Manufacturing Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.36 Billion |

| Market Size (2031) | USD 10.17 Billion |

| Growth Rate (2026 - 2031) | 9.84% CAGR |

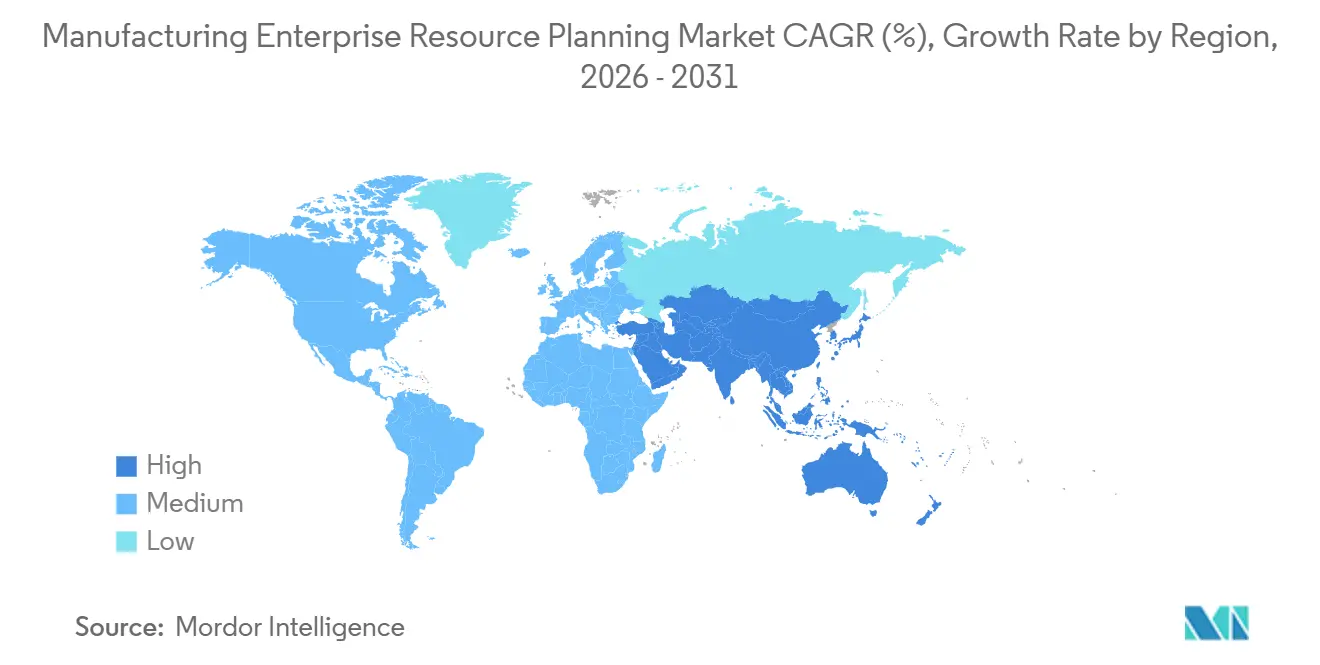

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Manufacturing Enterprise Resource Planning Market Analysis by Mordor Intelligence

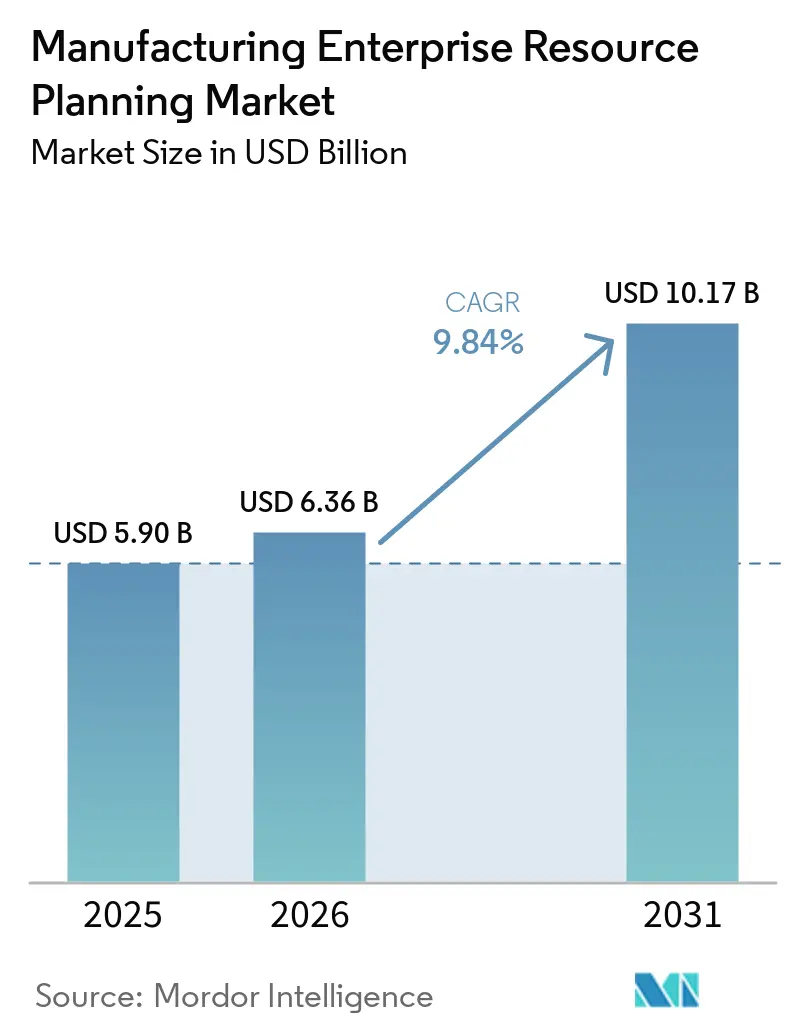

The manufacturing ERP market size is projected to expand from USD 5.90 billion in 2025 and USD 6.36 billion in 2026 to USD 10.17 billion by 2031, registering a CAGR of 9.84% between 2026 and 2031. Growing demand for integrated intelligence that merges IIoT telemetry, predictive analytics, and real-time supply-chain orchestration is steering adoption across discrete and process plants alike. Cloud deployments dominate current spending, yet hybrid architectures are scaling quickly as sovereignty rules in the European Union, and China pushes sensitive data back on-premise. Vertical SaaS suites are lowering entry barriers for small- and medium-sized manufacturers, while regulatory pressure for traceability and ESG disclosure is making ERP modernization a board-level compliance priority. Competitive intensity remains moderate, with the top five vendors controlling a significant percent of revenue, leaving substantial headroom for industry-specific challengers.

Key Report Takeaways

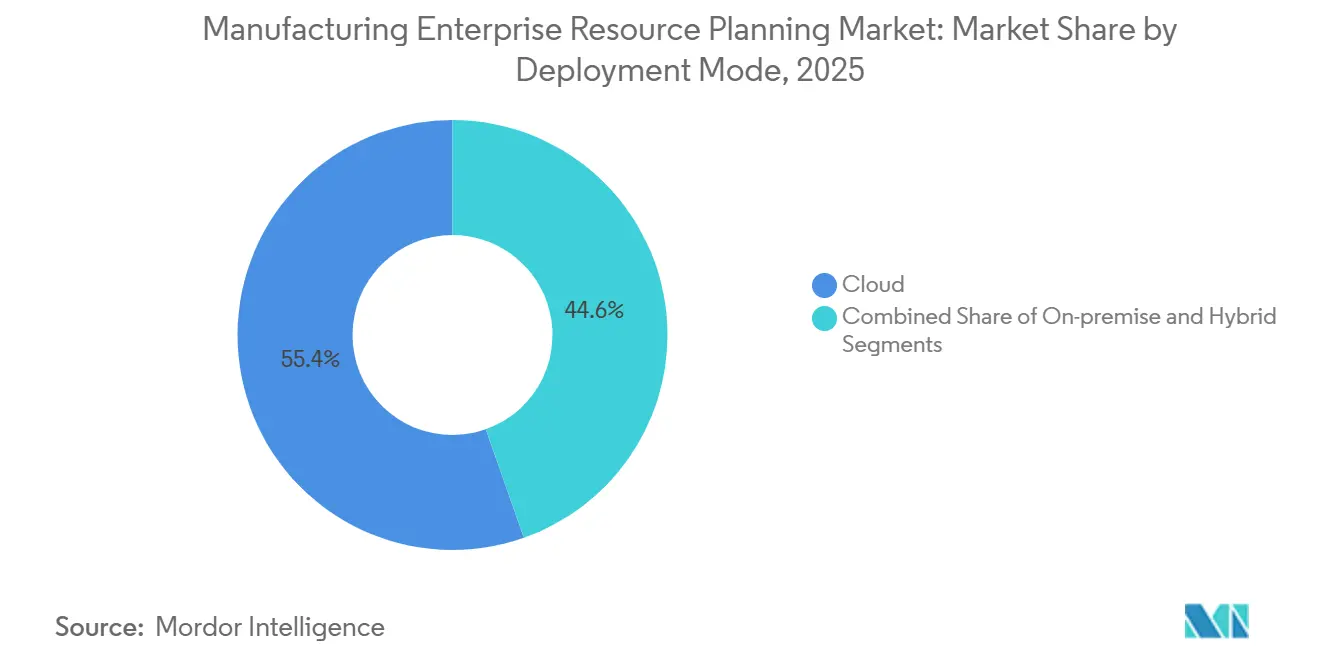

- By deployment model, cloud held 55.40% of spending in 2025, while hybrid is forecast to record an 18.00% CAGR through 2031.

- By organization size, large enterprises accounted for 58.30% of 2025 revenue, yet SMEs are expected to grow at a 17.00% CAGR over 2026-2031.

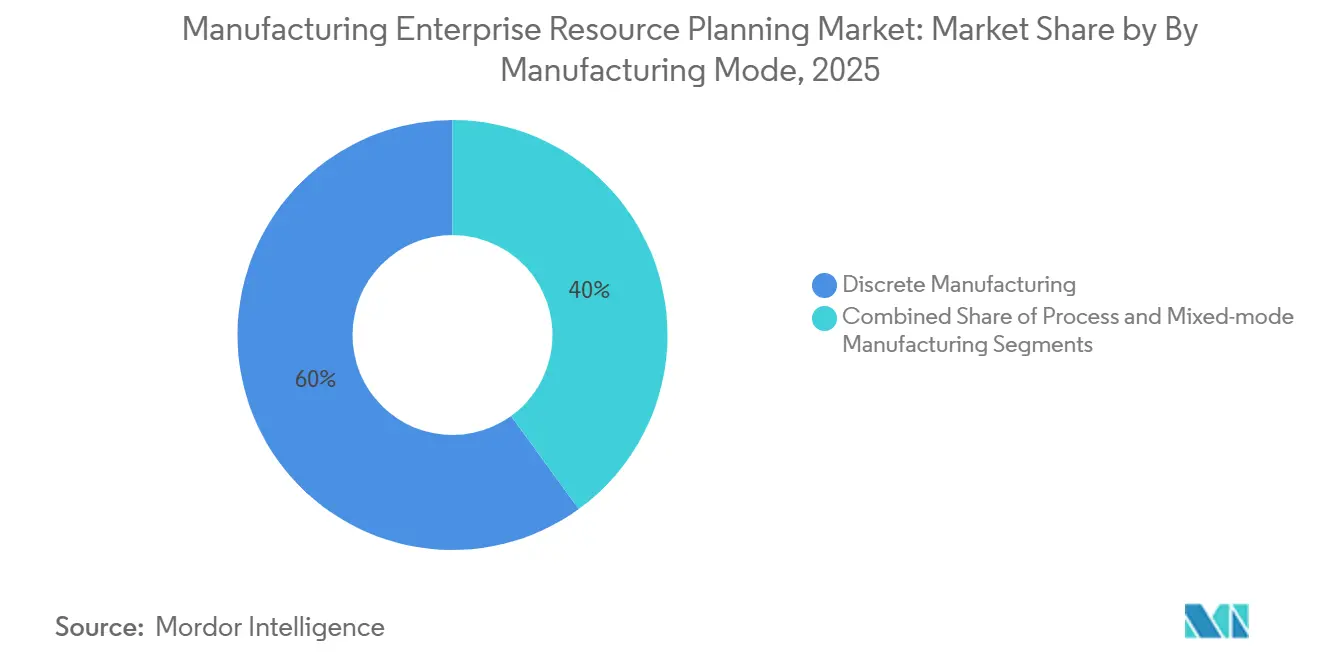

- By manufacturing mode, discrete operations accounted for 60.00% of implementations in 2025, whereas mixed-mode platforms are projected to grow at an 11.50% CAGR to 2031.

- By end-industry vertical, automotive led with 25.00% of spending in 2025, but electronics and high-tech are poised for the fastest expansion, with a 10.70% CAGR through 2031.

- By geography, North America accounted for 38.60% of 2025 revenue; Asia-Pacific is the fastest-growing region, with an 8.80% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Manufacturing Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-First Digital Transformation Initiatives in Manufacturing | +2.8% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Integration of IIoT and Real-Time Analytics with ERP Platforms | +2.3% | Global, APAC core with spill-over to Middle East and Africa | Medium term (2-4 years) |

| Regulatory Pressure for Traceability and Compliance Across Global Supply Chains | +1.9% | North America, Europe, Asia-Pacific pharmaceutical and food hubs | Long term (≥ 4 years) |

| Shift Toward AI-Enabled Predictive Maintenance and Quality Management | +1.6% | Global, concentrated in automotive and aerospace verticals | Medium term (2-4 years) |

| Proliferation of Industry-Specific SaaS ERP Offerings for SMB Manufacturers | +1.4% | Global, particularly strong in North America and Europe SMB clusters | Short term (≤ 2 years) |

| Sustainability Reporting Mandates Driving ERP Adoption for ESG Data | +1.2% | Europe (CSRD), North America (SEC climate rules), expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Digital Transformation Initiatives in Manufacturing

Manufacturers are relocating transactional workloads to public-cloud infrastructure at scale, lifting cloud adoption to 55.40% market share in 2025. Subscription pricing eliminates upfront license fees for mid-tier firms, and elastic compute lets globally distributed design and procurement teams collaborate in real time, a capability that helped electronics suppliers reroute constrained semiconductors within hours during the 2025 shortage. United States subsidy programs under the CHIPS and Science Act require digital-twin and cloud analytics capabilities, turning modernization into a prerequisite for federal grants[1]U.S. Department of Commerce, “One Year Later, CHIPS and Science Act Spurs American Competitiveness, Innovation, and National Security,” commerce.gov. Europe’s Machinery Regulation 2023/1230 sets a similar tone by mandating digital product passports by 2026. To balance sovereignty concerns, plants keep recipes on-premises while offloading demand planning to the cloud, which underpins the 18.00% CAGR expected for hybrid deployments.

Integration of IIoT and Real-Time Analytics with ERP Platforms

Terabytes of sensor data from CNC machines and assembly robots often reside outside planning cycles, yet modern ERP suites now ingest MQTT and OPC-UA streams to trigger predictive maintenance and automatically reschedule orders. Tier-one automotive suppliers that closed this loop cut unplanned downtime in 2025, boosting on-time delivery and preferred-supplier status. APAC electronics assemblers lead adoption due to high-mix lines where yield losses are costly. Edge gateways retain millisecond-sensitive control logic on site, while summarized KPIs flow to cloud ERP dashboards, proving that latency and insight can coexist in a tiered architecture.

Regulatory Pressure for Traceability and Compliance Across Global Supply Chains

Serialization mandates such as the United States DSCSA and the EU Falsified Medicines Directive require drug makers to assign unique identifiers to each saleable unit, a burden that is unsustainable with spreadsheets[2]U.S. Food and Drug Administration, “Drug Supply Chain Security Act (DSCSA),” fda.gov. Food processors face parallel demands under the 2026 FSMA traceability rule. ERP systems automate pedigree capture, link vials to pallets, and expose APIs for third-party logistics verification, trimming compliance labor up to 50%. Aerospace and defense primes must also log AS9100 provenance and ITAR data, making traceability a decisive selection factor for multinational roll-outs.

Shift Toward AI-Enabled Predictive Maintenance and Quality Management

Machine-learning models embedded in ERP quality modules compare live vision-inspection data against historical patterns, alerting operators before drift drives defects. Automotive stamping plants saw first-pass yield escapes increase significantly in 2025. Similar algorithms forecast bearing or seal failures using vibration spectra and oil analysis, enabling condition-based replacement instead of periodic overhauls. Because the models reside inside the planning engine, flagged assets automatically trigger rescheduling, eliminating the fragmentation that hampered standalone condition-monitoring systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership and Complex Implementation for Legacy-Heavy Plants | -1.8% | Global, acute in North America and Europe brownfield sites | Medium term (2-4 years) |

| Cybersecurity and IP Theft Concerns in Cloud-Based Deployments | -1.3% | Global, heightened in aerospace, defense and semiconductor sectors | Short term (≤ 2 years) |

| Shortage of Skilled ERP Implementation Professionals in Manufacturing Hubs | -0.9% | North America, Europe, select Asia-Pacific metros | Medium term (2-4 years) |

| Organizational Change Resistance and Disruption to Established Production Workflows | -0.7% | Global, concentrated in family-owned and unionized facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership and Complex Implementation for Legacy-Heavy Plants

Brownfield facilities still running three-decade-old controllers face integration costs 40-60% above greenfield benchmarks because proprietary protocols demand custom middleware. A 2025 survey found 38% of North American plants using MS-DOS shop-floor systems that cannot exchange live data, forcing parallel manual entry that erodes automation gains. [3]Manufacturing Leadership Council, “State of Manufacturing Technology Report 2025,” manufacturingleadershipcouncil.com Replacing antiquated automation often exceeds the software budget, so projects stretch 24-36 months while consultants reverse-engineer undocumented customizations, tying up capital and depressing output during cut-over phases.

Cybersecurity and IP Theft Concerns in Cloud-Based Deployments

Ransomware incidents against manufacturing jumped 150% between 2024 and 2025, with attackers exploiting ERP portals to halt production and demand payment. Aerospace and defense firms also grapple with ITAR data restrictions, which require FedRAMP-approved regions or on-premises enclaves that raise costs and architectural complexity.[4]U.S. Department of Defense, “Cybersecurity Maturity Model Certification (CMMC),” acq.osd.mil Semiconductor fabs fear design-file exfiltration, slowing cloud adoption despite potential efficiency gains. These risks underpin the rise of hybrid strategies that isolate sensitive IP on-site while shifting less critical workflows to the cloud.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Gains Traction Amid Sovereignty Mandates

The manufacturing ERP market size for hybrid deployments is advancing at an 18.00% CAGR as companies reconcile cloud agility with residency laws. In 2025, cloud held 55.40% of the manufacturing ERP market share, yet plants in regulated sectors such as defense and pharmaceuticals still favor on-premises control for export-controlled data. The European GDPR and China’s Cybersecurity Law keep recipes and customer files within national borders, pushing firms toward tiered architectures that sync anonymized planning data into public cloud analytics engines.

Edge gateways process millisecond-grade telemetry locally, then post aggregated KPIs to cloud dashboards. As vendors deliver containerized services that run wherever compute resides, hybrid has become the default compromise, particularly for multinational automakers juggling divergent jurisdictional rules.

By Organization Size: SMEs Accelerate Cloud Adoption

Large enterprises still account for the majority of purchasing, yet SMEs are the fastest-growing cohort in the manufacturing ERP market, with a 17.00% CAGR. Subscription models eliminate the USD 500,000 capex hurdle of perpetual licenses, while pre-configured vertical SaaS suites compress implementation from 18 months to roughly 8 weeks. Greenfield shops with minimal legacy baggage jump directly to mobile-native interfaces, freeing supervisors from desktop workstations.

Succession-planning pressures also spur digitization as retiring founders codify shop-floor knowledge in software to attract buyers. Regional grants in the United States and Europe further de-risk modernization for smaller plants, accelerating the pivot toward cloud.

By Manufacturing Mode: Mixed-Mode Platforms Converge Process and Discrete

Discrete operations accounted for 60.00% of manufacturing ERP market deployments in 2025, yet mixed-mode solutions are closing the gap with a 11.50% CAGR. Pharmaceutical firms now blend batch vial filling and continuous API synthesis in a single ledger for genealogy reporting. Food processors combine continuous pasteurization with discrete packaging, requiring allergen tracking and unit-based costing in the same database.

Unified platforms remove the dual-ERP overhead that previously forced manual financial consolidation and duplicate master data. Vendors embedding process-specific logic, shelf-life control, catch-weight handling, and inside discrete cores are capturing this growth wave.

By End-Industry Vertical: Electronics Outpaces Automotive Growth

Automotive retained 25.00% of spending in 2025 due to the complexity of electric-vehicle BOMs and IATF 16949 quality standards. Still, electronics and high-tech are advancing at a forecast 10.70% CAGR as the EU Chips Act imposes strict traceability requirements and smartphone makers compress design-to-shelf cycles. Aerospace and defense seek AS9100-compliant modules and ITAR safeguards, while pharmaceutical serialization under DSCSA makes ERP upgrades unavoidable.

Food and beverage companies are deploying traceability functions ahead of the 2026 FSMA rule. Industrial machinery and engineered-to-order sectors rely on advanced configurators inside ERP to manage variant complexity that mass-production suites cannot address natively.

Geography Analysis

North America generated 38.60% of global revenue in 2025 as the CHIPS and Science Act incentives tied grants to cloud-based digital twins, prompting semiconductor plants to standardize on modern ERP from day one. reshoring efforts and Mexico’s nearshoring boom extend standardized platforms across NAFTA trade corridors, while Canadian factories adopt carbon-tracking features to prepare for prospective border-adjustment levies.

Europe invests heavily to meet the CSRD’s Scope 3 emission-disclosure mandate that makes ERP the data backbone for carbon accounting. Germany’s Industrie 4.0 and the Machinery Regulation’s digital passport requirement accelerate spending in automotive and machinery clusters. Southern European plants tap EU digitization funds to offset subscription fees, narrowing the digital divide with the north.

Asia-Pacific is the fastest-growing region, with a 8.80% CAGR. India links Production-Linked Incentive payouts to ERP-driven production reporting. China mandates domestic ERP systems for state-owned firms to curb IP leakage, opening the door for local vendors. Southeast Asian contract manufacturers adopt cloud suites to meet real-time visibility standards imposed by electronics OEMs. South America, the Middle East, and Africa together remain smaller but show hotspots of rapid adoption, notably in GCC petrochemicals and Brazilian EV supply chains.

Competitive Landscape

Five global vendors-SAP, Oracle, Microsoft, Infor, and Epicor-held a significant share in 2025. They pursue breadth, offering PLM, HCM, and analytics in unified suites that lock in global accounts. Vertical challengers such as Plex and SYSPRO emphasize domain depth, shipping pre-configured workflows for automotive tier suppliers or FDA-compliant food plants that reduce costly customization.

Partnerships between ERP and automation vendors, illustrated by Rockwell Automation’s FactoryTalk integrations, streamline PLC data ingestion and shorten brownfield timelines. White-space lies in mixed-mode platforms that fuse process and discrete logic, and in AI-native architectures capable of real-time anomaly detection without bolted-on analytics.

Security certifications such as ISO 27001 and CMMC are becoming must-haves for aerospace bids, raising entry barriers for smaller firms. Hyperscale-cloud providers now bundle ERP, IoT, and analytics as platform services, threatening to disintermediate traditional software if OEMs pivot to these ecosystems for supplier onboarding.

Manufacturing Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Infor, Inc.

Epicor Software Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SAP released SAP S/4HANA Cloud for Sustainable Manufacturing, adding real-time carbon-footprint tracking and automated Scope 3 reporting.

- January 2026: Microsoft launched Dynamics 365 Supply Chain Center, a control tower using Azure OpenAI to explain disruptions and cut expedited freight up to 25%.

- November 2025: Oracle acquired Traverse Systems for more than USD 400 million, embedding edge-IoT middleware into Oracle Fusion Cloud Manufacturing.

- September 2025: Infor partnered with Siemens to pre-integrate CloudSuite Industrial with Opcenter MES, trimming implementation testing time.

Global Manufacturing Enterprise Resource Planning Market Report Scope

The Manufacturing Enterprise Resource Planning (ERP) market comprises integrated software solutions that manage and optimize core manufacturing business processes, including production planning, inventory control, procurement, finance, and supply chain operations. These systems enable real-time visibility, process automation, and data-driven decision-making across discrete, process, and mixed-mode manufacturing environments.

The Manufacturing Enterprise Resource Planning Report is Segmented by Deployment Model (Cloud, On-Premise, Hybrid), Organization Size (Large Enterprises, SMEs), Manufacturing Mode (Discrete, Process, Mixed-Mode), End-Industry Vertical (Automotive, Aerospace and Defense, Electronics and High-Tech, Food and Beverage, Industrial Machinery, Pharmaceuticals, Other), and Geography (North America, Europe, Asia-Pacific, South America, Middle East, Africa).

| Cloud |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises (SMEs) |

| Discrete Manufacturing |

| Process Manufacturing |

| Mixed-Mode Manufacturing |

| Automotive |

| Aerospace and Defense |

| Electronics and High-Tech |

| Food and Beverage |

| Industrial Machinery |

| Pharmaceuticals |

| Other End-Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Deployment Model | Cloud | |

| On-Premise | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises (SMEs) | ||

| By Manufacturing Mode | Discrete Manufacturing | |

| Process Manufacturing | ||

| Mixed-Mode Manufacturing | ||

| By End-Industry Vertical | Automotive | |

| Aerospace and Defense | ||

| Electronics and High-Tech | ||

| Food and Beverage | ||

| Industrial Machinery | ||

| Pharmaceuticals | ||

| Other End-Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the manufacturing ERP market expected to grow through 2031?

It is projected to expand at a 9.84% CAGR from 2026 to 2031, reaching USD 10.17 billion by the end of the period.

Which deployment model is gaining momentum under data-sovereignty rules?

Hybrid deployments are rising at an 18.00% CAGR because they keep sensitive data on-premise while leveraging cloud analytics.

Why are small and medium-sized manufacturers embracing ERP now?

Subscription pricing and vertical SaaS templates cut capital outlay and shrink implementation timelines to as little as eight weeks.

What regulations are driving ERP adoption in the food sector?

The 2026 FSMA traceability rule requires end-to-end lot tracking that spreadsheets cannot support, prompting ERP upgrades.

Which region shows the fastest future growth for manufacturing ERP?

Asia-Pacific, led by India and China, is forecast to advance at an 8.80% CAGR through 2031.

Page last updated on: