DRAM DIMM Module Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

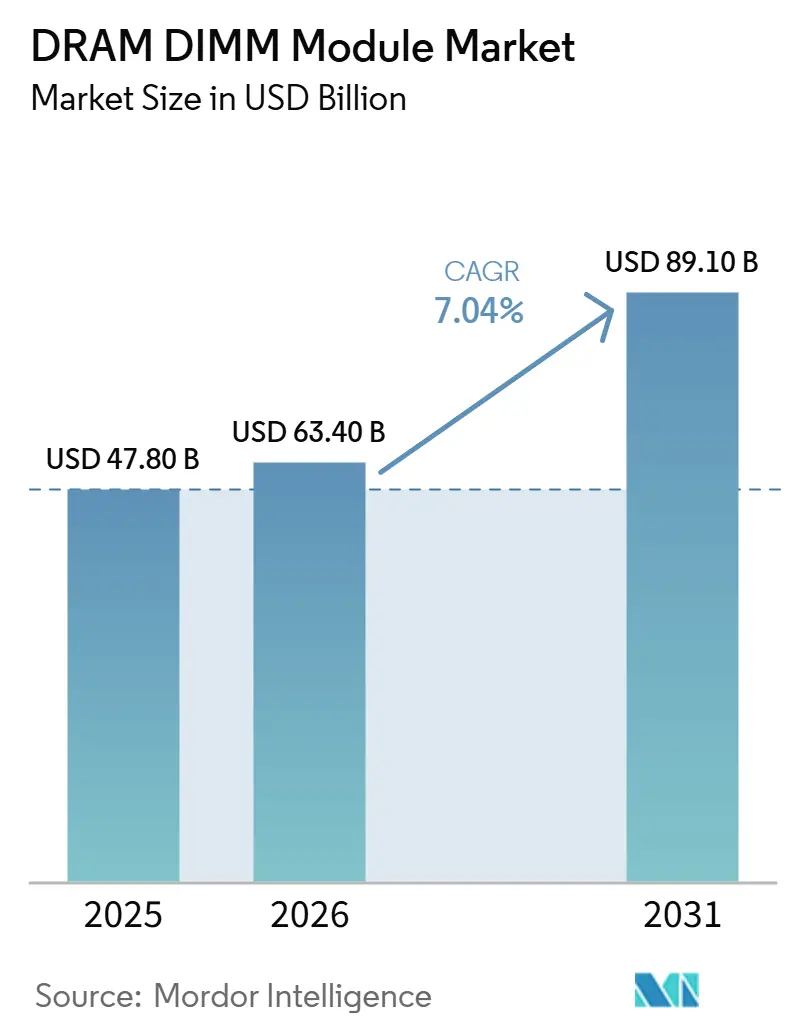

| Market Size (2026) | USD 63.40 Billion |

| Market Size (2031) | USD 89.10 Billion |

| Growth Rate (2026 - 2031) | 7.04% CAGR |

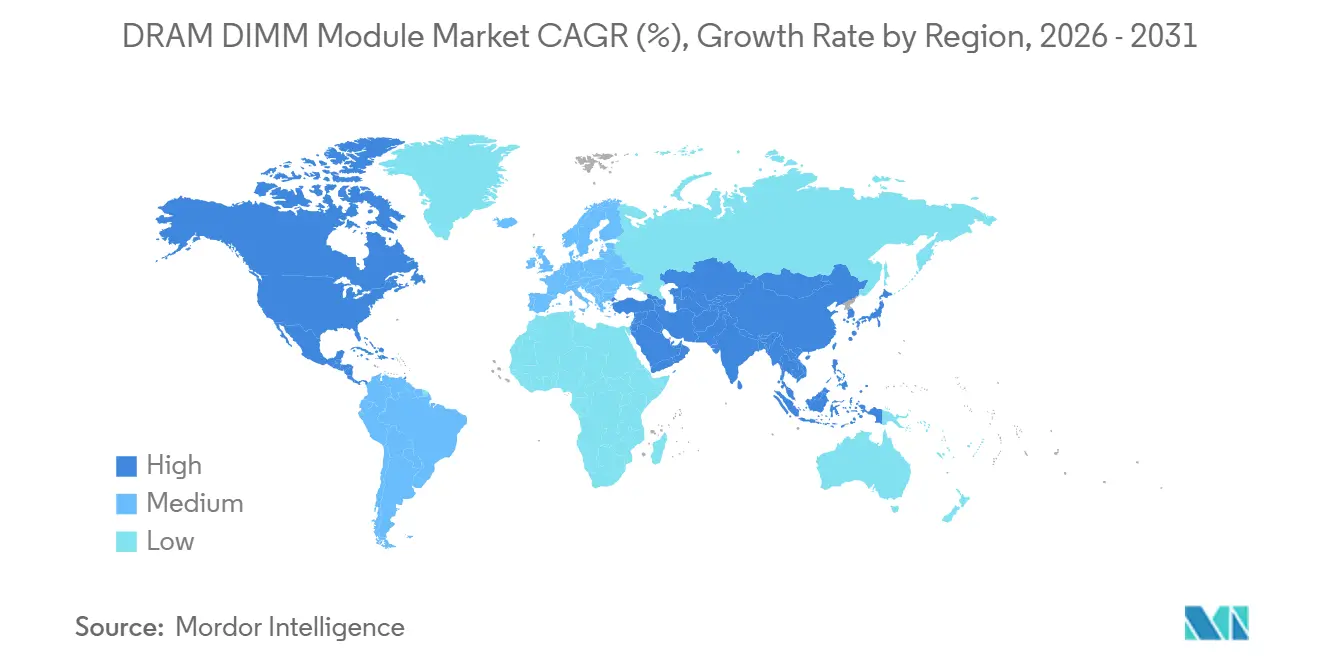

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DRAM DIMM Module Market Analysis by Mordor Intelligence

The DRAM DIMM module market size is projected to expand from USD 47.80 billion in 2025 and USD 63.40 billion in 2026 to USD 89.10 billion by 2031, registering a CAGR of 7.04% between 2026 to 2031. The DRAM DIMM module market is being lifted by a clear move toward server-grade DDR5 modules, with procurement centered on higher-density memory for AI-ready systems and new server platforms. The shift of AI spending toward inference infrastructure is widening demand for conventional server DIMMs, because inference deployments need large CPU-side memory pools across a broader installed base than training clusters alone. The DRAM DIMM module market is also shaped by an upstream supply structure in which a small group of die suppliers influences availability, while downstream module vendors compete through platform certification, supply consistency, and specialization. Asia-Pacific remained the core production and assembly base in 2025, while North America is expected to post the fastest regional expansion through 2031 as AI infrastructure programs move into larger commercial deployments. The main near-term pressure on the DRAM DIMM module market comes from supply tightness, qualification delays, and input-cost volatility, which together make procurement planning more complex than the headline growth rate suggests.

Key Report Takeaways

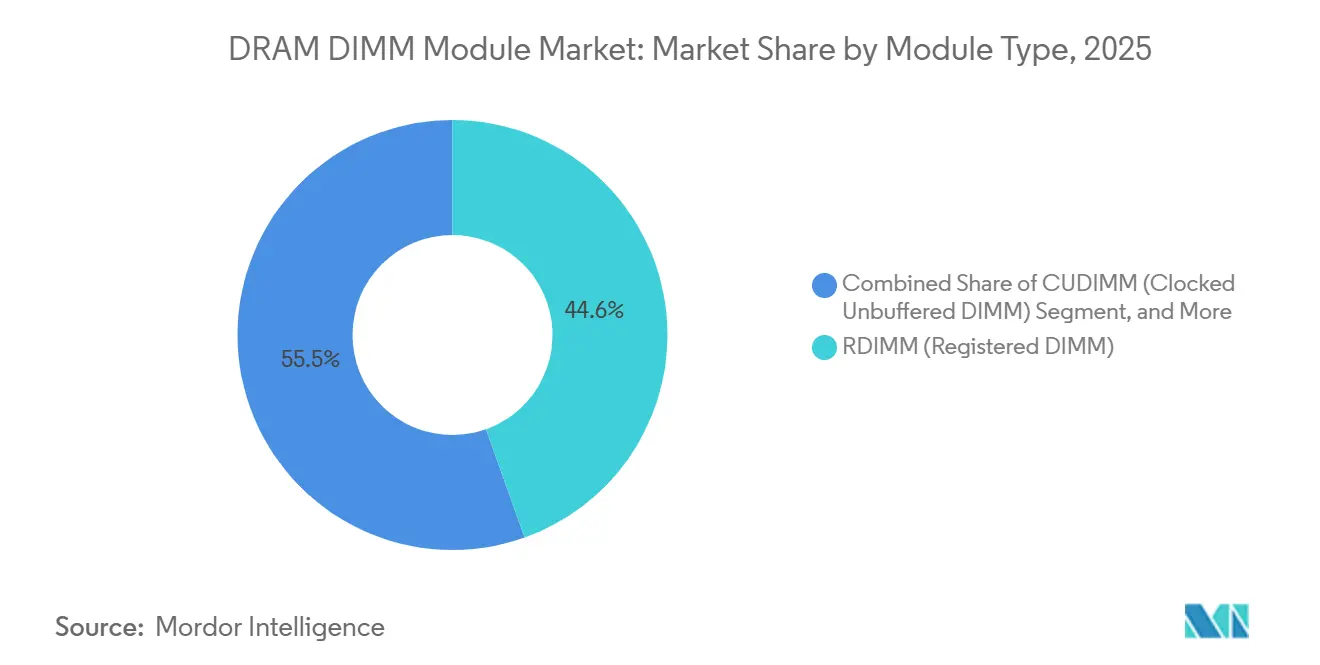

- By module type, RDIMMs held 44.55% of the DRAM DIMM module market share in 2025, while MRDIMM and MCR-DIMM are projected to expand at a 7.45% CAGR through 2031.

- By DRAM technology generation, DDR5 accounted for a 65.44% share of revenue in 2025, while the same generation is expected to record the fastest CAGR of 7.62% from 2026 to 2031.

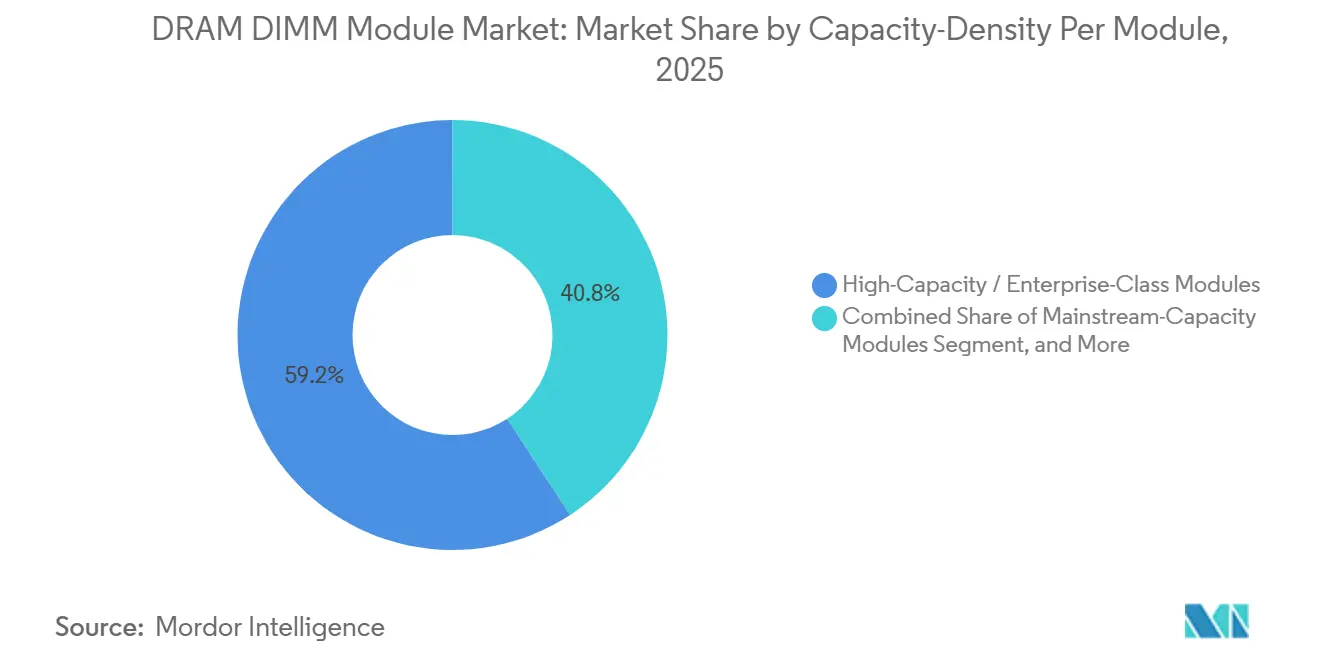

- By capacity, high-capacity and enterprise-class modules accounted for 59.22% of the DRAM DIMM module market size in 2025 and are projected to grow at a 7.34% CAGR through 2031.

- By end-use platform, enterprise and hyperscale data centers accounted for 42.44% of revenue in 2025, while AI servers and HPC are expected to expand at a 7.56% CAGR through 2031.

- By geography, Asia-Pacific held 58.44% of global revenue in 2025, while North America is projected to record the fastest regional CAGR of 7.73% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global DRAM DIMM Module Market Trends and Insights

Shift From AI Training to Inference Broadens Server DIMM Procurement

The DRAM DIMM module market is gaining support from the move of AI infrastructure spending from training concentration toward broader inference deployment. Inference systems need large CPU-attached memory pools for model weights, key-value cache handling, tokenization, and low-latency serving across distributed deployments. The DRAM DIMM module market therefore benefits from a wider memory demand base, because more nodes require high-capacity DDR5 RDIMMs rather than a smaller number of highly specialized training boxes. That change also shifts buyer behavior, because supply assurance is now becoming as important as nominal purchase price when procurement teams plan multi-quarter server builds. High-capacity RDIMMs have become the core target inside enterprise and hyperscale qualification lists, which reinforces demand for 64 GB, 96 GB, 128 GB, and higher-density configurations. The DRAM DIMM module market is therefore seeing a structural increase in server DIMM relevance as inference deployment spreads beyond isolated AI clusters.

DDR5 Platform Migration Across Enterprise and Hyperscale Servers

The DRAM DIMM module market is also being lifted by the fact that DDR5 is now the practical baseline for new server deployments in 2026. Current Intel Xeon 6 systems, AMD EPYC server platforms, and cloud-native architectures are aligned with DDR5, which reduces the role of DDR4 in greenfield builds and platform refreshes. DDR5 brings lower operating voltage, higher transfer speeds, and on-die ECC, which together improve performance stability in dense server environments. Samsung Electronics and AMD signed a memorandum of understanding in March 2026 that included high-performance DDR5 memory solutions for 6th-generation AMD EPYC CPUs within the AMD Helios rack-scale architecture, showing how platform and memory roadmaps are being coordinated more closely.[1]Samsung Electronics Co., Ltd., “Samsung and AMD Expand Strategic Collaboration on Next-Generation AI Memory Solutions,” Samsung Global Newsroom, news.samsung.com The DRAM DIMM module market is, therefore, rewarding module vendors that achieved early platform certification with major CPU ecosystems. Those suppliers are in a stronger position to capture enterprise and hyperscale qualification slots before later entrants close the certification gap.

Tight Supply and Inventory Prioritization for High-Capacity RDIMMs

The DRAM DIMM module market is facing a supply environment in which availability matters more than weak demand. Tightness is being shaped by capacity allocation across higher-value memory categories, which limits flexibility for conventional DRAM output and keeps high-capacity server modules under pressure. This is important for enterprises building DDR5 capacity through 2027, because lead times and approved configurations now matter as much as pricing discipline in the buying process. The DRAM DIMM module market is therefore favoring suppliers that can offer reliable delivery of high-density RDIMMs within qualified server roadmaps. Micron Technology and the U.S. government announced in June 2025 a domestic manufacturing and R&D program covering new fabs in Idaho and New York, expansion in Virginia, and first DRAM wafer output from the Idaho facility targeted for mid-2027, which shows that meaningful supply relief remains tied to a future window rather than immediate capacity gains. Until those additions begin contributing output, supply security remains a central design criterion across the DRAM DIMM module market.

Data Center Power Efficiency Push Accelerates DDR5 And High-Capacity Module Adoption

The DRAM DIMM module market is also benefiting from tighter power-efficiency targets inside large data center fleets. DDR5 operates at 1.1 V versus DDR4 at 1.2 V, which helps improve performance per watt in installations where power and cooling constraints are becoming more binding. That matters for AI inference deployment, because operators need more memory capacity without allowing rack-level and facility-level power intensity to rise too quickly. A detailed production server study found that moving from DDR5 RDIMM-6400 to MRDIMM-8800 increased memory bandwidth by 41%, improved bandwidth-bound workload performance by 27-41%, and delivered up to 30% server energy savings in memory-bound applications.[2]Ariel Oleksiak et al., “A Detailed Evaluation of a Production Server With High-End MRDIMM Main Memory,” arXiv, arxiv.org Those results give the DRAM DIMM module market a second demand path beyond raw compute expansion, because module choice now affects throughput and energy profile at the same time. As a result, higher-efficiency DDR5 and advanced buffered module formats are moving into procurement discussions earlier in the server-planning cycle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy DDR4 and DDR3 Installed Base Slows Full-Rate Replacement | -0.6% | Global | Medium term (2-4 years) |

| Qualification Cycles and Platform Validation Delays Slow Commercial Rollout | -0.5% | Global | Short term (≤ 2 years) |

| Mature DRAM Price Volatility Reduces Visibility for Module Buyers | -0.4% | Global | Short term (≤ 2 years) |

| High Platform Upgrade Cost and Motherboard Compatibility Constraints | -0.3% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy DDR4 and DDR3 Installed Base Slows Full-Rate Replacement

The DRAM DIMM module market is still being held back by the size of the installed DDR4 and legacy DDR3 base across enterprise and specialized server fleets. A full move from DDR4 to DDR5 is not a simple memory replacement, because it also requires new motherboards, compatible CPUs, updated power delivery, and thermal redesign in many systems. That stretches decision cycles, especially in sectors that qualify hardware over long periods and cannot replace large fleets at once. The DRAM DIMM module market therefore sees a meaningful share of refresh spending remain tied to supporting older platforms instead of converting directly into new DDR5 revenue. This drag becomes stronger when the cost of keeping DDR4 environments running rises at the same time that full DDR5 platform migration also remains capital intensive. The result is a slower replacement curve than the performance case for DDR5 alone would normally suggest.

Qualification Cycles and Platform Validation Delays Slow Commercial Rollout

The DRAM DIMM module market also faces a timing gap between product availability and commercial volume because validation and certification take time. Server buyers treat approved platform compatibility as a practical requirement, even when a formal validation path is technically voluntary, because qualified memory reduces deployment risk in large fleets.[3]Intel Corporation, “Platform Memory Validation, Specifications, and Results,” Intel, intel.com This delay is more visible in advanced formats such as MRDIMM and in very high-density RDIMMs, where ecosystem readiness is still maturing across controllers, boards, and server qualification programs. SK hynix became the first company to complete Intel Data Center Certification for a 256 GB DDR5 RDIMM in December 2025, which showed that even a tier-1 supplier needed extensive co-validation before broad commercial readiness could be established. JEDEC published the DDR5 Multiplexed Rank Data Buffer standard in April 2026 and confirmed that the MRDIMM Gen2 standard was nearing completion, which means the next wave of qualification is only now moving onto a firmer standards base. The DRAM DIMM module market therefore shows a smoother real revenue adoption curve than roadmap announcements alone might imply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Module Type: RDIMMs Remain the Core Server Standard While MRDIMMs Push Performance Upward

RDIMMs held a 44.55% share of the DRAM DIMM module market in 2025, which reflects their position as the default server memory format across Intel, AMD, and ARM-based data center platforms. RDIMMs also represented 44.55% of DRAM DIMM module market share in 2025, which underlines how central registered server memory remained to procurement across enterprise and hyperscale environments. Their lead comes from the registered clock driver architecture, which supports higher memory rank configurations per channel and helps preserve signal integrity as server complexity rises. This design becomes more valuable as CPU core counts increase and memory-bandwidth-to-core-count ratios tighten in cloud and enterprise workloads. LRDIMMs and 3DS RDIMMs remained important for memory-intensive use cases that require deeper DIMM-slot utilization, including in-memory databases and AI training nodes. UDIMMs continued to serve consumer desktops and mainstream workstations, while SO-DIMMs and CSODIMMs remained relevant in notebooks and embedded form factors where board space and power envelopes limit module choice.

MRDIMM and MCR-DIMM are projected to grow at the fastest pace within module type, at a 7.45% CAGR from 2026 to 2031, which places them at the leading edge of the DRAM DIMM module industry. JEDEC published JESD82-552 for the DDR5 Multiplexed Rank Data Buffer in April 2026 and stated that the Gen2 MRDIMM standard was nearing completion with a 12,800 MT/s target, which gives the format a clearer interoperability path and a stronger road map. A detailed production server study found that moving from DDR5 RDIMM-6400 to MRDIMM-8800 increased memory bandwidth by 41% and improved bandwidth-bound workload performance by 27-41%, while also delivering up to 30% energy savings in memory-bound cases. Those results explain why advanced buffered modules are gaining attention in AI and HPC designs that cannot scale efficiently on standard RDIMMs alone. CUDIMMs are also opening a premium niche in high-performance desktop and workstation deployments, and JEDEC published the updated JESD323B common standard for CUDIMM and CQDIMM in February 2026. ADATA Technology, in collaboration with MSI and Intel, unveiled the industry’s first 4-RANK DDR5 CUDIMM at CES 2026 with up to 128 GB per module and speeds up to 7,200 MT/s on Intel Z890 prototype platforms, which shows how desktop-class memory is also moving up the performance ladder.

By DRAM Technology Generation: DDR5 Moves From Transition Phase To Market Baseline

DDR5 accounted for a 65.44% share of the DRAM DIMM module market in 2025 and also stands as the fastest-growing DRAM generation with a 7.62% CAGR through 2031. That dual position shows that DDR5 is not only the replacement path, but also the center of new server memory demand across the DRAM DIMM module market. The main reason is platform alignment, because current server launches across x86 and ARM designs are built around DDR5 rather than DDR4. Samsung Electronics and AMD expanded their strategic collaboration in March 2026, with Samsung set to serve as AMD’s primary DDR5 memory provider for 6th-generation EPYC CPUs within the Helios rack-scale architecture. That kind of platform-level coordination shortens adoption friction and raises confidence in DDR5 road maps for large enterprise buyers. The DRAM DIMM module market is therefore treating DDR5 as the new baseline for forward procurement rather than as a premium upgrade choice.

SK hynix became the first company in the industry to complete Intel Data Center Certification for a 256 GB DDR5 RDIMM in December 2025, which gave DDR5 a stronger commercial proof point at the high-density end of enterprise qualification. DDR4 still retained revenue in 2025 for maintenance spending, selective server expansion, and workloads where near-term replacement remained hard to justify from a capital-planning standpoint. Legacy DRAM, including DDR3 and earlier generations, still served industrial, defense, and telecommunications replacement cycles with no growth path visible over the forecast period. This creates a narrow planning window for organizations caught between keeping older platforms alive and committing to a full generational change. JEDEC’s standards committees continue to publish updates that manage DDR5 interoperability and compliance requirements, which reinforces the generation’s role as the common base for future qualification rather than an optional high-end tier. The DRAM DIMM module market therefore depends not only on technology readiness, but also on the timing and discipline of enterprise migration programs.

By Capacity-Density Per Module: Enterprise-Class Density Leads Both Revenue and Growth

High-capacity and enterprise-class modules accounted for 59.22% of the DRAM DIMM module market in 2025 and are projected to grow at a 7.34% CAGR through 2031. They also represented 59.22% of the DRAM DIMM module market size in 2025, which shows how strongly procurement shifted toward 64 GB, 96 GB, 128 GB, and higher-density server modules. This density tier leads because AI inference systems, memory-optimized servers, and large virtualization environments require much larger DRAM footprints per node than standard enterprise servers. In practical deployment terms, that keeps enterprise-class density at the center of procurement for hyperscalers, cloud service providers, and large enterprise data centers. SK hynix completed Intel certification for a 256 GB DDR5 RDIMM in December 2025, which expanded the deployable density ceiling for qualified server memory and strengthened the case for denser system configurations. The DRAM DIMM module market is therefore seeing density become a commercial differentiator rather than a technical specification alone.

Mainstream-capacity modules continued to matter in general-purpose enterprise servers, mid-tier cloud infrastructure, and workloads where memory-to-core ratios are less demanding. Low-capacity modules remained concentrated in edge systems, network appliances, and embedded deployments where the total memory envelope is constrained by system design. This creates a layered demand profile inside the DRAM DIMM module industry, with enterprise-class density driving revenue while lower tiers continue to serve specialized or cost-sensitive roles. Vendors that can cover both ends of the portfolio gain an advantage because they can support customers through a broader platform transition cycle. The DRAM DIMM module market also shows that density is now tied to server architecture and workload placement, because memory capacity affects both utilization and system design choices. That dynamic should keep high-capacity modules in the lead even if buyers remain selective in other parts of the module mix.

By End-Use Platform: Data Centers Hold the Largest Revenue Base While AI And HPC Lead Growth

Enterprise and hyperscale data centers accounted for 42.44% of the DRAM DIMM module market in 2025, making them the largest end-use platform for server-grade modules. This segment leads because it absorbs the broadest mix of RDIMMs, LRDIMMs, high-density DDR5 modules, and emerging MRDIMM formats across large fleet deployments. The DRAM DIMM module market is closely tied to these buyers because they purchase memory through structured qualification programs, not through short replacement cycles, which makes platform alignment and supply reliability central to vendor selection. AI servers and HPC are projected to expand at the fastest pace, at a 7.56% CAGR from 2026 to 2031, as commercial AI deployment increases the need for large-context memory allocation and high-bandwidth server design. JEDEC compliance across electrical, mechanical, and power-management requirements remains the baseline gate for this part of the market, because certified module behavior directly affects deployment confidence in large server fleets. The DRAM DIMM module market therefore remains anchored in data centers even as its fastest growth comes from AI-oriented server clusters.

Desktop PCs accounted for a mid-single-digit share, with support coming from premium CUDIMM platform adoption and an emerging AI PC refresh pattern rather than broad consumer replacement. ADATA Technology, MSI, and Intel introduced a 4-RANK DDR5 CUDIMM in January 2026 that targeted high-performance desktop systems with server-like density characteristics, which highlights how premium client memory is moving closer to workstation-class use cases. Notebooks and mobile workstations remained an adjacent revenue stream through CSODIMM and SO-DIMM formats, with rising average memory content in more demanding designs even as price pressure stayed present. Industrial, telecommunications, and embedded systems formed a smaller but resilient part of the DRAM DIMM module market because these customers prioritize long lifecycle support, thermal tolerance, and stable qualification over rapid upgrade cycles. Innodisk launched DDR5 CAMM2 and LPDDR5X CAMM2 memory modules in August 2025 for rugged industrial applications, with speeds up to 6,400 MT/s and 8,533 MT/s and a 60% space reduction versus traditional SO-DIMM configurations. That keeps specialized embedded memory as a stable revenue layer even while the center of the DRAM DIMM module market remains in data centers and AI systems.

Geography Analysis

Asia-Pacific held 58.44% of the global DRAM DIMM module market in 2025, giving the region the largest regional position in both supply and demand. Asia-Pacific also accounted for 58.44% of DRAM DIMM module market share in 2025, which reflects its role as the center of die manufacturing, module assembly, and domestic procurement across server, client, and industrial memory. South Korea anchors the supply side through Samsung Electronics and SK hynix, which remain central to advanced DRAM die output and influence global availability conditions across the DRAM DIMM module market. Taiwan reinforces that position through a broad module assembly base that includes companies such as ADATA and Innodisk, whose product launches show sustained regional capability across client, industrial, and high-performance memory. This combination of upstream die leadership and downstream module specialization keeps Asia-Pacific at the center of the global value chain.

North America is projected to grow at the fastest regional pace, at a 7.73% CAGR from 2026 to 2031. The region’s growth is tied to large AI infrastructure programs, strong enterprise server refresh activity, and rising interest in securing a future domestic memory base. Micron Technology and the U.S. government announced in June 2025 a program covering USD 150 billion in manufacturing investment and USD 50 billion in R&D across Idaho, New York, and Virginia, with first wafer output from the new Idaho facility targeted for mid-2027. That investment does not change near-term supply tightness, but it strengthens North America’s long-run position in the DRAM DIMM module market and supports future supply diversification. Europe held a stable share, with demand concentrated in Germany, the United Kingdom, and France, where enterprise refresh cycles and data-sovereignty considerations continue to support on-premises and regionally anchored infrastructure.

The Rest of the World represented a low single-digit share of the DRAM DIMM module market in 2025, but it still contained several targeted growth pockets tied to sovereign digital infrastructure and selective data center buildouts. Demand in this group was driven less by broad client replacement and more by cloud localization, telecom modernization, and government-backed digital capacity programs. South America remained led by Brazil’s expanding digital economy and infrastructure investment, although module procurement stayed heavily dependent on imports from Asia-Pacific suppliers. Africa was the smallest contributor, with early-stage data center and edge deployments in countries such as South Africa and Nigeria providing the main near-term demand base. These markets are still small in absolute terms, but they widen the geographic footprint of the DRAM DIMM module market beyond its primary supply and consumption hubs.

Competitive Landscape

The DRAM DIMM module market operates through two linked competitive layers that shape pricing power and brand differentiation in different ways. At the upstream level, Samsung Electronics, SK hynix, and Micron Technology control the vast majority of advanced DRAM die supply, which gives them strong influence over availability, price direction, and the pace of technology transition across the DRAM DIMM module market. At the downstream module level, competition is more fragmented, with Kingston Technology, ADATA, Corsair, G.SKILL, Transcend, and Innodisk differentiating through design depth, thermal management, platform certification, channel relationships, and end-market focus. This structure means the DRAM DIMM module market combines a concentrated supply base with a broader field of module brands that compete on execution rather than wafer-scale manufacturing reach. Compliance with JEDEC standards remains a practical market-entry filter, because module vendors without designs aligned to the latest standards struggle to access the most profitable enterprise qualification channels.

The 3 largest component suppliers are also pursuing competing strategies in advanced module formats. Conference material from the Future Memory and Storage Association in 2025 showed Samsung developing 128 GB MRDIMM modules for AI training at DDR5-8000 speeds, SK hynix advancing MRDIMM for AI inference in HPC clusters, and Micron sampling MRDIMM at 8,800 MT/s in Q1 2025. Samsung Electronics and AMD expanded their strategic collaboration in March 2026, which strengthened Samsung’s position across premium server DIMMs and adjacent AI memory demand. Kingston Technology launched the Kingston FURY Renegade Pro DDR5 RDIMM in May 2026 for high-end workstations and on-premises AI workflows, which showed how module brands are moving into semi-professional technical computing niches. The DRAM DIMM module market is therefore seeing competition intensify in niches where early validation, specialized cooling, and tighter workload targeting matter more than pure unit volume.

White-space opportunities in the DRAM DIMM module market remain concentrated in rugged industrial memory, early qualification of new formats, and products that address high-capacity use cases outside standard enterprise racks. Innodisk’s August 2025 launch of DDR5 CAMM2 and LPDDR5X CAMM2 modules for rugged industrial systems showed how long-lifecycle and space-constrained deployments can command specialized positioning and pricing. CUDIMM and MRDIMM validation also remains an area where early movers can build durable advantages, because certification lag still limits how quickly later entrants can compete in qualified channels. Chinese participation remains at an earlier stage, but the appearance of Chinese DDR5 components in broader commercial channels suggests that an additional supply vector may gradually emerge in mainstream-speed modules. That possibility does not change the upstream concentration of the DRAM DIMM module market today, but it does introduce a longer-term source of pricing pressure and supplier diversification.

DRAM DIMM Module Industry Leaders

Samsung Electronics Co., Ltd.

SK hynix Inc.

Micron Technology, Inc.

Kingston Technology Company, Inc.

ADATA Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Kingston Technology launched the Kingston FURY Renegade Pro DDR5 RDIMM with a heat spreader, designed for high-end workstations and on-premises AI workflows supporting Intel XMP and AMD EXPO profiles. The launch marks Kingston's expansion into ECC-protected overclockable DIMM territory, a segment previously dominated by channel-specific enterprise suppliers, and signals growing demand for semi-professional DDR5 modules in AI-adjacent workstation deployments.

- April 2026: JEDEC's JC-45 committee published JESD82-552, the DDR5 Multiplexed Rank Data Buffer (MDB) standard, and confirmed the MRDIMM Gen2 module standard is nearing completion, with Gen2 targeting 12,800 MT/s and Gen3 interface logic already in active development. This milestone provides the interoperability foundation required for module manufacturers to begin Gen2 MRDIMM design validation, unlocking a new performance tier critical for AI and HPC server platforms.

- March 2026: Samsung Electronics and AMD signed a memorandum of understanding expanding their strategic collaboration on next-generation AI memory and computing technologies. Under the agreement, Samsung will serve as AMD's primary DDR5 memory provider for 6th-generation EPYC CPUs (codenamed "Venice") within the AMD Helios rack-scale architecture, reinforcing Samsung's position across both the premium server DIMM and AI accelerator memory stack.

- February 2026: SK hynix's board approved KRW 21.61 trillion (USD 15.7 billion) in capital expenditure for Phases 2 through 6 of its Yongin Semiconductor Cluster, targeting mid- to long-term DRAM production capacity expansion through 2030. The investment supports growing demand for server-grade DDR5 DIMMs and positions SK hynix to expand wafer capacity to 70,000 wafers per month at its M15X Cheongju facility by year-end 2026.

Global DRAM DIMM Module Market Report Scope

The Global DRAM DIMM Module Market refers to the industry segment focused on the production, distribution, and deployment of Dual In-Line Memory Modules (DIMMs) that utilize Dynamic Random-Access Memory (DRAM) technology to provide high-speed, volatile storage for computing systems.

The DRAM DIMM Module Market Report is Segmented by Module Type (UDIMM (Unbuffered DIMM), CUDIMM (Clocked Unbuffered DIMM), RDIMM (Registered DIMM), LRDIMM / 3DS RDIMM, MRDIMM / MCR-DIMM, and Others (SO-DIMM, CSODIMM)), DRAM Technology Generation (DDR5, DDR4, and Legacy DRAM Modules (DDR3 and Earlier)), Capacity / Density Per Module (Low-Capacity Modules, Mainstream-Capacity Modules, and High-Capacity / Enterprise-Class Modules), End-Use Platform (Enterprise and Hyperscale Data Centers, AI Servers and High-Performance Computing, HPC, Desktop PCs, Notebooks and Mobile Workstations, and Industrial, Telecom and Embedded Systems), and Geography (North America, Europe, Asia Pacific, Rest of the World). The Market Forecasts are Provided in Terms of Value (USD).

| UDIMM (Unbuffered DIMM) |

| CUDIMM (Clocked Unbuffered DIMM) |

| RDIMM (Registered DIMM) |

| LRDIMM / 3DS RDIMM |

| MRDIMM / MCR-DIMM |

| Other Module Types (SO-DIMM, CSODIMM) |

| DDR5 |

| DDR4 |

| Legacy DRAM Modules (DDR3 and Earlier) |

| Low-Capacity Modules |

| Mainstream-Capacity Modules |

| High-Capacity / Enterprise-Class Modules |

| Enterprise and Hyperscale Data Centers |

| AI Servers and High-Performance Computing, HPC |

| Desktop PCs |

| Notebooks and Mobile Workstations |

| Industrial, Telecom and Embedded Systems |

| North America | United States |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| Rest of Asia Pacific | |

| Rest of the World | South America |

| Middle East | |

| Africa |

| By Module Type | UDIMM (Unbuffered DIMM) | |

| CUDIMM (Clocked Unbuffered DIMM) | ||

| RDIMM (Registered DIMM) | ||

| LRDIMM / 3DS RDIMM | ||

| MRDIMM / MCR-DIMM | ||

| Other Module Types (SO-DIMM, CSODIMM) | ||

| By DRAM Technology Generation | DDR5 | |

| DDR4 | ||

| Legacy DRAM Modules (DDR3 and Earlier) | ||

| By Capacity / Density Per Module | Low-Capacity Modules | |

| Mainstream-Capacity Modules | ||

| High-Capacity / Enterprise-Class Modules | ||

| By End-Use Platform | Enterprise and Hyperscale Data Centers | |

| AI Servers and High-Performance Computing, HPC | ||

| Desktop PCs | ||

| Notebooks and Mobile Workstations | ||

| Industrial, Telecom and Embedded Systems | ||

| By Geography | North America | United States |

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Rest of Asia Pacific | ||

| Rest of the World | South America | |

| Middle East | ||

| Africa | ||

Key Questions Answered in the Report

What is the expected size of the DRAM DIMM module market by 2031?

The DRAM DIMM module market is projected to reach USD 89.10 billion by 2031, rising from USD 63.40 billion in 2026 at a CAGR of 7.04% over 2026-2031.

Which module type currently leads DRAM DIMM demand?

RDIMMs led module type demand with a 44.55% revenue share in 2025 because they remained the standard server memory format across major data center platforms.

Why is DDR5 becoming the default choice for new server deployments?

DDR5 accounted for 65.44% of revenue in 2025 and is projected to grow at a 7.62% CAGR, supported by new server platform alignment, higher speed, lower voltage, and wider qualification momentum.

Which end-use area is expanding the fastest for DRAM DIMMs?

AI servers and HPC are projected to expand at a 7.56% CAGR through 2031 as commercial AI deployment increases the need for larger memory pools and higher bandwidth.

Which region holds the strongest position in DRAM DIMMs today?

Asia-Pacific held 58.44% of global revenue in 2025, supported by South Korean die production, Taiwanese module assembly, and a broad regional procurement base.

What is the main near-term challenge for DRAM DIMM buyers?

The main near-term challenge is supply tightness rather than weak demand, because allocation pressure, long validation cycles, and input-cost volatility continue to affect procurement planning.

Page last updated on: