Automotive Motors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

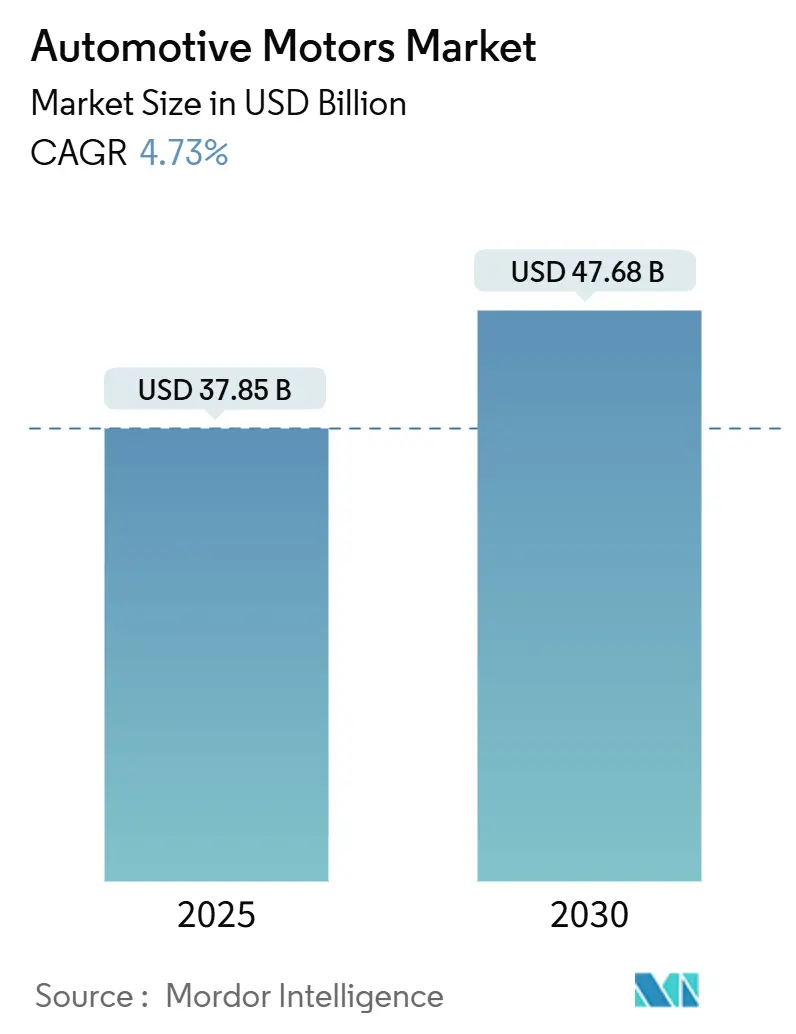

| Market Size (2025) | USD 37.85 Billion |

| Market Size (2030) | USD 47.68 Billion |

| Growth Rate (2025 - 2030) | 4.73% CAGR |

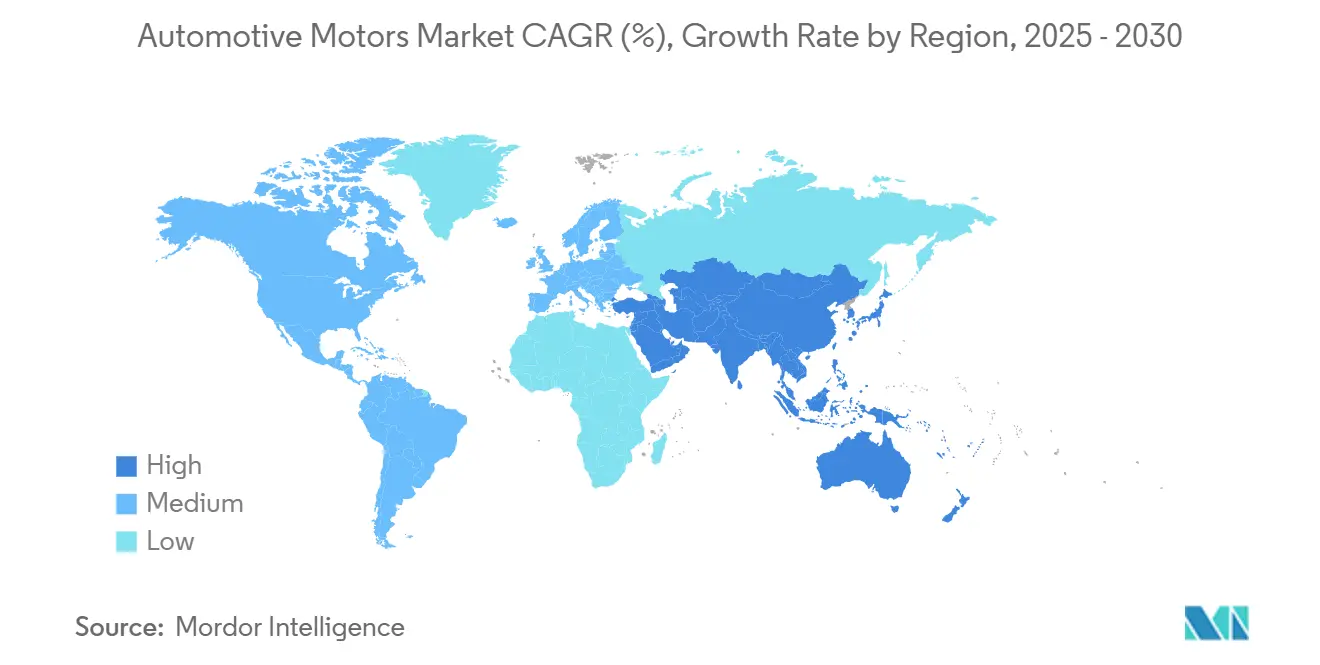

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

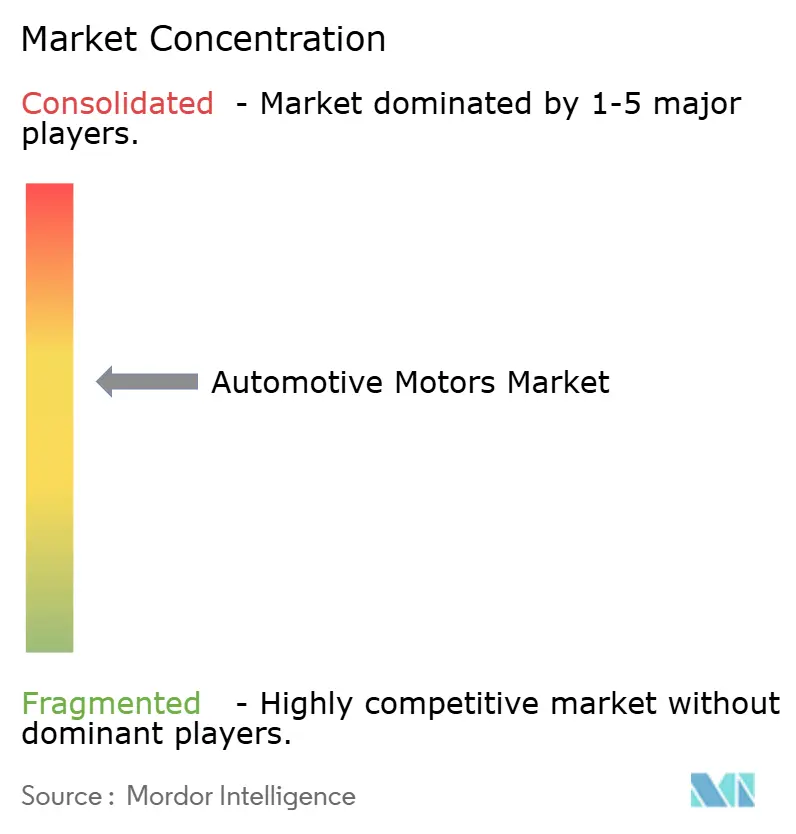

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Motors Market Analysis by Mordor Intelligence

The Automotive Motors Market size is estimated at USD 37.85 billion in 2025, and is expected to reach USD 47.68 billion by 2030, at a CAGR of 4.73% during the forecast period (2025-2030). Demand stems from the accelerating transition to electrified powertrains, the proliferation of advanced driver assistance features, and regulatory pressure for energy-efficient auxiliaries. Brushless technologies are winning share as OEMs replace belt-driven accessories with compact electric pumps, compressors, and blowers. At the same time, traction motors underpin the roll-out of battery-electric platforms, while 48 V mild-hybrid architectures serve volume models that cannot yet justify full-EV costs. Suppliers able to integrate motors with silicon-carbide electronics, embedded diagnostics, and cybersecurity safeguards are securing long-term sourcing agreements that influence the competitive balance of the automotive motors market. Material price swings for copper and rare-earth elements remain the chief cost headwind, yet process innovations and magnet-light designs partially offset volatility.

Key Report Takeaways

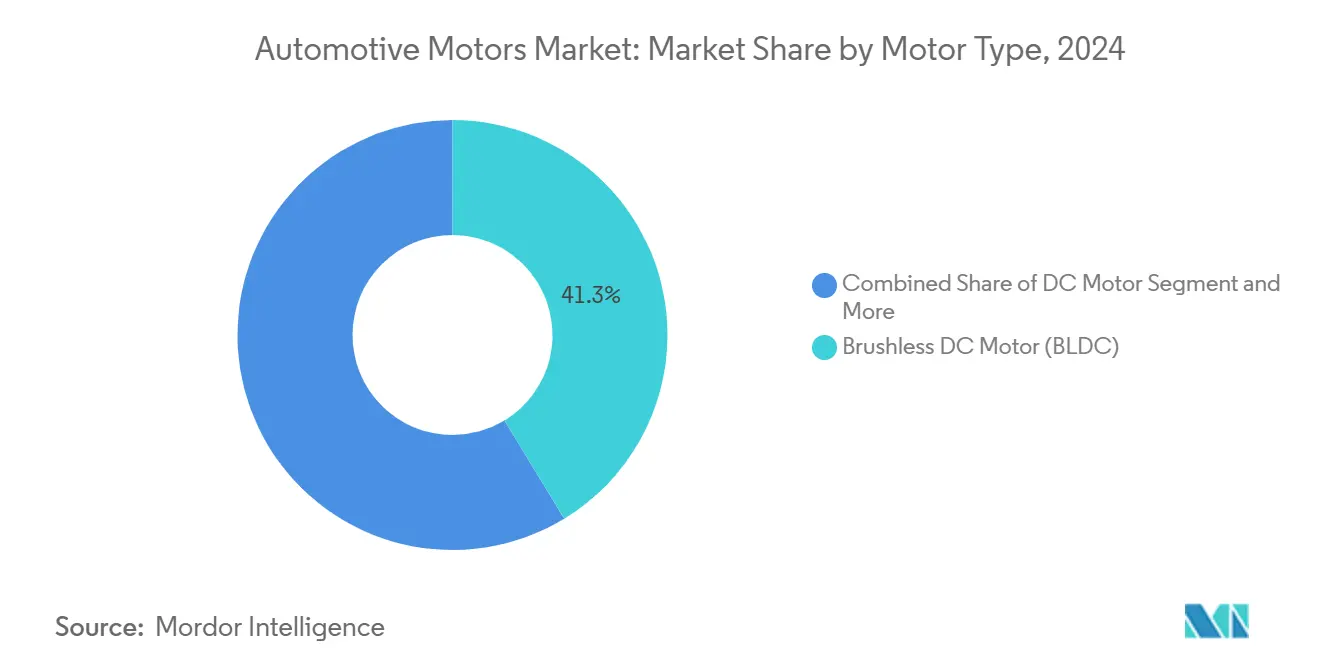

- By motor type, Brushless DC motors captured 41.27% of the automotive motor market share in 2024. Traction motors are projected to grow at a 4.75% CAGR through 2030.

- By application, powertrain systems commanded 45.58% of the automotive motors market size in 2024. Safety systems are advancing at a 4.86% CAGR to 2030.

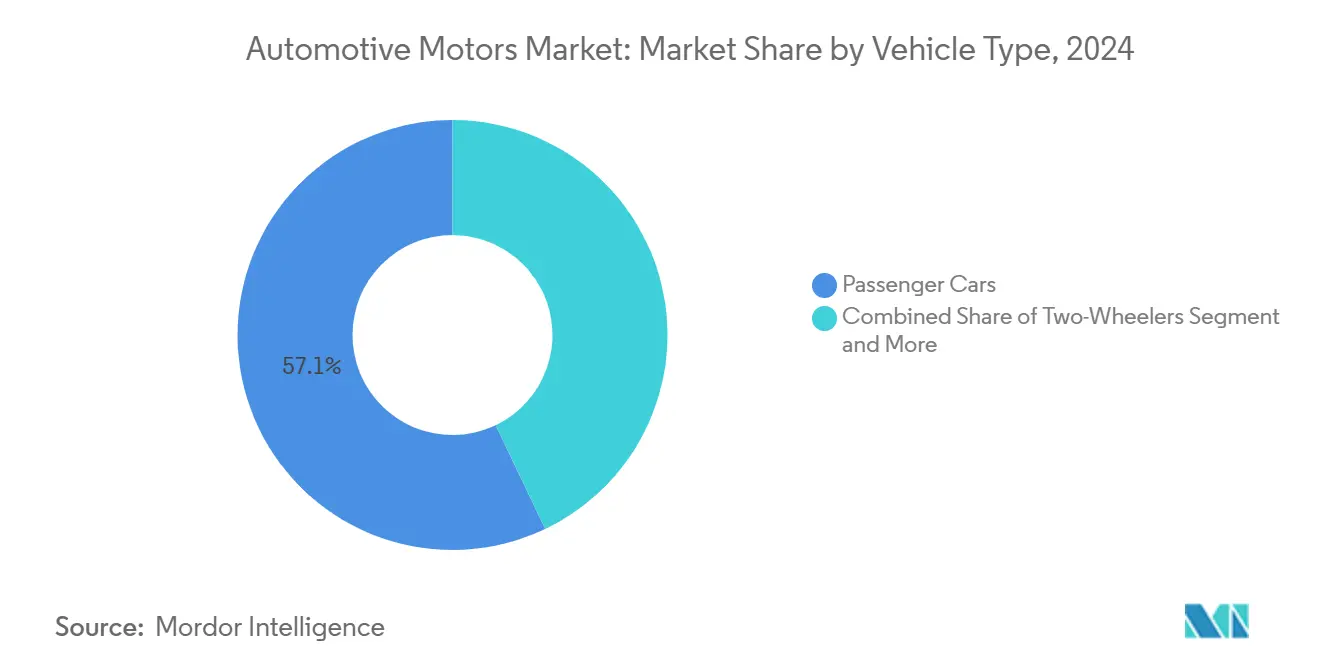

- By vehicle type, passenger cars accounted for a 57.14% share of the automotive motors market size in 2024 and are forecast to expand at a 4.78% CAGR through 2030.

- By sales channel, the OEM segment held 81.25% of the automotive motors market share in 2024, while the aftermarket is projected to post a 4.82% CAGR to 2030.

- By geography, Asia-Pacific led 46.53% of the automotive motors market share in 2024; it is also the fastest-growing region, with a 4.81% CAGR to 2030.

Global Automotive Motors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification of Auxiliary Systems | +1.2% | Global, with Asia Pacific and Europe leading | Medium term (2-4 years) |

| Rapid Adoption of ADAS-Grade Safety Actuators | +1.0% | North America and EU, expanding to Asia Pacific | Short term (≤ 2 years) |

| Rising OEM Focus on 48-V Mild-Hybrid Architectures | +0.9% | Global, with Europe and China early adopters | Medium term (2-4 years) |

| Regulatory Push For Energy-Efficient HVAC Blowers | +0.7% | North America and EU regulatory zones | Long term (≥ 4 years) |

| Growth of In-Cabin Comfort | +0.6% | Premium segments globally, Asia Pacific luxury focus | Medium term (2-4 years) |

| Increasing Demand For Low-Noise BLDC Solutions | +0.5% | Global EV markets, premium segment focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification of Auxiliary Systems (E-Pumps, E-Compressors)

Auxiliary electrification removes parasitic losses from belt-driven accessories, delivering one-fifth fuel-economy gains in urban cycles. Integrated BLDC pump-motor assemblies combine hydraulics, electronics, and software in compact housings that slot into congested engine bays. Uptake accelerates as the automotive motors market relies on 48 V networks to power coolant, brake-boost, and steering pumps without costly high-voltage safety measures. European CO₂ limits and U.S. CAFE rules compel OEMs to prioritize these low-hanging efficiency wins[1]“Corporate Average Fuel Economy Standards,” U.S. Environmental Protection Agency, epa.gov . Module suppliers quoting efficiency and cradle-to-gate emissions advantages win lifetime supply awards that stabilize volumes for the next model cycle.

Rapid Adoption of ADAS-Grade Safety Actuators

Lane-keeping, emergency braking, and automatic parking demand millisecond-level motor response and proven fault tolerance. Electric power-steering units integrate torque-overlay motors, while electromechanical brake boosters use compact, high-torque servomotors to replace hydraulic boosters. The NHTSA proposal to mandate automatic emergency braking on all new vehicles from 2029 cements volume prospects for safety-critical motors[2]“Proposed AEB Requirement for Light Vehicles,” National Highway Traffic Safety Administration, nhtsa.gov. Suppliers must meet ISO 26262 ASIL-D requirements, pushing them to adopt redundant hall sensors, self-diagnostics, and secure bootloaders. Design wins are shifting toward companies able to co-develop motion-control software with OEMs and certify to cybersecurity regulations.

Rising OEM Focus on 48 V Mild-Hybrid Architectures

A 48 V bus powers superchargers, integrated starter generators, and active suspension without the weight, cost, or orange-cable complexity of complete high-voltage systems. European marques deploy 48 V across diesel and gasoline lines, while Chinese OEMs use it to lift performance in price-sensitive segments. For the automotive motors market, the architecture multiplies demand for compact BLDC machines and drives down unit prices as economies of scale solidify. Tier-1 suppliers bundle motors with inverters and software to present turnkey modules. Because 48 V vehicles outnumber BEVs in many showrooms today, this bridge technology secures revenue streams through the decade.

Regulatory Push for Energy-Efficient HVAC Blowers

Mobile air-conditioning consumes up to one-fifth of vehicle energy under hot-soak conditions. North American and EU efficiency mandates now include blower and compressor performance, effectively sidelining brushed motors. Next-generation HVAC modules use variable-speed BLDC blowers with intelligent algorithms that adjust airflow to cabin occupancy. DOE minimum motor-efficiency standards elevate permanent-magnet designs for heavy-duty delivery trucks that idle AC systems at loading docks[3]“Electric Motor Minimum Efficiency Standards,” U.S. Department of Energy, energy.gov . Suppliers able to validate endurance in dusty, high-humidity conditions under −40 °C to 85 °C win fleet contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper and Rare-Earth Price Volatility | -0.8% | Global, with China supply concentration risk | Short term (≤ 2 years) |

| Thermal Management Challenges | -0.6% | Global, affecting premium EV segments | Medium term (2-4 years) |

| Supply-Chain Concentration Of Traction-Motor Magnets | -0.5% | Global, with Asia Pacific manufacturing dependence | Long term (≥ 4 years) |

| Competition From Integrated Smart Actuators | -0.4% | North America and EU, technology-forward markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Copper & Rare-Earth Price Volatility

Over the past year, LME cash copper varied by two-fifths, while neodymium oxide spot quotes whipsawed on policy uncertainty. Permanent-magnet traction motors contain up to 1 kg of rare-earth material, tying their bill of materials to geopolitical risk. Western OEMs mandate dual-sourcing, prompting suppliers to develop ferrite-magnet or reluctance alternates that cut rare-earth use by half but at a minimal efficiency penalty. The automotive motors market, therefore, faces hedging costs, redesign cycles, and longer qualification timelines that can slow program ramps.

Thermal Management Challenges at Higher Power Densities

Compact motors spin at 20,000 rpm or higher, concentrating losses that raise rotor temperatures past 180 °C. Oil-spray cooling and direct-stator sleeve channels manage hotspots but add pumps and seals that heighten system cost. In commercial vans that deliver groceries all day, motors run at peak torque for extended periods, exposing magnets to demagnetization risk. Engineers must balance heavier copper fills against higher-grade insulation and more expensive thermal interfaces, a tradeoff that restrains gross-margin improvement across the automotive motors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: Efficiency Drives BLDC Dominance

BLDC machines held 41.27% of the automotive motors market share in 2024 and underpin nearly every new auxiliary or safety function. Their brush-free design slashes maintenance and improves partial-load efficiency, which is crucial for EV range and hybrid fuel economy targets. As BEV volumes rise, the automotive motors market size allocated to traction motors is projected to swell at a 4.75% CAGR through 2030. Servo motors occupy high-precision niches such as active suspension and steer-by-wire, generating attractive margins for suppliers capable of meeting low-noise and high-torque demands. Older brushed DC and stepper formats remain cost-effective for window lifts and HVAC flaps, but see gradual displacement as OEMs consolidate platforms around scalable BLDC topologies.

In parallel, patent filings show OEMs refining materials; carbon-sleeved rotors lift speed limits, and grain-oriented electrical steels cut core losses. Nidec’s expanded capacity aligns with long-term contracts for comfort, safety, and traction motors, signaling confidence in multi-segment demand. Overall, the automotive motors market continues transitioning toward high-efficiency, high-integration BLDC solutions that ship with embedded diagnostics.

By Application: Powertrain Scale Meets Safety Momentum

Powertrain functions captured 45.58% of the automotive motors market size in 2024 as traction, starter-generator, and e-supercharger deployments multiplied across vehicle classes. Electrified drivetrains demand continuous innovation in winding technology and inverter control to balance torque density with cost. Though smaller in absolute value, safety systems recorded the fastest 4.86% CAGR, reflecting regulatory moves to standardize automatic emergency braking and lane-keeping on mainstream models. HVAC motor demand grows steadily as premium climate features cascade down to entry trims, while comfort features such as hands-free tailgates bolster small-motor unit counts.

The infotainment domain evolves: articulated screens and haptic feedback applications introduce micro-servo requirements, broadening the supplier base. Emerging niches such as active aerodynamics and adaptive lighting create exploratory programs where small-batch, high-spec motors test novel architectures—often hybrid reluctance or magnet-reduced layouts—to bypass raw-material volatility. These shifts reinforce the need for flexible production assets within the automotive motors market.

By Vehicle Type: Passenger Cars Anchor Volume Growth

Passenger cars retained a 57.14% slice of the automotive market share in 2024 and remain the highest-growth vehicle group at 4.78% CAGR. The mass-market pivot to battery-electric and sophisticated ADAS turns each new model year into a fresh design-win cycle for motors. Light commercial vehicles grow steadily as e-commerce distribution relies on quiet, emissions-compliant vans that navigate urban zero-emission zones. Two-wheelers, especially electric scooters in Asian megacities, expand the addressable automotive motors market; their small yet high-RPM traction units reward suppliers with consumer-electronics style volumes.

Heavy trucks and off-highway equipment leverage electrified auxiliaries to trim idle consumption, but adoption rates diverge by region as duty-cycle requirements vary. Across categories, the market values suppliers that can tailor winding fill, magnet grade, and cooling solution to duty cycle without rewriting control software, enabling platform re-use and cost containment.

By Sales Channel: OEM Integration Still Dominates

OEM programs secured 81.25% of the automotive market share in 2024, reflecting the platform-level integration required for safety and powertrain motors. Early collaboration on packaging, EMC, and software validation creates barriers to entry that strengthen incumbents. Yet the aftermarket, growing at 4.82% CAGR, presents rising opportunity: fleets retrofitting 48 V systems into existing chassis need certified pump and blower kits, and aging vehicles demand replacements for seat, window, or HVAC motors. Complexity favors authorized networks with specialized diagnostic tools, though e-commerce channels are emerging for plug-and-play BLDC assemblies.

As electrification deepens, independent repair shops must upskill on inverter diagnostics and high-speed bearing service. Suppliers that package motors with self-calibrating controllers ease installation and claim a higher aftermarket share, broadening the mix of the automotive motors market beyond factory lines.

Geography Analysis

Asia-Pacific commands 46.53% of the automotive motors market share in 2024, propelled by China’s EV output and India’s maturing supplier base. Government incentives, dense local supply chains, and rising disposable income keep the regional automotive motors market on a 4.81% CAGR path. Chinese vendors partner with Southeast Asian assemblers, exporting learning curves in yield and automation. India’s Production-Linked Incentive programs encourage local magnet fabrication, tilting material security calculus, and favoring domestic content.

North America focuses on technology localization. OEM commitments such as GM’s powertrain revamp and Bosch’s SiC wafer project support a resilient domestic value chain[4]“Bosch Expands SiC Production with CHIPS Act Support,” Robert Bosch GmbH, bosch.com . U.S. policy links EV tax credits to North American content, pushing tiers to expand Mexican and Canadian capacity. The region favors premium ADAS actuation and high-power HVAC solutions for large pickups and SUVs, ensuring diverse demand in the automotive motors market.

Europe positions itself as the regulatory vanguard and premium engineering hub. Emissions ceilings narrow and Euro-NCAP star ratings grow stricter, sustaining appetite for efficient BLDC blowers and safety-grade servo units. As exemplified by Schaeffler closing its Vitesco acquisition, mergers create end-to-end electric drive portfolios that capture traction, auxiliary, and power electronics demand. Municipal zero-emission zones accelerate 48 V city-delivery van adoption, entrenching demand for compact, high-torque motors tailored to stop-start cycles.

Competitive Landscape

The automotive motors market shows moderate concentration, with Bosch, Denso, Nidec, and Mitsubishi Electric controlling multi-application portfolios spanning comfort to traction categories. Their vertically integrated footprints covering design, magnet manufacturing, inverter development, and embedded software create cost and validation synergies prized by global OEMs. Scale backs recurring R&D and purchasing leverage, keeping entry hurdles high.

Consolidation heats up as suppliers chase electrification breadth. Schaeffler’s 2024 Vitesco deal adds traction inverters and 800 V technologies to its e-axle lineup, challenging traditional motor specialists. Start-ups target niches such as axial-flux architectures and magnet-free switched-reluctance designs, pitching raw-material resilience. Yet certification demands and warranty liabilities limit rapid displacement.

Technology differentiation depends on silicon-carbide integration, harmonic-reduction winding patterns, and over-the-air-updatable control firmware. Bosch’s CHIPS Act-funded fab underpins domestic SiC supply, while GM patents grain-oriented steel rotors to raise flux density. Tier-ones also court software revenue by bundling predictive maintenance analytics that flag bearing wear or demagnetization events before failures, reinforcing customer stickiness in the automotive motors market.

Automotive Motors Industry Leaders

Robert Bosch GmbH

DENSO Corporation

Nidec Corporation

Continental AG

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Bosch and Farizon Auto signed a strategic cooperation agreement at Auto Shanghai 2025 to co-develop methanol-hydrogen-electric technologies and deploy 1,000 commercial vehicles in H2 2025.

- April 2025: Bosch partnered with X-Motors and CATL to open Indonesia’s first Bosch Car Service flagship center in Jakarta, with plans to expand to 120 locations.

- March 2025: Samvardhana Motherson invested USD 5–7 million to maintain its 18.6% stake in REE Automotive and accelerate the commercialization of the REEcorner integrated wheel module.

Global Automotive Motors Market Report Scope

| DC Motor |

| Brushless DC Motor (BLDC) |

| Stepper Motor |

| Traction Motor |

| Servo Motor |

| Powertrain |

| Comfort Systems |

| Safety Systems |

| HVAC |

| Infotainment |

| Others |

| Two-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Heavy Commercial Vehicles (HCVs) |

| Off-Highway Vehicles |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Motor Type | DC Motor | |

| Brushless DC Motor (BLDC) | ||

| Stepper Motor | ||

| Traction Motor | ||

| Servo Motor | ||

| By Application | Powertrain | |

| Comfort Systems | ||

| Safety Systems | ||

| HVAC | ||

| Infotainment | ||

| Others | ||

| By Vehicle Type | Two-Wheelers | |

| Passenger Cars | ||

| Light Commercial Vehicles (LCVs) | ||

| Heavy Commercial Vehicles (HCVs) | ||

| Off-Highway Vehicles | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the automotive motors market in 2025, and what growth is expected by 2030?

It is valued at USD 37.85 billion in 2025 and is projected to reach USD 47.68 billion by 2030 on a 4.73% CAGR trajectory.

Which motor type holds the most significant revenue share?

Brushless DC motors lead with 41.27% share in 2024, driven by superior efficiency and durability.

Which application segment is expanding fastest?

Safety systems show the strongest momentum, advancing at a 4.86% CAGR through 2030 as ADAS features become standard.

What region dominates demand?

Asia-Pacific commands 46.53% of 2024 revenue and remains the fastest-growing region at a 4.81% CAGR.

How concentrated is supplier competition?

The market earns a moderate concentration score due to the few top suppliers control majority of the global revenue.

What is the key raw material challenge for motor makers?

Volatile copper and rare-earth prices squeeze margins and encourage the development of magnet-light or alternative-topology designs.

Page last updated on: