ASEAN Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

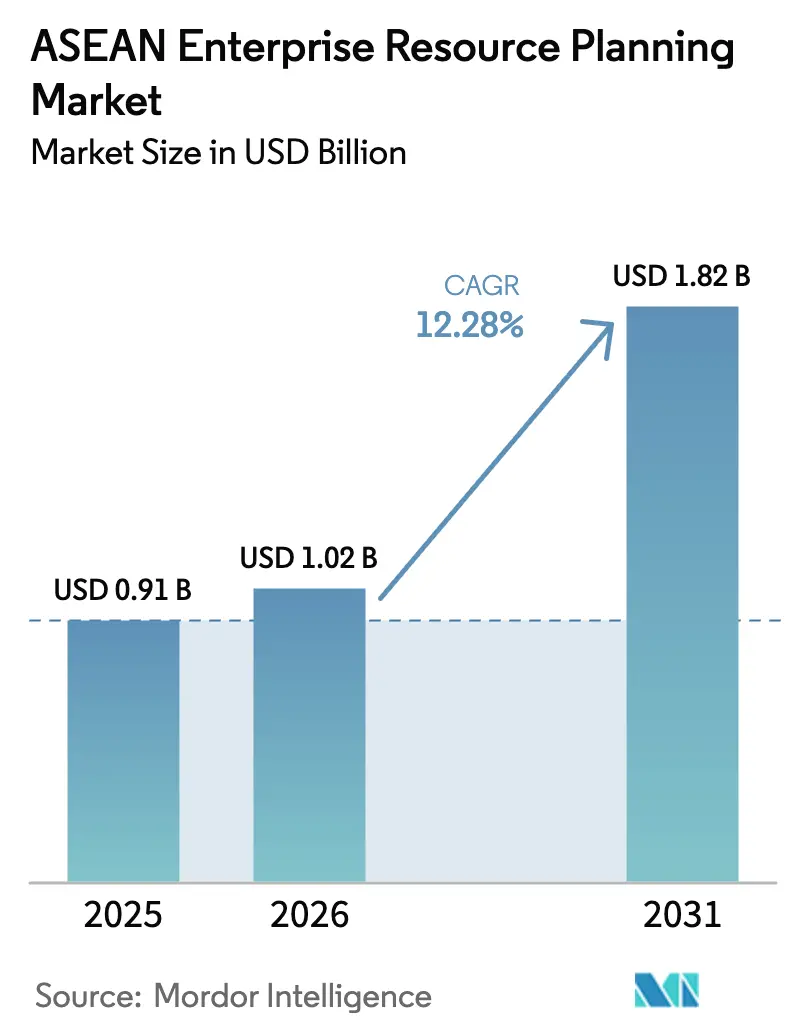

| Base Year Market Size (2025) | USD 0.91 Billion |

| Market Size (2026) | USD 1.02 Billion |

| Market Size (2031) | USD 1.82 Billion |

| Growth Rate (2026 - 2031) | 12.28% CAGR |

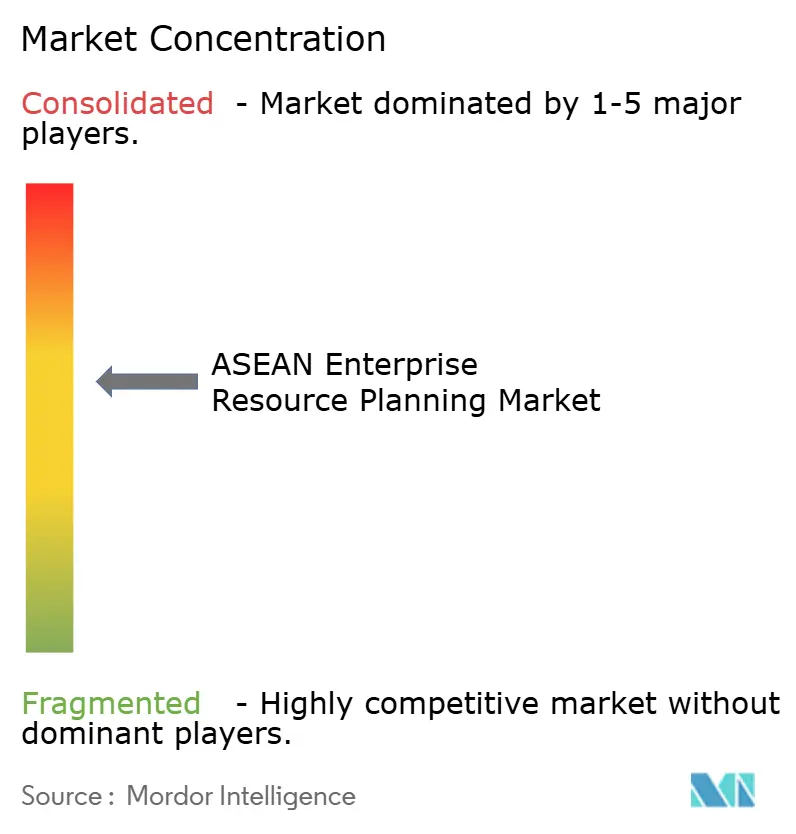

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Enterprise Resource Planning Market Analysis by Mordor Intelligence

The ASEAN enterprise resource planning market size is expected to grow from USD 0.91 billion in 2025 to USD 1.02 billion in 2026 and is forecast to reach USD 1.82 billion by 2031 at a 12.28% CAGR over 2026-2031. Momentum rests on synchronized digital-economy mandates, cross-border data-flow harmonization, and a rapid pivot away from fragmented legacy systems in Indonesia, Thailand, Malaysia, Singapore, and the Philippines. Cloud deployments dominate new rollouts, but country-specific data-sovereignty rules are steering enterprises toward hybrid topologies that keep sensitive datasets on-premises while running transactional layers in the public cloud. Demand for integrated human capital, finance, and supply chain suites is rising as mid-market manufacturers, retailers, and healthcare providers pursue real-time visibility, statutory payroll accuracy, and traceability. Vendor competition centers on AI-embedded decision engines, industry-specific templates, and regional implementation capacity, which shorten time-to-value for both large enterprises and high-growth SMEs.

Key Report Takeaways

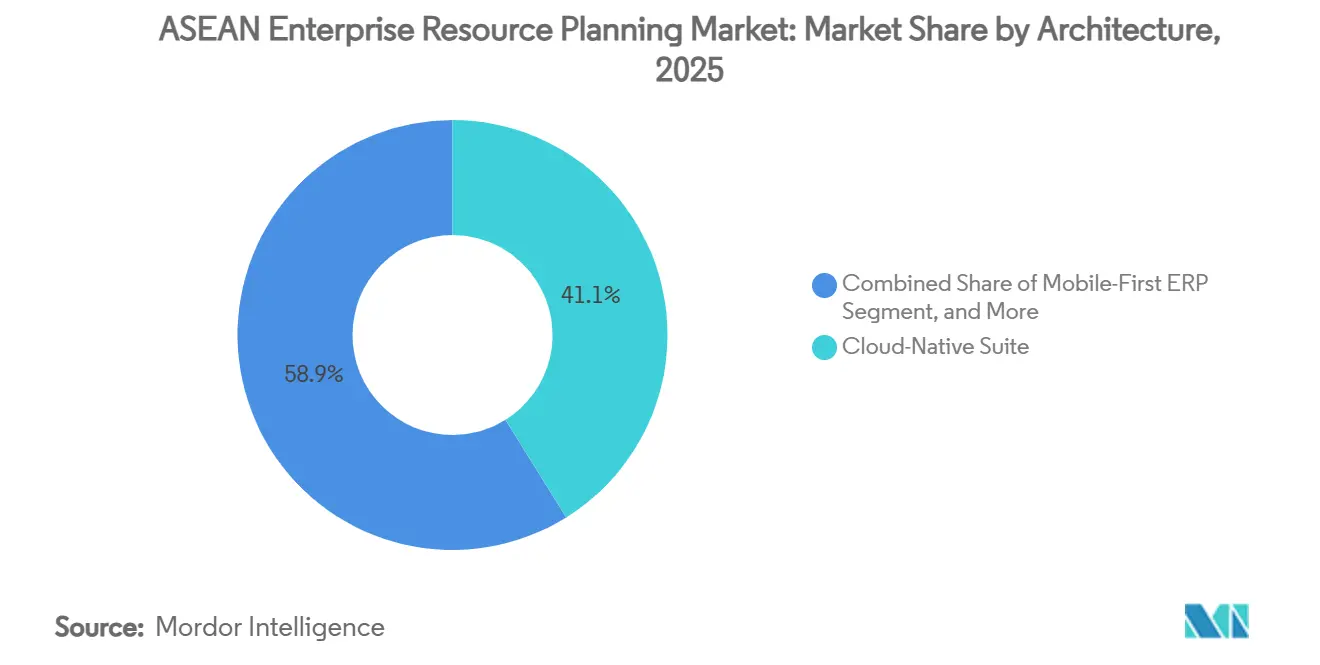

- By deployment model, cloud commanded 71.26% of the ASEAN enterprise resource planning market share in 2025, while two-tier or edge architectures are projected to expand at a 13.08% CAGR through 2031.

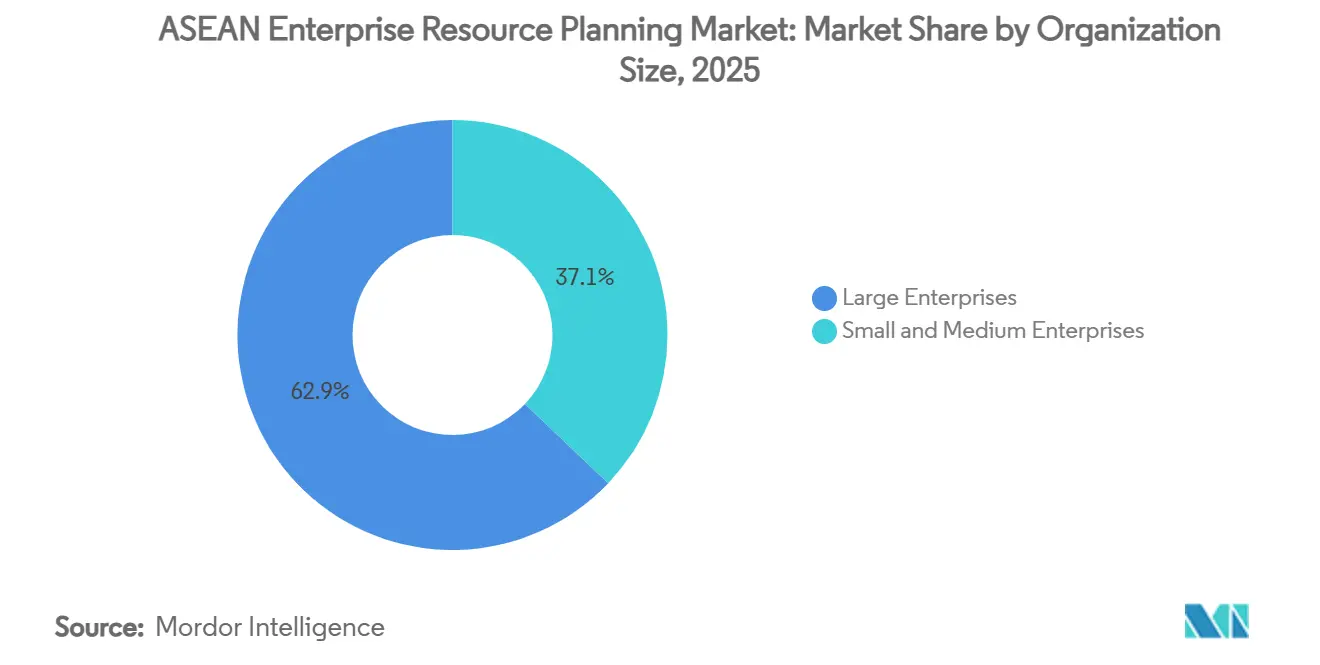

- By organization size, large enterprises accounted for 62.89% of the ASEAN ERP market in 2025, yet the SME segment is set to grow at a 12.68% CAGR through 2031.

- By business function, the finance and accounting segment is expected to account for the largest share, 35.16%, over the forecast period. Human-capital management grew by 13.28%, outpacing finance modules.

- By industry vertical, manufacturing captured 26.77% of the market share in 2025, whereas healthcare and life sciences are forecast to grow at a 13.68% CAGR.

- By geography, Singapore led with 29.14% revenue share in 2025, and Indonesia is on track for the fastest country-level growth at 13.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

ASEAN Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud Migration Acceleration among ASEAN SMEs | +2.8% | Indonesia, Philippines, Vietnam, early gains in Thailand and Malaysia | Medium term (2-4 years) |

| Rising Government Digital Economy Initiatives | +2.5% | ASEAN-wide, strongest in Indonesia, Thailand, Singapore | Long term (≥ 4 years) |

| Integration of AI and Analytics into ERP | +2.1% | Singapore, Malaysia, Thailand core; spill-over to Indonesia, Philippines | Medium term (2-4 years) |

| Adoption of Modular Two-Tier ERP for Subsidiaries | +1.7% | Regional headquarters in Singapore, subsidiaries across ASEAN | Short term (≤ 2 years) |

| Growing Mobile Workforce Demanding Anytime Access | +1.4% | ASEAN-wide, led by Indonesia and Philippines | Short term (≤ 2 years) |

| Surge in ESG Reporting Needs Driving ERP Upgrades | +1.2% | Singapore, Thailand, Malaysia; emerging in Indonesia and Philippines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud Migration Acceleration Among ASEAN SMEs

Small and medium enterprises are shifting to cloud-native suites to avoid capital expenditure on servers, scale modules incrementally, and keep statutory requirements up to date without manual patching. Digital-native retailers and logistics firms founded after 2024 bypassed desktop accounting entirely, choosing subscription packages that bundle inventory, payroll, and e-invoicing. Subsidy programs in Malaysia and Indonesia routinely offset up to half of first-year fees, compressing payback periods to under 18 months. Vendors that offer free trials and localized tax engines win conversions quickly, and quarterly automatic updates ensure compliance with rapid regulatory changes, reducing audit-related downtime.

Rising Government Digital Economy Initiatives

Regional policy frameworks now treat ERP software as foundational infrastructure. Preferential procurement scoring for suppliers connected via API to government portals and low-interest transformation loans pressure manufacturers, healthcare providers, and service firms to upgrade. Thailand 4.0 incentives, Indonesia’s co-funding roadmap, and Singapore’s Smart Nation 2.0 collectively underwrite upgrade costs, making ERP adoption a prerequisite for accessing trade-finance, tax holidays, or fast-track licensing.[1]Source: Singapore Government, “Smart Nation 2.0 Procurement Guide,” smartnation.gov.sg Enforcement mechanisms, such as real-time invoice or e-tax submission, convert policy into immediate operating requirements rather than aspirational goals.

Integration of AI and Analytics into ERP Suites

Artificial intelligence modules embedded in finance, supply chain, and maintenance workflows reduce days sales outstanding, predict equipment failures, and highlight spend anomalies. Natural-language query interfaces allow controllers to surface non-compliant payments within seconds, halving the month-end close time. Predictive planning aligns procurement with demand signals from e-commerce portals, trimming excess inventory by double digits in pilot projects. The transition re-positions ERP as an active decision partner rather than a passive system of record.

Adoption of Modular Two-Tier ERP for Subsidiaries

Multinationals deploy heavyweight suites at headquarters and lightweight, country-specific platforms at ASEAN subsidiaries, syncing ledgers nightly to meet consolidation deadlines without incurring the expense of global-instance customizations. Local teams gain autonomy to meet e-invoicing, VAT, and payroll localization mandates, while headquarters maintains group-wide visibility. Pre-built connectors slash deployment time from 9 months to as little as 8 weeks, mitigating talent shortages and reducing consulting costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Sovereignty and Localization Regulations | -1.8% | Indonesia, Thailand, Vietnam; moderate in Malaysia, Philippines | Medium term (2-4 years) |

| Shortage of ERP Implementation Talent in ASEAN | -1.5% | ASEAN-wide, most acute in Indonesia, Philippines, Vietnam | Long term (≥ 4 years) |

| Legacy System Integration Complexities | -1.1% | Manufacturing and BFSI sectors across ASEAN | Short term (≤ 2 years) |

| High Total Cost of Ownership for SMEs | -0.9% | Indonesia, Philippines, Vietnam, Thailand SME segment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Sovereignty and Localization Regulations

Mandates in Indonesia, Thailand, and Vietnam require local data storage for citizen or sensitive records, forcing ERP vendors to operate domestic cloud regions or hybrid topologies. Indonesia's Government Regulation 71/2019 mandates that all electronic systems handling citizen data must store and process information within the country, effectively prohibiting pure public-cloud ERP deployments for government contractors, healthcare providers, and financial institutions unless vendors establish in-country data centers.[2]Source: Baker McKenzie, “Indonesia Government Regulation 71/2019 Data Localization,” bakermckenzie.comAdditional audit, infrastructure, and legal costs inflate subscription pricing by up to one-quarter and slow feature parity relative to markets without residency restrictions. Enterprises that cannot justify the expense of private cloud defer modernization, preserving a pool of on-premises systems that drags overall growth.

Shortage of ERP Implementation Talent in ASEAN

Regional demand for certified functional consultants exceeds supply, pushing wages 30% above those for general IT roles and stretching implementation timelines from 6 to 10 months. Out-migration of experienced Philippine and Indonesian specialists deepens the gap, while language barriers limit the pool in Vietnam. Vendors respond with low-code configuration and pre-built templates, yet complex cutover weekends and post-go-live stabilization still require scarce experts, extending project risk and cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Two-Tier Configurations Lead Subsidiary Modernization

Two-tier architectures captured 13.08% growth and represent the fastest-expanding segment within the ASEAN enterprise resource planning market. These architectures enable headquarters instances of SAP or Oracle to synchronize nightly with subsidiary platforms such as NetSuite or Business Central. This synchronization eliminates manual currency translation errors, streamlines financial reporting, and reduces consolidation cycles from weeks to just a few days. Cloud-native suites accounted for 41.12% of the installed base in 2025, while mobile-first platforms cater to logistics and field-service operators who require seamless smartphone access for their operations.

Localized compliance requirements significantly drive the adoption of this architecture. The presence of separate e-tax portals, payroll statutes, and invoice formats across five key ASEAN markets makes it economically unfeasible to customize a single global instance. Instead, subsidiaries can implement localized platforms and go live within 3 months, with support from regional partners well-versed in domestic regulations. Meanwhile, headquarters retains centralized control over group reporting and financial oversight. Consequently, two-tier adoption has become a cornerstone of hybrid rollouts, solidifying its role in the growth and evolution of the market.

By Business Function: Human Capital Management Outpaces Finance Modules

Human-capital suites will expand at 13.28% through 2031, eclipsing finance as enterprises seek accurate payroll, leave, and benefits processing across 11 statutory landscapes. The finance and accounting segment accounts for 35.16% of spend, but growth moderates as many firms have already automated core ledgers. Fragmented social-security rules expose firms to penalties when calculations go awry, turning payroll accuracy into a board-level risk. Unified cloud payroll covering Indonesia, Malaysia, Thailand, Singapore, the Philippines, and Vietnam reduces manual filing errors by over one-third.[3]Source: Ramco Systems, “Global Payroll Localization Across Southeast Asia,” ramco.com In turn, policy-driven complexities in overtime and severance accelerate demand for modern HCM suites in the ASEAN enterprise resource planning market.

The market is divided into finance, human resources, supply chain management, manufacturing, procurement, and customer relationship management (CRM). Finance modules continue to serve as the foundation of ERP implementations, as they play a critical role in financial reporting, budgeting, taxation, and regulatory compliance. However, supply chain and procurement functions are seeing increased adoption as businesses in the region expand cross-border trade and seek enhanced visibility into supplier networks, inventory management, and logistics. At the same time, CRM modules are gaining traction as companies prioritize customer engagement, sales forecasting, and service management.

By Deployment Model: Cloud Dominance Masks Hybrid Reality

Cloud solutions currently hold a significant 71.26% share of the market; however, hybrid cloud deployment patterns are increasingly prevalent, particularly in regulated industries. In these sectors, application layers are typically hosted in the public cloud to leverage scalability and automatic updates. Meanwhile, databases containing sensitive, personally identifiable information are often kept on-premises to comply with stringent data localization regulations. This trend is especially evident in countries such as Indonesia, under Regulation 71, and Thailand, under the Personal Data Protection Act (PDPA). As a result, organizations in these regions adopt a blended cloud topology that balances the benefits of public cloud services with the need for strict data control and compliance.

On-premise solutions remain critical in specific industries, such as the Thai automotive sector and Indonesian mining operations. In these cases, legacy manufacturing execution systems or challenges like unreliable network bandwidth make low latency a non-negotiable requirement. Consequently, adoption of pure public cloud solutions grows more slowly in these industries. However, overall spending on hybrid cloud solutions continues to drive growth in the ASEAN ERP market, as businesses increasingly seek flexible, compliant IT infrastructure to meet their operational needs.

By Organization Size: SME Growth Outpaces Enterprise Segment

Large enterprises accounted for 62.89% of the projected revenue in 2025, yet small and medium enterprises (SMEs) are expected to record a compound annual growth rate (CAGR) of 12.68% through 2031, gradually narrowing the revenue gap. Freemium models or low-cost subscription bundles, typically priced under USD 200 per month, are increasingly appealing to micro-retailers and digital-native startups. These businesses are opting for such solutions to bypass traditional spreadsheet-based operations from the outset. Additionally, government initiatives, such as credits and co-funding programs, significantly reduce first-year costs, effectively halving the financial burden for firms with annual revenues below USD 5 million, thereby accelerating their return on investment.

Meanwhile, enterprise buyers are reallocating their budgets toward advanced AI-powered add-ons, managed services, and the modernization of complementary platforms, such as analytics and warehouse management systems. Mid-market vendors are seizing opportunities by offering tailored solutions, particularly in scenarios where global vendors struggle to justify their resource-intensive consulting models. These evolving dynamics are contributing to a more diverse vendor landscape within the ASEAN ERP market.

By Industry Vertical: Healthcare Digitalization Accelerates

Manufacturing retained a 26.77% share in 2025, thanks to automotive and electronics corridors, yet healthcare and life sciences will post a 13.68% CAGR, the fastest among segments. Hospital accreditation now requires electronic records integration, while distributors chase serialization and Good Distribution Practice compliance. Retail and e-commerce operators merge point-of-sale, marketplace, and social commerce data into a unified ERP to eliminate stock mismatches. Banks and insurers overlay anti-money laundering or IFRS 17 modules on their finance cores. Each use case feeds verticalized demand, enlarging the ASEAN enterprise resource planning market.

Healthcare providers across ASEAN countries are increasingly adopting modern ERP solutions to comply with regulatory requirements for electronic medical records (EMR) integration, digital patient data management, and standardized reporting systems. Simultaneously, pharmaceutical distributors and medical supply chains are leveraging ERP systems to comply with drug serialization mandates, verify product authenticity, and meet Good Distribution Practice (GDP) regulations, thereby enhancing transparency and safety within the healthcare supply chain.

Geography Analysis

Singapore generated 29.14% of 2025 revenue and continues to serve as the implementation hub for the ASEAN enterprise resource planning market. The country houses regional support centers for major vendors such as SAP, Microsoft, Oracle, and Workday. Smart Nation procurement rules require API integration, ensuring a consistent flow of upgrades as suppliers compete to meet contract eligibility standards. Additionally, financial-services regulators in Singapore actively endorse cloud adoption, driving core-banking overhauls valued at over USD 1 billion between 2024 and 2026. While growth in Singapore remains steady, it is expected to slow toward baseline levels as market saturation increases. Incremental revenue in the region is anticipated to shift toward AI-driven analytics and the expansion of ERP modules.

Indonesia is projected to achieve a robust 13.48% CAGR, leading the region in growth. Government co-funding initiatives, a booming consumer internet sector, and the need for nuanced localization are key drivers of ERP adoption in the country. Specific requirements, such as e-Faktur invoicing, BPJS contributions, and provincial labor law variations, create strong demand for tailored ERP suites. While domestic vendors dominate the micro-enterprise segment, global platforms are increasingly securing contracts with state-owned enterprises and multinational corporations.

Thailand, Malaysia, and the Philippines are expected to grow slightly above the regional average. In Thailand, automotive and food-processing exporters are deploying traceability modules to maintain access to the EU and U.S. markets. Malaysia’s electronics and palm oil supply chains are adopting sustainability reporting practices to comply with international deforestation regulations. Meanwhile, Philippine business-process-outsourcing firms are integrating ERP systems with CRM and patient-management platforms to better control margins and adhere to data-privacy laws. Vietnam, although smaller in terms of measured revenue, is benefiting significantly from the China-plus-one manufacturing strategy. This trend is fueling rapid adoption of cloud-based supply-chain solutions, further contributing to the growth of the ASEAN ERP market.

Competitive Landscape

The ASEAN enterprise resource planning market is moderately concentrated: SAP, Microsoft, Oracle, Infor, and Workday collectively control approximately 60% of enterprise-tier licenses, while the SME segment remains fragmented among numerous regional specialists. Global vendors differentiate themselves through advanced offerings such as AI co-pilots, vertical clouds tailored to specific industries, and sovereign-cloud options designed to meet stringent data sovereignty requirements. On the other hand, regional challengers gain a competitive edge by focusing on shorter implementation timelines, localized tax engines tailored to specific regulatory needs, and user-friendly native-language interfaces.

Key disruption themes in the market include the rise of open-source ERP models, which are scaling to cost-effective monthly subscriptions of around USD 150, and the integration of AI querying capabilities that significantly reduce financial close cycles. Additionally, asset-lifecycle acquisitions are adding environmental, social, and governance (ESG) functionalities, which are becoming increasingly important for compliance and sustainability reporting. Vendors with ISO 27001 and SOC 2 certifications are gaining a competitive advantage, particularly when bidding for contracts with banks, healthcare providers, and government agencies. Emerging trends such as hybrid deployment models, halal-food traceability systems, and specialized Islamic-finance modules are also shaping the competitive landscape and creating new opportunities for growth.

Strategic alliances are playing a crucial role in the market. For instance, SAP’s merchant integration with Grab and Microsoft’s USD 2.2 billion Southeast Asia cloud expansion are positioning these incumbents to defend their market share while simultaneously targeting regulated industries. At the same time, the persistent shortage of skilled ERP professionals is driving demand for managed-service providers. These providers are increasingly relied upon to stabilize go-live processes and manage post-deployment optimization, thereby redistributing services revenue across the ASEAN enterprise resource planning market and ensuring smoother transitions for businesses adopting ERP solutions.

ASEAN Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Infor Inc.

The Sage Group Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Avanade, a top-tier provider of Microsoft solutions, was set to acquire Total eBiz Solutions. Headquartered in Singapore, Total eBiz Solutions boasts a strong proficiency in Microsoft technologies. This acquisition, Avanade's inaugural move in Southeast Asia, bolsters its capacity to assist mid-market businesses and public sector clients in their transformation journeys.

- July 2025: Rolling Arrays Consulting, a top HR transformation firm based in Singapore and supported by Skyform & Seatown Capital Master Fund, has officially joined the Workday global partner program. This partnership aims to harness innovation and underscores a pivotal step in bolstering Workday's footprint in Southeast Asia (SEA). With a focus on delivering state-of-the-art HR and ERP solutions, Rolling Arrays is poised to meet the region's dynamic workforce demands.

- April 2025: ABeam Consulting, a prominent global management consulting firm, has forged a strategic alliance with WalkMe, an SAP subsidiary and a frontrunner in the Digital Adoption Platform (DAP) arena. This partnership seeks to redefine ERP implementation and digital transformation services throughout Southeast Asia, amplifying value for clients and solidifying ABeam Consulting's stature as a digital transformation leader.

- February 2025: Microsoft committed USD 2.2 billion to new Azure zones in Indonesia and Thailand, enabling Dynamics 365 customers to satisfy data-localization rules.

ASEAN Enterprise Resource Planning Market Report Scope

The ASEAN enterprise resource planning (ERP) market encompasses the adoption and implementation of ERP systems across various industries in the ASEAN region. ERP systems integrate core business processes, including finance, supply chain, human resources, and customer relationship management, into a unified platform to enhance operational efficiency, data accuracy, and decision-making capabilities. This market focuses on solutions tailored to the unique needs of businesses in the ASEAN region, accounting for regional regulations, industry-specific requirements, and the growing demand for cloud-based, mobile-first ERP solutions.

The ASEAN enterprise resource planning market report is Segmented by Architecture (Cloud-Native Suite, Mobile-First ERP, Social/Collaborative ERP, and Two-Tier/Edge ERP), Business Function (Finance and Accounting, Supply-Chain and Operations, Human Capital Management, Customer Relationship and Commerce, and Manufacturing Execution and Quality), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Manufacturing, Retail and E-commerce, BFSI, Government and Public Sector, IT and Telecom, Healthcare and Life Sciences, and Others Industry Verticals), and Geography (Singapore, Thailand, Malaysia, Indonesia, Philippines, and Rest of ASEAN). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Native Suite |

| Mobile-First ERP |

| Social / Collaborative ERP |

| Two-Tier / Edge ERP |

| Finance and Accounting |

| Supply-Chain and Operations |

| Human Capital Management |

| Customer Relationship and Commerce |

| Manufacturing Execution and Quality |

| On-Premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing |

| Retail and E-commerce |

| BFSI |

| Government and Public Sector |

| IT and Telecom |

| Healthcare and Life Sciences |

| Others Industry Verticals |

| Singapore |

| Thailand |

| Malaysia |

| Indonesia |

| Philippines |

| Rest of ASEAN |

| By Architecture | Cloud-Native Suite |

| Mobile-First ERP | |

| Social / Collaborative ERP | |

| Two-Tier / Edge ERP | |

| By Business Function | Finance and Accounting |

| Supply-Chain and Operations | |

| Human Capital Management | |

| Customer Relationship and Commerce | |

| Manufacturing Execution and Quality | |

| By Deployment Model | On-Premise |

| Cloud | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Industry Vertical | Manufacturing |

| Retail and E-commerce | |

| BFSI | |

| Government and Public Sector | |

| IT and Telecom | |

| Healthcare and Life Sciences | |

| Others Industry Verticals | |

| By Geography | Singapore |

| Thailand | |

| Malaysia | |

| Indonesia | |

| Philippines | |

| Rest of ASEAN |

Key Questions Answered in the Report

What is the projected value of the ASEAN enterprise resource planning market in 2031?

The market is forecast to reach USD 1.82 billion by 2031.

Which deployment model is growing fastest across Southeast Asia?

Two-tier and edge architectures are expanding at 13.08% CAGR, the quickest among all deployment types.

Why are human-capital modules seeing higher adoption than finance modules?

Complex multi-country payroll laws in ASEAN drive organizations to modern HCM suites that automate statutory compliance.

Which country is expected to deliver the highest ERP growth through 2031?

Indonesia is poised for the fastest growth, projected at 13.48% CAGR.

How do data-localization rules affect ERP adoption?

Mandated in Indonesia, Thailand, and Vietnam, these rules push enterprises toward hybrid or in-country cloud regions, raising costs but ensuring legal compliance.

Page last updated on: