Supply Chain Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

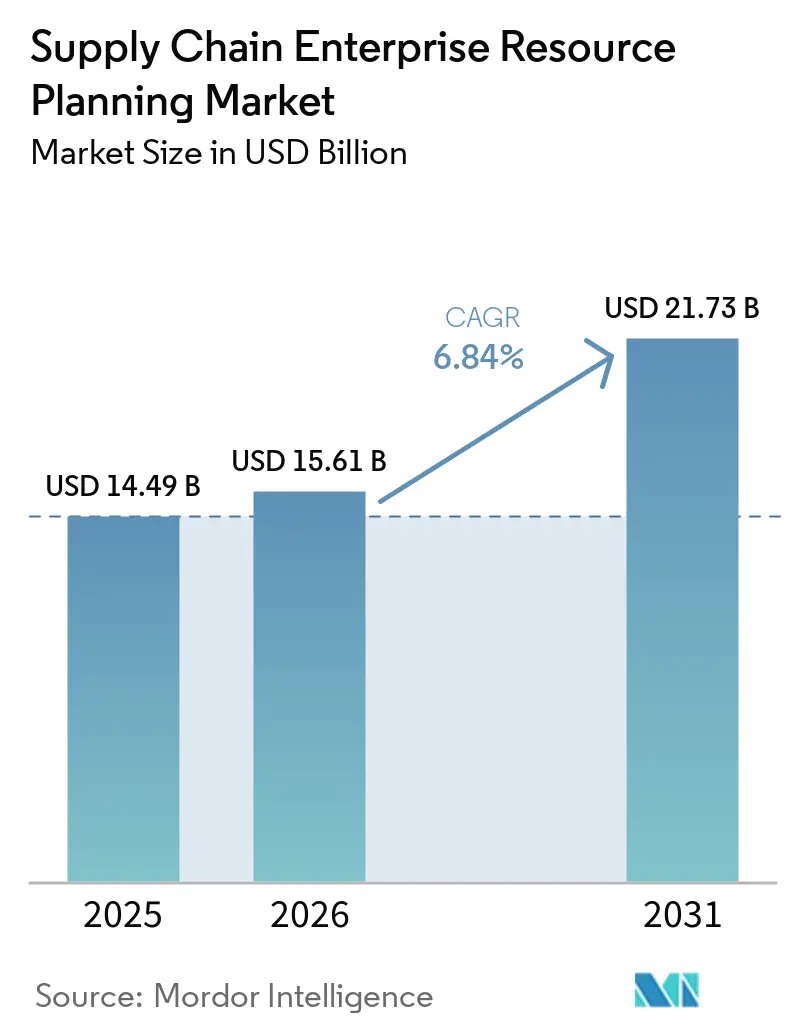

| Market Size (2026) | USD 15.61 Billion |

| Market Size (2031) | USD 21.73 Billion |

| Growth Rate (2026 - 2031) | 6.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

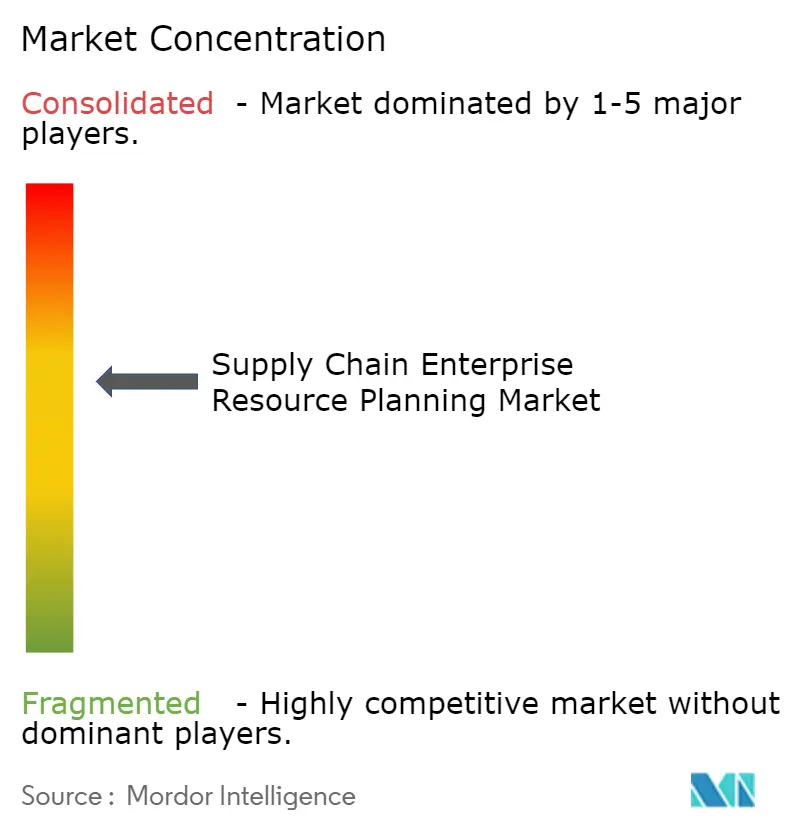

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Supply Chain Enterprise Resource Planning Market Analysis by Mordor Intelligence

The supply chain enterprise resource planning market size was valued at USD 14.49 billion in 2025 and estimated to grow from USD 15.61 billion in 2026 to reach USD 21.73 billion by 2031, at a CAGR of 6.84% during the forecast period (2026-2031). Structural replacement of fragmented legacy tools with unified, cloud-native suites is the fundamental engine of growth. Vendors now anchor roadmaps around real-time visibility, elastic compute, and artificial-intelligence-driven automation that shorten decision cycles in procurement, inventory, logistics, and order orchestration. Scope-3 carbon-tracking rules, data-residency mandates, and near-shoring programs are reshaping platform selection criteria, pushing buyers toward solutions that ingest supplier emissions data and satisfy region-specific sovereignty laws. Generative-AI copilots already draft purchase orders, reconcile invoices, and recommend shipment reroutes, compressing tasks that used to consume entire work shifts. Competitive dynamics remain intense as hyperscalers embed ERP inside broader analytic and AI stacks, while specialized challengers exploit industry niches with composable, sensor-rich modules.

Key Report Takeaways

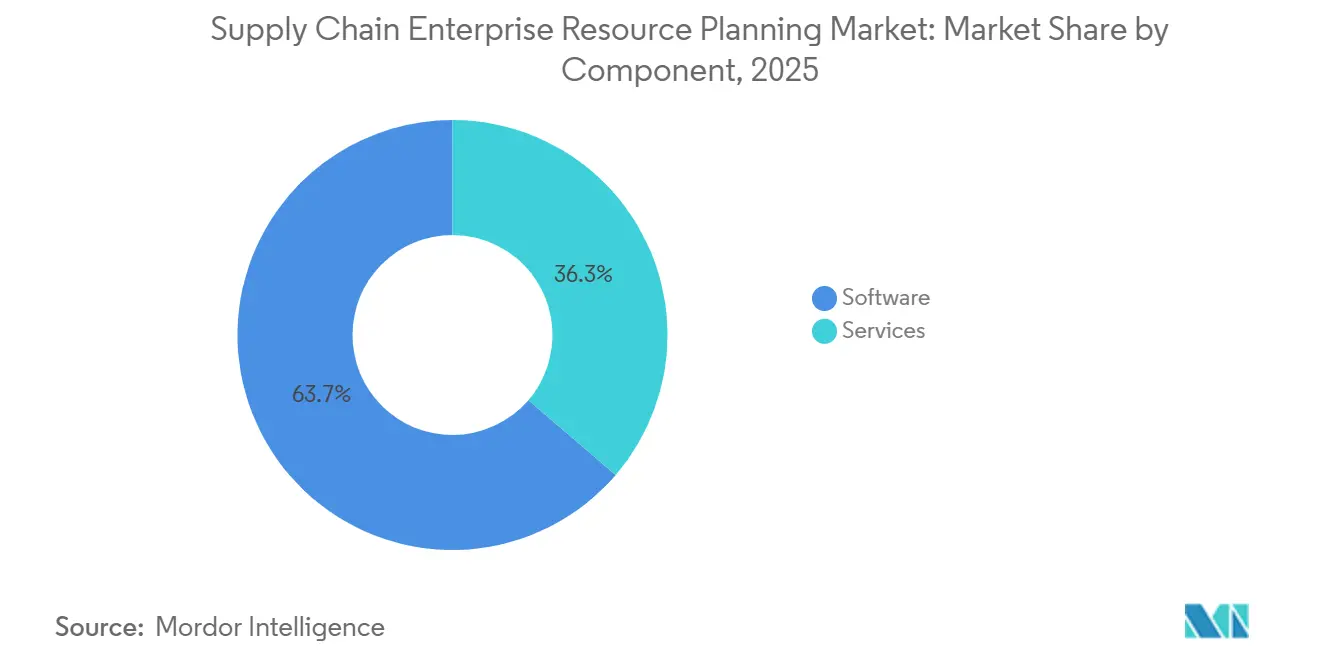

- By component, software led with 63.71% revenue share in 2025, whereas the services segment is advancing at a 7.24% CAGR to 2031.

- By deployment mode, the cloud-based segment accounted for 58.83% of the supply chain enterprise resource planning market in 2025 and recorded the fastest growth at 7.44% through 2031.

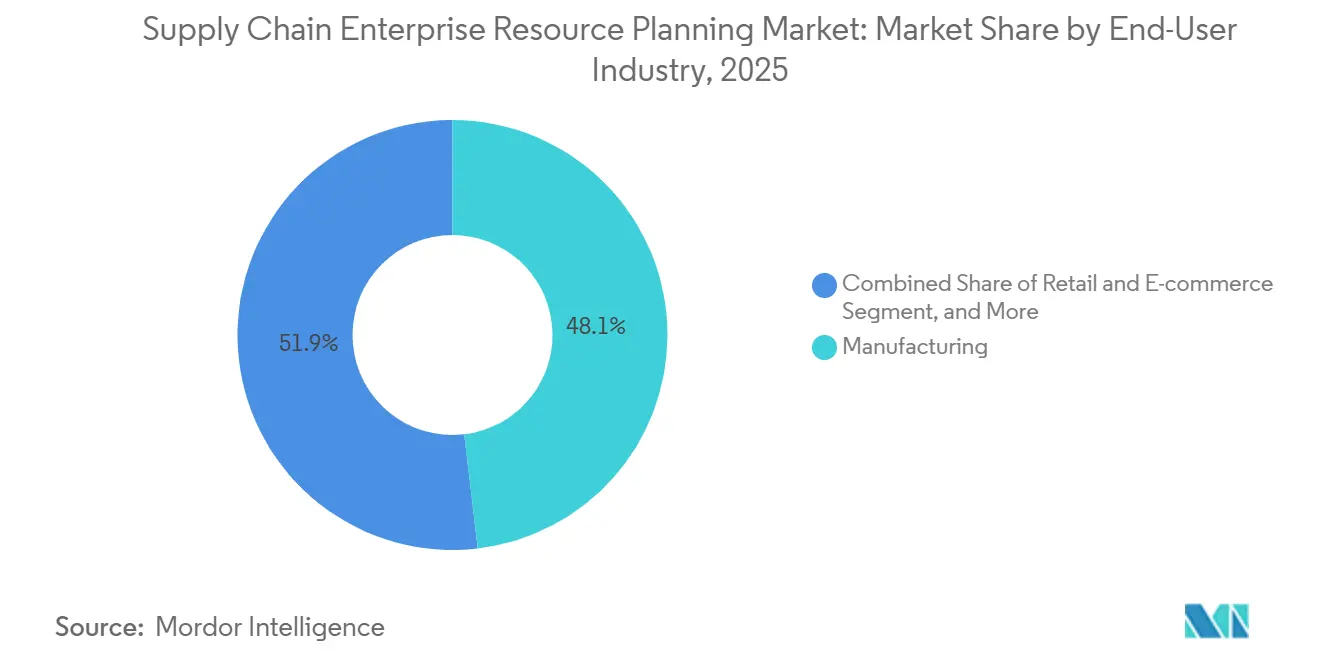

- By end-user industry, manufacturing accounted for 48.12% of 2025 spending, while retail and e-commerce are projected to grow at a 7.82% CAGR through 2031.

- By organization size, large enterprises accounted for 68.67% of 2025 revenue; small and medium enterprises are expanding at a 7.38% CAGR through 2031 in the supply chain ERP market.

- By geography, North America dominated with a 36.18% share in 2025, yet Asia-Pacific posts the highest regional CAGR at 7.84% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Supply Chain Enterprise Resource Planning Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-First Migration of Tier-1 ERP Suites | +1.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| AI-Enabled Predictive Supply Chain Planning | +1.5% | North America, Europe, Asia-Pacific (China, Japan, India) | Short term (≤ 2 years) |

| Rise of Composable and Modular Architectures | +1.2% | Global, with early traction in North America and Western Europe | Long term (≥ 4 years) |

| Near-Shoring and Resilience Programs | +1.0% | North America and Europe plus Mexico, Central Europe, Southeast Asia | Medium term (2-4 years) |

| Sustainability and Scope-3 Mandates | +0.9% | Europe, North America, expanding into Asia-Pacific | Long term (≥ 4 years) |

| Generative-AI Agents in Procure-to-Pay | +0.7% | Early adopters in North America, Europe, and Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cloud-First Migration of Tier-1 ERP Suites

Tier-1 vendors target aggressive cloud-adoption milestones, promising continuous feature delivery, elastic simulation capacity, and easier integration with third-party logistics. Migrations typically lower the five-year total cost of ownership by a moderate share, yet hidden data cleansing and process re-engineering work often extends project timelines. Vendors bundle automated migration toolkits and fixed-price packages to reduce friction, while customers increasingly insist on outcome-based contracts tied to go-live milestones. Additionally, the shift to cloud-based solutions is driving innovation in service delivery models. The supply chain ERP market vendors are leveraging artificial intelligence and machine learning to enhance predictive analytics, enabling businesses to make data-driven decisions more effectively. This trend is particularly evident in industries like manufacturing and retail, where real-time insights are critical for optimizing operations. As a result, companies are increasingly viewing cloud adoption not just as a cost-saving measure but as a strategic investment to gain a competitive edge.

AI-Enabled Predictive Supply Chain Planning

Machine-learning algorithms now ingest unstructured weather feeds, supplier emails, and social sentiment to fine-tune demand forecasts and proactively reroute shipments. Embedded copilots reduce manual data entry by up to a moderate share and enable enterprises to maintain leaner safety stock without eroding service levels. Reliability still hinges on harmonized historical data, giving an additional push toward unified, cloud-native environments. As a result, businesses are increasingly prioritizing investments in advanced analytics to enhance operational efficiency and decision-making.[1]Microsoft Corporation, “Dynamics 365 Copilot Capabilities,” microsoft.com

Rise of Composable and Modular Architectures

Decoupled microservices let enterprises plug in best-of-breed quality, transportation, or advanced-planning engines without overhauling the transactional core. Early adopters cite faster rollout of new functionality, though governance becomes more complex once business logic spans multiple vendors. API-first philosophies are therefore matched with stricter data-ownership rules and centralized event hubs, ensuring seamless integration and enhanced operational efficiency.[2]IFS AB, “Composable ERP and Microservices Architecture,” ifs.com

Near-Shoring and Resilience Programs

Investment incentives such as the U.S. CHIPS Act and European clean-energy credits catalyze factory relocation closer to end markets. New plants need ERP suites that map multi-echelon inventory, model tariff scenarios, and track country-of-origin attributes. Vendors now embed control-tower dashboards directly in core ERP to eliminate bolt-on visibility tools. These dashboards provide real-time insights, enabling quicker decision-making and improved operational efficiency. Additionally, they help businesses adapt to dynamic regulatory requirements and supply chain disruptions with greater agility.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-Security and Data-Sovereignty Costs | -0.8% | Europe, Asia-Pacific, North America | Medium term (2-4 years) |

| Shortage of ERP-Skilled Talent | -0.7% | Global, acute in North America and Western Europe | Short term (≤ 2 years) |

| Vendor Lock-In Concerns | -0.5% | Global, mid-market enterprises most affected | Long term (≥ 4 years) |

| Integration Complexity with Legacy Systems | -0.4% | Mature markets with large installed base | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security and Data-Sovereignty Compliance Costs

Jurisdictions such as the EU, China, and India demand in-country data storage and impose stiff penalties for violations. Multinationals, therefore, maintain region-specific ERP instances, thereby increasing infrastructure costs and complicating master data synchronization. Zero-trust security, multi-factor authentication, and anomaly detection add 10-15% to annual subscription fees, a burden felt most acutely by mid-market firms. Additionally, compliance with these regulations often requires significant investment in IT infrastructure upgrades to meet local standards. This trend, in the supply chain ERP market, is driving demand for specialized consulting services to navigate the complexities of regional compliance requirements.

Shortage of ERP-Skilled Supply-Chain Talent

Cloud migrations outpace the availability of consultants trained on modern architectures. Project lead times stretch beyond six months in several geographies, and daily rates for senior architects often cross USD 2,000. Enterprises respond with in-house academies and offshore centers, while vendors ship low-code tooling and templated configurations to shrink reliance on scarce specialists. Additionally, organizations are increasingly leveraging AI-driven tools to automate repetitive migration tasks, thereby reducing their reliance on human expertise. This shift not only accelerates project timelines but also helps mitigate rising costs associated with skilled labor shortages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Scale Faster Than Software

The services slice of the supply chain enterprise resource planning market is expanding at a 7.24% CAGR, eclipsing software growth as projects require intensive data cleansing, integration, and change management. Implementation and managed-service contracts increasingly hinge on performance outcomes such as order-to-cash cycle days. Software still generated 63.71% of value in 2025, buoyed by subscription revenue from tier-1 suites and algorithmic planning add-ons that underpin modern supply networks. Continuous-improvement retainers now keep consultants embedded long after go-live, turning services into an annuity stream. Meanwhile, software providers blur category lines by bundling basic support and hosting, prompting buyers to evaluate true cost across both line items. Open-source challengers leverage all-inclusive pricing to cut total ownership costs and woo small and medium enterprises.

As the market evolves, enterprises increasingly prioritize agility and scalability in their ERP solutions to adapt to dynamic supply chain demands. Vendors are responding by integrating advanced analytics and AI-driven insights to enhance decision-making capabilities. Additionally, the shift toward modular ERP systems allows businesses to adopt functionalities incrementally, reducing upfront costs and implementation risks. This trend is particularly appealing to mid-market firms, which often face budget constraints but require robust solutions to remain competitive. The growing emphasis on sustainability and compliance further drives innovation, with ERP providers embedding features to track carbon footprints and ensure regulatory adherence.

By Deployment Mode: Cloud-Based Momentum Intensifies

Cloud installations accounted for 58.83% of 2025 revenue and are accelerating by 7.44% through 2031, propelled by hyperscaler discounts and elastic capacity for simulation workloads. Hybrid structures persist in defense, utilities, and public-sector contexts where sensitive ledgers remain on-premise while collaboration modules live in the cloud. On-premise adoption is declining, but endures where air-gapped security trumps scalability. Edge-caching appliances and regional data centers mitigate latency and residency hurdles, broadening cloud appeal in bandwidth-constrained territories. Subscription models also distribute cash outlays more evenly, an advantage for manufacturers juggling capital budgets. As a result, cloud footprints are expected to exceed 70% of new deployments well before the forecast horizon, further reshaping vendor economics.

Additionally, the integration of advanced technologies such as artificial intelligence (AI) and machine learning (ML) into cloud-based ERP systems is driving operational efficiencies across industries. These technologies enable real-time data analysis, predictive insights, and automated decision-making, which are critical for businesses aiming to stay competitive in dynamic markets. Furthermore, the growing emphasis on sustainability is pushing organizations to adopt cloud solutions that optimize energy consumption and reduce carbon footprints. Vendors are increasingly offering green cloud services, aligning with corporate environmental, social, and governance (ESG) goals, which is expected to further accelerate cloud adoption during the forecast period.

By End-User Industry: Retail and E-Commerce Lead Growth Arc

Manufacturing held 48.12% of the supply chain enterprise resource planning market share in 2025, reflecting its intricate bill-of-materials and equipment-telemetry demands. Retail and e-commerce, however, are scaling at a 7.82% CAGR to 2031 on the back of omnichannel fulfillment and last-mile delivery orchestration. Healthcare, food and beverage, and consumer goods form a diverse mid-tier, each introducing compliance-driven features such as serialization, lot traceability, and trade promotion analytics. In retail, unified inventory ledgers enable buy online, pick up in store models, while AI-powered pricing engines dynamically adjust markdowns. Manufacturers deepen plant connectivity through sensors that feed predictive-maintenance algorithms, reducing unplanned downtime and aligning production with demand signals.

Additionally, the adoption of cloud-based ERP solutions is accelerating across industries due to their scalability and cost-effectiveness. These solutions enable businesses to access real-time data, improving decision-making and operational efficiency. The integration of advanced technologies, such as artificial intelligence and machine learning, is further enhancing ERP functionalities, offering predictive analytics and automation capabilities. As a result, companies are increasingly leveraging these systems to streamline their supply chains, improve customer satisfaction, and gain a competitive edge in the market.

By Organization Size: Templates Democratize Adoption

Large organizations accounted for 68.67% of 2025 revenue, often deploying hundreds of legal entities that require multi-currency, multi-tax, and multi-language capabilities. These enterprises integrate advanced planning and scheduling modules that model global constraints, driving premium license tiers. The small and medium segment is growing at a 7.38% CAGR as vendors roll out vertical templates that cut implementation from a year to a single fiscal quarter. Low-code configurators enable internal power users to build workflows, lessening dependence on external integrators. Subscription pricing with tiered module activation further lowers barriers, allowing SMEs to start lean and scale functionality as complexity rises.

The increasing adoption of cloud-based solutions is also driving innovation in deployment strategies, particularly for SMEs. Vendors are focusing on offering modular solutions that cater to specific industry needs, enabling businesses to adopt tailored functionalities without overhauling their existing systems. Additionally, integrating artificial intelligence (AI) and machine learning (ML) into these solutions enhances predictive analytics and decision-making capabilities, providing organizations with a competitive edge. As a result, both large enterprises and SMEs are leveraging these advancements to optimize operations and improve overall efficiency, further fueling market growth.

Geography Analysis

North America remains the single largest regional contributor, with a 36.18% share in 2025, anchored by the United States' drive toward AI-augmented planning and nearshore manufacturing. Canadian producers adopt ERP systems to meet export rules-of-origin documentation requirements, while Mexican maquiladoras upgrade systems to manage dual-sourcing models spanning domestic and U.S. suppliers. Widespread 5G connectivity and hyperscaler data-center density enable real-time control-tower dashboards, shrinking response times to supply disruptions.

Asia-Pacific posts the most dynamic growth trajectory with a CAGR of 7.84% over the forecast period. India’s compliance-ready templates automate goods and services tax reporting, encouraging even mid-market firms to migrate away from spreadsheets. Japanese conglomerates are phasing out on-premises systems as domestic cloud vendors guarantee low-latency availability zones. In China, state-led substitution campaigns steer enterprises toward locally maintained ERP copies that pass stringent cybersecurity reviews, without sacrificing integration with global supply networks.

Europe balances regulatory compliance with sustainability leadership. The ViDA e-invoicing roll-out enables borderless data exchange across the region, while the Digital Product Passport requires manufacturers to trace their carbon footprint from raw extraction through end-of-life recycling. German automotive suppliers pilot blockchain-backed certificates of origin built directly into ERP line items. Nordic retailers incorporate circular-economy returns data, enabling refurbish and resale programs. Eastern European plants leverage EU cohesion funds to digitalize factories, adding incremental demand for modular suites. South America, the Middle East, and Africa are smaller markets but are steadily growing as governments invest in digital infrastructure and local enterprises aim to compete with multinational subsidiaries. Brazil's ERP adoption surpassed 33% in 2025, with further growth expected as the government digitizes tax compliance processes.[3]Brazilian Ministry of Economy, “Digital Economy Initiatives,” gov.br

Competitive Landscape

Global competition is moderately concentrated. SAP, Oracle, and Microsoft collectively capture roughly 45% of annual revenue, providing wide functional breadth and hyperscaler adjacency that raise switching costs. They entrench positions by packaging data lakes, AI model hosting, and integration hubs inside enterprise deals, often discounted when clients commit to multi-year consumption minima. Patent filings reveal an uptick in AI-enabled predictive planning and blockchain-based traceability, underscoring ongoing innovation races.

Mid-tier players such as Infor, Epicor, and IFS exploit asset-heavy niches. By welding sensor telemetry and maintenance analytics into procurement and production modules, they solve industry-specific pain points that broad suites address only superficially. Geographic expansion through new data centers in Singapore, Sydney, and São Paulo pairs low latency with data-residency compliance, heightening regional appeal. This strategy enables these players to cater to localized regulatory requirements while maintaining competitive service levels.

Disruptors, including Odoo and Acumatica, target cost-sensitive SMEs with open-core or all-inclusive tariff models. Low-code orchestrators let customers tailor workflows without great technical skills, while community marketplaces speed extension development. Strategic alignments with hyperscalers, chipmakers, and analytics vendors add momentum, yet all vendors face an implementation-capacity bottleneck sparked by scarce cloud-ERP talent. AI-assisted configurators and pre-templatized industry packets are interim relief but do not fully remove the need for domain expertise. Patent filings in the ERP space have surged, with SAP and Oracle submitting over 200 patents on AI-enabled supply chain planning and blockchain-based traceability.[4]United States Patent and Trademark Office, “Patent Application Full-Text,” uspto.gov

Supply Chain Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Infor, Inc.

Blue Yonder Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SAP and NVIDIA launched a partnership to embed large-language-model demand sensing into S/4HANA Cloud, targeting a 20-30% reduction in forecast error.

- January 2026: Oracle finalized the USD 1.2 billion purchase of Cerner’s supply-chain assets, adding medical-device traceability to Fusion Cloud ERP.

- December 2025: Infor invested USD 150 million to deploy new CloudSuite Industrial data centers in Singapore and Sydney for low-latency, compliant hosting.

- November 2025: IFS acquired Ultimo Software for USD 320 million to integrate enterprise asset management workflows into its ERP core.

Global Supply Chain Enterprise Resource Planning Market Report Scope

The supply chain ERP market solutions manage and optimize supply chain operations across organizations. These ERP systems integrate core supply chain functions such as procurement, inventory management, logistics, demand planning, order management, and supplier coordination within a unified platform. By centralizing supply chain data and processes, these solutions enable businesses to improve operational efficiency, enhance visibility across the supply network, reduce costs, and support better decision-making.

The Supply Chain Enterprise Resource Planning Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), End-User Industry (Manufacturing, Retail and E-commerce, Healthcare and Pharmaceuticals, Food and Beverage, and Consumer Goods), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Manufacturing |

| Retail and E-commerce |

| Healthcare and Pharmaceuticals |

| Food and Beverage |

| Consumer Goods |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | Cloud-Based | ||

| On-Premise | |||

| Hybrid | |||

| By End-User Industry | Manufacturing | ||

| Retail and E-commerce | |||

| Healthcare and Pharmaceuticals | |||

| Food and Beverage | |||

| Consumer Goods | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the supply chain enterprise resource planning market expected to grow to 2031?

It is forecast to advance at a 6.84% CAGR, reaching USD 21.73 billion by 2031.

Which deployment mode is expanding most quickly?

Cloud-based installations are growing at 7.44% through 2031, outpacing hybrid and on-premise options.

Why are retail and e-commerce companies adopting supply-chain ERP platforms rapidly?

Omnichannel fulfillment requires synchronized inventory across stores, dark stores, and third-party logistics, driving a 7.82% CAGR in the segment.

What is the biggest restraint on wider ERP adoption?

The global shortage of consultants skilled in modern cloud-ERP architectures is delaying projects and inflating implementation costs.

Which region shows the highest growth momentum?

Asia-Pacific holds the fastest trajectory at 7.84% CAGR, powered by tax-aligned templates in India, rapid cloud uptake in Japan, and domestic software substitution in China.

How concentrated is the vendor landscape?

Moderately concentrated, with SAP, Oracle, and Microsoft capturing about 45% of revenue, yielding a concentration score of 6.

Page last updated on: