Automotive Advanced DRAM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.77 Billion |

| Market Size (2031) | USD 2.84 Billion |

| Growth Rate (2026 - 2031) | 29.83% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Advanced DRAM Market Analysis by Mordor Intelligence

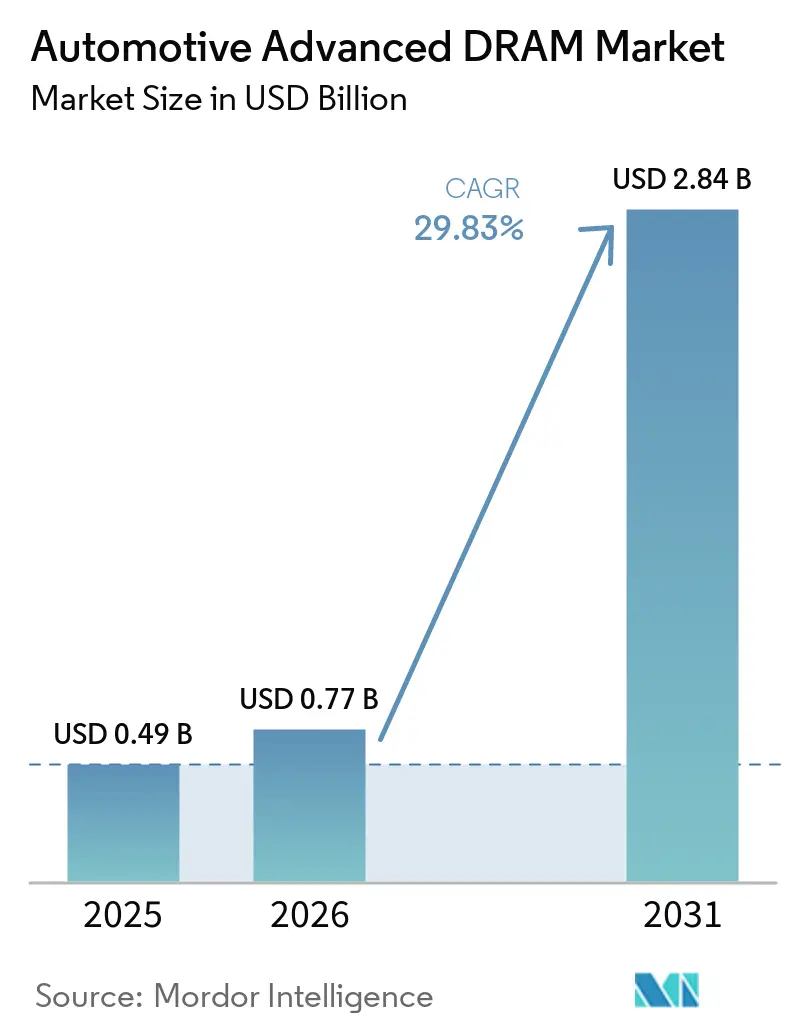

The automotive advanced DRAM market size is expected to grow from USD 0.49 billion in 2025 to USD 0.77 billion in 2026 and is forecast to reach USD 2.84 billion by 2031 at 29.83% CAGR over 2026-2031. A deeper redesign of vehicle electronics is shaping growth, as automakers move more sensing, computing, and user interface functions onto memory-hungry platforms inside the vehicle. Demand is rising because ADAS sensor-fusion workloads, centralized and zonal controllers, and AI-enabled cockpit systems all need more bandwidth and more persistent working memory than older automotive electronics stacks. The supplier base remains concentrated, with large memory manufacturers competing on process technology, safety certification, product breadth, and supply assurance, while smaller module specialists defend positions in long-life and high-reliability programs. The strongest near-term opportunities sit in software-defined vehicle programs, premium EV platforms, and cockpit and controller architectures that need LPDDR5 and LPDDR5X-class performance across both passenger and commercial vehicles. The main constraint remains supply security, because advanced-node wafer allocation, rising automotive DRAM prices, and the phaseout of older memory generations are forcing faster migration cycles than many vehicle programs originally planned.

Key Report Takeaways

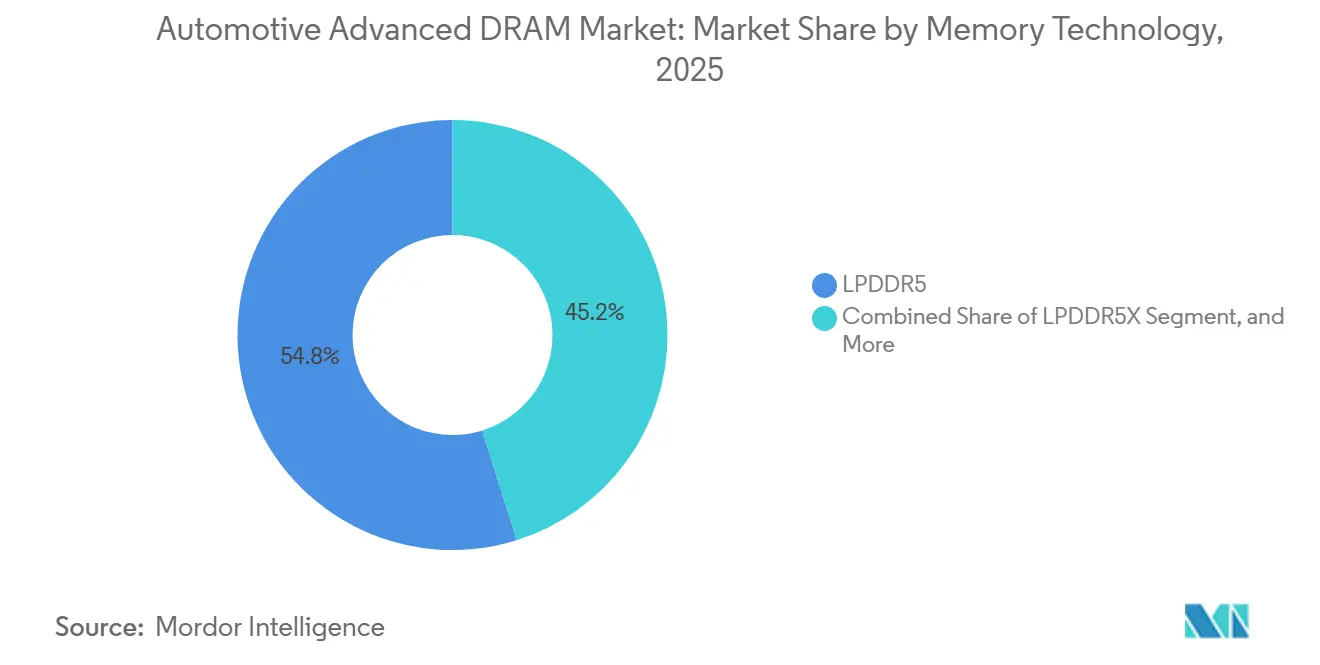

- By memory technology, LPDDR5 held 54.82% share of the automotive advanced DRAM market in 2025, while LPDDR5X is projected to grow at a 30.82% CAGR through 2031.

- By memory density, 32 GB accounted for 33.49% of market value in 2025, while 128 GB and above is projected to expand at a 31.03% CAGR through 2031.

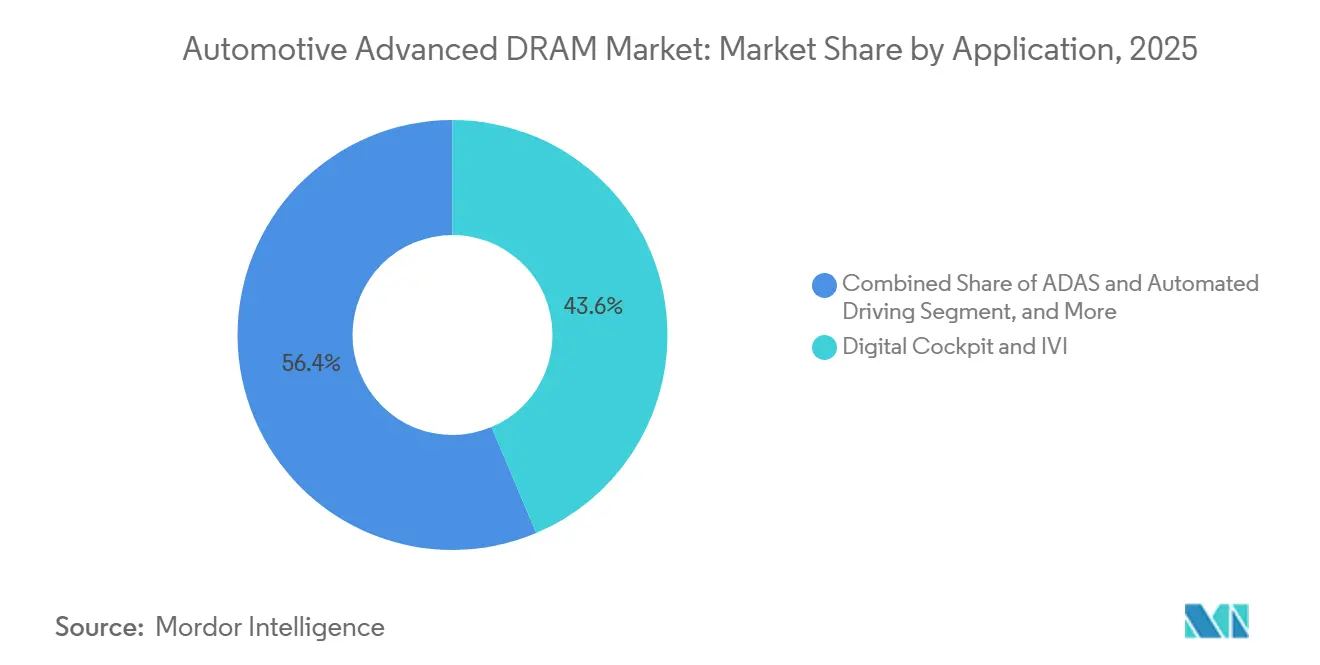

- By application, digital cockpit and IVI represented 43.63% of the market in 2025, while central compute, domain, and zonal controllers are projected to grow at a 30.67% CAGR through 2031.

- By vehicle type, passenger cars held 86.21% share in 2025, while commercial vehicles are projected to advance at a 30.23% CAGR through 2031.

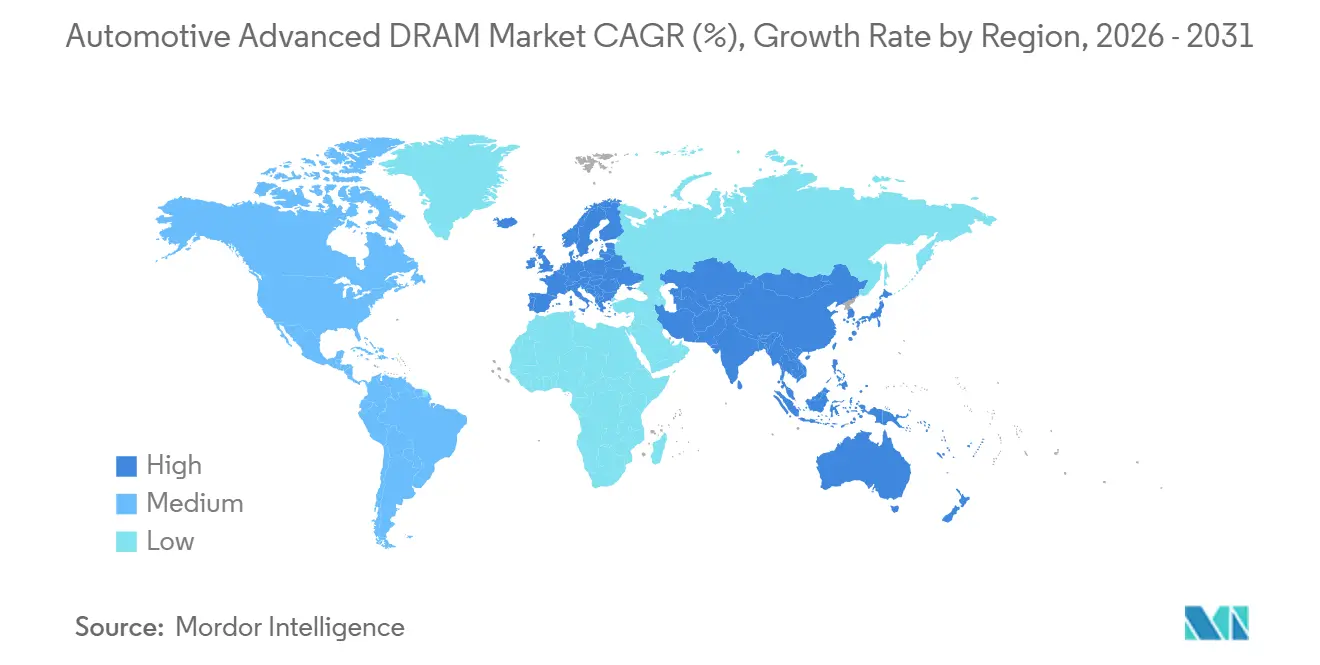

- By geography, Asia-Pacific held 56.89% of the automotive advanced dynamic random access memory (DRAM) market in 2025, while Europe is projected to expand at a 30.59% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Advanced DRAM Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADAS Sensor-Fusion Memory Intensity | +3.2% | Global, with concentrated gains in Asia-Pacific, North America, and Japan | Short term (≤ 2 years) |

| Centralized and Zonal Compute Migration | +2.8% | Global, particularly strong in North America, Europe, and China | Medium term (2-4 years) |

| Digital Cockpit and In-Cabin AI Expansion | +2.1% | Global, led by China, Europe, and North America premium segments | Short term (≤ 2 years) |

| EV Power-Budget Preference for Low-Power DRAM | +1.8% | Asia-Pacific, led by China, with spillover into Europe and North America | Medium term (2-4 years) |

| Functional-Safety-Certified LPDDR5 Adoption | +1.3% | Europe and North America, expanding into Asia-Pacific | Medium term (2-4 years) |

| SoC Memory-Bus Co-Design Around 256-Bit and 512-Bit Nodes | +0.9% | Global, concentrated in Taiwan, the United States, and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ADAS Sensor-Fusion Memory Intensity

ADAS workloads remain the sharpest near-term demand engine in the automotive advanced DRAM market, as camera, radar, and LiDAR systems generate continuous, high-speed data flows that must be stored and processed without delay. Micron stated in its automotive engineering research that Level 4 and higher autonomous systems can require DRAM bandwidth exceeding 1 TB/s, underscoring how quickly memory demand rises as vehicles add more sensing and inference layers.[1]Micron Technology, “New Research Shows Cars Need More Memory Than A Rocket,” Micron Technology, micron.com This also changes the design cycle, because memory channel count, bus width, and topology need to be fixed during SoC definition, well before the vehicle reaches production. JEDEC confirmed that LPDDR5X at 9,600 Mbps is already positioned for automotive use, while automotive certification for GDDR7 remained pending as of mid-2026. That sequencing matters because it ties present supplier commitments to the memory architecture of vehicles that will ship several years from now. In the automotive advanced dynamic random access memory (DRAM) market, this gives suppliers more leverage at the subsystem design stage than at the final procurement stage, since the architecture is largely set before production starts.

Centralized And Zonal Compute Migration

The automotive advanced DRAM market is also being pulled higher by the shift from many distributed control units to fewer centralized and zonal compute platforms. NXP introduced the S32K5 MCU family in March 2025 as the automotive sector's first 16 nm FinFET MCU with embedded MRAM for zonal SDV architectures, which shows how suppliers are already building around this system shift. The platform supports LPDDR5 and LPDDR5X interfaces, which directly widens the addressable demand base for advanced automotive memory in controller programs. As this architecture spreads, memory decisions move upward from many ECU programs to fewer Tier-1 and domain controller platforms, reducing the number of design touchpoints but increasing the value of each. It also raises DRAM content per computing unit because a single centralized controller replaces functions that were once spread across many smaller electronic modules. In the automotive advanced DRAM market, this means that one platform win now carries a larger, longer-term volume commitment than under older distributed procurement models.

Digital Cockpit And In-Cabin AI Expansion

The digital cockpit has become one of the heaviest memory users in the automotive advanced DRAM market as vehicles add more displays, driver monitoring, voice recognition, and richer software interfaces. These features require steady bandwidth and sufficient working memory to support graphical rendering, natural-language interaction, and feature updates throughout the vehicle's life cycle. That requirement is not limited to launch content, because OTA software rollouts create pressure to leave memory headroom for features that will arrive after the vehicle is sold. Micron estimated that 3 million new vehicles were equipped with cockpit domain controllers in 2025, and that number was expected to reach 16.5 million in 2026, which underlines how quickly this architecture is scaling into the mainstream. The shift from single-chip IVI units to multi-domain cockpit platforms is therefore increasing DRAM density and bandwidth requirements, even in vehicles not at the highest autonomy tier. In the automotive advanced DRAM market, cockpit programs now act as a near-term demand bridge between infotainment, AI features, and broader software-defined vehicle rollouts.

EV Power-Budget Preference For Low-Power DRAM

Battery-electric vehicles are adding another demand layer to the automotive advanced DRAM market, as every compute module must fit within tight thermal and power constraints. LPDDR5 and LPDDR5X are better suited to that environment than conventional DDR5 SDRAM because they are built for lower operating power and more granular energy-saving modes. Micron stated that its automotive LPDDR5X with Direct Link ECC Protocol delivered around 10% lower power consumption on a pJ/b basis, at least 6% more addressable memory space, and a 15%-25% bandwidth gain over inline-ECC approaches. That combination matters for EV platforms because more efficient memory can support advanced cockpit, ADAS, and centralized compute tasks without adding the same thermal burden. Samsung also positioned its 12 nm-class automotive LPDDR5X for safety-critical, centralized systems, underscoring how the product category aligns with the compute demands of modern EV architectures. The automotive advanced DRAM market is therefore benefiting from a practical design preference, where automakers increasingly choose low-power memory not just for efficiency, but also to enable higher in-vehicle compute within real operating limits.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HBM-Led Wafer Allocation Squeeze | -2.4% | Global, most acute in North America and Asia-Pacific | Short term (≤ 2 years) |

| Long Automotive Qualification Cycles | -1.7% | Global, with particular effect in Europe and North America | Medium term (2-4 years) |

| Thermal Derating in High-Density Edge Placements | -1.1% | Global, notable in Asia-Pacific and North America ADAS platforms | Medium term (2-4 years) |

| Limited Second-Source Options for ASIL-D LPDDR5 | -0.8% | Europe and North America, especially in compliance-driven programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

HBM-Led Wafer Allocation Squeeze

The strongest supply-side restraint on the automotive advanced DRAM market is the shift of advanced-node wafer capacity toward HBM for AI accelerators. S&P Global Automotive Insights stated in December 2025 that HBM production was already consuming around 23% of global DRAM wafer output, and that Samsung, Micron, and SK Hynix had moved more than 80% of advanced process capacity toward HBM. That leaves less room for automotive-grade DRAM, which has stricter temperature, traceability, and reliability requirements than consumer memory and cannot be easily replaced with standard parts. The same S&P Global source said automotive DRAM prices in 2026 were expected to rise by 70%-100% above 2025 contract levels, indicating how tight the supply position had become. This creates a deeper problem than pricing, because the decline of DDR4 and LPDDR4 availability after 2027 forces migration even for vehicle programs that were not ready to change platforms. In the automotive advanced DRAM market, supply security now matters almost as much as performance, since OEMs and Tier-1 suppliers must secure future-qualified memory while redesigning around newer generations.

Long Automotive Qualification Cycles

Long qualification timelines continue to slow the pace at which the automotive advanced DRAM market can absorb new memory generations. Automotive memory programs must align with stress testing, package reliability checks, controller tuning, ECC validation, and functional safety requirements that go far beyond mobile-grade certification. JEDEC published LPDDR6 in July 2025, yet the automotive path for that standard still points to a later design-in cycle because supplier, SoC, and Tier-1 validation work takes much longer in vehicle programs.[2]JEDEC Solid State Technology Association, “LPDDR, GDDR, And HBM For Auto AI Applications,” JEDEC, jedec.org The burden also falls on the full subsystem, since suppliers need to validate memory behavior alongside controller IP, PHY tuning, and safety methods, rather than certify the memory device alone. ISO work on the next edition of ISO 26262 is still under committee review, and that process is expected to deepen semiconductor-level safety expectations rather than relax them. As a result, the automotive advanced dynamic random access memory (DRAM) market cannot respond to stronger demand as quickly as the mobile or PC memory segments, because reliability and safety rules stretch every product migration cycle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Technology: LPDDR5 Leads, LPDDR5X Accelerates Fastest

LPDDR5 held 54.82% of the automotive advanced DRAM market share in 2025, supported by mature qualification coverage, a broader supply base, and close alignment with current ADAS and cockpit SoC programs. That lead reflected a practical balance between bandwidth, power efficiency, and proven automotive readiness across multiple vehicle platforms. LPDDR5X is projected to grow at a 30.82% CAGR from 2026 to 2031, making it the fastest-growing memory technology segment as centralized compute and AI-heavy cockpit programs move into production. Samsung stated that its 12 nm-class automotive LPDDR5X can deliver 307.2 GB/s on a 256-bit bus, which meets the throughput needs of controllers handling camera, radar, and AI workloads simultaneously. The automotive advanced DRAM market is therefore moving along a two-step path, with LPDDR5 maintaining the large installed base and LPDDR5X serving as the upgrade path for higher-bandwidth systems.

DDR5 SDRAM continues to fill a complementary role on vehicle platforms that need strong compute performance and can accommodate different thermal and power profiles. GDDR6 remains more specialized, with its strongest fit in graphics-intensive applications such as advanced HUD and augmented reality display systems, where rendering bandwidth matters more than low power. The others and emerging advanced DRAM category remain small in current production, but they are gaining strategic importance because JEDEC's LPDDR6 publication in 2025 provides the market with a clear post-LPDDR5X roadmap target. That matters for the automotive advanced DRAM market because 2028 and later vehicle design cycles will increasingly be shaped by decisions being made now around qualification timing and interface readiness. Smaller memory suppliers, including Taiwanese houses serving lower-density tiers, still have room where cost, continuity, and qualification depth matter more than peak bandwidth, but the center of gravity is clearly moving toward LPDDR5X-class platforms.

By Memory Density: 32 GB Anchors Current Platforms, High-Density Tiers Lead Future Growth

The 32 GB tier accounted for 33.49% of the automotive advanced DRAM market in 2025, underscoring its fit with current premium cockpit controllers and central compute platforms already in production. It offers enough headroom for today's multi-display, connectivity, and moderate ADAS tasks without forcing every platform into the highest-cost density class. The 128 GB and above tier is projected to expand at a 31.03% CAGR through 2031, making it the fastest-growing density band as automated driving stacks require larger pools of memory. That growth is closely tied to controller consolidation, because central compute systems combine tasks that were once handled by many separate modules. The automotive advanced DRAM market is therefore seeing density demand shift from platform adequacy toward future software headroom, especially in architectures meant to support richer sensing and AI inference over time.

The 16 GB and 24 GB tiers remain important in volume IVI and digital cluster applications where automakers prefer stable, standardized hardware baselines. The 64 GB and 96 GB tiers are gaining ground in L2+ and L3 programs, where additional memory is needed for more demanding ADAS and cockpit combinations without moving straight to the top-density class. Samsung noted that its 12 nm-class LPDDR5X is available in capacities from 3 GB to 24 GB per die, and that multi-die scaling can extend total system density without requiring a full SoC redesign. That modularity is important for the automotive advanced DRAM market because it lets suppliers match memory content to vehicle program requirements while preserving hardware reuse across several trims and compute packages. Qualification requirements linked to automotive operating temperature and long-life reliability also narrow the field of suppliers that can serve the highest-density tiers at production scale, supporting continued concentration at the upper end of the category.

By Application: Cockpit Dominates By Value, Compute Controllers Surge By Growth Rate

Digital cockpits and IVIs captured 43.63% of the automotive advanced DRAM market in 2025, making it the largest application segment by value across current vehicle programs. This leadership came from the widespread rollout of multi-display layouts, richer graphics, voice features, and connected software environments in both EV and internal combustion vehicles. Central compute, domain, and zonal controllers are projected to grow at a 30.67% CAGR through 2031, reflecting the shift toward fewer but far more capable in-vehicle compute units. Micron's automotive research on cockpit domain controller adoption shows how quickly advanced in-cabin and controller architectures are moving into mainstream production volumes. In the automotive advanced DRAM market, this mix means cockpit remains the volume anchor today, while centralized compute becomes the strongest growth channel for the next platform cycle.

ADAS and automated driving remain the second-largest application and carry disproportionate strategic weight because each added sensor and higher-resolution stream increases memory bandwidth and buffering requirements. Instrument cluster and HUD demand is more stable, though advanced windshield and augmented reality displays still create a selective pull toward higher graphics memory performance. Telematics and connectivity controllers are also moving toward LPDDR5-class memory as OTA update loads, connected services, and V2X software stacks become larger and more persistent. ISO 26262 and the broader use of reusable safety cases, such as SEooC, are helping suppliers shorten integration time for qualified memory across multiple vehicle programs. The automotive advanced DRAM industry is therefore being shaped by application convergence, in which cockpit, ADAS, connectivity, and centralized control increasingly draw on the same pool of higher-bandwidth memory technologies.

By Vehicle Type: Passenger Cars Anchor Volume, Commercial Vehicles Close The Gap

Passenger cars accounted for 86.21% of the automotive advanced DRAM market share in 2025, reflecting their volume lead and the concentration of advanced cockpit, ADAS, and EV programs in consumer vehicle platforms. This segment still sets the scale for supplier planning because most design wins, qualification cycles, and product ramps are tied to passenger vehicle programs. Commercial vehicles are projected to grow at a 30.23% CAGR from 2026 to 2031, making them the fastest-growing vehicle type as fleet automation, platooning software, and predictive maintenance systems gain traction. That growth also reflects the rising role of connected software in trucks and logistics fleets, where high-memory compute is increasingly used for route optimization, safety functions, and uptime management. In the automotive advanced DRAM market, commercial vehicles are moving from a niche to a more meaningful growth contributor, even though passenger cars still dominate current revenue.

High-end EV passenger platforms incorporated more than USD 150 in DRAM content per vehicle, while entry-level internal combustion platforms remained below USD 24, underscoring how sharply memory value rises with compute intensity. This matters because EV adoption lifts average memory content even without a matching increase in total vehicle volumes. It also explains why premium EVs remain the reference point for future memory roadmaps across the broader automotive advanced DRAM market. Commercial vehicle procurement follows a different logic, since fleet operators place far more weight on long service life, traceability, and replacement availability over a 10 to 15-year period. That creates space for module-level specialists to supply long-lifecycle LPDDR5 products with stable qualifications, even as large manufacturers dominate the highest-volume passenger vehicle programs.

Geography Analysis

Asia-Pacific held 56.89% of the automotive advanced DRAM market in 2025, making it the largest regional contributor by a wide margin. That position stems from a combination of strong EV production, deep regional electronics manufacturing, and the presence of the world's largest DRAM suppliers. China remained the main demand center inside the region, because local automakers continued to push ADAS, AI cockpit, and EV platform rollouts despite tighter memory supply and higher input costs. South Korea strengthened its role in January 2026 when SK Hynix completed ASIL-D certification for automotive LPDDR5X through TÜV SÜD, reinforcing the region's lead in functional safety readiness for next-generation memory.[3]SK Hynix, “SK Hynix LPDDR5X Earns ASIL-D, Top Automotive Safety Rating,” SK Hynix, news.skhynix.com Japan continued to shape qualification and integration cycles through its Tier-1 supplier base, while Taiwan remained important for advanced packaging and multi-chip module assembly tied to LPDDR5X-based automotive systems.

Europe is the fastest-growing regional segment, and the automotive advanced DRAM market size in the region is projected to expand at a 30.59% CAGR through 2031. Software-defined vehicle programs, premium vehicle architectures, and a strong focus on safety and compliance are pushing the region's demand profile. ISO 26262 remained central to memory qualification and system design, and ongoing committee work toward the next edition continued to signal tighter semiconductor-level safety expectations rather than a weaker rule base. That environment is encouraging German and French automakers to move faster on LPDDR5 and LPDDR5X transitions as older memory generations approach end-of-life. Europe is also more willing than many markets to lock in long-term supply agreements, which gives memory suppliers a steadier demand signal even when pricing remains volatile.

North America remained a key region in the automotive advanced DRAM market because U.S.-based EV, ADAS, and software-defined vehicle programs continue to set high baseline expectations for in-vehicle computing. Vehicle platforms in the region have helped normalize larger working-memory footprints for sensor fusion, cockpit software, and centralized controllers, thereby influencing design direction in other geographies. The rest of the world remained the smallest regional segment, but demand is gradually widening as connected vehicle features and EV portfolios spread into South America, the Middle East, Africa, and smaller Southeast Asian markets. South America is still early in the cycle, yet imported premium vehicles and early ADAS adoption are beginning to create a measurable pull for more advanced memory content than earlier vehicle generations required.

Competitive Landscape

The automotive advanced DRAM market remained moderately concentrated in 2025, with Samsung Electronics, Micron Technology, and SK Hynix collectively accounting for around 88% of supply. Competition among these suppliers centered on process node leadership, functional safety qualification, long-term supply assurance, and packaging efficiency rather than on price alone. Korea JoongAng Daily reported in May 2026, citing S&P Global Mobility data, that Samsung reached a 40% share of automotive memory supply in 2025 and moved ahead of Micron at 36%. That shift reflected stronger traction in the Chinese EV market and a wider product mix across LPDDR and UFS memory. In the automotive advanced DRAM market, leadership is therefore determined by a mix of bandwidth, safety readiness, product breadth, and the ability to support large automotive customers through tight supply cycles.

Micron has pushed a clear differentiation strategy around its automotive LPDDR5X with Direct Link ECC Protocol, which the company said offers a 15%-25% bandwidth gain, around 10% lower power use, and at least 6% more addressable memory space than inline-ECC approaches.[4]Micron Technology, “LPDDR5X With Enhanced ECC For Automotive Rises To The Challenge,” Micron Technology, micron.com That matters to Tier-1 suppliers because it supports performance gains while preserving compatibility and supply flexibility in multi-supplier designs. SK Hynix strengthened its position in January 2026 when its LPDDR5X received ASIL-D certification, which improved its standing in central compute and safety-sensitive controller programs. Samsung has also used packaging and process innovation to defend share, including its 12 nm-class automotive LPDDR5X and newer compact package formats for thermally constrained designs. These moves show that the top tier is competing on an integrated product strategy rather than on a single feature.

Below the large IDMs, ATP Electronics, Innodisk, SMART Modular Technologies, and similar specialists continue to serve parts of the market where long-term availability, traceability, and qualification depth outweigh raw performance. The realities of the automotive program support their position, as many vehicles require production support for 5 to 7 years and service support for another 10 to 15 years after that. This gives module suppliers room in edge applications and fleet programs that require stable, long-life LPDDR5 solutions rather than the newest bandwidth class. A potential future disruptor is CXMT, which announced LPDDR5X mass production at up to 10,667 Mbps in October 2025 and started customer sampling of its fastest variant, though broader automotive qualification remains the real threshold for competitive entry. The automotive advanced dynamic random access memory (DRAM) market, therefore, remains concentrated at the top, but still leaves selective openings for specialists and emerging regional suppliers where supply continuity and qualification strategy can matter as much as scale.

Automotive Advanced DRAM Industry Leaders

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

SK hynix Inc.

Nanya Technology Corporation

Winbond Electronics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Samsung Electronics overtook Micron Technology to become the world's largest supplier in the automotive memory semiconductor market, capturing a 40% share of global automotive memory in 2025, up from 35% the prior year. The gain was driven by Samsung's expansion in the Chinese EV market and its advanced LPDDR5X and UFS memory product portfolio, with customers including Qualcomm, Bosch, Tesla, and Denso.

- February 2026: SK Hynix began mass production of automotive-grade HBM3E 12-high stack memory delivering 1.15 TB/s bandwidth, targeting Level 4 AI controllers. This marked the first automotive-targeted HBM production ramp and signaled the beginning of a memory architecture bifurcation between LPDDR-class and HBM-class platforms at the highest autonomy tiers.

- January 2026: SK Hynix's automotive LPDDR5X received ASIL-D functional safety certification from TÜV SÜD, satisfying ISO 26262 requirements including SPFM ≥ 99%, LFM ≥ 90%, and PMHF ≤ 10 FIT. The product features on-die ECC, a dual-fuse defect response mechanism, and fault notification functions, positioning it as a primary high-reliability memory solution for next-generation ADAS and SDV platforms.

- January 2026: Micron Technology and General Motors signed a multi-year supply agreement to provide LPDDR5 DRAM and UFS 3.1 storage for GM's Ultifi platform, targeting a 50% reduction in software installation time and establishing a long-term memory supply baseline for GM's SDV architecture across its global model portfolio.

Global Automotive Advanced DRAM Market Report Scope

The Automotive Advanced DRAM Market refers to the global market for high-performance dynamic random-access memory (DRAM) solutions specifically designed and qualified for automotive applications. These memory technologies provide the high bandwidth, low latency, reliability, and thermal endurance required to support increasingly data-intensive vehicle functions, including advanced driver-assistance systems (ADAS), automated driving platforms, digital cockpits, infotainment systems, instrument clusters, telematics modules, and centralized vehicle computing architectures. Automotive advanced DRAM enables real-time processing of sensor data, artificial intelligence workloads, graphics rendering, connectivity functions, and software-defined vehicle operations while meeting stringent automotive safety and quality standards.

The Automotive Advanced DRAM Market Report is Segmented by Memory Technology (LPDDR5, LPDDR5X, DDR5 SDRAM, GDDR6, and Others/Emerging Advanced DRAM), Memory Density (16 GB, 24 GB, 32 GB, 64 GB, 96 GB, and 128 GB and above), Application (ADAS and Automated Driving, Digital Cockpit and IVI, Instrument Cluster and HUD, Telematics and Connectivity, and Central Compute, Domain and Zonal Controllers), Vehicle Type (Passenger Cars, and Commercial Vehicles), and Geography (North America, Europe, Asia-Pacific, Rest of the World). The Market Forecasts are Provided in Terms of Value (USD).

| LPDDR5 |

| LPDDR5X |

| DDR5 SDRAM |

| GDDR6 |

| Others / Emerging Advanced DRAM |

| 16 GB |

| 24 GB |

| 32 GB |

| 64 GB |

| 96 GB |

| 128 GB and above |

| ADAS and Automated Driving |

| Digital Cockpit and IVI |

| Instrument Cluster and HUD |

| Telematics and Connectivity |

| Central Compute, Domain and Zonal Controllers |

| Passenger Cars |

| Commercial Vehicles |

| North America | |

| Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Memory Technology | LPDDR5 | |

| LPDDR5X | ||

| DDR5 SDRAM | ||

| GDDR6 | ||

| Others / Emerging Advanced DRAM | ||

| By Memory Density | 16 GB | |

| 24 GB | ||

| 32 GB | ||

| 64 GB | ||

| 96 GB | ||

| 128 GB and above | ||

| By Application | ADAS and Automated Driving | |

| Digital Cockpit and IVI | ||

| Instrument Cluster and HUD | ||

| Telematics and Connectivity | ||

| Central Compute, Domain and Zonal Controllers | ||

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Geography | North America | |

| Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

How large is the automotive advanced DRAM market in 2026 and where is it headed by 2031?

The automotive advanced DRAM market was projected at USD 0.77 billion in 2026 and is forecast to reach USD 2.84 billion by 2031, growing at a 29.83% CAGR over 2026-2031.

Which memory technology leads current demand in vehicles?

LPDDR5 led in 2025 with 54.82% share because it balanced proven automotive qualification, bandwidth, and power efficiency across current ADAS and cockpit platforms.

Which product area is growing fastest in vehicle memory demand?

Central compute, domain, and zonal controllers are the fastest-growing application area, with a projected 30.67% CAGR through 2031 as automakers consolidate vehicle electronics into fewer high-compute platforms.

Why is LPDDR5X gaining momentum in automotive programs?

LPDDR5X is growing fastest at a 30.82% CAGR because newer cockpit, ADAS, and centralized compute programs need higher bandwidth, lower power use, and stronger safety-ready positioning.

Which region is the strongest today and which one is expanding fastest?

Asia-Pacific led with 56.89% share in 2025 due to its EV production scale and memory supply base, while Europe is the fastest-growing region at a 30.59% CAGR through 2031.

What is the biggest risk to supply over the next few years?

The main risk is tighter automotive DRAM availability as advanced-node wafer capacity shifts toward HBM for AI accelerators, while older automotive memory generations move toward phaseout.

Page last updated on: