Automotive Electronic Control Unit Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

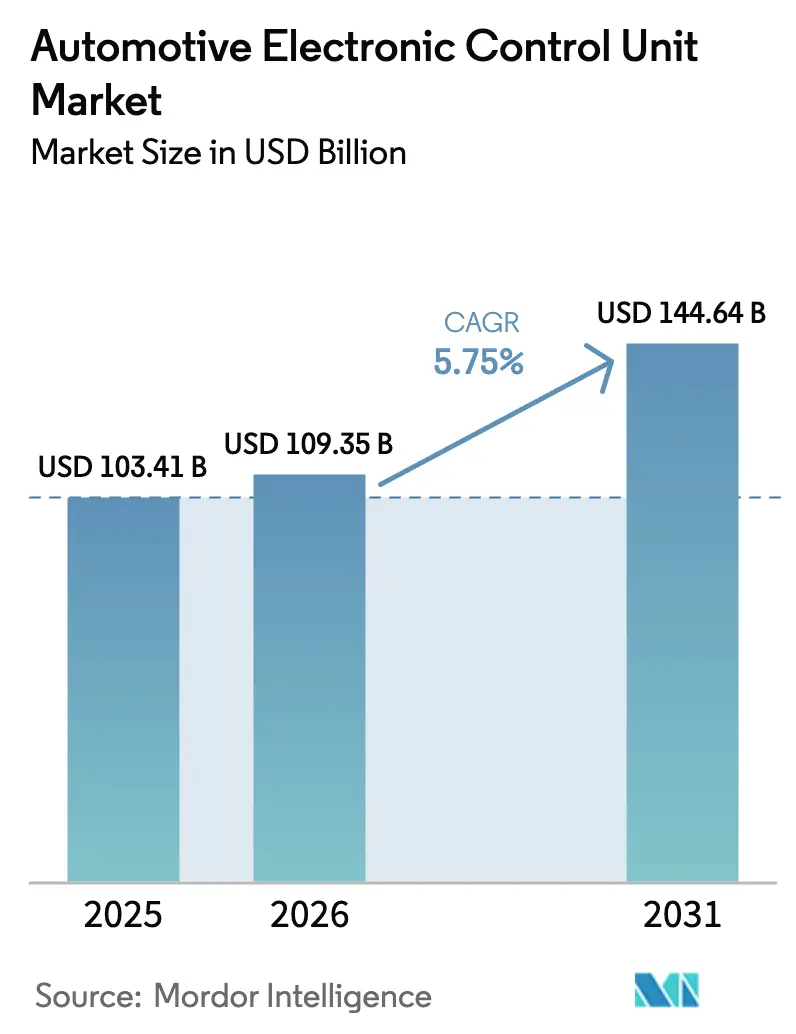

| Market Size (2026) | USD 109.35 Billion |

| Market Size (2031) | USD 144.64 Billion |

| Growth Rate (2026 - 2031) | 5.75% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Electronic Control Unit Market Analysis by Mordor Intelligence

The Automotive Electronic Control Unit Market size in 2026 is estimated at USD 109.35 billion, growing from 2025 value of USD 103.41 billion with 2031 projections showing USD 144.64 billion, growing at 5.75% CAGR over 2026-2031. The primary growth engines are regulatory deadlines for advanced driver-assistance systems, rapid electrification of passenger and commercial fleets, and the migration to centralized vehicle architectures. Battery electric vehicles require multiple new control domains—battery, inverter, on-board charger, and thermal management, multiplying the semiconductor bill of materials per vehicle.

Key Report Takeaways

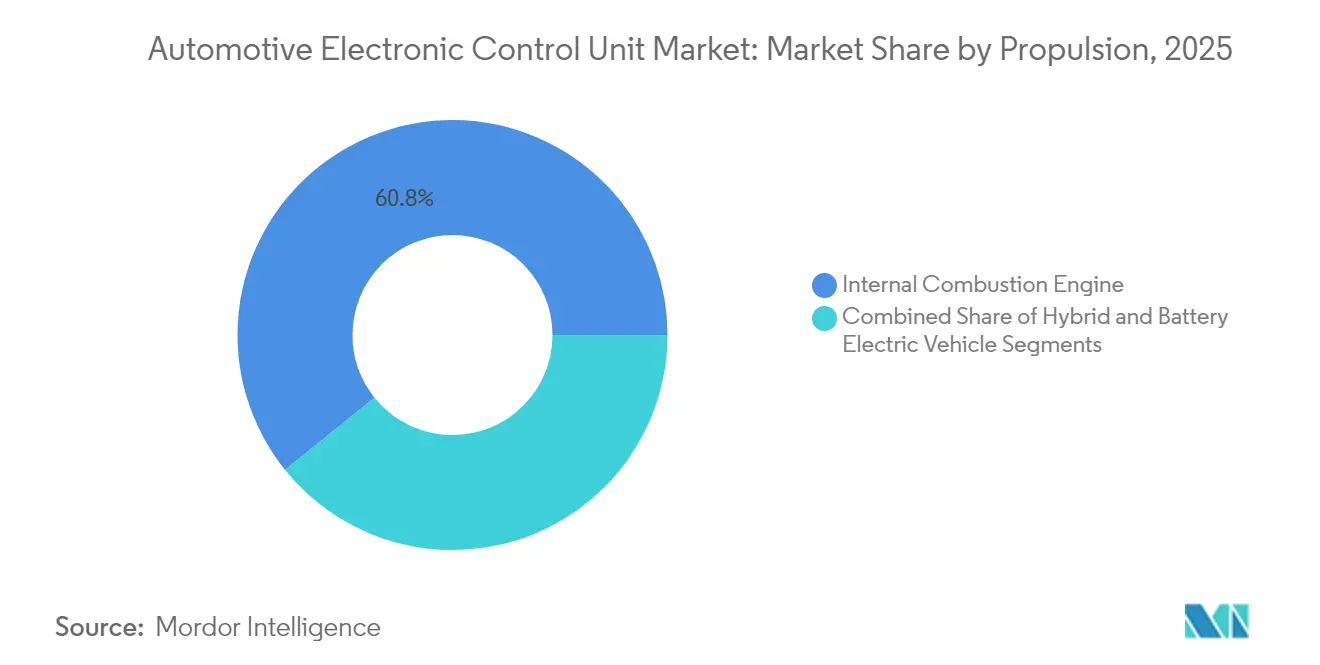

- By propulsion, internal-combustion vehicles held 60.78% of Automotive ECU Market share in 2025, while battery-electric vehicles are projected to grow at a 6.51% CAGR through 2031.

- By application, powertrain systems accounted for 40.92% of the automotive electronic control unit market size in 2025; ADAS & safety systems are advancing at a 4.27% CAGR to 2031.

- By ECU capacity, 32-bit devices led with 53.74% of the market share in 2025, whereas 64-bit devices are expanding at a 6.79% CAGR.

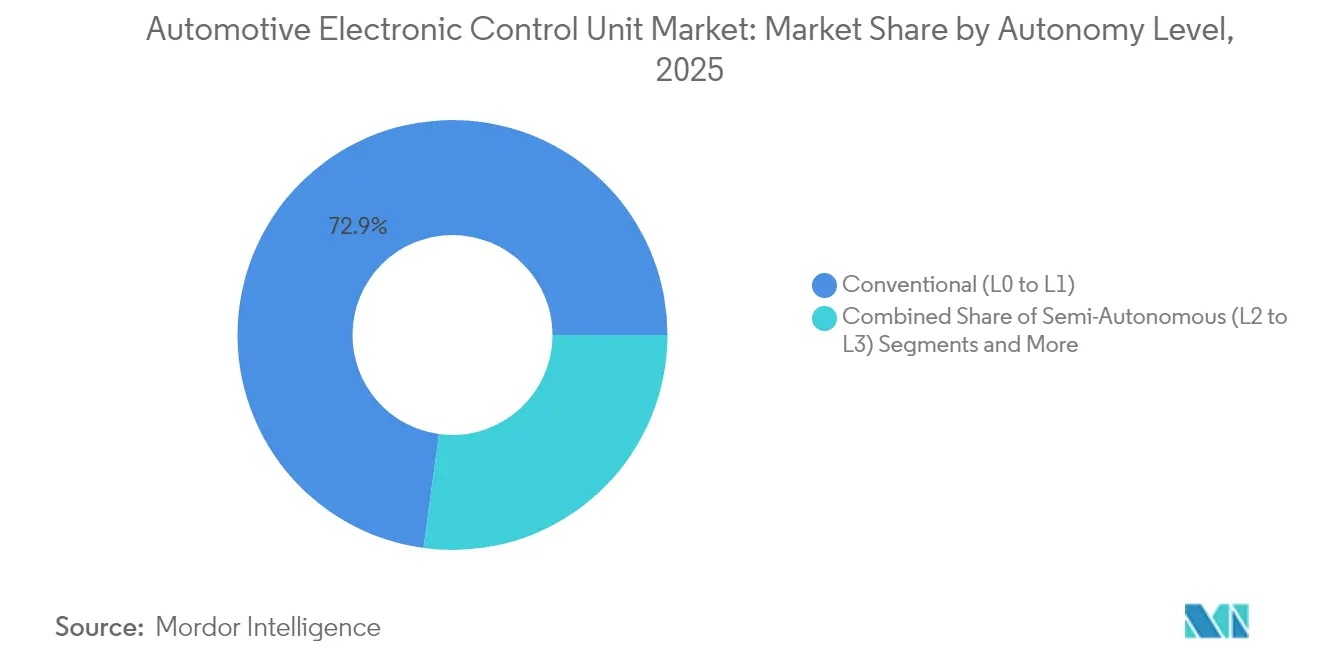

- By autonomy level, conventional L0-L1 vehicles represented 72.85% of the market size in 2025, while L4-L5 systems deliver the fastest 8.27% CAGR.

- By vehicle type, passenger cars led with 68.15% of automotive electronic control unit market share in 2025; whereas commercial vehicles is growing at a CAGR of 5.73%.

- By geography, Asia-Pacific accounted for 48.29% of automotive electronic control unit market share in 2025; whereas it is also expanding at a robust CAGR of 7.72% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Electronic Control Unit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification Wave Raises ECU | +1.8% | Global, led by China and Europe | Medium term (2-4 years) |

| ADAS Mandates in US, EU, China | +1.2% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Centralized/Zonal E/E Architectures | +0.9% | Global, early adoption in premium segments | Long term (≥ 4 years) |

| Rapid Semiconductor Cost Declines | +0.7% | Global, accelerated in developed markets | Medium term (2-4 years) |

| Cyber-Secure, Over-the-Air Update Capability | +0.5% | Global, regulatory focus in EU and US | Short term (≤ 2 years) |

| Heavy-Duty and Off-Highway Electrification | +0.4% | China, North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification Wave Raises ECU Count Per Vehicle

Battery electric powertrains introduce dedicated control units for battery management, inverter logic, charging negotiation, and regenerative braking. Each function adds processing overhead that traditional combustion platforms never required, lifting semiconductor spend per vehicle from USD 420 in 2019 to an expected USD 1,350 by 2030.[1]“Semiconductor Demand Forecast for EVs,” NITI Aayog, niti.gov.in Hybrid configurations magnify integration complexity because algorithms must coordinate two propulsion sources seamlessly. Cummins reports that its electronic powertrain control modules optimize diesel, hydrogen, natural-gas, and fully electric systems, a preview of how diversified fuel strategies will keep ECU counts elevated. Consequently, the Automotive ECU Market gains incremental volume every time an OEM launches a new battery-electric or fuel-cell program.

ADAS Mandates in US, EU, China Boost Demand

The European Union activated the revised General Safety Regulation in July 2024, obligating every new car to ship with intelligent speed assistance, autonomous emergency braking, and reversing detection. China’s Level-2 penetration reached 42.4% of new passenger-car sales in 1H 2024 under its intelligent connected-vehicle rules, and NHTSA is advancing similar ADAS provisions for North America. Each mandate needs a high-reliability controller capable of real-time sensor fusion and functional-safety diagnostics. The resulting volume uplift directly feeds the automotive ECU market.

Centralized/Zonal E/E Architectures Need High-Performance ECUs

OEMs are migrating from 100-plus distributed boxes to 20–30 zonal controllers that govern multiple subsystems, cutting weight and wiring cost. Only 2% of vehicles used zonal layouts in 2024, but adoption will climb to 38% by 2034. NXP’s S32 CoreRide platform integrates multi-gig Ethernet networking, hardware security, and domain processing on a single board to address this shift. As domain consolidation proceeds, each remaining ECU must handle far higher compute loads, increasing average selling prices and expanding revenue potential within the automotive ECU market.

Cyber-Secure, Over-the-Air Update Capability Becomes Sourcing Criterion

UN Regulations 155 and 156 enforce mandatory cybersecurity management and software-update governance for every new model launched in markets that adopt UNECE rules. HARMAN already manages over-the-air software for 35 million vehicles and reports file-size reduction of up to 97% via smart delta technology. OEMs view OTA as a multi-billion-dollar cost-avoidance lever because it eliminates many safety-recall workshops. Consequently, contract awards increasingly stipulate secure boot, data-at-rest encryption, and OTA stacks, pushing suppliers to embed these features in next-generation ECUs and sustaining growth in the automotive ECU market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global Chip-Supply Volatility | -1.1% | Global, acute in automotive-specific nodes | Short term (≤ 2 years) |

| OEM Reluctance to Cede Data-Control to Tier-1s | -0.8% | Global, pronounced in premium segments | Medium term (2-4 years) |

| Software–Hardware Integration Complexity | -0.6% | Global, amplified in advanced vehicle architectures | Medium term (2-4 years) |

| Emerging Right-to-Repair Laws | -0.4% | North America, Europe, selective enforcement | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global Chip-Supply Volatility

Automotive ECUs still rely on mature 90 nm and larger process technology, a node class where global wafer capacity is chronically tight. VDA estimates that semiconductor demand from automakers will triple by 2030 while their share of overall chip output rises only from 8% to 14%. Suppliers cannot easily pivot foundry lines to trailing-edge nodes, so shortages linger even as leading-edge supply improves. Siemens promotes model-based verification that allows software teams to validate ECU code before silicon arrives, somewhat insulating programs from physical chip scarcity. Still, shortfalls can delay entire vehicle launches, knocking percentages off the automotive electronic control unit market CAGR.

OEM Reluctance to Cede Data-Control to Tier-1s

Vehicle data underpins predictive maintenance, usage-based insurance, and in-car subscriptions. OEMs therefore protect access, complicating integration for suppliers that build standalone ECUs. In the United States, the bipartisan 2025 REPAIR Act seeks to guarantee independent repairers access to diagnostic information long controlled by manufacturers. European Regulation 715/2007 already imposes similar transparency, yet implementation often remains partial. Until governance clarifies who can read and write vehicle data, the pace at which unified platforms displace legacy architectures could slow, restricting upside for the automotive ECU market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion: Electrification Drives Architectural Complexity

Even though internal-combustion platforms retained 60.78% of the automotive ECU market share in 2025, battery electric vehicles added the fastest 6.51% CAGR between 2026 and 2031. Heavy-duty segments supercharge the trend: global electric-truck registrations jumped nearly 80% in 2024, with China launching more than 430 battery-electric heavy-duty models. Cummins emphasizes flexible control firmware that can adapt from diesel to hydrogen to full battery packs, illustrating how propulsion diversity increases code complexity and total ECU demand.

In contrast, combustion platforms continue to place large orders for engine-management units because emissions rules tighten every model year. Euro 7, published in 2024, mandates onboard monitoring of particulate filters and battery durability, adding new diagnostics channels to existing powertrain ECUs. OEMs therefore face a dual platform strategy through the decade: maintain robust combustion controls while adding incremental electronics for hybrid and pure EV programs. This tension supports steady incremental revenue for the automotive electronic control unit market even as powertrain architectures diverge.

By Application: Safety Systems Lead Innovation While Powertrains Dominate Volume

Powertrain controllers generated 40.92% of the market share in 2025 because every vehicle-combustion, hybrid, or full electric-still needs torque, thermal, and energy management. ADAS & safety controllers, however, expand at 4.27% CAGR, making them the innovation flagship of the automotive electronic control unit market. Europe's General Safety Regulation and China's intelligent-connected guidelines require features such as automatic emergency braking, driver-monitoring cameras, and intelligent speed assistance, each relying on dedicated high-bandwidth microcontrollers. As lidar and radar migrate down price tiers, sensor-fusion loads grow, intensifying demand for 64-bit multicore processors.

Body, comfort, and lighting subsystems illustrate how legacy domains evolve; zonal controllers now replace multiple discrete boxes for windows, HVAC, and seat motors. Infotainment and telematics remain the smallest slice, but OTA services and subscription models compel OEMs to upgrade head units to gigahertz-class system-on-chips. The combined push from safety regulation and digital-service revenue gives the automotive electronic control unit market continuous headroom even after powertrain saturation.

By ECU Capacity: 64-Bit Migration Accelerates Despite 32-Bit Dominance

While 32-bit architectures accounted for a commanding 53.74% of the automotive electronic control unit market share in 2025, 64-bit devices are accelerating at a 6.79% CAGR, reflecting the compute jump required for sensor fusion and AI inference. The automotive electronic control unit market share for 64-bit designs grows whenever OEMs roll out zonal or domain controllers because these designs aggregate multiple functional-safety-rated workloads under one kitchen-sink processor. NXP's 16 nm S32K5 microcontroller family incorporates embedded MRAM for 15× faster writes than NOR flash, enabling real-time over-the-air patching without downtime. Infineon's new RISC-V AURIX line shows the industry's appetite for open instruction sets that can customize compute pipelines for EV traction or automated-driving math.

Legacy 16-bit units persist in cost-sensitive actuators such as wiper motors and seat-belt pretensioners, but code growth for diagnostics and cybersecurity slowly forces these nodes upward. Even entry-level microcontrollers now embed CAN-FD, LIN, and Ethernet, features that overwhelm the headroom of 8- or 16-bit cores. Consequently, migration momentum remains firmly in favor of higher bit-depth devices, reinforcing the long-term expansion thesis for the automotive electronic control unit market.

By Autonomy Level: L4–L5 Systems Drive Premium Growth

Conventional L0-L1 platforms accounted for 72.85% of the automotive electronic control unit market share in 2025, but L4-L5 stacks are projected to soar at an 8.27% CAGR through 2031. Each step up the SAE ladder amplifies the computational workload exponentially, especially for perception and path-planning algorithms. China already demonstrates early-adopter scale: Level-2 systems captured 42.4% of passenger-car sales in 1H 2024, preparing buyers for higher autonomy tiers.

UNECE Regulation 171, effective September 2024, standardizes highway-assist safety requirements, forcing controller redundancy and robust fallback strategies. Suppliers, therefore, invest in scalable hardware platforms that can span from Level 2+ driver assistance to full Level 4 robotaxis within the same software stack. These high-margin controllers lift both average selling price and content per vehicle, bolstering revenue across the automotive electronic control unit market.

By Vehicle Type: Commercial Vehicles Drive Electrification Innovation

Passenger cars accounted for 68.15% of the automotive electronic control unit market share in 2025, yet medium-and heavy-duty trucks are the laboratory for advanced high-voltage systems. The Clean Freight Coalition estimates that full electrification of the US truck fleet demands USD 620 billion in charging hardware and USD 370 billion in grid reinforcement, implying a massive addressable electronics pool.

Voltage levels in heavy trucks could hit 48 V for auxiliary loads and 800 V for traction by 2030, each requiring dedicated monitoring and safety-isolation controllers. ZF's 5 million-unit brake-by-wire contract signals how mechatronic modules displace pneumatics, with dual-channel ECUs meeting ISO 26262 ASIL-D requirements. As commercial fleets expand at a CAGR of 5.73%chase total-cost-of-ownership savings and emissions compliance, their demand for ruggedized, high-power controllers feeds incremental value into the automotive electronic control unit market.

Geography Analysis

Asia-Pacific anchored 48.29% of the market share in 2025, thanks to China's intelligent-connected vehicle roadmap and deep domestic semiconductor supply chain advantages, expanding at a CAGR of 7.72%. Level-2 penetration above 40% underscores how quickly the region adopts new control domains, and Chinese OEMs launched more than 430 battery-electric truck models in 2024 alone. Japan and South Korea added momentum with unified autonomous-driving legislation, while India's Production Linked Incentive scheme positions the country as a future electronics manufacturing hub. Collectively, these programs guarantee a dense pipeline of ECU contracts, securing Asia-Pacific's lead within the automotive ECU market

Europe follows as the strictest rule-setter. Euro 7, published in May 2024, layers battery durability metrics on top of core emissions caps, demanding more complex powertrain controllers. The General Safety Regulation simultaneously mandates intelligent speed assistance, reversing cameras, and driver-monitoring systems in all light vehicles. To localize chip supply, the European Investment Bank extended a EUR 1 billion loan to NXP for R&D in automotive radar and 5 nm processors. Continental responded by adding 700 new engine-management references for the aftermarket, illustrating how European suppliers monetize regulatory churn. These factors position Europe for steady share gains,

North America leans on financial incentives to close technology gaps. Bosch secured up to USD 225 million from the US CHIPS Act to build silicon-carbide wafers for electric drivetrains, and the EPA's Phase 3 greenhouse gas plan obligates OEMs to slash heavy-truck emissions beginning in 2027. The REPAIR Act proposes open diagnostic data to foster independent servicing, influencing how ECU software is partitioned between OEMs and aftermarket players. NXP and VIS meanwhile will spend USD 7.8 billion on a 300 mm fab in Singapore-production starts 2027-to guarantee regional supply resilience for future automotive ECU market demand.

Competitive Landscape

The sector remains moderately concentrated. Infineon is one of the global key players in the automotive microcontroller segment in 2024, leveraging in-house security IP and power-management leadership. NXP, Renesas, Bosch, and Continental retain long-standing design-win pipelines, yet software specialists are entering via domain-controller contracts as zonal architectures shift value toward high-level compute. Hardware suppliers hedge by forming ecosystem alliances: Bosch Engineering works with EDAG on whole-vehicle systems engineering, and DENSO partners with ROHM on wide-bandgap semiconductors.

Technology differentiation now centers on secure-update workflows and AI accelerators. NXP’s CoreRide bundles a Gbit Ethernet switch, functional safety island, and power gate array on one die, while Infineon’s RISC-V launch promises tool-chain openness previously unavailable in safety MCUs. Compliance competence is a second differentiator. Suppliers must demonstrate UNECE cybersecurity type approval to remain on OEM tender lists, turning certification audits into gatekeepers for market access.

White-space opportunities arise in heavy-duty electrification, where traditional passenger-car volumes do not dictate architectures. ZF’s brake-by-wire win and Cummins’s fuel-agnostic control platform both show tier-1s moving beyond commodity engine-ECUs into high-value mechatronics. Start-ups building zonal reference designs are also securing series nominations, raising competitive intensity and pushing incumbents to accelerate software-defined migration plans within the automotive electronic control unit market.

Automotive Electronic Control Unit Industry Leaders

Robert Bosch GmbH

Continental AG

ZF Friedrichshafen AG

DENSO Corporation

Aptiv PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Infineon introduced the first automotive RISC-V microcontroller family under the AURIX brand, targeting zonal and autonomous platforms.

- March 2025: NXP launched the 16 nm S32K5 MCU line featuring embedded MRAM for fast OTA updates.

- March 2025: Hyundai Mobis expanded semiconductor production for EV components, creating a 300-person chip team and a Silicon Valley lab.

- December 2024: Bosch received up to USD 225 million from the US Commerce Department to produce silicon-carbide power semiconductors in California.

Global Automotive Electronic Control Unit Market Report Scope

An automotive electronic control unit is a family of computer systems that control and maintain the entirety of a vehicle's electronic, electrical, and mechanical systems. Automotive functions ranging from the movement of the windows to the amount of air-fuel mixture required for each engine cylinder have an ECU system embedded with them, which is recorded, analyzed, and stored in the microcontroller.

The scope of the report covers segmentation based on propulsion, application, ECU, autonomous, vehicle, and geography. By propulsion type, the market is segmented into internal combustion engine, hybrid, and battery electric vehicles.

By application type, the market is segmented into ADAS and safety systems, body control and comfort system, infotainment and communication system, and powertrain system. By ECU type, the market is segmented into 16-bit ECU, 32-bit ECU, and 64-bit ECU.

By autonomous type, the market is segmented into conventional vehicle, semi-autonomous vehicle, and autonomous vehicles. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. For each segment, market sizing and forecast have been done on basis of value (USD billion).

| Internal Combustion Engine |

| Hybrid |

| Battery Electric Vehicle |

| ADAS & Safety Systems |

| Body Control & Comfort Systems |

| Infotainment & Communication Systems |

| Powertrain Systems |

| 16-bit ECU |

| 32-bit ECU |

| 64-bit ECU |

| Conventional (L0–L1) |

| Semi-Autonomous (L2–L3) |

| Autonomous (L4–L5) |

| Passenger Car |

| Commercial Vehicle |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Propulsion | Internal Combustion Engine | |

| Hybrid | ||

| Battery Electric Vehicle | ||

| By Application | ADAS & Safety Systems | |

| Body Control & Comfort Systems | ||

| Infotainment & Communication Systems | ||

| Powertrain Systems | ||

| By ECU Capacity | 16-bit ECU | |

| 32-bit ECU | ||

| 64-bit ECU | ||

| By Autonomy Level | Conventional (L0–L1) | |

| Semi-Autonomous (L2–L3) | ||

| Autonomous (L4–L5) | ||

| By Vehicle Type | Passenger Car | |

| Commercial Vehicle | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the automotive electronic control unit market by 2031?

The market is expected to reach about USD 144.64 billion in 2031, expanding at a 5.75% CAGR from its 2026 baseline.

Which vehicle propulsion type is growing fastest for ECU demand?

Battery electric vehicles are driving the highest incremental ECU content, with a 6.51% CAGR through 2031.

Why are 64-bit ECUs gaining popularity over 32-bit designs?

Zonal architectures, sensor fusion, and AI functions require more processing power and memory bandwidth, which 64-bit microcontrollers deliver.

How do regulatory mandates influence ECU adoption?

Rules such as the EU General Safety Regulation and UNECE cybersecurity notifications force OEMs to integrate additional safety and security controllers into every new model.

What regions currently dominate the automotive electronic control unit market?

Asia-Pacific leads with 48.29% share, propelled by China's intelligent-connected vehicle policies and extensive domestic semiconductor capacity.

How will chip-supply constraints affect future ECU growth?

While shortages could trim near-term production, structural semiconductor demand from electrification and autonomy keeps the market on a long-term growth trajectory.

Page last updated on: