Automotive Active Spoiler Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

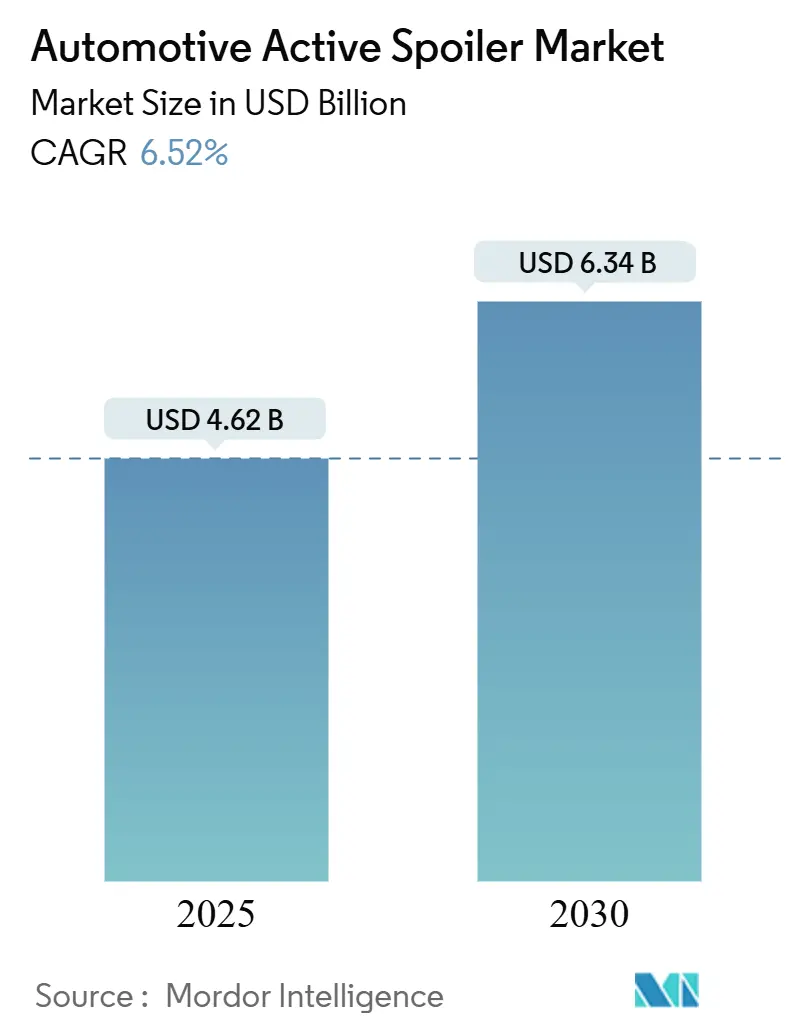

| Market Size (2025) | USD 4.62 Billion |

| Market Size (2030) | USD 6.34 Billion |

| Growth Rate (2025 - 2030) | 6.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Active Spoiler Market Analysis by Mordor Intelligence

The automotive active spoiler market size is valued at USD 4.62 billion in 2025 and is forecast to grow to USD 6.34 billion by 2030, registering a 6.52% CAGR during the forecast period. Vehicle makers are channeling investment toward aerodynamic add-ons that trim drag coefficients, which in turn helps them meet tightening fuel-economy and CO₂ targets, extend electric-vehicle range, and curb compliance costs. Active and passive spoilers have shifted from styling accents to cost-effective regulatory tools, a transition reinforced by robust demand for SUVs and the rapid electrification of passenger-car platforms. Asia-Pacific commands the highest regional share, while carbon-fiber, motorized, and battery-electric sub-segments represent the fastest growth pockets within the automotive spoiler market.

Key Report Takeaways

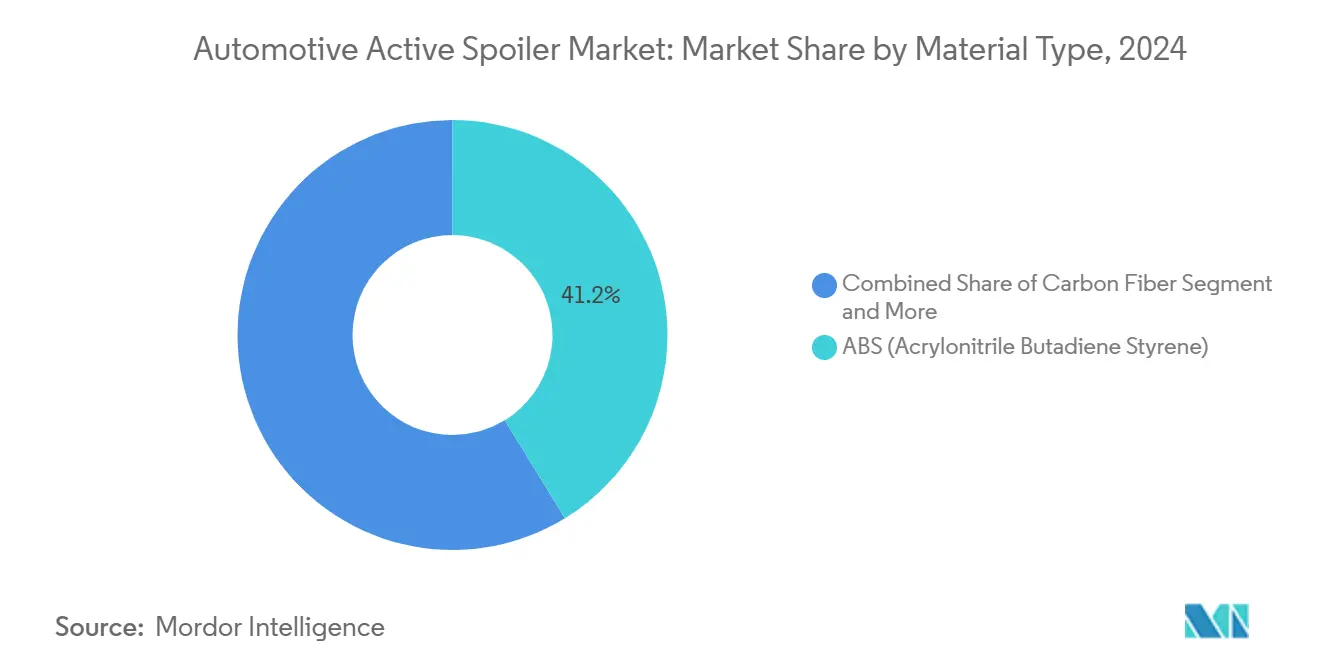

- By material, ABS plastic led with 41.23% of the automotive active spoiler market share in 2024; carbon fiber is projected to expand at an 8.34% CAGR through 2030.

- By type, adjustable spoilers accounted for 55.62% of the automotive active spoiler market share in 2024, while motorized variants are advancing at a 7.26% CAGR to 2030.

- By vehicle class, SUVs held 40.18% of the automotive active spoiler market share in 2024; sports cars are poised for the fastest 7.88% CAGR through 2030.

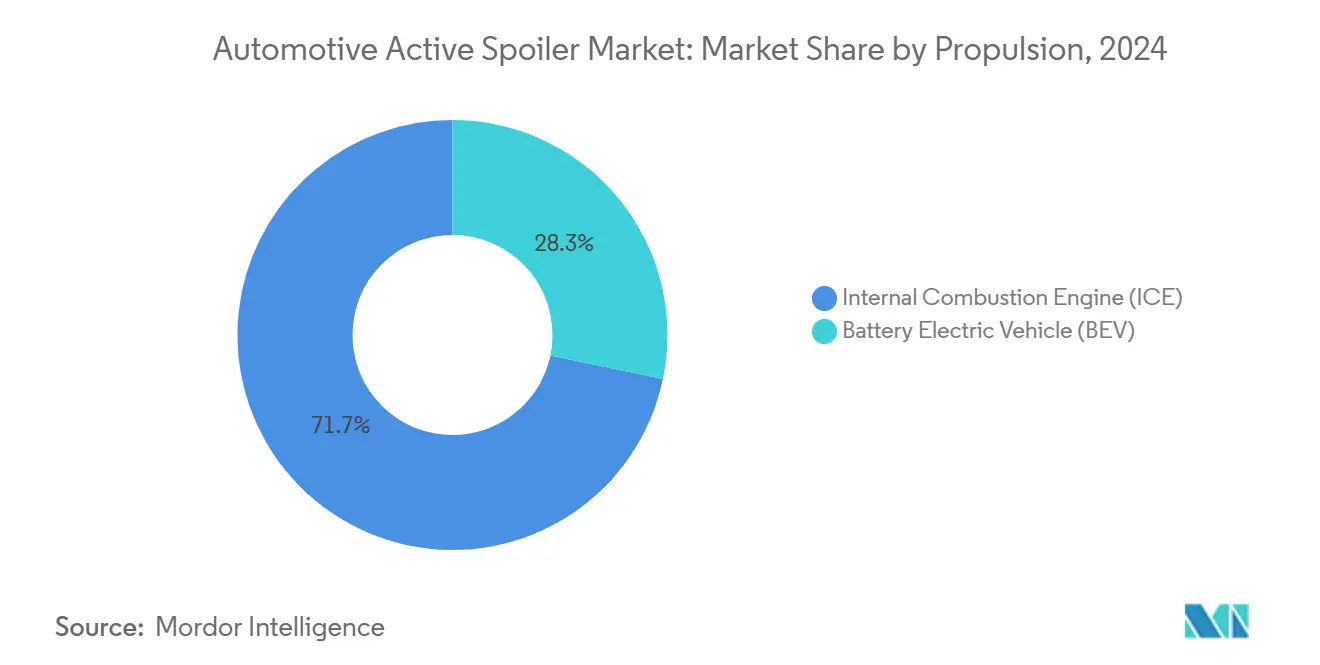

- By propulsion, internal-combustion models represented 71.72% of the automotive active spoiler market share in 2024, whereas battery-electric vehicles are accelerating at an 8.96% CAGR through 2030.

- By channel, OEM fitments dominated, with an 84.63% share of the automotive active spoiler market in 2024, yet aftermarket sales are growing at a 7.34% CAGR through 2030.

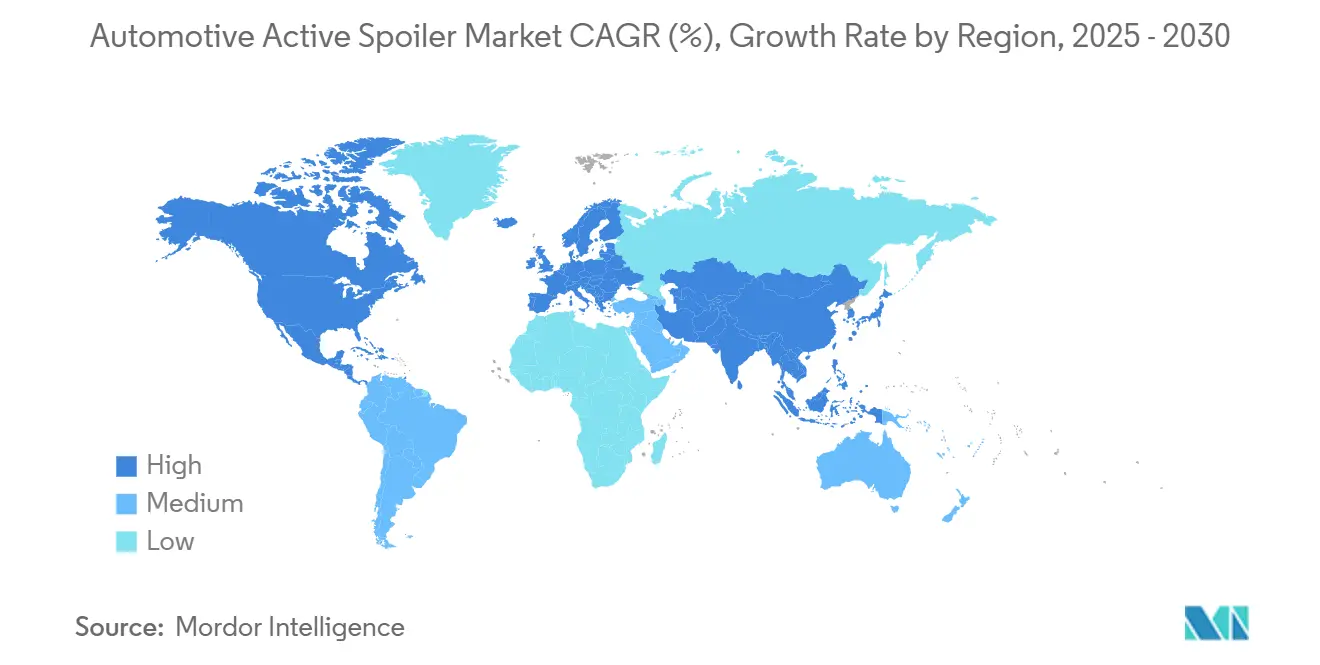

- By geography, Asia-Pacific captured 37.43% of the automotive active spoiler market share and is expected to grow 7.86% by 2030.

Global Automotive Active Spoiler Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tough Global CO₂ and Fuel Rules | +1.8% | Global; EU and China lead | Medium term (2-4 years) |

| OEMs Adopting Active Aero for EVs | +1.5% | North America and EU; expanding to Asia-Pacific | Medium term (2-4 years) |

| Rise in Lightweight Composites (CF, CFRTP) | +1.2% | Global; premium focus | Long term (≥ 4 years) |

| SUV/Performance Body Styles Growing (C+ Segment) | +0.9% | Global; Asia-Pacific and North America lead | Short term (≤ 2 years) |

| Low-Cost Electromechanical Actuators (Tier-1) | +0.7% | Global; developed markets first | Medium term (2-4 years) |

| OTA-Driven Dynamic Spoiler Control | +0.4% | North America and EU; premium OEMs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global CO₂ and Fuel-Economy Mandates

Fleet-average CO₂ caps in the European Union (95 g/km from 2024) and China’s dual-credit scheme force automakers to harvest every aerodynamic gain possible. U.S. CAFE rules aiming for 49 mpg by 2026 apply similar pressure [1]“CAFE Standards for 2026,”, U.S. Environmental Protection Agency, epa.gov. Spoilers, once cosmetic, now deliver quantifiable fleet-wide benefits because marginal drag cuts translate to meaningful fuel economy or range improvements. Computational fluid-dynamics modeling validates spoiler effectiveness, prompting sustained R&D spend cheaper than power-train redesigns. As a result, the automotive spoiler market continues to deepen its regulatory value proposition.

Rapid OEM Shift to Active-Aero Packages in EV Platforms

Electric-vehicle range anxiety has recast active rear spoilers into energy-management devices. Tesla, for instance, credits its software-driven units for helping the Model S hit a 0.208 drag coefficient [2]“Model S Specifications,”, Tesla Inc., tesla.com. Hyundai’s Active Air Skirt system, which deploys above 80 km/h, underlines mainstream adoption [3]“Active Air Skirt Technology Release,”, Hyundai Motor Company, hyundai.com. These moves position active aerodynamics as a core differentiator in the automotive spoiler market.

Wider Adoption of Lightweight Composites (Carbon Fiber, CFRTP)

Premium OEMs now specify carbon-fiber or CFRTP spoilers that weigh less than ABS yet meet stringent structural requirements. Hexcel’s HexTow fiber and Teijin’s recyclable CFRTP showcase supply-chain momentum toward lighter, stronger parts [4]“Automotive Carbon Fiber Investment,”, Hexcel Corporation, hexcel.com. Automated fiber placement and compression molding lower cost curves, creating broader diffusion beyond luxury segments throughout the automotive spoiler industry.

OTA Software Updates Enabling Dynamic Spoiler Logic

Centralized vehicle controllers now push over-the-air updates that refine spoiler deployment algorithms based on driver habits, weather, or load state. This software layer transforms spoilers into smart subsystems that enhance brand loyalty through continuous performance gains, sustaining organic growth in the automotive spoiler industry.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost: Motorized Systems and CF Skins | -1.1% | Global, with premium segments most affected | Short term (≤ 2 years) |

| Reliability Issues in Extreme Climates | -0.8% | Northern regions and desert climates globally | Medium term (2-4 years) |

| Tariff Risks in Composite Supply Chains | -0.6% | North America and Europe, with China trade dependencies | Medium term (2-4 years) |

| Low Consumer Awareness Beyond Premium Segments | -0.4% | Global, concentrated in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Unit Cost of Motorized Mechanisms and Carbon-Fiber Skins

Brushless motors, linkage arms, control modules, and carbon-fiber skins can add USD 200–500 at build, a hurdle for price-sensitive mainstream models. Carbon-fiber panels carry material premiums over ABS, while integrating sensors and harnesses inflates the bill of materials. Supply-chain concentration in aerospace-grade fiber also amplifies cost volatility, holding back faster penetration in the automotive spoiler market.

Reliability Concerns in Harsh Climates (Dust, Ice)

Active spoilers must endure ISO 16750 temperature swings, dust ingress, and ice buildup that can jam electric actuators. Field failure can generate warranty claims exceeding any fuel-saving payback, making OEMs cautious about rolling out motorized units in colder or sand-prone geographies. Continued sealing, materials, and testing improvements are critical to mitigate this restraint.

Segment Analysis

By Material Type: Carbon Fiber Drives Premium Lightweighting

ABS retained a 41.23% share of the automotive active spoiler market in 2024, thanks to low cost and scalable injection molding. Carbon fiber captured the fastest 8.34% CAGR through 2030, while demand for lighter composites that enable complex geometries makes carbon solutions essential for premium battery-electric and sports cars. Teijin’s recyclable CFRTP demonstrates the pivot toward circular materials, a theme that supports long-term expansion of the automotive spoiler market.

ABS remains dominant for m,ass-market hatchbacks and sedans, balancing impact resistance and affordability. Fiberglass keeps a foothold in mid-range SUVs, and sheet metal retreats to commercial-vehicle niches where durability outweighs weight penalties. The automotive spoiler market size, attributed to emerging bio-based composites, should climb as sustainability targets rise.

By Type: Motorized Systems Accelerate Despite Complexity

Adjustable spoilers, including multi-angle manual designs, held a 55.62% share of the automotive active spoiler market in 2024 because they cost less and fit easily into aftermarket channels. Motorized versions are projected to expand at a 7.26% CAGR through 2030. They rely on compact actuators and real-time sensors to maximize drag reduction during highway cruising and retract for city use. These features align with the software-defined vehicle era and raise the profile of motorized units within the automotive spoiler market.

Integration complexities—wiring, firmware, and diagnostic protocols—still limit deployment in value brands. Yet Magna’s next-gen electromechanical modules and standardized LIN-bus controls are lowering the integration burden, positioning motorized spoilers for broader OEM adoption once unit costs align with volume economics.

By Vehicle Type: Sports Cars Lead Innovation Despite SUV Volume

Sport utility vehicles (SUVs) accounted for a 40.18% share of the automotive active spoiler market in 2024 because aerodynamics matter most on large crossovers that face stringent fuel-economy penalties. Sports cars, clocking the top 7.88% CAGR through 2030, remain innovation incubators: OEMs debut active wings on halo models and then cascade lessons to volume segments. As torque-rich electric drivetrains demand stable high-speed downforce, sports-car R&D is shaping future spoiler norms within the automotive spoiler industry.

Hatchbacks and MPVs continue to use fixed spoilers in emerging markets for mild fuel-saving benefits and aesthetic flair. They also fertilize the thriving aftermarket, which sells cost-effective upgrades that mirror OE designs but avoid complex electronics.

By Propulsion: BEV Adoption Transforms Aerodynamic Priorities

Internal-combustion vehicles hold a 71.72% share of the automotive active spoiler market in 2024. Still, battery-electric models show the strongest 8.96% CAGR through 2030 because every drag reduction directly converts to range extension. Tesla’s speed-sensitive rear wing shows how software and hardware squeeze every mile from a kilowatt-hour. As the automotive spoiler market evolves, hybrids will exploit both efficiency and performance angles, but the most disruptive gains lie in pure EVs that monetize aero gains most visibly.

By Distribution Channel: Aftermarket Gains Momentum Beyond OEM Dominance

OEM installations owned an 84.63% share of the automotive active spoiler market in 2024 because complex calibration for active units favors factory fitment. Even so, the aftermarket’s 7.34% CAGR reflects rising DIY culture and e-commerce penetration through 2030. RealTruck and other web-based retailers now bundle airflow simulations and instructional videos that demystify spoiler selection. ISO-compliant materials and easy-fit kits safeguard quality, nurturing consumer confidence and diversifying revenue streams across the automotive spoiler market.

Geography Analysis

Asia-Pacific holds a 37.43% share of the automotive active spoiler market in 2024 and will post the quickest 7.86% CAGR through 2030. Japanese suppliers excel in actuator miniaturization, while South Korean groups exploit advanced carbon-fiber lines, anchoring an integrated regional supply chain. Government incentives and rapidly expanding charging networks amplify spoiler uptake, particularly within long-range EV programs.

Due to robust EPA and EU frameworks mandating stringent fuel-efficiency targets, North America and Europe remain technologically influential. Premium brands in these regions order carbon-fiber and motorized solutions with higher margins, feeding innovation for the global automotive spoiler market. Cold-weather validation labs in Canada and northern Scandinavia also shape reliability standards for active systems.

South America, the Middle East, and Africa form an emerging tri-cluster. Brazil’s industrial base and local-content policies encourage domestic spoiler tooling, while desert climates from Saudi Arabia to Morocco create demand for dust-sealed actuators. These regions still trail in per-capita EV adoption. Yet, the aftermarket scene is expanding thanks to online retail, which paves the way for gradual spoiler penetration across broader vehicle cohorts.

Competitive Landscape

The automotive active spoiler market features mid-level fragmentation, allowing Tier-1s, material specialists, and software newcomers to coexist. Plastic Omnium restructured its Exterior & Lighting unit to sharpen its focus on integrated aero-lighting modules.

Hexcel, SGL Carbon, and Teijin dominate aerospace-grade fibers and are extending capacity for automotive-grade tow sizes to make carbon more accessible. New entrants with over-the-air software prowess compete on algorithmic deployment logic rather than hardware. However, ISO 16750 test regimes and OEM audit protocols raise barriers that favor incumbents with proven quality systems. M&A and co-development alliances are likely as suppliers chase vertical integration, from resin formulation to final actuator assembly, tightening competition within the automotive spoiler industry.

Automotive Active Spoiler Industry Leaders

Magna International Inc.

Aisin Seiki Co., Ltd.

Polytec Holdings AG

OPMOBILITY SE

SMP Deutschland GmbH (Samvardhana Motherson)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: MG Motors introduced the MG7, a premium sedan, in Turkey. This model has advanced features such as a 360-degree camera, a 9-speaker BOSE sound system, an electrically retractable panoramic glass roof, and an active spoiler.

- November 2024: Hyundai introduced a rear spoiler and a fresh color option to its updated Verna sedan. The new rear spoiler for all Verna variants will be included in the package.

- February 2024: Hyundai Motor Group rolled out its Active Air Skirt technology across various electric vehicle platforms, backed by a USD 50 million development initiative. This system activates automatically at speeds exceeding 80 km/h, enhancing aerodynamic efficiency. Additionally, it integrates with the rear spoiler for holistic airflow management.

Global Automotive Active Spoiler Market Report Scope

| ABS (Acrylonitrile Butadiene Styrene) |

| Carbon Fiber |

| Fiberglass |

| Sheet Metal |

| Others |

| Adjustable |

| Motorized |

| Hatchback |

| Sports Utility Vehicles (SUVs) |

| Multi-Purpose Vehicles (MPVs) |

| Sports Cars |

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Material Type | ABS (Acrylonitrile Butadiene Styrene) | |

| Carbon Fiber | ||

| Fiberglass | ||

| Sheet Metal | ||

| Others | ||

| By Type | Adjustable | |

| Motorized | ||

| By Vehicle Type | Hatchback | |

| Sports Utility Vehicles (SUVs) | ||

| Multi-Purpose Vehicles (MPVs) | ||

| Sports Cars | ||

| By Propulsion | Internal Combustion Engine (ICE) | |

| Battery Electric Vehicle (BEV) | ||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big will the global automotive spoiler market be by 2030?

It is projected to reach USD 6.34 billion by 2030, expanding at a 6.52% CAGR.

Which spoiler material is growing the fastest?

Carbon fiber is expanding at an 8.34% CAGR because premium OEMs value its light weight and structural performance.

Why are electric-vehicle makers adopting active spoilers?

Motorized units cut drag at highway speeds, adding measurable driving range without major battery changes.

Which region leads demand for spoilers?

Asia-Pacific holds 37.43% of 2024 revenue and will post the quickest 7.86% CAGR.

What is the main challenge limiting motorized spoiler rollout?

High component costs and reliability issues in dusty or icy climates slow mass-market adoption.

Page last updated on: