Automotive Hypervisor Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 0.57 Billion |

| Market Size (2031) | USD 1.51 Billion |

| Growth Rate (2026 - 2031) | 21.49% CAGR |

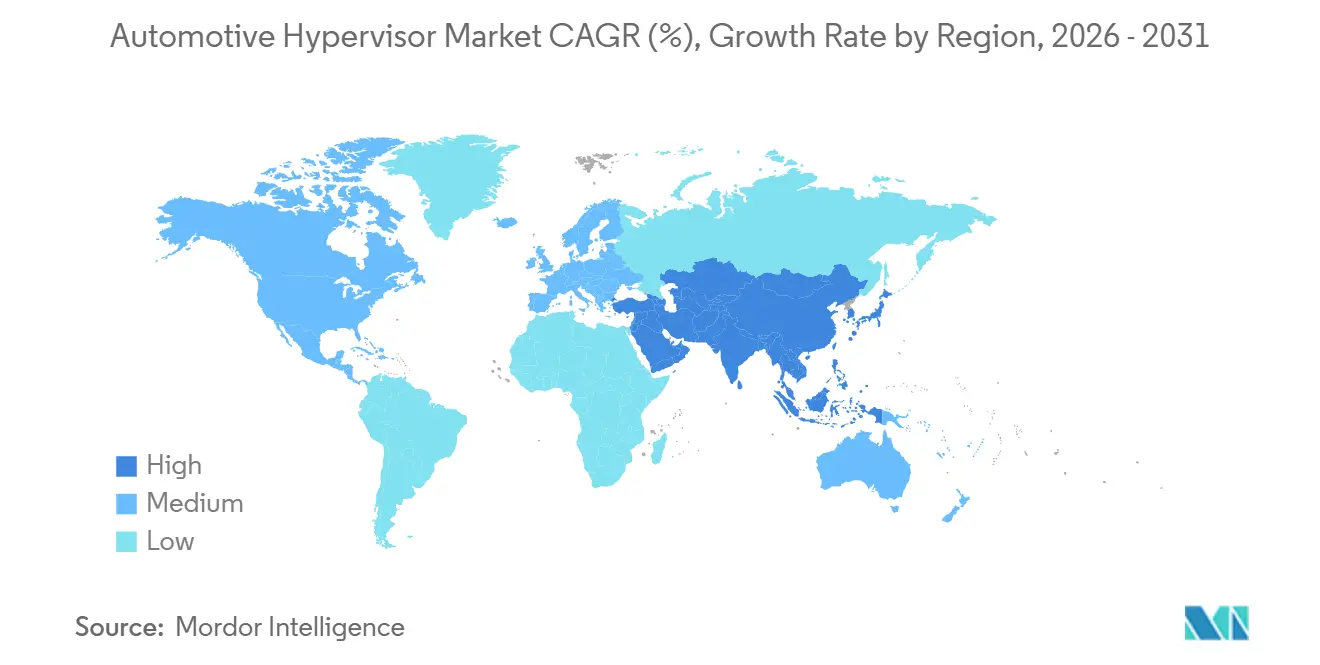

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Hypervisor Market Analysis by Mordor Intelligence

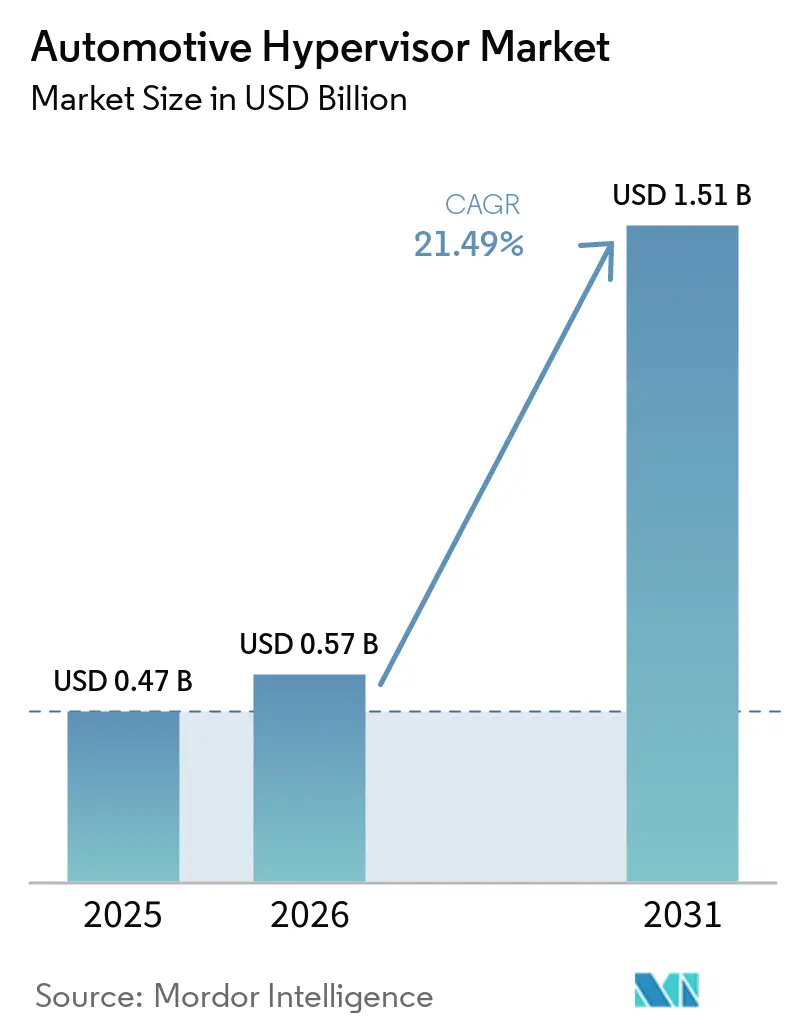

The Automotive Hypervisor Market size is expected to increase from USD 0.47 billion in 2025 to USD 0.57 billion in 2026 and reach USD 1.51 billion by 2031, growing at a CAGR of 21.49% over 2026-2031. Rapid growth is tied to the automotive sector’s pivot toward software-defined vehicles that consolidate multiple ECUs onto domain controllers while keeping safety-critical and non-critical workloads strictly isolated. Mandatory cybersecurity regulations, rising mixed-criticality workloads, and OEM efforts to reduce wiring complexity continue accelerating demand. Competitive dynamics have intensified after Qualcomm acquired OpenSynergy’s virtualization assets, underscoring the importance of semiconductor–software integration in next-generation vehicle platforms. Meanwhile, the scarcity of certified virtualization engineers and entrenched ECU investments at Tier-1 suppliers pose near-term constraints even as regulatory pressure forces wider adoption.

Key Report Takeaways

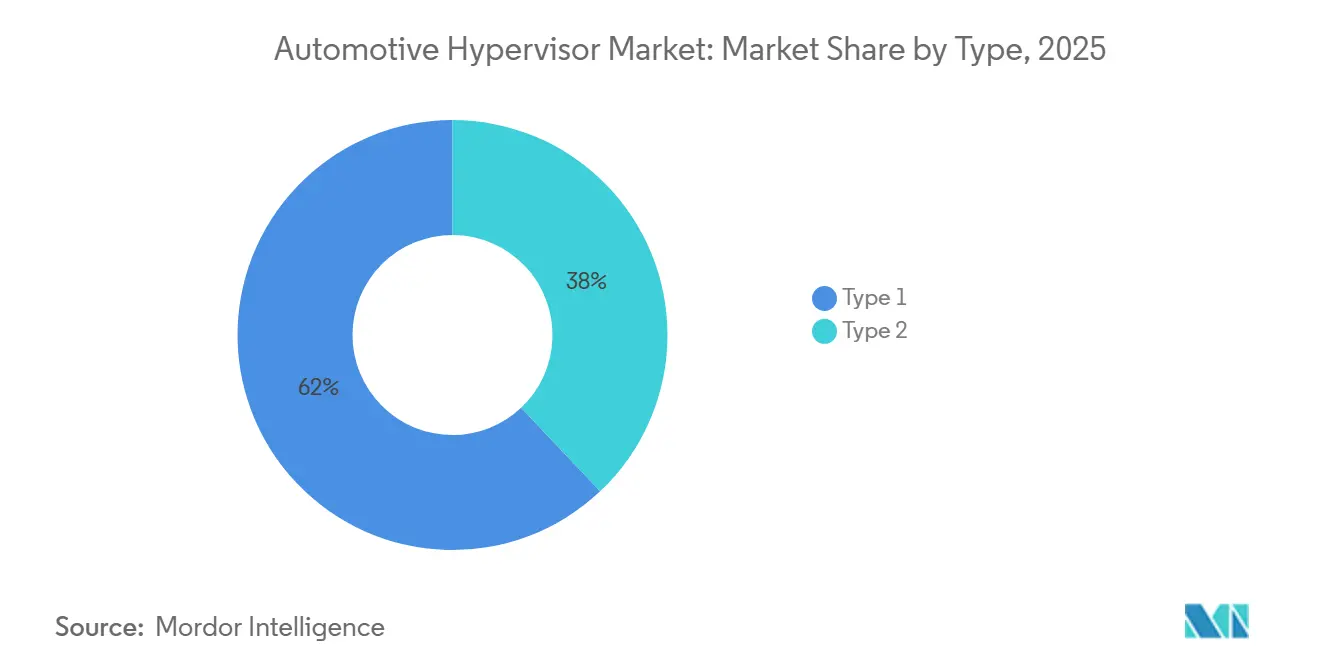

- Type 1 bare-metal hypervisors commanded 62.04% of the automotive hypervisor market share in 2025. Type 2 hosted hypervisors are forecast to post the fastest CAGR of 16.82% to 2031.

- Passenger cars accounted for 58.28% of the automotive hypervisor market in 2025, while light commercial vehicles (LCVs) are advancing at a 19.41% CAGR through 2031.

- Semi-Autonomous held 64.07% of the automotive hypervisor market in 2025, while Autonomous Vehicles are projected to grow at a 19.39% CAGR through 2031.

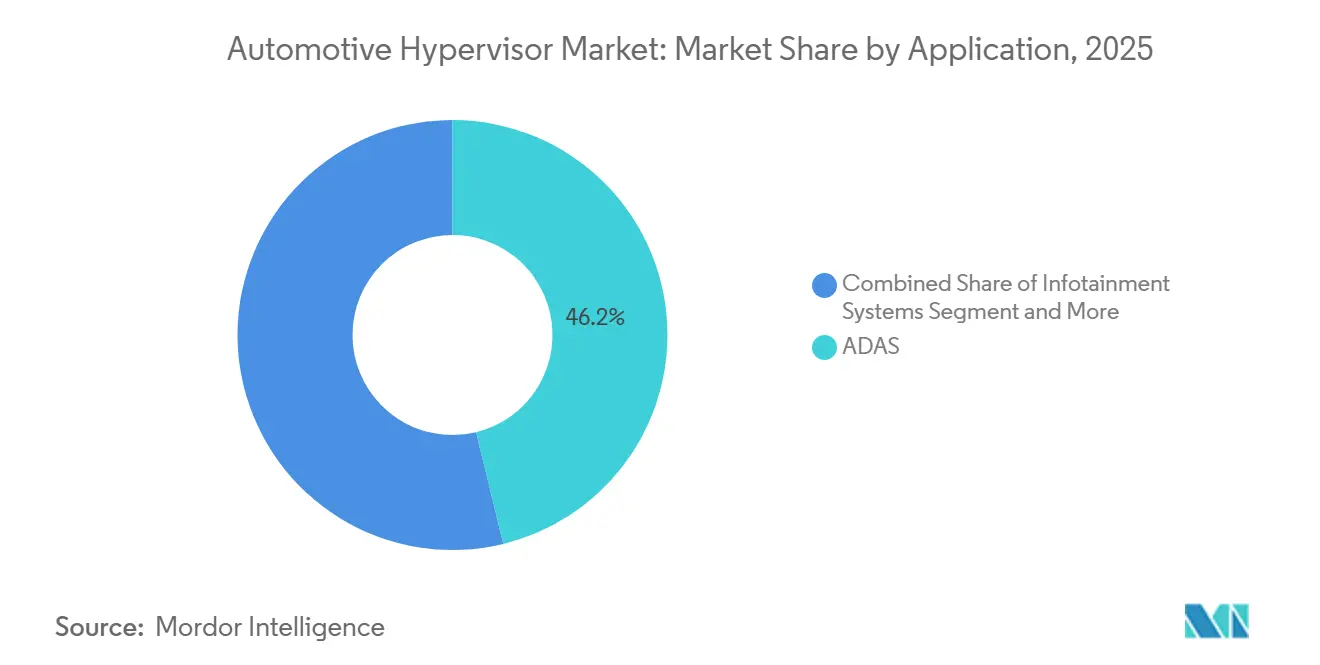

- ADAS accounted for 46.17% of the automotive hypervisor market in 2025, while Connectivity and Telematics are expanding at a 17.88% CAGR through 2031.

- OEM channels accounted for 77.53% of demand in 2025 and remain the fastest-growing distribution path, with a 13.63% CAGR.

- Asia-Pacific captured a 37.81% share of the automotive hypervisor market in 2025; the region is projected to expand at a 14.79% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Hypervisor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domain-Controller Architectures | +4.2% | Global; strongest in Europe and Asia-Pacific | Medium term (2–4 years) |

| Cybersecurity Compliance Mandates | +3.8% | Europe, Japan, South Korea; expanding globally | Short term (≤ 2 years) |

| SoC Function Consolidation | +3.5% | Global; premium OEMs lead | Medium term (2–4 years) |

| Vehicle-as-a-Service Models | +3.1% | North America, Europe | Long term (≥ 4 years) |

| Zonal Architecture Adoption | +3.0% | Global; Asia-Pacific manufacturing hubs | Medium term (2–4 years) |

| Software-Defined Vehicles | +2.1% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Domain-Controller E/E Architectures

The automotive industry's transition from distributed ECU architectures to centralized domain controllers fundamentally reshapes vehicle electrical/electronic (E/E) systems, with hypervisors as the critical enabler for consolidating 100+ individual ECUs onto fewer than 10 high-performance computing units. This architectural shift reduces vehicle weight by approximately 15-20 kilograms while cutting wiring harness complexity by up to 40%, directly impacting electric vehicle range and manufacturing costs[1]Chris Atkinson, "Multi-source automotive software stacks," SBD Automotive, sbdautomotive.com.. The consolidation is also creating significant opportunities in the automotive hypervisor market, as each domain controller requires advanced virtualization software to manage mixed-criticality workloads across ASIL-D safety functions and non-safety applications. OEMs are increasingly adopting hypervisor-based architectures to future-proof vehicle platforms against evolving software demands, with Tesla, BMW, and Volkswagen leading the move toward software-defined vehicles.

Mandatory Cybersecurity Compliance (ISO/SAE 21434, UNECE R155/R156)

Regulatory mandates for automotive cybersecurity are driving compliance-led growth in the automotive hypervisor market. UNECE R155 requires Cybersecurity Management Systems (CSMS) certification as a precondition for vehicle type approval in EU member countries, Japan, and South Korea since July 2024[2]"UNECE Automotive Cybersecurity Compliance Requirements," UL Solutions, www.ul.com.. The regulation's emphasis on organizational-level cybersecurity processes and regular threat analysis and risk assessment (TARA) activities drives OEMs to adopt hypervisor-based architectures that provide hardware-backed isolation between safety-critical and connectivity domains. ISO/SAE 21434 compliance requirements are particularly stringent for mixed-criticality systems, where hypervisors must demonstrate freedom from interference between different ASIL-rated applications running on shared hardware resources.

Consolidation of Infotainment, ADAS and Powertrain on Single SoCs

Converging traditionally separate vehicle domains onto unified system-on-chip (SoC) platforms is accelerating growth in the automotive hypervisor market.OEMs seek to leverage economies of scale in semiconductor procurement while maintaining functional isolation between critical and non-critical applications. Advanced SoCs from suppliers like NXP's S32 CoreRide platform and Renesas R-Car S4 now integrate automotive-specific peripherals with high-performance CPU/GPU clusters, enabling hypervisors to manage heterogeneous workloads ranging from real-time powertrain control to AI-accelerated ADAS processing[3]"Green Hills Software Delivers Industry’s Most Comprehensive Production-Focused Software-Defined Vehicle (SDV) Solutions for NXP’s Open S32 CoreRide Platform," Green Hills Software, www.ghs.com..

OEM Push Toward Software-Defined Vehicles (SDVs)

The automotive industry's shift toward software-defined vehicles is transforming the automotive hypervisor market, expanding the role of hypervisors from basic virtualization platforms to comprehensive software lifecycle management systems. OEMs like Tesla, BMW, and Mercedes-Benz are developing in-house software capabilities that require flexible, updatable virtualization architectures. SDV architectures demand hypervisors capable of supporting over-the-air (OTA) updates for individual virtual machines without affecting other domains, creating new technical requirements for secure boot, measured attestation, and rollback protection mechanisms. The shift toward continuous software delivery models drives demand for hypervisors with container-orchestration capabilities, enabling OEMs to deploy microservice-based applications across distributed vehicle computing resources.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy ECU Lock-Ins | -2.8% | Global; entrenched supply chains | Short term (≤ 2 years) |

| ASIL-D Certification Costs | -1.9% | Global; most acute in cost-sensitive segments | Medium term (2–4 years) |

| Performance and Latency Issues | -1.2% | Global; safety-critical domains | Short term (≤ 2 years) |

| Virtualization Skill Shortage | -1.1% | Global; emerging markets most affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy ECU Investment Lock-ins at Tier-1s

The automotive industry’s heavy investment in legacy ECU architectures remains a major challenge for growth in the automotive hypervisor market, as Tier-1 suppliers face potential write-offs of billions of dollars in existing toolchains, manufacturing equipment, and engineering expertise optimized for distributed control systems. Many established suppliers have developed proprietary AUTOSAR Classic implementations and safety-certified software stacks requiring extensive re-engineering to operate within hypervisor environments, creating financial disincentives for rapid migration. The challenge is compounded by long automotive development cycles. ECU designs frozen in 2022-2023 will continue shipping in production vehicles through 2028-2030, limiting the addressable market for hypervisor solutions during the forecast period.

Hypervisor Certification Costs for ASIL-D Compliance

The substantial financial and temporal investments required to achieve ASIL-D functional safety certification remain a key restraint for the automotive hypervisor market, particularly among smaller OEMs and cost-sensitive vehicle programs. Achieving ISO 26262 ASIL-D certification for a hypervisor platform typically requires 18-36 months of development effort and costs ranging from USD 5-15 million, including safety analysis, verification activities, and independent assessment by certified auditors. The certification process becomes more complex for hypervisors supporting mixed-criticality workloads, where safety engineers must demonstrate freedom from interference between ASIL-D applications and non-safety functions sharing the same hardware resources. Additional cybersecurity certifications required under ISO/SAE 21434 and UNECE R155 compound the cost burden, as hypervisor vendors must maintain separate certification evidence for safety and security requirements that often conflict in their implementation approaches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Bare-Metal Dominance Drives Platform Consolidation

Type 1 bare-metal hypervisors hold 62.04% market share in 2025, reflecting their superior performance and direct hardware access capabilities, which are essential for safety-critical automotive applications. These hypervisors operate directly on vehicle hardware without an underlying operating system, providing deterministic real-time performance and minimal latency overhead crucial for ADAS and powertrain control systems. Type 2 hosted hypervisors, despite a smaller market share, are experiencing rapid growth at a 16.82% CAGR through 2031, driven by their flexibility in development environments and ease of integration with existing Linux-based infotainment platforms.

The performance advantages of bare-metal architectures become particularly pronounced in mixed-criticality scenarios, where ASIL-D safety functions must coexist with non-safety applications on shared hardware resources. Type 1 hypervisors, such as Green Hills' INTEGRITY Multivisor and Wind River's Helix Virtualization Platform, provide hardware-assisted virtualization features that enable strict temporal and spatial partitioning required for functional safety compliance. However, Type 2 solutions are gaining traction in specific use cases such as software development, testing, and non-safety infotainment applications where their simplified deployment model outweighs performance considerations. The market evolution suggests a bifurcated future, with Type 1 hypervisors dominating production vehicle deployments while Type 2 solutions capture development tool and aftermarket segments.

By Vehicle Type: Passenger Cars Lead While Autonomous Platforms Accelerate

Passenger cars account for 58.28% of automotive hypervisor deployments in 2025, driven by the segment's high-volume production and the increasing integration of advanced infotainment and ADAS features that benefit from domain consolidation. The passenger car segment's dominance reflects OEMs' focus on differentiating consumer vehicles through software-defined features and over-the-air updates, which require robust virtualization platforms. Light Commercial Vehicles (LCVs) and Medium/Heavy Commercial Vehicles (HCVs) collectively account for the remaining market share, with commercial segments showing growing interest in hypervisor-enabled fleet management and telematics applications.

The LCV (Light Commercial Vehicle) segment is the fastest-growing category in the automotive hypervisor market, owing to the rapid digitalization of fleet operations and the adoption of connected, software-driven architectures. Rising demand for real-time telematics, driver assistance, and over-the-air updates in logistics and last-mile delivery fleets is accelerating the integration of hypervisors across LCV platforms. Automakers are consolidating multiple control domains—infotainment, ADAS, and powertrain—into virtualized ECUs to reduce hardware costs and enhance system efficiency. Furthermore, compliance with cybersecurity regulations and the shift toward electrified LCVs require secure and scalable virtualization frameworks. As a result, the LCV segment offers the highest deployment potential for automotive hypervisors during the forecast period.

By Mode of Operation: Semi-Autonomous Dominance Shifting to Full Autonomy

Semi-autonomous vehicles currently dominate with 64.07% market share in 2025, reflecting the widespread deployment of Level 2 ADAS systems that require hypervisor-based isolation between safety-critical perception algorithms and non-safety infotainment functions. This segment's market leadership stems from regulatory mandates for automatic emergency braking and lane-keeping assistance in major markets, driving volume adoption of hypervisor-enabled domain controller architectures. The semi-autonomous segment benefits from established supply chains and proven safety certification processes that reduce deployment risks for OEMs.

Autonomous vehicles are experiencing rapid growth at a 19.39% CAGR through 2031, driven by the computational complexity of Level 3+ systems, which necessitate hypervisor-based resource management across multiple AI accelerators, sensor fusion processors, and safety monitoring systems. The autonomous segment's expansion is supported by regulatory clarity emerging in key markets, with Germany legalizing Level 4 operations and Japan targeting nationwide Level 4 deployment by 2027.

By Application: ADAS Leadership with Connectivity Surge

Advanced Driver Assistance Systems (ADAS) applications dominate with 46.17% market share in 2025, reflecting the critical role of hypervisors in managing the complex sensor fusion, perception, and decision-making algorithms required for modern safety systems. ADAS applications drive hypervisor adoption through their stringent functional safety requirements, where ISO 26262 ASIL-D compliance necessitates strict isolation between safety-critical functions and other vehicle systems. Regulatory mandates for automatic emergency braking and blind spot monitoring across major automotive markets reinforce the segment's leadership position.

Connectivity and Telematics will emerge as the fastest-growing applications, with a 17.88% CAGR through 2031, driven by the proliferation of 5G V2X communication systems and vehicle-as-a-service business models that require secure, updateable connectivity stacks.

By Demand Type: OEM Integration Dominates Market Strategy

Original Equipment Manufacturer (OEM) channels account for 77.53% of automotive hypervisor demand in 2025, reflecting the strategic importance of virtualization decisions in vehicle platform architecture and the complexity of integrating hypervisor technology into safety-critical automotive systems. The OEM segment's dominance stems from hypervisors' fundamental role in enabling software-defined vehicle architectures, where platform-level decisions about domain consolidation and virtualization strategy must be made during early vehicle development phases. OEM adoption is driven by competitive pressures to differentiate vehicles through software capabilities and reduce hardware costs through ECU consolidation.

The OEM segment maintains the fastest growth rate at 13.63% CAGR through 2031, indicating continued platform-level integration of hypervisor technology as standard automotive architecture rather than an optional add-on capability. Replacement market opportunities remain limited due to hypervisors' deep integration with vehicle hardware and safety systems, though aftermarket applications are emerging in commercial vehicle fleet management and retrofit connectivity solutions.

Geography Analysis

Asia-Pacific led with 37.81% share in 2025 and is advancing at a 14.79% CAGR as Chinese OEMs race to localize silicon and adopt software-defined architectures. Roughly one-third of vehicles built in China for the 2025 model year will feature domain controllers, each of which embeds at least one hypervisor instance. Domestic chipmakers are now shipping early RISC-V automotive SoCs, prompting the development of localized virtualization stacks tuned for Chinese security algorithms.

North America follows, buoyed by widespread autonomous testing across 38 states and emerging NHTSA data-sharing mandates that require secure logging—an inherent hypervisor use case. U.S. supply-chain de-risking policies curtailing the use of Chinese telematics components are pushing OEMs toward domestic and allied software vendors.

Europe remains the reference market for rigorous functional safety. UNECE R156 update processes call for three-year re-certification cycles, generating recurring revenue for hypervisor suppliers offering compliance monitoring. Germany’s 2024 Level 4 ordinance and France’s 2025 black-box rules create unique opportunities for solutions that guarantee crash-proof data isolation.

Competitive Landscape

The field remains moderately fragmented: the top five providers captured almost half of global revenue in 2025. Green Hills Software, BlackBerry QNX, and Wind River capitalize on decades of RTOS pedigree and existing ASIL-D certificates. Semiconductor firms, notably NXP and Renesas, embed lightweight hypervisors to lock in silicon attach rates, while Continental and Elektrobit vertically integrate to secure software license margins.

Qualcomm’s 2024 purchase of OpenSynergy shifts the center of gravity toward SoC-embedded virtualization that bundles RF, AI, and graphics IP. The deal pressured rivals to deepen partnerships; Wind River and Elektrobit responded with a co-developed middleware stack that shortened domain controller integration time by six months. Start-ups are carving niches in zonal compute orchestration and OTA security attestation, yet high certification barriers and talent shortages temper their scale prospects.

GENIVI’s Automotive Virtual Platform Specification aims to standardize I/O virtualization, potentially commoditizing basic hypervisor functions. Suppliers therefore differentiate via advanced features such as deterministic inter-VM communication, AI accelerator partitioning, and integrated DevSecOps pipelines that map directly into OEM continuous-delivery workflows.

Automotive Hypervisor Industry Leaders

-

BlackBerry QNX

-

Green Hills Software

-

Wind River

-

Continental AG

-

Elektrobit

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Qualcomm completed its acquisition of OpenSynergy's automotive virtualization assets, integrating the company's EB corbos Hypervisor technology and engineering team to strengthen Qualcomm's software-defined vehicle platform capabilities and accelerate hypervisor development for next-generation automotive SoCs.

- April 2024: Green Hills Software announced comprehensive production-focused SDV solutions for NXP's S32 CoreRide platform, delivering ASIL-D certified INTEGRITY RTOS with Multivisor virtualization capabilities and integrated development tools to enable mixed-criticality consolidation across heterogeneous multicore processors.

Global Automotive Hypervisor Market Report Scope

| Type 1 (Bare-Metal Hypervisor) |

| Type 2 (Hosted Hypervisor) |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (HCVs) |

| Autonomous Vehicles |

| Semi-Autonomous Vehicles |

| Advanced Driver Assistance Systems (ADAS) |

| Infotainment Systems |

| Connectivity and Telematics |

| Powertrain and Engine Control Systems |

| Others |

| OEM |

| Replacement |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Type 1 (Bare-Metal Hypervisor) | |

| Type 2 (Hosted Hypervisor) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Medium and Heavy Commercial Vehicles (HCVs) | ||

| By Mode of Operation | Autonomous Vehicles | |

| Semi-Autonomous Vehicles | ||

| By Application | Advanced Driver Assistance Systems (ADAS) | |

| Infotainment Systems | ||

| Connectivity and Telematics | ||

| Powertrain and Engine Control Systems | ||

| Others | ||

| By Demand Type | OEM | |

| Replacement | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the automotive hypervisor market?

The market is valued at USD 0.47 billion in 2025.

Which hypervisor type dominates vehicle production?

Type 1 bare-metal platforms lead with a 62.04% share in 2025 because they deliver deterministic performance for ASIL-D workloads.

Why are hypervisors critical for autonomous vehicles?

Level 3+ systems need strict workload isolation and fail-operational redundancy that only hypervisors can provide, driving a 19.41% CAGR in the autonomous segment.

Which region is expanding the fastest?

Asia-Pacific is growing at a 14.79% CAGR, propelled by China’s EV boom and semiconductor localization drives.

How do cybersecurity regulations influence adoption?

UNECE R155/R156 and ISO/SAE 21434 require demonstrable threat isolation, making hypervisor architecture a practical path to compliance across major markets.

Page last updated on: