Automotive Control Panel Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

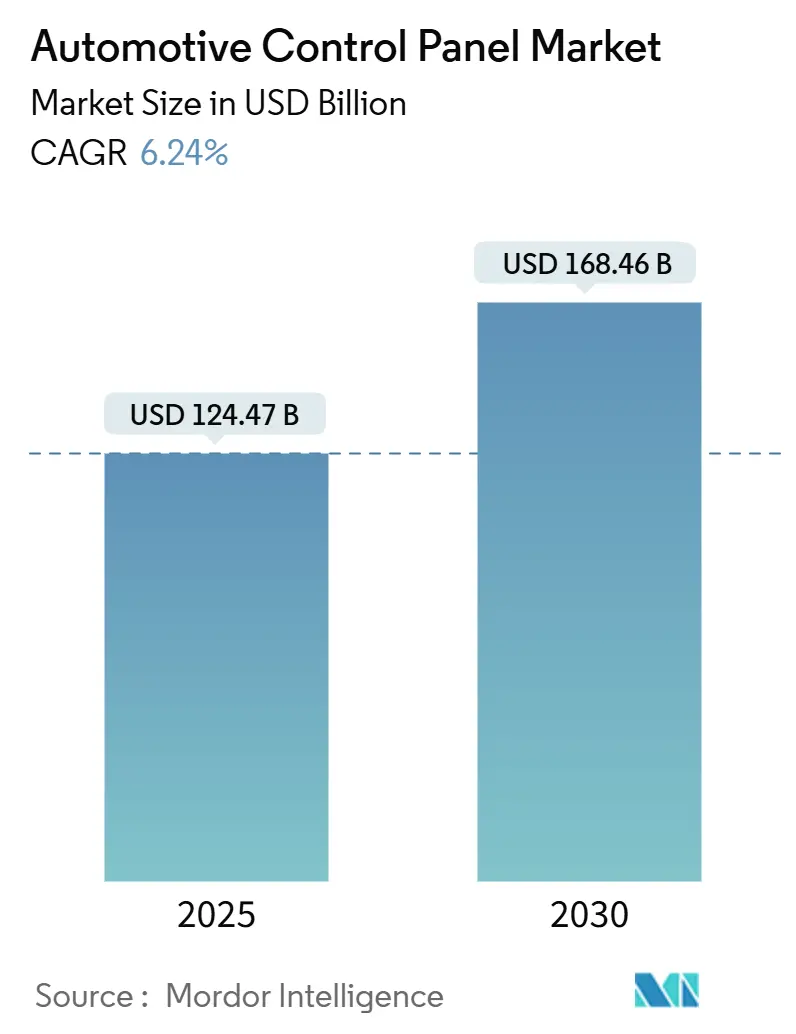

| Market Size (2025) | USD 124.47 Billion |

| Market Size (2030) | USD 168.46 Billion |

| Growth Rate (2025 - 2030) | 6.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Control Panel Market Analysis by Mordor Intelligence

The automotive control panel market size stands at USD 124.47 billion in 2025 and is projected to reach USD 168.46 billion by 2030, and is expected to grow at a 6.24% CAGR during the forecast period (2025-2030). This growth reflects the rapid move toward software-defined vehicles, where digital cockpits consolidate infotainment, climate, and driver-assistance controls onto unified platforms. Rising electric-vehicle sales demand reconfigurable interfaces, while ADAS adoption pushes suppliers to deliver intuitive human–machine interaction. Consumers expect smartphone-like experiences, encouraging touchscreen dominance, capacitive haptic adoption, and over-the-air feature updates that compress refresh cycles. Competition intensifies around domain controller consolidation, enabling cost reduction and AI-powered personalization that distinguish premium models. Overall, the automotive control panel market benefits from electrification, semiconductor innovation, and regulatory momentum that favor safer, connected, and easily upgradable cockpit architectures.

Key Report Takeaways

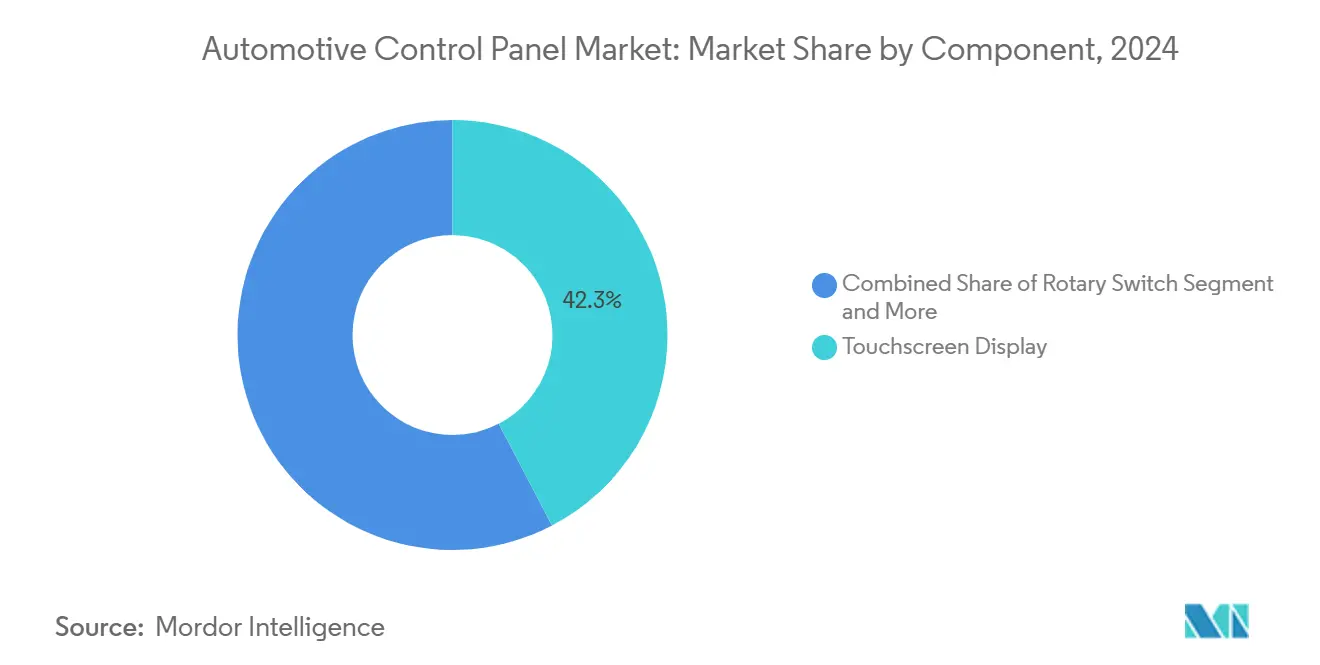

By component, touchscreen modules captured a 42.34% share of the automotive control panel market in 2024. In contrast, the haptic-feedback actuators segment is expected to grow at an 8.97% CAGR during the forecast period (2025-2030).

By technology, digital control panels led the automotive control panel market with a 55.44% share in 2024, while the capacitive-touch panels segment is expected to grow at a 9.58% CAGR during the forecast period (2025-2030).

By application, infotainment dominated the automotive control panel market, with a 48.38% share in 2024; driver assistance is expected to grow at a 10.28% CAGR during the forecast period (2025-2030).

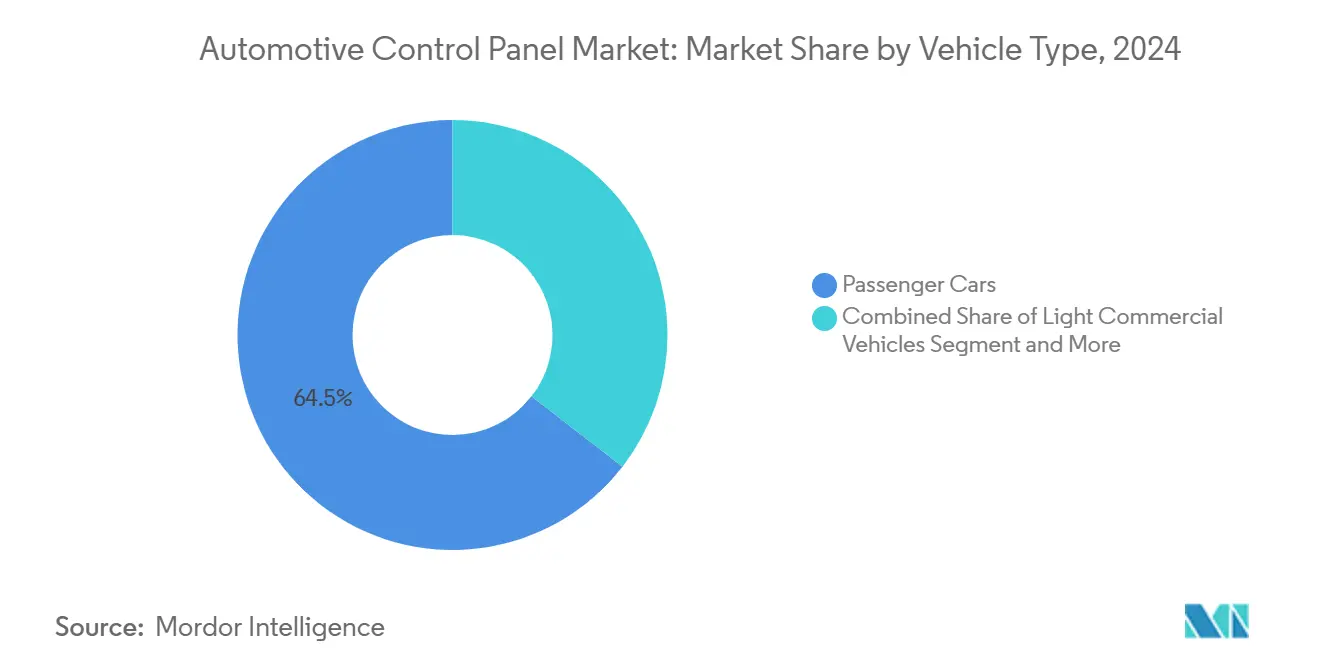

By vehicle type, passenger cars held a 64.51% share of the automotive control panel market in 2024, yet buses and coaches are expected to grow at a 7.86% CAGR during the forecast period (2025-2030).

By distribution channel, OEM installations accounted for 78.62% share of the automotive control panel market in 2024, while the aftermarket segment is expected to grow at a 9.07% CAGR during the forecast period (2025-2030), on retrofit demand.

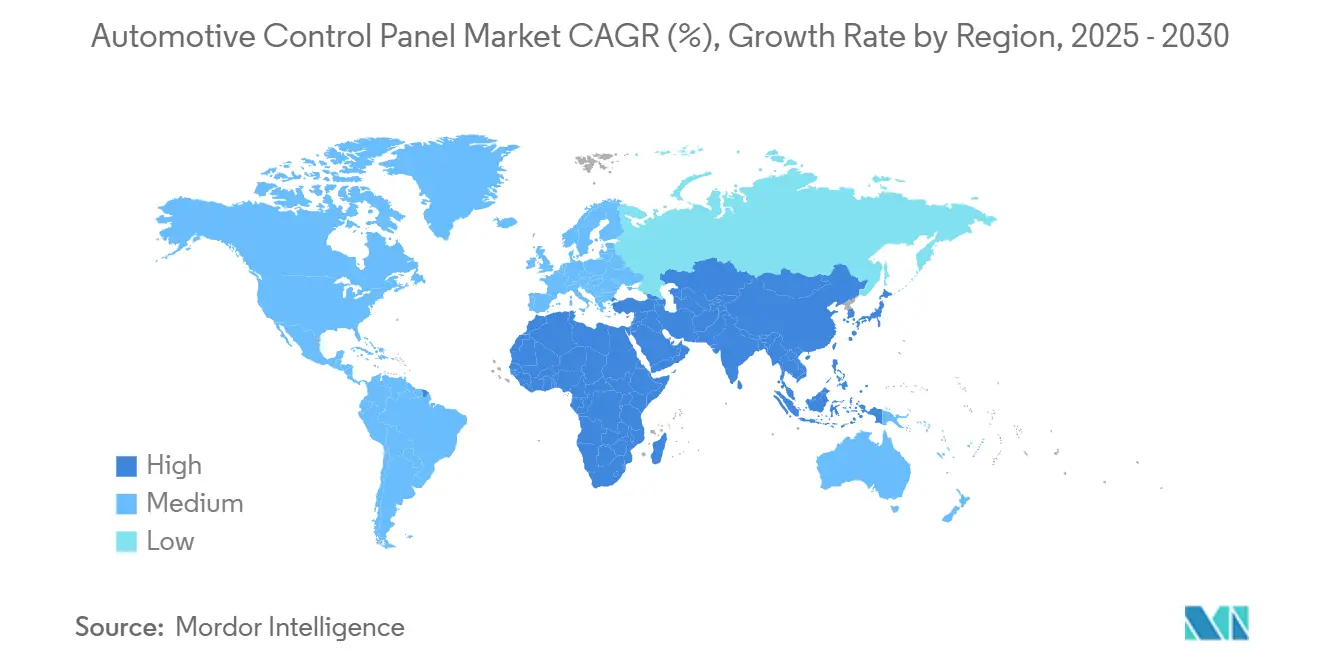

By geography, Asia-Pacific was the largest region with a 36.29% share of the automotive control panel market in 2024 and is expected to grow at a CAGR of 8.67% during the forecast period (2025-2030).

Global Automotive Control Panel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Cockpits and Infotainment | +1.5% | Global, with APAC and North America leading adoption | Medium term (2-4 years) |

| Capacitive-Touch and Haptics Integration | +1.2% | Global, concentrated in premium segments | Short term (≤ 2 years) |

| ADAS-Driven Driver-Assistance HMIs | +0.9% | North America & EU regulatory push, APAC volume growth | Medium term (2-4 years) |

| Re-Configurable Panel Layout Requirement | +0.8% | APAC core, spill-over to Europe and North America | Long term (≥ 4 years) |

| In-Mold Electronics | +0.6% | Global, with Europe leading manufacturing innovation | Long term (≥ 4 years) |

| Domain-Controller Consolidation | +0.4% | Global, driven by Tier-1 supplier capabilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Digital Cockpits and Infotainment

Digital cockpit adoption redefines vehicle interiors by merging traditionally separate displays into a single software-defined hub that supports subscription services and personalized profiles. Continental’s Emotional Cockpit uses E Ink elements to adjust themes dynamically and lower driver cognitive load, while maintaining safety certifications[1]"Emotional Cockpit Platform and E Ink Display Technology." Continental AG, https://continental.com.. Harman’s Ready platform pairs Samsung display technology with isolated operating systems that separate safety-critical tasks from entertainment, allowing rapid multimedia upgrades without hardware changes[2]"TOPpage | Panasonic Automotive Systems Co., Ltd." Panasonic Automotive Systems Co., Ltd., https://automotive.panasonic.com/en.. OEMs view these cockpits as revenue generators, offering paid apps and cloud services during ownership. The shift forces suppliers to provide hardware, middleware, and application layers together, raising entry barriers. As cockpit data bandwidth grows, domain controllers replace multiple ECUs, cutting part count and enabling AI-driven personalization that differentiates models quickly.

Rapid Integration of Capacitive-Touch and Haptics

Capacitive touchscreens paired with haptic feedback overcome distraction issues by providing tactile confirmation on smooth glass. Hap2U’s piezoelectric actuators create localized friction variations that emulate physical buttons without moving parts, improving durability and silence[3]"Corporate Profile | Panasonic Automotive Systems Co., Ltd." Panasonic Automotive Systems Co., Ltd., https://automotive.panasonic.com/en/corporate/about/overview.. Volkswagen’s earlier steering-wheel touch controls drew criticism, demonstrating the need for precise haptic tuning; newer piezo systems respond faster than linear resonant actuators and satisfy safety rules. Mid-air haptic prototypes allow contactless gesture input, preparing for autonomous cabins where passengers face displays rather than road. Automakers now demand supplier roadmaps that include programmable haptic libraries, letting OTA updates refine feel over time. These advancements keep touchscreen adoption high while meeting stricter driver-attention regulations.

Adoption of ADAS-Driven Driver-Assistance HMIs

Level 2+ and Level 3 autonomy escalate interface complexity, requiring clear machine-to-driver communication. Continental couples driver-monitor cameras with vibrating steering-wheel nodes that escalate alerts if gaze drifts, aligning with UN Regulation 79 on steering automation. Harman’s Ready Aware links sensor fusion with AR-enabled displays to spotlight hazards before they appear, boosting situational awareness. Such multi-modal HMIs blend visual, audible, and haptic cues to reduce confusion during control handovers. Suppliers integrate graphics engines, sensor feeds, and actuator loops onto central compute platforms, creating high software content per vehicle. Standardized iconography and color codes emerge as regulation tightens, ensuring brand driver familiarity.

EV Shift Requiring Re-Configurable Panel Layouts

Electric vehicles drop legacy powertrain gauges, freeing designers to re-task screen real estate for range, charging, and energy optimization data. Panasonic’s full-display meter in Mazda CX-70 lets drivers switch between traditional and EV-specific layouts via software themes. Tesla’s single-screen minimalism proves extreme consolidation viable, though critics note navigation of nested menus during dynamic driving. Suppliers now pitch modular display kits that scale from compact EVs to large SUVs, sharing hardware but customizing software layers per brand. This adaptability reduces tooling costs and accelerates model launches. As EV sales grow, demand rises for thin in-mold electronics that lighten dashboards while housing flexible OLED panels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Costly Displays and Touch ICs | -0.7% | Global, with acute pressure in emerging markets | Short term (≤ 2 years) |

| Driver-Distraction Safety Regulations | -0.5% | North America & EU regulatory enforcement, APAC adoption | Medium term (2-4 years) |

| Glass / Touch-IC Supply-Chain Volatility | -0.4% | Global, with concentration risk in APAC manufacturing | Short term (≤ 2 years) |

| Cyber-Security Vulnerabilities | -0.3% | Global, with varying regulatory enforcement | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Displays and Touch ICs

Automotive-grade OLEDs and haptic-ready DDICs cost three-fold more than basic LCDs due to temperature tolerance and lifetime guarantees. Extended lead times—often 52 weeks—force OEMs to lock designs early, limiting mid-cycle upgrades. When shortages strike, discrete distributors step in with certified stock, but premiums inflate the bill of materials. To control costs, automakers negotiate multi-year volume contracts and push suppliers toward panel standardization across platforms. However, such strategies limit differentiation and can clash with fast-changing consumer tech benchmarks.

Driver-Distraction Safety Regulations

NHTSA and European ECE guidelines cap visual-manual interaction to 15 seconds per task, compelling UI simplicity. Compliance testing extends timelines and necessitates adaptive interfaces that adjust complexity to driving conditions, adding development overhead. ISO 26262 functional safety demands redundancy for critical controls, raising hardware counts even in “button-free” designs. Differences between U.S., EU, and China rules complicate global rollouts, forcing region-specific validation cycles that strain budgets and schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Touchscreen Adoption Spurs Integration

Touchscreen modules accounted for 42.34% share of the automotive control panel market in 2024, confirming their status as the primary interaction surface in modern cabins. Haptic actuators bolster their usability, with the category expected to grow at an 8.97% CAGR as suppliers integrate piezo elements that replicate button clicks. Push buttons remain for hazard lights and other critical actions where muscle memory matters. Rotary switches gain premium appeal for drive-mode or volume control, delivering a precise tactile feel alongside digital menus.

Haptic-feedback growth exemplifies a hardware shift that supports software personalization. Continental’s piezo-based steering-wheel controls illustrate how one component can host multiple virtual buttons, reducing dashboard clutter while retaining safety certifications. Suppliers bundle displays, touch layers, and actuators as cost curves fall into single modules, trimming wiring and easing assembly. This convergence positions integrated touch-haptic units as a standard bill-of-materials element in the automotive control panel market.

By Technology: Digital Dominance Fuels Software Evolution

Digital panels commanded a 55.44% share of the automotive control panel market in 2024, underscoring the mainstreaming of screen-based HMIs. Due to slim profiles and multi-touch support compatible with smartphone gestures, capacitive variants are expected to grow at a 9.58% CAGR during the forecast period (2025-2030). Analog controls linger in cost-sensitive fleet vehicles and base trims, where durability and low acquisition price outweigh novelty. Force-sensing panels carve a niche in steering-wheel spokes and center stacks, translating press depth into variable commands useful for ADAS engagement.

The automotive control panel market size for capacitive touch technology is forecast to climb steadily as OEMs migrate mid-segment models from hard keys to glass. Unified compute architectures mean one SoC can drive multiple screens, lowering incremental cost per additional display. Software update capability encourages OEMs to launch hardware first and activate new features later, aligning revenue with the vehicle’s life cycle. Suppliers able to decouple hardware from feature delivery gain leverage in contract negotiations.

By Application: Infotainment Rules, ADAS Gathers Pace

Infotainment retained a 48.38% share of the automotive control panel market in 2024, propelled by consumer demand for streaming, gaming, and social apps during commutes. Driver-assistance interfaces are expected to grow at a 10.28% CAGR, mirroring regulatory pressure for clearer ADAS status indication and takeover prompts. Climate controls remain essential, yet their dedicated hardware shrinks as functions migrate to central displays or voice commands. Navigation blurs with infotainment once smart routing and augmented-reality overlays share the same GPU pipeline.

As the automotive control panel market broadens, boundaries between entertainment and safety functions dissolve. Subscription-based mapping, video conferencing, and vehicle health monitoring now reside on one display stack, supported by over-the-air patching. Suppliers thus must balance cybersecurity with user experience, embedding hardware root-of-trust alongside cloud APIs. Firms offering turnkey infotainment-ADAS bundles capture higher per-vehicle content than those selling discrete modules.

By Vehicle Type: Commercial Uptake Surprises

Passenger cars led with a 64.51% share of the automotive control panel market in 2024, reflecting sheer production volume and consumer tech appetite. Buses and coaches are expected to grow at a 7.86% CAGR as urban fleets electrify and add passenger-facing displays for route updates and infotainment. Light commercial vehicles integrate telematics and delivery-route apps, raising cockpit sophistication. Heavy trucks adopt large touch panels to manage autonomous platooning, load monitoring, and regulatory logging.

The automotive control panel market sees commercial buyers prioritize uptime and total cost of ownership. Modular panels reduce service downtime: defective touch layers can be swapped without re-certifying whole dashboards. Fleet managers appreciate remote diagnostics delivered via the same displays drivers use for navigation, tying maintenance savings directly to HMI investment. Suppliers that bundle ruggedized hardware with fleet software suites gain traction.

By Distribution Channel: Aftermarket Retrofits Gather Steam

OEM channels captured a dominant 78.62% share of the automotive control panel market 2024, underscoring the intricate integration and stringent safety certification demands. These factors increasingly tilt the balance towards factory installations, rather than aftermarket modifications, for sophisticated control panel systems. Yet aftermarket sales are expected to grow at a 9.07% CAGR as owners seek Apple CarPlay-ready or larger screens for older vehicles. ISO-compliant interface kits now abstract vehicle-specific signals, letting third-party head units integrate without warranty risk.

Aftermarket momentum impacts the automotive control panel industry by extending revenue beyond the initial sale. Suppliers create modular bezel-less displays that fit multiple dashboards via adaptor plates, cutting SKU count. OTA software frameworks mean even third-party devices receive security patches, easing regulator concerns. The aftermarket's share could climb further as standardized interfaces and modular architectures enable compatible upgrades without compromising vehicle safety or warranty coverage.

Geography Analysis

Asia-Pacific led with a 36.29% share of the automotive control panel market in 2024, and is expected to record the fastest 8.67% CAGR through 2030. China’s dominance in electric-vehicle production drives bulk demand for configurable touch panels that manage battery status and ADAS alerts. Japan contributes advanced manufacturing techniques that integrate flexible displays with haptic layers, while South Korea’s semiconductor giants supply high-bandwidth domain controllers powering unified cockpits. Regional governments push intelligent-connected-vehicle standards, accelerating digital cockpit penetration.

North America is expected to show healthy expansion at 4.45% CAGR, fueled by premium pickup and SUV demand that values large screens and AI-based personalization. The National Highway Traffic Safety Administration sets stringent distraction guidelines, compelling suppliers to add gaze tracking and haptic confirmations. Tesla’s minimalist UI sets consumer expectations for software-centric cabins, prompting legacy OEMs to roll out full-width LED panels. Limited chip fabs in the region spur joint ventures to secure supply, even as domestic policy incentivizes on-shore semiconductor plants.

Europe are the expected to grow at 3.83% CAGR, balancing luxury brand demands with strict cybersecurity and ecological directives. Regulations R155 and R156 require over-the-air update compliance, influencing control-panel architecture worldwide. German OEMs emphasize sustainable materials and low-power displays, pushing suppliers toward recyclable substrates and micro-LED tech. Language diversity forces flexible UI localization, opening contracts for software providers specializing in regionalization.

Competitive Landscape

The automotive control panel market exhibits moderate concentration, creating a competitive environment where established Tier-1 suppliers leverage automotive safety expertise while technology companies pursue disruptive integration strategies. Continental leads, combining traditional mechanical controls with digital cockpit solutions that integrate E Ink and haptic steering inputs. Robert Bosch follows, leveraging sensor portfolios and compute modules to offer end-to-end HMIs. Fragmentation allows niche firms focusing on haptic actuators, flexible OLEDs, or cybersecurity middleware to partner with larger Tier-1s.

Strategy trends focus on domain controller consolidation. Harman’s Ready platform merges infotainment, telematics, and ADAS visualization on a single SoC, backed by Samsung fabrication capacity. Suppliers bet on software-defined value by embedding update frameworks and app stores, letting OEMs monetize features post-sale. Semiconductor entrants like Qualcomm provide reference boards that simplify cockpit integration, challenging legacy suppliers reliant on discrete modules.

White-space opportunities surface in mid-air haptics, where companies like Boréas Technologies demo ultrasonic solutions that offer tactile cues without physical contact. Flexible display pioneers court dashboard designs that contour to interior surfaces, reducing glare and weight. Cybersecurity specialists integrate hardware roots-of-trust into touch controllers, satisfying R155 mandates. M&A activity centers on acquiring software talent and display IP that shorten time-to-market for software-centric vehicles.

Automotive Control Panel Industry Leaders

-

Continental AG

-

Robert Bosch GmbH

-

Visteon Corporation

-

Denso Corporation

-

Faurecia (FORVIA)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Valeo and Capgemini announced a collaboration to validate Level 2+ ADAS systems.

- July 2025: BlackBerry QNX and Vector signed an MoU to deliver a foundational vehicle software platform for software-defined vehicles.

- June 2025: NXP Semiconductors partnered with Rimac Technology to co-develop centralized architectures using S32E2 processors.

Global Automotive Control Panel Market Report Scope

| Rotary Switch |

| Push Buttons |

| Touch Pad / Touchscreen Module |

| Haptic-Feedback Actuators |

| Analog Control Panel |

| Digital Control Panel |

| Capacitive Touch Panel |

| Force-Sensing Panel |

| Infotainment |

| Climate Control |

| Navigation |

| Lighting |

| Driver Assistance |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (MHCVs) |

| Buses and Coaches |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Component | Rotary Switch | |

| Push Buttons | ||

| Touch Pad / Touchscreen Module | ||

| Haptic-Feedback Actuators | ||

| By Technology | Analog Control Panel | |

| Digital Control Panel | ||

| Capacitive Touch Panel | ||

| Force-Sensing Panel | ||

| By Application | Infotainment | |

| Climate Control | ||

| Navigation | ||

| Lighting | ||

| Driver Assistance | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Medium and Heavy Commercial Vehicles (MHCVs) | ||

| Buses and Coaches | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the automotive control panel market by 2030?

The market is projected to reach USD 168.46 billion by 2030, growing at a 6.24% CAGR.

Which component category is growing the fastest?

Haptic-feedback actuators advance at 8.97% CAGR as they enhance touchscreen usability with tactile confirmation.

Why is Asia-Pacific the leading region?

Asia-Pacific holds 36.29% share due to China’s EV production, Japan’s manufacturing precision, and South Korea’s chip expertise.

How are driver-distraction rules affecting cockpit design?

Regulations cap visual task duration, pushing automakers to incorporate gaze monitoring, haptics, and simplified UIs.

What drives aftermarket growth in control panels?

Owners retrofit older vehicles with larger screens and connectivity upgrades, lifting aftermarket revenue by a 9.07% CAGR.

Which companies dominate the competitive landscape?

Continental at 14.5% and Robert Bosch at 12.7% lead, yet the top five combined hold just 51.1%, leaving room for specialists.

Page last updated on: