Automotive Closure Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

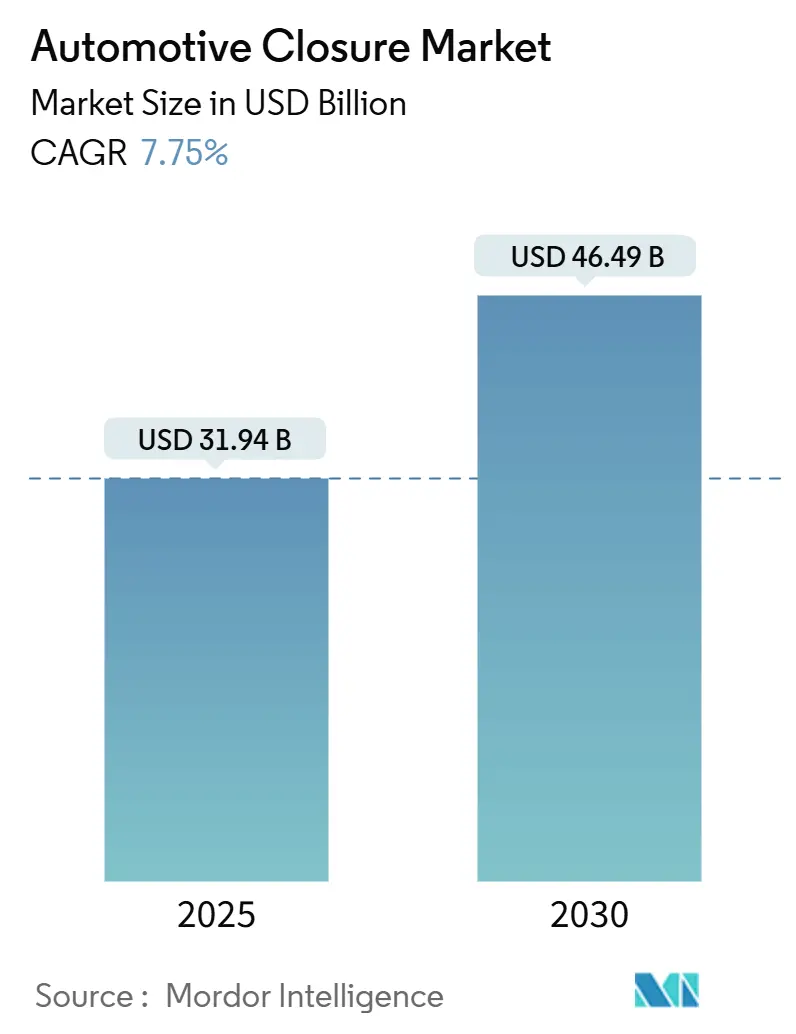

| Market Size (2025) | USD 31.94 Billion |

| Market Size (2030) | USD 46.49 Billion |

| Growth Rate (2025 - 2030) | 7.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Closure Market Analysis by Mordor Intelligence

The automotive closure market size is valued at USD 31.94 billion in 2025 and is projected to reach USD 46.49 billion by 2030, advancing at a 7.75% CAGR over the forecast period. Rapid electrification mandates, expanding integration of panoramic smart-glass roofs, and software-defined vehicle architectures that enable over-the-air monetization of comfort functions are redefining closure systems from mechanical parts into intelligent, connected interfaces. Tier-1 suppliers respond with vertically integrated hardware-plus-software portfolios, while OEM strategies center on lightweight, powered designs that satisfy side-impact regulations without sacrificing energy efficiency. Competitive intensity is increasing as sensor-rich door architectures for autonomous fleets invite electronics specialists into a field historically led by mechanical component makers.

Key Report Takeaways

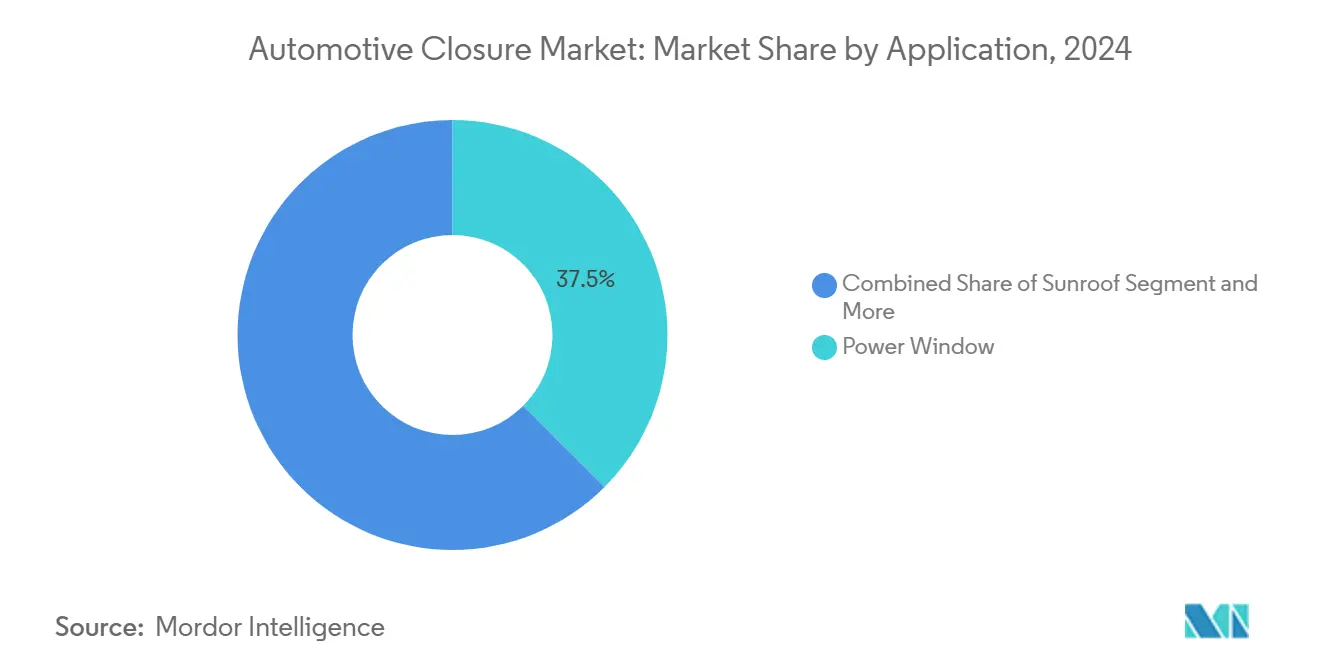

- By application, power windows led the automotive closure market with 37.51% of the share in 2024, while sunroofs are advancing at a 13.23% CAGR through 2030.

- By component, motor/actuator systems accounted for 32.08% of the automotive closure market in 2024; electronic control units (ECUs) represent the fastest-growing component, with an 11.37% CAGR to 2030.

- By type, powered systems commanded a 68.14% share of the automotive closure market in 2024 and are projected to expand at a 9.83% CAGR during the forecast period.

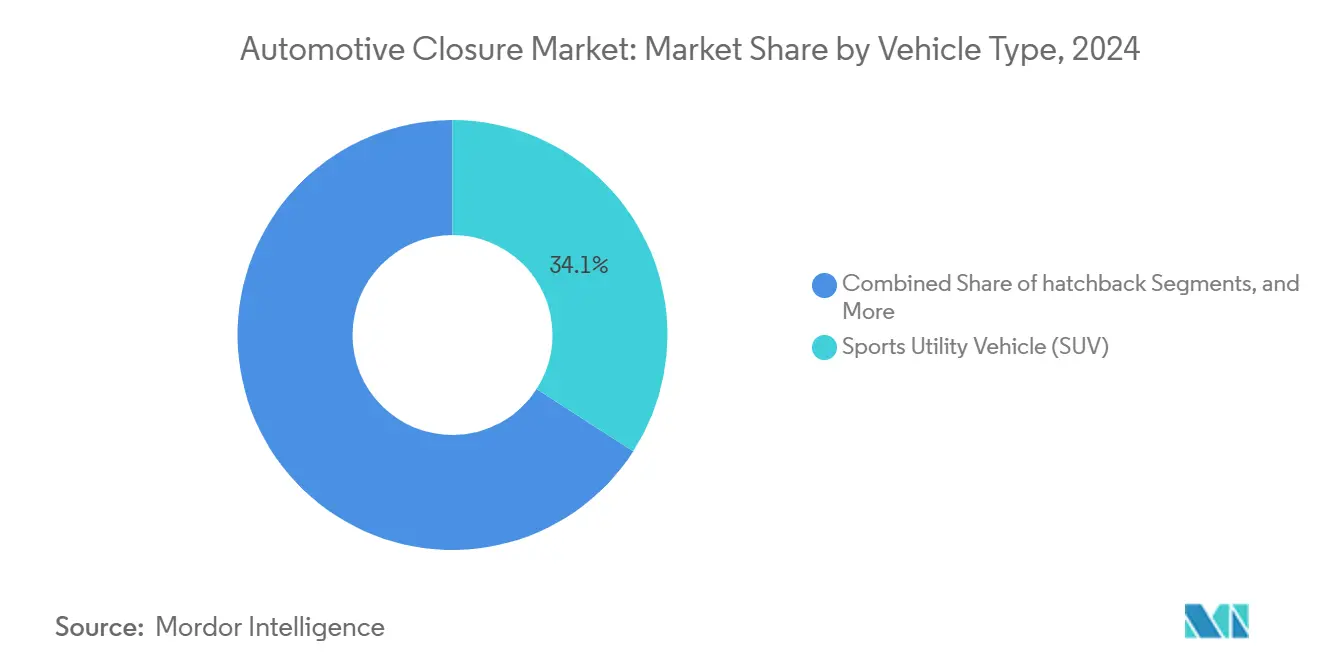

- By vehicle type, Sports Utility Vehicles (SUVs) captured a 34.12% share of the automotive closure market size in 2024, and are expected to grow at a CAGR of 12.58% through 2030.

- By distribution channel, OEM sales retained 79.06% of the automotive closure market in 2024. Yet, aftermarket demand is expanding at a 10.11% CAGR as retrofit kits add connected functionality to the older vehicle parc.

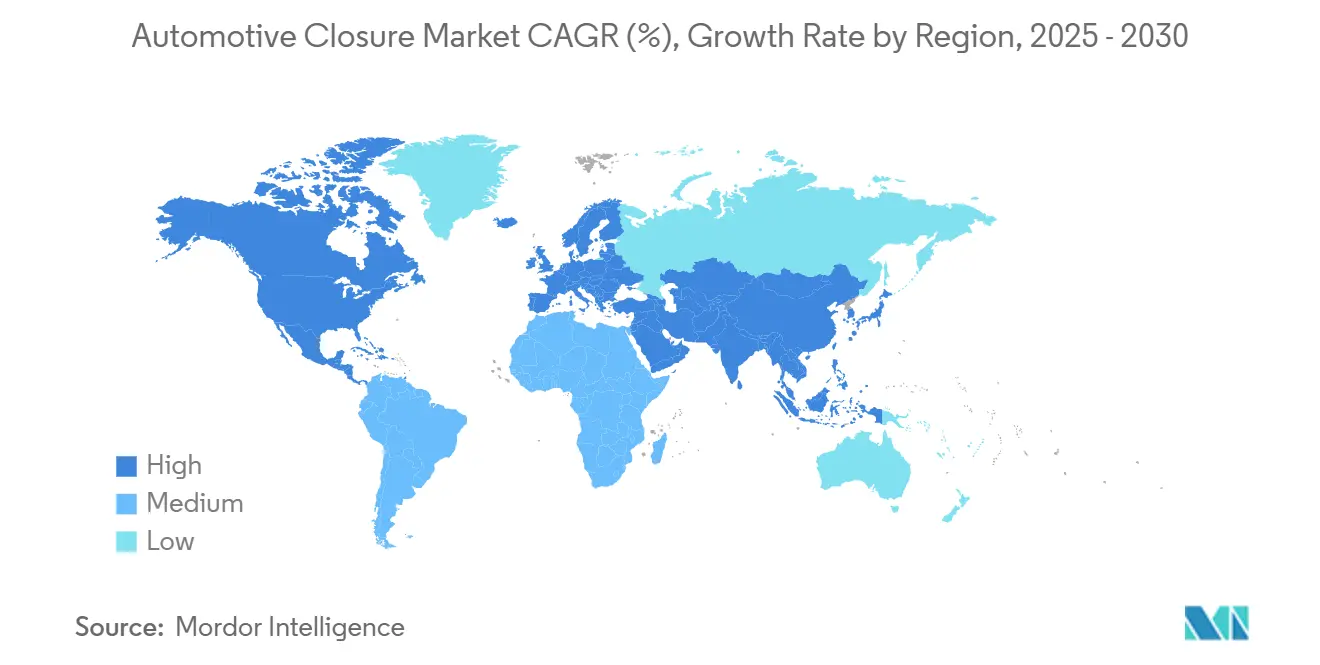

- By geography, Asia-Pacific held 41.07% share of the automotive closure market in 2024 and is forecast to surge at an 11.92% CAGR through 2030.

Global Automotive Closure Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Electrification Driving Demand for Lightweight Powered Closures | +1.8% | Global, with Asia-Pacific and EU leading adoption | Medium term (2-4 years) |

| Growing Adoption of Panoramic Smart-Glass Sunroofs in Mass-Segment Vehicles | +0.9% | North America and EU premium segments, expanding to APAC | Short term (≤ 2 years) |

| Stricter Global Side-Impact and E-Latch Safety Regulations | +1.2% | Global, with EU and North America enforcement priority | Long term (≥ 4 years) |

| Software-Defined Vehicles Enabling OTA Up-Sell of Closure Comfort Functions | +0.7% | North America and EU early adoption, Asia-Pacific following | Medium term (2-4 years) |

| Sensor-Fusion Door Systems for Autonomous Ride-Hail Fleets | +0.6% | Urban centers in North America, EU, and China | Long term (≥ 4 years) |

| Emerging Circular-Economy Mandates Favouring Recyclable Thermoplastic Door Modules | +0.4% | EU primary, with North America regulatory development | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification Driving Demand for Lightweight Powered Closures

Electric vehicle architecture fundamentally reshapes closure system requirements, as automakers prioritize weight reduction to maximize battery range while integrating powered mechanisms that enhance aerodynamic sealing. Tesla's Model Y achieves weight reduction in door assemblies through aluminum-intensive construction and eliminates traditional mechanical linkages in favor of electronic actuators that respond to proximity sensors. This shift creates demand for 48-volt electrical systems that power closure motors without compromising 12-volt accessory circuits, though penetration remains limited in price-sensitive regions where infrastructure costs challenge adoption. The electrification mandate extends beyond premium segments, as mass-market EVs from BYD and Volkswagen integrate powered tailgates and sliding doors to differentiate value propositions. Regulatory influence through CAFE standards and EU CO2 targets accelerates lightweight closure adoption, as every kilogram saved in door assemblies translates to measurable range improvements that affect regulatory compliance and consumer acceptance.

Growing Adoption of Panoramic Smart-Glass Sunroofs in Mass-Segment Vehicles

Smart-glass sunroof technology migrates from luxury segments to mainstream vehicles as electrochromic glass costs decline and consumer preference shifts toward cabin transparency and perceived spaciousness. BMW's iX integrates panoramic smart-glass that transitions from transparent to opaque within 30 seconds, eliminating mechanical sunshades. This technology enables automakers to offer premium experiences in mid-tier vehicles, with Ford's Mustang Mach-E and Hyundai's Ioniq 5 featuring smart-glass options that previously appeared only in luxury segments. The mass-market adoption accelerates as suppliers like Gentex scale production and achieve cost parity with traditional tinted glass within 2-3 years. Consumer willingness to pay premiums for smart-glass features creates new revenue streams for OEMs, while the technology's integration with vehicle climate control systems improves energy efficiency metrics crucial for electric vehicle range optimization.

Stricter Global Side-Impact and E-Latch Safety Regulations

Regulatory frameworks increasingly mandate electronic latch systems that ensure door integrity during side-impact collisions, with FMVSS 214 and Euro NCAP protocols establishing performance thresholds that mechanical systems cannot consistently achieve. The UNECE R11 regulation requires e-latch systems to maintain structural integrity at impact forces exceeding 18,000 Newtons, driving adoption of reinforced electronic actuators with backup power systems[1]"Concerning the Adoption of Uniform Technical Prescriptions for Wheeled Vehicles, Equipment and Parts which can be fitted and/or be used on Wheeled Vehicles and the Conditions for Reciprocal Recognition of Approvals Granted on the Basis of these Prescriptions," UNECE, unece.org. China's C-NCAP Door Opening Warning (DOW) requirements mandate sensor-based detection of approaching vehicles or cyclists before door release, creating demand for radar and camera-equipped closure systems that integrate with vehicle safety networks. These regulations extend beyond passenger vehicles to commercial fleets, where liability concerns accelerate the adoption of automated safety systems. Compliance frameworks like ISO 26262 for functional safety require extensive validation testing that increases development costs but creates competitive moats for suppliers with established certification capabilities, while smaller players struggle to meet regulatory requirements within acceptable timeframes.

Software-Defined Vehicles Enabling OTA Up-Sell of Closure Comfort Functions

Vehicle software architectures enable automakers to monetize closure features through over-the-air updates, transforming one-time hardware sales into recurring revenue streams that extend throughout vehicle lifecycles. Mercedes-EQS owners can purchase "Comfort Closing" functionality, which adds soft-close mechanisms and personalized entry sequences through software activation of existing Mercedes-Benz hardware. This model requires closure suppliers to embed advanced capabilities in base-level systems while allowing OEMs to unlock features based on customer preferences and willingness to pay. The approach creates new competitive dynamics where hardware differentiation matters less than software ecosystem integration and user experience design. Tesla's strategy of enabling dog mode and camp mode through closure system integration demonstrates how software-defined features create customer loyalty and generate post-purchase revenue. At the same time, traditional automakers struggle to replicate these capabilities due to legacy system constraints and dealer channel conflicts.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material Volatility for High-Grade Aluminum and Smart Glass | -0.8% | Global, with particular impact on cost-sensitive Asia-Pacific markets | Short term (≤ 2 years) |

| Cyber-Security Certification Costs for Connected E-Latch ECUs | -0.5% | North America and EU regulatory markets primarily | Medium term (2-4 years) |

| Short-Term OEM Cap-Ex Deferrals Amid BEV Programme Delays | -0.6% | Global, especially in Asia-Pacific and North America | Short term (≤ 2 years) |

| Limited 48-V Architecture Penetration in Price-Sensitive Regions | -0.4% | Asia-Pacific emerging markets, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Volatility for High-Grade Aluminum and Smart Glass

Aluminum prices surged 10%[2]"2024 Aluminum Prices in Review," Metal Miner, oilprice.com in 2024 due to Chinese production constraints and energy costs, directly impacting closure system economics as high-grade alloys represent 40-60% of component costs in lightweight door assemblies. Smart-glass substrate costs increased as rare earth element supply chains faced disruption, particularly affecting electrochromic materials essential for premium sunroof applications. This volatility forces suppliers to implement dynamic pricing mechanisms and hedge strategies that compress margins and complicate long-term OEM contracts. Smaller suppliers lack the financial resources to weather price fluctuations, creating consolidation pressure that could reduce competitive intensity but increase supply chain concentration risks. Alternative materials like carbon fiber composites and advanced polymers offer potential substitutes. However, certification timelines and performance validation requirements limit near-term adoption in safety-critical applications where regulatory approval processes extend 2-3 years beyond material availability.

Cyber-Security Certification Costs for Connected E-Latch ECUs

Electronic control units in closure systems require cybersecurity certification under UNECE R155 and ISO 21434 standards, with validation costs reaching higher per ECU variant across different vehicle platforms. These requirements mandate secure boot processes, encrypted communication protocols, and intrusion detection capabilities that add 15-20% to component costs while extending development timelines by 12-18 months. Smaller suppliers struggle to absorb certification expenses across limited production volumes, creating competitive advantages for established players with resources to invest in cybersecurity infrastructure. The certification burden intensifies as closure systems integrate with vehicle networks and external connectivity, requiring ongoing security updates and monitoring capabilities that transform one-time hardware sales into continuous service obligations. Compliance frameworks vary across regions, with EU and North American standards leading global adoption. At the same time, Asia-Pacific markets develop parallel requirements that may create fragmentation and increase certification complexity for international suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Sunroofs Accelerate Premium Feature Migration

Power windows maintain a 37.51% share of the automotive closure market in 2024, reflecting their universal adoption across vehicle segments and established supply chain maturity, enabling cost-effective integration. However, sunroofs emerge as the fastest-growing application at 13.23% CAGR through 2030, driven by consumer preference for premium cabin experiences and automaker strategies to differentiate mid-tier offerings through panoramic glass systems. Tailgate applications benefit from SUV market expansion and automated loading convenience, while convertible roof systems remain niche but command premium pricing that sustains supplier interest. Side doors represent the most significant volume opportunity as electrification mandates powered mechanisms for aerodynamic sealing, though growth rates moderate due to market maturity.

Sliding door applications concentrate in commercial vehicle segments where loading efficiency drives adoption, particularly in last-mile delivery fleets, optimizing urban operations. Integrating smart-glass technology in sunroof applications creates new revenue streams as electrochromic systems command 40-50% price premiums over conventional glass while reducing cabin cooling loads that improve electric vehicle efficiency metrics. Regulatory influence through safety standards increasingly favors powered applications that provide consistent performance under emergency conditions. At the same time, manual systems face declining adoption as automation costs decrease and consumer expectations shift toward convenience features that enhance daily usability.

By Component: ECUs Drive Intelligence Integration

Motor/actuator systems accounted for a 32.08% share of the automotive closure market in 2024, reflecting their critical role in powered closure mechanisms and the mechanical complexity required for reliable operation across temperature extremes and duty cycles. Electronic control units accelerate at 11.37% CAGR through 2030, as the fastest-growing component, driven by software-defined vehicle architectures that require intelligent closure management and integration with vehicle safety systems. Switch components maintain steady demand through traditional interface requirements, while relay systems face displacement by solid-state alternatives that offer improved reliability and reduced electromagnetic interference.

Latch mechanisms undergo fundamental transformation as electronic systems replace mechanical designs to meet side-impact safety requirements and enable remote operation capabilities. The ECU growth trajectory reflects cybersecurity certification requirements under UNECE R155 that mandate secure communication protocols and intrusion detection capabilities, adding complexity but creating competitive differentiation for suppliers with advanced software capabilities. Component integration trends favor suppliers offering complete closure systems rather than individual parts, as automakers seek to reduce complexity and improve system-level optimization through single-source relationships that enable coordinated development and warranty coverage across interconnected subsystems.

By Type: Powered Systems Dominate Through Convenience Demand

Powered closure systems captured a 68.14% share of the automotive closure market in 2024 and will witness a 9.83% CAGR growth through 2030, reflecting consumer preference for convenience features and regulatory requirements for consistent performance in safety-critical applications. Manual systems retain relevance in cost-sensitive segments and commercial applications where simplicity and serviceability outweigh automation benefits. However, their market share continues declining as powered system costs decrease through scale economies. The powered segment benefits from electrification trends that integrate closure systems with vehicle energy management and enable features like soft-close mechanisms that enhance perceived quality.

Regulatory compliance factors increasingly favor powered systems that provide repeatable performance under emergency conditions. At the same time, manual alternatives face challenges in meeting side-impact safety requirements that demand precise timing and force application. The cost differential between powered and manual systems narrows as suppliers achieve scale economies and integrate electronic components across vehicle platforms, making automation accessible in previously price-sensitive segments where consumer willingness to pay for convenience features continues expanding through generational preference shifts toward technology-enabled experiences.

By Vehicle Type: SUVs Lead Growth Acceleration

Sport Utility Vehicles (SUVs) hold a 34.12% share of the automotive closure market in 2024, driven by consumer preference for higher seating positions and cargo accessibility that benefits from powered tailgate and sliding door systems. SUVs are set to dominate as the fastest-growing segment, boasting a robust CAGR of 12.58% through 2030, reflecting automaker strategies to maximize electric vehicle range through aerodynamic closure designs and lightweight construction that reduces overall vehicle mass. Hatchback applications maintain steady demand in compact segments where cost sensitivity limits powered feature adoption, while sedan markets face declining volumes as consumer preferences shift toward utility vehicles.

MPV and pickup truck segments benefit from commercial applications where automated closure systems improve loading efficiency and reduce operator fatigue in high-duty-cycle operations. Van applications concentrate in last-mile delivery fleets where sliding door automation enhances urban maneuverability and package handling efficiency. The EV-focused growth creates opportunities for suppliers offering integrated solutions that combine closure functionality with battery thermal management and aerodynamic optimization, while traditional mechanical systems face displacement by electronic alternatives that enable precise control over sealing forces and energy consumption patterns crucial for electric vehicle efficiency optimization.

By Distribution Channel: Aftermarket Gains Through Vehicle Longevity

Original equipment manufacturer (OEM) channels hold a 79.06% share of the automotive closure market in 2024, reflecting the integrated nature of closure systems and automaker preferences for single-source supplier relationships that enable coordinated development and warranty coverage. However, aftermarket channels accelerate at 10.11% CAGR through 2030, as vehicle longevity increases and retrofit opportunities emerge for connected closure upgrades that add convenience features to existing vehicles. The aftermarket growth benefits from consumer willingness to upgrade manual systems to powered alternatives and the availability of universal retrofit kits that enable feature migration across vehicle platforms.

Service channel dynamics favor suppliers with established dealer networks and technical support capabilities, while direct-to-consumer sales remain limited by installation complexity and warranty considerations. The OEM dominance reflects regulatory requirements for safety-critical components that mandate original equipment specifications and certification compliance, though aftermarket opportunities expand in non-safety applications like convenience features and aesthetic upgrades. Distribution strategies increasingly emphasize digital channels and direct customer engagement as vehicle connectivity enables remote diagnostics and predictive maintenance that create service revenue opportunities throughout vehicle lifecycles.

Geography Analysis

Asia-Pacific captured 41.07% of the automotive closure market in 2024, propelled by a rise in electric car sales in China by almost 40% year-on-year in 2024[3]"Trends in electric car markets," IEA, iea.org and India’s capacity expansions under production-linked incentives. Japan’s keiretsu supply chains accelerate ECU innovation, although domestic volumes plateau. South Korea complements this with advanced semiconductor capability, ensuring local OEMs such as Hyundai benefit from tight sensor-software integration.

North America ranked second and is characterized by high-margin pickup and SUV models that frequently bundle powered tailgates and panoramic roofs. U.S. FMVSS side-impact protocols incentivize electronic latches, and California’s ZEV regulations encourage lightweight door modules that extend range. Mexico’s near-shoring wave attracts closure manufacturers looking to de-risk Asian supply chains; six new actuator lines are scheduled to come online by 2026, primarily feeding the United States assembly plants.

Europe keeps its competitive edge through premium marques focused on technology differentiation. German OEMs spearhead over-the-air monetization models, enabling pay-per-use soft-close features. EU circular-economy directives already influence material choices, with thermoplastic door skins holding a significant share in 2024. Eastern European countries provide cost-effective labor, but rising energy prices and geopolitical uncertainties weigh on long-term investment decisions. Meanwhile, regulatory harmonization under UNECE allows suppliers to scale compliant ECUs across multiple regions.

Competitive Landscape

The automotive closure market is dominated by the top five suppliers, holding a significant share. Brose, Magna, and Continental cement leadership by controlling everything from latch motors to embedded firmware, offering one-stop solutions that de-risk OEM sourcing. Continental’s recent contract with BMW for R155-compliant e-latches underscores the value of cybersecurity expertise in award decisions.

Mergers and acquisitions continue. Brose’s takeover of Preh Car Connect adds radar and gesture-control IP vital for autonomous fleet doors. Meanwhile, electronics giants like Bosch and Denso are leveraging ADAS sensor know-how to design integrated door modules capable of object detection and adaptive opening angles. To stay relevant, smaller players respond by specializing in retrofit kits or niche materials such as recycled thermoplastic seals.

Regulatory compliance under UNECE R155 elevates certification costs, favoring large players with dedicated cybersecurity labs. As OTA update frequency rises, lifetime service contracts emerge, altering revenue mix toward subscription models and creating ongoing supplier-OEM engagement. Circular-economy mandates add another competitive layer: suppliers capable of validating recycled content without compromising crash performance gain an edge in European RFQs.

Automotive Closure Industry Leaders

-

Magna International Inc.

-

Continental AG

-

Aisin Corporation

-

Brose Fahrzeugteile SE and Co. KG

-

GESTAMP SERVICIOS, S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Brose Sitech acquired the Proseat Group, a German foam manufacturer, expanding its capabilities in automotive seating and closure systems.

- May 2025: Aisin showcased its Integrated Electric Drive Unit (Xin1) at the Automotive Engineering Exposition 2025, aiming to improve energy efficiency and packaging for electric vehicles.

Global Automotive Closure Market Report Scope

| Power Window |

| Sunroof |

| Tailgate |

| Convertible Roof |

| Sliding Door |

| Side Door |

| Switch |

| ECU |

| Latch |

| Motor/Actuator |

| Relay |

| Manual |

| Powered |

| Hatchback |

| Sedan |

| Sport Utility Vehicles (SUVs) |

| Multi-Purpose Vehicles (MPVs) |

| Pickup-Trucks |

| Vans |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Power Window | |

| Sunroof | ||

| Tailgate | ||

| Convertible Roof | ||

| Sliding Door | ||

| Side Door | ||

| By Component | Switch | |

| ECU | ||

| Latch | ||

| Motor/Actuator | ||

| Relay | ||

| By Type | Manual | |

| Powered | ||

| By Vehicle Type | Hatchback | |

| Sedan | ||

| Sport Utility Vehicles (SUVs) | ||

| Multi-Purpose Vehicles (MPVs) | ||

| Pickup-Trucks | ||

| Vans | ||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Which application segment is growing the fastest?

Sunroof systems are the fastest-growing application, advancing at a 13.23% CAGR as smart-glass costs decline.

Why are ECUs gaining a larger share of closure system costs?

Software-defined vehicles require secure, intelligent ECUs to manage powered doors and enable OTA upgrades, driving an 11.37% CAGR for this component.

How do stricter safety regulations affect closure designs?

UNECE R11 and U.S. FMVSS mandates push adoption of electronic latches that maintain integrity during side impacts, accelerating the shift from mechanical to powered systems.

Which region leads market share and growth?

Asia-Pacific holds 41.07% of revenue and is also the fastest-growing region at an 11.92% CAGR due to China’s EV boom and India’s manufacturing incentives.

What opportunities exist in the aftermarket?

Retrofit kits for powered windows, tailgates, and connected features are expanding at a 10.11% CAGR as vehicles stay on the road longer and owners seek modern conveniences.

Page last updated on: