Oil And Gas Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

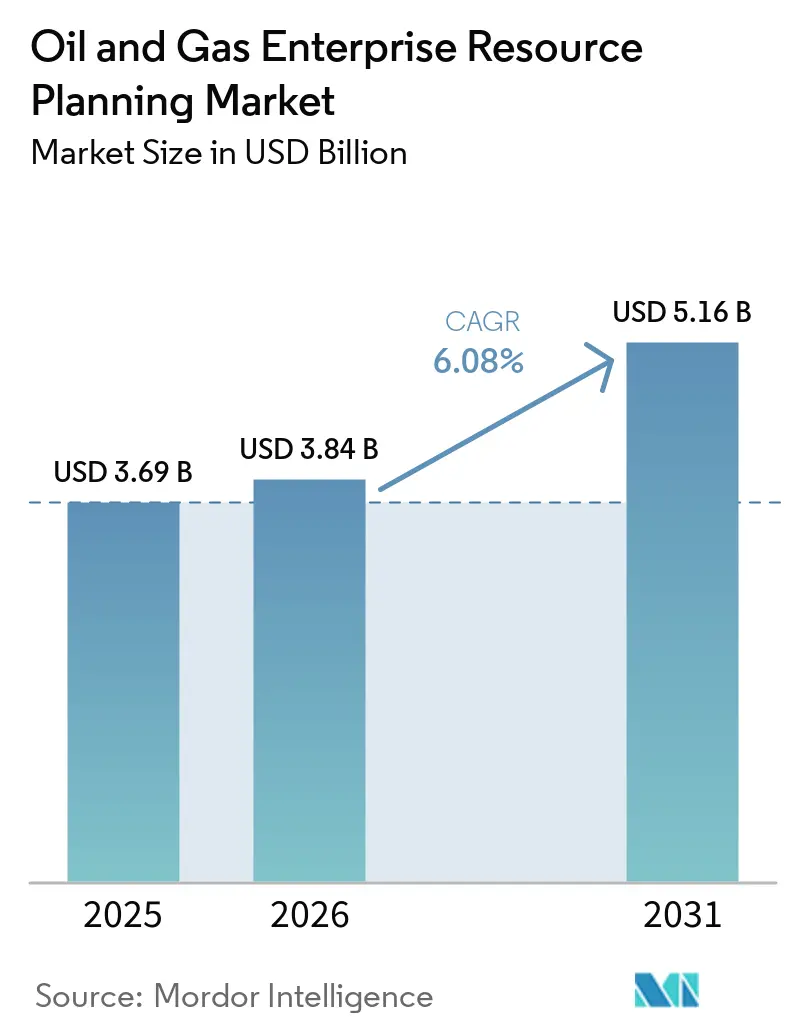

| Market Size (2026) | USD 3.84 Billion |

| Market Size (2031) | USD 5.16 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

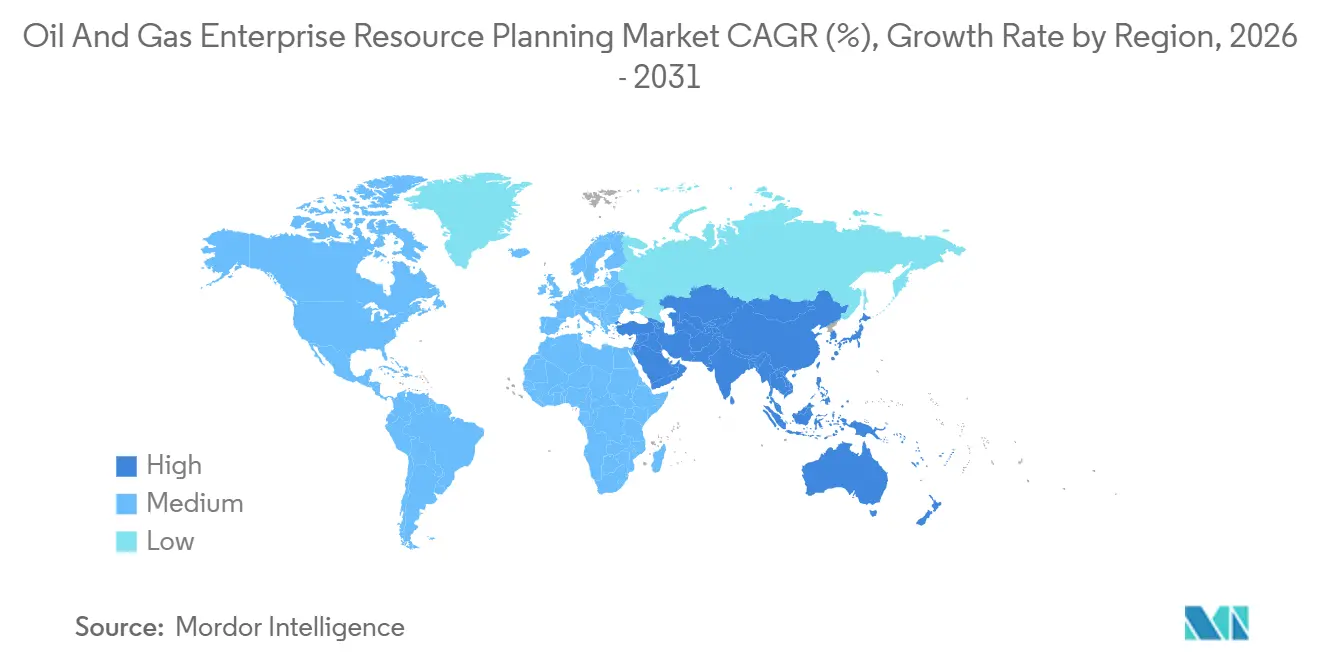

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

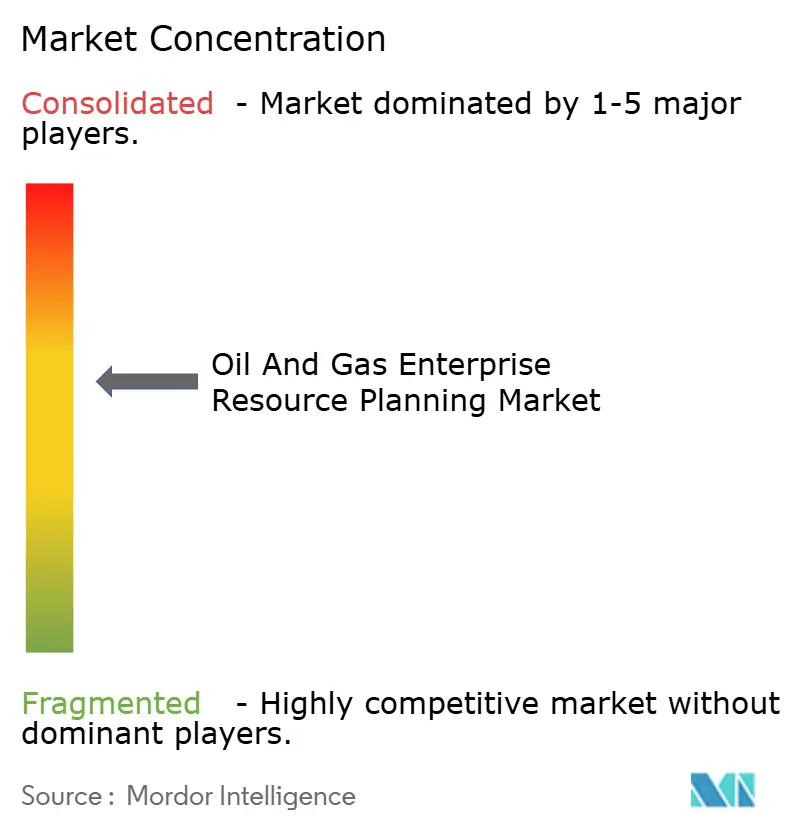

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oil And Gas Enterprise Resource Planning Market Analysis by Mordor Intelligence

The oil and gas ERP market size is projected to be USD 3.69 billion in 2025, USD 3.84 billion in 2026, and reach USD 5.16 billion by 2031, growing at a CAGR of 6.08% from 2026 to 2031. Capital-intensive assets, multi-year validation cycles, and strict cybersecurity mandates temper the adoption curve, yet sustained investment in predictive maintenance and ESG reporting keeps spending on an upward path. Cloud deployment remains the default choice for new rollouts, while hybrid models are gaining traction as national oil companies seek regional data residency and rapid scalability. Vendors differentiate with AI-driven asset modules that forecast failures weeks in advance, and with joint-venture accounting engines that automate complex revenue splits. Operators also weigh the total cost of ownership, talent availability, and integration with brownfield SCADA systems when selecting an ERP partner.

Key Report Takeaways

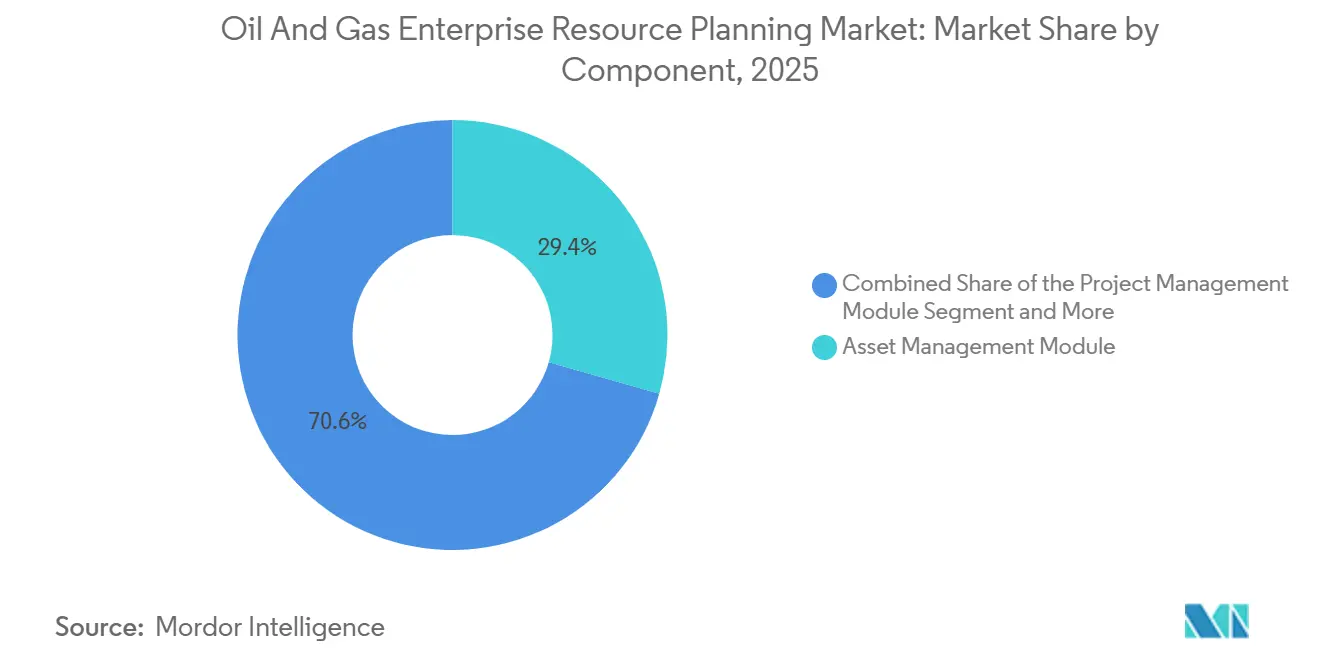

- By component, the Asset Management Module accounted for 29.40% of revenue in 2025. The Project Management Module is projected to post the fastest CAGR at 11.80% through 2031.

- By deployment mode, cloud held 62.10% of the oil and gas ERP market share in 2025, while hybrid configurations are advancing at a 13.10% CAGR.

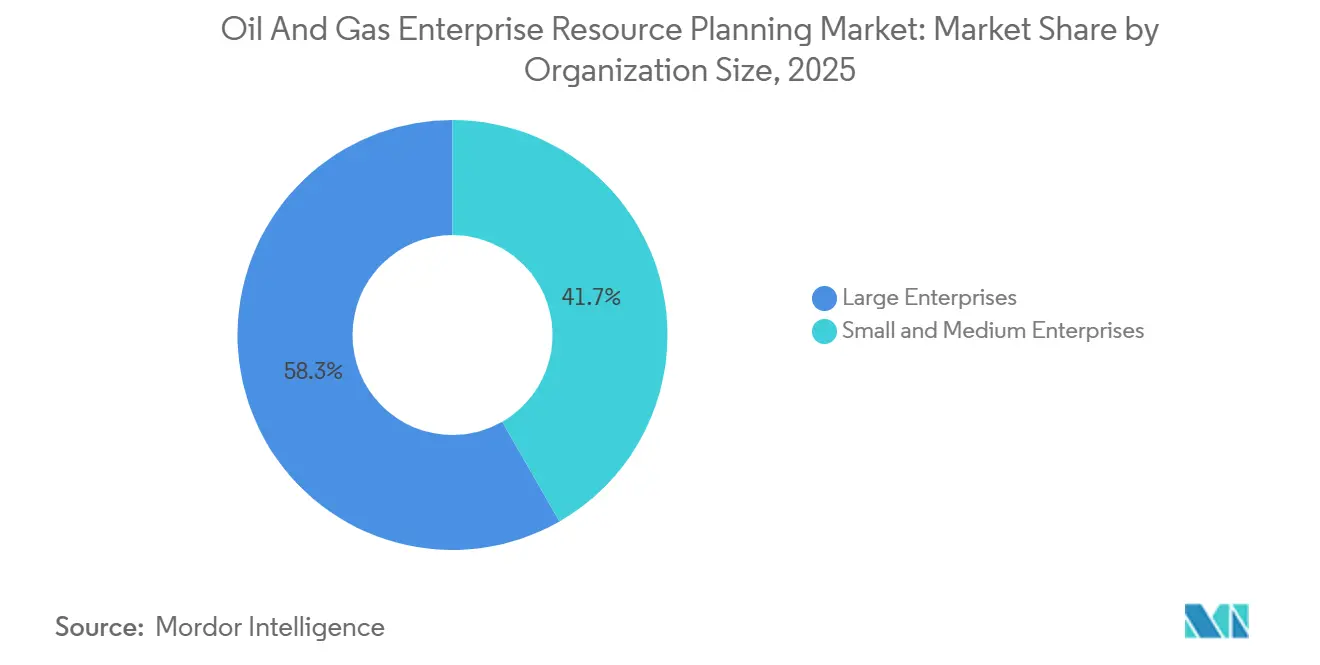

- By enterprise size, large enterprises accounted for 58.30% of 2025 spending, yet small and medium enterprises are growing at 12.20% CAGR through 2031.

- By application, upstream operations commanded 43.60% of revenue in 2025, and oilfield services are forecast to expand at a 12.90% CAGR through 2031.

- By geography, North America led with a 44.90% share in 2025, while Asia-Pacific is the fastest-growing region at a 11.30% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Oil And Gas Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Cloud-Based ERP Solutions | +0.9% | Global, strong in North America and Middle East | Medium term (2-4 years) |

| Rise of AI-Driven Predictive Maintenance | +0.8% | Offshore and remote assets worldwide | Short term (≤ 2 years) |

| Integration of Asset and Financial Management | +0.7% | Early uptake in North America and Europe | Medium term (2-4 years) |

| Increasing Regulatory and Compliance Demands | +0.5% | North America and Europe, rising elsewhere | Long term (≥ 4 years) |

| Demand for Integrated ESG and Carbon Reports | +0.5% | North America and Europe lead | Long term (≥ 4 years) |

| Joint Venture Accounting Automation | +0.4% | Global, concentrated in upstream partnerships | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption Of Cloud-Based ERP Solutions

Cloud captured 62.10% of the oil and gas ERP market in 2025 after hyperscalers launched region-specific data centers and industry-certified security frameworks. S-OIL consolidated 14 legacy modules into a single cloud instance and cut month-end close from 12 days to 5, while Sharjah National Oil Corporation moved finance and procurement workloads to public cloud but retained production data on-premise. Hybrid growth at a 13.10% CAGR shows that operators prefer to keep real-time SCADA streams local and shift corporate functions to elastic infrastructure. This pattern supports consumption-based pricing, which trims upfront capital outlay by up to 60% for smaller firms. Data residency guarantees in Saudi Arabia and the United Arab Emirates further accelerate migrations.

Rise Of AI-Driven Predictive Maintenance

Each unplanned shutdown costs an upstream operator nearly USD 38 million, so predictive maintenance drives the highest near-term ROI. Analytics suites embedded in ERP asset modules process vibration and pressure data to predict failures 30-45 days ahead, enabling repairs during planned turnarounds. Early adopters in Abu Dhabi report a 15% drop in inventory carrying costs after synchronizing procurement with real-time production schedules.[1]Abu Dhabi National Oil Company, “AI Tools Drive Inventory Gains,” adnoc.ae Edge computing pushes algorithms to the wellhead, delivering millisecond latency without network upgrades. Vendors now bundle generative tools that read maintenance logs, auto-create work orders, and dispatch technicians, shrinking mean time to repair by more than one-fifth.

Integration Of Asset And Financial Management

Asset Management accounted for the majority of revenue in 2025 because operators want a single source of truth for equipment life cycles and capital budgets. Unifying ledgers with maintenance histories eliminates manual reconciliations that once consumed hundreds of labor hours each month. Compliance with IFRS 16 lease accounting is easier when right-of-use assets, depreciation schedules, and work orders live in the same database. Operators shifting from reactive to condition-based maintenance report 12-18% lower spend and 20-30% longer asset service life, while finance teams gain real-time visibility into work-in-progress balances that analysts track closely.

Increasing Regulatory And Compliance Demands

The United States Securities and Exchange Commission now requires Scope 1 and Scope 2 emissions to be audited within annual filings, pushing firms to automate carbon calculations inside ERP suites. Similar mandates under Europe’s Corporate Sustainability Reporting Directive and the North American Electric Reliability Corporation’s cybersecurity rules broaden the compliance footprint. Modules that map production data to emission factors and generate XBRL tags shorten reporting cycles and lower audit risk. New wholesale power rules, such as Federal Energy Regulatory Commission Order 2222, require settling virtual power plant transactions in revenue ledgers. Together, these policies make compliance functionality a core purchase criterion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation and Switching Costs | -0.7% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Data Security and Sovereignty Concerns | -0.6% | Middle East, Asia-Pacific, and Russia | Medium term (2-4 years) |

| Talent Shortage for Domain-Specific ERP | -0.5% | Global, strongest in North America and Middle East | Long term (≥ 4 years) |

| Legacy System Integration Complexity | -0.4% | Mature basins with aging infrastructure worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation And Switching Costs

Total cost of ownership ranges from USD 50,000 for a twelve-user cloud roll-out to more than USD 50 million for a multinational swap-out across upstream, midstream, and downstream units. Data migration of decades of well logs and partner records can stretch 18-24 months and lift budgets by double-digit percentages. Operators also absorb change-management expenses as employees adapt to new workflows. Subscription licenses shift spend from capital to operating budgets, yet multi-year commitments can still top USD 500,000 annually for midsize producers. Such economics dampen upgrade velocity when commodity prices soften.

Data Security And Sovereignty Concerns

Middle East regulators forbid storing production data outside national borders, making local data centers essential. Saudi Aramco’s partnership with Microsoft funds facilities in Riyadh and Dammam, but round-trip latency remains a hurdle to real-time SCADA integration when traffic spans long distances.[2]Saudi Aramco, “Microsoft Partnership Strengthens Digital Sovereignty,” aramco.com A recent survey found 43% of oil and gas IT leaders rank data residency as their primary cloud barrier. Hybrid architectures ease concerns but add middleware costs and dual support contracts, while ransomware events underscore the need for zero-trust frameworks and hardware security modules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Asset Management Dominance Reflects Maintenance Intensity

Asset Management retained 29.40% of 2025 revenue because offshore outages can halt production for weeks and trigger force majeure penalties. The oil and gas ERP market size tied to this module is set to expand steadily as operators install more sensors and feed real-time data into AI engines. Vendors that pair work-order automation with financial posting see faster adoption among producers striving for integrated reporting. In contrast, the Project Management Module grows at 11.80% CAGR as joint-venture drilling campaigns demand granular cost tracking.

Project Management gains traction in complex capital projects and partner allocations, particularly in deepwater basins. Supply Chain Management continues to matter for tubulars, drilling fluids, and critical spares, yet its growth lags because many firms have already optimized procurement cycles. Financial Management remains foundational, though budgets shift toward ESG and predictive analytics add-ons. Human Capital Management becomes more relevant in markets with strict safety certification renewal requirements.

By Deployment Mode: Hybrid Architectures Balance Sovereignty And Scalability

Cloud deployment held 62.10% of the oil and gas ERP market share in 2025, yet hybrid models posted the fastest growth at a 13.10% CAGR. Operators in Gulf states mix on-premises clusters for production data with public cloud for corporate functions to comply with sovereignty laws and enable burst capacity. Hybrid adoption also stems from latency needs, as automated well-control sequences tolerate less than 50 milliseconds round-trip time. The oil and gas ERP market size for on-premises solutions continues to shrink, surviving mainly in sanctioned regions or areas with limited connectivity.

Hybrid environments require strict master data governance because inconsistent well identifiers or vendor records can corrupt consolidated statements. Firms often invest USD 200,000-500,000 in middleware and API gateways to synchronize records. Despite the added complexity, the model offers resilience because workloads can swing between local and cloud nodes during outages or maintenance windows.

By Enterprise Size: SMEs Embrace Modular Cloud Solutions

Large enterprises accounted for 58.30% of 2025 spending, reflecting sprawling, multi-segment operations that demand joint-interest billing and multi-currency consolidation. Small and medium enterprises, however, expand at 12.20% CAGR by adopting subscription licenses that start at USD 150 per user per month. Turnkey templates for purchase orders, time sheets, and invoicing shorten deployment time from years to weeks, letting crews in the field capture costs on mobile devices. The talent shortage complicates rollouts for both tiers, but it affects SMEs harder because they struggle to attract experienced ERP consultants.

Advanced analytics remain the differentiator for large enterprises, which embed decline-curve forecasting and hedging simulations within their ERPs. SMEs rely more on vendor dashboards that highlight revenue per employee or inventory turns. As the talent gap persists, vendors add low-code tooling to let power users create reports without great technical skills.

By Application: Oilfield Services Pursue Real-Time Job Costing

Upstream governed 43.60% of 2025 revenue, but oilfield services recorded the highest forecast CAGR at 12.90%. Drilling contractors want dashboards that display rig utilization and let supervisors invoice within hours of job completion, shrinking days' sales outstanding. Operators increasingly insist that service partners deliver open APIs that expose real-time job progress, forcing a shift from legacy on-premises systems to cloud platforms. Midstream users seek tariff calculation and pipeline capacity modules, while downstream refiners prioritize blend optimization and inventory control.

Oil and gas ERP market share trends show service companies embracing consumption pricing that scales with active users. Integrating edge data, such as pump pressure or flow rates, into work orders moves maintenance from reactive to condition-based scheduling, extending asset life by up to 30%.

Geography Analysis

North America retained 44.90% share in 2025, anchored by Permian shale output and Gulf of Mexico deepwater spends. SEC climate-disclosure rules drive demand for embedded carbon reporting, and operators integrate ERP with emissions sensors to meet audit timelines. Canadian oil sands firms add custom modules to blend data from mining dispatch and upgrader units, while Mexican service companies cite uptime gains after modernizing legacy systems.

Asia-Pacific is the fastest-growing region, with a 11.30% CAGR through 2031. National oil companies in China are upgrading ERPs to link liquefied natural gas terminals to long-term sales contracts. Indian upstream operators digitize joint venture ledgers for Krishna-Godavari deepwater blocks, complying with the Directorate General of Hydrocarbons' e-submission mandates.[3]Directorate General of Hydrocarbons, “Electronic Data Submission Guidelines,” dghindia.gov.in Australian liquefied natural gas exporters leverage ERP to monitor billion-dollar engineering milestones.

The Middle East sees rapid adoption as national champions pursue diversification agendas and local-cloud partnerships. Saudi data-sovereignty laws steer vendors toward in-kingdom hosting, while Abu Dhabi National Oil Company rolls out hundreds of AI tools inside its SAP landscape. Europe focuses on modernizing Brownfield North Sea assets where decades-old SCADA systems still run. Emerging African producers prefer cloud to avoid high capital outlays, though limited offshore bandwidth slows real-time replication.

Competitive Landscape

The field remains moderately fragmented. SAP, Oracle, and Microsoft lead enterprise deals, while Quorum, Enertia, and P2 Energy Solutions compete on deep domain logic for joint-interest billing and land management. SAP deployments at S-OIL and Sharjah National Oil Corporation show how in-memory databases deliver real-time analytics.

Oracle pairs its ERP with Primavera project management tools to improve capital campaign visibility, and Microsoft gains momentum through its industrial AI partnership with Saudi Aramco. [4]Oracle, “Cloud ERP for Energy,” oracle.com Cloud-native challengers such as Acumatica and Odoo win small and medium enterprise accounts with rapid, template-based launches. IFS distinguishes itself with generative AI agents that parse maintenance logs and auto-dispatch technicians. RigER and Capgemini EnergyPath specialize in oilfield services, enabling mobile work orders and same-day invoicing.

Consolidation stays muted because tier-one vendors prefer in-house module development over niche acquisitions. Integration with operational technology is now a baseline requirement, pushing ERP vendors to partner with automation majors for secure data pipelines.

Oil And Gas Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Infor, Inc.

IFS AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Saudi Aramco and Microsoft agreed to co-develop industrial AI modules and build data centers in Riyadh and Dammam, with plans to train 10,000 nationals in cloud skills.

- February 2026: Abu Dhabi National Oil Company reported more than 200 AI tools integrated into its SAP ERP, cutting inventory carrying costs by 15% and boosting demand-forecast accuracy by 12%.

- September 2025: Sharjah National Oil Corporation chose RISE with SAP, hosting finance, procurement, and human resources on Azure UAE Central to support gas expansion plans.

- May 2025: Aramco Digital launched NextEra, blending edge sensors and ERP workflows to forecast equipment failures up to 45 days ahead.

Global Oil And Gas Enterprise Resource Planning Market Report Scope

The Oil and Gas ERP market comprises specialized enterprise software solutions and associated services that manage, integrate, and optimize core business processes across the oil and gas value chain.

The Oil and Gas ERP Market Report is Segmented by Component (Financial Management Module, Asset Management Module, Supply Chain Management Module, Project Management Module, Human Capital Management Module, Other Components), Deployment Mode (Cloud, On-Premise, Hybrid), Enterprise Size (Small and Medium Enterprises, Large Enterprises), Application (Upstream, Midstream, Downstream, Oilfield Services), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Financial Management Module |

| Asset Management Module |

| Supply Chain Management Module |

| Project Management Module |

| Human Capital Management Module |

| Other Components |

| Cloud |

| On-Premise |

| Hybrid |

| Small and Medium Enterprises |

| Large Enterprises |

| Upstream |

| Midstream |

| Downstream |

| Oilfield Services |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | Nigeria |

| South Africa | |

| Rest of Africa |

| By Component | Financial Management Module | |

| Asset Management Module | ||

| Supply Chain Management Module | ||

| Project Management Module | ||

| Human Capital Management Module | ||

| Other Components | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| Hybrid | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Application | Upstream | |

| Midstream | ||

| Downstream | ||

| Oilfield Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | Nigeria | |

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the oil and gas ERP market be by 2031?

It is forecast to reach USD 5.16 billion by 2031, rising from USD 3.84 billion in 2026 at a 6.08% CAGR.

Which ERP component attracts the most spending today?

The Asset Management Module leads with 29.40% of 2025 revenue because predictive maintenance cuts costly unplanned downtime.

Why are hybrid deployments growing fastest?

National data residency laws and the need for sub-50-millisecond latency on production data push operators toward hybrid architectures that mix local clusters with public cloud.

What drives ERP adoption among small and medium oilfield service firms?

Subscription pricing around USD 150 per user per month and mobile templates for job costing allow smaller contractors to improve cash flow without heavy IT investment.

Which region is expanding at the quickest pace?

Asia-Pacific posts the fastest regional CAGR at 11.30% through 2031 as national oil companies modernize systems for liquefied natural gas and energy transition portfolios.

How are new regulations shaping ERP functionality?

SEC climate disclosures and European sustainability directives require automated carbon accounting and XBRL tagging, making compliance modules a top purchase criterion.

Page last updated on: