Automotive Robotics Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Market Size (2026) | USD 18.61 Billion |

| Market Size (2031) | USD 35.82 Billion |

| Growth Rate (2026 - 2031) | 14.01% CAGR |

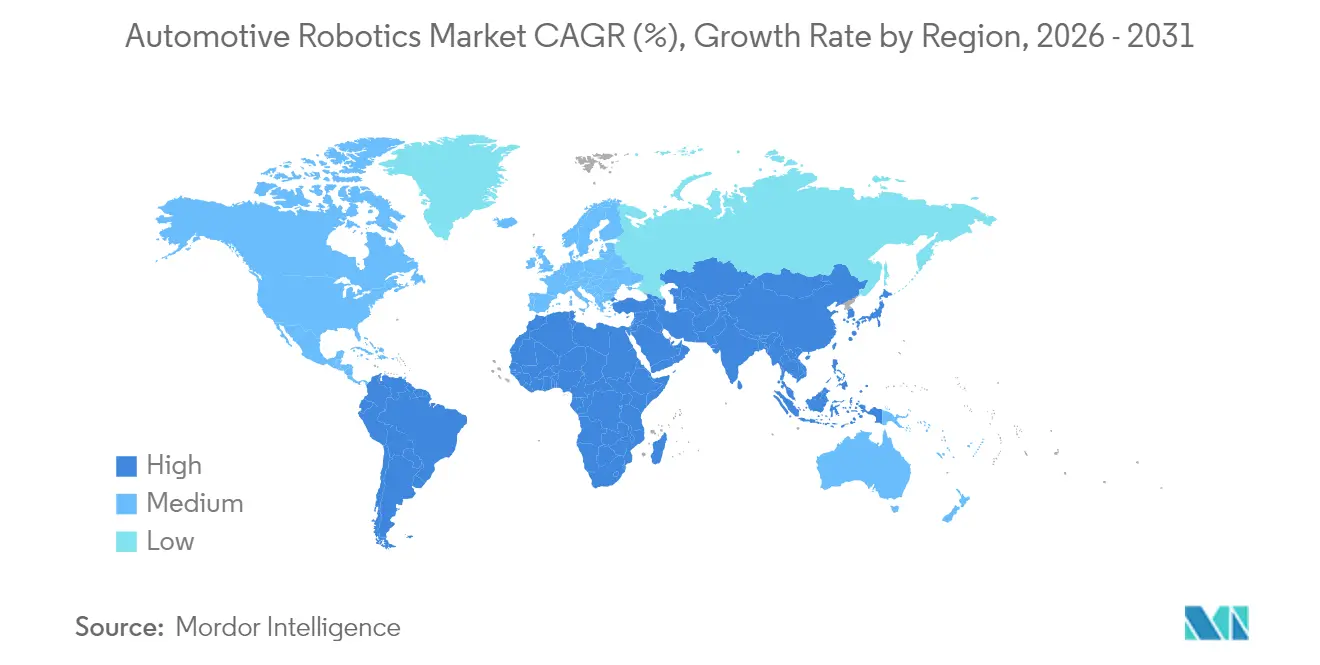

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Robotics Market Analysis by Mordor Intelligence

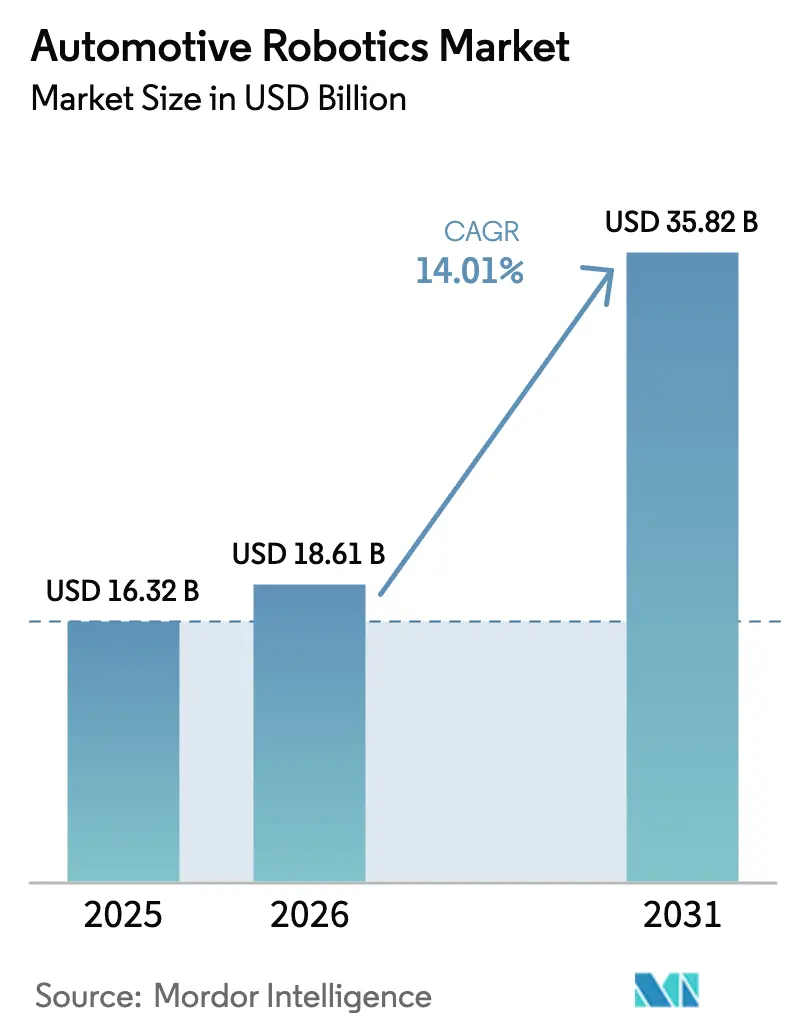

The automotive robotics market size was valued at USD 16.32 billion in 2025 and estimated to grow from USD 18.61 billion in 2026 to reach USD 35.82 billion by 2031, at a CAGR of 14.01% during the forecast period (2026-2031). Rapid electrification, widening labor gaps, and mounting quality expectations are prompting vehicle makers to replace manual stations with intelligent articulated and collaborative cells. Electric-vehicle battery pack integration, e-powertrain assembly, and full-body quality verification increasingly require motion precision that manual processes cannot match, especially as OEMs press for 100% inspection.

Key Report Takeaways

- By end-user type, vehicle manufacturers held 60.75% of the automotive robotics market share in 2025, whereas service centers are on track for a 14.12% CAGR between 2026 and 2031.

- By component type, robotic arms dominated with a 35.96% share in 2025, and software and services registered the highest 14.38% CAGR outlook.

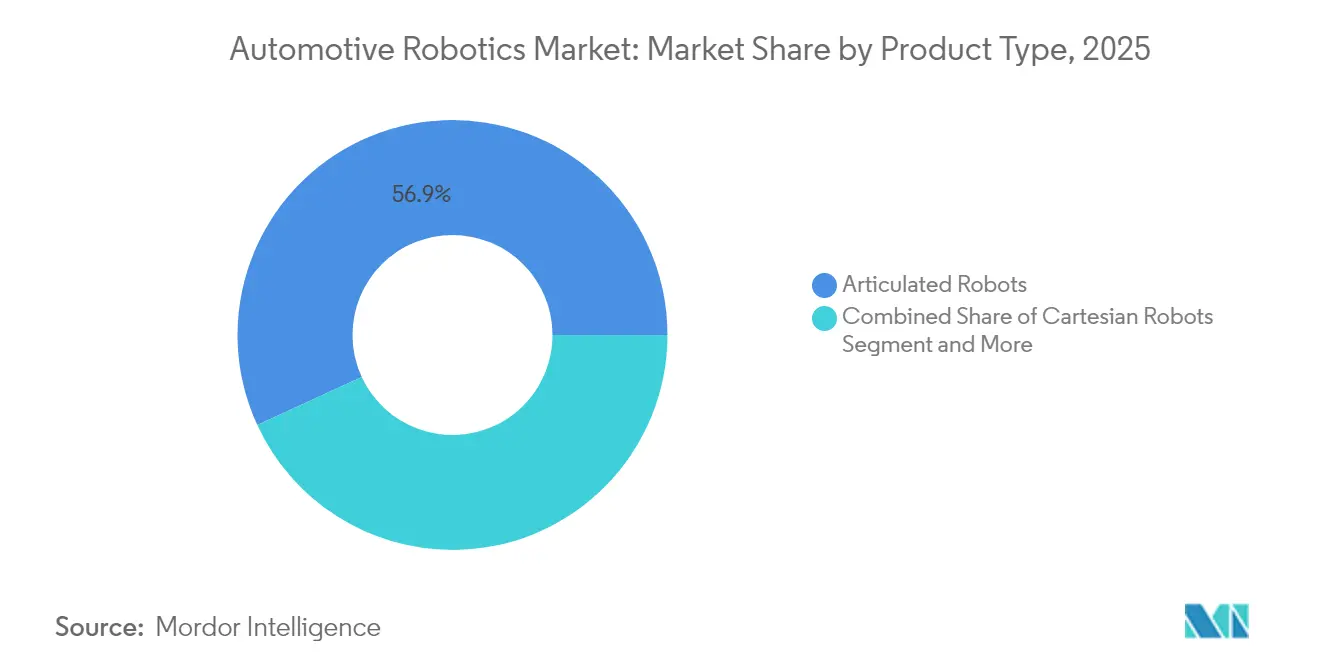

- By product type, articulated robots led with 56.88% revenue share in 2025, while collaborative robots are projected to grow at a 14.08% CAGR to 2031.

- By function type, welding robots accounted for 40.70% of the automotive robotics market size in 2025; inspection and quality-testing systems post the fastest expansion at a 14.19% CAGR through 2031.

- By geography, Asia-Pacific commanded a 46.10% share in 2025; South America represents the fastest-growing region at a 14.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Robotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automation to Boost Throughput and Quality | +3.2% | Global, concentrated in APAC and North America | Medium term (2-4 years) |

| EV-battery and E-powertrain Manufacturing Needs | +2.8% | Global, with early adoption in Europe and China | Long term (≥ 4 years) |

| Labor shortages and Wage Inflation in auto hubs | +2.5% | North America and EU, spill-over to APAC | Short term (≤ 2 years) |

| Tighter OEM Quality-Consistency Mandates | +2.1% | Global, stringent in premium segments | Medium term (2-4 years) |

| Cobots Enabling Flexible Mixed-Model Lines | +1.8% | APAC core, expanding to North America and EU | Medium term (2-4 years) |

| Emerging-Market Production-linked Incentives | +1.4% | South America, Southeast Asia, Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Automation to Boost Throughput & Quality

Manufacturers cite automation as the quickest route to alleviate production bottlenecks; 65.3% plan new robot investments to raise line throughput. The International Federation of Robotics logged a 14% rise in operational industrial robots during 2024, marking the steepest annual jump since 2018. Advanced inspection cells now test parts 10 times faster than coordinate-measuring machines, opening the door to 100% inspection without extending cycle time. AI-enabled vision detects defects smaller than 0.05 mm, creating a new quality baseline for body-in-white welding and final trim. As hardware prices drop, many plants recover capital outlays in one to three years, reinforcing the business case for expanded fleets.

EV-Battery & E-Powertrain Manufacturing Needs

Electric-vehicle assembly introduces heavier yet fewer sub-assemblies that require distinct handling, sealing, and welding methods. ABB estimates that 80 planned gigafactories will still leave battery supply short of demand, underscoring the need for high-throughput robotic production [1]“Automation Trends in Battery Manufacturing,” ABB Ltd., abb.com . Co-locating battery lines with final assembly promotes sustainability and reduces logistics, but only if robots can alternate between battery and body tasks. Specialized aluminum welding cells and end-of-life disassembly robots such as Thoth’s DisMantleBot illustrate new niches emerging from the EV shift.

Labor Shortages & Wage Inflation in Auto Hubs

Unfilled U.S. manufacturing roles hit 750,000 in 2024 and could top 2.1 million by 2030, forcing plants to automate to sustain output. Welding trades face the sharpest shortfall, with an annual supply of 82,500 recruits against demand for 330,000 jobs. Germany lost 19,000 automotive positions in 2024, yet struggles to recruit automation technicians. Robotics-as-a-service offerings and simplified teach-pendants are closing the skills gap, while FANUC’s partnerships with 1,500 educational institutions highlight the parallel need for workforce development.

Tighter OEM Quality-Consistency Mandates

Premium OEMs now stipulate zero-defect delivery. BENTELER’s Vigo plant replaced sample-based checks with ABB’s 3D metrology robots that compare every part to CAD files in real time, trimming rework and warranty exposure. AI software predicts failure patterns before they surface, shifting quality assurance from reactive control to predictive prevention. Cycle-time-neutral 100% inspection enhances regulatory compliance for ADAS and battery safety.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex & installation costs | -1.8% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Scarcity of skilled robot programmers | -1.2% | North America and EU, emerging in APAC | Medium term (2-4 years) |

| Cyber-security risks in connected cells | -1.0% | Global, with concentration in digitally advanced facilities | Medium term (2-4 years) |

| Servo-motor / chip supply volatility | -0.8% | Global, with acute impact in high-volume production | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex & Installation Costs

Small and medium suppliers still view six-figure robot cells as risky despite falling price points. Robotics-as-a-service vendors such as Rapid Robotics offset sticker shock through monthly contracts that bundle hardware, service, and software. Integration often doubles upfront spend because lines must be re-rigged for guarding, vision calibration, and operator training. FANUC’s USD 110 million Auburn Hills campus expansion shows the ecosystem investment needed to make turnkey deployment viable. Total cost of ownership also hinges on maintenance, software refreshes, and cyber-patching, often underestimated in business cases.

Scarcity of Skilled Robot Programmers

An acute shortage of programmers threatens to slow advanced deployments. User-friendly interfaces, manual-guidance teaching, and offline simulation via digital twins lower the barrier, yet AI-adaptive robots need deeper skills in data science and cybersecurity. KUKA’s plug-and-play software and ABB’s no-code path planning widen the talent funnel, but formal training pipelines still lag adoption growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Type: Vehicle Manufacturers Dominate Despite Service Growth

Vehicle makers held 60.75% of the automotive robotics market in 2025, reflecting their ability to absorb capital costs and embed articulated welders, painters, and sealers across every major line. This cohort now prioritizes AI vision for trim-and-final inspection and seeks cobots that can tackle ergonomic tasks once left to humans. Service centers form the fastest-growing slice, riding a 14.12% CAGR as EV diagnostics and ADAS calibration push mechanized processes into aftermarket bays.

Upskilling remains critical. OEMs such as Mercedes-Benz integrate humanoid robots to relieve staff from repetitive fetching tasks, while independent garages invest in robotic wheel alignment systems to shorten appointment times. Continued migration of complex repairs from dealerships to multi-brand centers will buoy the automotive robotics market into the next decade.

By Component Type: Software Services Surge Past Hardware

Robotic arms represented 35.96% of revenue in 2025, yet value is quickly shifting toward analytics, vision, and cyber-secure controllers. Software and services are advancing at a 14.38% CAGR, making this the prime strategic battleground. Cloud-hosted dashboards track utilization and issue predictive alerts, converting one-time capex into annuity streams.

Fleet-level orchestration platforms unify hundreds of cells into one virtual entity, enabling production planners to redeploy tasks in minutes rather than days. As hardware margins compress, vendors differentiate through continuous software updates and app-store ecosystems, reinforcing the automotive robotics market’s move toward outcome-based contracting.

By Product Type: Collaborative Robots Challenge Articulated Dominance

Articulated models still own 56.88% share thanks to payload capacity and six-axis dexterity. Even so, collaborative robots are climbing at 14.08% CAGR as manufacturers redesign lines for mixed-model builds. New cobots blend industrial-grade speed with force-limiting features that permit fenceless layouts, trimming floor space by up to 20%.

Humanoid variants such as Apptronik’s Apollo, under trial at Mercedes-Benz’s Berlin Digital Factory Campus, hint at a future where robots walk to sub-assembly zones and fetch kitted parts. This versatility aligns with automakers’ push for just-in-sequence flows, spurring broader adoption across the automotive robotics market.

By Function Type: Inspection Robots Accelerate Quality Demands

Welding held a 40.70% share in 2025, yet high-speed cameras and deep-learning classifiers are propelling inspection cells at a 14.19% CAGR. Aluminum body panels and battery casings require adaptive welding schedules that articulate torque and angle in milliseconds, achieved through lasers tied to machine-vision feedback loops.

Automated optical inspection can now scan a complete door in 80 seconds, exporting pass-fail data directly into MES dashboards. The quest for zero-defect output—especially for safety-critical ADAS housings and battery enclosures—positions inspection as the next frontier in the automotive robotics market.

Geography Analysis

Asia-Pacific retained 46.10% of the automotive robotics market in 2025, anchored by China’s 429,500 unit output and a robot density of 470 per 10,000 workers. Domestic vendors such as Siasun and Estun benefit from state incentives that keep acquisition costs low, while Japanese integrators continue to refine lean robotic cells for high-mix assembly. Southeast Asian governments extend production-linked incentives, inviting OEMs to localize EV lines with fully automated battery pack stations.

South America logs the highest 14.55% CAGR as multinationals commit fresh capital: Stellantis has earmarked EUR 5.6 billion for flexible EV capacity, and General Motors is spending USD 1.4 billion on robotic body shops in Brazil. Technology-transfer clauses in these deals allow local integrators to license advanced welding software, accelerating domestic expertise. Rising wage inflation reinforces the shift to robotics, particularly in Brazil’s chassis and powertrain plants.

North America pursues reshoring to mitigate geopolitical risk. USMCA rules of origin encourage suppliers to automate to maintain cost competitiveness despite labor shortages. Federal credits targeting battery production spark new gigafactory projects that integrate high-payload robots for cell stacking and module assembly. Europe holds steady yet demands high functional-safety compliance that favors premium robotic solutions. Germany continues to act as an R&D hub, even as margin pressure spurs automakers to transfer volume production to lower-cost regions.

Regulatory Landscape

Industrial robot deployments in automotive plants are shaped by evolving safety standards for robots, robot cells, and human-robot collaboration. ISO updated core industrial robot safety standards in 2025 (ISO 10218-1:2025 and ISO 10218-2:2025), tightening expectations around safe integration, lifecycle risk management, and compliance practices for industrial robots used in welding, material handling, and inspection cells.

Alongside this, vehicle automation policy work affects what OEMs expect from robotics-enabled verification and validation inside automotive manufacturing, especially for ADAS/ADS-related components. In the United States, USDOT has an Automated Vehicles framework (2025), and NHTSA reported ongoing research and rulemaking activity on automated driving systems in July 2025, reinforcing the emphasis on traceable test evidence, data handling, and repeatable inspection processes that are increasingly delivered through robotic metrology and vision systems.

Value Chain Analysis

The automotive robotics value chain covers core component suppliers (controllers, drives/servo systems, sensors/vision, end effectors), robot OEMs offering articulated and collaborative platforms, and a growing software layer that includes offline simulation, cell orchestration, and predictive maintenance. System integrators and line builders connect these elements to OEM and tier production lines, where commissioning, safety validation, and ongoing calibration often determine total deployment cost and uptime, particularly in mixed ICE/hybrid/EV plants that need frequent reconfiguration.

Recent moves show broader value-chain expansion beyond traditional robot makers into actuators, AI stacks, and service-led deployment models. Hyundai Mobis partnered with Boston Dynamics to develop robot actuators (with Boston Dynamics as the initial customer), and Toyota Motor Manufacturing Canada signed a Robots-as-a-Service commercial agreement with Agility Robotics to deploy Digit humanoid robots in RAV4 production. OEM-led co-development is also pushing upstream into manufacturing-ready humanoids, including Mitsubishi Motors signing an MOU with startup Highlanders to jointly develop humanoid robots and assess mass production feasibility at its Kyoto Plant, reinforcing that OEM plants are both adoption sites and capability-development nodes.

Competitive Landscape

The automotive robotics market exhibits moderate concentration. FANUC, ABB, KUKA, and Yaskawa still control a majority of installed bases, leveraging global support networks and vertically integrated portfolios. They now rush to embed AI chipsets such as NVIDIA Orin into next-generation controllers to deliver real-time adaptive path planning. Yaskawa’s Motoman NEXT exemplifies this convergence of hardware and machine intelligence.

OEM investments are reshaping competitive boundaries. Hyundai Motor Group absorbed Boston Dynamics for USD 1.1 billion, aiming to fold bipedal robots into logistics flows [2]“Boston Dynamics Acquisition Details,” Hyundai Motor Group, hyundai.com. Mercedes-Benz took a strategic stake in Apptronik to accelerate humanoid applications on final-trim lines [3]“Apptronik Collaboration Announcement,” Mercedes-Benz Group AG, mercedes-benz.com . Suppliers also internalize automation; Lear’s purchase of WIP Industrial Automation shows the appeal of proprietary systems to defend margins during platform transitions.

White-space opportunities surface in battery disassembly, aftermarket repair, and humanoid logistics. Emerging challengers pitch subscription models that de-risk adoption for tier-two suppliers. Success increasingly hinges on software ecosystems, cybersecurity robustness, and the breadth of service networks rather than on pure manipulator count, redefining how leadership is measured in the automotive robotics market.

Automotive Robotics Industry Leaders

ABB Ltd

FANUC Corporation

Yaskawa Electric Corporation

Kawasaki Heavy Industries (Robotics)

Nachi-Fujikoshi Corp

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is building around flexible automation for mixed-model production and EV-specific processes where precision handling and in-line quality verification are difficult to sustain with manual workflows. OEM plant investments and publicized deployments point to active demand: in June 2026, General Motors installed about 50 FANUC robot arms at its Factory Zero plant in Detroit to automate assembly tasks, and Maruti Suzuki inaugurated the Kharkhoda facility in India in July 2026, positioning it as a smart factory using Industry 5.0 practices and collaborative robots for human-machine collaboration.

Suppliers also have a clearer path to monetization through software, simulation, and service packaging that reduces integration risk and speeds changeovers. In July 2026, Toyota Motor North America announced a USD 3.6 billion expansion of its San Antonio, Texas plant to add advanced technology for assembly-line flexibility, aligning with OEM focus on reconfigurable robotics and digitally enabled cells. At the frontier, Mitsubishi Motors and Highlanders (July 2026) outlined joint development and mass-production exploration for humanoid robots at the Kyoto plant, creating an opportunity set for safety-certified humanoid manipulation, plant-ready actuator modules, and integration services that connect new robot form factors into MES and quality systems.

Recent Industry Developments

- July 2026: Mitsubishi Motors signed an MOU with startup Highlanders to jointly develop humanoid robots for manufacturing and explore mass production at Mitsubishi Motors' Kyoto Plant. The program connects humanoid R&D with an OEM production environment, opening a new integration lane for suppliers focused on actuators, safety systems, and line-ready deployment workflows.

- April 2026: FANUC America launched the CRX-3iA ultra-lightweight collaborative robot and added new capabilities across the CRX cobot lineup. The smaller payload class targets high-mix automotive tasks such as small-part assembly and inspection, supporting flexible redeployment where space and guarding constraints limit traditional industrial robot cells.

- October 2025: ABB announced an agreement to divest its Robotics division to SoftBank Group. The proposed ownership change represents a major restructuring for a top-tier industrial robotics supplier, with implications for product roadmaps, software ecosystem alignment, and global support models for automotive robot installed bases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The automotive robotics market is defined as the value of robots, related components, and supporting software and services used to automate tasks in automotive manufacturing. This covers core shop-floor functions such as welding, painting, assembly, material handling, and inspection.

Scope exclusions: We exclude general factory automation that is not deployed for automotive production lines, along with non-industrial consumer robots.

Segmentation Overview

- By End-User Type

- Vehicle Manufacturers (OEMs)

- Component Manufacturers (Tier-1 and 2)

- After-market and Service Centers

- By Component Type

- Controllers

- Robotic Arms

- End Effectors

- Drives and Sensors

- Software and Services

- By Product Type

- Cartesian Robots

- SCARA Robots

- Articulated Robots

- Collaborative Robots (Cobots)

- Other Types (Parallel, Cylindrical)

- By Function Type

- Welding Robots

- Painting Robots

- Assembly and Disassembly Robots

- Cutting and Milling Robots

- Material-Handling Robots

- Inspection and Quality-Testing Robots

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- South-East Asia

- Rest of Asia Pacific

- Middle East and Africa

- Turkey

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the market model and to anchor it to trackable signals tied to automotive production automation. We referenced public sources such as International Federation of Robotics (IFR) releases, national statistics agencies for industrial production, UN Comtrade for machinery trade flows, USITC and EU trade statistics portals, and peer-reviewed manufacturing and industrial engineering journals.

Alongside those, we reviewed company filings, investor presentations, and reputable industry press to understand product mix shifts (for example, higher cobot adoption in selected operations) and pricing direction. Where public disclosures were thin, a paid subscription covering company financials and another covering patents were used to cross-check revenue exposure and technology activity patterns. The desk research sources listed here are illustrative only, and we also reviewed other public and subscription sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on expert interviews and structured surveys with robotics suppliers, system integrators, automation distributors, and automotive manufacturing stakeholders who influence purchase cycles and utilization rates. For a global market like this, we tested assumptions across APAC, EMEA, and the Americas so gaps from uneven plant automation intensity and robot model mix could be corrected before finalizing the sizing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 17% | APAC: 41% |

| Mid tier: 46% | Functional/Unit leaders: 23% | EMEA: 34% |

| Smaller Players: 18% | Managers: 60% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach. Production and automation intensity indicators were first used to reconstruct the demand pool, then checked against supplier and channel realities. The top-down side leaned on automotive production levels, robot installation trends, and trade movement for industrial robots and key components, which were mapped to automotive use where adoption is consistently observed.

To keep the model practical, a few inputs were treated as the main drivers and refreshed every cycle. These included robot density in automotive plants, average system value progression by function (for example, welding versus inspection), the share of collaborative robots in applicable tasks, commissioning and integration time assumptions, and replacement plus retrofit rates. Results were corroborated with selective bottom-up approximations such as sampled average selling price times shipped unit ranges, integrator revenue exposure checks, and segment level sanity checks by major functions. When direct bottom-up data was missing in smaller countries, gaps were handled through proxy ratios tied to vehicle output and plant automation maturity, then adjusted after primary feedback.

For forecasting, scenario analysis was used, supported by trend fitting on core drivers like vehicle production outlook, capex cycles in body shops and paint shops, and the pace of EV platform line expansions. Each scenario was reviewed with primary respondents to settle on a base case consistent with observable factory investment behavior.

Data Validation & Update Cycle

Validation was done through triangulation across independent signals, followed by checks for year-to-year variance that could not be explained by production, pricing, or mix. Outliers were reworked by revisiting inputs such as function mix, assumed ASP changes, and the timing of major plant expansions, and then re-tested through follow-up calls when needed.

Before sign-off, the full model goes through multi-step analyst review so formulas, unit conversions, and scope mapping are consistent across regions and functions. The report is refreshed annually, with interim updates triggered when material events occur, such as sharp automotive production resets or major automation capex waves. Right before delivery, a final pass is completed so clients receive the latest updated view rather than an older snapshot.

Mordor Intelligence's Automotive Robotics Market Size Compared With Other Published Estimates

Published market values for automotive robotics often differ because the underlying scope, the way functions are counted, and the timing of price and currency assumptions are not the same across sources. Differences also show up when one estimate emphasizes robot hardware only, while another includes integration services, software, and aftermarket activity.

The main gap comes from whether software and services are counted alongside robot components, and from how function-level pricing is updated year to year. This is where Mordor Intelligence treats the market as a combined system value across core functions rather than a hardware-only roll-up tied to installation counts.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.32 B (2025) | |

| Industry Publisher A | USD 11.21 B (2025) | This figure appears to sit closer to a narrower counting logic that can understate total value when software, services, and integration are not consistently captured across functions like welding, inspection, and material handling. |

| Global Consultancy B | USD 9.70 B (2024) | A different base year and a likely heavier reliance on earlier-cycle pricing and adoption assumptions can shift the number downward, especially if retrofits and replacement demand are treated conservatively or not scaled with plant automation maturity. |

Across the three values, most of the spread is explained by scope and timing, rather than a disagreement on where automation is headed in automotive plants. By tying the model to function mix, realistic pricing progression, and repeatable adoption signals, the estimate is easier to reconcile with what buyers and suppliers see in actual procurement cycles.

Key Questions Answered in the Report

What is the current size of the automotive robotics market?

The automotive robotics market is valued at USD 18.61 billion in 2026 with a forecast to approach USD 35.82 billion by 2031.

Which robot type leads automotive applications?

Articulated robots dominate with 56.88% share, chiefly due to their versatility in welding, painting, and assembly.

Why are collaborative robots gaining popularity in automotive plants?

Cobots enable flexible mixed-model assembly without protective fencing and are projected to grow at a 14.08% CAGR through 2031.

Which geographic region is expanding fastest?

South America shows the highest growth pace at a 14.55% CAGR, propelled by large EV investments in Brazil and neighboring countries.

Page last updated on: