Automotive Air Suspension Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

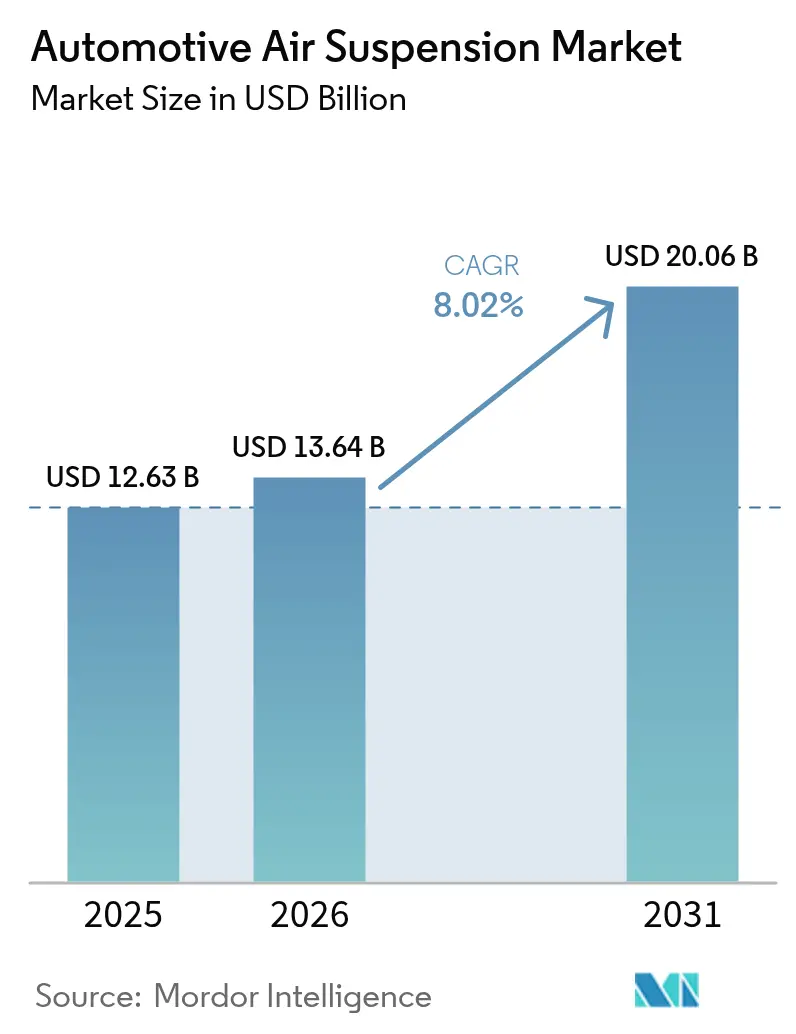

| Market Size (2026) | USD 13.64 Billion |

| Market Size (2031) | USD 20.06 Billion |

| Growth Rate (2026 - 2031) | 8.02% CAGR |

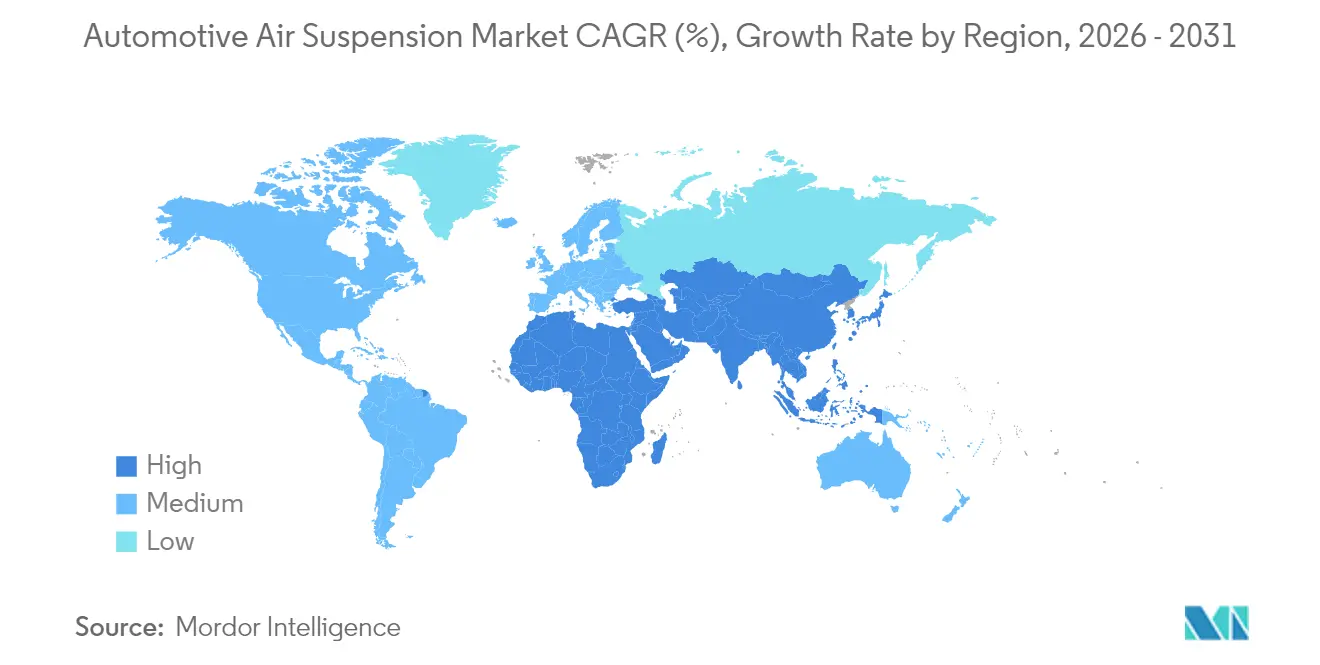

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Air Suspension Market Analysis by Mordor Intelligence

Automotive Air Suspension Systems Market size in 2026 is estimated at USD 13.64 billion, growing from 2025 value of USD 12.63 billion with 2031 projections showing USD 20.06 billion, growing at 8.02% CAGR over 2026-2031. Rising demand for premium ride quality, deeper integration with software-defined chassis, and the electrification of both passenger and commercial vehicles create a strong growth runway. OEM platform strategies increasingly position air suspension as a core enabler for adaptive dynamics, while tier-1 suppliers consolidate electronic control, damping, and sensing technologies into modular offerings. Passenger cars still anchor volume, yet electrified heavy trucks and SUVs are unlocking new value pools where optimized weight transfer and predictive height control translate directly into energy savings. Regional momentum remains strongest in Asia-Pacific, buoyed by Chinese luxury sales and Japanese innovation, whereas the Middle East and Africa are emerging as the fastest-growing arena on the back of infrastructure investment and premium vehicle uptake

Key Report Takeaways

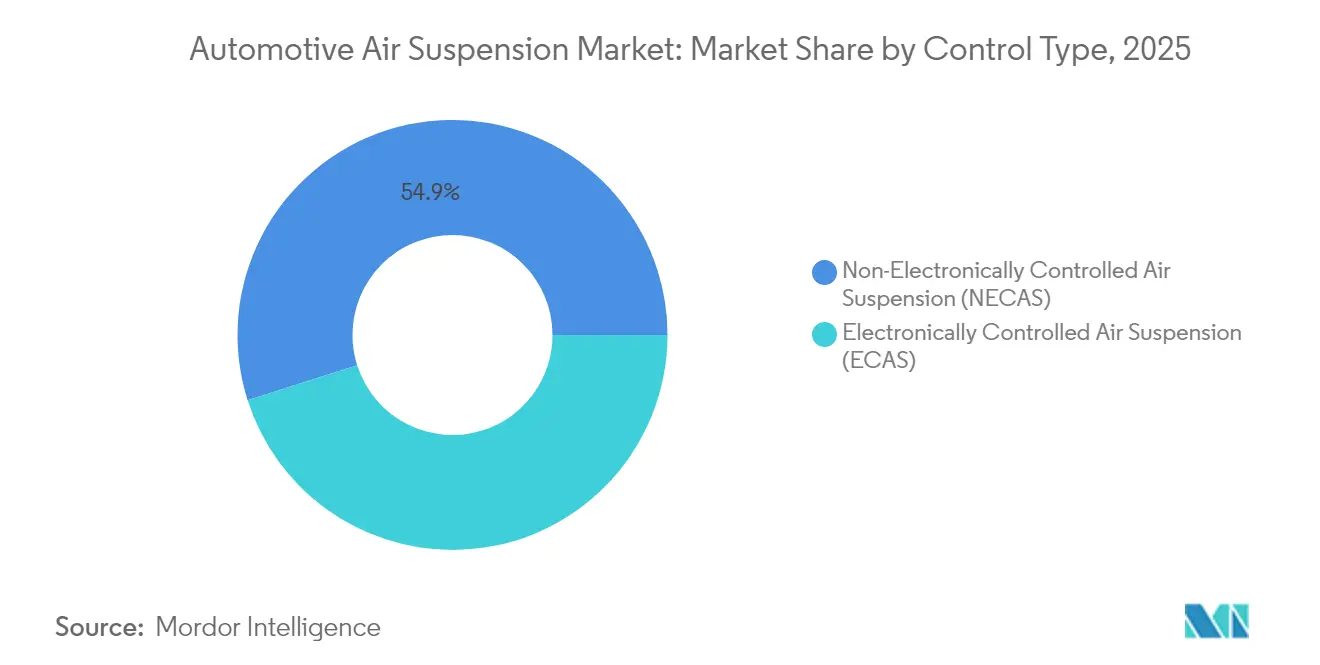

- By control type, non-electronically controlled air suspension maintained the largest 2025 share at 54.90%, while electronically controlled air suspension is projected to post the fastest 2026-2031 growth at 9.03% CAGR.

- By vehicle type, passenger cars led with 65.10% of 2025 installations; heavy trucks are expected to expand the quickest at an 7.94% CAGR through 2031.

- By end user, OEM fitment accounted for 73.60% of 2025 revenue, whereas the aftermarket is forecast to grow at a 7.38% CAGR over the outlook period.

- By component, air springs represented 33.95% of 2025 sales, but electronic control units are set to rise the fastest at a 9.96% CAGR.

- By propulsion, internal-combustion-engine vehicles dominated with an 84.60% 2025 share; battery-electric vehicles are on track for the highest growth at an 10.78% CAGR.

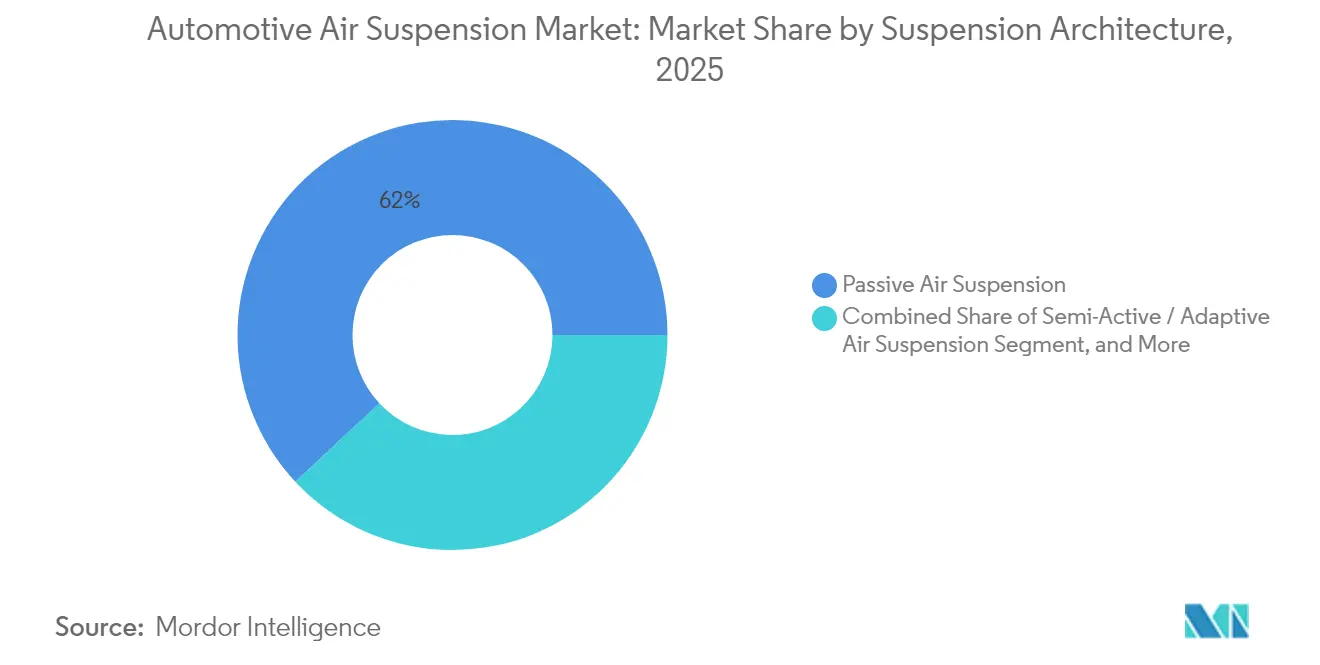

- By suspension architecture, passive air suspension captured 61.95% of 2025 demand, yet fully active air suspension is expected to advance at a 11.62% CAGR.

- By sales channel, direct-to-OEM deliveries formed 61.90% of 2025 volume, while tier-1 or module-supplier channels should grow at an 7.89% CAGR.

- By geography, Asia-Pacific held the largest regional share at 38.90% in 2025, and the Middle East and Africa is poised to be the fastest-growing region with a 6.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Air Suspension Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for ride quality and cabin comfort | +1.8% | Global, with premium focus in Europe and Asia-Pacific | Medium term (2-4 years) |

| Growing luxury and premium vehicle sales in Asia-Pacific and Europe | +1.5% | Asia-Pacific core, Europe secondary | Long term (≥ 4 years) |

| Integration of ECAS with ADAS and chassis domain controllers | +1.2% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Fleet fuel-saving benefits for electric heavy-duty trucks | +0.8% | Global commercial vehicle markets | Long term (≥ 4 years) |

| Predictive-maintenance digital twins lowering TCO for logistics fleets | +0.6% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Vibration-sensitive cargo regulations tightening | +0.4% | Europe and North America regulatory focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Ride Quality and Cabin Comfort

Premium comfort expectations are now evident even in mainstream segments, driven by consumer awareness and brand differentiation strategies. INFINITI’s 2025 QX80 illustrates this shift with an Electronic Air Suspension that adjusts dynamic height for easy ingress, off-road articulation, and towing stability[1]“2025 QX80 Debuts With Electronic Air Suspension,”, INFINITI Motor Company, infinitiusa.com. Asian buyers, supported by rising disposable incomes, are particularly responsive to features that marry convenience with perceived status. In battery-electric SUVs, integrating two-chamber air springs, such as Vibracoustic’s system for XPeng’s G9, allows simultaneous ride compliance and battery thermal management[2]"Two-Chamber Air Springs for Xpeng G9,", Vibracoustic, vibracoustic.com. Predictive algorithms using road-surface data further enhance comfort and handling; Land Rover’s latest Range Rover employs navigation-fed eHorizon information to pre-condition damper settings. Collectively, these advances reinforce air suspension as a tangible differentiator across global markets.

Growing Luxury and Premium Vehicle Sales in Asia-Pacific and Europe

China remains the epicenter of premium demand, with domestic and imported marques expanding electronic air suspension fitment to secure aspirational buyers. BMW achieved a 17.4% EV mix in 2024 global deliveries, underscoring how electrification often coincides with optional air suspension packages for cabin tranquility and aero-optimized stance control. Mercedes-Benz’s enlarged R&D footprint in Shanghai accelerates the localization of chassis technologies, including air suspension modules designed for local road conditions. Chinese premium EV startups, keen to undercut Western rivals, are bringing cost-controlled air systems to mid-tier price points, quickening regional adoption.

Integration of ECAS with ADAS and Chassis Domain Controllers

Vehicle dynamics are shifting from reactive damping toward predictive, software-defined control. ZF’s sMOTION active suspension deployed in the Porsche Panamera and Taycan adjusts damping force in real time while interfacing with vehicle motion sensors and road-preview data[2]. A 48 V electrical backbone supplies efficient power to valves and actuators, an architecture now proliferating across BMW’s next-generation platforms. Continental has reported more orders, of which a sizeable share reflects demand for integrated ECAS modules bundled with stability and steering electronics. The upshot is a chassis network where a single electronic control unit orchestrates ride height, roll mitigation, and hazard avoidance, amplifying the role of air suspension in overall safety perception.

Fleet Fuel-Saving Benefits for Electric Heavy-Duty Trucks

Electric truck operators analyze every kilowatt-hour consumed per mile. Stellantis’ STLA Frame platform, engineered for a 500-mile BEV range and 14,000-pound towing, integrates adaptive air suspension to trim aerodynamic drag at cruise height and level payload mass when stationary. When paired with predictive maintenance analytics, fleet operators can prolong component life, improving the total cost of ownership.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High system and integration cost for mid-segment vehicles | -1.1% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Reliability and maintenance complexity concerns | -0.7% | Commercial vehicle segments globally | Medium term (2-4 years) |

| Cyber-security risks in ECU-connected ECAS | -0.5% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Elastomer and composite price volatility | -0.3% | Global supply chain impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High System and Integration Cost for Mid-Segment Vehicles

The electronic air suspension bill of material can exceed conventional steel springs by several hundred USD, discouraging inclusion in cost-sensitive C-segment cars. Complex calibration work added ECU logic and reinforced chassis mounts, further inflating engineering spending. Emerging-market OEMs prioritize lower transaction prices over advanced chassis comfort, delaying penetration in mass segments. Nonetheless, localized sourcing in China and leaner component designs are narrowing the gap; XPeng’s decision to deploy Vibracoustic’s two-chamber springs while keeping the G9’s price competitive exemplifies cost-down innovation.

Reliability & Maintenance Complexity Concerns

Fleet managers accustomed to mechanical leaf or steel spring suspensions perceive air systems as downtime risks. Height sensors and compressors introduce new failure modes and require skilled technicians with diagnostic tooling. Limited service networks in developing regions exacerbate these fears, prompting some operators to stick with passive hardware. Suppliers are responding with reinforced membrane materials, corrosion-resistant fittings, and digital twin diagnostics. SAF-HOLLAND’s post-Haldex portfolio now bundles online monitoring services that proactively flag leaks and valve degradation, a move intended to reassure commercial buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Control Type: ECAS Drives Digital Integration

NECAS Solutions retained a 54.90% share of the air suspension systems market in 2025, mainly because fleet buyers value proven simplicity and lower acquisition costs. The segment remains prevalent in buses, trailers, and basic pickup models where static load leveling suffices. In contrast, ECAS is scaling fast at a 9.03% CAGR as OEMs migrate toward software-centric architectures. ECAS units harvest data from accelerometers, cameras, and map services to predict suspension settings, improving both comfort and handling on the fly. ECAS also supports variable ride height for EV aero optimization, making it indispensable for forthcoming premium crossovers.

Software-defined vehicles emphasize over-the-air calibration and feature unlocks, capabilities inherent to ECAS. ZF’s sMOTION and Continental’s E-Level families allow post-sale updates that fine-tune spring curves or add off-road modes. NECAS remains relevant in retrofit and cost-driven regions. Yet, its share is projected to decline as ECAS becomes standard on mid-size luxury sedans, performance SUVs, and electric delivery vans. The ongoing price erosion of valves and pressure sensors will accelerate the pivot toward ECAS across value segments.

By Vehicle Type: Commercial Electrification Accelerates Adoption

Passenger cars captured 65.10% of the air suspension systems market share in 2025 through luxury sedans and SUVs, where heightened comfort is a selling point. Medium and Heavy trucks, however, are on track for an 7.94% CAGR, the highest among all vehicle categories. Electrified drivelines amplify the value of air suspension by enabling automated load balancing and ride-height control that extend the range and protect battery packs. Light commercial vans and coaches adopt the technology for urban delivery efficiency and passenger comfort, respectively, although their growth profile lags medium and heavy trucks.

Air suspension technology in Class 8 electric tractors mitigates battery mass penalties by distributing axle loads while preserving legal weight limits. Passenger cars will keep leading in volume terms, yet commercial segments drive innovation cycles, influencing component durability and predictive maintenance capabilities that later cascade into retail models

By End User: Aftermarket Gains Momentum

OEM fitment accounted for 73.60% of the air suspension systems market share in 2025 revenue because of integration complexity and the need to align suspension tuning with crash safety and ADAS calibration. The aftermarket expands at 7.38% CAGR as vehicle parc ages and enthusiasts seek comfort or stance upgrades. Arnott Industries, now under MidOcean Partners, is aggressively expanding multi-brand replacement kits for European SUVs and American muscle cars, signaling consolidation intent within the retrofit domain.

Consumers turn to aftermarket kits when factory air springs reach end-of-life, often after eight years. Increased availability of plug-and-play ECAS replacement modules reduces installation time, broadening appeal. OEM channels remain indispensable for first-fitment, where warranty coverage, homologation, and integrated diagnostics are paramount. The aftermarket will capture incremental revenue from aging fleets, performance enthusiasts, and niche off-road communities seeking adjustable ground clearance.

By Component: ECU Leads Technology Evolution

Air springs formed the largest slice at 33.95% of the air suspension systems market share in 2025 revenues, reflecting their irreplaceable function in bearing vehicle load. Yet electronic control units represent the fastest-growing piece, advancing at 9.96% CAGR. ECUs orchestrate compressor output, valve timing, and sensor feedback, and they increasingly host machine-learning algorithms that anticipate road inputs. Compressors, reservoirs, and sensors scale broadly in line with the total system volume, while damper innovation focuses on integrating magnetorheological fluid chambers with air bladders for superior roll control.

Continental’s record order book demonstrates how OEMs purchase complete control stacks that unite air suspension with brake and steering logic. Air spring suppliers continue material breakthroughs, such as textile-reinforced bellows that withstand higher pressures while trimming unsprung weight. Meanwhile, ECU suppliers embed cybersecurity modules to guard against wireless updates, a response to growing concern over vehicle hacking exposure.

By Propulsion: BEV Integration Drives Innovation

Internal combustion platforms still represent 84.60% of revenue share in the air suspension systems market in 2025, yet BEVs outpace every propulsion group at an 10.78% CAGR. Electric SUVs and pickups, burdened by battery packs, leverage air suspension to maintain a consistent ride height regardless of state of charge or payload. XPeng’s G9 employs variable stiffness chambers that shift pressure to optimize thermal management and range, reflecting propulsion-linked design demands.

As BEV volumes scale, the scope for integrating chassis domain control with energy-management software elevates air suspension from optional comfort equipment to a strategic efficiency device.

By Suspension Architecture: Active Systems Gain Traction

Passive architectures accounted for 61.95% of the Air Suspension Market share in 2025. They are favored in trailers, vans, and entry-level luxury cars, where basic self-leveling suffices. Fully active systems, though expensive, are growing at 11.62% CAGR due to premium sedans and autonomous-ready robotaxis that demand ultra-flat ride profiles. Semi-active designs offer a midpoint, using solenoid-controlled valves to vary damping in milliseconds without the expense of full hydraulic actuators.

The Range Rover’s adaptive system bridges passive and active paradigms by reading road topography via GPS to prime dampers ahead of bumps. As the price delta narrows, semi-active setups will proliferate into mid-price crossovers, while fully active units become the flagship offering on executive EVs and Level 3 autonomous prototypes.

By Sales Channel: Tier-1 Integration Expands

Direct OEM procurement kept a 61.90% share in the air suspension systems market in 2025, aligned with traditional sourcing of safety-critical chassis parts. Tier-1 modular suppliers are expanding at 7.89% CAGR, capitalizing on OEM desire for turnkey chassis sub-frames that package air springs, dampers, sensors, and electronics. ZF’s creation of a unified Chassis Solutions Division typifies this push toward vertical integration, letting the supplier deliver harmonized hardware and software under a single part number.

Small component vendors face rising qualification costs for cybersecurity and functional safety compliance, nudging them toward partnering or acquisition by larger system integrators. SAF-HOLLAND’s addition of Haldex broadens its axle and suspension system scope, appealing to global truck makers looking for simplified supply chains

Geography Analysis

Asia-Pacific led the air suspension systems market with a 38.90% share in 2025. Chinese luxury and electric vehicle demand fuels most of the volume, while Japanese brands continue to refine comfort technologies. Mercedes-Benz's localized R&D and manufacturing footprints by global tier-1 suppliers shorten supply chains and adapt specifications for regional ride-comfort preferences. Government support for new energy vehicles also raises the ceiling for advanced chassis integration.

As infrastructure projects and affluent consumer bases converge, the Middle East and Africa will deliver the fastest CAGR at 6.94% through 2031. Premium SUVs and pickups dominate the mix, and buyers value height-adjustable suspensions for desert terrain versatility. Europe retains high penetration because stringent fleet CO₂ limits encourage lightweight air springs and height-based aero efficiency strategies. North America’s dynamics hinge on pickup and heavy-truck adoption. Stellantis and other Detroit-Three manufacturers are reorganizing body-on-frame platforms around air suspension modules to satisfy towing stability and BEV aerodynamics. South America remains emergent but shows rising uptake in Brazilian premium SUV assembly, aided by import-duty reductions on components that enhance fuel economy.

Regulatory Landscape

Automotive air suspension systems sit within broader vehicle safety and type-approval frameworks that cover chassis components, electronic controls, and commercial-vehicle build requirements. In the European Union, Regulation (EC) No 661/2009 (General Safety Regulation) is a key anchor for type-approval requirements relevant to vehicles and trailers, where suspension performance and system integration can affect safety outcomes. UNECE WP.29 construction and safety references, including consolidated vehicle construction resolutions and bus safety requirements such as UN Regulation No. 107, also shape harmonized expectations across many non-EU markets that follow UN regulations.

In the United States, compliance is governed through FMVSS (49 CFR Part 571) and related NHTSA processes, with market access also influenced by trade policy for auto parts. The Section 232 automobile and auto parts tariff program (25% duty on covered parts) added a material cost and compliance variable for imported subcomponents such as air springs, valves, sensors, and modules. The U.S. Department of Commerce opened an inclusions window from April 1 to April 14, 2026 for submissions tied to the Section 232 inclusions process, reinforcing the need for suppliers to actively manage classification, sourcing footprints, and duty-offset mechanisms.

Value Chain Analysis

The automotive air suspension value chain starts with upstream materials and subcomponents, including elastomers and reinforcements for bellows, aluminum and engineered plastics for housings, compressors, reservoirs, solenoid valves, height and pressure sensors, and electronic control units. These components are assembled by tier suppliers into air springs, struts, and integrated ECAS modules, which are then delivered by tier-1 and module suppliers as complete corner modules or axle and trailer systems to OEMs and trailer makers using just-in-time delivery models. Aftermarket specialists also supply replacement air springs and struts, along with retrofit kits, through parts distributors and installer networks.

Supply-side signals point to both localization and chain fragility. Audi nominated China-based KHAT as an air spring supplier for two all-electric SUV models following a September 2024 project kickoff, which highlights the growing qualification of Chinese manufacturers on premium EV platforms. At the same time, Stellantis halted Jeep Cherokee production at its Toluca Assembly Plant on March 14, 2026 due to a supplier dispute over suspension module deliveries, showing how tightly coupled module logistics and OEM assembly schedules have become. On the technology and footprint side, ZF started series production of its fifth-generation OptiRide ECAS for Hyundai in June 2025, reflecting continued migration toward consolidated smart pneumatic actuators. New commercial product entries, including VB-Airsuspension launching VB-FullAir 4C for Ford Transit Custom and Volkswagen Transporter (available from end-April 2026), indicate that commercial van platforms are pulling more complete air-suspension packages into broader distribution channels.

Competitive Landscape

The market shows moderate concentration. Continental, ZF Friedrichshafen, Hendrickson, and ThyssenKrupp Bilstein are the majors players of market, leveraging deep chassis portfolios and decades-long OEM programs. Competitive levers include control-software sophistication, sensor integration, and global production footprints that de-risk supply.

ZF consolidated its Active Safety and Chassis Technology teams, offering bundled steering, braking, and suspension solutions that help OEMs meet functional-safety norms while reducing component count. Continental is aggressively pursuing software-defined architectures that allow ride-profile updates over the air, meeting consumer appetite for post-purchase personalization. Hendrickson focuses on commercial-vehicle robustness, launching the PRIMAAX EX severe-duty line with low-pressure large-volume springs that suit e-trucks.

Private-equity interest is rising; MidOcean Partners’ purchase of Arnott Industries aims to unify fragmented aftermarket supply and expand electronically controlled retrofit kits. Meanwhile, Chinese disruptors such as XPeng integrate proprietary air systems into EVs to undercut established brands, signaling future price competition. Sustainability claims are also becoming differentiators; FORVIA committed to 30% CO₂ reduction across new air suspension innovations at AutoShanghai 2025, responding to OEM decarbonization mandates.

Automotive Air Suspension Industry Leaders

-

Continental AG

-

ZF Friedrichshafen AG

-

Hendrickson International

-

Thyssenkrupp Bilstein

-

Vibracoustic SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A whitespace is forming around localized, software-integrated pneumatic platforms for commercial vehicles, where OEMs and fleet operators are looking for modular air supply, processing, and electronically controlled air suspension functions. Announcements from May to June 2026 around the Bosch, Brakes India, and Wheels India 50:50 joint venture to engineer and manufacture advanced commercial vehicle air systems in India, including air suspension modules, point to suppliers building regional design and manufacturing capacity for trucks and buses with ECAS and related air-management content.

Capacity expansion and supplier qualification moves also support opportunities in trailer and heavy-duty applications, as well as in premium EV programs. Hendrickson Trailer disclosed a USD 13 million investment in June 2026 to increase trailer air suspension production capacity at its Somerset, Kentucky facility, suggesting incremental manufacturing scale for North American trailer suspension demand. On the premium EV side, Audi selecting KHAT for air spring supply on two all-electric SUV models in March 2026 reflects OEM willingness to diversify sourcing beyond traditional European incumbents, creating room for cost-competitive suppliers that can pass stringent validation. Across segments, the shift toward integrated ECAS modules that bundle sensors, valves, and ECU logic strengthens the case for tier-1 and module suppliers that can provide software-ready chassis components aligned with domain-controller architectures and over-the-air calibration requirements.

Recent Industry Developments

- June 2026: Hendrickson announced a USD 13 million investment to expand production capacity for trailer air suspension systems at its Somerset, Kentucky facility. The move supports higher output of trailer suspension hardware for dry van and refrigerated fleets and helps position Hendrickson for procurement cycles that prioritize uptime-focused suspension packages.

- June 2025: ZF began series production of its fifth-generation OptiRide electronically controlled air suspension (ECAS) for Hyundai Motor Company. The platform-level supply reinforces the shift toward consolidated smart pneumatic actuator designs that bundle valves and sensors, raising the integration bar for competing ECAS suppliers in commercial vehicles.

- July 2024: Continental introduced the Tough RuNR air spring line using a natural rubber and EPDM compound, targeting a reported reduction of more than 50% in the carbon footprint of air spring production. The product development highlights how material choices and sustainability claims are becoming competitive differentiators alongside ride and durability performance.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from automotive air suspension systems used to improve ride comfort, load leveling, and vehicle height control, across passenger and commercial vehicles, and across OEM fitment and aftermarket replacement.

Scope exclusions: The sizing excludes non-automotive air suspension use cases (such as industrial, rail, or trailer-only pneumatic systems that are not part of a road vehicle suspension).

Segmentation Overview

-

By Control Type

- Electronically Controlled Air Suspension (ECAS)

- Non-Electronically Controlled Air Suspension (NECAS)

-

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Trucks

- Buses & Coaches

-

By End User

- OEM

- Aftermarket

-

By Component

- Air Springs

- Compressors and Reservoirs

- Electronic Control Units

- Height & Pressure Sensors

- Shock Dampers

-

By Propulsion

- ICE Vehicles

- Battery-Electric Vehicles

-

By Suspension Architecture

- Passive Air Suspension

- Semi-Active / Adaptive Air Suspension

- Fully Active Air Suspension

-

By Sales Channel

- Direct to OEM

- Tier-1 / Module Supplier

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Nigeria

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the basic market boundaries, build the demand context, and make sure our assumptions matched publicly visible industry signals. We referenced sources such as vehicle production statistics from organizations like OICA, trade and tariff line data from platforms like UN Comtrade, road vehicle registration series published by transport agencies, and safety or technical standards references (where available) that signal fitment and compliance trends.

To keep the model realistic, we also reviewed public company filings, annual reports, and investor presentations to understand revenue mix cues, product positioning, and regional exposure for suspension related businesses. In a few places, we used paid subscriptions for company financials and intelligence, news and financials, and patent databases to cross-check technology direction and identify where new programs may shift adoption. These desk research sources are illustrative only, and other public references were also used to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary work was done through expert interviews and structured surveys with OEM-side engineering or purchasing contacts, component suppliers, distributors, and aftermarket participants, and then the feedback was compared against the desk signals. Since this is a global market, inputs were validated across APAC, EMEA, and the Americas so regional differences in fitment rates, premium vehicle mix, and replacement cycles could be reflected in the final assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 48% |

| Mid tier: 57% | Functional/Unit leaders: 28% | EMEA: 29% |

| Smaller Players: 15% | Managers: 57% | Americas: 23% |

Market-Sizing & Forecasting

Market sizing was built using a top-down and bottom-up logic. On the top-down side, we reconstructed the addressable demand pool by combining vehicle production and parc signals with air suspension fitment rates by vehicle type and propulsion, and then applied pricing bands that reflect control type and component content. Once the demand pool was built, results were corroborated with selective bottom-up checks using sampled supplier revenue cues, OEM program mix discussions, and a simple units times average selling price approach for key components, which are then used to tune totals when mismatches appear.

For this market, the premium passenger car share, air suspension penetration in new vehicles versus retrofits, and the compressor and air spring replacement cycles were key inputs. We also tracked the split between electronically controlled systems and non-electronic systems, plus regional mix shifts tied to SUV growth and electrification. Where a data gap existed for smaller countries or thin aftermarket reporting, we filled the missing piece using proxy ratios from similar vehicle parks and then tested the assumption during interviews so the final estimate stays grounded.

For forecasting, scenario analysis was used so adoption and pricing can move in a controlled way under different vehicle production and premiumization paths, and then it was smoothed using trend behavior from the historical series. Assumptions on penetration change, component content per system, and price progression were checked with experts, and we kept adjustments conservative when inputs were mixed.

Data Validation & Update Cycle

Validation was done in several passes so the totals do not rely on a single assumption. Model outputs were compared with independent signals such as regional vehicle output trends, expected adoption curves for premium platforms, and consistency checks between units and value outcomes, followed by analyst reviews where unusual jumps were questioned and recalculated.

If a large variance showed up between interview feedback and desk indicators, we re-contacted respondents to clarify what changed (for example, a platform launch delay, a pricing reset, or a supply constraint) before final sign-off. Reports are refreshed annually, and interim updates are made when material events occur. A final pre-delivery check is also completed so clients receive the most current view.

Mordor Intelligence's Automotive Air Suspension Market Estimate Compared With Other Published Estimates

Published market sizes for automotive air suspension often do not match, even when the topic name looks the same. Differences usually come from what gets counted as an air suspension system, the year used as the starting point, and whether value is built from a vehicle demand pool or from broader supplier revenue baskets.

The table shows a wide spread mainly because some sources anchor the market in earlier years with different price levels, and some also include adjacent pneumatic suspension categories that sit outside a road vehicle air suspension system definition. The table also points to timing, since one estimate is stated for 2024 and another for 2025, while in Mordor Intelligence's model the current-year value is stated for 2026 and aligned to OEM and aftermarket demand across passenger and commercial vehicles, before being extended to 2031 using the same scope rules.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.64 B (2026) | |

| Global Consultancy A | USD 10.01 B (2024) | Uses an earlier pricing environment and a different base year, and it also splits out OE, cabin, and electric and hybrid sub-markets, which can shift what is counted as automotive air suspension value in the total. |

| Industry Publisher B | USD 7.48 B (2025) | Bases the series on 2025 with a narrower reported market value, and differences in component coverage and how electronic versus non-electronic systems are priced can pull the headline number down versus a demand-pool build. |

Taken together, the spread is largely explained by timing and scope handling, rather than a single math error. By keeping the inputs tied to vehicle production, fitment, replacement patterns, and realistic pricing bands, the approach produces a transparent total that can be rechecked and repeated as new programs and prices evolve.

Key Questions Answered in the Report

How big is the Automotive Air Suspension Market?

The Automotive Air Suspension Market size is expected to reach USD 13.64 billion in 2026 and grow at a CAGR of greater than 8.02% to reach USD 20.06 billion by 2031.

Which region leads the air suspension systems market?

Asia-Pacific leads with 38.90% share in 2025, driven by Chinese luxury demand and Japanese technology leadership

How fast is electronically controlled air suspension growing?

Electronically controlled systems are expanding at a 9.03% CAGR, outpacing non-electronic setups due to deeper integration with ADAS and digital chassis platforms

Is the aftermarket for air suspension growing?

Yes, the aftermarket segment is expanding at a 7.38% CAGR as aging vehicles and performance enthusiasts drive demand for retrofit and replacement kits.

Why are air suspension systems important for electric trucks?

They improve energy efficiency by up to 3.5% through optimized load transfer and aerodynamic ride-height control, directly extending vehicle range.

Page last updated on: