Automotive Electronics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 303.41 Billion |

| Market Size (2030) | USD 435.58 Billion |

| Growth Rate (2025 - 2030) | 7.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Electronics Market Analysis by Mordor Intelligence

The Automotive Electronics Market size is estimated at USD 303.41 billion in 2025, and is expected to reach USD 435.58 billion by 2030, at a CAGR of 7.75% during the forecast period (2025-2030).

Expanding electronic content per vehicle, regulatory mandates for safety and emissions, and accelerating electrification keep demand resilient across vehicle classes. Semiconductor content now drives most innovation cycles, while zonal architectures enable over-the-air updates that lower lifetime software costs. After recent chip shortages, supply-chain resilience, particularly in wide-bandgap devices, has become a strategic priority. Competitive intensity rises as traditional Tier-1 suppliers defend system-integration strengths against fabless and IDM semiconductor entrants targeting high-value ADAS and power-train domains.

Key Report Takeaways

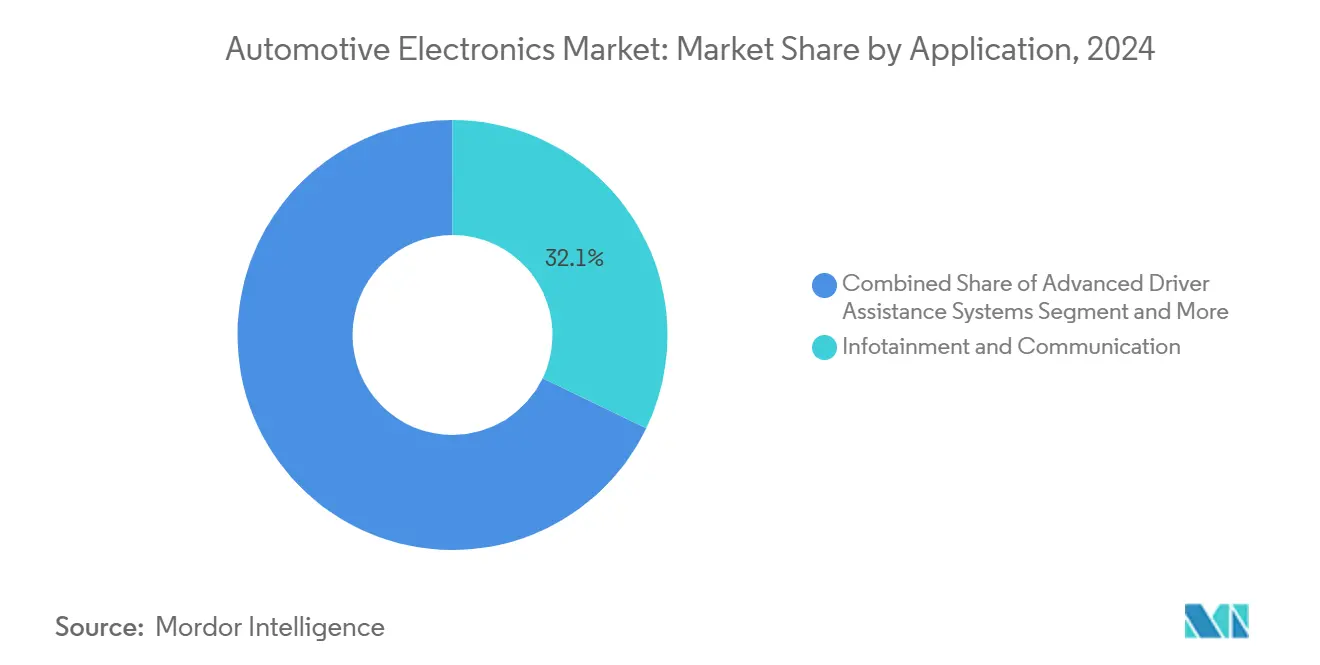

- By application, infotainment and communication led with a 32.13% of the automotive electronics market share in 2024, whereas advanced driver assistance systems is advancing at a 10.79% CAGR.

- By component, microcontrollers accounted for 30.11% of the automotive electronics market share in 2024, while power electronics is expected to grow at an 11.14% CAGR to 2030.

- By vehicle type, passenger vehicles commanded 64.29% of the automotive electronics market share in 2024, yet electric vehicles exhibit a 13.21% CAGR to 2030.

- By propulsion, internal-combustion models retained 62.71% of the automotive electronics market share in 2024, but electric propulsion is projected to rise at a 13.61% CAGR through 2030.

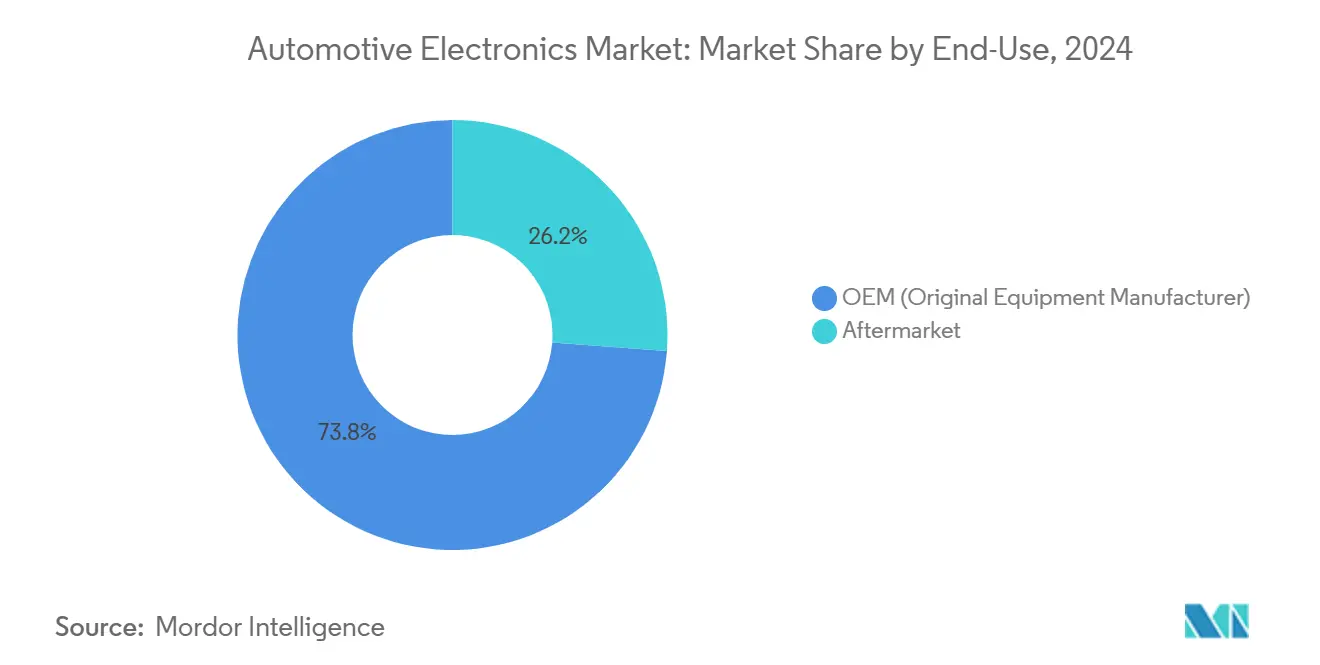

- By end-use, OEM channels captured 73.82% of the automotive electronics market share in 2024, while the aftermarket segment is on track for a 10.72% CAGR to 2030.

- By sales channel, direct agreements represented 47.36% of the automotive electronics market share in 2024, whereas online platforms are forecast to expand at an 11.71% CAGR through 2030.

- By geography, Asia-Pacific held 43.81% of the automotive electronics market share in 2024, while it is also projected to post the fastest 11.29% CAGR through 2030.

Global Automotive Electronics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Powertrain Electrification Surge | +2.1% | Global; China, Europe, California | Long term (≥ 4 years) |

| Tightening ADAS Safety Mandates | +1.8% | Global; Europe and China lead | Medium term (2-4 years) |

| Shift to Software-Defined Vehicles and OTA | +1.4% | Global; premium segments | Medium term (2-4 years) |

| Rise of Zonal E/E Architectures | +1.2% | Global; premium OEMs | Long term (≥ 4 years) |

| Automotive Semiconductor Cost Decline | +0.9% | Global; Asia-Pacific cost edge | Short term (≤ 2 years) |

| OEM Monetization of In-Car Data and Services | +0.8% | North America and Europe; expanding Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification of Vehicle Powertrains

China’s passenger-car EV share reached 35.7% in 2024, and Europe crossed 20% despite macroeconomic pressure[1]. Power electronics increasingly drive value in battery electric vehicles (BEVs), outpacing their presence in conventional cars. Silicon-carbide devices, now approved for high-voltage traction inverters, deliver performance and cost benefits compared to their traditional silicon counterparts. With the rising complexity of battery packs, battery management electronics are commanding a bigger portion of the overall system cost. In a bid to remain competitive, traditional Tier-1 suppliers are either partnering with or acquiring semiconductor companies. This strategy bridges gaps in high-voltage design and manufacturing, solidifying their foothold in the electrified vehicle landscape.

Stringent ADAS Safety Mandates

The July 2024 enforcement of the EU General Safety Regulation Phase 2 forces every new model to integrate Automatic Emergency Braking, Lane Keeping Assist, and Driver Monitoring Systems. Similar rules appear in China and the United States, where NHTSA will grade AEB performance in the New Car Assessment Program by 2026[2]“NCAP Roadmap 2025,”, National Highway Traffic Safety Administration, nhtsa.gov. As regulations mandate using multiple radar, camera, and LiDAR channels, the push for advanced driver-assistance systems drives up vehicle semiconductor content. In addition to regulatory pressures, insurance incentives are further fueling this adoption. Moreover, global standards, such as UN-ECE’s lane-keeping rules, streamline designs and reduce fragmentation. This alignment bolsters the argument for scalable electronics platforms and underscores the pivotal role of semiconductor suppliers in the journey towards automotive autonomy.

Shift Toward Software-Defined Vehicles and OTA Updates

The shift to centralized compute nodes with virtualization streamlines vehicle architecture by replacing discrete domain controllers, reducing wiring complexity, and enabling seamless feature upgrades. Over-the-air update capability is rapidly expanding, especially in premium models, unlocking new revenue streams through subscriptions for features like full self-driving and connectivity. Compliance with cybersecurity standards such as ISO/SAE 21434 is increasing development complexity and timelines. OEMs explore subscription revenue streams, following Tesla’s annual USD 1.5 billion in FSD and connectivity sales. Supplier ecosystems reorganize around software platforms, sparking alliances between automakers and cloud providers[3]“2024 Impact Report,”, Tesla Inc., tesla.com.

Emergence of Zonal E/E Architectures

Premium OEMs migrate to zonal topologies that consolidate functions and slash wiring length[4]“Automotive Electronics 2025 Portfolio,”, Bosch GmbH, bosch.com. Centralized platforms ease software distribution and facilitate functional upgrades through OTA. The architecture also future-proofs hardware, allowing processors to be swapped without major harness redesigns. Suppliers focus R&D on high-speed Ethernet backbones, galvanic isolation, and advanced thermal materials to handle higher power densities in fewer enclosures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive Chip Supply Volatility | -1.3% | Global; Asia-Pacific concentration risk | Short term (≤ 2 years) |

| High Integration and Validation Costs | -0.9% | Global; regulated markets | Medium term (2-4 years) |

| Cybersecurity and Safety Compliance Burden | -0.7% | Global; strictest in Europe and United States | Long term (≥ 4 years) |

| Thermal Limits in Compact ECU Designs | -0.5% | Global; high-performance use cases | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Volatility in Automotive Chips

The industry faces significant geopolitical and natural disaster exposure, with most automotive semiconductors fabricated in East Asia. Events like the TSMC production halt have extended lead times for key components such as microcontrollers. Dual sourcing is challenging due to lengthy qualification cycles and limited capacity for advanced substrates like silicon carbide. OEMs are responding by holding higher inventory levels, which strains working capital and may accelerate consolidation among smaller suppliers unable to absorb the financial impact, reshaping the competitive landscape of the automotive electronics market.

High Integration and Validation Costs for New Electronics

Stringent validation requirements, including AEC-Q, ISO 16750, ISO 26262, and Automotive SPICE, are significantly impacting automotive electronics development costs and timelines. The need for a substantial upfront investment in testing infrastructure and prolonged go-to-market cycles poses formidable entry barriers. This challenge is especially pronounced for smaller innovators venturing into domains like V2X communication and sensor fusion. Consequently, these innovators are increasingly turning to partnerships or licensing agreements with established Tier-1 companies as vital routes to commercialization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: ADAS Drives Next-Generation Growth

Advanced Driver Assistance Systems account for the quickest 10.79% C AGR, delivering the most significant incremental revenue through 2030. Infotainment & Communication retained 32.13% of 2024 revenue, demonstrating entrenched consumer demand for connected services. ADAS semiconductor value per vehicle rose after July 2024 regulatory deadlines, lifting the automotive electronics market size within the application stack. Centralized sensor fusion platforms now host multiple Level 2+ functions, and safety standards create a global baseline that streamlines homologation. Insurers in Europe offer discounts for compliant vehicles, reinforcing adoption.

Continuing integration pulls camera, radar, and LiDAR feeds into a common compute, reducing redundant ECUs. Infotainment systems converge with digital cockpits using 3-nm GPUs, while subscription features for streaming and navigation enter mid-segment vehicles. Body electronics gain share from expanding comfort functions such as zoned climate control. OTA capability lets OEMs monetize feature unlocks during ownership, embedding recurring revenue in the automotive electronics market.

By Component Type: Power Electronics Leads Innovation Wave

Power electronics grow at 11.14% CAGR, the fastest within the component mix, as silicon-carbide traction inverters migrate from premium to mid-range EVs. Microcontrollers secured the highest 30.11% 2024 revenue, underscoring their ubiquity. The automotive electronics market share for wide-bandgap devices will expand as production ramp-ups in Japan and the United States lower substrate cost. Thermal-interface material upgrades enable higher junction temperatures, simplifying cooling.

Sensor shipments climb alongside ADAS and thermal-management monitoring. Zonal controllers substitute many low-end ECUs, increasing function density per board. Displays transition to OLED and micro-LED, enhancing power efficiency and enabling flexible form factors across dashboards. Connector makers innovate high-speed, high-current solutions for 48 and 800 V systems, ensuring reliability over vehicle lifetimes.

By Vehicle Type: Electric Transition Reshapes Electronics Content

Electric vehicles grow 13.21% annually to 2030, surpassing the broader automotive electronics market. Passenger cars held 64.29% of 2024 units, buoyed by safety mandates and infotainment trends. Commercial fleets accelerate electrification for urban logistics because the total cost of ownership now favors battery systems. Content differentials of USD 2,000–4,000 per EV attract semiconductor and thermal-management suppliers seeking higher margins.

Electric buses and delivery vans adopt 800 V architectures, demanding upgraded traction inverters and onboard chargers across the automotive electronics market. Heavy-duty trucks test fuel-cell range-extenders, introducing power-electronics complexity that blends proton-exchange membranes with lithium-ion buffers. Conventional vehicles integrate start-stop and 48 V mild hybrid subsystems, preserving baseline demand for ignition and body control ECUs.

By Propulsion Type: Electric Architecture Transformation

Electric propulsion delivers 13.61% CAGR, redefining electronic architectures. The automotive electronics market size tied to internal-combustion platforms shrinks despite content additions for emission compliance. Battery management systems now apply model-based algorithms to 300-plus cell packs, increasing controller sophistication. Silicon-carbide inverters achieve 98% efficiency, extending real-world range and cutting heat load.

Hybrid vehicles remain a bridge where charging networks lack density. They combine high-voltage traction hardware with 12 V legacy systems, keeping demand diversified across microcontrollers, sensors, and DC-DC converters. Fuel-cell prototypes drive R&D investment in hydrogen pressure monitoring, stack control, and high-voltage boost converters.

By End-Use: Aftermarket Digitization Accelerates

The aftermarket posts a 10.72% CAGR as vehicle lifespans lengthen. Retrofit ADAS kits and telematics dongles expand the addressable pool outside new-car channels, lifting the automotive electronics market. Independent repair shops adopt advanced diagnostics to service 150-plus ECU architectures. Parts suppliers create plug-and-play modules with guided installation to offset rising system complexity.

OEMs defend their share by offering certified retrofit upgrades through dealer networks. Subscription software unlocks additional revenue without hardware change, influencing the broader automotive electronics market, although European right-to-repair laws mandate data access for independent operators. Online portals facilitate aftermarket part identification, improving transparency and shortening lead times.

By Sales Channel: Digital Transformation Gains Momentum

Online platforms compound at 11.71% through 2030 as procurement shifts to e-commerce. Direct OEM arrangements still held 47.36% of the 2024 flow because safety-critical parts need tight integration. The automotive electronics market now leverages B2B marketplaces that pair technical filters with logistics services, enabling smaller Tier-2 suppliers to reach global buyers.

Distributors pivot toward design-in support, simulation tools, and kitting services, enhancing their role in the automotive electronics market. Augmented-reality applications allow remote troubleshooting, saving travel costs and accelerating design cycles. Customer experience improves through real-time inventory visibility and predictive delivery windows, aligning with lean manufacturing goals.

Geography Analysis

Asia-Pacific controlled 43.81% of 2024 revenue and led growth at 11.29% CAGR. China’s EV policies and semiconductor localization drive volume, while Japanese IDMs remain strong in microcontrollers and power MOSFETs. South Korea invests in automotive DRAM and AI accelerators, leveraging foundry capacity. The regional automotive electronics market faces geopolitical risk from concentrated wafer capacity, prompting local governments to co-fund new fabs in Singapore and Malaysia.

Europe is the second-largest bloc, benefitting from the EU General Safety Regulation and fit-for-55 emission targets. German OEMs spearhead software-defined vehicle projects, partnering with cloud hyperscalers to shorten development cycles. Government incentives for battery gigafactories support local power-electronics supply chains. Brexit-related customs changes add marginal cost, yet the region gains from a strong Tier-1 presence in ADAS and chassis control.

North America experiences steady expansion under California’s Advanced Clean Cars II and U.S. tax credits of up to USD 7,500 for qualifying EVs. Mexico grows as a manufacturing hub, taking advantage of USMCA and lower labor costs, while Canada attracts inverter and battery-materials investment. Longer vehicle age in the United States sustains aftermarket demand for retrofit connectivity and ADAS kits, enlarging the automotive electronics market across service channels.

Competitive Landscape

The automotive electronics market remains moderately concentrated. Bosch, Continental, and Denso deliver full-system solutions, while Infineon, NXP, and STMicroelectronics lead component innovation. They reflect balanced competition. Recent alliances, such as the May 2025 Denso-Rohm silicon-carbide joint venture, illustrate vertical cost and supply security collaboration. Tesla and Samsung committed USD 16.5 billion to custom AI processors in July 2025, signaling OEM efforts to own critical silicon.

Acquisitions focus on cybersecurity, as shown by Continental’s March 2025 purchase of Argus Cyber Security. Patent filings intensify in sensor fusion and zonal architecture, with leading suppliers protecting unique IP to defend margins. Foundries diversify into automotive-grade capacity in Singapore and Texas, reducing single-region risk and supporting future automotive electronics market growth.

Automotive Electronics Industry Leaders

Robert Bosch GmbH

Continental AG

Denso Corporation

Aptiv PLC

Panasonic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Tesla and Samsung Electronics announced a USD 16.5 billion partnership for advanced automotive semiconductors, including custom AI processors for Full Self-Driving applications.

- May 2025: Denso and Rohm formed a joint venture to cut silicon-carbide device costs by 40% by 2027.

- October 2024: Denso licensed neural-processing-unit IP from Quadric to achieve 10× inference speed improvements in ADAS.

Global Automotive Electronics Market Report Scope

| Advanced Driver Assistance Systems (ADAS) |

| Infotainment and Communication |

| Powertrain Control |

| Body Electronics |

| Safety Systems |

| Others |

| Electronic Control Units (ECUs) |

| Sensors |

| Microcontrollers |

| Integrated Circuits |

| Displays |

| Connectors |

| Others |

| Passenger Vehicles |

| Commercial Vehicles |

| Internal Combustion Engine (ICE) |

| Hybrid Vehicle |

| Electric Vehicle |

| OEM (Original Equipment Manufacturer) |

| Aftermarket |

| Direct Sales |

| Distributors |

| Online Platforms |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Advanced Driver Assistance Systems (ADAS) | |

| Infotainment and Communication | ||

| Powertrain Control | ||

| Body Electronics | ||

| Safety Systems | ||

| Others | ||

| By Component Type | Electronic Control Units (ECUs) | |

| Sensors | ||

| Microcontrollers | ||

| Integrated Circuits | ||

| Displays | ||

| Connectors | ||

| Others | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Hybrid Vehicle | ||

| Electric Vehicle | ||

| By End-Use | OEM (Original Equipment Manufacturer) | |

| Aftermarket | ||

| By Sales Channel | Direct Sales | |

| Distributors | ||

| Online Platforms | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the 2025 value of the automotive electronics market?

The sector totals USD 303.41 billion in 2025 under current estimates.

How fast will electronic content per car grow through 2030?

Content rises with a 7.75% CAGR, outpacing vehicle unit growth due to electrification and safety mandates.

Which application will add the most new revenue by 2030?

ADAS leads incremental growth at a 10.79% CAGR as regulations mandate advanced safety systems.

Which region will expand fastest in this space?

Asia-Pacific grows the quickest at 11.29% CAGR, driven by China’s aggressive EV policies and semiconductor investment.

What technology shift will most influence future architectures?

The move to zonal E/E platforms enables over-the-air software updates and reduces wiring complexity, reshaping vehicle electronics design.

Page last updated on: