Automotive Electronic Stability Control Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

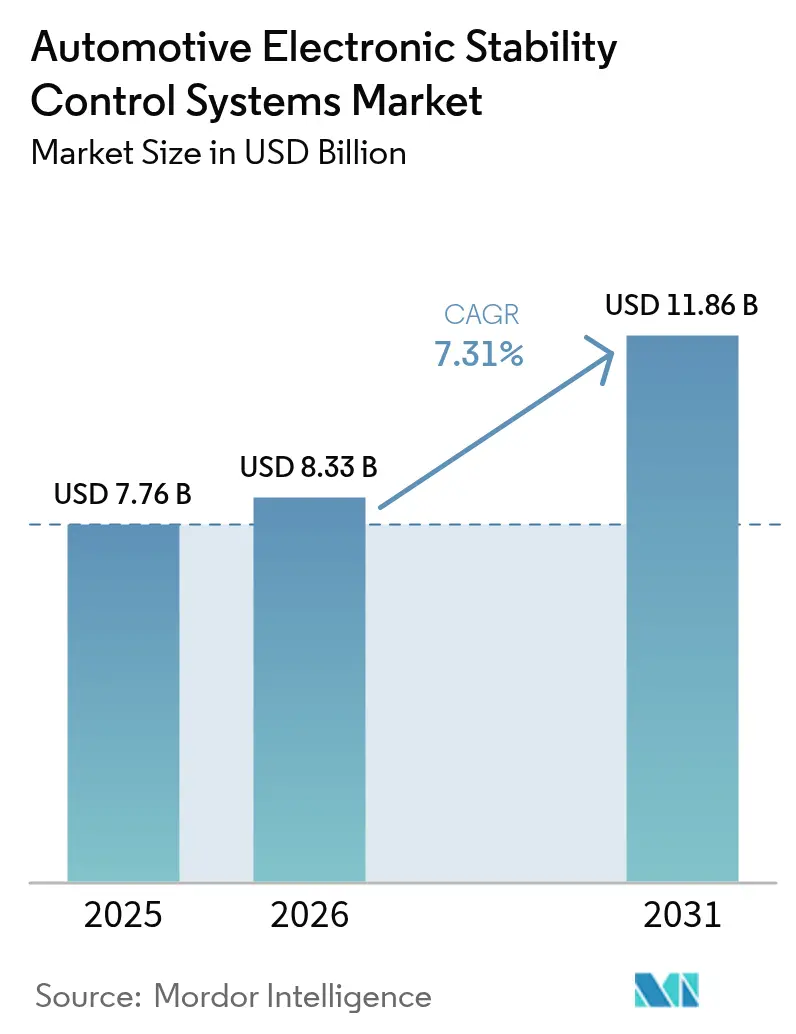

| Market Size (2026) | USD 8.33 Billion |

| Market Size (2031) | USD 11.86 Billion |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

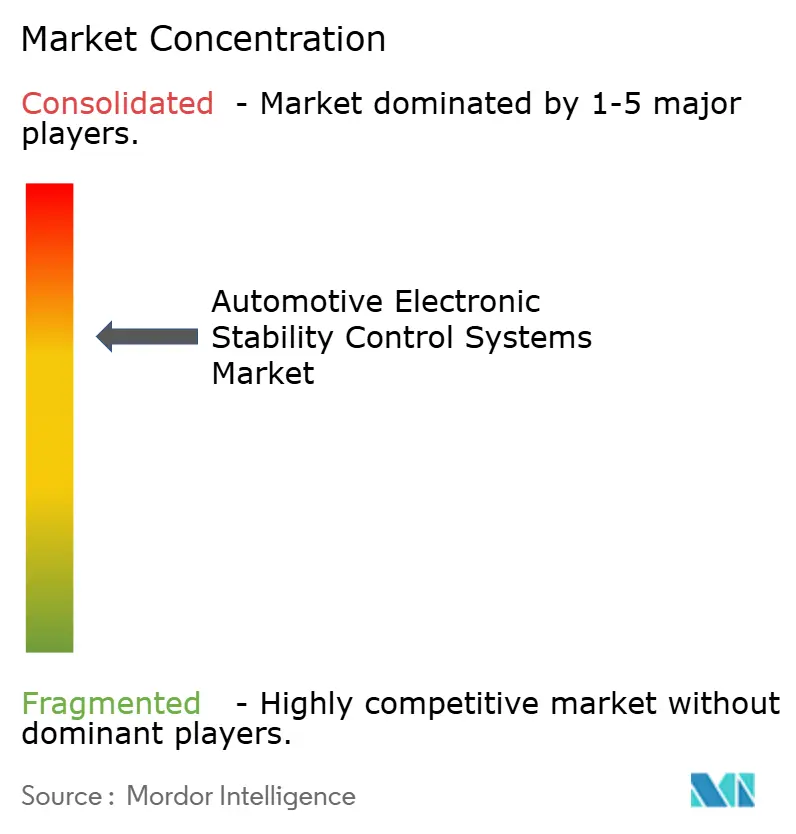

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Electronic Stability Control Systems Market Analysis by Mordor Intelligence

The automotive electronic stability control market size was valued at USD 7.76 billion in 2025 and estimated to grow from USD 8.33 billion in 2026 to reach USD 11.86 billion by 2031, at a CAGR of 7.31% during the forecast period (2026-2031). Growth stems from regulatory mandates that embed stability control into every new vehicle platform, rising electric-vehicle penetration that heightens regenerative-braking complexity, and automakers’ pivot toward software-defined architectures that demand real-time vehicle-dynamics management. Suppliers use integrated hardware-software stacks to trim bill-of-materials costs, while brake-by-wire programs compress actuator response times and unlock predictive control logic. In parallel, Asia-Pacific production scale reduces per-unit electronics costs, North American OEMs package ESC with advanced driver-assistance functions to lift consumer value perception, and European policymakers tighten safety requirements that ripple through export supply chains. Semiconductor content inflation remains the key margin risk, pushing tier-1s to differentiate through algorithm portfolios rather than commodity sensors.

Key Report Takeaways

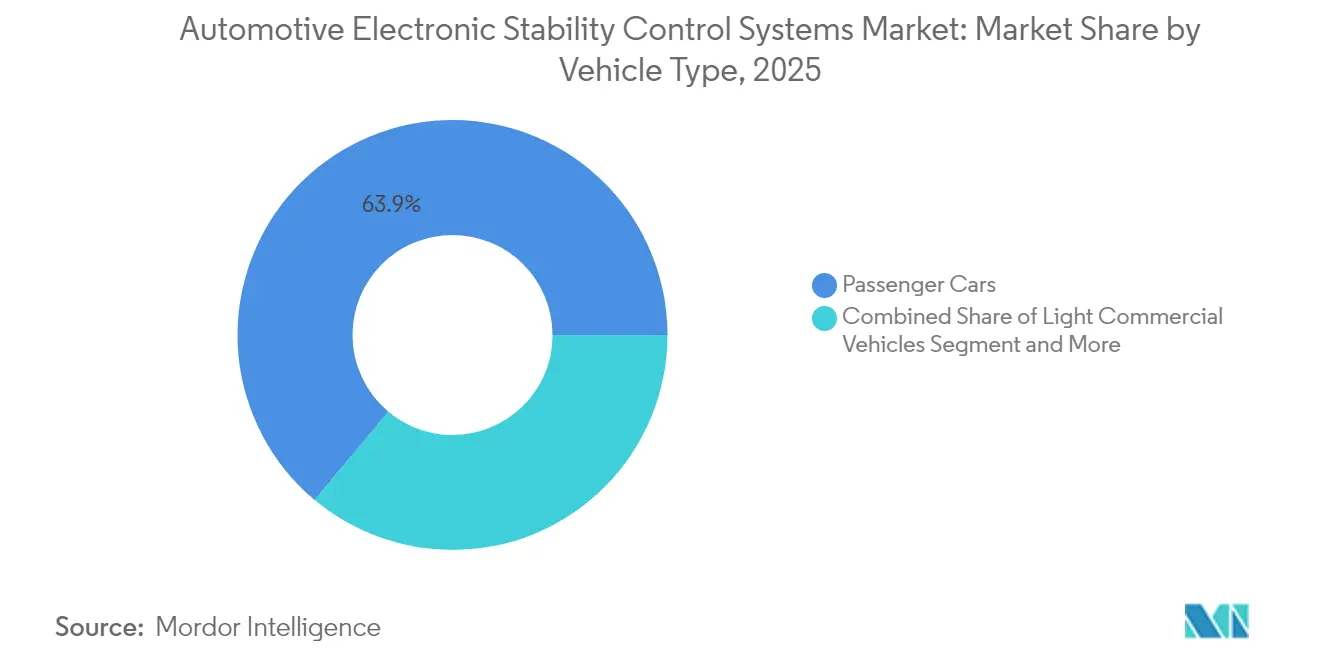

- By vehicle type, passenger cars led with 63.92% of the automotive electronic stability control market share in 2025 and are anticipated to grow at 7.62% CAGR through 2031.

- By component, sensors commanded a 44.25% share of the automotive electronic stability control market size in 2025, while software and algorithms recorded the fastest CAGR at 17.65% to 2031.

- By technology, hydraulic systems held 70.21% revenue share in 2025; electro-hydraulic and electro-mechanical systems are advancing at a 18.74% CAGR.

- By propulsion type, internal-combustion vehicles accounted for 57.71% of the automotive electronic stability control market size in 2025, whereas battery-electric vehicles posted the highest 21.96% CAGR.

- By sales channel, OEM-fitted installations captured 88.95% share in 2025, while the aftermarket segment grew at 15.28% CAGR.

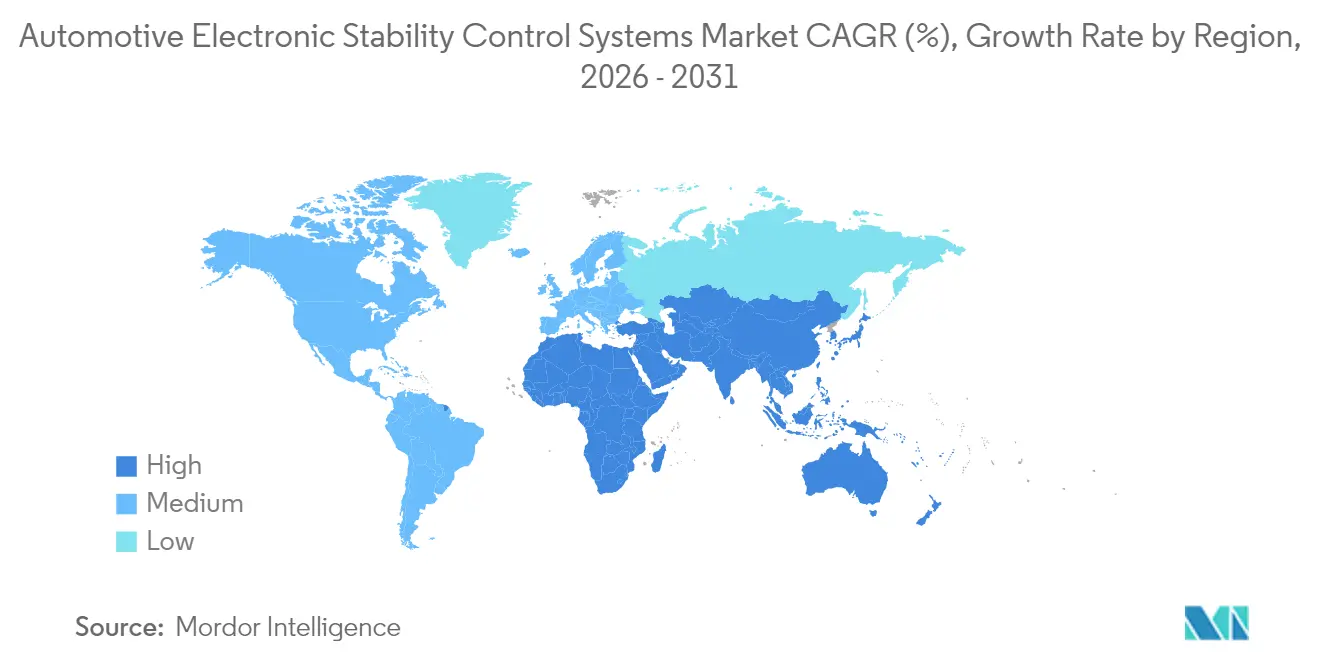

- By geography, Asia-Pacific represented 48.12% of the automotive electronic stability control market share in 2025; the Middle East & Africa region is set to grow the fastest at a 10.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Electronic Stability Control Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory ESC Legislation In Light-Vehicles | +2.8% | Global, with EU and North America leading | Short term (≤ 2 years) |

| Rapid ADAS And Automated-Driving Adoption | +2.1% | North America & EU core, APAC following | Medium term (2-4 years) |

| EV-Specific Regenerative-Braking Stability Needs | +1.6% | Global, with China and EU leading | Medium term (2-4 years) |

| Transition Toward Brake-By-Wire Architectures | +1.4% | Premium segments globally | Long term (≥ 4 years) |

| Growing Focus On 5-Star NCAP Ratings | +0.9% | Europe, North America, expanding to APAC | Short term (≤ 2 years) |

| Rising Light-Vehicle Output In Emerging Economies | +0.7% | APAC core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory ESC Legislation in Light-Vehicle Categories

Global rulemaking elevates the automotive electronic stability control market from an optional technology to a compulsory vehicle sub-system. The European Union’s General Safety Regulation II, in force for new models from July 2024, obliges every passenger vehicle and light commercial vehicle to incorporate ESC along with other active-safety functions. Comparable standards apply in the United States under FMVSS 126[1]“49 CFR Parts 571 and 585 [Docket No. NHTSA-2007-27662],” National Highway Traffic Safety Administration, nhtsa.gov. Harmonised deadlines motivate OEMs to integrate ESC at the platform-definition stage, fuelling bulk supply agreements that lower the cost per channel. This scale benefit is especially pronounced in compact-car segments, where prior option-take rates were modest. Component makers must therefore synchronize validation, homologation, and software-release calendars across three continents, shortening development loops and raising the value of modular architectures that can be flashed for brand-specific pedal-feel tuning.

Rapid ADAS and Automated-Driving Adoption

Lane-keeping, automatic emergency braking, and adaptive cruise control rely on a stable chassis attitude during sensor-fusion events. ESC thus becomes the backbone of the domain controller, shifting its role from reactive skid correction to predictive trajectory governance. Centralized compute platforms feed yaw-rate, lateral-acceleration, and steering-angle data into machine-learning models that forecast friction limits and pre-condition brake pressure. The outcome is smoother intervention, which improves passenger comfort and reduces warranty claims. Higher processor throughput also enables suppliers to push over-the-air updates that refine algorithm parameters without workshop visits, creating annuity revenue streams inside the automotive electronic stability control market.

EV-Specific Regenerative-Braking Stability Needs

Electric powertrains inject variable deceleration torque into the driveline, forcing ESC to arbitrate between regenerative and hydraulic braking. Real-time coordination secures significant energy-recovery efficiency while preventing wheel lock-up during abrupt pedal inputs. In cold climates, battery temperature swings alter regen capacity, so ESC logic must seamlessly transition to friction brakes. Tier-1s respond with electro-hydraulic boosters that blend torque within milliseconds, a capability now specified by most Chinese premium EV programs. As battery-electric volumes rise, this use case accelerates procurement of high-bandwidth sensors and drives incremental silicon demand that benefits semiconductor vendors anchored in the Electronic Stability Control industry.

Transition Toward Brake-by-Wire Architectures

Replacing physical fluid columns with wires slashes response latency and allows four-corner pressure individualisation. A 2025 supply contract covering nearly 5 million vehicles demonstrates OEM trust in electro-mechanical actuation performance[2]Sebastian Blanco, “CES 2025 Bosch mobility,” SAE, sae.org . Brake-by-wire also future-proofs platforms for Level 3 automated driving because it supports redundant power domains. The architecture’s complexity elevates software content to nearly half of the total system cost, creating a battleground for middleware APIs, diagnostics, and functional-safety libraries. Suppliers that master these stacks secure integration stickiness that is difficult for low-cost imitators to dislodge, making brake-by-wire a structural accelerator for the automotive electronic stability control market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront and Lifecycle Cost | -1.8% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Platform Saturation In Mature Markets | -1.2% | North America & Europe primarily | Medium term (2-4 years) |

| Networked ESC ECU’s Cybersecurity Risks | -0.7% | Global, with highest concern in premium segments | Long term (≥ 4 years) |

| Suspension/Tyre Retrofit Calibration Issues | -0.5% | Aftermarket segments globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront and Lifecycle Cost of ESC Modules

At USD 300 to 800 per vehicle in stand-alone form and escalating toward USD 2,000 when bundled with radar, the bill can absorb a double-digit share of entry-segment transaction prices. Semiconductor inflation doubles the per-vehicle electronics spend by 2030, prompting OEMs to demand volume discounts and local sourcing. On the ownership side, post-collision repairs cost 50-100% more when calibration rigs are required. Fleets therefore evaluate total-cost-of-operation rather than headline retail prices, slowing penetration in informal ride-sharing markets and ageing car parks.

Platform Saturation in Mature Markets

United States passenger cars have carried mandatory ESC since model-year 2012; Western Europe followed a similar timing, pushing penetration above 95%. Consequently, growth now hinges on replacement cycles and feature upgrades such as predictive-yaw modules. Suppliers compensate through software sales and data analytics services, but total unit shipments plateau. This saturation drags the average automotive electronic stability control market CAGR in developed economies below the global mean, encouraging vendors to redirect investment toward high-growth emerging regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger-Car Dominance with EV Tailwinds

Passenger cars generated 63.92% of 2025 revenue in the automotive electronic stability control market, supported by legal mandates and consumer safety awareness. Light commercial vehicles contribute a sizeable demand as e-commerce accelerates urban delivery traffic that benefits from rollover mitigation. The passenger cars segment is anticipated to witness the fastest growth rate during the forecast period, marking a CAGR of 7.62%, primarily due to battery electric cars, requiring torque-vectoring logic that keeps high-instant-torque drivetrains on course.

In premium sedans, ESC algorithms coordinate with active-suspension dampers to manage weight transfer during rapid lane changes, a feature now standard in Europe’s C-segment. Fleet operators of delivery vans employ telematics portals that feed ESC-trigger events into driver-coaching dashboards, cutting insurance claims. These usage cases illustrate how software analytics enlarge the value pool inside the Automotive electronic stability control market beyond hardware margins.

By Component: Sensor Weight Today, Software Upside Tomorrow

Sensor assemblies held 44.25% of 2025 spend, reflecting the need for gyroscopes, accelerometers, and wheel-speed pick-ups that capture vehicle-dynamics data. Software and algorithm stacks, however, advance at 17.65% CAGR as OEMs migrate to centralized compute zones. Electronic control units remain the nerve centre, balancing data bus bandwidth and real-time operating-system determinism.

Algorithm suppliers exploit over-the-air pipelines to extend feature life, enabling subscription-based performance modes that unlock more aggressive torque allocation on track days. As vehicles transition to gigabit Ethernet backbones, sensor fusion broadens to include lidar and camera feeds, further pushing the automotive electronic stability control market toward digital rather than mechanical differentiation.

By Technology: Hydraulic Legacy versus Electro-Mechanical Future

Hydraulic platforms preserved a 70.21% share in 2025 because of cost efficiency and field-service familiarity. Yet, electro-hydraulic and fully electro-mechanical solutions accelerate at 18.74% CAGR, propelled by brake-by-wire projects in premium EVs. Cost curves fall as modular motor-pump units replace cast-iron master cylinders, trimming mass and eliminating hydraulic fluid reservoirs.

The performance delta is visible in stopping-distance benchmarks: electro-mechanical units cut dry-surface braking distance by up to 6 m from 100 km/h compared with legacy pumps. Government crash-avoidance protocols increasingly measure this metric, fuelling OEM migration. Consequently, value migrated from steel fabrication to firmware, reshaping supplier power dynamics in the electronic stability control industry.

By Propulsion Type: ICE Majority, BEV Momentum

Internal-combustion platforms retained 57.71% revenue in 2025, yet battery-electric vehicles log a superior 21.96% CAGR to 2031. Hybrids straddle both camps, adding algorithm complexity that oversees mode-switch brake-pressure harmonization. The market size for battery-electric SUVs alone is forecast to surpass USD 6.08 billion by 2031.

High-density battery packs lower centre-of-gravity but introduce rear-axle mass bias; ESC compensates through front-rear torque apportioning. In plug-in hybrids, powertrain blending demands yaw-torque smoothing during engine-start events. Suppliers that master these edge cases win program nominations, expanding the software licensing component of the electronic stability control market revenue.

By Sales Channel: OEM Standard-Fit Supremacy, Aftermarket Niche

OEM installations absorbed 88.95% of 2025 shipments as regulatory timelines aligned with model-launch cycles. Factory fitment ensures sensor placement accuracy and permits platform-wide software reuse. Aftermarket retrofits, while growing at 15.28% CAGR, face workshop skill gaps and homologation hurdles.

Retrofit demand concentrates in fleets subject to new safety laws for existing vehicles. Calibration rigs that map yaw-sensor zero-points to tyre sizes are scarce, capping short-term volume. Nevertheless, some specialist service chains bundle ESC upgrades with suspension kits, illustrating a niche yet profitable pocket inside the automotive electronic stability control market.

Geography Analysis

Asia-Pacific contributed 48.12% of global revenue in 2025, while the Middle East and Africa are expected to be the fastest-growing regions with a 10.66% CAGR through 2031. China’s automakers extended production into ASEAN, lifting regional light-vehicle output projections from 4.2 million to nearly 6 million units by the mid-2030s. Government incentives for new-energy vehicles accelerate software-centric braking adoption, while local semiconductor fabs shorten supply chains. India’s industrial policy seeks a USD 1 trillion automotive turnover by 2035, carving further runway for the electronic stability control market expansion. Japan and South Korea supply actuator and ECU expertise, anchoring technology leadership.

North America exhibits a mature yet stable trajectory. Mandated fitment since model-year 2012 saturates new-car penetration, shifting growth to replacement units and feature upgrades such as predictive-yaw modules that integrate with L3 highway pilots. Canadian assembly plants harmonize with United States regulations, ensuring continental-scale economies. Autonomous-shuttle pilots in Sun Belt states offer a fresh outlet for bespoke electro-mechanical brake systems, extending lifecycle value for suppliers.

Europe posts a moderate CAGR under a backdrop of plateauing vehicle sales yet stringent Euro-NCAP targets. The 2024 safety regulation bundle turned advanced ESC into a baseline specification, driving focus toward software updates that refine intervention smoothness. German tier-1s pilot brake-by-wire modules tied to energy recuperation analytics, while Southern European manufacturers focus on cost-optimized hydraulic blocks for A-segment city cars. Eastern-European contract assemblers import sensor modules from Asia, reinforcing cross-regional supply networks that stabilize the Middle East & Africa, unlock the fastest regional CAGR at 10.66%, propelled by infrastructure expansion and policy alignment with UNECE safety codes. Gulf Cooperation Council fleets demand rollover mitigation in high-centre-of-gravity SUVs used on desert highways, stimulating early adoption. South America follows with 7.98% CAGR, led by Brazil’s 400,018 vehicle registrations in 2023, which heighten local content mandates. Tariffs incentivize in-region production of electronic modules, which tempers currency volatility for multinational suppliers.

Competitive Landscape

The automotive electronic stability control market features a concentrated profile anchored by long-established tier-1 suppliers. Bosch, Continental and ZF collectively control over half of global shipments, leveraging decades of system-integration know-how and patent libraries covering sensor fusion and hydraulic modulation. Contract wins often bundle ESC with steering assist and camera systems, consolidating wallet share per vehicle.

Bosch sustains leadership through integrated ADAS portfolios; its 2025 showcase at CES highlighted Intelligent Turn Assist paired with predictive braking logic sae.org. Continental’s Aumovio platform signals a strategic pivot toward software-defined vehicle ecosystems, converting legacy mechanical competencies into cloud-connected update cycles. ZF secures volume via a 5 million-vehicle brake-by-wire award that underpins confidence in electro-mechanical reliability signatures.

Smaller specialists target aftermarket retrofit kits or niche performance cars but encounter steep homologation costs that deter scale. Semiconductor suppliers gain bargaining power as silicon content doubles, encouraging vertical partnerships where brake-control algorithms run on proprietary microcontrollers. Cyber-security credentials become a bid prerequisite as vehicles connect to OEM cloud stacks; vendors now bundle intrusion-detection modules to pre-empt regulation. Overall, competitive intensity pushes tier-1s to differentiate on software and data services, reshaping revenue composition inside the electronic stability control industry.

Automotive Electronic Stability Control Systems Industry Leaders

Robert Bosch GmbH

Continental AG

Denso Corporation

ZF Friedrichshafen AG

Hyundai Mobis Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: ZF secured a contract to equip nearly 5 million vehicles with electro-mechanical brake technology that supports advanced ESC functions.

- January 2025: Bosch Limited presented Intelligent Turn Assist and Auto Vehicle Hold at Bharat Mobility Global Expo 2025, underscoring its software-defined safety portfolio.

- September 2024: Continental announced a broad aftermarket expansion, introducing multifunction camera modules and radar systems aligned with Euro 7 compliance timelines.

- October 2024: Hyundai Mobis revealed 65 new mobility technologies, including advanced braking modules vital for ESC integration in electric vehicles.

Global Automotive Electronic Stability Control Systems Market Report Scope

An automotive electronic stability control system is designed to control and maintain the stability of the vehicles. The system prevents the vehicle from skidding and prevents the vehicle from crashing.

The automotive electronic stability control system market is segmented into vehicle type, component, sales channel, and geography. Based on the vehicle type, the market is segmented into passenger cars and commercial vehicles. Based on the components, the market is segmented into sensors, ECUs, actuators, and other components. Based on the sales channel, the market is segmented into OEM and aftermarket. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, and the rest of the world.

For each segment, the market sizing and forecast have been done based on the value (USD).

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Sensors |

| Electronic Control Unit (ECU) |

| Actuator / Hydraulic Unit |

| Software and Algorithms |

| Other Components |

| Hydraulic ESC |

| Electro-Hydraulic / Electro-Mechanical ESC |

| Internal-Combustion Engine Vehicles |

| Hybrid and Plug-in Hybrid Vehicles |

| Battery-Electric Vehicles |

| OEM-Fitted |

| Aftermarket Retrofit |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Component | Sensors | |

| Electronic Control Unit (ECU) | ||

| Actuator / Hydraulic Unit | ||

| Software and Algorithms | ||

| Other Components | ||

| By Technology | Hydraulic ESC | |

| Electro-Hydraulic / Electro-Mechanical ESC | ||

| By Propulsion Type | Internal-Combustion Engine Vehicles | |

| Hybrid and Plug-in Hybrid Vehicles | ||

| Battery-Electric Vehicles | ||

| By Sales Channel | OEM-Fitted | |

| Aftermarket Retrofit | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the automotive electronic stability control market?

The automotive electronic stability control market is valued at USD 8.33 billion in 2026 and is projected to reach USD 11.86 billion by 2031.

Which vehicle type leads adoption?

Passenger cars hold 63.92% of 2025 revenue, driven by mandatory fitment rules and 5-star safety-rating demand.

How fast is the battery-electric sub-segment growing?

Battery-electric passenger cars are set to expand at a 21.96% CAGR through 2031 as regenerative-braking control becomes critical.

Why are electro-mechanical brake systems gaining traction?

They cut actuator response times, support brake-by-wire architectures, and enable autonomous-driving functions, which boosts a 18.74% CAGR for the technology segment.

Which region shows the highest growth potential?

The Middle East & Africa region leads with a 10.66% CAGR to 2031 due to infrastructure growth and harmonized safety regulations.

Page last updated on: