAGR of 10.92% from 2026 to 2031. The upswing reflects enterprises retiring brittle point-to-point connectors in favor of API-first fabrics that synchronize cloud ERP systems with on-premises legacy assets in real time. Demand has shifted from one-off data-migration projects to continuous integration subscriptions that bundle security, observability, and AI-assisted mapping. Adoption is also propelled by regional data-sovereignty mandates that elevate hybrid architectures and by mounting penalties for non-compliance in regulated industries. Competitive pressure from hyperscalers embedding native integration into ERP-as-a-service bundles is compressing margins for stand-alone middleware while expanding the total addressable workload for managed iPaaS solutions.

Key Report Takeaways

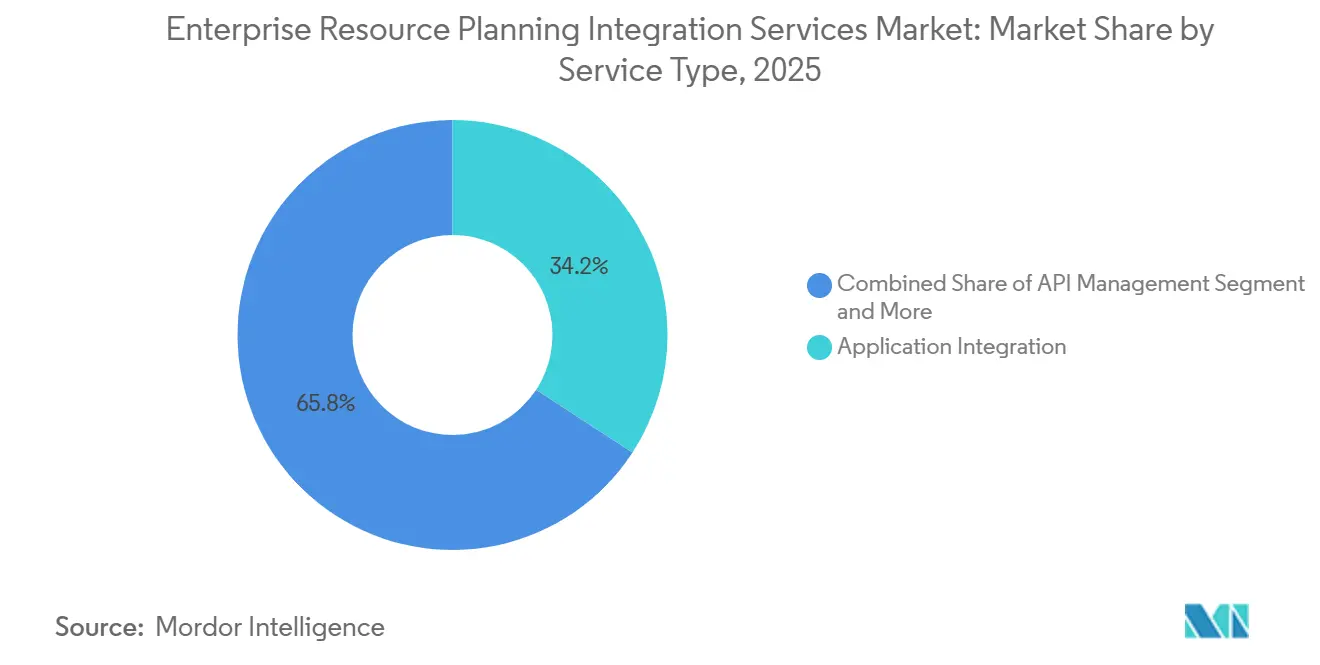

- By service type, application integration led with a 34.20% revenue share in 2025, while API management is forecast to grow at a 15.40% CAGR through 2031.

- By deployment mode, cloud configurations accounted for 57.50% of the ERP integration services market share in 2025, whereas hybrid deployments are advancing at a 14.00% CAGR over 2026-2031.

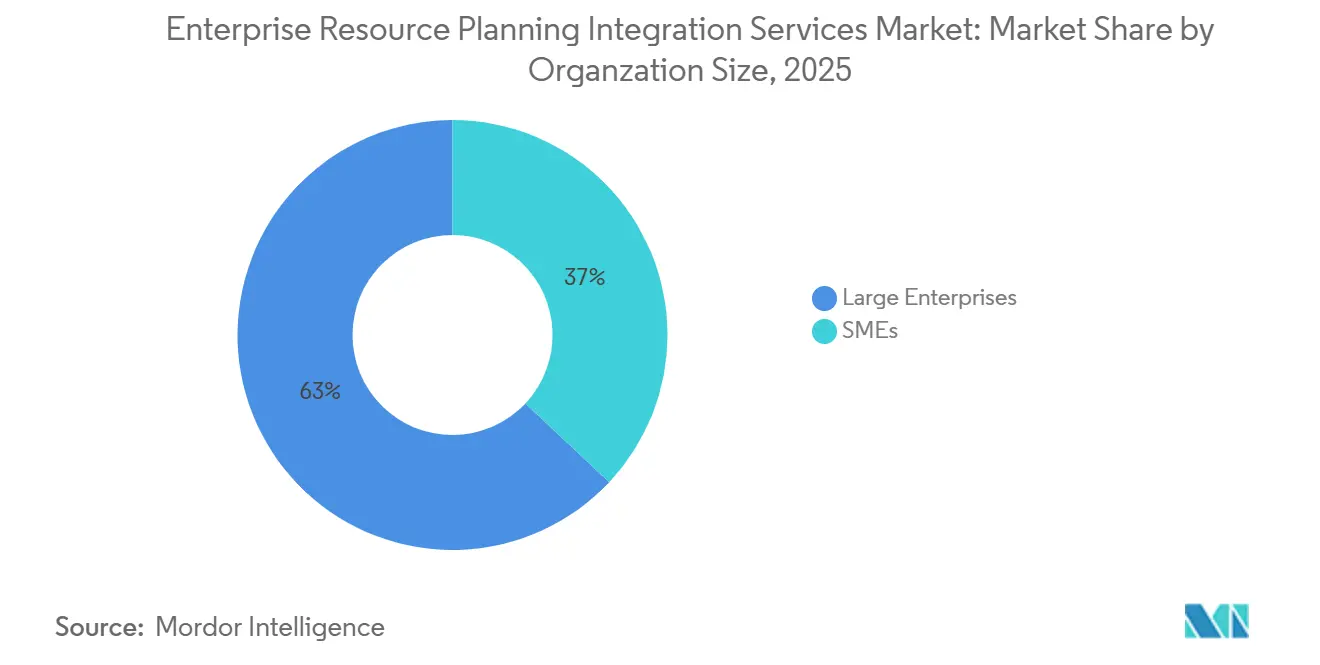

- By enterprise size, large enterprises accounted for 63.00% of 2025 revenue, while small and medium enterprises are expanding at a 13.80% CAGR as consumption-based iPaaS tiers lower entry barriers.

- By industry vertical, IT and telecom held 22.80% of 2025 spending, while healthcare is projected to record the fastest 16.10% CAGR through 2031.

- By geography, North America commanded 42.30% of 2025 revenue, whereas Asia-Pacific is set to expand at a 14.90% CAGR on the back of compressed SAP S/4HANA migration cycles.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Enterprise Resource Planning Integration Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Cloud-Based ERP Systems | +3.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Need for Real-Time Data Synchronization Across Heterogeneous Systems | +2.8% | Global, most acute in BFSI and manufacturing | Short term (≤ 2 years) |

| Increasing API-First Digital Transformation Strategies | +2.1% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Growing Popularity of iPaaS Platforms Among SMEs | +1.5% | Global with SME clusters in Asia-Pacific and South America | Long term (≥ 4 years) |

| Emergence of Low-Code/No-Code Integration Tools | +1.0% | North America, Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Compliance Mandates Driving Data Integration in Regulated Industries | +0.8% | North America (HIPAA), Europe (GDPR), global BFSI sector | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Cloud-Based ERP Systems

Cloud ERP deployments are displacing monolithic middleware with distributed integration fabrics that span multiple hyperscalers and private data centers. SAP Integration Suite connected 2.5 million systems as of February 2026, and 85% of those links involved non-SAP applications, signaling a decisive move toward open API gateways.[1]SAP News, “SAP Integration Suite Roadmap 2026,” SAP.com Microsoft Azure’s 99.95% service-level commitment for SAP private editions further reduces the perceived need for on-premises high-availability clusters. Odoo reported that cloud and hybrid setups formed 83% of new ERP deployments in 2025, mirroring the broader pivot to subscription economics.[2]Microsoft Azure, “Service Level Agreements,” Microsoft.com IBM’s RISE with SAP on Power Virtual Server shaved 15%-25% off migration timelines by bundling storage, networking, and backup, thereby tightening the window for third-party integrators to sell custom connectors.[3]IBM Newsroom, “IBM and SAP Expand Partnership to Help Clients Accelerate Cloud Transformation,” IBM.com As more production workloads move to the public cloud, the ERP integration services market is evolving toward pre-packaged adapters, policy-driven routing, and low-code orchestration to shorten time-to-value.

Need for Real-Time Data Synchronization Across Heterogeneous Systems

Overnight batch ETL cannot support dynamic pricing, real-time inventory allocation, or instant payments. Oracle embedded J. P. Morgan’s cross-border rails into Oracle Cloud ERP in 2025, eliminating 24-hour reconciliation delays for 160 countries.[4]Oracle, “Oracle Cloud ERP Embedded Banking with J. P. Morgan,” Oracle.com SAP-to-Snowflake Change Data Capture streams cut analytical latency from hours to seconds. Manufacturers processing 200 GB of sensor data daily now route only anomaly events to cloud ERP via sub-second brokers. More than 80 countries already operate instant-payment schemes, and ISO 20022 compliance is now table-stakes for integration vendors. These developments keep the ERP integration services market on a steady growth path as enterprises re-architect for streaming data.

Increasing API-First Digital Transformation Strategies

Enterprises are decomposing ERP monoliths into microservices that expose order-to-cash or procure-to-pay functions through REST and GraphQL. SAP Integration Suite ships 250 pre-built connectors that citizen developers can orchestrate in drag-and-drop designers. Microsoft’s Joule integration with Copilot lets users query purchase-order status by voice, demonstrating how AI agents rely on governed APIs rather than database access. API management platforms enforce rate limits and OAuth 2.0, plugging security gaps that turned hybrid-identity bridges into major attack surfaces in 2025. In the United Kingdom, embedded-finance revenue will more than double between 2024 and 2029, and every use case hinges on standardized ERP APIs. This API-first wave is a primary catalyst for the ERP integration services market.

Growing Popularity of iPaaS Platforms Among SMEs

iPaaS revenue exceeded USD 9 billion in 2025, with SMEs providing the largest incremental lift as consumption-based tiers wiped out capital-expenditure hurdles. Jitterbit topped G2’s Spring 2026 implementation index after showing it could compress configuration time from weeks to days through AI-assisted mapping. SnapLogic’s SnapGPT converts natural-language prompts into connector mappings, eliminating the need for specialist programmers. These advances underpin double-digit growth among smaller buyers and extend the addressable ERP integration services market beyond Fortune-class enterprises.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complexity of Legacy ERP Customizations | -2.5% | Global, acute in Europe and North America with aging SAP ECC installs | Medium term (2-4 years) |

| High Total Cost of Ownership for Large Integration Projects | -1.8% | Global, most severe in large enterprises and public sector | Short term (≤ 2 years) |

| Data Security and Governance Concerns in Hybrid Environments | -1.2% | Europe (GDPR), North America (HIPAA, SOC 2), Asia-Pacific emerging | Short term (≤ 2 years) |

| Shortage of Skilled Integration Specialists | -0.9% | Europe, North America, urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complexity of Legacy ERP Customizations

Roughly 21,000 SAP ECC installations, 61% of the installed base, remain unmigrated, with mainstream support ending in December 2027. Custom ABAP code and undocumented bolt-ons devour up to half of migration budgets, and consulting rates are set to rise as the deadline nears. Only 30% of organizations were fully live on SAP S/4HANA Cloud in 2025, indicating that the bulk of integration workloads will compress into a two-year window. As backlogs swell, the ERP integration services industry faces execution risk and potential project delays.

High Total Cost of Ownership for Large Integration Projects

Birmingham City Council's Oracle project experienced a significant cost escalation, rising from an initial budget of GBP 46 million (USD 58 million) to GBP 114 million (USD 144 million). This development highlights the inherent risks associated with budget overruns in large-scale technology implementations. Similarly, Lidl faced a considerable financial setback, writing off EUR 580 million (USD 620 million) after halting its SAP migration. This incident underscores the substantial financial implications that can arise when system integrations encounter critical challenges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: API Management Races Ahead of Legacy Integration

Application integration accounted for 34.20% of 2025 revenue, reflecting the entrenched web of connectors that tie ERP to CRM, supply chain, and HCM suites. Yet API management is projected to log a 15.40% CAGR over 2026-2031, the fastest within the service stack, as event-driven architectures supersede nightly ETL and embedded-finance use cases call for governed external APIs. The ERP integration services market registers accelerating demand for multi-protocol gateways that wrap REST, SOAP, EDIFACT, and GraphQL under a single policy layer, ensuring consistent authentication and rate controls. Vendors now auto-generate OpenAPI contracts, maintain version lineage, and monetize high-value endpoints through subscription billing.

Data-integration services remain core for analytical workloads, streaming CDC feeds into Snowflake and BigQuery in real time. Process-integration consultancies lean on low-code orchestrators and robotic process automation to knit end-to-end workstreams such as order-to-cash without swivel-chair tasks. B2B and EDI integration still rides demand from aerospace and consumer goods, where ANSI X12 and EDIFACT remain contractual bedrock. Cloud integration brokerage outsources connector maintenance and security patching to providers, freeing enterprise IT from upkeep. As containerized microservices proliferate, API management will command a larger share of the ERP integration services market size through 2031.

By Deployment Mode: Hybrid Models Bridge Sovereignty and Scale

Cloud deployments accounted for 57.50% of 2025 revenue, driven by hyperscaler bundles that combine infrastructure, licenses, and native integration. IBM’s RISE with SAP on Power Virtual Server posted 30% infrastructure savings by collapsing middleware layers. Yet hybrid configurations are expanding at a 14.00% CAGR, the highest among deployment options, as European and Asian data-residency mandates block certain records from leaving national borders. GDPR Article 48 forbids unsanctioned cross-border transfers, encouraging multinationals to keep master data on-premises while sending analytics to the cloud.

Hybrid topologies, therefore, require secure message buses, dual-region replication, and tenant-aware encryption. IBM X-Force cataloged 16 million devices infected by infostealer malware in 2025, with MuleSoft Anypoint and Microsoft Entra Connect often serving as breach entry points. Only 62% of surveyed SAP cloud users adhere to recommended security hardening, leaving plaintext keys in configs. Integration platforms must therefore bundle secrets management and audit logging that meet ISO 27001 and SOC 2 Type II requirements. Sovereignty and latency constraints ensure that the ERP integration services market share tied to hybrid topologies will continue to rise.

By Enterprise Size: SMEs Open a New Growth Frontier

In 2025, large enterprises accounted for 63.00% of total revenue, driven by extensive programs to integrate SAP, Oracle, and mainframe systems with cloud-based CRM and HCM suites. These multi-year initiatives reflect large organizations' strategic focus on modernizing their IT infrastructure to enhance operational efficiency and scalability. Meanwhile, small and medium enterprises are poised to experience a robust 13.80% CAGR from 2026 to 2031. This significant growth is primarily attributed to the adoption of consumption-based iPaaS tiers, which enable SMBs to pay only for completed tasks, thereby eliminating the need for substantial upfront capital investments.

Jitterbit’s visual designer, widely recognized for its ease of use, highlights the growing preference for no-code solutions within the SME segment. While larger corporations continue to allocate resources toward complex tax engines and multi-ledger requirements, the market is witnessing a notable shift. Incremental growth is increasingly skewing toward SMEs, which is contributing to the expansion of the overall ERP integration services market.

By Industry Vertical: Healthcare Sets the Pace Amid Compliance Pressure

IT and telecom took 22.80% of 2025 spend, but healthcare is projected to expand at a 16.10% CAGR through 2031. In January 2026, the U.S. Department of Health and Human Services raised HIPAA penalties to USD 2.19 million per violation and mandated TLS 1.3 and quarterly vulnerability scans, pushing providers toward secure, real-time integration fabrics. IBM pegs average healthcare breach costs at USD 9.77 million, almost double the cross-industry mean, bolstering ROI arguments for hardened integrations.

BFSI institutions embed payment rails directly into ERP; Oracle’s J. P. Morgan deal automates 160-country wires. Retail and e-commerce double down on omnichannel synchronization, riding the United Kingdom’s embedded-finance boom that will push revenue from USD 8.2 billion in 2024 to USD 20 billion by 2029.[5]UK Finance, “Embedded Finance UK 2025,” Ukfinance.org.uk These vertical dynamics ensure the ERP integration services market remains multi-sector rather than single-industry.

Geography Analysis

North America accounted for 42.30% of 2025 revenue, driven by mature ERP footprints in the United States and Canada that require ongoing integration as new SaaS modules roll in. AI-assisted workloads, such as Microsoft’s Jupyter Notebook Copilot for voice queries, accelerate the adoption of governed APIs, shortening user-training cycles. Tougher HIPAA penalties keep healthcare IT budgets flowing toward secure integration fabrics, cushioning any post-migration slowdown. Hence, North America remains a robust contributor to the ERP integration services market size.

Asia-Pacific is projected to post a 14.90% CAGR through 2031, the fastest regional rate. Deferred SAP S/4HANA migrations in China, India, Japan, and South Korea will compress into 2027-2029 as SAP ECC leaves mainstream support. IBM and SAP’s Power Virtual Server migrations reduce timelines by up to 25%. China’s Data Security Law forces local replication of sensitive records, promoting hybrid integration proxies. Consequently, the ERP integration services market share tied to Asia-Pacific will surge as deadlines loom.

Europe balances entrenched customizations with GDPR fidelity. Article 48’s cross-border restrictions promote sovereign-cloud offerings such as SAP Sovereign Cloud. South America and the Middle East and Africa remain smaller but promising. Brazil and Saudi Arabia lead government digitization, and Mexico’s USMCA membership accelerates cross-border supply-chain integrations that need real-time ERP connectors. Together, geographic diversification cushions the global ERP integration services market against localized shocks.

Competitive Landscape

The top five players, Accenture, IBM, SAP, Oracle, and Microsoft, command a significant combined share, leaving a long tail of regional integrators and pure-play iPaaS vendors to service niche needs. IBM’s vertical integration with RISE on Power Virtual Server delivered 30% infrastructure savings, underscoring how hyperscalers bundle integration to squeeze independent middleware margins. Pure-play iPaaS firms such as MuleSoft, Boomi, SnapLogic, and Workato are embedding low-code workflow tools and AI-assisted mapping to fend off encroachment by Microsoft Power Automate and SAP Build Process Automation. Jitterbit’s Spring 2026 G2 ranking shows that product-led growth rooted in ease of use resonates in the SME tier.

Industry-specific accelerators are emerging as a key battleground. Oracle and Microsoft released a blueprint that pipes Azure IoT telemetry into Oracle Fusion Cloud SCM for sub-second work-order automation, differentiating through supply-chain depth rather than middleware plumbing. SnapLogic’s SnapGPT highlights how generative AI can lower technical barriers, while Workato’s community recipes encourage peer-to-peer reuse. Skills shortages, particularly for SAP Basis and ABAP in Europe, are inflating delivery timelines; deep specialists now command up to EUR 180,000 (USD 192,000) annually and take more than 90 days to hire. Vendors respond with offshore centers and certification boot camps to de-risk capacity crunches.

Security certifications have become table stakes. ISO 27001 and SOC 2 Type II attestations are now prerequisites for enterprise shortlists, and vendors invest in continuous penetration testing and zero-trust roadmaps. Meanwhile, pricing shifts toward outcome-based contracts that peg subscription tiers to invoice volumes or API calls rather than static seats, creating room for innovation in commercial models. As vertical differentiation, AI-assisted tooling, and compliance assurances shape buying criteria, the ERP integration services market maintains moderate fragmentation with ample headroom for challengers.

Enterprise Resource Planning Integration Services Industry Leaders

Accenture plc

IBM Corporation

SAP SE

Oracle Corporation

Tata Consultancy Services Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: SAP rolled out a services portfolio that bundles integration, security, and AI into subscription tiers aligned to business outcomes, moving away from milestone-based contracts.

- March 2026: European recruitment data showed time-to-hire for SAP S/4HANA specialists surpassing 90 days, with salaries hitting EUR 180,000 (USD 192,000) for niche roles.

- February 2026: SAP’s Integration Suite roadmap confirmed 250 pre-built connectors and event-driven orchestration for 2.5 million connected systems.

- January 2026: The U.S. Department of Health and Human Services raised maximum HIPAA penalties to USD 2.19 million per violation per year and mandated TLS 1.3 and quarterly scans.

Global Enterprise Resource Planning Integration Services Market Report Scope

The ERP Integration Services market refers to the ecosystem of specialized services that enable seamless connectivity, interoperability, and synchronization between Enterprise Resource Planning (ERP) systems and other enterprise applications, data sources, and external partner systems.

The ERP Integration Services Market Report is Segmented by Service Type (Application Integration, Data Integration, Process Integration, API Management, B2B/EDI Integration, Cloud Integration Brokerage, Other Services), Deployment Mode (On-Premises, Cloud, Hybrid), Enterprise Size (SMEs, Large Enterprises), Industry Vertical (Manufacturing, BFSI, Retail and Ecommerce, Healthcare, IT and Telecom, Government and Public Sector, Energy and Utilities, Other Industry Verticals), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Application Integration |

| Data Integration |

| Process Integration |

| API Management |

| B2B/EDI Integration |

| Cloud Integration Brokerage |

| Other Services |

| On-Premises |

| Cloud |

| Hybrid |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Manufacturing |

| BFSI |

| Retail and Ecommerce |

| Healthcare |

| IT and Telecom |

| Government and Public Sector |

| Energy and Utilities |

| Other Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Service Type | Application Integration | |

| Data Integration | ||

| Process Integration | ||

| API Management | ||

| B2B/EDI Integration | ||

| Cloud Integration Brokerage | ||

| Other Services | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| Hybrid | ||

| By Enterprise Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Industry Vertical | Manufacturing | |

| BFSI | ||

| Retail and Ecommerce | ||

| Healthcare | ||

| IT and Telecom | ||

| Government and Public Sector | ||

| Energy and Utilities | ||

| Other Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the ERP integration services market expected to grow from 2026 to 2031?

It is projected to expand at a 10.92% CAGR, lifting revenue from USD 14.45 billion in 2026 to USD 24.25 billion by 2031.

Which service type will add the most incremental revenue by 2031?

API management, forecast to grow at a 15.40% CAGR as enterprises embrace event-driven and embedded-finance use cases.

Why are hybrid deployments gaining momentum in Europe and Asia-Pacific?

Data-sovereignty and residency laws restrict certain records from leaving national borders, so firms split workloads between on-premises and public cloud while using integration platforms to keep the environments in sync.

What is driving healthcare spending on ERP integration?

Tougher HIPAA penalties, FHIR-based interoperability mandates, and the industrys high average breach costs are pushing providers toward secure, real-time integration fabrics.

How are generative AI tools changing integration projects?

Platforms such as SnapLogics SnapGPT and Jitterbits Maia convert natural-language prompts into data mappings, cutting configuration time from weeks to days and lowering the skills barrier for SMEs.

What competitive moves are hyperscalers making in this space?

IBM, Microsoft, and Oracle are embedding native integration into ERP-as-a-service bundles, offering vertically integrated stacks that reduce infrastructure costs and compress margins for stand-alone middleware vendors.

Page last updated on: