Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

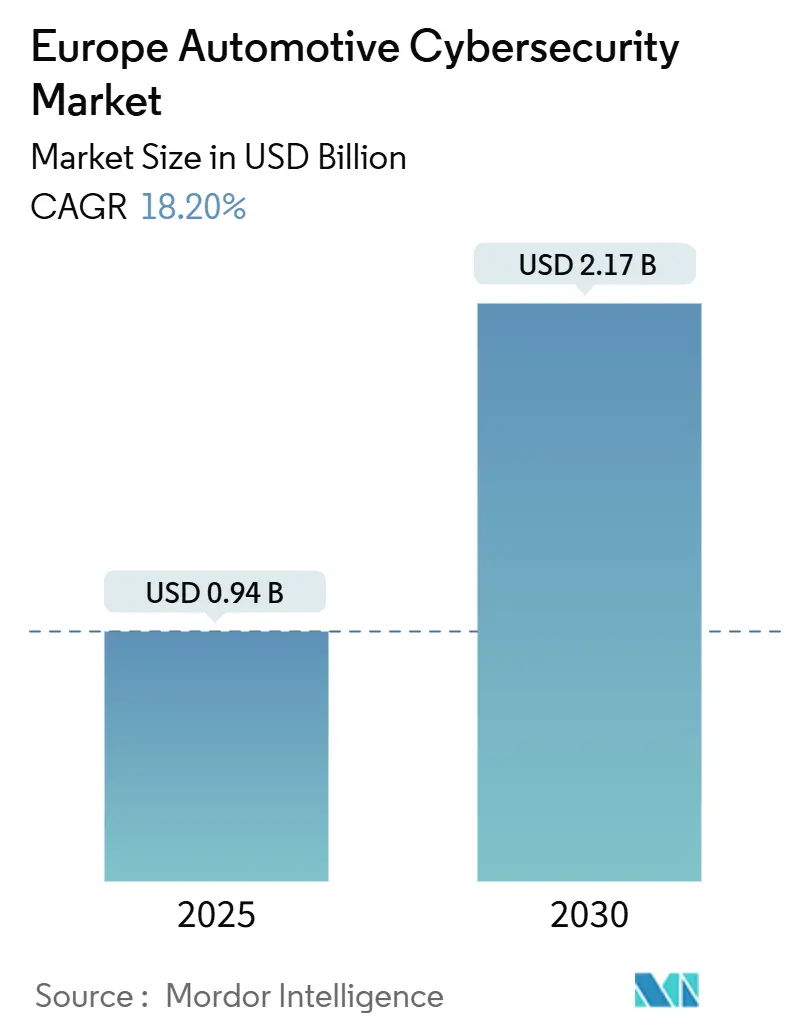

| Market Size (2025) | USD 0.94 Billion |

| Market Size (2030) | USD 2.17 Billion |

| Growth Rate (2025 - 2030) | 18.20% CAGR |

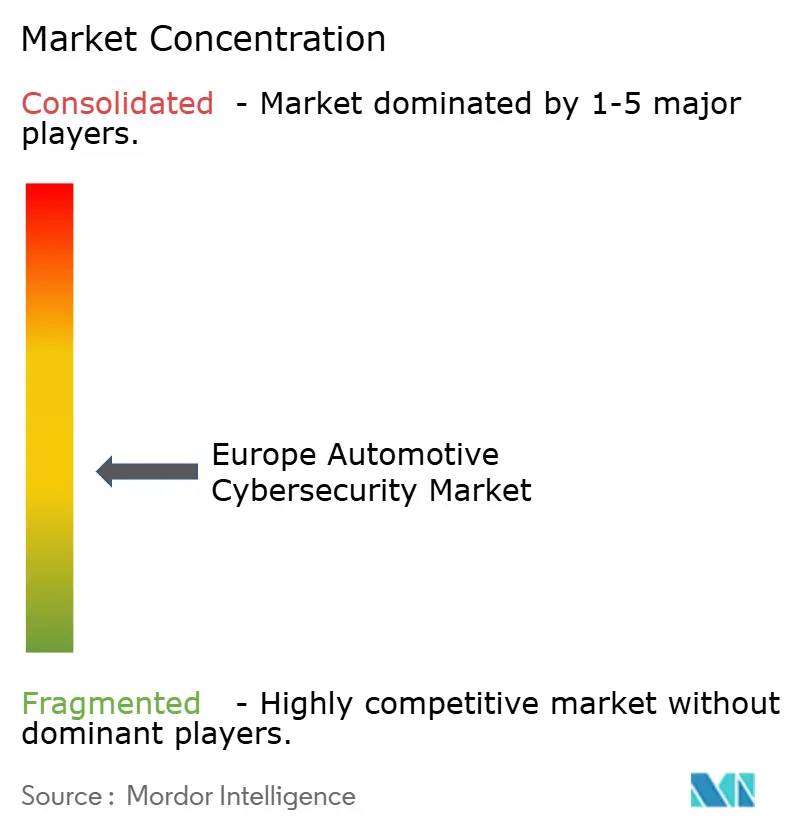

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automotive Cybersecurity Market Analysis by Mordor Intelligence

The Europe Automotive Cybersecurity Market size is estimated at USD 0.94 billion in 2025, and is expected to reach USD 2.17 billion by 2030, at a CAGR of 18.20% during the forecast period (2025-2030).

Rising vehicle digitization, mandatory UN R155 compliance from July 2024, and the broader EU Cyber Resilience Act are reshaping security architectures across the automotive value chain. Automakers must now embed security-by-design principles, maintain software update management systems, and prove continuous risk monitoring to gain type approval. The shift toward software-defined vehicles expands the threat surface, driving demand for comprehensive end-to-end cloud, network, and endpoint protection. Tier-1 suppliers expand their security portfolios, while specialized vendors introduce AI-driven threat intelligence and automated incident-response tools to help OEMs address post-quantum migration, over-the-air (OTA) update validation, and vehicle-to-everything (V2X) communication risks.

Key Report Takeaways

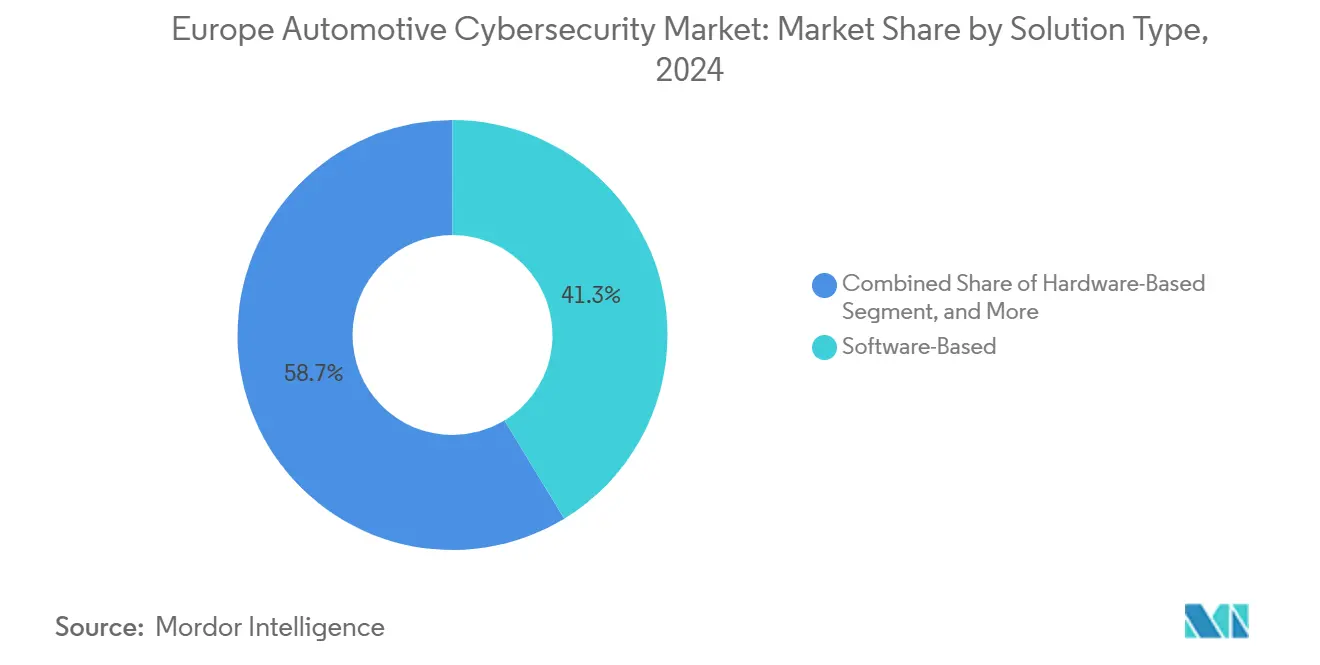

- By solution type, software accounted for 41.3% of the Europe automotive cybersecurity market share in 2024; systems integration is projected to grow at an 18.5% CAGR through 2030.

- By security domain, network security led with a 39.3% revenue share in 2024, whereas cloud and OTA security are advancing at a 20.3% CAGR.

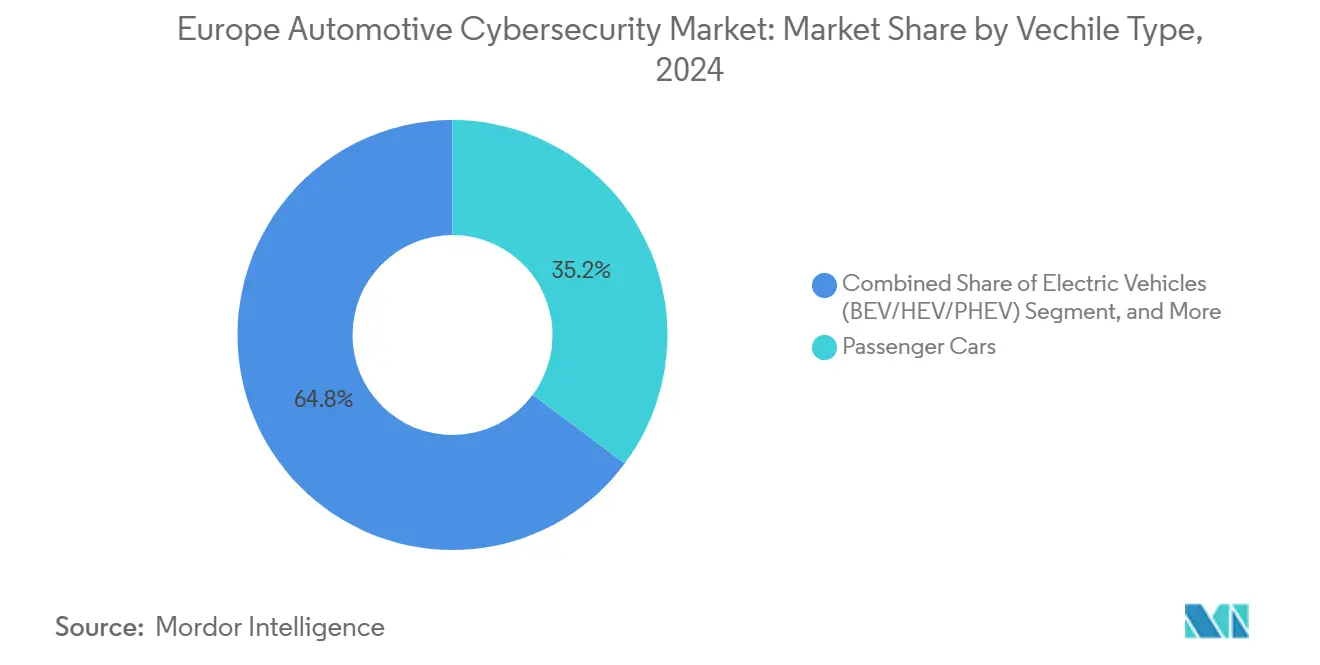

- By vehicle type, passenger cars accounted for 35.2% of the Europe automotive cybersecurity market size in 2024, while electric vehicles are expected to expand at a 20.7% CAGR between 2025 and 2030.

- By application, telematics and connectivity held 27.5% of the Europe automotive cybersecurity market size in 2024, while ADAS and Safety are set to expand at a 19.5% CAGR between 2025 and 2030.

- By country, Germany commanded a 34.1% share of the Europe automotive cybersecurity market in 2024; Italy showed the quickest growth at an 18.9% CAGR.

Europe Automotive Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU UNECE WP.29 and ISO/SAE 21434 compliance deadlines | +4.2% | Europe-wide, with Germany and France leading implementation | Short term (≤ 2 years) |

| Rapid proliferation of connected and V2X-enabled cars | +3.8% | Global with European focus on ETSI ITS-G5 and C-V2X standards | Medium term (2-4 years) |

| Increasing OTA software-update penetration | +3.1% | Europe and North America, with Nordic countries as early adopters | Medium term (2-4 years) |

| EV and autonomous-driving rollout raises attack surface | +2.9% | Europe-wide, concentrated in Germany, Norway, Netherlands | Long term (≥ 4 years) |

| Cyber-security-as-a-service revenue models for OEMs | +2.4% | Europe and North America, premium segments first | Long term (≥ 4 years) |

| Fleet-leasing cyber-insurance mandates | +1.8% | Europe, particularly UK and Germany commercial fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU UNECE R155 and ISO/SAE 21434 compliance deadlines

The July 2024 full-market enforcement of UN R155 compels all newly registered vehicles to prove an operational cybersecurity management system. ISO/SAE 21434 supplies the engineering blueprint, obliging OEMs to document threat analysis, risk assessment, and mitigation from concept through decommissioning.[1]United Nations Economic Commission for Europe, “UN Regulation No 155,” unece.org Harmonization across 54 contracting parties reduces duplication costs, yet necessitates restructuring of the development process and spurs immediate demand for audit, penetration testing, and CSMS orchestration platforms.

Rapid proliferation of connected and V2X-enabled cars

Mandatory advanced driver assistance systems under the European General Safety Regulation and smart mobility programs, such as Talking Traffic (Netherlands), accelerate the adoption of ETSI ITS-G5 and C-V2X radio stacks. Interoperability gaps between the two protocols necessitate multi-layer network security appliances that can safeguard simultaneous links.[2]CAR 2 CAR Communication Consortium, “C-ITS FAQs,” car-2-car.orgReal-time vehicular fog-computing trials have already cataloged 33 discrete threat vectors, reinforcing OEM interest in unified, AI-assisted intrusion-detection engines.

Increasing OTA software-update penetration

UN R156 requires manufacturers to maintain a software update management system in conjunction with cyber-risk monitoring. However, an Oxford study found 84% of European charging stations lacked TLS, leaving OTA channels exposed to man-in-the-middle attacks.[3]University of Oxford, “Security Measurement Study of CCS EV Charging Deployments,” arxiv.orgOEMs now seek end-to-end encryption, code signing, version control, and rollback protection services, driving the uptake of cloud-native security platforms that verify every binary before deployment.

EV and autonomous-driving rollout raises attack surface

ISO 15118-20 enables plug-and-charge but also introduces new certificate-handling complexities; only 12% of analyzed European chargers implement the protocol securely. Simultaneously, AI-centric autonomous stacks require continual model updates, multiplying OTA cycles. Security vendors respond with embedded hardware root-of-trust, battery-management systems, firewalls, and attack-simulation labs that stress-test perception algorithms against adversarial inputs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and long validation cycles for certifiable solutions | -2.8% | Europe-wide, particularly affecting SME suppliers | Short term (≤ 2 years) |

| Shortage of skilled automotive-security engineers | -2.1% | Europe-wide, most acute in Germany and Nordic countries | Medium term (2-4 years) |

| Liability-fragmentation across multi-tier supply chain | -1.6% | Europe and North America, complex in cross-border operations | Medium term (2-4 years) |

| Looming post-quantum crypto uncertainty | -1.3% | Global, with early impact on long-lifecycle automotive products | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost and long validation cycles for certifiable solutions

Achieving third-party certification under UN R155 routinely stretches development timelines 18-24 months and demands six-figure USD budgets per vehicle line. Smaller suppliers risk market exit or consolidation because they cannot amortize test-bench, pen-test, and documentation costs across large volumes. The looming need to recertify every control unit for post-quantum algorithms before the 2035 NIST cut-off compounds expenditure.

Shortage of skilled automotive-security engineers

The EU recorded a 299,000-person cybersecurity shortfall in 2024, with automotive expertise particularly scarce. Germany alone forecasts a gap of 106,000 specialists by 2026. Complex cross-domain skillsets, combining CAN-FD, AUTOSAR, cloud SecOps, and regulatory know-how, lengthen recruitment cycles, raising labor costs and delaying project delivery despite initiatives such as the Cybersecurity Skills Academy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Software Dominance Drives Integration

Software platforms captured 41.3% of the Europe automotive cybersecurity market share in 2024. Systems-integration spending will post an 18.5% CAGR through 2030 as OEMs transition from discrete countermeasures to lifecycle orchestration. The Europe automotive cybersecurity market size linked to integration services is projected to add USD 386 million by 2030, reflecting demand for end-to-end DevSecOps pipelines, digital twins, and security operations center (SOC) outsourcing.

Hardware security modules (HSMs) and secure gateways remain vital for cryptographic acceleration and domain isolation, but represent a niche growth path. Professional services revenue grows steadily because audit, certification, and red-teaming remain mandatory for each vehicle variant. Vendors such as VicOne integrate threat-intelligence feeds into popular CI/CD environments, letting developers flag vulnerabilities during code check-in rather than after deployment.

By Security Domain: Network Security Leads Cloud Migration

Network security suites accounted for 39.3% of the revenue in 2024, driven by in-vehicle Ethernet firewalls, CAN anomaly detection, and secure diagnostics. Yet, cloud and OTA security will surge at a 20.3% CAGR as centralized data lakes and fleet-wide patching become dominant in OEM strategies. The Europe automotive cybersecurity market size attached to cloud controls is anticipated to reach USD 524 million by 2030.

Endpoint defenses remain critical for infotainment and telematics units that expose third-party apps. Emerging domains include vehicle-to-grid encryption and post-quantum VPN tunnels safeguarding predictive-maintenance telemetry. Continental’s planned acquisition of Motorola Electronics underscores how incumbents expand from hardware gatekeepers to full-stack cloud security providers.

By Vehicle Type: Electric Vehicles Accelerate Security Demand

Passenger cars represented 35.2% of 2024 deployments, but electric vehicles will register a 20.7% CAGR through 2030 as charging-network vulnerabilities widen the risk matrix. EV-specific spending within the Europe automotive cybersecurity market is forecast to nearly triple, supported by the rollout of ISO 15118 certificate-authority systems and battery-management intrusion-detection systems.

Light-commercial fleets adopt cybersecurity more quickly than heavy trucks because leasing firms often include coverage in their insurance policies. Heavy-commercial platforms face longer refresh cycles yet must secure logistics APIs and over-the-air parameter updates for digital tachographs.

By Application: ADAS Safety Systems Drive Growth

Telematics and connectivity modules commanded 27.5% of 2024 revenues. ADAS and safety applications are expected to expand at a 19.5% CAGR, thereby increasing their contribution to the Europe automotive cybersecurity market size as Level 2+ autonomy gains mainstream traction. Malware-resilient perception stacks, sensor-fusion integrity checks, and fail-operational fallback paths underpin investment.

Infotainment security remains a persistent necessity given consumer app ecosystems, while powertrain control units migrate to domain controllers that consolidate hundreds of legacy ECUs driving encrypted intra-domain messaging and secure boot mandates. Charging infrastructure and V2G protections form a nascent but rapidly growing segment due to smart-grid integration.

Geography Analysis

Germany’s 34.1% revenue share in 2024 stems from its role as an OEM hub, regulatory stewardship, and strong R&D investment. Bosch alone spent EUR 7.3 billion (USD 8.47 billion) on innovation in 2024. Italy’s Europe automotive cybersecurity market is expected to grow at a 18.9% CAGR, driven by the digitization of luxury brands and favorable public funding incentives. France follows, leveraging national cybersecurity strategies and its semiconductor ecosystem.

The United Kingdom remains aligned with UNECE, despite Brexit, and continues to craft parallel homologation to preserve exportability. Nordic states act as early adopters for OTA and V2G pilots, shaping pan-European best practices. Eastern Europe diversifies production footprints and gradually onboards CSMS capabilities, providing greenfield opportunities for service providers.

Competitive Landscape

The Europe automotive cybersecurity market is moderately fragmented. Continental, Bosch/ESCRYPT, and Infineon hold a significant share of the 2024 revenue, leveraging their scale, homologation expertise, and embedded-control portfolios to secure OEM contracts. Continental’s May 2025 purchase of Motorola’s automotive electronics arm broadens its stack from gateways to cloud analytics, indicating horizontal consolidation.

Pure-play vendors, such as Argus, Karamba, and VicOne, differentiate themselves via AI-centric detection, binary-level hardening, and DevSecOps pipelines. VicOne’s August 2025 pact with Panasonic embeds xCarbon in cockpit systems, demonstrating how specialized firms integrate within Tier-1 subsystems while jointly marketing UN R155-ready solutions. Upstream pairs fleet telematics data with Ocean AI to automate anomaly triage, partnering with Google Cloud to scale inference workloads.

Post-quantum migration acts as a disruptive equalizer. Incumbents must redesign HSMs and VPNs, while startups focusing on lattice-based cryptography or quantum-random-number generation may leapfrog legacy architectures. Strategic alliances, such as VicOne-Microsoft and Upstream-OTORIO, signal a pivot toward platform ecosystems that span design, manufacturing, and in-use monitoring.

Europe Automotive Cybersecurity Industry Leaders

IBM Corporation

Cisco Systems Inc

Visteon Corporation

Continental AG

Escrypt GmbH (ETAS/Bosch)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: VicOne and Panasonic Automotive Systems expanded integrated cockpit-security offerings, completing Automotive Grade Linux reference validation.

- May 2025: Continental AG agreed to acquire Motorola’s automotive-electronics business, enlarging its cybersecurity footprint.

- May 2025: VicOne introduced xAurient, an AI-powered automotive threat-intelligence platform enabling on-demand investigations.

- February 2025: Upstream Security launched Ocean AI to accelerate complex cyber-attack forensics for connected fleets.

Europe Automotive Cybersecurity Market Report Scope

The scope of the study characterizes the European market for cybersecurity of cars, based on the type of solution, which includes software-based, hardware-based, professional service, Integration, and security that includes network security, application security, cloud security. The study also includes the assessment of the impact of COVID-19 on the market.

The europe automotive cybersecurity market report is segmented by solution type (software-based, hardware-based, professional services, systems integration, solution type), security domain (network security, application/endpoint security, cloud and over-the-air security, other security domains), vehicle type (passenger cars, light commercial vehicles, heavy commercial vehicles, electric vehicles (BEV/HEV/PHEV)), application (infotainment, telematics and connectivity, powertrain/propulsion control, ADAS and safety, charging infrastructure and V2G), and Country (Germany, France, United Kingdom, Italy, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Solution Type

| Software-Based |

| Hardware-Based |

| Professional Services |

| Systems Integration |

| Other Solution Type |

By Security Domain

| Network Security |

| Application/Endpoint Security |

| Cloud and Over-the-Air Security |

| Other Security Domain |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Electric Vehicles (BEV/HEV/PHEV) |

By Application

| Infotainment |

| Telematics and Connectivity |

| Powertrain/Propulsion Control |

| ADAS and Safety |

| Charging Infrastructure and V2G |

By Country

| Germany |

| France |

| United Kingdom |

| Italy |

| Rest of Europe |

| By Solution Type | Software-Based |

| Hardware-Based | |

| Professional Services | |

| Systems Integration | |

| Other Solution Type | |

| By Security Domain | Network Security |

| Application/Endpoint Security | |

| Cloud and Over-the-Air Security | |

| Other Security Domain | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| Electric Vehicles (BEV/HEV/PHEV) | |

| By Application | Infotainment |

| Telematics and Connectivity | |

| Powertrain/Propulsion Control | |

| ADAS and Safety | |

| Charging Infrastructure and V2G | |

| By Country | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the European automotive cybersecurity market by 2030?

The market is forecast to reach USD 2.17 billion by 2030 at an 18.20% CAGR.

Which solution segment is growing the fastest?

Systems integration services are expanding at an 18.5% CAGR as OEMs pursue holistic security orchestration.

Why is Germany the largest national market?

Germany combines a dense OEM base, proactive BSI guidance and significant supplier R&D investment, giving it a 34.1% share in 2024.

How will post-quantum cryptography affect automotive cybersecurity?

All control units must migrate to quantum-safe algorithms before 2035, triggering recertification cycles and new revenue streams for security vendors.

Page last updated on: