Europe Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

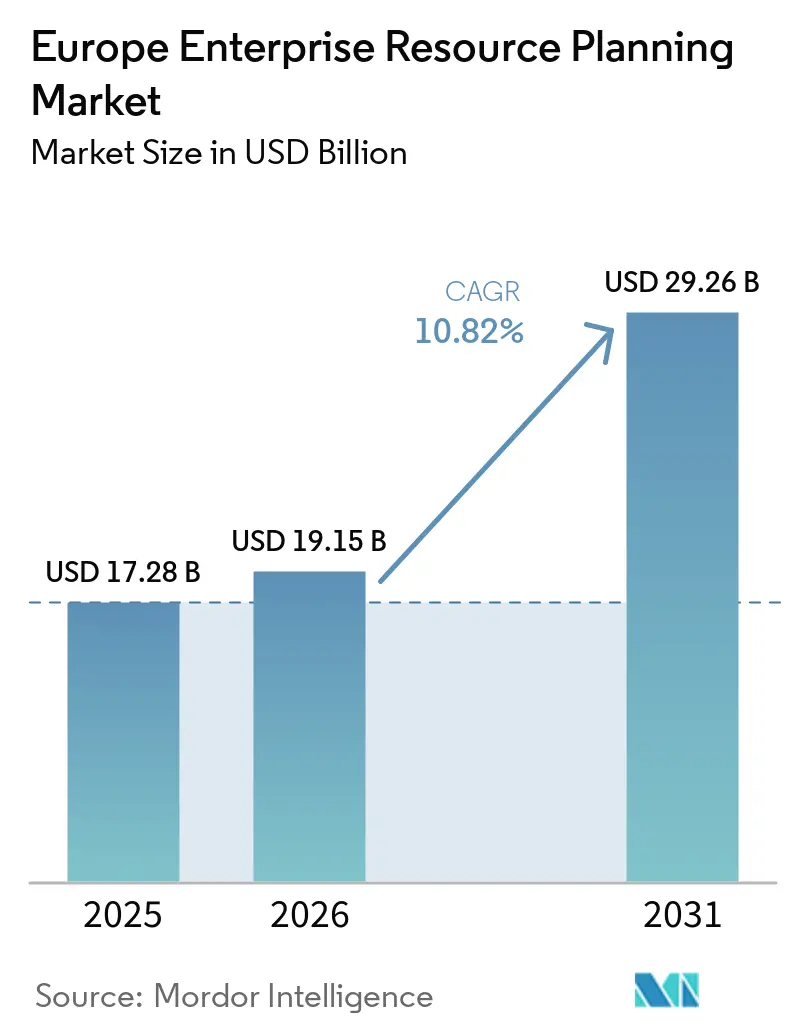

| Base Year Market Size (2025) | USD 17.28 Billion |

| Market Size (2026) | USD 19.15 Billion |

| Market Size (2031) | USD 29.26 Billion |

| Growth Rate (2026 - 2031) | 10.82% CAGR |

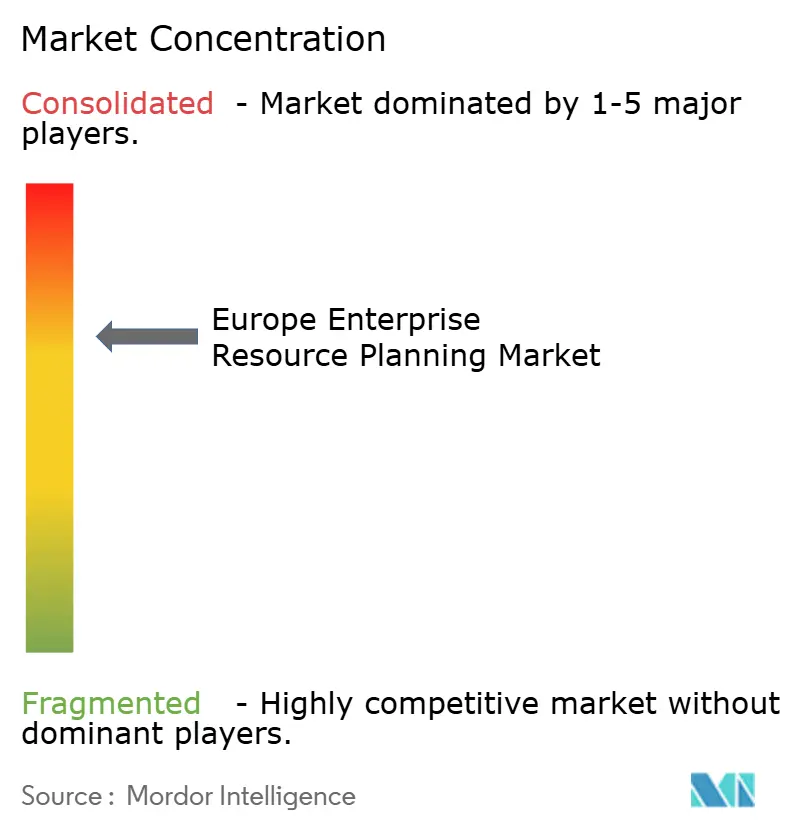

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Enterprise Resource Planning Market Analysis by Mordor Intelligence

The Europe Enterprise Resource Planning Market size is expected to grow from USD 17.28 billion in 2025 to USD 19.15 billion in 2026 and is forecast to reach USD 29.26 billion by 2031 at a 10.82% CAGR over 2026-2031. Escalating demand for cloud-native suites, the rapid infusion of generative AI into core workflows, and a tightening web of European data-sovereignty laws are accelerating platform modernization across manufacturing, retail, and public-sector domains. Adoption momentum intensifies as the European Commission’s Digital Decade program urges enterprises to embrace cloud, AI, and big data solutions, while sovereign cloud launches from leading vendors neutralize privacy concerns and unlock regulated verticals.[1]Source: European Commission, “Digital Decade Policy Programme 2030,” ec.europa.eu Mid-market manufacturers, retailers, and local governments are front-loading projects to capitalize on European Recovery and Resilience Facility grants, thereby expanding the addressable base for subscription-priced offerings. Competitive pressure is rising as incumbents embed AI copilots and industry clouds, even as mid-tier challengers gain ground by bundling localized compliance and flexible consumption into lean deployments.

Key Report Takeaways

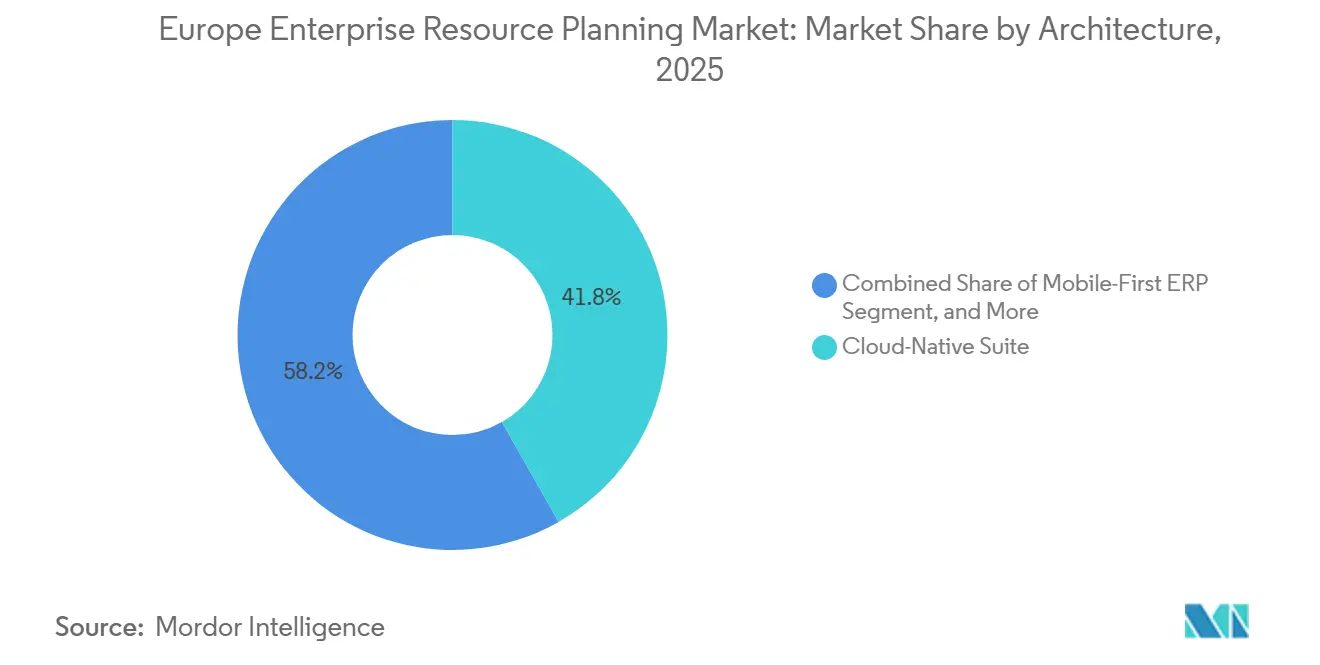

- By architecture, cloud-native suites held 41.78% share of the Europe enterprise resource planning market in 2025, while mobile-first architectures are advancing at a 9.65% CAGR through 2031.

- By business function, finance and accounting led with 28.67% share of 2025 revenue of Europe ERP market, whereas customer relationship and commerce modules are expanding at an 8.85% CAGR.

- By deployment model, cloud deployment captured 64.13% of the 2025 investment, and the same model is posting the segment-best 9.25% CAGR to 2031.

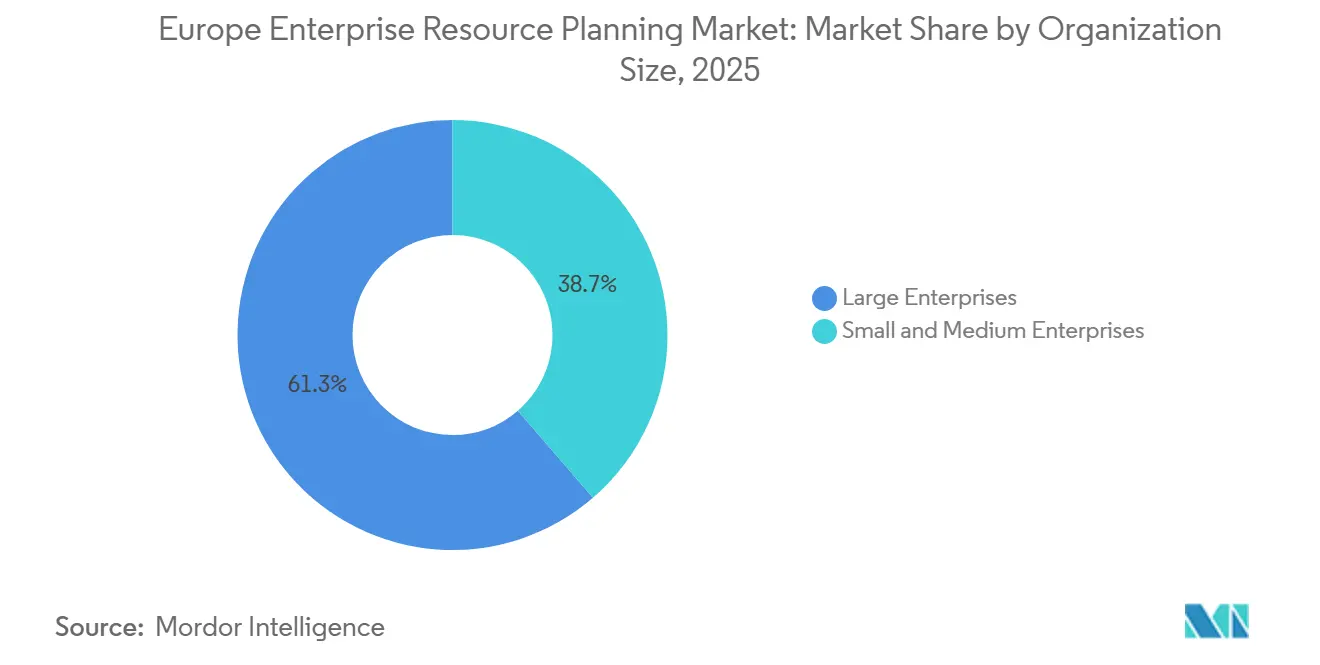

- By organization size, large enterprises accounted for 61.33% of 2025 outlays, yet small and medium enterprises are growing at a 9.78% CAGR.

- By industry vertical, manufacturing represented 27.59% of 2025 implementations, while retail and e-commerce solutions are accelerating at a 10.25% CAGR.

- By geography, Germany accounted for 24.12% of 2025 revenue, and Spain recorded the fastest 10.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Enterprise Resource Planning Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to Cloud ERP Solutions | +2.1% | Pan-European, strongest in Nordics and Benelux | Medium term (2-4 years) |

| Integration of AI and Advanced Analytics | +1.8% | Germany, UK, France; expanding to Spain and Italy | Short term (≤ 2 years) |

| Regulatory Mandates on Data Privacy (GDPR, NIS2) | +1.5% | EU-wide, with heightened enforcement in Germany and France | Long term (≥ 4 years) |

| SME Uptake Through EU Recovery and Resilience Facility | +1.2% | Spain, Italy, Eastern Europe; concentrated in manufacturing and tourism SMEs | Medium term (2-4 years) |

| Carbon-Accounting Requirements Across Supply Chains | +0.9% | Germany, France, Netherlands; extending to automotive and chemicals sectors | Long term (≥ 4 years) |

| Edge-Based ERP for Real-Time Manufacturing Control | +0.7% | Germany, Czech Republic, Poland; focused on discrete manufacturing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift to Cloud ERP Solutions

Cloud migration is redefining the cost profile of the European enterprise resource planning market by converting hardware-heavy installations into pay-as-you-go subscriptions that match expenditure with demand cycles. Record growth in SAP’s RISE program and Microsoft Dynamics 365 cloud suites underscores a wholesale pivot toward consumption economics that appeal to finance chiefs seeking predictable operating costs. The availability of European sovereign cloud regions calms residency concerns and unlocks regulated sectors such as public administration and healthcare. Mid-market manufacturers are accelerating adoption after user-group surveys confirmed a doubling of S/4HANA cloud footprints between 2023 and 2025. In the Europe ERP market, vendors package fixed-price migration bundles that compress project timelines and de-risk budget overruns, encouraging even risk-averse industrial groups to retire legacy estates.

Integration of AI and Advanced Analytics

Generative AI is moving from pilot to production, placing conversational copilots within procurement, finance, and human resources modules. Early adopters reduce time-to-insight and manual reconciliations by roughly half, strengthening the value proposition of next-generation ERP suites. European manufacturers use predictive models to simulate supply-chain shocks, enabling proactive stock positioning in response to tariff or logistics disruptions. Vendors embed transparent audit trails to comply with the European AI Act, ensuring high-risk functions, such as recruitment scoring, remain explainable and human-governed. This rapid infusion of AI raises user productivity, drives licence upgrades, and cements the Europe enterprise resource planning market as a centerpiece of digital operating models.

Regulatory Mandates on Data Privacy (GDPR, NIS2)

The convergence of GDPR enforcement and NIS2 cybersecurity obligations assigns hefty penalties for inadequate controls, pushing enterprises to consolidate governance inside core transactional platforms. Vendors respond by integrating zero-trust authentication, continuous monitoring, and automated breach-notification workflows that align with 24-hour reporting windows.[2]Source: European Union Agency for Cybersecurity, “NIS2 Directive: New Cybersecurity Requirements,” enisa.europa.eu Public-sector tenders increasingly demand in-suite compliance certificates, narrowing eligible supplier pools to orchestrated platforms with demonstrable, audit-ready capabilities. As fines accumulate and incident-reporting timetables shrink, demand for unified governance, risk, and compliance modules embedded in cloud ERP solutions across the Europe ERP market is growing.

SME Uptake Through EU Recovery and Resilience Facility

European grants and tax incentives reduce the cash hurdle for first-time ERP buyers, igniting demand among firms employing fewer than 250 workers. Spain and Italy channel multi-billion-euro allocations toward digitization vouchers that cover half of eligible software spend, while Nordic vendors step in with pre-configured vertical templates and local-language support teams. Subscription models with phased rollouts lower operational disruption and align monthly fees with revenue swings faced by family-owned manufacturers and tourism operators. The resulting wave of green-field installations expands the total Europe enterprise resource planning market beyond traditional large-enterprise strongholds.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Migration and Integration Costs | -1.4% | Pan-European, acute in large enterprises with legacy customizations | Short term (≤ 2 years) |

| Data-Sovereignty and Residency Concerns | -1.1% | Germany, France, Austria; concentrated in public sector and BFSI | Medium term (2-4 years) |

| Shortage of ERP-Specialised Talent in Europe | -0.8% | Germany, UK, Nordics; affecting SAP and Oracle implementations | Long term (≥ 4 years) |

| Energy-Price Volatility Pressuring IT Budgets | -0.6% | Germany, Italy, Spain; impacting energy-intensive manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Migration and Integration Costs

Complex, customization-rich estates inflate budgets when enterprises shift to modern platforms, often doubling initial estimates once data cleansing, interface rewrites, and dual-running periods are included. Consulting fees for scarce SAP and Oracle skills have climbed above USD 500 per hour, squeezing capital allocation at mid-market manufacturers. Fixed-price migration bundles and credit-backed cloud offers temper, but do not eliminate, financial risk, prompting regulated industries to defer projects until business-case certainty firms up and feeding a near-term drag on the Europe ERP market.

Data-Sovereignty and Residency Concerns

Court rulings that nullified prior trans-Atlantic data frameworks increase scrutiny on any platform hosted outside European jurisdiction. German and French agencies stipulate strict in-region hosting and prohibit extra-territorial data access, effectively excluding non-compliant offerings from public-sector procurements. In 2024, Germany's Federal Office for Information Security (BSI) mandated that operators of critical infrastructure must store their operational data within European borders. Additionally, the BSI emphasized that foreign governments should not force cloud service providers to disclose data without oversight by European courts.[3]Source: German Federal Office for Information Security, “Cloud Computing Compliance Catalogue (C5),” bsi.bund.de Vendors counter with dedicated sovereign clouds and joint ventures under the region's control, but the need to operate duplicate infrastructure inflates costs and fragments scale economies, restraining broader cloud conversion across the European enterprise resource planning market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Cloud-Native Foundations and Mobile Momentum

Cloud-native suites captured 41.78% of 2025 spending, establishing themselves as the control tower for real-time analytics and automated patching. Vendors release monthly updates that add AI features without disrupting operations, raising user expectations for evergreen functionality. Mobile-first platforms, expanding at a 9.65% CAGR, equip field technicians and warehouse pickers with offline-capable apps that sync the moment connectivity returns, a capability now central to distributed workforces across utilities and logistics. IFS Cloud Mobile and similar offerings demonstrate how edge caching cuts unplanned downtime and accelerates inventory turns, contributing incremental share gains.[4]Source: IFS AB, “IFS Cloud Mobile,” ifs.com

Two-tier architectures gain traction as multinationals deploy lightweight cloud systems at subsidiaries while core financials remain on high-control stacks, an approach that balances local agility with headquarters oversight. Edge-enabled ERP units on factory floors orchestrate millisecond-level operations for robots and inspection cameras, then feed aggregated metrics to the cloud parent. This hybrid pattern tightens quality loops and conforms to Industrie 4.0 mandates, strengthening vendor lock-in within the Europe enterprise resource planning market.

By Business Function: Finance Core, Commerce Catalyst

Finance and accounting modules accounted for 28.67% of 2025 revenue, underscoring their role as statutory systems of record and gatekeepers of audit integrity across 27 tax regimes. Continuous close, automated reconciliation, and embedded analytics reduce cycle times and free finance teams for value-add analysis. Customer relationship and commerce modules are advancing at an 8.85% CAGR as retailers stitch together e-commerce, order orchestration, and service engagement in a single data model. Real-time inventory allocations and dynamic pricing drive margin protection during geopolitical supply shocks while enhancing customer experience.

Supply-chain suites remain mission-critical, simulating freight corridors and alternative supplier mixes in response to Red Sea or rail bottlenecks. Human capital management solutions differentiate via AI-driven skills ontologies that match internal talent with project demand, alleviating regional labor shortages. Manufacturing execution and quality modules embed electronic batch records, satisfying GMP audits and delivering granularity that flows upstream into sustainability disclosures, anchoring multi-module adoption inside the European enterprise resource planning market.

By Deployment Model: Cloud Ascendancy

Cloud deployment accounted for 64.13% of 2025 investment and continues to post a 9.25% CAGR as enterprises exit depreciating data centers and pivot budgets to innovation sprints. Public-cloud ERP minimizes total cost of ownership for resource-constrained SMEs, while private-cloud editions satisfy stringent regulators that require tenant isolation and local hosting. Hybrid footprints persist during transition phases, creating stepped migration paths that mitigate cutover risk and stabilize cash outflows. On-premises instances persist in air-gapped defense and nuclear settings, yet even these enclaves adopt edge-to-cloud sync during maintenance windows to surface analytics on centralized dashboards. Vendors accelerate de-support deadlines for legacy releases, compelling procrastinators into the European enterprise resource planning market’s subscription orbit.

Additionally, the shift toward cloud-based ERP systems is driven by the increasing need for scalability, flexibility, and real-time data access. Enterprises are leveraging these systems to enhance operational efficiency and gain a competitive edge in the market. The integration of advanced technologies, such as artificial intelligence and machine learning, into ERP solutions further boosts their adoption, enabling predictive analytics and automated decision-making. This trend underscores the growing importance of cloud ERP in addressing the dynamic needs of modern businesses while ensuring compliance with evolving regulatory requirements.

By Organization Size: SME Acceleration

Large enterprises accounted for 61.33% of 2025 revenue, leveraging multi-currency and multi-ledger capabilities to orchestrate global subsidiaries. However, the small and medium enterprise cohort is powering incremental growth with a 9.78% CAGR. Subscription pricing, rapid-configure templates, and government subsidies lower the barrier for firms with fewer than 250 staff. Localized VAT, payroll, and e-invoicing rules built into modern suites eliminate the need for custom code, flattening the complexity curve.

Open-source alternatives such as Odoo lure price-sensitive startups with modular extensions and community support, whereas mid-tier vendors focus on vertical depth to shorten time-to-value. These solutions provide flexibility and scalability, making them attractive to businesses with evolving needs. The European enterprise resource planning market size for SMEs is therefore expected to expand faster than the overall curve and diversify the competitive set beyond the three global incumbents.

By Industry Vertical: Manufacturing Pillar, Retail Surge

Manufacturing accounted for 27.59% of deployments in 2025, led by discrete and process segments that rely on bills of material, routings, and compliance dashboards. Integration with industrial IoT drives predictive maintenance, reducing downtime and lifting overall equipment effectiveness across auto and machinery plants. Retail and e-commerce solutions are growing at a 10.25% CAGR, driven by omnichannel initiatives that align online baskets with in-store stock levels and green-checkout reporting.

Banks and insurers embed ERP-like engines to streamline core administration and meet stringent capital regulations, whereas public-sector agencies modernize fragmented finance ledgers to publish near-real-time transparency portals. Healthcare and life sciences players adopt embedded quality and traceability functions that align with pharmacovigilance rules and future-proof against expanding European sustainability directives. These vertical dynamics broaden addressable use cases and sustain long-run growth for the European enterprise resource planning market.

Geography Analysis

Germany led the European enterprise resource planning market with 24.12% of 2025 revenue, underpinned by an advanced manufacturing base that integrates edge analytics with cloud financials. Federal grants covering up to half of eligible ERP costs accelerate adoption among Mittelstand exporters, while C5 compliance rules oblige vendors to locate data centers on German soil, marginally inflating delivery costs but deepening domestic commitment. Steady momentum persists as automotive and machinery groups shift to predictive maintenance studios embedded in next-generation suites, driving double-digit software renewal pipelines.

The United Kingdom remains pivotal due to a dense concentration of global headquarters across finance, legal, and consulting services. Post-Brexit regulatory autonomy prompts firms to upgrade multicurrency treasury, liquidity, and tax engines, ensuring frictionless settlement across the region and non-European entities. France’s sovereignty doctrine channels state investment toward EU-controlled platforms, energizing local provider ecosystems and opening multiyear tenders in public administration and healthcare. Italy leans on generous Transizione 4.0 tax credits to modernize family-owned manufacturers in Lombardy and Veneto, pulling cloud suppliers into regional clusters where bilingual support and rapid prototyping are prized.

Spain represents the fastest-growing geography, logging a 10.05% CAGR through 2031 as EUR 4.3 billion (USD 5 billion) in recovery funding subsidizes digital transformation vouchers for small businesses. Hospitality, fashion, and food producers pivot to cloud suites that blend point-of-sale mobility with supply-chain transparency, locking in real-time margin dashboards. Across the Nordics and Benelux, near-full broadband penetration and progressive digital-government programs push cloud adoption rates above 75%, fostering experimentation with AI copilots and ESG dashboards. Eastern European manufacturers, buoyed by the region's structural funds, exit legacy stacks and create fresh demand for entry-tier subscription suites, further broadening the Europe enterprise resource planning market footprint.

Competitive Landscape

The market shows moderate concentration as SAP, Oracle, and Microsoft collectively hold roughly 55-60% of regional revenue, yet mid-tier challengers and open-source innovators fragment the long tail. Incumbents deepen their moats by embedding AI co-pilots, industry clouds, and carbon-accounting capabilities that automate invoice matching, candidate screening, and Scope 3 emissions reporting. Sovereign-cloud expansions into Germany and the Netherlands reinforce vendor eligibility for public-sector contracts and position platforms as trusted repositories for regulated workloads.

Specialists such as IFS, Unit4, and Visma exploit vertical and geographic niches with localized compliance packs and flexible consumption models, often bundled with depth in asset management or project accounting that is absent from generic stacks. Aggressive acquisition sprees, IFS targeting asset-intensive targets, and Visma consolidating Nordic SME software, tighten solution breadth and accelerate cross-sell synergies. Open-source projects like Odoo and ERPNext attract cost-sensitive startups by trading enterprise-grade support for unlimited extensibility, adding competitive tension at the low end.

Sustainability reporting emerges as a decisive battleground. Vendors that hard-wire ESG metrics into transaction flows gain mindshare among corporates preparing for CSRD disclosures. As consolidation accelerates, the Europe enterprise resource planning market remains dynamic, with innovation cycles driven by AI efficacy, sovereign-cloud footprints, and differentiated vertical content. Additionally, the increasing emphasis on compliance and data sovereignty further shapes the competitive landscape, compelling vendors to adapt swiftly to regulatory demands.

Europe Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

The Sage Group Plc

IFS AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SAP expanded its EU sovereign-cloud network to Frankfurt and Amsterdam, giving public-sector buyers in Germany and the Netherlands the option of national-border hosting.

- January 2026: Microsoft launched Dynamics 365 Copilot for Finance, halving month-end close cycles for early users such as Siemens and Unilever.

- December 2025: Oracle acquired Cerner’s European healthcare operations for USD 1.2 billion, integrating clinical and ERP workflows on Fusion Cloud.

- November 2025: IFS secured a USD 300 million contract with Airbus to deploy IFS Cloud across 15 manufacturing sites, replacing legacy platforms by 2027.

- October 2025: Workday opened a Dublin data center, enabling EU-resident customers to localize HR, payroll, and finance data within the European Economic Area.

Europe Enterprise Resource Planning Market Report Scope

The Europe Enterprise Resource Planning Market Report is Segmented by Architecture (Cloud-Native Suite, Mobile-First ERP, Social/Collaborative ERP, and Two-Tier/Edge ERP), Business Function (Finance and Accounting, Supply-Chain and Operations, Human Capital Management, Customer Relationship and Commerce, and Manufacturing Execution and Quality), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Manufacturing, Retail and E-commerce, BFSI, Government and Public Sector, IT and Telecom, Healthcare and Life Sciences, and Other Industry Verticals), and Geography (United Kingdom, Germany, France, Italy, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Native Suite |

| Mobile-First ERP |

| Social / Collaborative ERP |

| Two-Tier / Edge ERP |

| Finance and Accounting |

| Supply-Chain and Operations |

| Human Capital Management |

| Customer Relationship and Commerce |

| Manufacturing Execution and Quality |

| On-Premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing |

| Retail and E-commerce |

| BFSI |

| Government and Public Sector |

| IT and Telecom |

| Healthcare and Life Sciences |

| Other Industry Verticals |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Architecture | Cloud-Native Suite |

| Mobile-First ERP | |

| Social / Collaborative ERP | |

| Two-Tier / Edge ERP | |

| By Business Function | Finance and Accounting |

| Supply-Chain and Operations | |

| Human Capital Management | |

| Customer Relationship and Commerce | |

| Manufacturing Execution and Quality | |

| By Deployment Model | On-Premise |

| Cloud | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Industry Vertical | Manufacturing |

| Retail and E-commerce | |

| BFSI | |

| Government and Public Sector | |

| IT and Telecom | |

| Healthcare and Life Sciences | |

| Other Industry Verticals | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How large will the Europe enterprise resource planning market be by 2031?

The market is projected to reach USD 29.26 billion by 2031, reflecting an 10.82% CAGR over 2026-2031.

Which deployment model is growing the fastest across Europe?

Cloud deployment is advancing at a 9.25% CAGR as organizations retire on-premise data centers and adopt subscription economics.

Why is Spain the fastest-growing country for ERP adoption?

Spain benefits from EUR 4.3 billion in EU recovery funding that subsidizes SME digitalization, pushing annual growth to 10.05% through 2031.

What functional modules show the strongest momentum?

Customer relationship and commerce modules are expanding at an 8.85% CAGR thanks to rising omnichannel retail and direct-to-consumer strategies.

Page last updated on: