Automotive Predictive Technology Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 56.94 Billion |

| Market Size (2031) | USD 88.06 Billion |

| Growth Rate (2026 - 2031) | 9.11% CAGR |

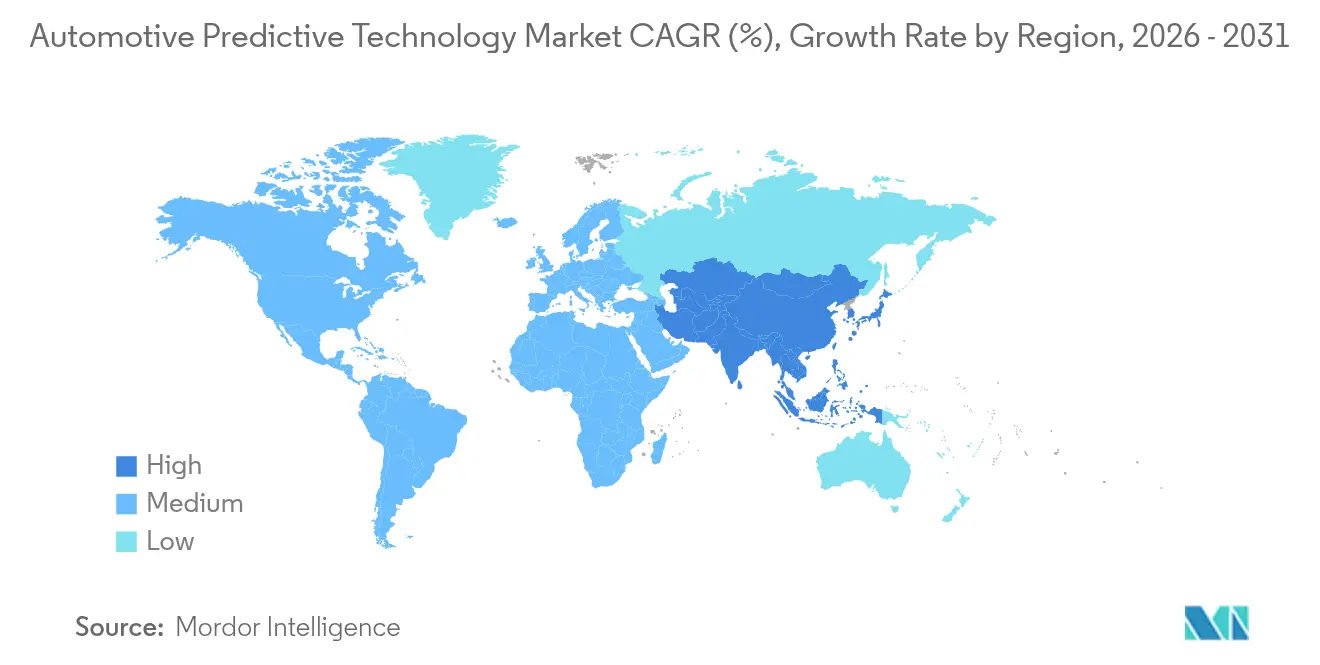

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Predictive Technology Market Analysis by Mordor Intelligence

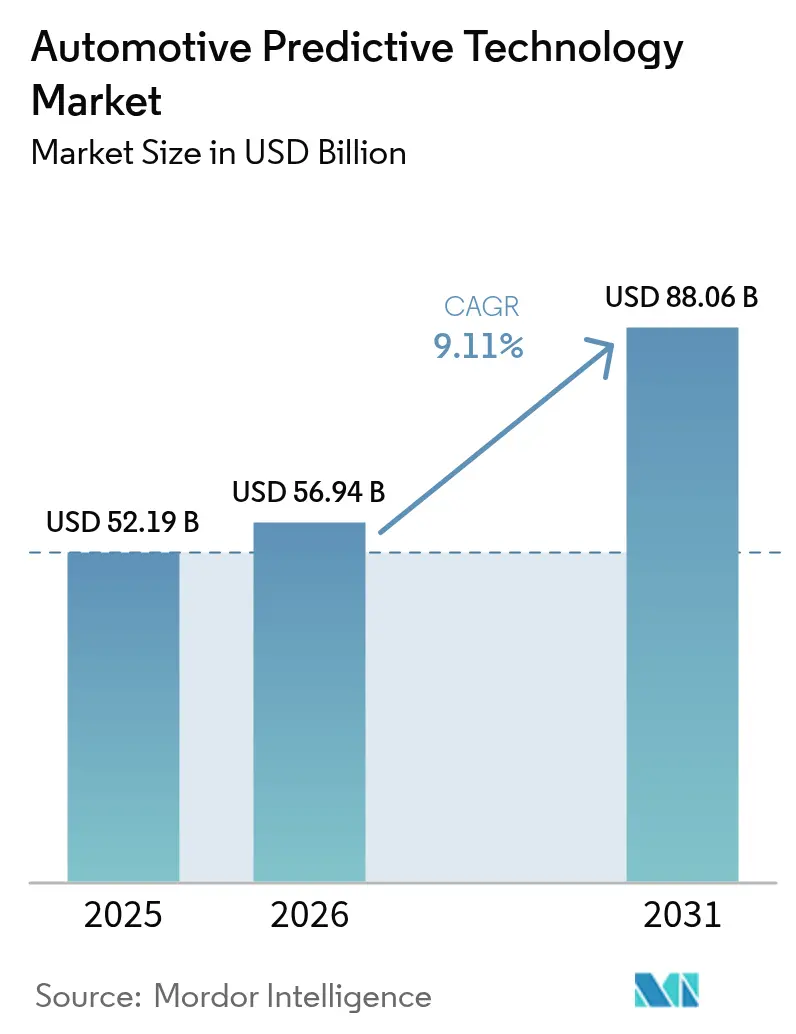

The Automotive Predictive Technology Market size is projected to expand from USD 52.19 billion in 2025 and USD 56.94 billion in 2026 to USD 88.06 billion by 2031, registering a CAGR of 9.11% between 2026 to 2031. Commercial fleets and insurers are prioritizing real-time data monetization, so capital is shifting from reactive diagnostics to anticipatory analytics that support usage-based insurance, over-the-air feature sales, and fleet-optimization contracts. Predictive maintenance already dominates adoption, yet faster-growing proactive-alert systems underline the premium placed on millisecond-early warnings that reduce claim severity. Technology choices mirror this pivot: machine-learning algorithms still account for most deployments, but transformer-based artificial-intelligence architectures running on centralized compute platforms are scaling quickly as OEMs replace rule-based logic with generative AI perception. Regionally, North America leads in revenue because NHTSA now requires event-data recorders that support crash-avoidance analytics, while Asia-Pacific is closing the gap through Chinese cloud investments that make large-scale telematics processing cost-efficient.

Key Report Takeaways

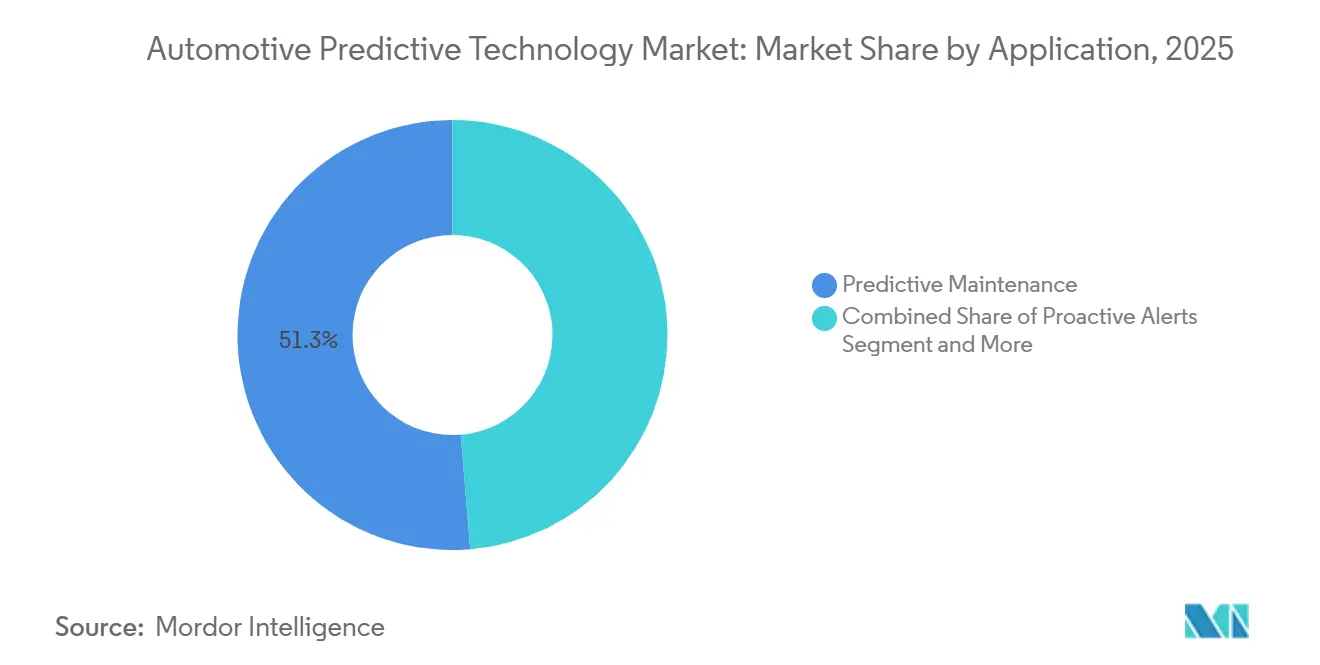

- By application, predictive maintenance accounted for 51.31% of the predictive technology automotive market share in 2025, while proactive alerts are forecast to expand at an 11.48% CAGR through 2031.

- By vehicle type, passenger cars captured 63.24% of the predictive technology automotive market in 2025, whereas medium- and heavy-duty commercial vehicles are projected to grow at a 10.14% CAGR between 2026-2031.

- By deployment, on-premises systems accounted for 54.88% of 2025 revenue, and cloud-based architectures are advancing at a 11.76% CAGR through 2031.

- By hardware, ADAS components led with a 36.28% share in 2025; sensors are the fastest-growing category, with a 10.81% CAGR through 2031.

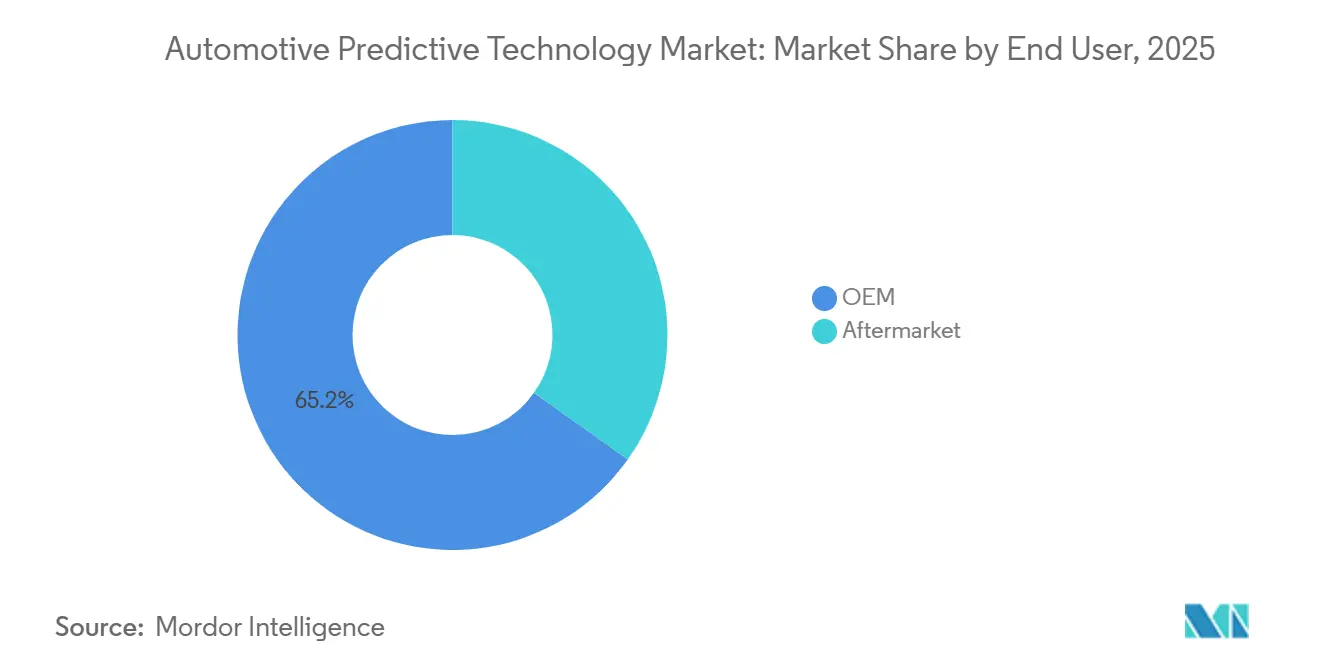

- By end user, OEM-integrated solutions accounted for 65.18% of 2025 revenue, while the aftermarket segment is expected to expand at 11.05% CAGR over 2026-2031.

- By 2025, machine learning held a 63.26% share; artificial-intelligence architectures are poised for a 12.36% CAGR, reflecting a migration toward transformer models.

- By geography, North America held 44.61% of the revenue share in 2025, and Asia-Pacific is forecast to record the fastest CAGR of 10.49% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Predictive Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of Connected Telematics | +2.1% | North America, Europe | Short term (≤ 2 years) |

| OEM AI/ML for Predictive Maintenance | +1.8% | Global manufacturing hubs | Medium term (2-4 years) |

| Regulatory Emphasis on Vehicle Safety | +1.5% | North America, EU primary | Long term (≥ 4 years) |

| Expansion of EV Fleets | +1.3% | Asia-Pacific core | Medium term (2-4 years) |

| Edge-AI Chips for On-Vehicle Processing | +1.0% | Global semiconductor hubs | Long term (≥ 4 years) |

| Usage-Based Insurance Demand | +0.8% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Connected Telematics and 5G

The FCC approved the allocation of the 5.9 GHz band for C-V2X, eliminating spectrum uncertainties and enabling rapid vehicle-to-infrastructure alerts[1]“5.9 GHz C-V2X Report & Order,”, Federal Communications Commission, FCC.GOV. Revised ETSI standards now require interoperability between 5G and DSRC, allowing OEMs to deploy hybrid telematics control units that operate seamlessly across regions. Pilot tests conducted by the 5G Automotive Association demonstrated real-time sensor fusion for numerous vehicles per cell, significantly reducing round-trip latency. This advancement enables fleets to integrate legacy DSRC data with new 5G streams into unified predictive dashboards. Furthermore, the EU’s updated eCall system mandates vehicles to transmit crash-severity predictions, embedding AI inference into telematics modules. Insurers can utilize this data to enhance the accuracy of usage-based policy pricing.

OEM Integration of AI/ML for Predictive Maintenance

By routing controller telemetry to cloud-based machine learning models, BMW has successfully monitored a significant portion of its assembly conveyors in Regensburg, resulting in notable reductions in downtime. This innovative architecture has also been implemented in BMW's plants located in Dingolfing, Leipzig, and Berlin. Furthermore, BMW holds patents specifically for its anomaly-detection algorithms. Meanwhile, ZF's Vehicle Health Monitoring system is advancing real-time analytics. It now extends its reach to critical components such as steer-by-wire and brake-by-wire, proactively alerting parcel-delivery fleets to potential failures before stress peaks. The industry is witnessing a shift: while OEMs are asserting data ownership, Tier-1 experts are leveraging it to create a premium tier of proprietary stacks. In contrast, volume manufacturers are opting to license these modular services, a strategy aimed at offsetting their R&D investments.

Regulatory Emphasis on Vehicle Safety and Emissions

Data recorders capturing pre-crash sensor streams are now mandated by NHTSA, compelling OEMs to develop telematics capable of executing machine-learning inferences[2]"NHTSA's Event Data Recorder (EDR) regulation", U.S. Department of Transportation, transportation.gov. Europe’s General Safety Regulation sets a universal standard for predictive features, mandating advanced emergency braking and driver-drowsiness detection. UNECE WP.29 emphasizes the importance of cybersecurity and software update auditing over a vehicle’s lifespan, incentivizing suppliers who offer integrated security and over-the-air tools. On the emissions front, the EPA's stringent limits are driving heavy-duty OEMs to implement real-time predictive dosing algorithms for optimized catalytic reduction.

Expansion of EV Fleets Requiring Battery Prognostics

Tesla's battery-management system can forecast cell degradation 6-12 months before drivers notice a range loss, significantly reducing warranty claims. GM's Ultium platform offers analytics similar to those in commercial fleets, enabling them to swap battery packs during scheduled downtime. Ford Pro Intelligence not only predicts daily range but also schedules low-cost charging, resulting in an energy spend reduction of up to 18% for fleets. Rivian and Volvo have integrated thermal-management forecasting, enhancing range performance on cold or high-load routes. Insurers like AXA are testing premiums based on anticipated battery longevity, opening new avenues for monetization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy and Cybersecurity Concerns | -1.2% | EU most restrictive | Short term (≤ 2 years) |

| Implementation and Integration Costs | -1.0% | Emerging markets cost-sensitive | Medium term (2-4 years) |

| Shortage of Skilled Data-Science Talent | -0.8% | Global, acute in auto hubs | Long term (≥ 4 years) |

| Reliability of Predictive Models | -0.6% | Extreme climate regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cybersecurity Concerns

OEMs must now demonstrate continuous threat monitoring, as mandated by UNECE WP.29 R155. Deloitte estimates that initial certification costs are significant per brand. Meanwhile, ISO/SAE 21434 introduces component-level risk analysis, putting pressure on Tier-2 suppliers that often lack dedicated security teams. Under GDPR, EU drivers can seek clarifications for automated decisions, posing challenges for opaque predictive models. California's CCPA empowers motorists with opt-out rights, leading to fragmented telematics data pools. China's PIPL mandates foreign OEMs to store data locally in the cloud. AWS and Microsoft cater to this need, offering services in-country but with restricted AI capabilities. Additionally, Aptiv's PSIRT enables OEMs to navigate audits more efficiently than startups that lack formal programs.

High Implementation and Integration Costs

Continental prices its comprehensive predictive maintenance packages at a premium for new vehicles, making it a costly choice in price-sensitive segments. These packages include advanced technologies such as real-time monitoring, data analytics, and automated diagnostics, which contribute to the high costs. Retrofitting older fleets requires specialized sensor wiring and control-unit reprogramming, skills that smaller workshops struggle to offer profitably. Additionally, the lack of standardized retrofitting solutions further complicates the process, increasing costs and limiting adoption. OEMs in emerging markets, facing capital constraints, are delaying rollouts, waiting for a further drop in sensor costs to make these solutions more accessible and viable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Maintenance Intelligence Drives Market Leadership

Predictive maintenance accounted for 51.31% of 2025 revenue, anchoring the predictive technology automotive market as fleets realized 30-40% lower unplanned downtime than scheduled servicing. Proactive-alert subsystems are expanding at a 11.48% CAGR because insurers reward millisecond-early warnings that reduce claim severity. As regulatory bodies increasingly endorse safety measures, predictive collision avoidance systems are gaining traction. Meanwhile, traffic-management analytics are proving their worth, helping cities reduce commute times. While still a niche, driver-behavior scoring is becoming a prized tool for insurers seeking detailed risk profiles.

BMW's Regensburg plant showcases the crossover potential of these technologies. By implementing vehicle-grade algorithms on conveyors, the plant avoided significant downtime, underscoring that predictive logic isn't just for the road. In the realm of electric vehicles, fleets are leveraging battery-life forecasts, leading to notable reductions in demand-charge costs for Ford Pro customers. Urban Vehicle-to-Infrastructure (V2I) pilots reveal that when connected cars communicate their intended routes in real-time, intersection delays can be significantly reduced. These diverse applications are expanding the automotive market for predictive technology, shifting the focus from one-time diagnostics to recurring subscription fees.

By Vehicle Type: Commercial Fleets Accelerate Adoption

Passenger cars generated 63.24% of 2025 revenue, buoyed by production scale and premium ADAS options embedded at launch. Medium and heavy commercial vehicles, though smaller, will post a 10.14% CAGR because logistics operators see direct ROI from uptime gains. Light commercial vans sit between, pushed by last-mile delivery electrification that demands predictive routing and battery management.

Rivian leverages anonymized fleet telemetry to identify battery anomalies linked to deep-discharge cycles. Volvo's thermal forecasting enhances range in Nordic climates. In passenger cars, Tesla's early-warning battery analytics detect faults well in advance, reducing warranty losses. While insurance incentives and NHTSA data-recorder mandates drive ADAS adoption across all vehicles, the centralized purchasing and high utilization of commercial fleets position them as the immediate powerhouse of the predictive technology automotive market.

By Deployment: Cloud Migration Accelerates

On-premise inference still held 54.88% market share in 2025 because safety-critical models must run without cellular latency. However, cloud-based deployment will grow at a 11.76% CAGR as serverless computing aligns costs with bursty telematics loads, expanding the predictive technology automotive market in emerging regions that lack legacy data centers.

Microsoft's Azure Mobility stack is a prime example of how cloud vendors customize their offerings for the automotive industry. Hybrid models are now taking hold, running first-line predictions in-car while shipping non-urgent data to cloud clusters that refine algorithms and push updates over-the-air.

By Hardware: Sensor Innovation Drives Growth

ADAS domain controllers delivered 36.28% of 2025 hardware income, cementing their role as the brain of the predictive technology automotive industry. Sensor sales will outpace, growing at a 10.81% CAGR, as radar, lidar, and camera counts rise under multi-modal perception. Telematics control units aggregate data and manage edge-to-cloud links, while GPS modules enable location-specific predictions.

Telematics control units merge these feeds and host edge inference engines, while automotive-grade cameras provide visual inspection to detect leaks or uneven tire wear before humans can notice. This sensor proliferation underpins every layer of the automotive predictive technology market.

By End User: Aftermarket Disruption Challenges OEM Control

OEM-embedded solutions owned 65.18% of 2025 spending, reflecting control over CAN bus data and seamless integration during vehicle design. The aftermarket will grow at a 11.05% CAGR as fleets retrofit older vehicles and consumers install AI dashcams.

Aptiv’s Intelli-Maintenance kit installs in a few minutes and feeds real-time fault codes to small fleet dashboards. This retrofit wave addresses the majority of vehicles already on the road that lack built-in prognostics, and it pressures OEMs to offer extended service contracts that preserve brand engagement throughout a vehicle’s life.

By Technology: AI Acceleration Challenges ML Dominance

Machine-learning techniques like XGBoost and LSTM made up 63.26% of 2025 deployments, anchoring the predictive technology automotive market. Transformer and generative-AI architectures will post a 12.36% CAGR as centralized compute handles multimodal sensor fusion. Big-data analytics underpins offline training and fleet benchmarking, while IoT integration handles ingestion from millions of endpoints.

Big data analytics serves as the foundation, ingesting terabytes from over 100 sensors per vehicle, while IoT frameworks ferry data between the car, the cloud, and the infrastructure. Expect hybrid AI-ML suites that preserve deterministic safety behaviors yet adapt on the fly to new conditions, creating self-evolving vehicle ecosystems.

Geography Analysis

North America captured a 44.61% share in 2025, driven by 5G coverage, a significant share of major highway miles, and federal safety policies that reward telematics adoption. Heavy truck operators often face Federal Motor Carrier Safety Administration mandates requiring electronic inspection reporting, further nudging fleets toward predictive dashboards. Technology alliances proliferate; General Motors links its OnStar telematics with Microsoft Azure to push analytics-as-a-service packages to corporate customers.

Asia-Pacific is expanding at a 10.49% CAGR, catalyzed by China’s New Energy Vehicle target of 40% EV sales by 2030. Battery prognosis, therefore, ranks high on local priority lists. Japanese suppliers such as Denso bundle edge-AI chips inside next-generation electronic control units, and South Korea leverages semiconductor muscle from Samsung to cement regional leadership in hardware. Government-funded smart-transport pilots in India and Singapore accelerate the integration of urban analytics with predictive vehicle subsystems, reflecting a broader ecosystem push beyond individual vehicles toward city-level mobility orchestration.

Europe posts steady gains despite thorny privacy rules. German manufacturers pilot cross-vendor data-sharing trusts that satisfy GDPR while still training global models, and the EU’s cross-border emissions-trading schemes encourage fleetwide predictive monitoring. Siemens Mobility’s Digital Twin program, in collaboration with BMW, shows how industrial IoT stacks cross-fertilize automotive analytics, indicating that European growth will hinge on multiparty data alliances that transcend single-OEM silos.

Competitive Landscape

Continental, Bosch, and Aptiv dominate the automotive predictive technology market, leveraging embedded sensors, controllers, and analytics platforms directly integrated into OEM assembly lines. Meanwhile, NVIDIA, Microsoft, and IBM disrupt this status quo by offering AI toolchains devoid of legacy constraints, enabling automakers to curate top-tier capabilities. Qualcomm and Intel are carving out their niches with edge-processor roadmaps, enhancing inference workloads, and making the silicon layer a key differentiator.

Startups are venturing into specialized areas: from battery prognostics and predictive cybersecurity to universal data-aggregation APIs. A case in point is COMPREDICT, whose virtual sensor suite showcases how niche specialists can infiltrate OEMs by addressing specific software-driven pain points. However, hurdles like functional-safety certification, in-depth domain expertise, and established sales channels pose challenges for pure-tech entrants, reinforcing the dominance of Tier 1 suppliers.

Looking ahead, the lines between competitors will increasingly blur. Traditional suppliers are setting up cloud development centers, while tech behemoths are snapping up automotive testing labs, all in a bid to align with ISO 26262 and AUTOSAR standards. The future champions will seamlessly integrate in-vehicle resilience with expansive cloud learning, paving the way for the next wave of autonomous, self-repairing mobility platforms.

Automotive Predictive Technology Industry Leaders

-

Robert Bosch GmbH

-

Continental AG

-

Aptiv PLC

-

Valeo SA

-

Garrett Motion Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Webfleet and Questar Auto Technologies launched Predictive Vehicle Health Management, an AI maintenance solution that schedules service before breakdowns occur.

- September 2025: ZF debuted an AI-based chassis and drivetrain monitoring suite that flags loose wheel nuts and curb impacts in real time.

- January 2025: MyTVS unveiled Astra, an all-in-one telematics and diagnostics platform that automates service for India’s aftermarket.

Global Automotive Predictive Technology Market Report Scope

The automotive predictive technology market report is segmented by application (predictive maintenance, proactive alerts, safety and security, traffic management, and driver behavior monitoring), vehicle type (passenger cars, light commercial vehicles, and medium and heavy commercial vehicles), deployment (on-premise and cloud-based), hardware (ADAS components, telematics control units, sensors, GPS modules, cameras, and others), end user (OEM and aftermarket), technology (machine learning, big-data analytics, artificial intelligence, and IoT integration), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The market forecasts are provided in terms of value (USD).

| Predictive Maintenance |

| Proactive Alerts |

| Safety and Security |

| Traffic Management |

| Driver Behavior Monitoring |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| On-Premise |

| Cloud-Based |

| ADAS Components |

| Telematics Control Units |

| Sensors |

| GPS Modules |

| Cameras |

| Others |

| OEM |

| Aftermarket |

| Machine Learning |

| Big-Data Analytics |

| Artificial Intelligence |

| IoT Integration |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle-East and Africa |

| By Application | Predictive Maintenance | |

| Proactive Alerts | ||

| Safety and Security | ||

| Traffic Management | ||

| Driver Behavior Monitoring | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Deployment | On-Premise | |

| Cloud-Based | ||

| By Hardware | ADAS Components | |

| Telematics Control Units | ||

| Sensors | ||

| GPS Modules | ||

| Cameras | ||

| Others | ||

| By End User | OEM | |

| Aftermarket | ||

| By Technology | Machine Learning | |

| Big-Data Analytics | ||

| Artificial Intelligence | ||

| IoT Integration | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How big will predictive technology spending in vehicles be by 2031?

It is forecast to reach USD 88.06 billion, reflecting a 9.11% CAGR from 2026-2031.

Which automotive segment adopts predictive analytics fastest?

Medium and heavy commercial vehicles are set for a 10.14% CAGR as fleets seek uptime savings.

Why are proactive alerts gaining attention?

They warn of component failure milliseconds earlier than traditional diagnostics, cutting claim severity and downtime.

How do regulations influence market adoption?

Rules such as UNECE WP.29 and NHTSA FMVSS mandate cybersecurity and data recorders, making predictive features compulsory in many regions.

Page last updated on: