Automotive Glazing Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

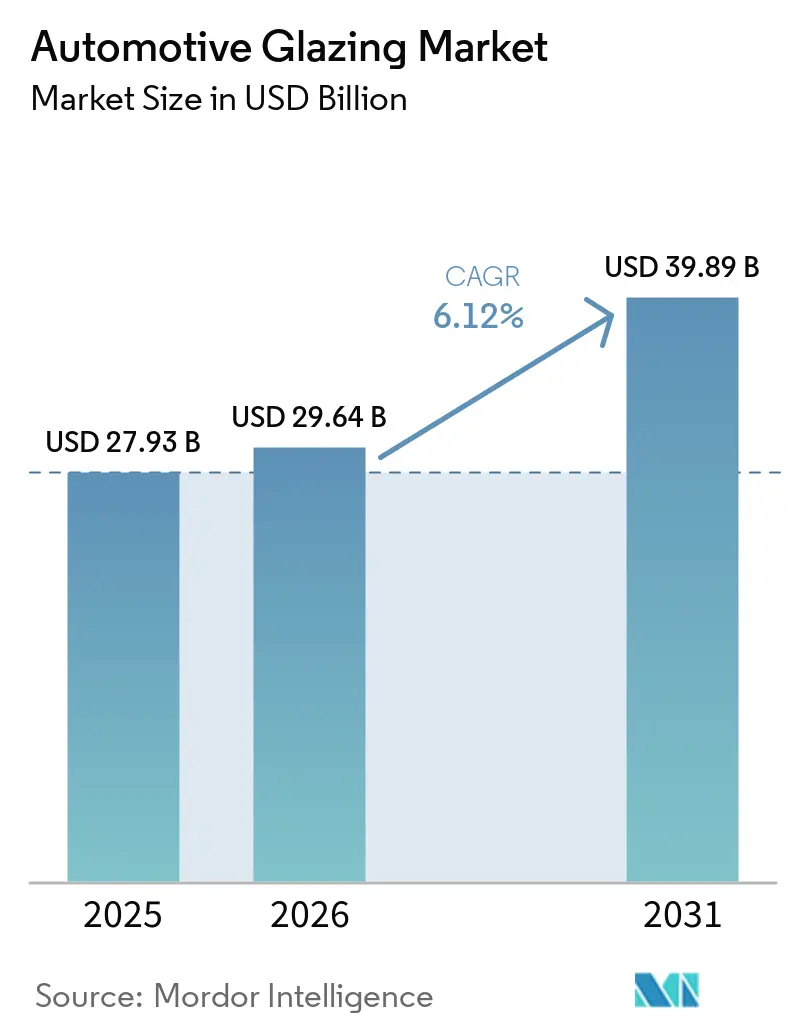

| Market Size (2026) | USD 29.64 Billion |

| Market Size (2031) | USD 39.89 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Glazing Market Analysis by Mordor Intelligence

The automotive glazing market size is expected to increase from USD 27.93 billion in 2025 to USD 29.64 billion in 2026 and reach USD 39.89 billion by 2031, growing at a CAGR of 6.12% over 2026-2031. Growth reflects a decisive shift toward lightweight substrates, panoramic sunroofs, and display-ready windshields as electric-vehicle scale-up, thermal-management rules, and connected-car features redefine competitive vehicle-glazing solutions. Weight reduction imperatives have pushed polycarbonate into side windows and roof modules, while thin, laminated glass remains critical wherever impact-retention rules apply. OEMs now specify heads-up display (HUD) wedges, photovoltaic (PV) films, and electrochromic dimming at the design stage, rather than relying on aftermarket retrofits. Regional production hubs in China and India accelerate technology diffusion, and regulatory pressure in Europe shapes safety, noise, and recycling benchmarks adopted worldwide.

Key Report Takeaways

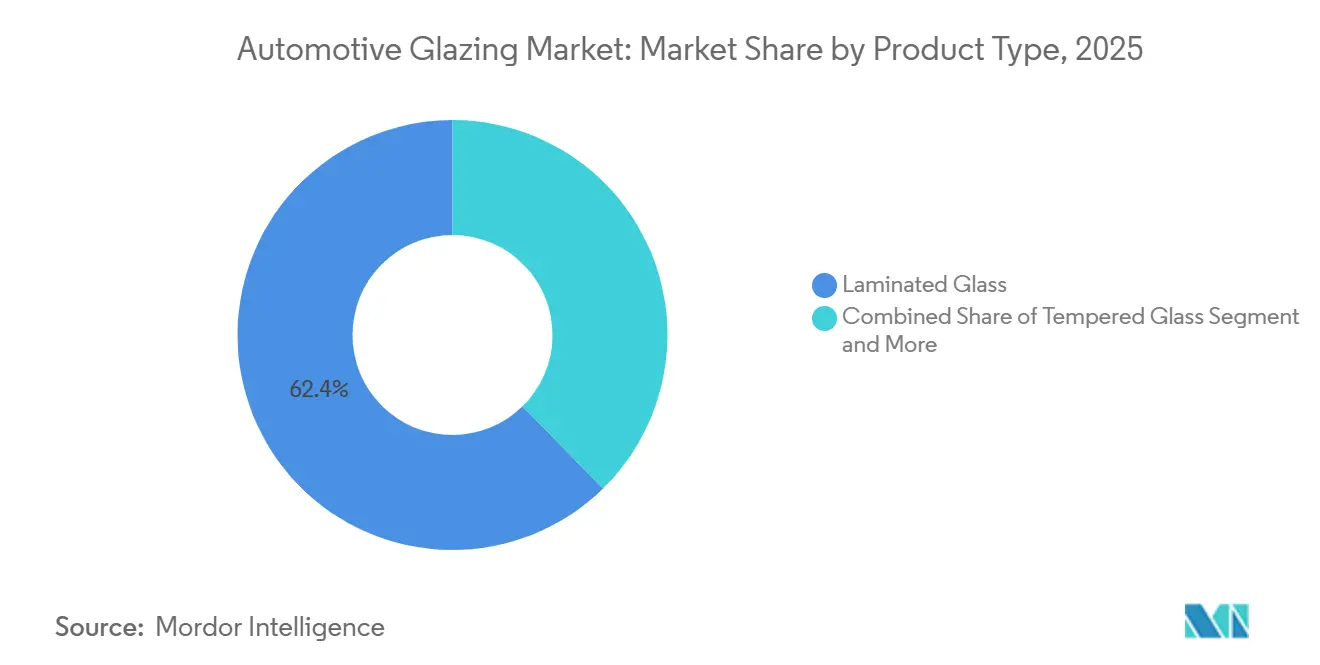

- By product type, laminated glass accounted for 62.35% of the automotive glazing market share in 2025, whereas the polycarbonate segment is forecast to grow at a 7.13% CAGR through 2031.

- By application, front windshields led with 47.22% share of the automotive glazing market size in 2025; sunroofs are projected to register the fastest 7.96% CAGR to 2031.

- By vehicle type, passenger vehicles accounted for 72.36% of the automotive glazing market share in 2025 and are projected to post the fastest growth rate of 6.62% CAGR to 2031.

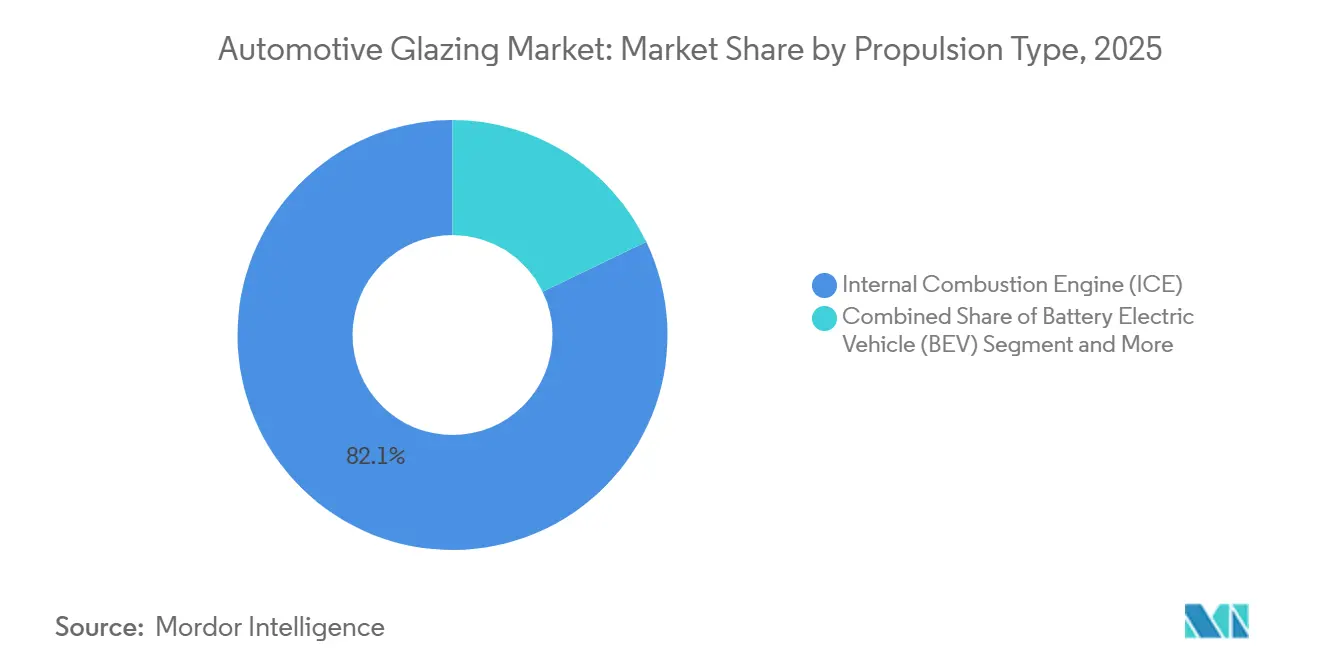

- By propulsion, internal-combustion platforms dominated with an 82.14% of the automotive glazing market share in 2025, yet battery-electric vehicles show the strongest 9.25% CAGR through 2031.

- By distribution channel, OEM installations accounted for 91.05% of the automotive glazing market in 2025 and remain the fastest-growing route, with a 7.01% CAGR through 2031.

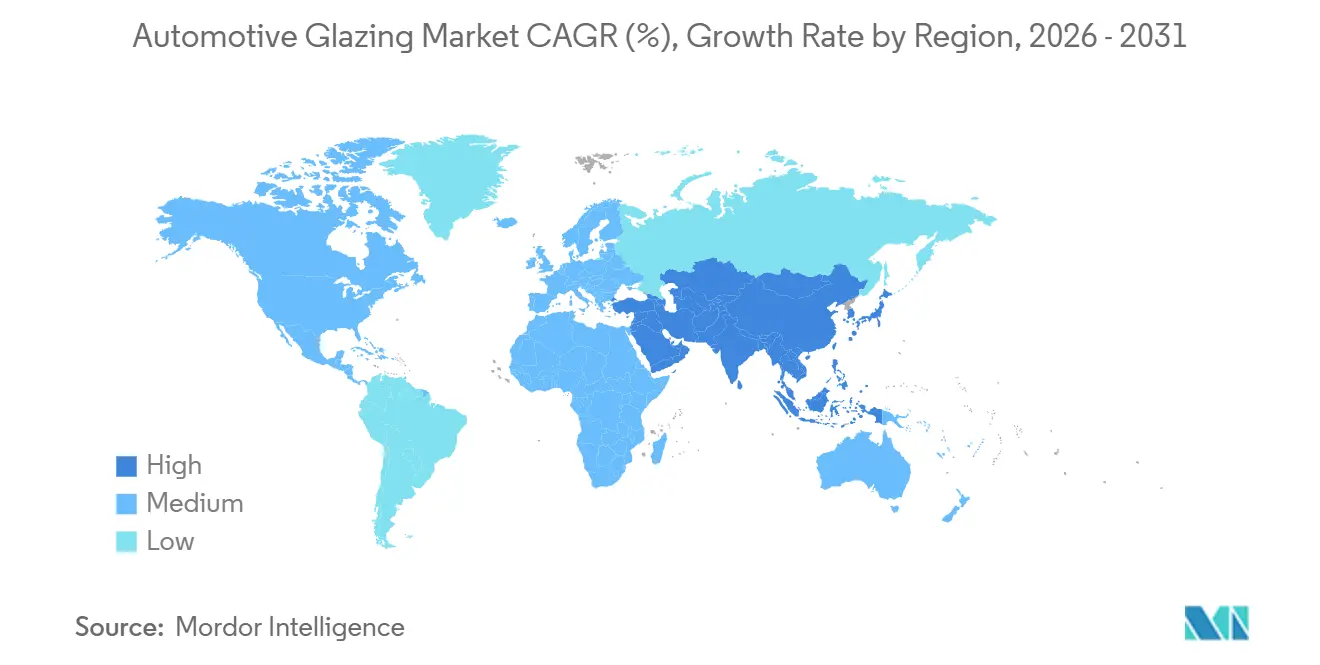

- By geography, Asia-Pacific led with a 45.81% share of the automotive glazing market in 2024 and is the fastest climber, with a 7.31% CAGR during the forecast period through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Glazing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vehicle Production in Emerging Economies | +1.2% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Lightweight Glazing Boosts EV Efficiency | +0.8% | Global, with early gains in Europe and China | Long term (≥ 4 years) |

| Surge in Panoramic Sunroofs | +0.7% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| OEM Demand for Display Glass | +0.6% | Global premium segments | Medium term (2-4 years) |

| Acoustic Glazing for Urban Noise | +0.5% | Europe core, expanding globally | Long term (≥ 4 years) |

| Solar Energy Harvesting with Glazing | +0.3% | Europe, Japan, California early adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Production in Emerging Economies

Factory output in India and the ASEAN corridor is expanding, pulling glazing supply chains toward localized float lines. Fuyao’s dual-plant blueprint, China as a scale engine, and Hungary for European just-in-time programs illustrate the responsiveness needed to win first-fit contracts in new assembly hubs. Technology once reserved for premium trims, such as UV-cut coatings and low-emissivity layers, is entering volume models as local tier-ones ramp capacity.

Lightweight Glazing Boosts EV Range and Fuel Efficiency

Electric-vehicle platforms treat every kilogram saved as extended driving range. Polycarbonate weighs roughly half as much as glass and shows lower thermal conductivity, easing HVAC demand that drains battery capacity[1]"Polycarbonate vs Glass: The Ultimate Showdown for Strength & Clarity," G-Crystal Plastic Industries, gcrystal-pc.com. AGC and Saint-Gobain validated hybrid laminates that meet frontal-impact rules while trimming mass, and Chinese producers deploy thinner interlayers on BEV side windows to compound savings. Global OEM adoption quickens wherever stringent fleet-average CO₂ standards compel weight reduction without increasing battery pack size.

Surging Adoption of Panoramic Sunroofs

Panoramic roofs have moved from a luxury option to a mainstream expectation, and suppliers now layer PV cells and electrochromic films to monetize that glass real estate. AGC’s 2024 launch of a TOPCon/HJT PV sunroof capable of producing up to 380 W confirmed OEM interest in dual-use roof modules that combine structural transparency and power generation in a single part[2]Valerie Thompson, "AGC Automotive Europe unveils photovoltaic panoramic sunroof for passenger vehicles," PV Magazine, www.pv-magazine.com. Design studios increasingly specify full-roof apertures even on B-segment crossovers, cementing sunroofs as the fastest-growing application.

OEM Push for HUD-Ready “Display” Glass

Engineered as optical components rather than mere passive barriers, windshields are essential for augmented-reality HUDs. Wedge interlayers prevent double imaging, while transparent OLED films prime the substrate for software-defined cabins. The lack of global brightness standards or fail-safe regulations allows early adopters to establish their own performance benchmarks, influencing the market's trajectory and fostering innovation in augmented-reality technology.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost and Process Complexity | -0.9% | Global, acute in price-sensitive segments | Short term (≤ 2 years) |

| Soda-Ash Shocks Inflate Glass Costs | -0.6% | Global, severe in Asia-Pacific | Medium term (2-4 years) |

| Regulations Limit Polycarbonate In Windscreens | -0.4% | Global, strict in Europe/United States | Long term (≥ 4 years) |

| Recycling Mandates Add Logistics Burden | -0.3% | Europe core, expanding to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost and Process Complexity of Advanced Glazing

Embedding photovoltaic layers, electrochromic stacks, or HUD interlayers forces suppliers to invest in capital-intensive furnace upgrades, tighter clean-room controls, and new inline inspection steps. Each additional layer multiplies yield risk because an imperfection in any sheet can condemn the entire laminate, so learning-curve scrap can erode profit margins before scale efficiencies arrive. The expense is felt most acutely in high-volume nameplates, where price elasticity is low, making it harder for OEMs to pass on material premiums to consumers. Certification testing, such as impact and UV-aging trials required under global safety codes, further lengthens development cycles and ties up working capital.

Soda-Ash Supply Shocks Inflating Glass Costs

Soda ash, a core melting ingredient, experienced sharp price swings after energy-market turbulence and logistics bottlenecks in 2025 disrupted export volumes into Europe and North America. Sudden cost spikes squeeze float-line operators because furnace temperatures cannot be modulated quickly, and shutdowns risk refractory damage, forcing producers to absorb elevated input bills or renegotiate contracts mid-stream. Regional price differences also distort competition; plants in China, where domestic soda-ash output is abundant, gained a margin buffer while peers reliant on imports saw contribution margins evaporate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Polycarbonate Gains Despite Laminated Dominance

Laminated glass maintained 62.35% of the automotive glazing market share in 2025, underlining its compliance with global impact-retention rules. Polycarbonate is the fastest-rising alternative, projected to expand at a 7.13% CAGR as automakers leverage its weight advantage for side windows and roof modules. Suppliers explore hybrid assemblies that pair laminated windshields with polycarbonate sidelites, enabling platforms to meet safety codes without sacrificing mass targets. Technical hurdles remain around scratch resistance and long-term clarity, yet ongoing coating advances suggest regulatory bodies could eventually relax front-glazing restrictions, opening additional volume.

Firms able to qualify multi-material solutions early will capture specification wins as next-generation electric architectures freeze designs. Continued R&D blurs categorical lines by marrying thin laminated sheets with polymer cores, helping incumbents defend their installed furnace base while meeting lightweight benchmarks. OEMs value the acoustics and infrared attenuation of laminated constructions, so a wholesale switch is unlikely in the near term. Instead, a coexistence model emerges in which each substrate is matched to specific vehicle zones to optimize cost, mass, and regulatory headroom.

By Application Type: Sunroofs Outpace Windshields

Front windshields held 47.22% share of the automotive glazing market size in 2025, anchored by legal mandates for laminated construction and the sheer surface area of the part. Sunroofs, however, lead growth with a 7.96% CAGR as panoramic layouts migrate from premium badges into compact crossovers. Designers champion full-roof transparency to create an airy cabin feel, and suppliers now integrate dimmable or photovoltaic films to add functional value without altering exterior sheet metal. The upgrade path aligns with OEM revenue strategies because roof glass offers high perceived luxury while requiring minimal platform re-engineering.

Windshields are simultaneously evolving from passive barriers into digital displays, thanks to wedge interlayers that support HUD projectors and augmented-reality overlays. These optics demand pristine surface flatness and strict refractive-index tolerances, tightening specification windows for glass makers. Side and rear lights lag in feature adoption but gradually inherit coatings first proven on windshields, creating trickle-down demand. The pace of cross-application migration will hinge on how quickly suppliers standardize new stacks across varied curvature and thickness requirements.

By Vehicle Type: Passenger Cars Drive Volume

Passenger vehicles dominated the automotive glazing market with 72.36% market share in 2025 and are set to post the fastest CAGR of 6.62%, reflecting both their production scale and consumer appetite for panoramic and acoustic features. Retail buyers associate expansive glass with premium ambiance, so manufacturers bundle large roof apertures and quiet cabins to lift transaction prices. In contrast, commercial fleets often specify utilitarian glass to control operating costs, thereby delaying the adoption of advanced substrates. Nevertheless, rising last-mile delivery activity nudges van makers to consider lightweight glass that offsets payload weight and extends electric range.

Suppliers therefore maintain dual development tracks: cost-optimized tempered sets for core fleet business and feature-rich laminates for lifestyle derivatives. The bifurcation challenges production planning because the same assembly line may alternate between commodity and high-spec builds. Robust scheduling and quick tooling changeovers become essential to preserve furnace utilization. Tier-ones with footprint flexibility can stage different product mixes by region, satisfying strict premium-content expectations in mature markets while meeting price points in growth economies.

By Propulsion Type: BEVs Lead Growth Metrics

Internal-combustion vehicles retained 82.14% share in 2025, yet battery electric vehicles chart the strongest 9.25% CAGR as policy incentives and charging infrastructure mature. BEV platforms use glazing as a thermal-management lever because every kilowatt saved on HVAC translates into additional driving range. Low-emissivity coats, integrated shading, and lightweight substrates, therefore, move from optional extras to baseline engineering requirements. Suppliers must align development cycles with rapid BEV model refreshes, which occur more quickly than legacy engine redesigns, compressing traditional certification timelines.

Because electrification by propulsion type cascades unevenly across regions, firms juggle portfolios that still serve high-volume ICE demand while scaling new coating and polymer lines for EV allocations. Investment resilience hinges on platform commonality; glass variants that accommodate sensors or roof PV arrays across both ICE and BEV derivatives spread tooling cost over larger volumes. Collaborative roadmaps between glazing specialists and battery-thermal engineers are becoming commonplace as OEMs pursue integrated energy-saving packages.

By Distribution Channel: OEM Installations Remain Predominant

OEM fitments captured 91.05% of the automotive glazing market share in 2025 and continue to grow at a 7.01% CAGR, driven by factory-installed solutions that ensure perfect alignment for cameras, antennas, and HUD projectors. Complex lamination stacks require controlled environments and tight takt times that independent repairers cannot easily replicate. As vehicles embed more sensors behind glass, calibration obligations shift additional revenue from the aftermarket toward authorized service programs. Insurers, facing higher claim costs for ADAS windshields, increasingly steer repairs to OEM-approved networks to guarantee functional restoration.

Aftermarket operators respond by specializing in standard tempered replacements where calibration needs are minimal, but the profit pool narrows as smart glass penetration rises. Some large chains invest in advanced recalibration rigs to preserve relevance. Yet, tooling costs deter smaller workshops. Glass makers therefore court two distinct customer sets: high-technology modules shipped directly to assembly plants and commodity panes distributed through collision-parts networks.

Geography Analysis

Asia-Pacific retained 45.81% of the automotive glazing market share in 2025 and shows the quickest 7.31% CAGR outlook. This growth is largely driven by a surge in Battery Electric Vehicles (BEVs) in China, increasing production in India, and a technological exchange from Japan and South Korea. Local suppliers are expanding their float-glass capacities, while governments are enticing investment through incentives, notably energy-efficient furnaces and recycling mandates.

While Europe and North America lag in volume, they excel in the value derived from vehicle content. In Europe, directives focused on acoustic emissions and end-of-life recycling are shaping Original Equipment Manufacturer (OEM) specifications. This emphasis has made features such as low-noise, easily dismantled glass essential in procurement. Meanwhile, North America is capitalizing on its regional supply chains, which span from float lines in the United States Midwest to assembly corridors in Mexico, effectively mitigating the challenges posed by currency fluctuations and freight costs.

Though South America, the Middle East, and Africa currently represent smaller segments of the automotive glazing market, there's evident potential. For instance, the rising demand for premium SUVs in Gulf states and experimental BEV initiatives in Brazil hint at this upside. However, realizing this potential will depend on factors such as economic stability, the skill level of the workforce, and clear policies on import duties in relation to incentives for local float-line production.

Competitive Landscape

The automotive glazing market exhibits moderate concentration. AGC, Saint-Gobain, Nippon Sheet Glass, Fuyao, and Xinyi anchor global float-glass capacity yet now race to combine coatings, solar films, and display substrates faster than Tier-2 innovators. AGC’s Volta hybrid melting cuts energy use while preserving optical clarity, signaling capital commitments that raise entry barriers.

Fuyao’s vertically integrated model, from soda-lime furnaces to laminated module assembly, helps it price aggressively and localize supply for European OEMs via its 2025 Hungarian plant. New entrants exploit white spaces in electrochromic and perovskite PV coatings, often partnering with electronics firms to leapfrog glass-only incumbents.

The convergence of software and substrates will define the next contest: windshield HUD calibration, solar roof power electronics, and real-time tint control will demand multidisciplinary teams. Regulatory mastery, meeting UNECE impact rules, ISO quality audits, and region-specific acoustic norms, remains a gatekeeping function that favors incumbents but can also reward nimble specialists who validate new chemistries ahead of standard-setting rounds.

Automotive Glazing Industry Leaders

-

AGC Inc.

-

Saint-Gobain S.A.

-

Nippon Sheet Glass Co., Ltd.

-

Fuyao Glass Industry Group Co., Ltd.

-

Xinyi Glass Holdings Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: AquaClear, a windshield treatment designed for enhanced clarity and ease of application on multiple surfaces, made its debut from NOVUS Polish.

- October 2025: FORVIA HELLA began mass production of a smart-dimming glass controller adopted by leading Chinese automakers, deepening its body-electronics footprint.

- March 2025: THACO Industries inaugurated a premium automotive glass plant in Vietnam with an annual capacity of 450,000 sets, boosting localization.

Global Automotive Glazing Market Report Scope

The Automotive Glazing Market is analyzed based on product type, application type, vehicle type, propulsion type, distribution channel, and geography.

By Product Type, the market is segmented into Laminated Glass, Tempered Glass, and Polycarbonate Glass. By Application Type, the market is segmented into Front Windshield, Rear Windshield, Sidelites (Side Windows), Sunroof, and Quarter Glass. By Vehicle Type, the market is segmented into Passenger Vehicles, Light Commercial Vehicles, and Medium and Heavy Commercial Vehicles. By Propulsion Type, the market is segmented into Internal Combustion Engine (ICE), Battery Electric Vehicle (BEV), Hybrid Electric Vehicle (HEV), Plug-In Hybrid Electric Vehicle (PHEV), and Fuel-Cell Electric Vehicle (FCEV). By Distribution Channel, the market is segmented into OEM and Aftermarket. By Geography, the market is segmented into North America (United States, Canada, and Rest of North America), South America (Brazil, Argentina, and Rest of South America), Europe (United Kingdom, Germany, Spain, Italy, France, Russia, and Rest of Europe), Asia-Pacific (India, China, Japan, South Korea, and Rest of Asia-Pacific), and Middle East and Africa (United Arab Emirates, Saudi Arabia, Turkey, Egypt, South Africa, and Rest of Middle East and Africa).

Market forecasts are provided in terms of Value (USD).

| Laminated Glass |

| Tempered Glass |

| Polycarbonate Glass |

| Front Windshield |

| Rear Windshield |

| Sidelites (Side Windows) |

| Sunroof |

| Quarter Glass |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) |

| Plug-In Hybrid Electric Vehicle (PHEV) |

| Fuel-Cell Electric Vehicle (FCEV) |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Laminated Glass | |

| Tempered Glass | ||

| Polycarbonate Glass | ||

| By Application Type | Front Windshield | |

| Rear Windshield | ||

| Sidelites (Side Windows) | ||

| Sunroof | ||

| Quarter Glass | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Battery Electric Vehicle (BEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Plug-In Hybrid Electric Vehicle (PHEV) | ||

| Fuel-Cell Electric Vehicle (FCEV) | ||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current growth outlook for the automotive glazing market?

The automotive glazing market is expected to increase from USD 27.93 billion in 2025 to USD 29.64 billion in 2026 and reach USD 39.89 billion by 2031, growing at a CAGR of 6.12% over 2026-2031

Which product dominates sales in automotive vehicle glass?

Laminated glass holds the highest share, securing 62.35% of 2025 revenue, thanks to its mandated use in front and rear windshields.

Why are panoramic sunroofs expanding so quickly?

Consumer preference for open cabins and OEM adoption of photovoltaic roof modules drive a 7.96% CAGR for sunroof applications.

How are battery electric vehicles changing glazing specifications?

BEVs need lightweight, low-emissivity, and sometimes solar-integrated glass to extend driving range and manage cabin heat.

Page last updated on: