Enterprise Resource Planning Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

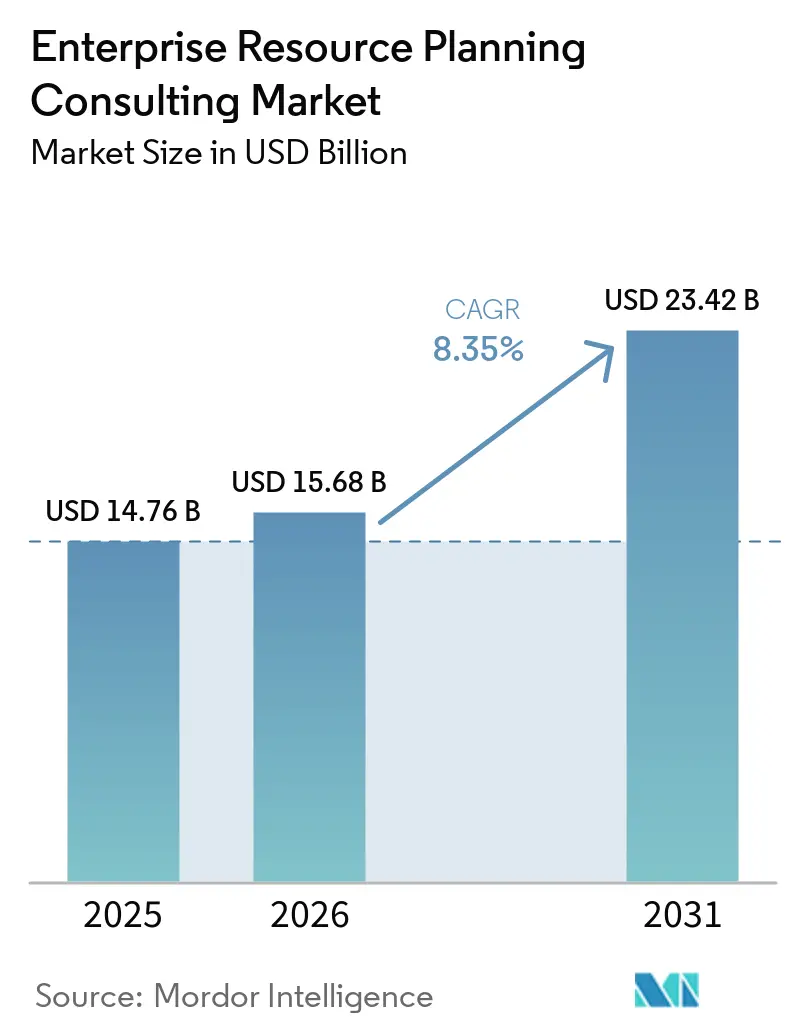

| Market Size (2026) | USD 15.68 Billion |

| Market Size (2031) | USD 23.42 Billion |

| Growth Rate (2026 - 2031) | 8.35% CAGR |

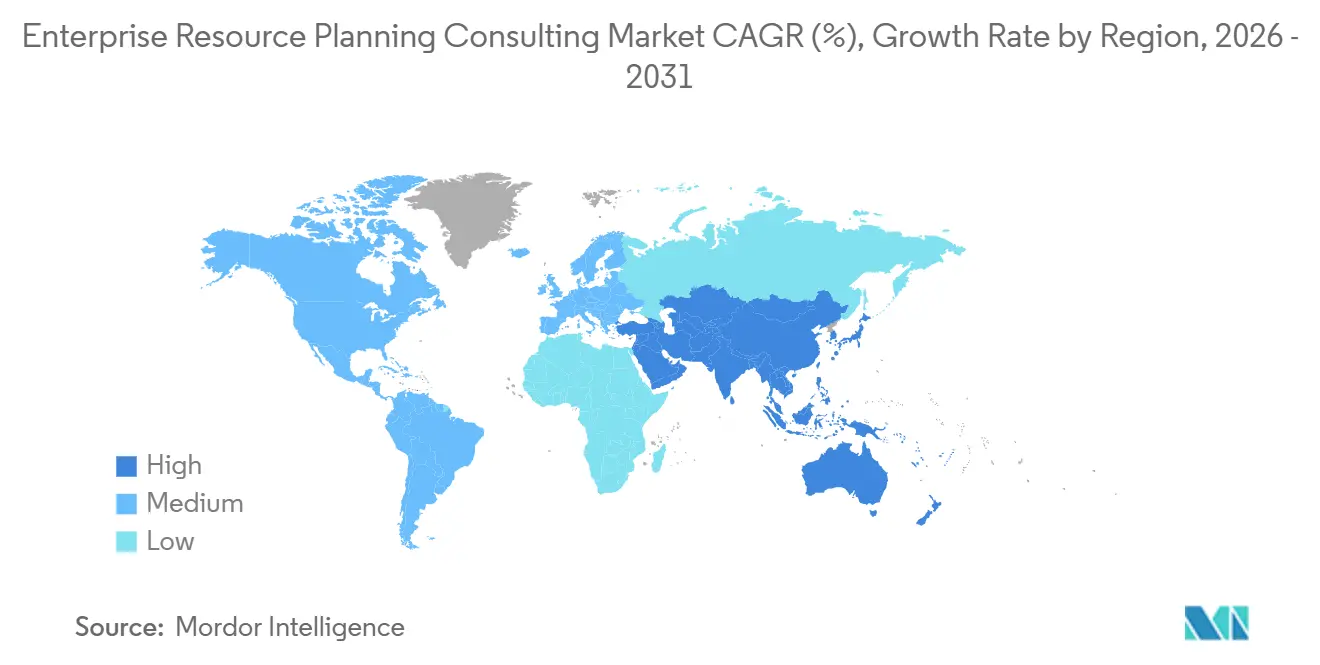

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

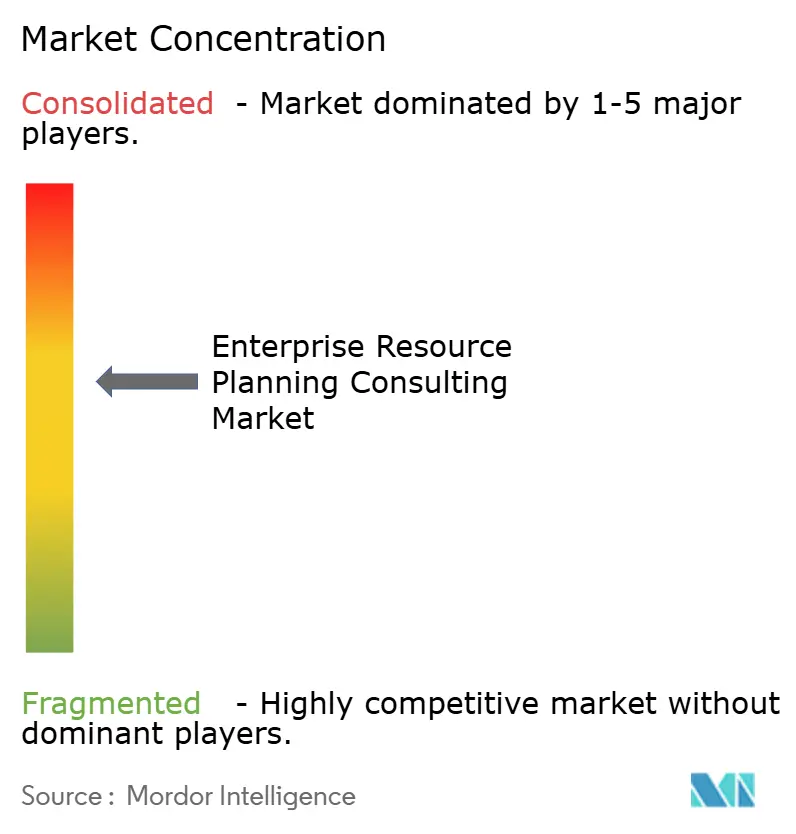

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Resource Planning Consulting Market Analysis by Mordor Intelligence

The ERP consulting services market size is projected to be USD 14.76 billion in 2025, USD 15.68 billion in 2026, and reach USD 23.42 billion by 2031, growing at a CAGR of 8.35% from 2026 to 2031. The shift toward subscription-based engagements is accelerating as enterprises migrate legacy environments to cloud-native and hybrid architectures, compressing implementation cycles and expanding post-go-live optimization demand. Outcome-based contracts that link fees to metrics such as order-to-cash reduction are replacing hourly billing, creating stronger alignment between consultants and clients. Cloud deployment already dominates new projects because it eliminates capital expenditure and supports continuous quarterly upgrades. Regulatory mandates on data privacy, cybersecurity, and sustainability reporting are further propelling advisory spend as organizations seek expert guidance on compliance, controls, and audit readiness.

Key Report Takeaways

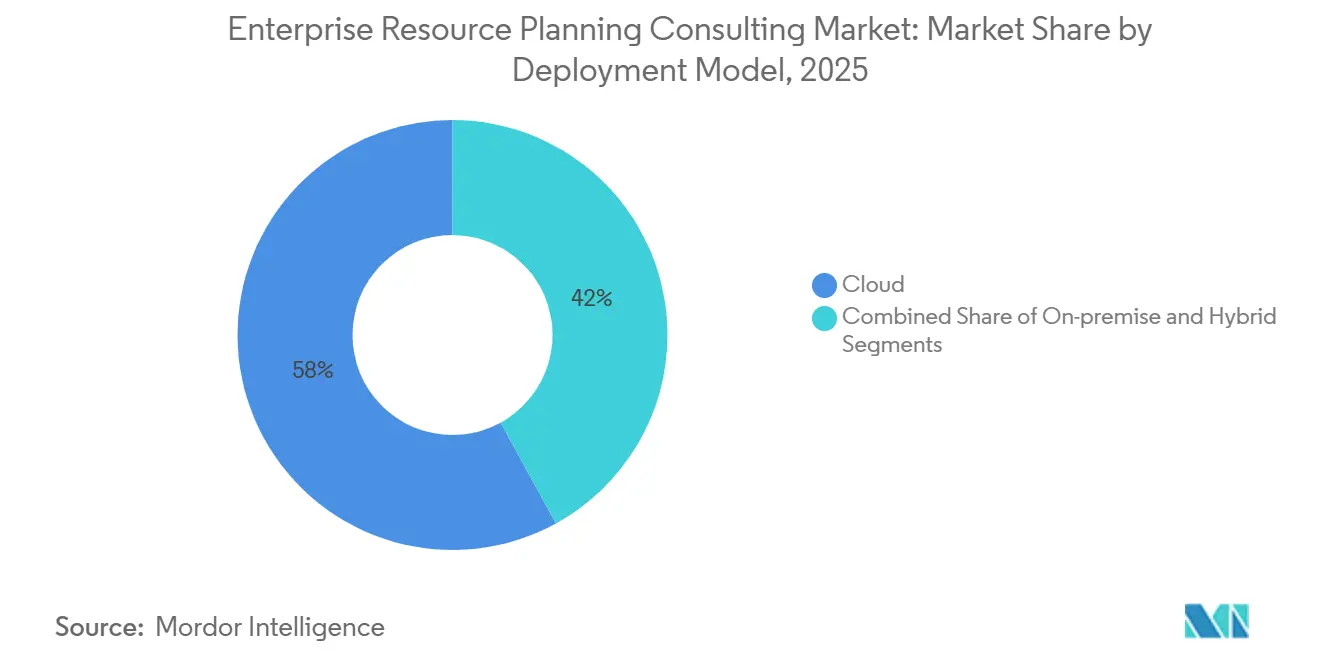

- By deployment mode, cloud led with 58% share in 2025 and is advancing at a 12.40% CAGR through 2031.

- By enterprise size, large enterprises held 61% share in 2025, while SMEs recorded the highest projected CAGR at 12.70% over 2026-2031.

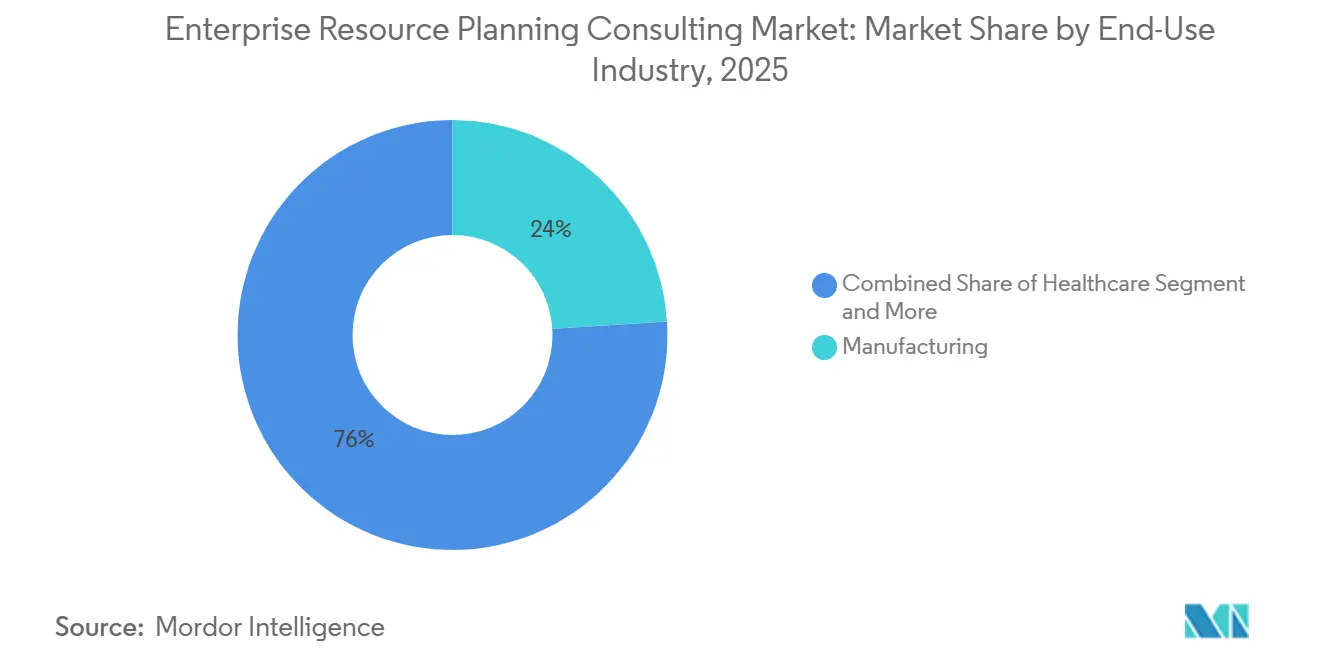

- By end user industry, manufacturing accounted for 24% of the ERP consulting services market share in 2025, whereas healthcare is forecast to expand at a 11.80% CAGR through 2031.

- By geography, North America accounted for 38% of revenue in 2025, and Asia-Pacific is set to grow at a 11.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Enterprise Resource Planning Consulting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-Native ERP Demand Among SMEs | +2.8% | Global, concentrated in urban North America, Europe, APAC | Medium term (2-4 years) |

| Shift to Composable ERP Architecture | +2.1% | Global, early adoption in North America and Western Europe | Long term (≥4 years) |

| Rise of Outcome-Based Consulting Contracts | +1.5% | North America and Europe, emerging in APAC | Medium term (2-4 years) |

| Post-Pandemic Digital Transformation Budgets Rebound | +1.3% | Global, strongest in North America and APAC | Short term (≤2 years) |

| Industry-Specific ERP Templates Accelerating Adoption | +0.9% | Global, vertical focus in manufacturing, healthcare, retail | Medium term (2-4 years) |

| Integration of AI-Driven Process Mining | +0.7% | North America, Europe, APAC tech hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Cloud-Native ERP Demand Among SMEs

Small and medium enterprises are adopting cloud platforms because subscription pricing aligns costs with revenue cycles and removes the burden of on-premises infrastructure. Workday earmarked CAD 1 billion (USD 770 million) to expand Canadian cloud ERP capacity, targeting firms with 500–5,000 employees that previously relied on entry-level accounting tools. Consulting partners fill migration skill gaps by supplying pre-configured templates that cut go-live timelines from 18 months to fewer than six. SAP confirmed that SMEs represented 60% of its Q4 2024 APAC wins through its RISE program.[1]Infosys Ltd., “Infosys and SAP Announce Strategic Collaboration to Accelerate Enterprise Cloud Transformation,” infosys.com Demand for data cleansing and GDPR-compliant residency services is growing across European boutique practices.

Shift to Composable ERP Architecture

Enterprises are decomposing monolithic suites into API-connected components that enable finance, supply chain, and HR modules to upgrade independently, reducing vendor lock-in risk. Banks separate customer-facing channels from core ledgers to launch products faster. Retailers pair SAP finance with Blue Yonder inventory engines via MuleSoft or Boomi middleware, creating demand for integration-centric consulting. Deloitte and Capgemini market proprietary accelerators that auto-map APIs, shortening design phases. Composability also aids mergers when multiple ERPs must coexist under a unified data layer, though inconsistencies in master-data governance spark advisory projects on stewardship frameworks.

Rise of Outcome-Based Consulting Contracts

Clients increasingly insist that consultants share risk through fee models tied to operational KPIs. TCS and SAP agreed to USD 1 billion of projects with performance guarantees, including penalties for missing 12-month targets. Continuous-improvement 'hyper-care' teams remain on site for up to a year post-go-live, extending engagement longevity but deferring revenue recognition. The model is strongest in North America and Europe, where legal enforcement of service-level agreements is robust; APAC adoption lags due to weaker contract frameworks. Consultants favor cloud platforms with embedded analytics to track KPI attainment transparently, minimizing disputes.

Post-Pandemic Digital Transformation Budgets Rebound

IT spending rebounded after pandemic freezes as CFOs redirected capital to projects that strengthen remote-work productivity and supply-chain resilience. Clorox allocated USD 580 million to an SAP S/4HANA rollout in 2024 after raw-material shortages highlighted limitations of its legacy system. Government stimulus in India and Southeast Asia funds public-sector ERP modernization, steering long-term consulting pipelines. Inflationary pressures force executives to seek 2-year ROI, favoring cloud deployments over capital-intensive on-premises estates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Certified ERP Consultants | −1.2% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Rising Cybersecurity Concerns Delaying Projects | −0.9% | Global, intense in regulated sectors | Short term (≤2 years) |

| Inflation-Driven IT Budget Compression | −0.6% | Global, severe in emerging markets | Short term (≤2 years) |

| Vendor Lock-In Risks Reducing Consulting Flexibility | −0.4% | North America and Europe, emerging in APAC | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified ERP Consultants

Demand for SAP S/4HANA, Oracle Fusion Cloud, and Microsoft Dynamics 365 skills exceeds supply, elevating salaries and stretching project timelines. SAP recorded a 30% deficit in certified S/4HANA consultants during 2024. Offshore training pipelines in India aim to certify 15,000 specialists annually, yet attrition of 20-25% shifts talent to hyperscaler cloud divisions. Latin America and Africa rely on fly-in talent, which increases project costs by up to 40%. Low-code accelerators reduce configuration effort, but smaller boutiques cannot fund proprietary IP at scale.

Rising Cybersecurity Concerns Delaying Projects

High-profile ransomware attacks targeting ERP platforms have forced enterprises to pause deployments until zero-trust architectures and encryption baselines are validated. A 2024 breach in Europe paused a multi-tenant SAP cloud migration for four months pending forensic audits. Healthcare providers, facing HIPAA fines of up to USD 1.5 million per incident, now mandate penetration testing before go-live, which can extend schedules by up to 6 weeks. EU and Chinese residency rules oblige multiple regional instances, doubling infrastructure spend IBM.COM. Supply-chain attacks embedded in vendor updates have triggered blackout periods during critical retail seasons, narrowing annual upgrade windows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Dominance Reshapes Consulting Economics

Cloud solutions accounted for 58% of the ERP consulting services market in 2025, and the segment is projected to grow at a 12.40% CAGR through 2031. This growth surpasses the overall ERP consulting services market by four percentage points, reflecting a decisive shift away from capital-intensive data centers. Hyperscalers expand their influence by packaging infrastructure, migration, and 1-year managed support into a single invoice, challenging independent advisors on price and accountability. Hybrid models persist among defense contractors subject to ITAR and among pharmaceutical plants, where validated manufacturing execution systems must remain on-premises.

Recurring optimization work streams emerge because quarterly SaaS releases demand regression testing, change management, and feature enablement. Consultants now sell evergreen DevOps-style subscriptions rather than project-based roadmaps, thereby subtly raising lifetime client value. On-premises estates, though contracting, still generate advisory revenue from API layer insertion and phased module retirement as firms pursue gradual de-customization. Hybrid footprints, forecast at a mid-single-digit CAGR, create niche demand for secure integration architectures that span private and public clouds while satisfying sovereignty audits.

By Enterprise Size: SME Acceleration Offsets Large-Enterprise Saturation

Large enterprises contributed 61% of 2025 revenue, yet their incremental growth is slowing as most have completed initial digital core migrations. Engagements now pivot toward continuous improvement, process mining, and AI-enabled predictive modules that optimize existing footprints.

SMEs, however, register a vibrant 12.70% CAGR through 2031, propelled by SaaS affordability and template-based quick starts. These clients value rapid time to benefit over deep customization, trimming average ticket sizes to USD 0.3–0.5 million but driving higher deal velocity. Workday, Oracle NetSuite, and Microsoft Business Central gain traction among firms with fewer than 1,000 employees, supported by marketplace extensions and low-code workflow builders. Consulting partners differentiate via localized compliance content, for instance, Brazilian e-invoicing schemas or Indian GST returns, anchoring regional boutiques in the ERP consulting services market. Rising SME participation diversifies revenue streams and cushions integrators against the cyclicality of mega-transformations in the Fortune 500.

By End User Industry: Healthcare Velocity Contrasts With Manufacturing Maturity

Manufacturing retained a 24% share in 2025, on the back of entrenched material requirements planning and shop-floor integration use cases. Growth moderates as penetration nears saturation in developed economies, redirecting consulting focus to Industry 4.0 analytics and digital twin pilots. Healthcare grows fastest at a 11.80% CAGR, expanding its share of the ERP consulting services market to an estimated USD 4 billion by 2031. Hospitals seek unified finance, supply chain, and HR data to manage value-based care reimbursement, driving demand for HIPAA-compliant cloud deployments and sterile supply chain optimization algorithms.

BFSI institutions decompose core systems into composable layers to accelerate product release cadences and satisfy Basel IV reporting within microservices-based ledgers. Retail and e-commerce organizations integrate point-of-sale, inventory, and order management inside a single ERP tenant to stem omnichannel margin leakage, with agentic AI bots automating invoice matching and goods receipt. Public-sector spending, fueled by tax-digitization mandates in India and GCC diversification plans, supports seven-year transformation projects that stabilize consultant backlogs. Energy and utilities, driven by 5G rollout and decarbonization targets, are integrating asset management with predictive analytics to reduce outage risk.

Geography Analysis

North America generated 38% of 2025 revenue, underpinned by stringent regulatory frameworks in pharmaceuticals, defense, and finance that necessitate specialized controls consulting. Fortune 500 mergers spur harmonization projects, while the United States near-shoring to Mexico elevates cross-border compliance work on USMCA origins. Canada attracts hyperscaler investment, exemplified by Workday’s CAD 1 billion (USD 770 million) expansion to service midsize manufacturers.[2]Financial Post Staff, “Workday to Invest CAD 1 Billion in Canada to Expand AI and Cloud Capabilities,” financialpost.com The ERP consulting services market continues to shift toward outcome-based deals as North American clients prioritize value realization over staff-augmentation hours.

Asia-Pacific is the fastest-growing region, with a 11.90% CAGR, capturing cloud migration contracts across India, China, Japan, and the ASEAN markets. SAP disclosed that 60% of its Q4 2024 APAC wins involved SMEs upgrading via RISE bundles.[3]SAP SE, “SAP Announces Strong Cloud Growth in APAC,” news.sap.com India’s production-linked incentives in electronics and pharmaceuticals accelerate traceability and quality audit adoption, while Chinese manufacturers adopt domestic Kingdee and Yonyou platforms to satisfy dual-circulation directives, creating parallel integration workloads. Japan’s aging workforce drives RPA integration with ERP systems to offset labor constraints, pushing consultancies to adopt bot-governance frameworks.

Europe experiences moderate growth as GDPR residency rules force multi-tenant cloud providers to spin up localized zones, complicating cross-border rollouts and inflating project scoping cycles. Germany, the United Kingdom, and France drive spending through Industry 4.0 investments tying ERP to IoT sensor data, while Southern Europe accelerates due to EU subsidy programs and Accenture’s acquisition of Fibermind in Portugal. Middle East sovereign-wealth funds bankroll government modernizations that digitalize procurement and tax while adhering to Islamic finance structures, attracting long-duration consulting engagements. Africa and South America remain emerging opportunities, though Brazil’s manufacturing and mining revamp, aided by Accenture’s Cientra purchase, signals an uptick in Latin American deal flow.

Competitive Landscape

The ERP consulting services market is moderately fragmented; the top ten firms, Accenture, Deloitte, IBM, Capgemini, TCS, Infosys, Wipro, Cognizant, HCLTech, and PwC, control a significant share of global revenue. Competitive focus has pivoted from billable hours to performance-based outcomes, compelling integrators to embed analytics squads post-go-live for real-time KPI tracking. Indian service providers leverage offshore delivery to undercut Western peers, though fixed-price guarantees compress margins as penalty clauses proliferate.

Hyperscalers deepen their influence by coupling infrastructure with ERP migration blueprints; Google Cloud, with HCLTech, and Microsoft, with IBM, integrate infrastructure provisioning, application refactoring, and twelve-month support windows into a single commercial construct. Boutique consultancies punch above their weight in healthcare, public sector, and cybersecurity, where local regulation knowledge trumps scale. AI-driven process mining is emerging as a high-margin niche, with consultants interpreting ERP event logs to redesign workflows and deliver quick ROI.

Mergers and acquisitions are intensifying as firms buy regional talent pools to counter certification shortages; Accenture’s 2025 acquisitions of Cientra in Brazil and Fibermind in Portugal exemplify this strategy. [4]Accenture plc, “Accenture Completes Acquisition of Cientra,” accenture.com Vendor alliances expand, with SAP, Oracle, and Microsoft subsidizing partner enablement and co-marketing. Certification hierarchies create a two-tier market where preferred partners secure pipeline advantage, leaving smaller unsponsored firms to specialize in vertical micro-solutions. Rising specialization solidifies moderate entry barriers but leaves space for niche innovators focused on governance, risk, and AI augmentation of cloud ERPs.

Enterprise Resource Planning Consulting Industry Leaders

Accenture plc

Deloitte Touche Tohmatsu Limited

International Business Machines Corporation

Capgemini SE

Infosys Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Tata Consultancy Services and SAP unveiled a USD 1 billion alliance to deliver AI-enabled transformations with penalty-backed KPI commitments.

- January 2025: Wipro won a multi-year mandate to roll out SAP S/4HANA Cloud at AusNet Services, supporting Australia’s transition to renewable energy grids.

- January 2025: Cognizant completed SAP S/4HANA Cloud deployment for Kramp Group, slashing order-processing time by 35%.

- January 2025: PwC expanded its SAP partnership, pledging to certify 5,000 consultants on Business Technology Platform.

Global Enterprise Resource Planning Consulting Market Report Scope

The ERP Consulting Services market comprises the ecosystem of advisory and professional services that support organizations in strategic planning, selection, design, and optimization of Enterprise Resource Planning (ERP) systems.

The ERP Consulting Services Market Report is Segmented by Deployment Mode (On-Premise, Cloud, Hybrid), Enterprise Size (Small and Medium Enterprises, Large Enterprises), End User Industry (Manufacturing, BFSI, Retail and E-Commerce, Healthcare, Government and Public Sector, IT and Telecom, Energy and Utilities, Other End User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| On-Premise |

| Cloud |

| Hybrid |

| Small and Medium Enterprises |

| Large Enterprises |

| Manufacturing |

| BFSI |

| Retail and E-Commerce |

| Healthcare |

| Government and Public Sector |

| IT and Telecom |

| Energy and Utilities |

| Other End User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Deployment Mode | On-Premise | |

| Cloud | ||

| Hybrid | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End User Industry | Manufacturing | |

| BFSI | ||

| Retail and E-Commerce | ||

| Healthcare | ||

| Government and Public Sector | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Other End User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the ERP Consulting market by 2031?

The market is forecast to reach USD 23.42 billion by 2031 growing at a CAGR of 8.35% during 2026-2031..

Which deployment model accounts for most new ERP projects?

Cloud leads, holding 58% share in 2025 and rising at 12.40% CAGR.

Why are SMEs adopting ERP now?

Subscription pricing and pre-configured templates cut upfront costs and shrink go-live timelines to under six months.

What is driving the shift to outcome-based contracts?

Clients want consultants to share risk, so fees are tied to KPIs like order-to-cash cycle reduction.

Which vertical shows the fastest consulting demand?

Healthcare, expanding at 11.80% CAGR as hospitals integrate finance, supply-chain, and HR data for value-based care models.

What is the biggest obstacle to ERP project timelines?

A global shortage of certified ERP consultants, which extends schedules and inflates labor costs.

Page last updated on: