Pharmaceutical Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

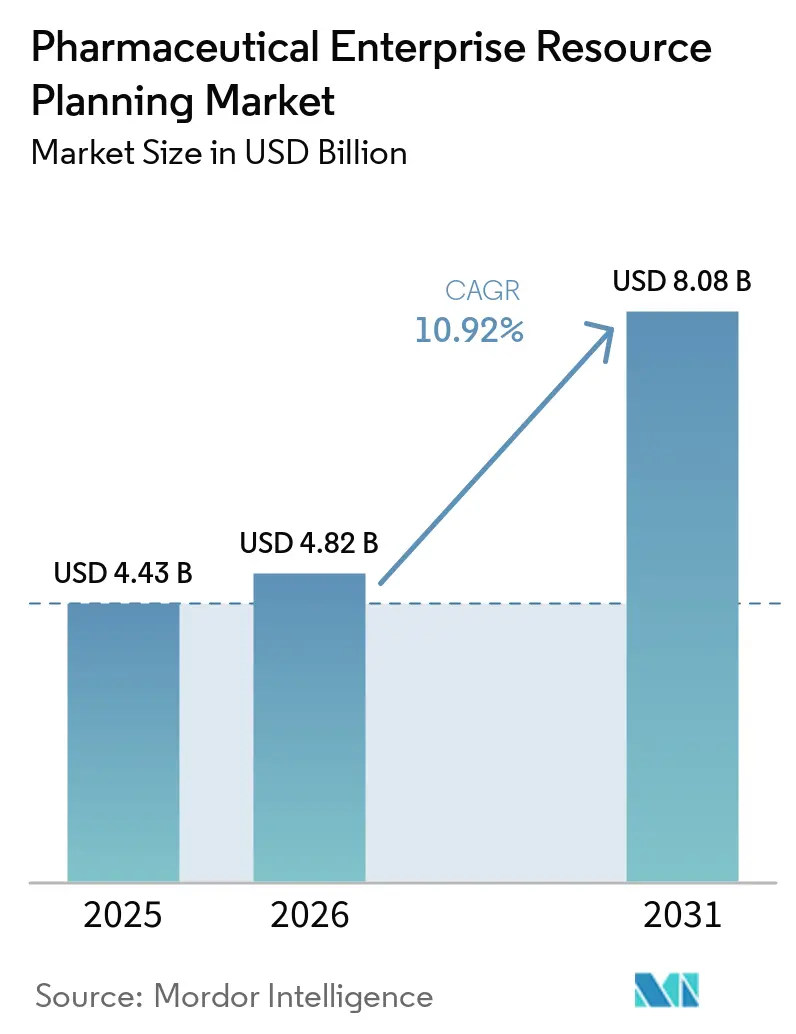

| Market Size (2026) | USD 4.82 Billion |

| Market Size (2031) | USD 8.08 Billion |

| Growth Rate (2026 - 2031) | 10.92% CAGR |

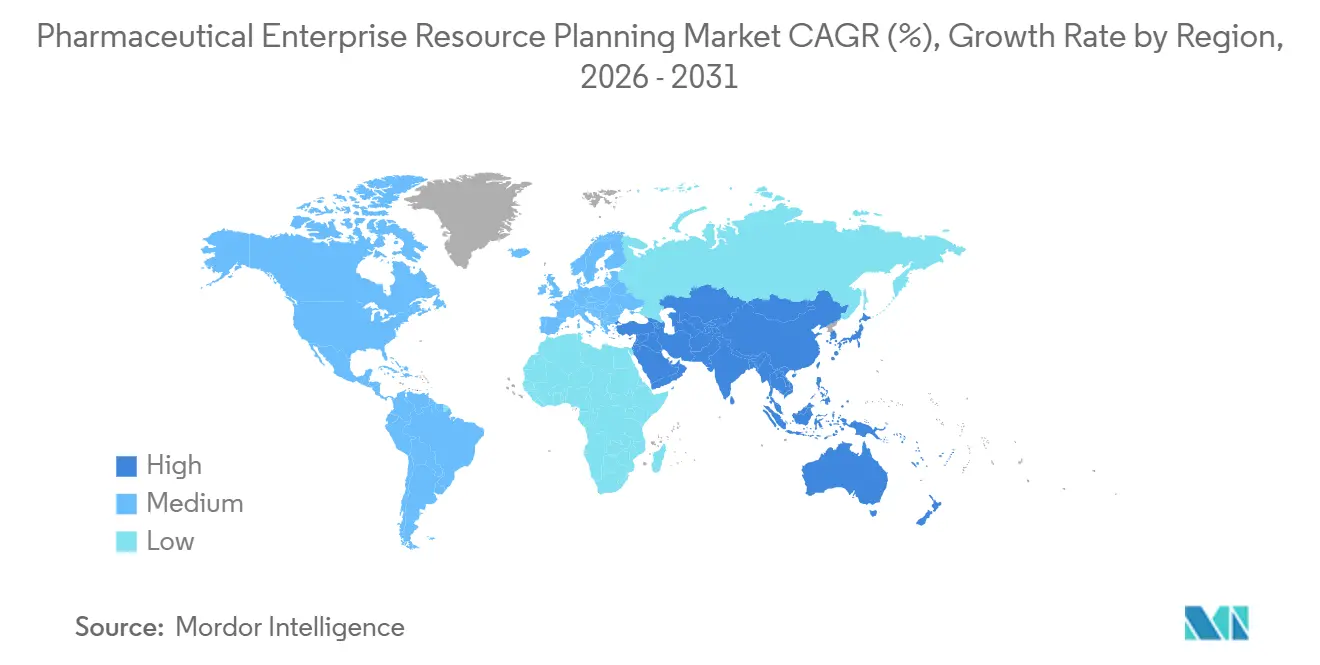

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

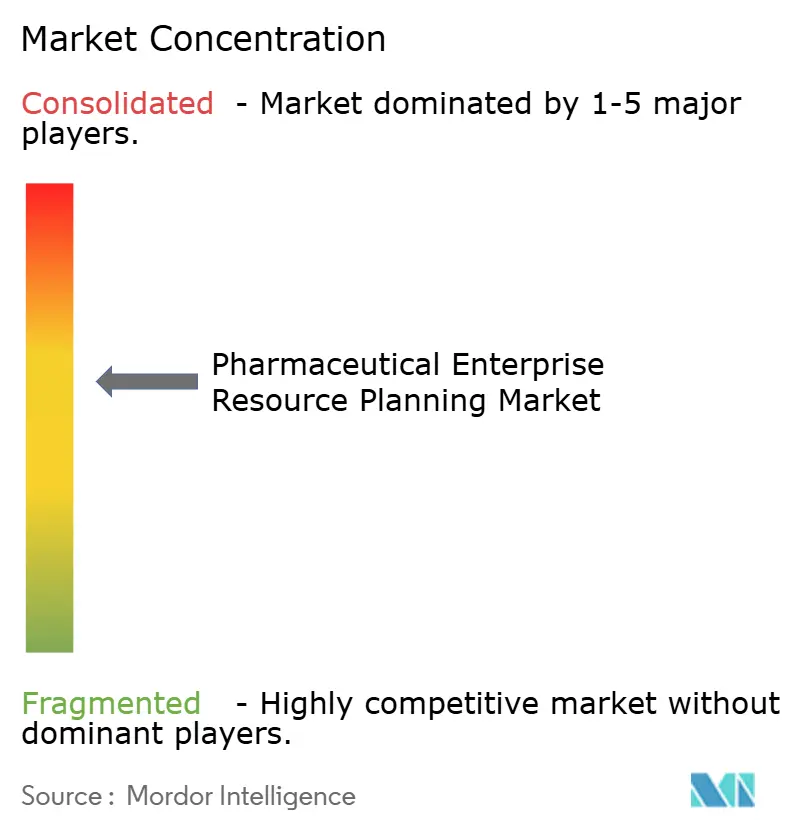

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Enterprise Resource Planning Market Analysis by Mordor Intelligence

The Pharmaceutical ERP market size is projected to expand from USD 4.43 billion in 2025 and USD 4.82 billion in 2026 to USD 8.08 billion by 2031, registering a CAGR of 10.92% between 2026 and 2031. Robust growth reflects the convergence of tightening serialization mandates, breakthroughs in cloud validation, and rapid expansion of contract manufacturing, all of which demand real-time batch traceability. Generative AI copilots embedded in enterprise suites are reducing deviation investigations from months to weeks, while modular cloud deployments enable manufacturers to comply with United States and European regulations without rebuilding legacy systems. Contract manufacturing organizations are scaling validated multi-tenant architectures that isolate sponsor data yet share common quality modules, accelerating biologics outsourcing. Vendors that pre-validate core workflows, automate audit-trail reviews, and offer shared documentation lower computer system validation spend by about a third, making cloud migrations viable for small and medium enterprises.

Key Report Takeaways

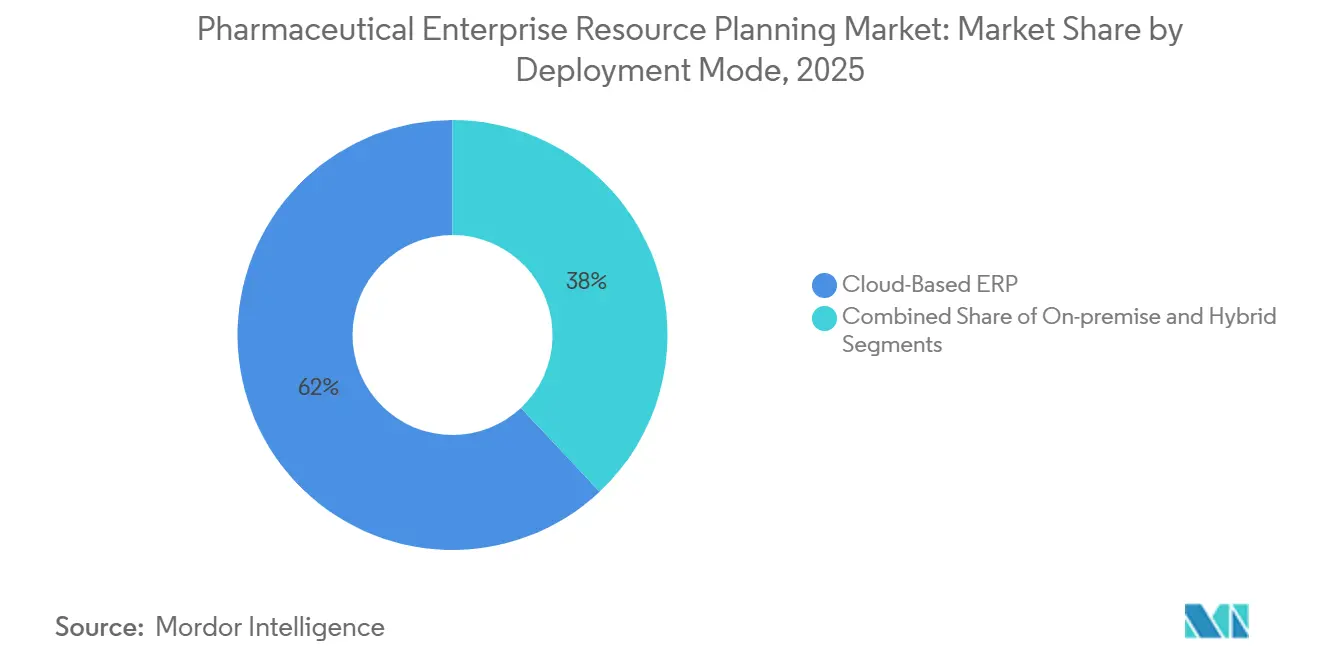

- By deployment mode, cloud-based ERP led with 62% revenue share in 2025; hybrid architectures are forecast to grow at an 11.80% CAGR to 2031.

- By module, quality and compliance accounted for 28.40% of the Pharmaceutical ERP market share in 2025, while research and development is projected to expand at a 12.60% CAGR through 2031.

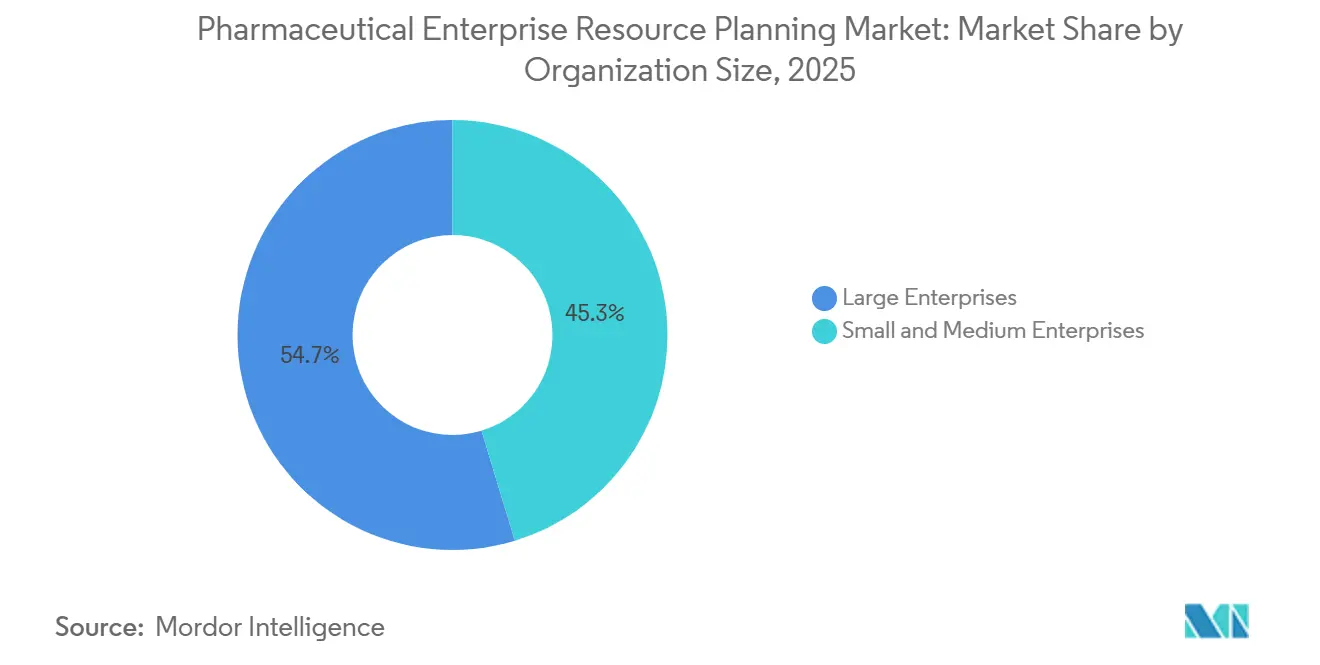

- By organization size, large enterprises held 54.70% of 2025 spending; small and medium enterprises are expected to grow at a 9.70% CAGR through 2031.

- By end user, contract manufacturing organizations posted the fastest growth outlook at 13.10% for 2026-2031, ahead of pharmaceutical manufacturers, distributors, biotechnology companies, and contract research organizations.

- By geography, North America captured 34.90% of 2025 revenue, while Asia-Pacific is forecast to advance at 10.20% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pharmaceutical Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for Cloud-Based Validated ERP Platforms | +2.8% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Tightening Global Serialization Deadlines | +2.4% | North America and Europe, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Rapid Expansion of Contract Manufacturing Organizations | +2.1% | Global, concentrated in Asia-Pacific and Europe | Medium term (2-4 years) |

| AI-Enabled Predictive Quality and Batch-Release Analytics | +1.6% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Government Incentives for Digital Pharma Plants | +1.3% | Asia-Pacific and North America | Medium term (2-4 years) |

| Growing Need for End-to-End ESG and Carbon Accounting | +0.9% | Europe, expanding to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand for Cloud-Based Validated ERP Platforms

Pharmaceutical manufacturers are moving workloads to the cloud to reduce capital expenditure, unlock real-time batch visibility, and cut validation timelines. SAP, Oracle, and Microsoft introduced pre-validated life sciences suites that embed GxP documentation, enabling companies to comply with 21 CFR Part 11 without maintaining on-premises environments. [1]SAP SE, “Chanelle Pharma Partnership Release 2026,” sap.com Contract manufacturing organizations prefer multi-tenant cloud architectures that isolate sponsor data yet share common quality modules, enabling faster onboarding and harmonized electronic batch records. However, data-residency rules in China and Russia force hybrid deployments that blend public-cloud financials with on-premise manufacturing execution systems.

Tightening Global Serialization Deadlines

The United States Drug Supply Chain Security Act completed its phased rollout in 2025, requiring manufacturers, wholesalers, and dispensers to integrate unit-level track-and-trace into their ERP systems.[2]SAP SE, “S/4HANA Cloud for Life Sciences,” sap.com The European Union Falsified Medicines Directive granted Italy and Greece extensions until 2027, creating a two-speed environment that favors modular, country-specific templates.[3]U.S. Food and Drug Administration, “Drug Supply Chain Security Act,” fda.gov Serialization drives demand for blockchain-enabled ERP integrations that provide immutable audit trails and real-time verification against national repositories REUTERS.COM.

Rapid Expansion of Contract Manufacturing Organizations

Lonza, Catalent, and Samsung Biologics invested billions to scale biologics capacity between 2024 and 2025, each relying on validated, cloud-ready ERP platforms to provide live dashboards for sponsors.[4]Samsung Biologics, “Contract Manufacturing Milestones 2025,” samsungbiologics.com Asia-Pacific gains momentum through India’s USD 2 billion production-linked incentive and China’s centralized procurement reforms, both of which push domestic players to adopt international GxP standards.

AI-Enabled Predictive Quality and Batch-Release Analytics

Pfizer cut batch rejection rates by 12% using machine-learning models that predict deviations 48 hours ahead, while Novartis trimmed investigation timelines to seven days through natural-language processing.[5]Pfizer Inc., “Manufacturing Innovation Overview 2025,” pfizer.com Microsoft launched AI copilots in 2026 that let quality teams query batch data conversationally. Regulatory agencies have yet to publish definitive AI validation rules, so manufacturers blend algorithmic insights with human oversight.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CSV Costs for SMEs | -1.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Shortage of Pharma-Savvy ERP Implementation Talent | -1.5% | Global, notably North America and Europe | Medium term (2-4 years) |

| Cyber-Security and Data-Residency Concerns | -1.1% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Legacy MES and LIMS Integration Complexities | -0.9% | Global, facilities with pre-2015 equipment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CSV Costs for SMEs

Computer system validation can consume up to 30% of an ERP project budget for small and medium enterprises, extending go-live dates by up to a year. External consultants bill USD 150-250 per hour, straining limited IT budgets. Vendors offer shared validation documentation, yet regulators insist that manufacturers retain ultimate responsibility for compliance. The burden is heavier for contract manufacturers that must satisfy divergent sponsor requirements.

Shortage of Pharma-Savvy ERP Implementation Talent

Validation specialists with dual expertise in GxP and cloud infrastructure command salary premiums exceeding 30%, resulting in project delays averaging 4 months. Certification programs from major vendors will take years to fill the gap. Emerging markets feel the pressure most, often importing expatriate consultants at six-figure annual costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Architectures Reshape Validation Economics

Cloud-based solutions accounted for 62% of revenue in 2025, and this share of the Pharmaceutical ERP market is set to grow at a 11.80% CAGR through 2031. Hybrid models satisfy jurisdictions that restrict patient data movement while unlocking cloud scalability for non-GxP functions. The Pharmaceutical ERP market size for cloud deployments is projected to command the majority of new spend by 2031. Early adopters report significantly lower validation costs after switching from on-premises suites. Contract manufacturing organizations dominate uptake because multi-tenant clouds enable sponsor segregation and rapid onboarding.

On-premises deployments persist in China and Russia, where data localization laws remain strict. Facilities with legacy equipment lack OPC-UA connectivity, so migrating to the public cloud can trigger costly re-validation of entire production lines. Hybrid architectures let manufacturers migrate financials and human resources to cloud services while retaining manufacturing execution on-site. Vendors that automate audit-trail reconciliation shorten CSV cycles from 18 months to six months, accelerating Pharmaceutical ERP market adoption among compliance-focused firms.

By Module: Quality and Compliance Dominate, R and D Accelerates

Quality and compliance accounted for 28.40% of 2025 revenue, reflecting the regulatory focus. This slice of the Pharmaceutical ERP market share underpins every major deployment, especially where DSCSA and EU FMD demand serialization. Manufacturing management modules orchestrate scheduling, procurement, and maintenance, offering process visibility across multi-site networks.

Research and development modules are expected to grow at a 12.60% CAGR as innovators integrate AI into formulation design and clinical-trial workflows. The Pharmaceutical ERP market for Research and Development tools, while still smaller than the quality management market, is growing fastest because AI shortens experimentation cycles. Supply chain modules benefit from blockchain pilots that create immutable product provenance, and human resources tools map employee training records to GxP tasks, ensuring only qualified staff perform critical operations.

By Organization Size: Large Enterprises Lead, SMEs Accelerate

Large enterprises held 54.70% of spending in 2025 because they maintain in-house validation talent and can fund global rollouts that stitch together manufacturing, quality, and finance. Their hybrid-cloud pilots preserve existing validation while capturing operating-expense flexibility. Small and medium enterprises are set to grow at a 9.70% CAGR through 2031, driven by consumption-based licenses and pre-configured templates that cut implementation time to 6 months.

Validation costs remain a choke point. SMEs allocate a higher share of budgets to CSV, delaying adoption unless vendors provide shared evidence packs. Government incentives, such as India’s production-linked scheme, subsidize digital upgrades, enabling smaller firms to join global supply networks. Vendors that address budget constraints while satisfying FDA 21 CFR Part 11 and EU Annex 11 will capture latent Pharmaceutical ERP market demand among resource-constrained manufacturers.

By End User: CMOs Outpace Traditional Manufacturers

Pharmaceutical manufacturers accounted for 41.30% of revenue in 2025, yet contract manufacturing organizations will grow the fastest at 13.10% over the forecast period. CMOs need multi-tenant, sponsor-separated data environments that traditional single-enterprise suites cannot provide. Consequently, the Pharmaceutical ERP market size linked to CMOs will expand more than any other sub-segment.

Biotechnology firms use predictive analytics to streamline batch release, while distributors invest in serialization modules to meet verification mandates. Contract research organizations integrate clinical-trial management with finance and HR so sponsors can monitor timelines and enrollment in real time. Data-residency and cybersecurity clauses push many providers toward hybrid clouds that protect patient data while offering cloud agility.

Geography Analysis

North America led with 34.90% of 2025 revenue, driven by stringent DSCSA rules and an innovation-oriented manufacturing base. The Pharmaceutical ERP market size in the United States benefits from early cloud validation pilots and broad AI experimentation. Canada leverages proximity to the United States to position itself as a biologics contract manufacturing hub, making cross-border batch visibility a must-have.

Europe maintains second position. The EU Falsified Medicines Directive mandates serialization, and the Corporate Sustainability Reporting Directive compels Scope 3 carbon accounting. These rules favor integrated ERP suites over point solutions. Data-residency considerations under GDPR encourage hybrid architectures that host patient data locally and move financial data to global clouds.

Asia-Pacific is the fastest-growing region, expected to advance at 10.20% through 2031. India’s USD 2 billion incentive propels local firms into export markets that demand FDA and EMA compliance. China’s USD 1.5 billion infrastructure push and centralized procurement reforms motivate domestic CMOs to embrace international GxP standards. Japan pilots AI batch-release analytics to offset labor shortages.

South America is growing more slowly due to macroeconomic volatility, though Brazil and Argentina are investing selectively in ERP modernization. The Middle East and Africa remain nascent but promising, as Saudi Arabia and the United Arab Emirates develop local pharma manufacturing to reduce reliance on imports.

Competitive Landscape

The top five suppliers account for a significant share, indicating moderate concentration. SAP, Oracle, and Microsoft dominate large enterprise deployments with end-to-end suites, while BatchMaster, Dexciss, and Aptean win mid-market deals using pre-configured templates that meet FDA and EU requirements at lower cost.

Competitive edges revolve around embedded GxP documentation, automated audit-trail reviews, and pre-validated cloud modules that reduce CSV file sizes by about one-third. SAP’s March 2026 alliance with Chanelle Pharma showcased cloud validation that slashed project timelines. Oracle automated the pre-population of deviation reports using historical data in 2025, simplifying inspections. Microsoft’s AI copilots, launched in January 2026, provide natural-language access to batch records.

Vendors without SOC 2 Type II credentials are losing bids as ransomware attacks raise cybersecurity stakes. Fewer than 20% of live deployments can reconcile Scope 3 emissions, leaving white-space for carbon-accounting innovators.

Pharmaceutical Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Infor, Inc.

QAD Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Microsoft released AI batch-release copilots that summarize quality data in Dynamics 365, reducing manual review time.

- January 2026: SAP completed S/4HANA Cloud for Life Sciences deployment at Pharmedic, enabling WHO GMP certification in Vietnam.

- November 2025: DSCSA dispenser deadline took effect, triggering a wave of cloud ERP upgrades among pharmacies.

- August 2025: DSCSA wholesaler deadline prompted mid-tier distributors to deploy serialization modules.

Global Pharmaceutical Enterprise Resource Planning Market Report Scope

The Pharmaceutical ERP market refers to the ecosystem of specialized enterprise software solutions and associated services designed to manage, integrate, and optimize core business processes within pharmaceutical and biotechnology organizations, while ensuring strict regulatory compliance and quality standards.

The Pharmaceutical ERP Market Report is Segmented by Deployment Mode (Cloud-Based ERP, On-Premise ERP, Hybrid ERP), Module (Manufacturing Management, Quality and Compliance Management, Supply Chain Management, Financial Management, Sales and Marketing, Human Resources Management), Organization Size (Large Enterprises, Small and Medium Enterprises), End User (Pharmaceutical Manufacturers, Contract Manufacturing Organizations, Pharmaceutical Distributors, Biotechnology Companies, Contract Research Organizations), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based ERP |

| On-Premise ERP |

| Hybrid ERP |

| Manufacturing Management |

| Quality and Compliance Management |

| Supply Chain Management |

| Financial Management |

| Sales and Marketing |

| Human Resources Management |

| Other Modules |

| Large Enterprises |

| Small and Medium Enterprises |

| Pharmaceutical Manufacturers |

| Contract Manufacturing Organizations |

| Pharmaceutical Distributors |

| Biotechnology Companies |

| Contract Research Organizations |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Deployment Mode | Cloud-Based ERP | |

| On-Premise ERP | ||

| Hybrid ERP | ||

| By Module | Manufacturing Management | |

| Quality and Compliance Management | ||

| Supply Chain Management | ||

| Financial Management | ||

| Sales and Marketing | ||

| Human Resources Management | ||

| Other Modules | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End User | Pharmaceutical Manufacturers | |

| Contract Manufacturing Organizations | ||

| Pharmaceutical Distributors | ||

| Biotechnology Companies | ||

| Contract Research Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the Pharmaceutical ERP market by 2031?

The market is projected to reach USD 8.08 billion by 2031.

Which deployment mode is expanding fastest?

Cloud-based ERP platforms are forecast to grow at an 11.80% CAGR during 2026-2031.

Which region shows the highest growth potential?

Asia-Pacific is expected to advance at a 10.20% CAGR through 2031, driven by incentives in India and reforms in China.

Why are contract manufacturing organizations investing heavily in ERP?

CMOs need multi-tenant architectures that segregate sponsor data while sharing validated quality modules, supporting rapid biologics outsourcing.

What is the main challenge for small and medium enterprises adopting ERP?

High computer system validation costs consume up to 30% of project budgets and extend timelines by up to a year.

How are vendors using AI inside ERP suites?

Generative and predictive models automate deviation investigations, predict batch failures, and provide natural-language insights to quality teams.

Page last updated on: