Automotive IoT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

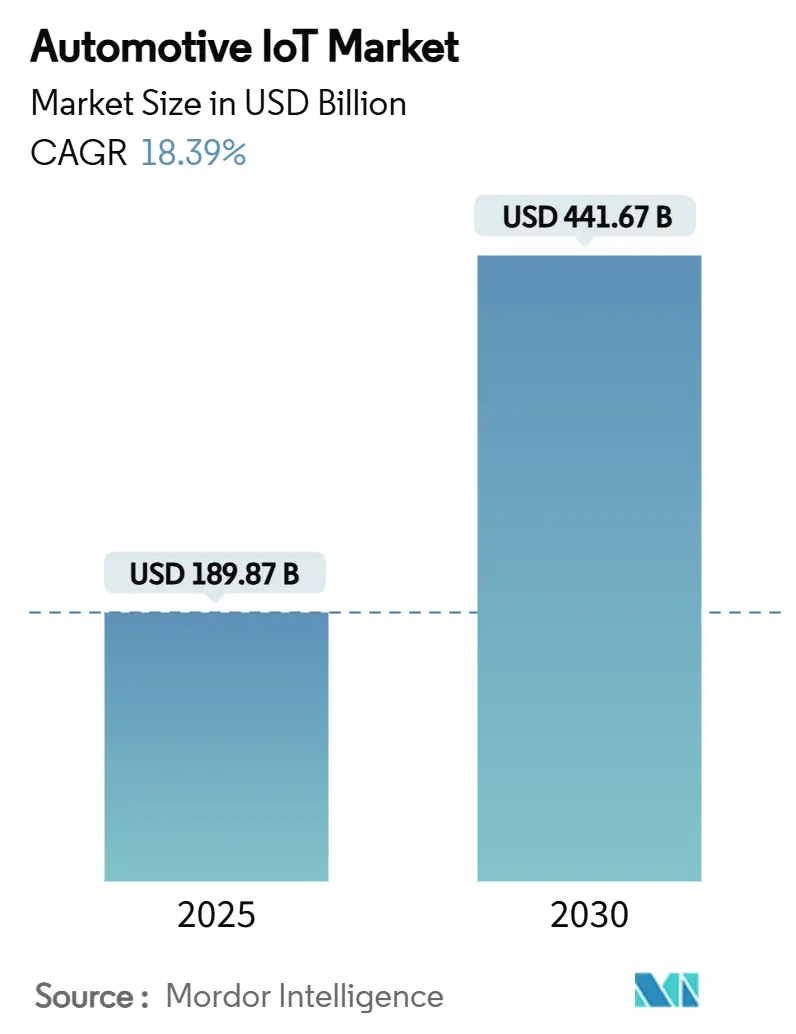

| Market Size (2025) | USD 189.87 Billion |

| Market Size (2030) | USD 441.67 Billion |

| Growth Rate (2025 - 2030) | 18.39% CAGR |

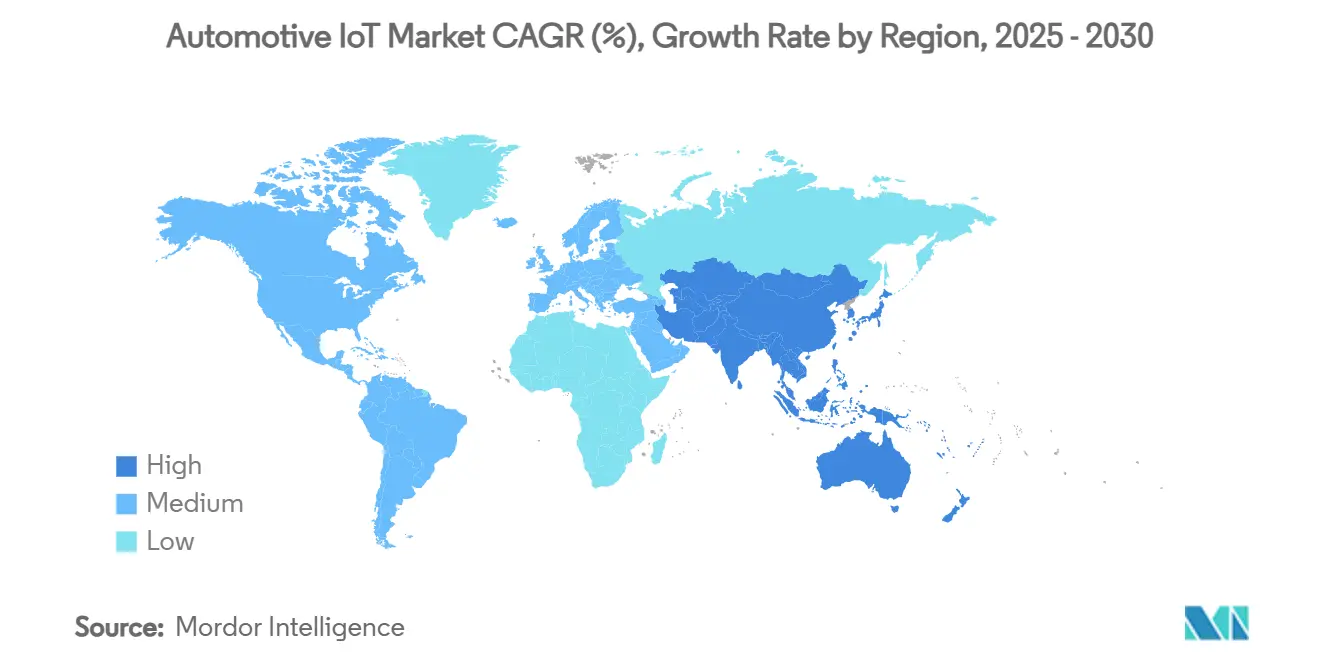

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive IoT Market Analysis by Mordor Intelligence

The Automotive IoT market size stands at USD 189.87 billion in 2025 and is forecast to reach USD 441.67 billion by 2030, advancing at an 18.39% CAGR in that period. This growth is propelled by the industry’s migration from mechanical engineering toward software-defined vehicle platforms, where always-on connectivity, over-the-air updates, and data-driven services outweigh traditional powertrain differentiation. Regulatory mandates such as the European eCall requirement and India’s AIS-140 standard are turning IoT hardware from an optional extra into compulsory safety infrastructure, thereby insulating the Automotive IoT market from cyclical demand swings. Automakers and suppliers are redirecting investment toward edge-cloud architectures that can meet sub-30 millisecond latency needs for vehicle-to-everything (V2X) use cases. Component ASPs are falling quickly, making embedded modules economically viable for mass-market cars, while usage-based insurance partnerships are monetizing real-time driving data and deepening post-sale revenue streams. Concurrently, 5G roll-outs in North America, Europe, and China are providing the high-bandwidth backbone required for predictive maintenance and cooperative driving services, further reinforcing demand for Automotive IoT market offerings.

Key Report Takeaways

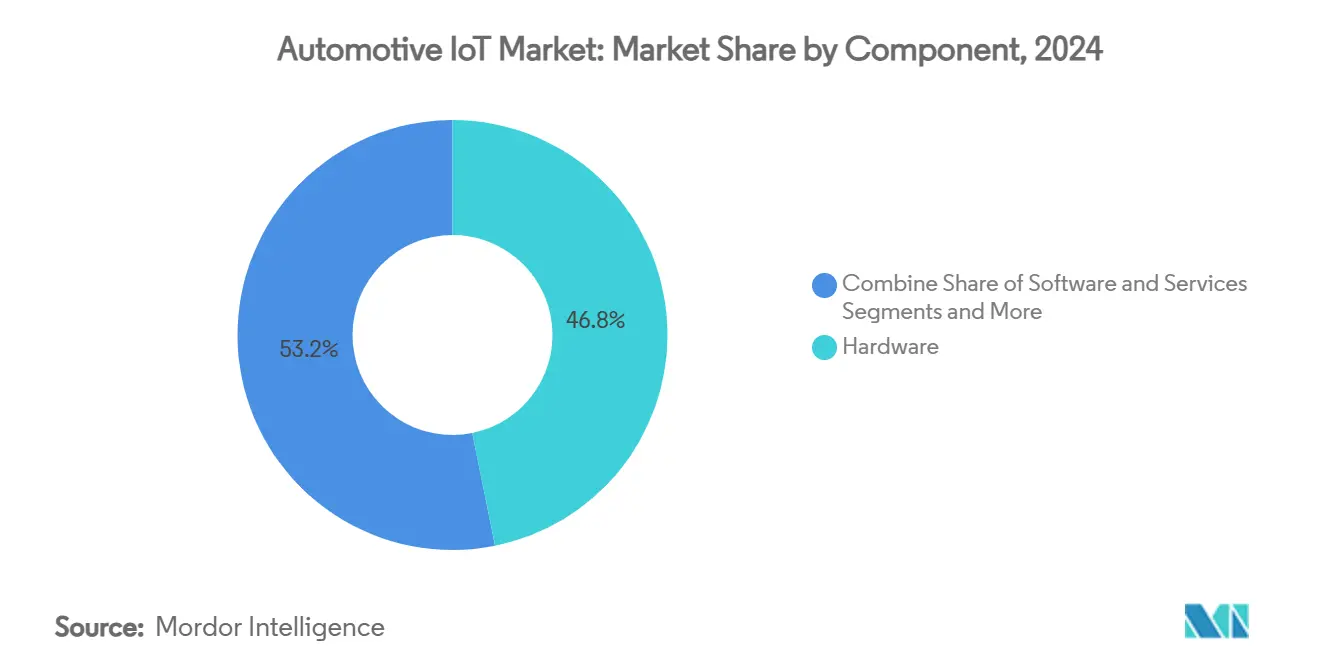

- By component, hardware captured 46.83% of the Automotive IoT market share in 2024, whereas services are projected to grow at a 20.94% CAGR through 2030.

- By connectivity form, embedded solutions commanded 51.34% of the Automotive IoT market size in 2024, while integrated connectivity is expanding at a 20.45% CAGR.

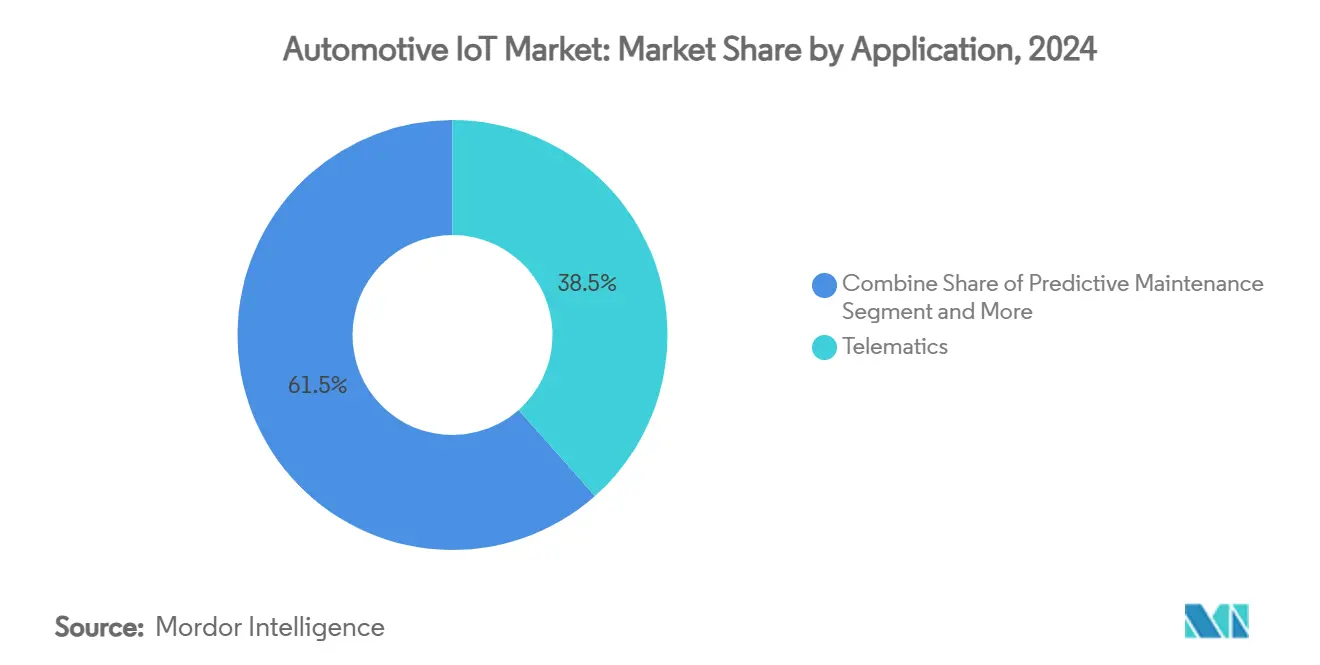

- By application, telematics held a 38.48% share of the Automotive IoT market in 2024, and predictive maintenance is advancing at a 19.98% CAGR.

- By network technology, cellular systems accounted for 58.95% of the Automotive IoT market size in 2024, registering a 21.54% CAGR through 2030.

- By geography, North America led with 39.45% revenue share in 2024, whereas Asia-Pacific is forecast to post a 21.78% CAGR to 2030.

Global Automotive IoT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid OEM shift toward software-defined vehicles | +3.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Mandatory e-Call and telematics regulations (EU, CN, BR, IN) | +2.8% | Europe, China, Brazil, India with spillover to other regions | Short term (≤ 2 years) |

| Falling cost of automotive-grade cellular modules | +2.1% | Global, particularly benefiting emerging markets | Medium term (2-4 years) |

| Expansion of high-bandwidth V2X edge-cloud infrastructure | +1.9% | North America, Europe, China leading deployment | Long term (≥ 4 years) |

| Rise of usage-based insurance telematics partnerships | +1.7% | North America, Europe, with expansion to Asia-Pacific | Medium term (2-4 years) |

| Growing demand for over-the-air (OTA) cybersecurity updates | +1.5% | Global, driven by regulatory requirements | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid OEM Shift toward Software-Defined Vehicles

Automakers are rebuilding electrical-electronic (E/E) architectures around centralized domain controllers that allow feature deployment through over-the-air updates, shortening development cycles and unlocking subscription revenues. BMW already pushes quarterly software releases to its full range, mirroring Tesla’s long-running update cadence. Centralized networks also simplify hardware variants, lowering bill-of-materials costs and improving in-field diagnostics accuracy. Suppliers are responding: Bosch invested USD 3.39 billion in 2024 to scale its vehicle-cloud platform, while Continental re-skilled 40% of its engineering staff toward software roles. These moves illustrate how competitive advantage is shifting from mechanical prowess to continuous software innovation, reinforcing demand across the Automotive IoT market.

Mandatory eCall and Telematics Regulations

The European Union requires every new car type-approved after March 2018 to ship with eCall, a system that automatically contacts emergency services after a severe crash, cutting average response times by up to 50%. China, Brazil and India enforce comparable rules, and India’s AIS-140 mandate covers commercial fleets as well. Because compliance is non-negotiable, volumes are guaranteed even during macroeconomic downturns. This creates scale economies that reduce component prices and broaden IoT inclusion across mid-price segments, sustaining the Automotive IoT market even when discretionary spending slows.

Falling Cost of Automotive-Grade Cellular Modules

Standardized chipsets and shared consumer-electronics supply chains have pushed LTE-A module prices below USD 40 per unit. Quectel’s globally certified AG525R-GL module shows how scale manufacturing is shrinking the cost gap versus smartphone radios. [1]Quectel Wireless Solutions, “AG525R-GL Module Certification,” quectel.com Lower hardware outlays enable automakers in cost-sensitive regions to embed IoT connectivity without inflating vehicle MSRP, and open room for bundled connectivity plans that improve data capture density. Tata Motors cut per-vehicle connectivity cost 40% in 2024 by switching to next-generation modules, underscoring how affordability accelerates Automotive IoT market penetration.

Expansion of High-Bandwidth V2X Edge-Cloud Infrastructure

Deutsche Telekom and Nokia demonstrated that roadside multi-access edge computing can trim round-trip latency to below 30 milliseconds, a prerequisite for safety-critical automated driving. Carriers such as Verizon are now co-locating micro-data centers near traffic corridors, enabling real-time hazard detection and dynamic signal control. These edge nodes underpin cooperative lane-merge functions and platooning, adding value to premium service tiers and lifting average revenue per connected vehicle within the Automotive IoT market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent CAN bus legacy integration bottlenecks | -2.3% | Global, particularly affecting established OEMs with legacy architectures | Medium term (2-4 years) |

| Data-ownership disputes between OEMs, dealers and fleets | -1.8% | North America and Europe primarily, with regulatory uncertainty | Short term (≤ 2 years) |

| Semiconductor supply-chain geopolitical volatility | -1.6% | Global, with particular impact on Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Limited ROI for connected-vehicle services in emerging markets | -1.4% | Emerging markets in Asia, Africa, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent CAN Bus Legacy Integration Bottlenecks

Controller Area Network links top out near 10 Mbps, a ceiling that constrains high-resolution sensor fusion and continuous data upload. Migrating to automotive Ethernet demands extensive re-validation of safety-critical domains, often stretching platform programs by multiple model years. Volkswagen spent EUR 2 billion over three years to retrofit a centralized network into its MEB architecture, illustrating the substantial transition cost. The lag slows adoption of data-rich functions and temporarily caps total addressable value within the Automotive IoT market.

Data-Ownership Disputes between OEMs, Dealers and Fleets

Regulators are scrutinizing how vehicle data is stored and commercialized. The US Federal Trade Commission barred General Motors from selling driver behavior data for five years after privacy complaints. [2]The Verge, “GM Banned from Selling Driving Data,” theverge.com Texas followed with a lawsuit alleging unauthorized data monetization. [3]The New York Times, “Texas Sues GM over Driver Data,” nytimes.com Europe’s forthcoming Data Act seeks clarity, but cross-border enforcement remains uncertain. Until contractual norms settle, some stakeholders delay investments in analytics-heavy services, restraining the Automotive IoT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Recurring Revenue Transformation Anchored in Services

Hardware still delivered 46.83% of Automotive IoT market revenue in 2024, anchored by sensors, gateways, and antennas bundled with every connected platform. Services, however, deliver the fastest upside, advancing at 20.94% CAGR to 2030 as OEMs commercialize data dashboards, feature unlocks, and predictive maintenance subscriptions. The Automotive IoT market size attached to services reflects the widening acceptance of pay-as-you-drive models for navigation, entertainment, and insurance add-ons. Hardware commoditization is visible in falling module ASPs and rising cross-platform interchangeability, compressing margins for tier-one suppliers.

Tesla’s vertically integrated full-stack architecture maximizes software capture and sets a benchmark that peers are racing to emulate. Continental responded by reorganizing toward software orchestration, while Bosch earmarked USD 3.39 billion to accelerate middleware toolchains. These moves are designed to secure share of a services-heavy Automotive IoT market, where customer lifetime value depends on active monthly users rather than unit shipments. Outsourcing of non-differentiated hardware production is likely to intensify, freeing resources for cloud analytics, machine-learning personalization, and in-cabin app ecosystems.

By Connectivity Form: Embedded Dominance with Integration Upside

Embedded modems equipped 51.34% of connected cars in 2024, confirming consumer appetite for seamless always-on services free from smartphone tethering hassles. The Automotive IoT market share attached to embedded options is supported by automaker desire to control data flows and security keys. Integration-ready architectures, combining embedded baseband boards with replaceable communication front-ends, are accelerating at 20.45% CAGR. They strike a balance between future-proofing and cost control, enabling 5G or satellite module swaps without full redesigns.

Case in point: Ford’s switch to embedded 5G in the 2024 F-150 Lightning drove a 60% jump in connected-service enrollment and halved connectivity-related warranty claims. Tethered solutions persist in low-cost vehicles and aftermarket retrofits, but user experience gaps limit incremental revenue potential. As 5G coverage expands, integrated platforms will likely bridge the divide by combining the permanence of embedded SIMs with modular RF front-end flexibility, further lifting the Automotive IoT market.

By Application: Predictive Maintenance Rises above Telematics Volume Base

Telematics delivered 38.48% of Automotive IoT market revenue in 2024, reflecting the long-established use case of fleet tracking and stolen-vehicle recovery. Predictive maintenance is the breakout story, climbing at a 19.98% CAGR as fleets emphasize uptime economics. DHL cut unplanned downtime 35% in 2024 by layering machine-learning diagnostics over aggregated CAN and vibration data, saving EUR 50 million annually. Infotainment is evolving into a streaming-centric service with revenue-sharing models involving content providers.

Advanced driver assistance and V2X safety alerts are merging into cooperative maneuvering suites that can command premium subscription fees. In-depth data analytics turns raw sensor feeds into actionable insights that reduce total cost of ownership, reinforcing the Automotive IoT market size linked to predictive services. As sensor fusion and AI processing mature, predictive maintenance’s share will likely overtake traditional telematics in high-duty-cycle commercial segments.

By Network Technology: Cellular 5G Cementing Leadership

Cellular solutions owned 58.95% of Automotive IoT market revenue in 2024 and are growing at 21.54% CAGR through 2030, driven by 5G’s ultra-reliable low-latency capability. Verizon added edge nodes along freight corridors in 2024 to ensure sub-10 millisecond round trips for real-time hazard detection, validating infrastructure readiness. Wi-Fi and Wi-Fi HaLow remain vital for software updates in stationary scenarios and for in-vehicle media sharing, yet coverage gaps constrain their mobility utility. Bluetooth and BLE connect personal devices and sensor clusters, complementing cellular uplinks, while satellite back-up channels provide resilience in remote zones.

The Automotive IoT market size linked to 5G is reinforced by regulatory and safety targets: cooperative adaptive cruise control and automated lane merge need network reliability levels currently achievable only over licensed cellular spectrum. As network slicing matures, automakers can reserve deterministic bandwidth for mission-critical services, opening new monetization avenues tied to quality-of-service differentiated tariffs.

Geography Analysis

North America maintains clear leadership with a 39.45% Automotive IoT market share in 2024. Mature 5G coverage, consumer acceptance of subscription models and robust data-governance frameworks underpin adoption. Automaker–tech coalitions such as the high-power charging venture involving BMW, General Motors, Hyundai and others demonstrate a coordinated infrastructure approach that shortens go-to-market cycles for new data services. Policy focus is intensifying on privacy; the proposed Auto Data Privacy and Autonomy Act would require explicit consent for cross-border data transfers, compelling OEMs to reinforce encryption and in-country processing. These measures ensure trust yet raise compliance costs that only large platforms can absorb, favoring incumbents.

Asia-Pacific is the fastest-growing region, posting a 21.78% CAGR through 2030. China’s new energy vehicle penetration exceeds 40% of light-vehicle sales and every model must log data to government servers for over-the-air diagnostics. Trade-in subsidies and value-added tax rebates further accelerate replacement cycles. India is preparing to tie Bharat NCAP safety stars to connectivity readiness, which may include V2X handling metrics. Localized telematics service providers are emerging to navigate pricing sensitivities while leveraging fast-growing 4G+ networks. Regional OEMs such as BYD and SAIC integrate IoT gateways at bill-of-materials parity with legacy head units, confirming structural cost advantages that amplify Automotive IoT market momentum.

Europe ranks third in revenue but sets global regulatory tone. The eCall mandate created baseline connectivity while the upcoming Data Act clarifies ownership, potentially unlocking third-party service ecosystems. Suppliers like FORVIA are coupling with Asian OEMs to establish assembly hubs in Hungary, ensuring localized production of IoT-equipped cockpits for export across the EU. Cybersecurity certification under UNECE WP.29 forces continuous patch management, pushing software-update capabilities to the fore. Although overall vehicle sales remain flat, higher attach rates for premium connected options keep the Automotive IoT market expanding steadily.

Competitive Landscape

The Automotive IoT market is moderately fragmented yet consolidating as software scale economics intensify. Qualcomm’s 2025 purchase of Autotalks folded production-ready V2X chipsets into its Snapdragon Digital Chassis portfolio, tightening its grip on vehicular connectivity layers. Lear acquired WIP Industrial Automation to blend robotics with cabin electronics, signalling ambition to own end-to-end cockpit domain control. Such moves illustrate how hardware firms are absorbing niche specialists to deliver turnkey stacks spanning silicon, middleware and cloud analytics.

Strategic partnerships proliferate when competencies are complementary. Honda, Nissan and Mitsubishi formed a research pact covering battery management, e-Axles and scalable software-defined vehicle platforms, spreading R&D burden and accelerating road-map convergence. Cloud providers, cybersecurity startups and telecom operators frequently co-market joint offerings, blurring industry lines. Meanwhile, vertical integrators like Tesla and Chinese NEV entrants hold cost and update-velocity advantages due to direct software pipelines, compelling legacy OEMs to reconsider outsourcing norms.

White-space niches include OTA security orchestration and AI-driven data monetization dashboards. New entrants must navigate stringent safety audits and the long homologation timelines unique to automotive. Consequently, market power is gravitating toward entities that command both horizontal (cross-OEM) scale and vertical (chip-to-cloud) integration, reshaping the competitive chessboard of the Automotive IoT market.

Automotive IoT Industry Leaders

Robert Bosch GmbH

Continental AG

Denso Corporation

Aptiv plc

Harman International Industries Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Uber committed USD 300 million to Lucid Motors for 20,000 robotaxis integrating Nuro’s Level 4 autonomy.

- July 2025: Standard Motor Products acquired Kade Trading GmbH to bolster European thermal systems for EVs.

- June 2025: Qualcomm finalized its Autotalks takeover, adding dual-mode DSRC/C-V2X chipsets to its digital chassis.

- December 2024: Honda and Nissan unveiled a merger plan with Honda assuming control to pool EV and IoT R&D resources.

Global Automotive IoT Market Report Scope

| Hardware |

| Software |

| Services |

| Embedded |

| Tethered |

| Integrated |

| Telematics |

| Infotainment and In-Car Services |

| Advanced Driver Assistance Systems (ADAS) and Safety |

| Fleet Management |

| Predictive Maintenance |

| Cellular (3G/4G/5G) |

| Wi-Fi / Wi-Fi HaLow |

| Bluetooth / BLE |

| Satellite and GNSS |

| NFC and UWB |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Connectivity Form | Embedded | ||

| Tethered | |||

| Integrated | |||

| By Application | Telematics | ||

| Infotainment and In-Car Services | |||

| Advanced Driver Assistance Systems (ADAS) and Safety | |||

| Fleet Management | |||

| Predictive Maintenance | |||

| By Network Technology | Cellular (3G/4G/5G) | ||

| Wi-Fi / Wi-Fi HaLow | |||

| Bluetooth / BLE | |||

| Satellite and GNSS | |||

| NFC and UWB | |||

| by Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current Automotive IoT market size and growth outlook?

The Automotive IoT market size is USD 189.87 billion in 2025 and is projected to reach USD 441.67 billion by 2030, expanding at an 18.39% CAGR.

Which component segment is growing fastest within the Automotive IoT market?

Services, including data subscriptions and OTA updates, are rising at a 20.94% CAGR, outpacing hardware and software components.

Why are embedded connectivity solutions favored by automakers?

Embedded modems hold 51.34% share because they deliver seamless connectivity, tighter security and OEM control over data without relying on customer smartphones.

What factors drive Asia-Pacific’s rapid Automotive IoT market expansion?

Aggressive electric-vehicle adoption in China, government-mandated connectivity rules and growing manufacturing scale push Asia-Pacific to a 21.78% CAGR through 2030.

How are chip shortages impacting Automotive IoT deployments?

Supply-chain disruptions have inflated component costs by up to 30% and forced features deletions, temporarily tempering growth until new fabrication capacity comes online.

Which network technology underpins future Automotive IoT services?

5G cellular, supported by edge computing, provides the low-latency, high-reliability links necessary for real-time V2X and autonomous driving applications.

Page last updated on: