Size and Share of Specialty Gases Market For DRAM Fabs

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

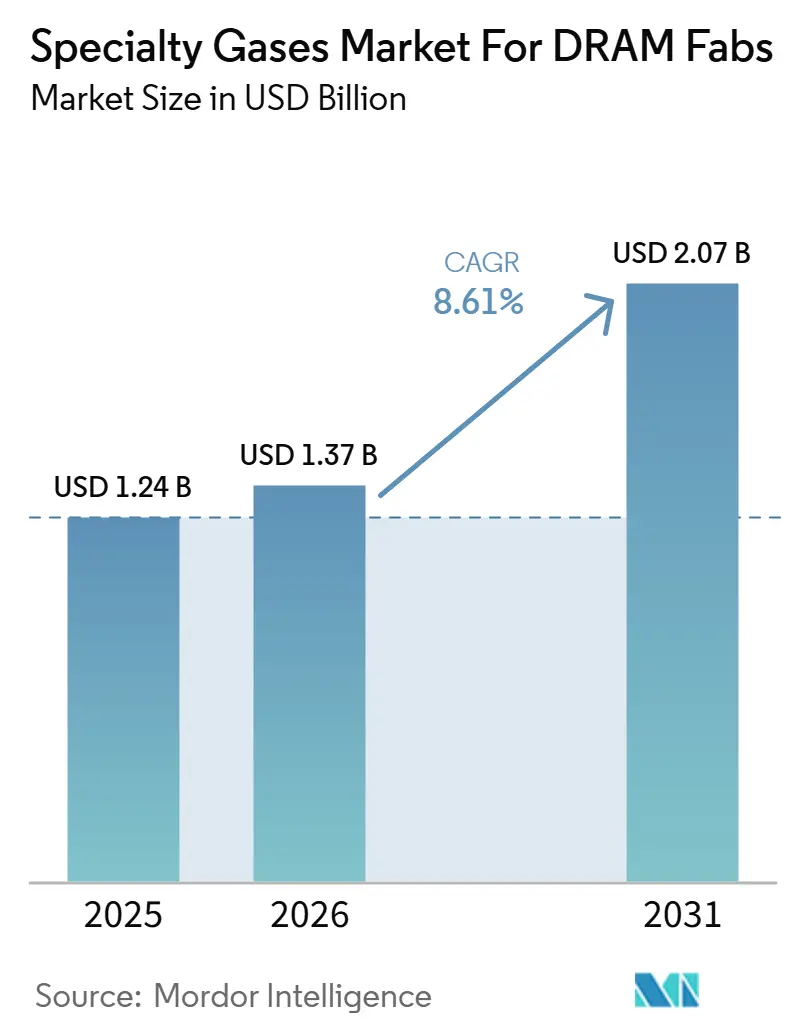

| Market Size (2026) | USD 1.37 Billion |

| Market Size (2031) | USD 2.07 Billion |

| Growth Rate (2026 - 2031) | 8.61% CAGR |

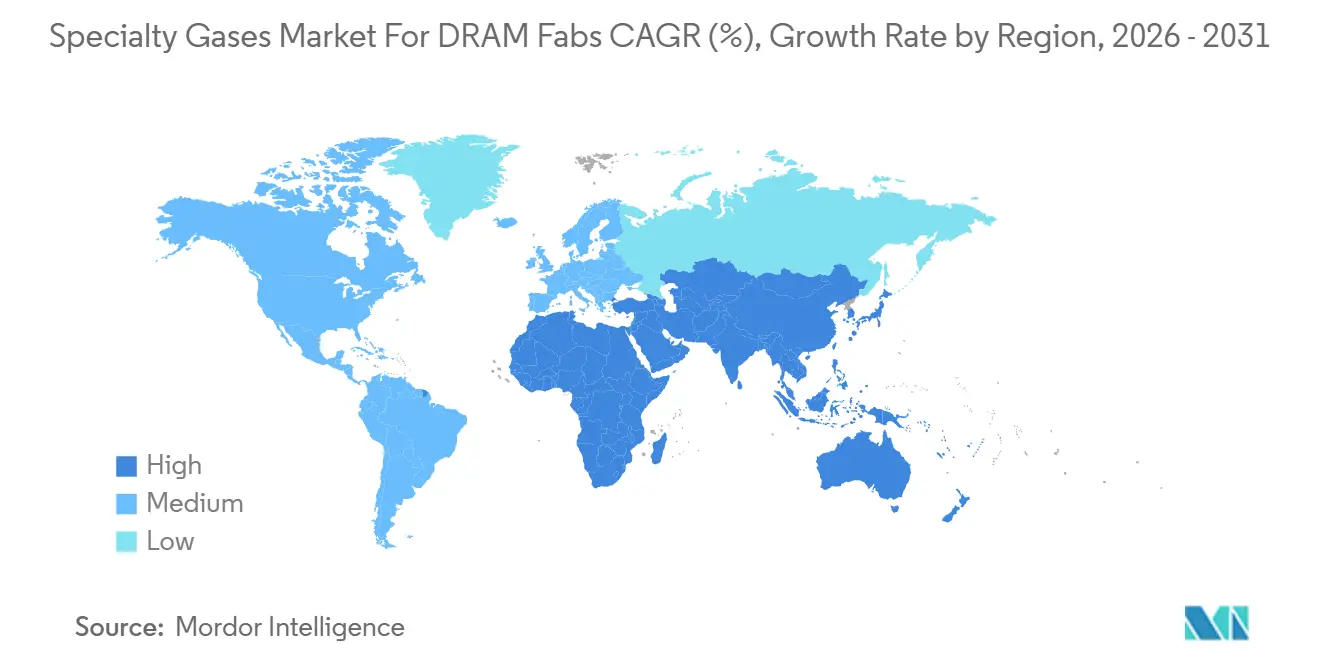

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

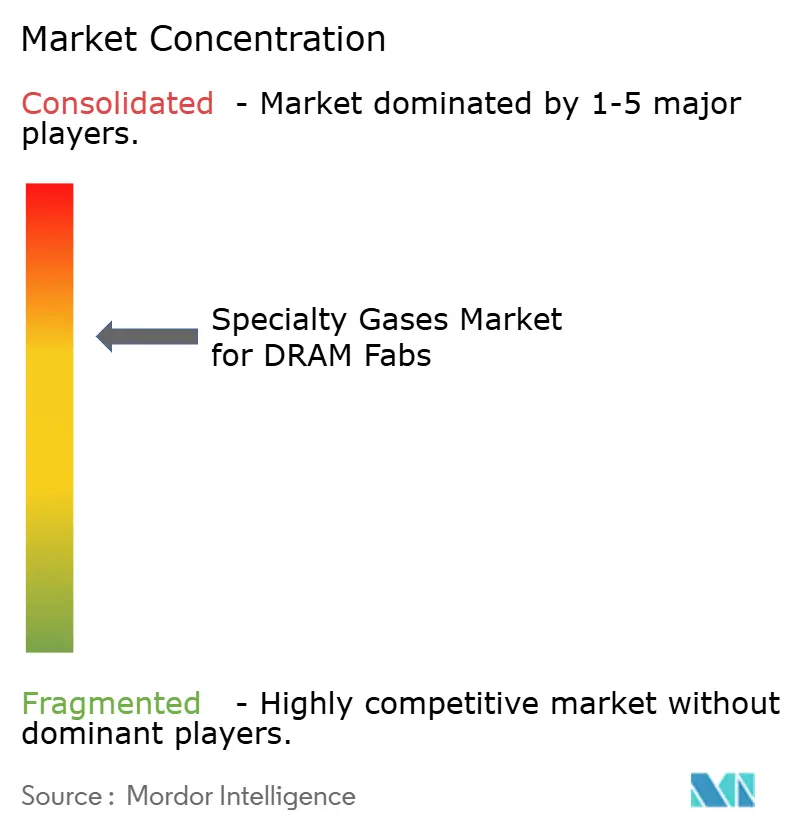

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Specialty Gases Market For DRAM Fabs by Mordor Intelligence

The Specialty Gases Market for DRAM Fabs was valued at USD 1.24 billion in 2025 and is estimated to grow from USD 1.37 billion in 2026 to USD 2.07 billion by 2031, at a CAGR of 8.61% during the forecast period (2026-2031). Growth in the sspecialty gases market for DRAM fabs industry is being shaped by the move to sub-10nm DRAM nodes, where each shrink adds more etch, cleaning, and deposition steps per wafer and increases gas use, even as wafer starts do not rise at the same pace. HBM production is adding a second layer of demand because taller stacks require repeated through-silicon via etch, barrier deposition, and fill steps that are not present in the same form in planar memory flows. These 2 shifts are happening together, so the specialty gases market for DRAM fabs are expanding across both process intensity and output growth rather than just wafer volume. Long-term on-site supply contracts still anchor competition, but recent supply disruptions in rare gases have pushed fabs to give more weight to sourcing resilience, regional redundancy, and qualification support than to price alone. That mix leaves the market with durable room for growth in fluorinated chemistries, advanced deposition precursors, ultra-high-purity delivery systems, and lower-GWP cleaning alternatives that can secure process-of-record status over time.

Key Report Takeaways

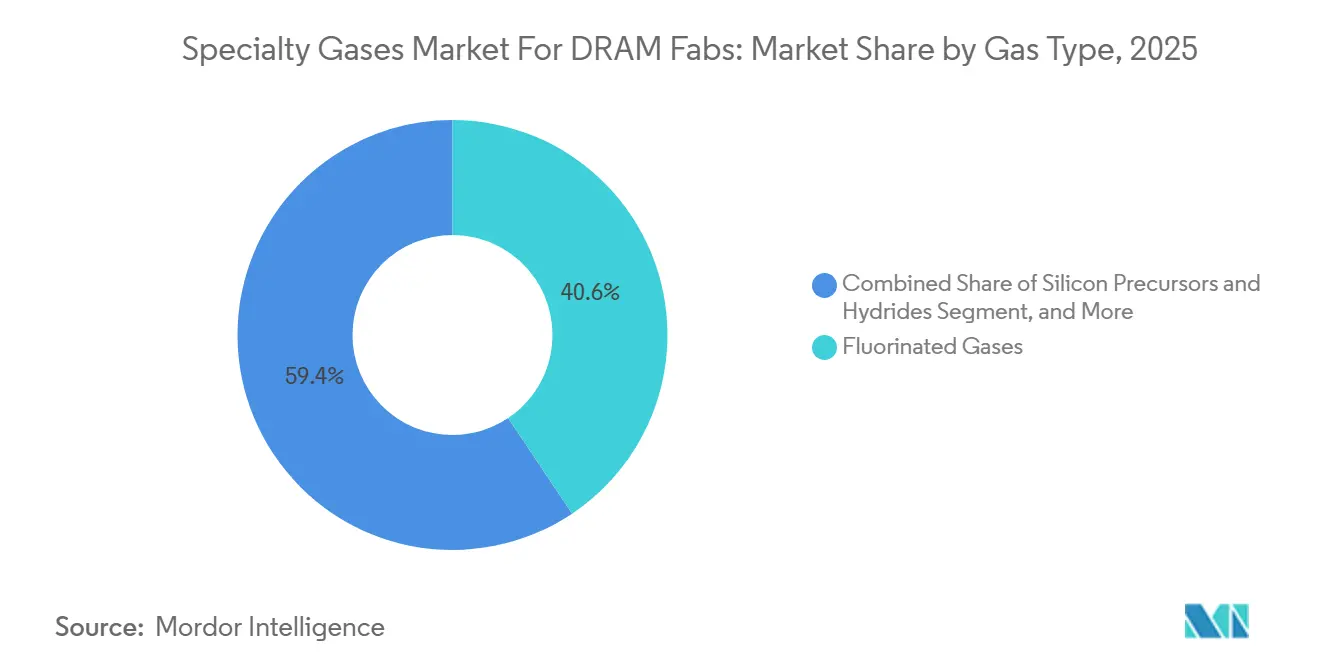

- By gas type, fluorinated gases led the specialty gases market for DRAM fabs industry with a 40.61% share in 2025, while silicon precursors and hydrides are projected to expand at a 9.38% CAGR through 2031.

- By process application, chamber cleaning accounted for a 37.94% share of the specialty gases market for DRAM fabs industry in 2025, while thin-film deposition is projected to grow at a 9.71% CAGR through 2031.

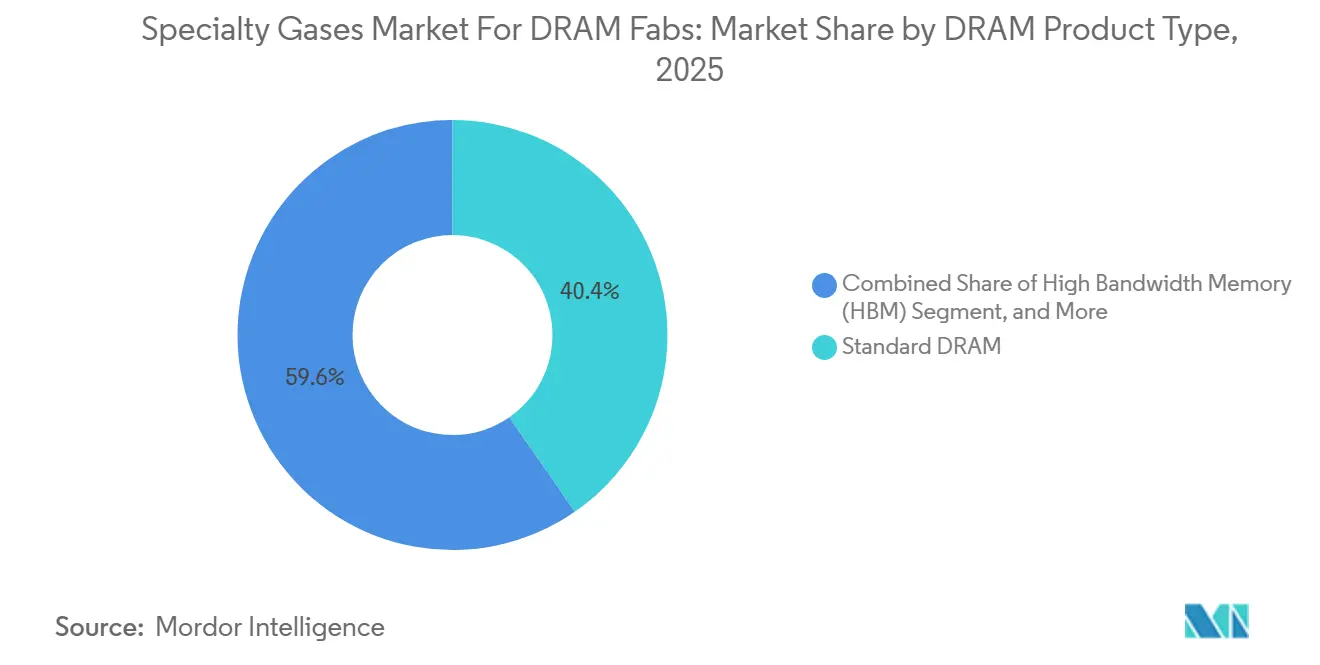

- By DRAM product type, standard DRAM held 40.37% share of the specialty gases market for DRAM fabs industry in 2025, while HBM is projected to expand at a 9.86% CAGR through 2031.

- By geography, Asia-Pacific held an 87.58% share in 2025, while North America is projected to grow at a CAGR at 9.38% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Specialty Gases Market For DRAM Fabs

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising DRAM Node Complexity and Multi-Patterning Intensity | +2.4% | Global, the highest concentration is in South Korea, Taiwan, and Japan | Short term (≤ 2 years) |

| HBM Stack Count Expansion Increasing Deposition and Etch Cycles | +1.9% | Global, concentrated in South Korea, Taiwan, and Japan | Short term (≤ 2 years) |

| Fab Capacity Additions in Asia-Pacific Memory Hubs | +1.5% | Asia-Pacific core, South Korea, Taiwan, Japan, China, spill-over to North America | Medium term (2-4 years) |

| Geopolitical Localization of Semiconductor Gas Supply Chains | +0.8% | Global, acutely in South Korea, Taiwan, North America, and Europe | Medium term (2-4 years) |

| Shift Toward Ultra-High-Purity In-Line Gas Delivery and Monitoring | +0.6% | Global, early gains in North America and Europe | Long term (≥ 4 years) |

| Increased Demand for Low-Defect Chamber Cleaning Chemistry | +0.4% | Global, concentrated in Asia-Pacific memory hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising DRAM Node Complexity and Multi-Patterning Intensity

The specialty gases market for DRAM fabs industry are gaining direct support from the move from 1z toward 1b and 1c process generations, because finer structures raise the number of deposition, spacer, pattern transfer, and clean steps needed to complete each wafer. In practical terms, fabs are using more fluorinated etch gases, more silicon-based materials, and more tightly controlled delivery conditions simply to preserve pattern fidelity as line dimensions narrow. That creates a structural rise in gas consumption per bit manufactured, which is more important than wafer output alone when advanced DRAM node migration is underway. Lam Research’s 2025 production adoption of EUV dry photoresist technology by a leading memory manufacturer also showed that step consolidation in one part of the flow can still introduce new gas-phase materials and new purity requirements in another part of the flow. The result is that specialty gases market for DRAM fabs industry continue to benefit even as the process roadmap changes its lithography mix, because the pressure to control pattern transfer, defect density, and film quality remains unchanged. This is why process escalation remains one of the strongest supports for demand growth across South Korean, Taiwanese, and Japanese DRAM fabs.

HBM Stack Count Expansion Increasing Deposition and Etch Cycles

The specialty gases market for DRAM fabs industry are also being boosted by HBM, where each additional die in the stack increases through-silicon via formation, more conformal barrier deposition, and more fill activity at the unit level. This matters because the HBM ramp is not only a volume story, it is also a process-density story, with more gas-intensive steps embedded into every finished package as stack heights rise. Taller stacks need deeper and cleaner etch performance, stronger process uniformity, and more repeatable ALD and CVD cycles, which raises the importance of stable fluorinated and deposition precursor supply. The HBM build-out is already feeding adjacent gas demand in packaging and testing as well, illustrated by Air Liquide’s June 2026 agreement to build and operate a nitrogen production unit for SK Hynix’s Cheongju P&T7 HBM site in South Korea. Because the specialty gases market for the DRAM fabs sector serve both wafer fabrication and the advanced memory ecosystem around it, HBM has become a demand multiplier rather than a narrow product niche. That is why suppliers are treating HBM-linked capacity, qualification, and localization decisions as core strategic priorities rather than as a side extension of standard DRAM demand.

Fab Capacity Additions in Asia-Pacific Memory Hubs

The specialty gases market for DRAM fabs remains closely linked to Asia-Pacific fab expansion, as the region still hosts almost all advanced DRAM manufacturing capacity and most of the highest-value HBM activity. Every major new 300mm cleanroom and every major packaging line expansion creates a durable pull for atmospheric gases, rare gases, and process-specific chemistries supported by long contract terms and embedded delivery systems. SK Hynix’s February 2026 decision to commit KRW 21.6 trillion (USD 15 billion) in additional investment to its first Yongin Semiconductor Cluster fab showed that memory producers still expect supply tightness and still see room for multi-year capacity additions.[1]SK hynix, “New Facility Investment for Yongin Semiconductor Cluster,” SK hynix Newsroom, skhynix.com Air Products reinforced the same direction in April 2026, when it announced multiple gas production facilities for Samsung’s next-generation fab in Pyeongtaek, underscoring how fab construction and on-site gas infrastructure continue to move together. As a result, specialty gases market for DRAM fabs industry continue to benefit from capacity additions protected by long asset lives and high switching barriers once installed. This keeps demand more durable than spot memory pricing would suggest, since the gas infrastructure decision is usually made for an operating horizon measured in years, not quarters.

Geopolitical Localization of Semiconductor Gas Supply Chains

The specialty gases market for DRAM fabs is being reshaped by localization, as gas procurement has moved beyond simple price and logistics decisions and has become part of fab risk management. Rare gas disruptions over the past 2 years made memory producers more willing to sign longer contracts, diversify source regions, and align supply with facilities that can demonstrate stable purification and delivery performance. That change favors suppliers that already have large balance sheets, multiple production bases, and the ability to place assets close to fab clusters. Air Liquide’s expansion in South Korea and Japan, together with Air Products’ large Pyeongtaek project, shows how leading suppliers are responding by building deeper regional positions rather than relying on a lean cross-border supply model. Linde’s continued expansion at Samsung’s Pyeongtaek complex points in the same direction, with embedded supply infrastructure serving as both a commercial moat and a resilience tool. In this setting, specialty gases market for DRAM fabs industry are becoming more region-specific in execution, even while remaining global in terms of technology and qualification standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tighter Fluorinated Gas Emissions Compliance Costs | -0.9% | Global, acute in Europe and North America, compliance influence extending to Asia-Pacific export-oriented fabs | Medium term (2-4 years) |

| High Qualification Burden for Memory Fab Gas Recipes | -0.7% | Global, concentrated in South Korea, Taiwan, and Japan | Long term (≥ 4 years) |

| Feedstock Concentration Risk for Rare Gases | -0.4% | Global, the highest structural exposure in South Korea, Taiwan, and Japan | Short term (≤ 2 years) |

| Long Procurement Cycles And Supplier Switching Inertia | -0.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tighter Fluorinated Gas Emissions Compliance Costs

Specialty gases market for DRAM fabs industry face clear cost constraints due to tighter controls on fluorinated greenhouse gases, because the same chemistries that remain central to etch and chamber cleaning also carry the greatest emissions burden. The European Union strengthened this direction under Regulation (EU) 2024/573, and the European Commission’s Implementing Regulation (EU) 2026/286 provided only a temporary semiconductor chiller exemption through 2029, rather than a permanent carve-out. That policy signal matters well beyond Europe because memory manufacturers often harmonize tool and chemistry decisions across global sites once a tighter standard begins to shape long-term cost and compliance planning. As DRAM etch depth increases and HBM layers rise, gas-intensive steps entail a larger abatement, reporting, and process-optimization burden, which raises the delivered cost of ownership even if physical demand remains firm. This does not stop the specialty gases market for DRAM fabs industry from growing, but it does narrow margin room for both fabs and suppliers and raises the commercial value of lower-GWP alternatives that can pass qualification. Over time, compliance costs will influence not only which gas is purchased, but also which supplier can support monitoring, traceability, and abatement integration at the fab level.

High Qualification Burden for Memory Fab Gas Recipes

The specialty gases market for DRAM fabs industry also remain constrained by the very long, exacting qualification cycle required for any gas, blend, or delivery change within an advanced memory fab. Qualification typically covers purity verification, analysis of metallic and non-metallic contamination, distribution stability checks, and wafer-level electrical validation before a supplier or chemistry can move into routine use. That process is slow by design because even trace contamination can damage yield, storage-node reliability, and line stability in advanced DRAM structures. The barrier is even higher when a new lower-GWP or lower-defect chemistry is proposed, because the fab must prove that environmental benefit does not come at the expense of throughput, particle control, or electrical performance. This means specialty gases market for DRAM fabs industry often reward incumbents that are already qualified, installed, and integrated with the fab’s delivery architecture. It also explains why supplier change in this market tends to occur during new fab build-outs, major node transitions, or tool introductions rather than through quick replacements within a stable, high-volume line.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Gas Type: Fluorinated Gases Remained the Core Process Chemistry

Fluorinated gases retained a 40.61% share of the specialty gases market for DRAM fabs industry in 2025, reflecting their central role in plasma etch and chamber cleaning across every major DRAM process flow. NF₃, CF₄, C₂F₆, CHF₃, and C₄F₈ remained difficult to displace because they support high-frequency steps that directly influence chamber condition, feature transfer, and throughput stability. That position is especially important in the specialty-gas market for DRAM fabs because cleaning and etch processes are repeated so often that even small process changes can alter total gas demand at the fab level. At the same time, competitive pressure is emerging, as IOP Science studies in 2026 showed that COF₂, including COF₂ with N₂O addition, can deliver promising silicon nitride chamber-cleaning performance with a much lower GWP profile than legacy options.

Silicon precursors and hydrides are the fastest-growing gas family in the specialty gases market for DRAM fabs industry at a 9.38% CAGR from 2026 to 2031, driven by the shift toward more conformal deposition in higher-aspect-ratio memory structures. As capacitor and barrier architectures become more demanding, fabs need tighter thickness control and cleaner surface behavior, which lifts the importance of ALD-oriented precursor chemistries and delivery stability. Noble and rare gases remain smaller in direct volume terms, but they carry outsize strategic importance because lithography support, etch stability, and purge performance can all be affected when sourcing becomes tight. Other gases such as N₂O, CO₂, and H₂ continue to serve oxidation, carrier, and conditioning roles that keep demand broad-based across the process flow even when they do not lead the mix by value. Within the specialty gases market for DRAM fabs industry, that creates a clear divide between suppliers that can support a broad chemistry basket and those that remain dependent on only 1 or 2 legacy product lines.

By Process Application: Thin-Film Deposition Is Expanding Fastest

Chamber cleaning accounted for 37.94% of specialty gases market for DRAM fabs industry in 2025, underscoring how heavily leading-edge DRAM fabs rely on frequent cleaning cycles to maintain deposition quality and control particle contamination. This application remained the largest because dense CVD and ALD tool fleets require repeatable in-situ and remote plasma cleaning to keep chambers productive and within specification. The specialty gases for the DRAM fabs market, therefore, continue to derive a large part of their baseline demand from tool uptime requirements rather than from end-product mix alone. Lam Research and STMicroelectronics also showed that optimized in-situ plasma chamber cleaning can reduce NF₃ use and carbon emissions by 32%, which matters because procurement, cost control, and emissions management are now being handled together rather than separately.[2]Lam Research, “Chamber Cleaning Optimizations Can Reduce Carbon Emissions By 32%,” Lam Research Newsroom, lamresearch.com That type of improvement does not remove demand, but it shifts value toward suppliers that can pair chemistry performance with tighter process efficiency.

Thin-film deposition is the fastest-growing application in the specialty gases market for DRAM fabs industry, with a 9.71% CAGR from 2026 to 2031, as advanced DRAM nodes use more conformal layers and more demanding dielectric and barrier schemes. Each move toward finer structures increases the need for controlled film growth in capacitor stacks, high-κ integration, and barrier formation, which in turn supports rising use of deposition precursors and associated carrier gases. Plasma etching remains another major gas-consuming category, since capacitor and bit-line features continue to push aspect ratios that depend on stable fluorinated gas mixtures and tightly managed process windows. Doping and ion implantation consume lower total volume, but the purity standard is severe and the value per unit of gas is high, especially for arsine, phosphine, and diborane applications. Accurate Gas Control Systems’ 2026 launch of its CryoSure platform also highlighted how delivery stability for diborane is becoming more important as advanced memory nodes demand tighter control of dopant behavior. Within the specialty gases market for DRAM fabs industry, the fastest gains are therefore moving toward suppliers that can support deposition complexity and not just bulk cleaning demand.

By DRAM Product Type: HBM Is Raising Gas Use Per Manufactured Unit

Standard DRAM retained a 40.37% share of the DRAM fab specialty gases market in 2025, supported by server and PC refresh demand tied to DDR5 adoption and continued volume manufacturing across leading producers. This segment still matters because it keeps baseline fab utilization high and sustains broad demand for etch, cleaning, and deposition gases across mature and advanced flows. In the specialty-gases-for-DRAM-fabs market, standard DRAM remains the volume anchor, even as newer product categories lead in growth intensity. Mobile DRAM also represents a meaningful demand layer, since LPDDR5 and LPDDR5X generations require tighter film and pattern control as smartphone platforms continue to push memory bandwidth. Graphics DRAM and server DRAM provide additional support through gaming, AI inference, and host memory requirements, keeping a large installed base of conventional DRAM production active.

HBM is the fastest-growing product type in the specialty gases market for DRAM fabs industry, with a 9.86% CAGR from 2026 to 2031, and that growth is driven by a much higher gas content per finished unit than in standard planar DRAM. The reason is straightforward: each extra die in a stacked package adds TSV etch, barrier deposition, and tungsten fill steps that directly increase the use of fluorinated gases and deposition precursors. That makes product mix an independent growth lever, because even a modest shift toward HBM changes gas demand intensity without needing the same jump in wafer starts. Mobile DRAM and server DRAM will continue to matter, but they do not carry the same structural step-count premium that HBM does. Within the specialty gases market for DRAM fabs industry, this is why suppliers are focusing so much attention on HBM-linked qualifications, co-location, and packaging-adjacent infrastructure, since the value created per unit of memory output is materially higher when the stack architecture becomes more complex.

Geography Analysis

Asia-Pacific commanded 87.58% of the specialty gases market size for DRAM fabs industry in 2025, reflecting the region’s overwhelming concentration of advanced DRAM manufacturing and the clustering of gas production assets around those fabs. South Korea remained the single most important national center within the sspecialty gases market for DRAM fabs industry, with Samsung’s Pyeongtaek complex and SK Hynix’s established and planned sites continuing to anchor long-term gas infrastructure commitments. Air Products’ April 2026 selection to build, own, and operate multiple gas production facilities at Samsung’s new advanced semiconductor fab in Pyeongtaek showed how deeply the supply base is being embedded into Korean memory expansion plans. SK Hynix’s February 2026 Yongin investment decision reinforced the same demand direction, as major fab projects of this scale lock in gas demand for many years once tool installation and qualification progress. Taiwan also strengthened its role in the specialty gases market for DRAM fabs industry through memory and materials activity, supported by Air Liquide’s March 2026 inauguration of its first large-scale advanced materials plant in Taichung for deposition and etching products.

Japan remained critical to the specialty gases market for DRAM fabs industry through upstream supply strength rather than sheer DRAM wafer volume, particularly in ultra-pure atmospheric gases, etching chemistries, and precursor support. Air Liquide’s April 2026 commitment of EUR 200 million (USD 226 million) for 2 ultra-pure gas production units in Hiroshima showed that Japan continues to attract long-horizon investment where advanced chip output requires extremely reliable gas supply.[3]Air Liquide, “Air Liquide Inaugurates Its First Advanced Materials Manufacturing Plant In Taiwan,” Air Liquide, airliquide.com China is becoming a more important demand center in the specialty gases market for DRAM fabs industry as local memory activity scales and domestic suppliers try to qualify more process gases for advanced use, a direction reflected in CXMT’s 2026 IPO prospectus and broader memory build-out plans. The rest of Asia-Pacific remains smaller in DRAM wafer fabrication, but it is becoming more relevant through advanced packaging support and regional supply-chain integration.

North America is the fastest-growing geography in the specialty gases market for DRAM fabs industry at a 9.38% CAGR from 2026 to 2031, because onshore semiconductor investment is creating new demand for local gas infrastructure, delivery systems, and specialty materials support. Entegris’ August 2025 plan for USD 700 million in domestic R&D and capital investment, together with its December 2024 CHIPS Act award agreement, showed how the U.S. supply base is expanding around advanced semiconductor materials and purity solutions. Europe and the rest of the world held a much smaller direct share of the specialty gases market for DRAM fabs industry because they do not host the same scale of volume DRAM fabrication. Even so, Europe still influences chemistry decisions globally, since its F-gas rules are pushing fabs and suppliers to prepare for stricter long-term emissions compliance.

Competitive Landscape

The specialty gases market for DRAM fabs industry shows moderate-to-high concentration in bulk and process gas supply, with Linde plc, Air Liquide S.A., and Air Products and Chemicals, Inc. holding the strongest positions through long-term on-site agreements with leading memory fabs. Linde’s April 2025 agreement to build an eighth air separation unit for Samsung’s Pyeongtaek site illustrated how incumbent suppliers deepen their position by expanding inside existing customer campuses rather than competing only for new accounts. Air Liquide strengthened its Korean footprint in 2026 through the DIG Airgas acquisition and then linked that broader position to a new long-term nitrogen supply agreement for SK Hynix’s Cheongju P&T7 HBM packaging site. Air Products also secured a major role in Samsung’s next-generation Pyeongtaek expansion, showing that the top tier of the specialty gases market for DRAM fabs industry still competes most effectively through scale, capital intensity, and installed infrastructure. These moves keep switching barriers high because once the supply network is built into a fab, replacement is costly, slow, and operationally risky.

Below that top layer, the specialty gases market for DRAM fabs industry remain open to Asian specialists that compete in fluorinated and silicon-based chemistries where process-level expertise matters more than sheer atmospheric gas scale. The most important opening point is low-GWP substitution, since qualification of COF₂ and F₂/N₂-style alternatives can gradually shift value away from legacy NF₃-centered supply lines if performance and defect control prove durable in volume production. Entegris sits in a separate high-value position through ion implant gases, ALD precursors, and ultra-high-purity delivery systems, and its USD 700 million U.S. investment plan showed that delivery architecture is becoming as important as the chemistry itself.[4]Entegris, “Entegris Announces Plans For USD 700 Million Investment In The United States, Technology Center In Illinois,” Business Wire, businesswire.com Chinese suppliers are also trying to gain ground in the specialty gases market for DRAM fabs industry by aligning local gas capability with the expansion of domestic memory manufacturing and qualification programs.

Competitive standards are strict across the specialty gases market for DRAM fabs industry, with certified purity, sub-ppb impurity reporting, and stable point-of-use performance serving as baseline requirements rather than differentiation points. That is why the next layer of advantage is increasingly coming from monitoring, delivery control, and co-development support rather than from commodity gas supply alone. Air Liquide’s March 2026 Taichung advanced materials plant captured that direction clearly, because it moved the company deeper into deposition and etching materials manufacturing near the customer base instead of limiting its role to bulk gas provision. As a result, the specialty gases market for DRAM fabs industry is likely to stay led by a few global majors in core supply, while narrower share shifts emerge in advanced chemistries, low-GWP cleaning, and ultra-high-purity delivery platforms.

Leaders of Specialty Gases Market For DRAM Fabs

Linde plc

Air Liquide S.A.

Air Products and Chemicals, Inc.

SK Materials Co., Ltd.

Nippon Sanso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Air Liquide signed a long-term contract with SK Hynix to build and operate a nitrogen production unit at the Cheongju P&T7 packaging and testing fab, investing EUR 200 million (USD 232 million). The facility will supply high-purity gases for advanced HBM chip packaging, with commissioning targeted for late 2027. This agreement leveraged Air Liquide's USD 3.3 billion acquisition of DIG Airgas, completed earlier in 2026.

- April 2026: Air Products and Chemicals was selected by Samsung Electronics to build, own, and operate multiple state-of-the-art gas production facilities at Samsung's new advanced semiconductor fab in Pyeongtaek, South Korea, supplying nitrogen, oxygen, argon, and hydrogen. Air Products characterized this as its largest investment in the semiconductor industry to date, with facilities expected onstream in multiple phases from 2028 through 2030.

- April 2026: Air Liquide committed EUR 200 million (USD 226 million) to build and operate 2 new industrial gas production units in Hiroshima, Japan, supplying ultra-pure nitrogen, oxygen, and argon for a global leading semiconductor manufacturer's advanced chip production. Operations are targeted to begin by end-2028.

- March 2026: Air Liquide inaugurated its first large-scale Advanced Materials manufacturing plant in Taichung City, Taiwan, producing deposition and etching materials for next-generation semiconductor fabs. The facility marks Air Liquide's transition from gas supply to advanced specialty chemistry manufacturing in Taiwan, where the company already operates 54 semiconductor-dedicated facilities.

Scope of Report on Specialty Gases Market For DRAM Fabs

Specialty gases for DRAM fabs industryare high-purity gases used in dynamic random-access memory (DRAM) fabrication facilities to support critical semiconductor manufacturing processes, including deposition, etching, cleaning, doping, and chamber conditioning. The scope includes gases used across DRAM wafer fabrication steps, such as nitrogen, argon, helium, hydrogen, ammonia, silane, tungsten hexafluoride, nitrous oxide, nitrogen trifluoride, fluorinated gases, and other electronic-grade specialty gases supplied to fabs for process, purge, carrier, and cleaning applications.

The Specialty Gases Market for DRAM Fabs Industry Report is Segmented by Gas Family (Fluorinated Gases, Silicon Precursors and Hydrides, Noble / Rare Gases, and Other Process Gases), Process Application (Chamber Cleaning, Plasma Etching / Reactive Ion Etching (RIE), Thin-Film Deposition (CVD / ALD / Epitaxy), Doping / Ion Implantation, and Others Process Applications), DRAM Product Type (Standard DRAM, Mobile DRAM (LPDDR), Graphics DRAM (GDDR), High Bandwidth Memory (HBM), Server DRAM, and Others DRAM Product Types), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The Market Forecasts are Provided in Terms of Value (USD).

| Fluorinated Gases |

| Silicon Precursors and Hydrides |

| Noble / Rare Gases |

| Other Gas Types |

| Chamber Cleaning |

| Plasma Etching / Reactive Ion Etching (RIE) |

| Thin-Film Deposition (CVD / ALD / Epitaxy) |

| Doping / Ion Implantation |

| Others Process Applications |

| Standard DRAM |

| Mobile DRAM (LPDDR) |

| Graphics DRAM (GDDR) |

| High Bandwidth Memory (HBM) |

| Server DRAM |

| Others DRAM Product Types |

| North America | |

| Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Gas Type | Fluorinated Gases | |

| Silicon Precursors and Hydrides | ||

| Noble / Rare Gases | ||

| Other Gas Types | ||

| By Process Application | Chamber Cleaning | |

| Plasma Etching / Reactive Ion Etching (RIE) | ||

| Thin-Film Deposition (CVD / ALD / Epitaxy) | ||

| Doping / Ion Implantation | ||

| Others Process Applications | ||

| By DRAM Product Type | Standard DRAM | |

| Mobile DRAM (LPDDR) | ||

| Graphics DRAM (GDDR) | ||

| High Bandwidth Memory (HBM) | ||

| Server DRAM | ||

| Others DRAM Product Types | ||

| By Geography | North America | |

| Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the projected size of the specialty gases market for DRAM fabs industry by 2031?

The specialty gases market for DRAM fabs industry is forecast to reach USD 2.07 billion by 2031, up from USD 1.37 billion in 2026, with an 8.61% CAGR.

Which gas family led demand in 2025?

Fluorinated gases led with a 40.61% share in 2025 because they remain essential in plasma etch and chamber cleaning across DRAM production.

Why is HBM increasing gas demand faster than standard DRAM?

HBM adds TSV etch, ALD barrier deposition, and fill steps for each extra die in the stack, so gas use per finished unit rises faster than in planar DRAM.

Which process application is growing the fastest?

Thin-film deposition is the fastest-growing application, with a 9.71% CAGR from 2026 to 2031, driven by rising ALD and advanced film requirements.

Which region dominates current demand?

Asia-Pacific led with an 87.58% share in 2025 because South Korea, Taiwan, Japan, and China host most advanced DRAM manufacturing capacity.

How are environmental rules changing supplier strategy?

Stricter fluorinated gas compliance is pushing suppliers to invest more in lower-GWP chemistries, abatement support, traceability, and tightly controlled delivery systems.

Page last updated on: