Aviation Cyber Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

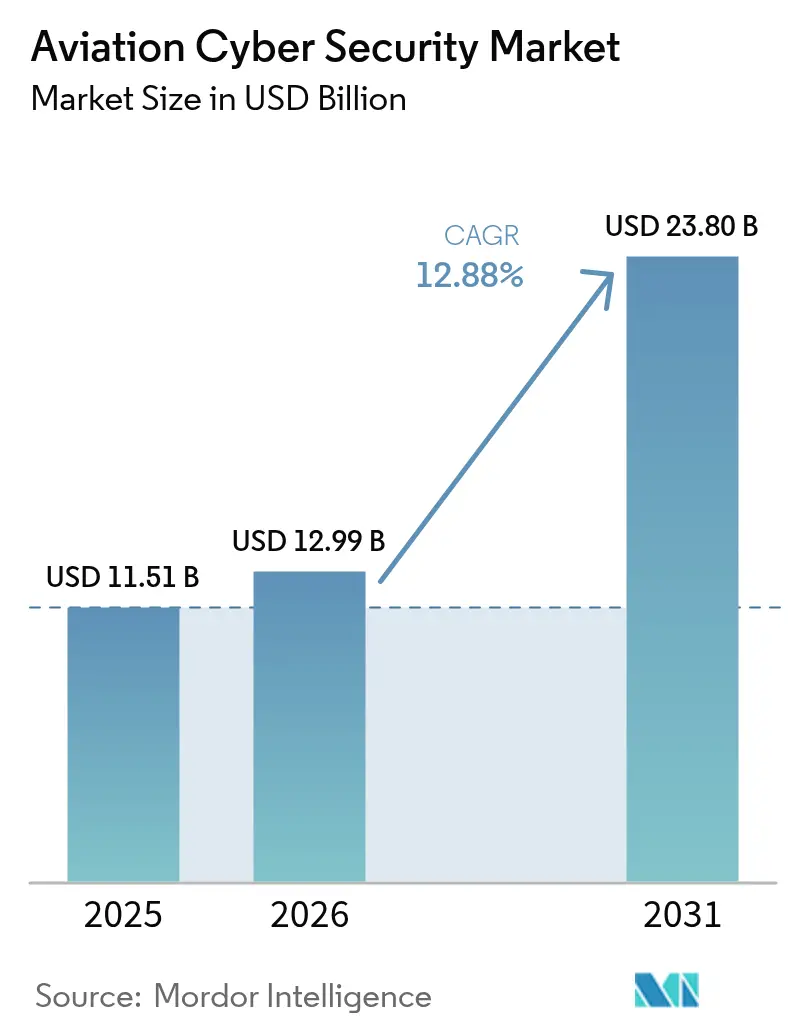

| Market Size (2026) | USD 12.99 Billion |

| Market Size (2031) | USD 23.8 Billion |

| Growth Rate (2026 - 2031) | 12.88% CAGR |

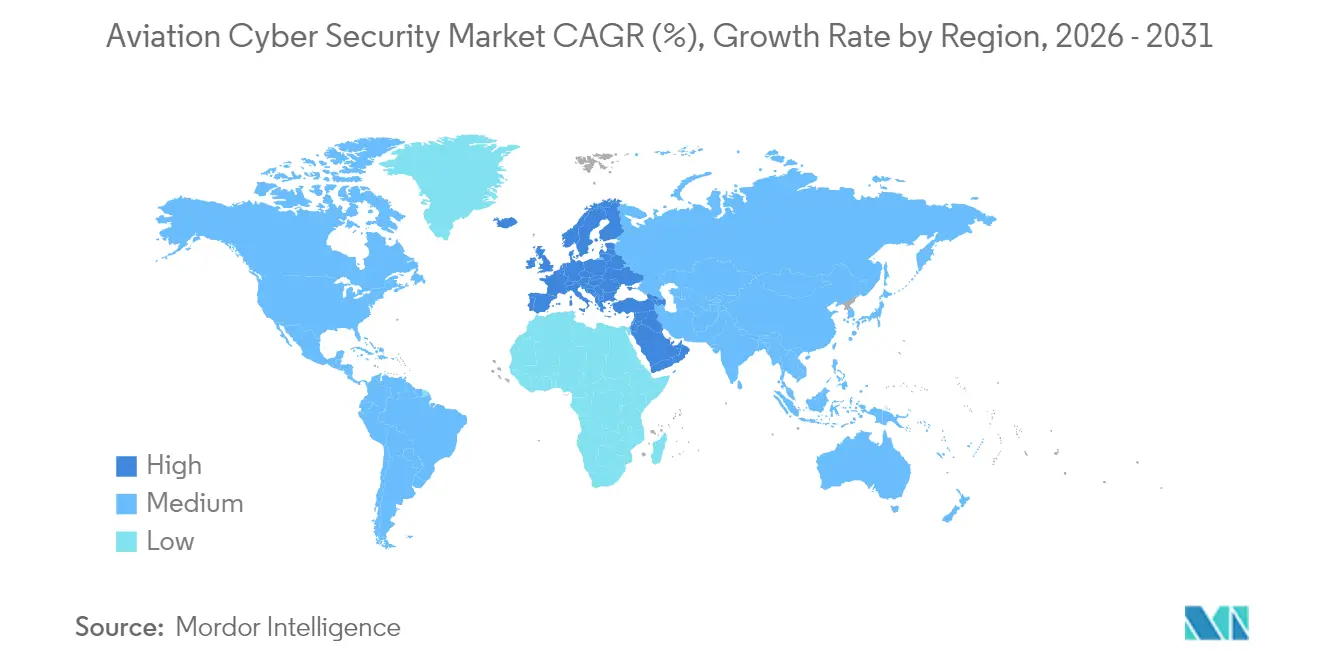

| Fastest Growing Market | Middle East |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aviation Cyber Security Market Analysis by Mordor Intelligence

Aviation cyber security market size in 2026 is estimated at USD 12.99 billion, growing from 2025 value of USD 11.51 billion with 2031 projections showing USD 23.8 billion, growing at 12.88% CAGR over 2026-2031. Rising cyber-attack frequency since 2020, rapid cloud migration, and the surge of connected assets across airports, aircraft, and air traffic control (ATC) systems underpin this expansion. North American regulatory funding, European harmonized rules, and Middle-Eastern infrastructure build-outs collectively elevate spending levels. Technology priorities are shifting toward zero-trust architectures, managed detection-and-response services, and quantum-safe encryption, while operators pursue outsourcing to address the sector’s persistent shortage of aviation-domain security talent. Intensifying merger activity among incumbents and niche vendors aims to close capability gaps in operational-technology (OT) protection, threat intelligence, and compliance automation across the aviation cyber security market.

Key Report Takeaways

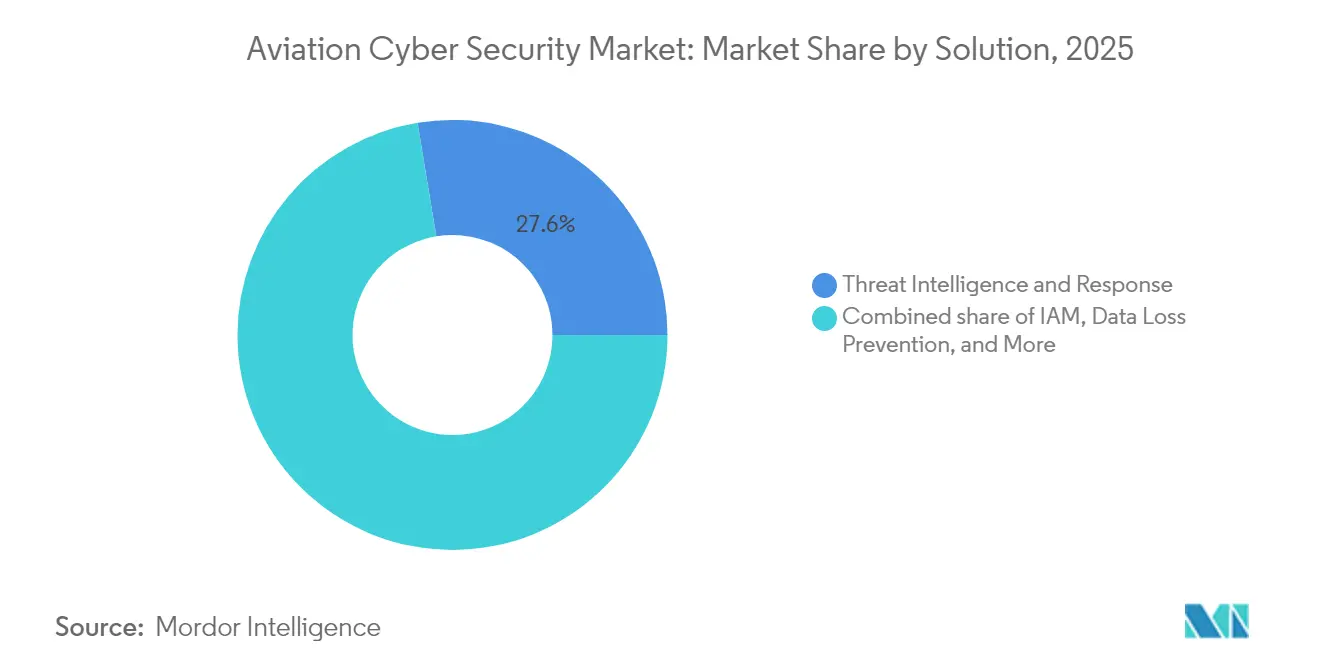

- By solution: Threat Intelligence & Response held 27.60% of 2025 revenue; Managed Security Services deliver the fastest growth at 13.4% CAGR as operators outsource specialized expertise.

- By security type: Network Security commanded 31.60% of the aviation cyber security market share in 2025, while Cloud Security is advancing at a 14.7% CAGR on the back of hybrid-cloud adoption.

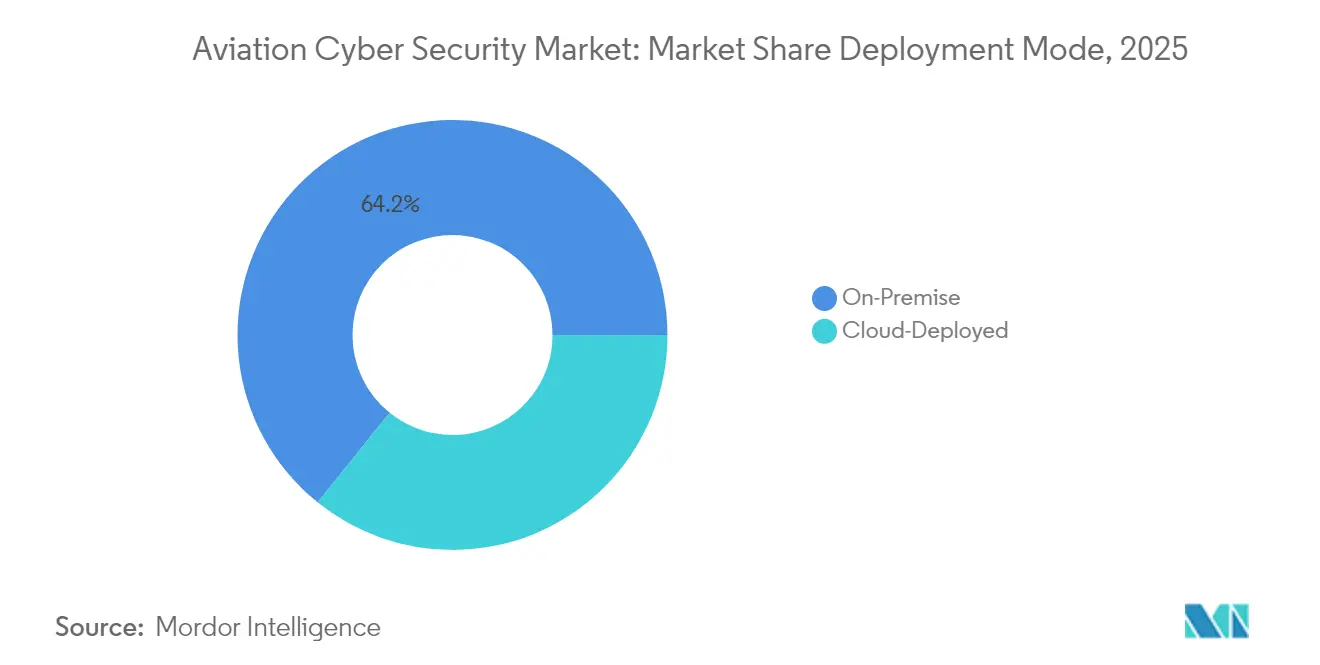

- By deployment: On-Premise held 64.20% of 2025 revenue; Cloud deliver the fastest growth at 16.8% CAGR due to increasing third-party demand.

- By application: Airport Management led with 34.40% revenue in 2025, whereas Air Traffic Control Management is forecast to expand at a 13.8% CAGR through 2031, reflecting accelerated ATC modernization within the aviation cyber security market size.

- By region: North America accounted for 39.40% of 2025 revenue, whereas the Middle East registers the highest regional CAGR of 13.05% to 2031, mirroring large-scale airport investments and rising threat intensity.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aviation Cyber Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Integrated Digital Aviation Ecosystems Expanding Cyber-Attack Surface | +2.8% | Global, with concentrated impact in North America & Europe | Medium term (2-4 years) |

| Rapid Adoption of Open Architecture Avionics & IoT Sensors in Aircraft Fleets | +2.1% | North America & APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Growth in Cloud-Based Airport Operations Platforms & SaaS Flight Applications | +1.9% | Global, early adoption in North America & EU | Short term (≤ 2 years) |

| Integration of 5G & Satellite Connectivity in ATC Networks Requiring Zero-Trust Security | +1.7% | APAC core, expanding to North America & Europe | Medium term (2-4 years) |

| Rise of eVTOL & Urban Air Mobility Operators Implementing Security-by-Design | +1.4% | North America & Europe, pilot programs in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Integrated Digital Aviation Ecosystems Expanding Cyber-Attack Surface

The convergence of passenger services, airport OT, aircraft data links, and third-party logistics is redefining the aviation cyber security market. In August 2024 a Port of Seattle breach brought down peripheral systems, demonstrating how lateral movement can disrupt operations even when flight safety is maintained.[1]Port of Seattle, “Cyber Incident Update August 2024,” portseattle.org US Transportation Security Administration allocated USD 136.17 million toward aviation-focused cyber defenses for FY 2025, signaling that perimeter-centric strategies are no longer sufficient.[2]Transportation Security Administration, “FY 2025 Budget Request,” dhs.gov Stakeholders now prioritize holistic architectures that map and secure interdependencies across the entire aviation cyber security market.

Rapid Adoption of Open-Architecture Avionics & IoT Sensors in Aircraft Fleets

Open standards cut lifecycle costs and enable plug-and-play upgrades, yet they propagate identical vulnerabilities across fleets. The FAA’s August 2024 proposal underscores risks from maintenance laptops, airport Wi-Fi, and Bluetooth sensors that can pivot to flight-critical domains. CISA advisories exposing flaws in collision-avoidance transponders add urgency[3]Cybersecurity and Infrastructure Security Agency, “ICS Advisory ICSA-24-245-01,” cisa.gov . Airlines and OEMs thus must blend secure-coding practices with runtime monitoring to mitigate systemic exposure within the aviation cyber security market.

Growth in Cloud-Based Airport Operations Platforms & SaaS Flight Applications

Cloud migration reorients defenses toward identity, encryption, and real-time analytics. SITA’s 2024 airline survey shows 77% of North American carriers ranking cybersecurity top-three, with 82% deploying AI in cloud threat detection. Hybrid estates mix legacy mainframes with container-based micro-services, forcing operators to reconcile disparate trust models inside the aviation cyber security market.

Integration of 5G & Satellite Connectivity in ATC Networks Requiring Zero-Trust Security

The switch to IP-based voice and data links modernizes ATC but also broadens attack vectors. FAA National Airspace modernization mandates zero-trust for ground-to-air links. EUROCONTROL’s CERT recorded a 530% jump in airline cyber incidents between 2019 and 2020, reinforcing the case for continuous authentication and micro-segmentation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Legacy Systems Hindering Unified Security Governance | -1.8% | Global, particularly acute in North America & Europe | Medium term (2-4 years) |

| Shortage of Aviation-Domain Cyber-Security Specialists in Emerging Markets | -1.5% | APAC & MEA core, with spillover to Latin America | Long term (≥ 4 years) |

| High Certification & Air-Worthiness Validation Costs Delaying Deployments | -1.2% | Global, with regulatory complexity in North America & EU | Long term (≥ 4 years) |

| Limited Budget Allocation Among Regional & General Aviation Airports | -0.9% | Global, particularly acute in emerging markets & rural regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Legacy Systems Hindering Unified Security Governance

Defense Industrial Base studies find that 98% of aviation organizations sustain supply-chain partnerships hit by cyber incidents, propagating risk across decades-old ATC and baggage networks. Encryption, multifactor authentication, and centralized logging remain absent from many legacy nodes, forcing airlines to juggle redundant controls that inflate cost while leaving material gaps.

High Certification & Air-Worthiness Validation Costs Delaying Deployments

Even incremental patches must pass stringent air-worthiness reviews. EASA Part-IS, effective October 2025, obliges operators to certify ISO/IEC 27001-aligned information-security management systems, extending project cycles and resource demand. Smaller airports defer upgrades, creating a two-speed aviation cyber security industry and slowing overall momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Managed Security Services Drive Operational Efficiency

Threat Intelligence & Response solutions captured 27.60% of 2025 revenue within the aviation cyber security market share, evidencing the sector’s pivot to proactive monitoring. Managed Security Services exhibit a 13.4% CAGR through 2031. This momentum stems from a limited pool of aviation-literate analysts and the need to meet 24×7 regulatory logging mandates without inflating internal headcount.

OEMs and airlines turn to managed offerings that bundle SIEM, OT anomaly detection, and compliance dashboards. The aviation cyber security market size for managed services is forecast to increase in tandem with mandatory incident-reporting timelines and zero-trust rollouts. Vendor differentiation now centers on possessing flight-certified engineers able to integrate with avionics and ATC workflows rather than generic SOC staffing models.

By Security Type: Cloud Security Transformation Accelerates

Network Security retained 31.60% of 2025 spend, underlining residual reliance on perimeter firewalls. Yet Cloud Security leads growth at a 14.7% CAGR as multi-cloud, containerized workloads move passenger check-in, crew rostering, and predictive maintenance off-premise. The aviation cyber security market size for cloud controls benefits from shared-responsibility education campaigns and the rollout of sovereign-cloud regions tailored for regulated sectors.

Endpoint protection stretches from crew tablets to engine-health sensors, compelling vendors to unify policy engines across distinct hardware. Application-level firewalls, API gateways, and runtime code-scanning also accelerate because SaaS flight-planning tools must pass both cyber and safety audits before release in the aviation cyber security market.

By Deployment Mode: Cloud Migration Reshapes Security Architecture

On-premise deployments still account for 64.20% of 2025 outlays as safety-critical workloads remain physically controlled for regulatory reasons. However, cloud-deployed solutions rise at 16.8% CAGR. Airlines are orchestrating phased migrations: loyalty programs and revenue accounting first, followed by maintenance analytics once data-sovereignty workflows mature. This staged approach reduces business-continuity risk while enabling proof-of-concept zero-trust pilots central to the aviation cyber security industry.

Hybrid topologies require encrypted tunnels and consistent identity brokering between airport data centers and hyperscale clouds. Vendors offering unified policy orchestration across these planes gain share, and the aviation cyber security market continues to pivot toward platforms that visualize risk posture across land-side, air-side, and cloud domains in a single console.

By Application: Air Traffic Control Modernization Drives Growth

Airport Management claimed 34.40% of 2025 sector revenue. Passenger self-service kiosks, baggage IoT tags, and building-automation systems create vast OT exposure, compelling asset-inventory and micro-segmentation projects. ATC, while smaller, shows the fastest 13.8% CAGR as legacy radar, VHF, and proprietary data buses give way to IP-based exchanges. The aviation cyber security market size allocated to ATC upgrades will accelerate as national air-navigation service providers unlock modernization grants.

Airline Management platforms integrate AI flight-disruption mitigation and fuel-optimization modules, making API security critical. Air Cargo Management gains priority as cross-border e-commerce expands, elevating requirements for blockchain-anchored chain-of-custody logs and continuous compliance scanning across the aviation cyber security market.

Geography Analysis

North America leads the aviation cyber security market with 39.40% revenue in 2025, underpinned by the FAA’s USD 35 million cybersecurity line item for FY 2026 and TSA’s USD 136.17 million allocation to harden airports. All major U.S. carriers now embed AI-driven threat detection, and Canadian ANSP NAV CANADA adopts zero-trust blueprints mirroring federal best practices. The region’s vendor ecosystem also benefits from defense primes cross-selling hardened solutions into commercial fleets.

Europe maintains robust adoption through EASA Part-IS and EUROCONTROL CERT coordination. Pan-EU harmonization reduces duplication and increases pooled intelligence sharing. Thales’ three-year AI partnership with CEA to develop trusted GenAI for defense highlights regional innovation targeted at detection-and-response acceleration. GDPR adds another compliance dimension, prompting privacy-by-design encryption and tokenization efforts inside the aviation cyber security market.

The Middle East posts a 13.05% CAGR driven by Gulf hub expansion and a documented 183% DDoS spike during Q1 2024, pushing operators to secure multi-airport portfolios rapidly. Flag carriers in the region now mandate managed SOC coverage for ground systems and deploy satellite-route diversity to counter spoofing attempts. Asia-Pacific, led by China, Japan, and India, follows close behind through large-scale fleet additions, government smart-airport grants, and the region’s first ministerial aviation-cyber summit hosted in Delhi in September 2024. Diverse regulatory baselines encourage both international vendors and regional specialists to localize offerings for different certification regimes.

Competitive Landscape

The aviation cyber security market remains moderately fragmented. Aerospace giants such as Honeywell, Thales, and Collins Aerospace leverage embedded-systems know-how and long-standing OEM relationships to cross-sell cyber suites. Honeywell’s USD 52 million purchase of SCADAfence in April 2024 adds OT-visibility analytics that map well to airport building-management systems. Cisco and Palo Alto Networks pursue partnerships with airport integrators to embed next-generation firewalls and SOC-as-a-service offerings compliant with FAA and EASA audit processes.

Acquisition momentum is expected to accelerate as prime contractors scout niche analytics, quantum-safe cryptography, and AI-based anomaly-detection start-ups. Post-Quantum Cryptography Coalition membership confers early-mover advantage on firms readying lattice-based algorithms for avionics firmware updates. Disruptors like RunSafe Security, backed by BMW i Ventures, tout moving-target hardening to safeguard embedded Linux distributions inside engine controllers.

Competition is increasingly service-centric. Operators prioritize 24×7 monitoring, regulatory reporting automation, and forensic readiness as Part-IS and Innovate28 deadlines approach. Vendors capable of integrating flight-safety risk scoring with cyber telemetry strengthen value propositions, setting new barriers to entry for generic IT security providers attempting to participate in the aviation cyber security market.

Aviation Cyber Security Industry Leaders

Cisco Sytems Inc.

Thales Group

Lockheed Martin Corporation

Honeywell International Inc.

Raytheon Technologies Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: U.S. Navy granted Rockwell Collins a USD 16.6 million lifecycle-support contract for E-6B aviation cyber upgrades, broadening Collins’ defense pedigree and giving the firm reference credibility for commercial fleet campaigns.

- May 2025: FAA issued its National Airspace modernization blueprint with USD 35 million earmarked for zero-trust pilots, ensuring vendor pipelines tied to next-gen ATC rollouts until 2030.

- December 2024: Northrop Grumman secured a USD 3.5 billion TACAMO aircraft award featuring electromagnetic-pulse resilience that raises the baseline for hardening standards across strategic-aircraft programs.

- December 2024: Japan Airlines sustained a DDoS attack that delayed more than 40 flights, catalyzing regional carriers to accelerate SOC outsourcing and multi-cloud redundancy.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we view the aviation cybersecurity market as the total spend on software, hardware, and managed services that secure civil aviation information technology and operational technology assets, spanning airlines, airports, cargo handlers, and air traffic control, from unauthorized access, disruption, or data loss. The construct covers on-premise and cloud deployments that prevent, detect, and respond to threats across network, endpoint, application, wireless, and satellite links.

Scope exclusion: Solutions sold solely to classified military programs or stand-alone drone detection platforms are outside this study.

Segmentation Overview

- By Solution

- Threat Intelligence and Response

- Identity and Access Management

- Data Loss Prevention

- Security and Vulnerability Management

- Managed Security

- By Security Type

- Network Security

- Endpoint Security

- Application Security

- Cloud Security

- Wireless and Satellite Link Security

- By Deployment Mode

- On-Premise

- Cloud-Deployed

- By Application

- Airline Management

- Air Cargo Management

- Airport Management

- Air Traffic Control Management

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Nordics

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed CISOs at major hub airports, airline IT directors, OT integrators, and MSSP specialists across North America, Europe, the Middle East, and Asia-Pacific. The conversations validated adoption curves for zero-trust architectures, average spend per gate, and license price erosion, allowing us to refine assumptions taken from desk work.

Desk Research

Our analysts began with authoritative public datasets such as ICAO cybersecurity incident notices, Eurocontrol flight movement statistics, FAA Form 5010 airport files, and UN Comtrade export codes for avionics and security appliances, which anchor fleet size, traffic intensity, and hardware trade flows. Government cybersecurity strategies, IATA guidance papers, and peer-reviewed journals supplied trend coefficients on attack frequency and cost impact. To enrich company-level signals, we accessed D&B Hoovers for financials and Dow Jones Factiva for rule-of-thumb deal values. This list is illustrative; many additional open sources were consulted during data gathering and cross-checks.

Market-Sizing & Forecasting

A top-down model converts passenger departures, aircraft in-service counts, and gate inventories into an addressable attack surface, which is then split by typical security spend per asset class. Supplier roll-ups and sampled ASP × volume checks give bottom-up reference points that temper over or under shoots. Key variables like cloud migration ratio, share of connected aircraft, breach incidence rate, regulatory penalty ceilings, and managed service penetration feed a multivariate regression that projects value to 2030. Where granular bottom-up inputs are patchy, interpolation uses three-year moving averages aligned to primary research ranges.

Data Validation & Update Cycle

Model outputs run through variance tests against historic breach losses, vendor revenue disclosures, and airport CAPEX patterns; anomalies trigger analyst rework before sign-off. Reports are refreshed annually, with interim updates when a material event, for example, a large regulatory mandate, shifts the baseline.

Why Mordor's Aviation Cyber Security Baseline Commands Reliability

Published estimates often diverge because firms choose different scopes, pricing ladders, or refresh cadences.

Key gap drivers include whether cargo terminals are counted, how managed service fees are annualized, and if cloud controls are priced at list or transacted values. Mordor applies a full civil aviation scope, periodically re-benchmarks asset multipliers, and converts all inputs to constant 2025 dollars, while some peers rely on single region proxies or outdated fleet data.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.51 B | Mordor Intelligence | - |

| USD 10.07 B | Global Consultancy A | Uses conservative threat spend ratio and omits airport cloud controls |

| USD 5.32 B | Market Research House B | Counts only network firewalls, excludes endpoint and IAM tools |

| USD 11.30 B | Trade Journal C | Extends 2023 data without updated connected aircraft metrics |

Taken together, the comparison shows our baseline is neither the highest nor the lowest; it is the one most transparently tied to verifiable traffic, asset, and spend indicators, giving decision makers a balanced platform for strategy and budgeting.

Key Questions Answered in the Report

What is the current value of the aviation cyber security market?

The market stands at USD 12.99 billion in 2026 and is projected to grow to USD 23.8 billion by 2031.

Which region leads spending on aviation cyber security solutions?

North America holds 39.40% of 2025 revenue, supported by robust FAA and TSA funding programs.

Why is cloud security the fastest-growing security type?

Airlines and airports are migrating passenger, maintenance, and analytics workloads to hybrid-cloud architectures, driving a 14.7% CAGR for cloud-focused controls.

How do certification requirements affect project timelines?

EASA Part-IS and FAA rules require extensive validation, often adding multiple years and significant cost before systems can enter service.

What role do managed security services play in this market?

Managed Security Services grow at 13.4% CAGR as operators outsource 24×7 monitoring and compliance to vendors with aviation-specific expertise.

Which application segment will expand the quickest?

Air Traffic Control cyber solutions will see a 13.8% CAGR on account of IP modernization and zero-trust mandates across national ANSP infrastructures.

Page last updated on: