Automotive Fluid Transfer System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

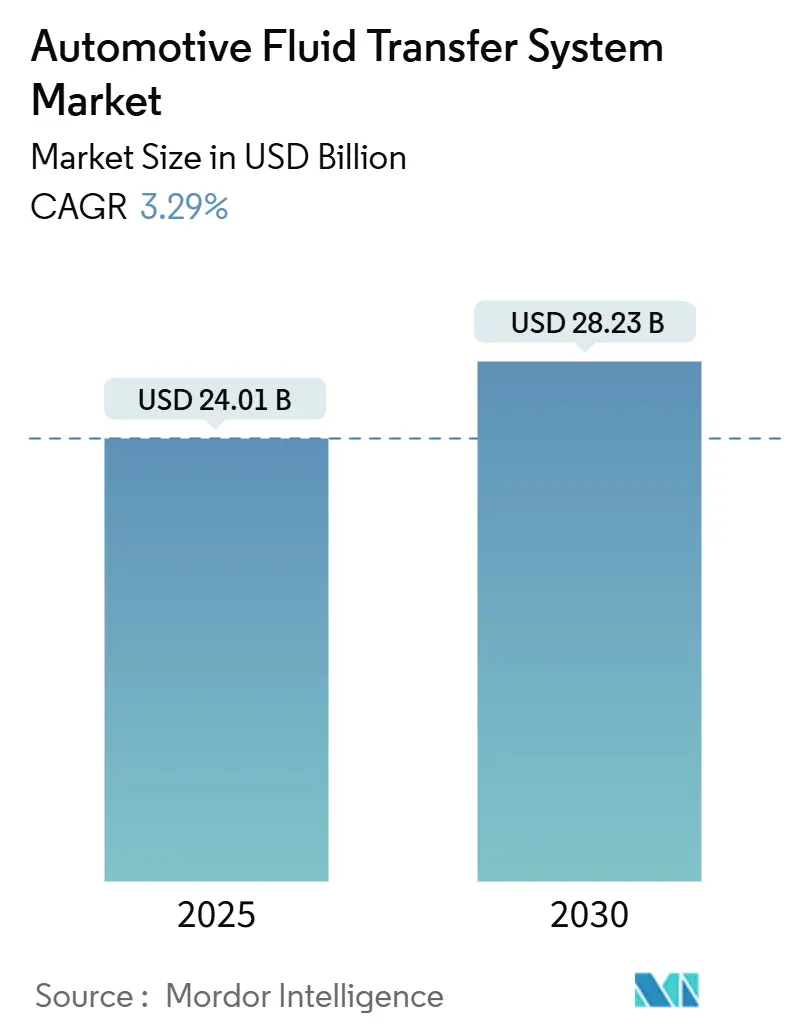

| Market Size (2025) | USD 24.01 Billion |

| Market Size (2030) | USD 28.23 Billion |

| Growth Rate (2025 - 2030) | 3.29% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

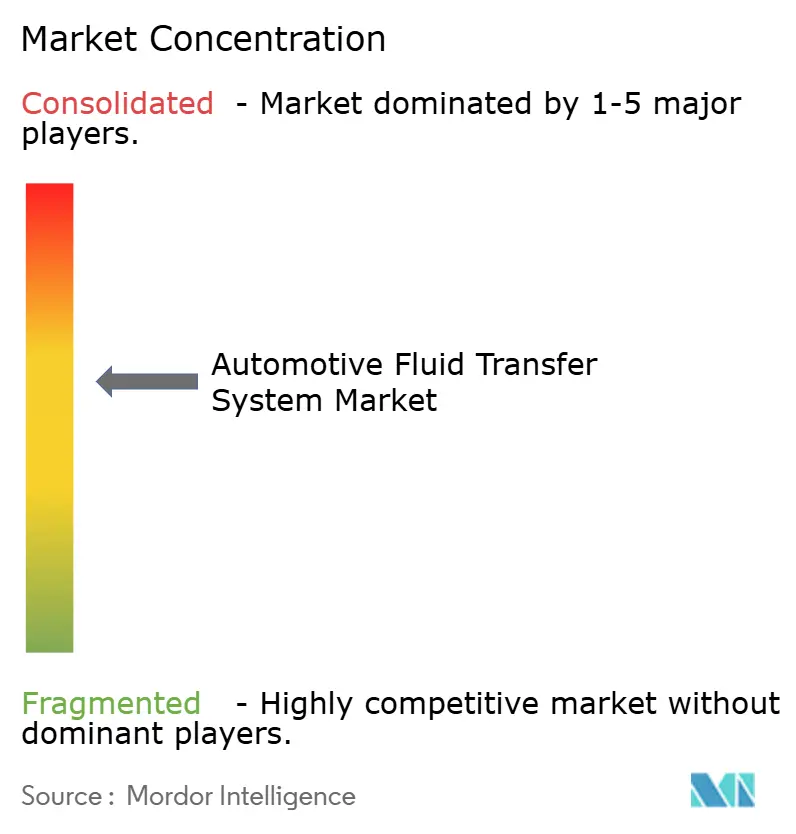

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Fluid Transfer System Market Analysis by Mordor Intelligence

The automotive fluid transfer system market posts a current value of USD 24.01 billion in 2025 and is forecast to reach USD 28.23 billion by 2030, advancing at a 3.29% CAGR over the period. The combination of investments in electrified platforms and tightening emission rules sustains steady demand for coolant, brake, transmission, and emerging dielectric circuits while tempering gains for conventional fuel lines. The growing complexity of multi-loop thermal architectures, especially in battery-electric and hybrid vehicles, favors suppliers that can deliver bundled hose, pump, and sensor assemblies. Aftermarket prospects brighten as vehicle lifecycles lengthen and service networks tackle more intricate fluid circuits, yet the competitive field stays moderately concentrated as leading tier-1s pivot their portfolios toward thermal management.

Key Report Takeaways

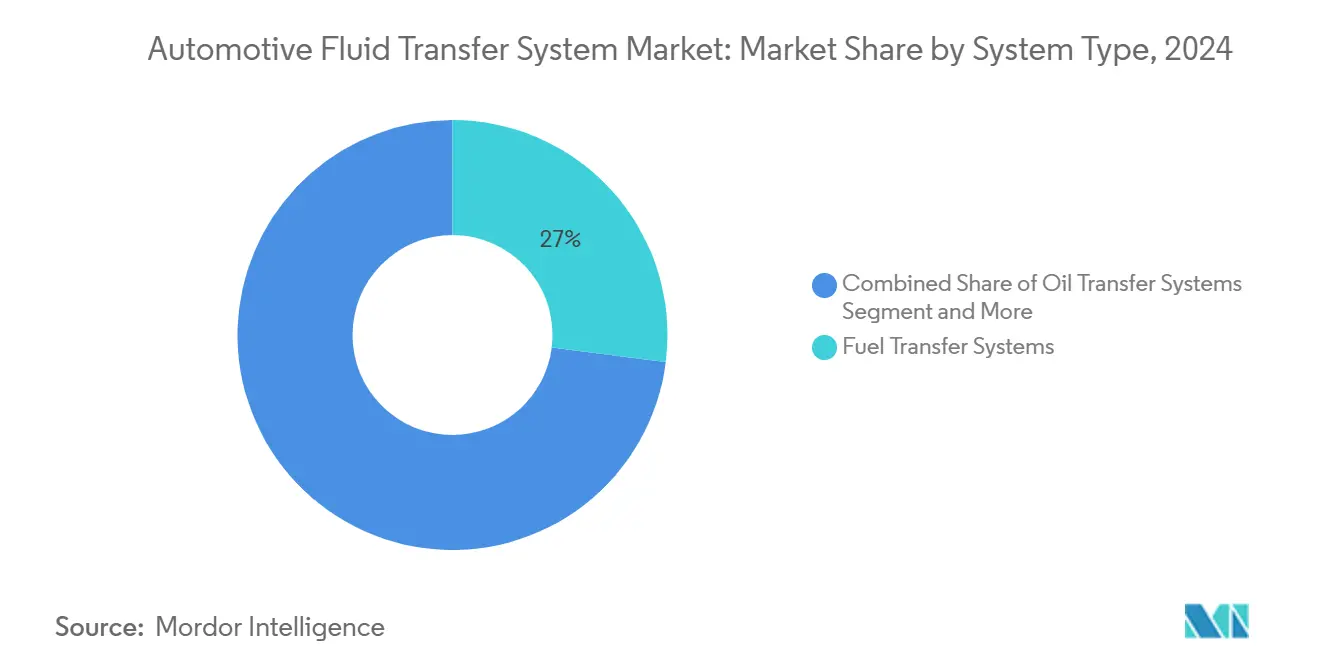

- By system type, fuel transfer retained 27.04% of the automotive fluid transfer system market share in 2024, while coolant transfer is projected to grow at a 3.86% CAGR to 2030.

- By vehicle type, passenger cars commanded a 62.15% of the automotive fluid transfer system market share in 2024, and medium-heavy commercial vehicles are poised to expand at a 4.67% CAGR through 2030.

- By propulsion type, internal combustion engines held 84.13% of the automotive fluid transfer system market share in 2024; battery-electric vehicles lead growth at a 6.49% CAGR to 2030.

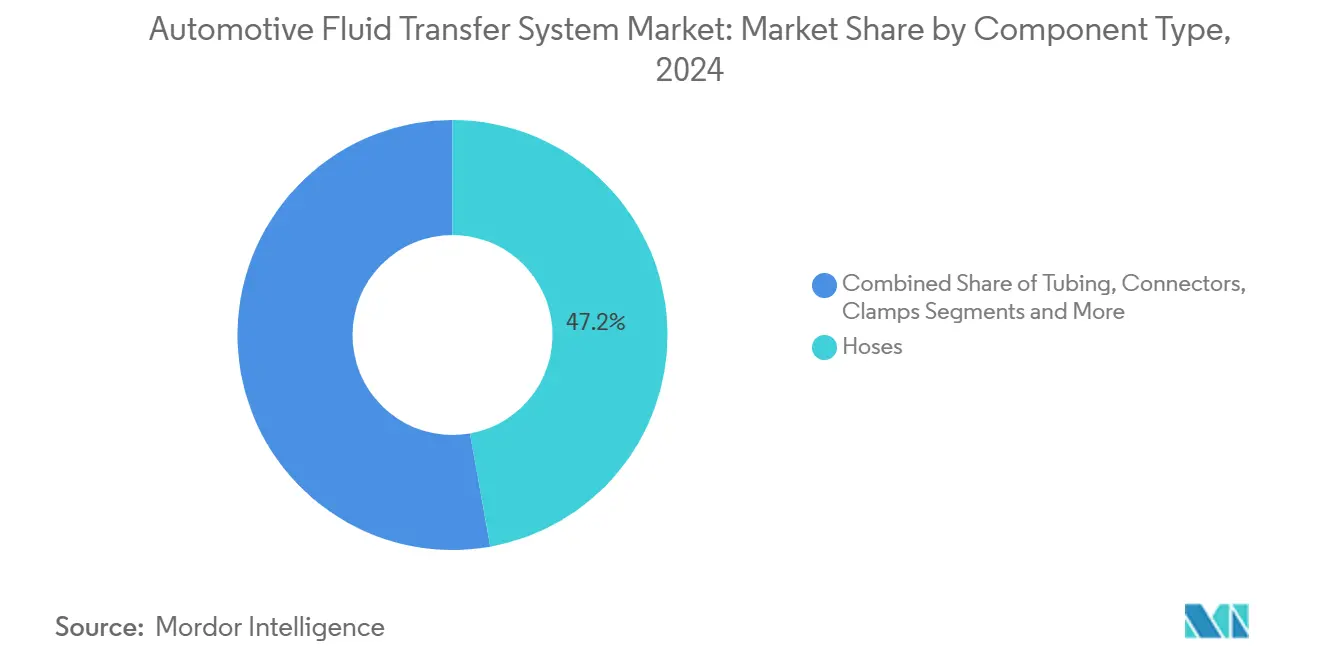

- By component type, hoses led with 47.22% of the automotive fluid transfer system market share in 2024, whereas pumps will climb at a 5.04% CAGR between 2025-2030.

- By distribution channel, OEM accounted for 73.18% of the automotive fluid transfer system market share in 2024, and the aftermarket is set to rise at a 5.23% CAGR during the forecast window.

- By geography, Asia-Pacific captured 48.33% of the automotive fluid transfer system market share in 2024; North America records the fastest 4.12% CAGR over 2025-2030.

Global Automotive Fluid Transfer System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-Loop Thermal Circuit Growth | +0.9% | Asia-Pacific, Europe | Long term (≥ 4 years) |

| DPF and SCR Fluid-Line Demand | +0.8% | Europe, North America | Medium term (2-4 years) |

| High-Temperature Oil and Coolant | +0.6% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Smart Hoses Enable Predictive Maintenance | +0.5% | North America, Europe | Medium term (2-4 years) |

| Laser-Welded Brake Tubing Cuts Weight | +0.4% | Global premiums | Short term (≤ 2 years) |

| Megawatt Charging Needs Coolant Connects | +0.3% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid BEV/HEV Sales Growth Creating Multi-Loop Thermal-Management Fluid Circuits

Liquid battery cooling that keeps cell temperatures within 15-35 °C has become standard on most 400 V passenger EVs and remains critical for fast charging above 350 kW. Hanon Systems integrates refrigerant-to-coolant plate heat exchangers so one chiller can precondition packs, power electronics, and cabin systems simultaneously [1]“Integrated EV Heat Pump Systems,” Hanon Systems, hanonsystems.com. Multi-loop layouts demand flexible hose assemblies that can route through tight under-floor tunnels while mitigating NVH and electrochemical interactions. Tier-1s are responding with modular manifolds that shorten assembly hours on high-volume production lines, positioning themselves as co-design partners rather than commodity hose suppliers.

Tightening Emission and Fuel-Economy Norms Accelerating Adoption of DPF/SCR Fluid Lines

Euro 7 rules, effective 2027, introduce brake particulate limits and stronger SCR efficiency targets, compelling OEMs to specify corrosion-resistant diesel exhaust fluid circuits that integrate heaters and quality sensors [2]“Euro 7: new emission standards for vehicles,” European Commission, europa.eu . Integrated sensor assemblies developed by TE Connectivity combine level, temperature, and urea-quality detection to meet these new diagnostics needs. Suppliers that already service AdBlue® lines in Europe are leveraging their expertise to bid on similar programs for North American truck platforms, cementing a cross-regional opportunity through the decade.

Turbo-GDI Engine Proliferation Raising Demand for High-Temperature Oil and Coolant Lines

Higher combustion pressures in turbocharged gasoline direct-injection engines push peak coolant temperatures to above 120 °C, obliging manufacturers to specify fluoroelastomer and PPS hose layers that resist permeation and thermal cycling. Gates Corporation markets turbocharger oil-return hoses that retain structural integrity at 230 °C continuous exposure. OEM powertrain teams increasingly model oil-supply routing together with turbo placement to cut lag, and those layout changes ripple directly to fluid line architecture. Meanwhile, mild-hybrid belts add electric motor heat loads that share the same coolant loops, spurring wider use of electronic flow valves for precise energy allocation.

Smart Hoses With Embedded Fluid-Quality Sensors Enabling Predictive Maintenance

Eaton’s iHose platform embeds MEMS temperature, conductivity, and particulate sensors directly into coolant and oil lines, streaming data to the vehicle CAN network for condition-based maintenance alerts [3]“iHose Intelligent Fluid Systems,” Eaton Corporation, eaton.com. Fleet operators using telematics dashboards can schedule service before fluid degradation leads to pump cavitation or line fouling, maximizing asset uptime. Early adopters in heavy-duty trucking report single-digit percentage reductions in unscheduled roadside events, validating the economic case for smart hoses despite higher unit cost.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ICE Phase-Out Curbs Demand | –0.7% | Europe, select regions | Long term (≥ 4 years) |

| Volatile PA-12 Inflates Polymer Costs | –0.5% | Global | Medium term (2-4 years) |

| Low Replacement Limits Aftermarket Revenue | –0.4% | Mature markets | Short term (≤ 2 years) |

| Direct-Immersion Cooling Cuts Hoses | –0.3% | Premium EVs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ICE Phase-Out Targets Curbing Long-Term Demand for Fuel and Oil Transfer Lines

The European Union’s plan to ban new light-duty ICE registrations from 2035 sparks strategic portfolio shifts by hose and tube suppliers away from gasoline and diesel lines toward thermal loops and hydrogen conduits. While replacement demand will persist for legacy fleets well into the 2040s, capital budgets are already tilting toward coolant innovation and sensor integration to hedge the eventual volume decline.

Volatile PA-12 Supply Inflating High-Performance Polymer Costs

A handful of Asian and European producers concentrate most PA-12 output; any force majeure event, such as the fire at a key plant, drives price spikes that ripple through brake and fuel line BOMs. Suppliers hedge risk via multi-source contracts and accelerated testing of bio-based polyamides, yet tooling switchover slows broad material substitution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Coolant Systems Drive Thermal Innovation

Fuel transfer held the largest 27.04% share of the automotive fluid transfer system market in 2024, as gasoline and diesel platforms still dominated global assemblies. Coolant transfer systems, however, are set to post the quickest 3.86% CAGR through 2030, reflecting the central role of battery, power electronics, and cabin thermal management in electrified vehicles. Many OEMs now specify dual coolant loops, one glycol water circuit for the inverter–motor string and a separate dielectric branch for pack immersion, to manage higher voltage architectures. That complexity lifts average vehicle hose counts despite falling ICE production, sustaining volumes for tier-1 integrators that bundle molded hose paths, quick connectors, and bleed valves into pre-validated modules. Suppliers of additive-enhanced coolants also benefit; partnerships with hose makers expedite approvals for compatible elastomer blends.

Transmission, brake, and oil circuits remain sizeable but mature, with pump electrification as the main value-adding lever. Automatic transmissions on high-torque BEVs adopt electric oil pumps to enable lubrication when the traction motor is off, boosting opportunities for compact integrated pump-reservoir units. Brake fluid lines evolve modestly as brake-by-wire calipers proliferate; redundancy demands keep dual hydraulic circuits even in EVs, so hose count per vehicle stays flat. Lube oil circuits in range-extended hybrids decline in total footage but command higher temperature ratings. Across these system lines, suppliers that can cross-sell sensorized hoses and lightweight multilayer tubing defend margins against commoditized rubber offerings, anchoring their relevance in the automotive fluid transfer system market.

By Vehicle Type: Commercial Vehicles Accelerate Electrification

Passenger cars accounted for 62.15% of the automotive fluid transfer system market in 2024, underpinned by mass production of compact and mid-size models across China, India, and Europe. Yet medium and heavy commercial vehicles are forecast to register a 4.67% CAGR between 2025-2030, the fastest among all classes, as fleets electrify to meet total-cost-of-ownership and regulatory targets. Class 8 tractors adopting 800 V platforms need larger-bore dielectric coolant hoses to manage inverter and charger heat during megawatt depot sessions. Municipal buses integrate roof-mounted battery thermal circuits, adding vertical hose runs that require kink-resistant reinforcement schemes. Light commercial vans for e-commerce deliveries incorporate compact heat-pump modules connected to cabin and battery loops, enlarging under-floor coolant routing complexity.

For passenger vehicles, growth shifts to premium EV segments, where integrated heat pump systems and comfort features such as radiant floor heating raise the number of low-pressure coolant branches. In emerging economies, small ICE vehicles still rely on cost-optimized rubber hoses, preserving baseline volume. The confluence of differing duty cycles demands configurable fluid architectures, enabling modular hose kits that share tooling across vehicle types. This flexibility becomes a competitive differentiator for manufacturers in the automotive fluid transfer system market.

By Propulsion Type: BEV Growth Reshapes Thermal Requirements

Internal combustion engines still formed 84.13% of the automotive fluid transfer system market share in 2024, maintaining baseline demand for fuel, oil, and turbo coolant lines. However, battery electric vehicles will post a 6.49% CAGR to 2030, outpacing all other powertrains. Each BEV carries separate coolant loops, driving up hose volume per unit. Plug-in hybrids introduce the greatest complexity, blending traditional fuel systems with high-voltage cooling and cabin heat pump plumbing. Suppliers capable of delivering integrated multi-fluid bundles—combining coolant, refrigerant, and brake lines in single over-braided harnesses—secure multi-year sourcing awards.

Fuel-cell electric vehicles, though niche, add hydrogen circulation and humidifier water loops, presenting a novel line of business for polymer tubing specialists. Conversely, propane and natural-gas ICEs use similar fluid architectures to gasoline platforms, so incremental volume gains are limited. Overall, the propulsion shift reallocates wallet share within the automotive fluid transfer system market toward thermal solutions and away from combustible-fuel delivery. Still, total hose length per vehicle continues to rise, blunting the value decline.

By Component Type: Pumps Lead Active System Adoption

Hoses delivered 47.22% of the automotive fluid transfer system market share in 2024, reflecting their ubiquitous function across all circuits. Pumps are expected to clock a robust 5.04% CAGR to 2030 as OEMs switch from belt-driven to brushless DC units, enabling variable flow. Cooper Standard’s eCoFlow Switch Pump illustrates how integrated logic controls can redirect flow between circuits, cutting component count and parasitic load. Electronic valves, smart reservoirs, and sensor modules populate the “Others” bucket and record significant growth, underpinning a gradual shift toward intelligent fluid networks.

Connectors and clamps see moderate expansion driven by higher quick-coupler penetration on dielectric coolant lines. Tubing takes a share from hoses, wherever continuous-extrusion aluminum lines deliver lower permeation and ease of assembly. Adoption of cloud-connected crimping equipment, like Gates’ GC20 Cortex, enhances in-shop traceability for aftersales hose fabrication, unlocking value-added service revenue and cementing aftermarket share in the automotive fluid transfer system market.

By Distribution Channel: Aftermarket Complexity Drives Growth

OEM supply retained a 73.18% share of the automotive fluid transfer system market in 2024 because most hose assemblies and pumps are first installed at the vehicle plant. Yet the aftermarket is projected to expand at a 5.23% CAGR as fleets pursue predictive maintenance and EV owners keep vehicles longer. Specialized service centers invest in leak-detection scanners and fluid analyzers, allowing them to replace hoses pre-emptively based on data rather than failure. Continental’s decision to commercialize high-pressure fuel pump kits for independent garages illustrates OEM players’ intent to monetize aftermarket demand. Digital catalogs paired with VIN decoding accelerate right-part selection, reducing downtime for logistics fleets.

The aftermarket’s challenge lies in mastering diverse quick-connect standards and EV-specific coolants. Training programs certified by hose manufacturers will become essential for retaining warranty coverage, effectively tying service providers closer to original suppliers. Nevertheless, parallel import lines serving cost-sensitive regions intensify price competition, preserving buyer leverage.

Geography Analysis

Asia-Pacific’s 48.33% of the automotive fluid transfer system market share in 2024 stems from concentrated vehicle production centers in China, Japan, South Korea, and India, each supported by integrated rubber and polymer supply chains. Chinese battery manufacturing volume scales coolant hose demand rapidly, and provincial subsidies accelerate the adoption of locally sourced aluminum-nylon brake tubes. India’s ICE export push sustains robust fuel-line orders, while new electric two-wheeler factories specify compact glycol circuits that mirror passenger-car designs.

North America posts the quickest 4.12% CAGR as federal incentives under the Inflation Reduction Act spur EV assembly investments. Class 8 electric truck developers source large-bore dielectric hoses from Michigan and Ontario plants to meet content rules. Simultaneously, DEF infrastructure upgrades for diesel fleets create a replacement wave for heated urea delivery lines. Canada’s cold-weather validation programs led to thicker insulation on coolant lines, setting design precedents later adopted by European OEMs.

Europe holds a steady market presence but showcases cutting-edge fluid architectures. German luxury brands integrate heat-pump-based multi-loop modules supplied by French and Italian hose specialists. Scandinavian pilot fleets test hydrogen fuel-cell trucks, catalyzing demand for high-pressure composite hydrogen lines. Eastern Europe’s cost advantage lures pump production, which ships across the EU’s tariff-free zone. Brexit adds customs friction for UK-based hose exporters, nudging some OEMs to dual-source from continental suppliers. Collectively, these regional trends confirm that the automotive fluid transfer system market continues to cluster production near final-assembly sites, minimizing logistics cost and enabling just-in-time sequenced deliveries.

Competitive Landscape

The automotive fluid transfer system market remains moderately concentrated. Continental, Gates, and Cooper-Standard lead with global engineering footprints, while Hanon Systems and TI Fluid Systems offer specialized thermal solutions. Continental leverages in-house rubber compounding to supply molded hoses, quick connectors, and heated DEF lines to OEMs from Europe and the United States. Gates dominates aftermarket hose kits and expands OE presence through thermostat housings integrated with sensor pods. Cooper-Standard’s eCoFlow Switch Pump secured production release on pickup hybrids, solidifying its role as a system integrator.

Strategic activity centers on forward integration into sensing and controls. Eaton acquires a Czech sensor start-up to embed dielectric-constant probes into coolant reservoirs, enhancing predictive-maintenance features. TI Fluid Systems pilots an aluminum-polymer fused brake tube with BMW, betting on weight reduction to win premium EV contracts. Meanwhile, Chinese newcomers such as Jinfei Hose combine low-cost extrusion with local OEM relationships to capture share in domestic EV segments.

Materials innovation represents another battleground. Arkema’s bio-based PA-11 offers carbon-footprint cuts that European OEMs can count toward Scope 3 targets, prompting hose makers to evaluate rapid substitution. Laser-welded multilayer technology diffuses from premium models into high-volume platforms, pressuring traditional single-wall steel tube suppliers. Across all fronts, tier-1s race to offer complete fluid-handling modules that bundle hoses, pumps, manifolds, and control software, reducing OEM engineering overhead and locking in multi-year volumes within the automotive fluid transfer system market.

Automotive Fluid Transfer System Industry Leaders

Cooper-Standard Holdings Inc.

TI Automotive (TI Fluid Systems)

Continental AG (ContiTech)

Gates Corporation

Kongsberg Automotive

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Stellantis received a United States patent for an electrically powered auxiliary oil pump that enhances automatic-transmission fluid drain and refill processes, enabling full exchange without engine idling.

- September 2024: TI Automotive Aftermarket launched the BKS1002 in-tank fuel pump kit, its highest-flow unit to date, engineered for sensorless 6-step commutation or FOC drive profiles.

Global Automotive Fluid Transfer System Market Report Scope

| Fuel Transfer Systems |

| Oil Transfer Systems |

| Brake Fluid Systems |

| Transmission Fluid Systems |

| Coolant Transfer Systems |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (M&HCVs) |

| Buses and Coaches |

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Fuel-Cell Electric Vehicle (FCEV) |

| Hoses |

| Tubing |

| Connectors |

| Clamps |

| Reservoirs |

| Pumps |

| Others |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By System Type | Fuel Transfer Systems | |

| Oil Transfer Systems | ||

| Brake Fluid Systems | ||

| Transmission Fluid Systems | ||

| Coolant Transfer Systems | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Medium and Heavy Commercial Vehicles (M&HCVs) | ||

| Buses and Coaches | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Battery Electric Vehicle (BEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Fuel-Cell Electric Vehicle (FCEV) | ||

| By Component Type | Hoses | |

| Tubing | ||

| Connectors | ||

| Clamps | ||

| Reservoirs | ||

| Pumps | ||

| Others | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the automotive fluid transfer system market by 2030?

It is projected to reach USD 28.23 billion.

Which vehicle category grows fastest in fluid transfer demand through 2030?

Medium and heavy commercial vehicles, advancing at a 4.67% CAGR.

Why are coolant loops gaining share within fluid transfer systems?

Electrified powertrains need multi-loop thermal management for batteries, power electronics and cabins.

Which region records the quickest market growth?

North America, at a 4.12% CAGR between 2025-2030.

Page last updated on: