Automotive Suspension System Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

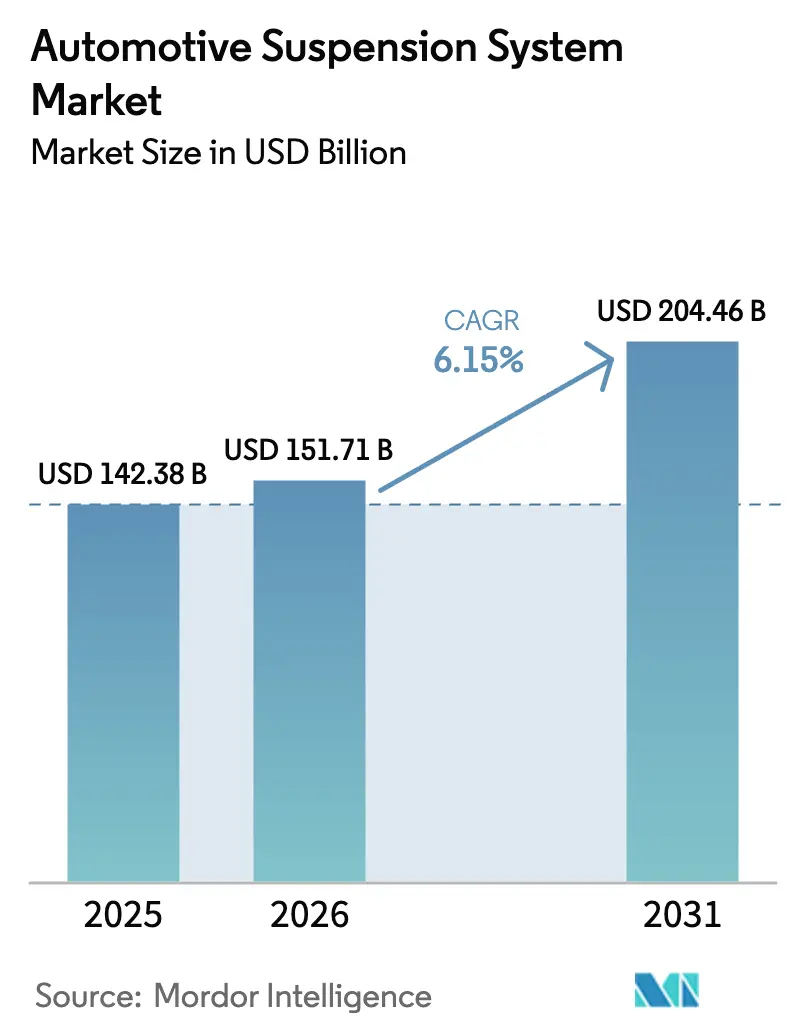

| Market Size (2026) | USD 151.71 Billion |

| Market Size (2031) | USD 204.46 Billion |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Suspension System Market Analysis by Mordor Intelligence

The automotive suspension system market size is expected to grow from USD 142.38 billion in 2025 to USD 151.71 billion in 2026 and is forecast to reach USD 204.46 billion by 2031, advancing at a 6.15% CAGR during the forecast period (2026-2031), as electrification and software-defined vehicle architectures reshape chassis design priorities. Demand is shifting from ride comfort alone toward digitally coordinated damping that feeds data to advanced driver-assistance systems, satisfying UN R171 lane-keeping response windows while improving energy efficiency in battery-electric vehicles. The OEM integration of suspension control units with centralized domain controllers is driving a surge in demand for sensors and ECUs. At the same time, subscription-based over-the-air unlocks are transforming adaptive damping into recurring revenue streams. The Asia-Pacific region emerged as the dominant contributor to revenue. However, the Middle East and Africa are experiencing the fastest growth, driven by Saudi Arabia's significant investment in Lucid. The industry's component mix is increasingly favoring electronic hardware. Moreover, there's a notable shift from traditional MacPherson struts to multi-link geometries, facilitating independent wheel control in dual-motor electric vehicles (EVs).

Key Report Takeaways

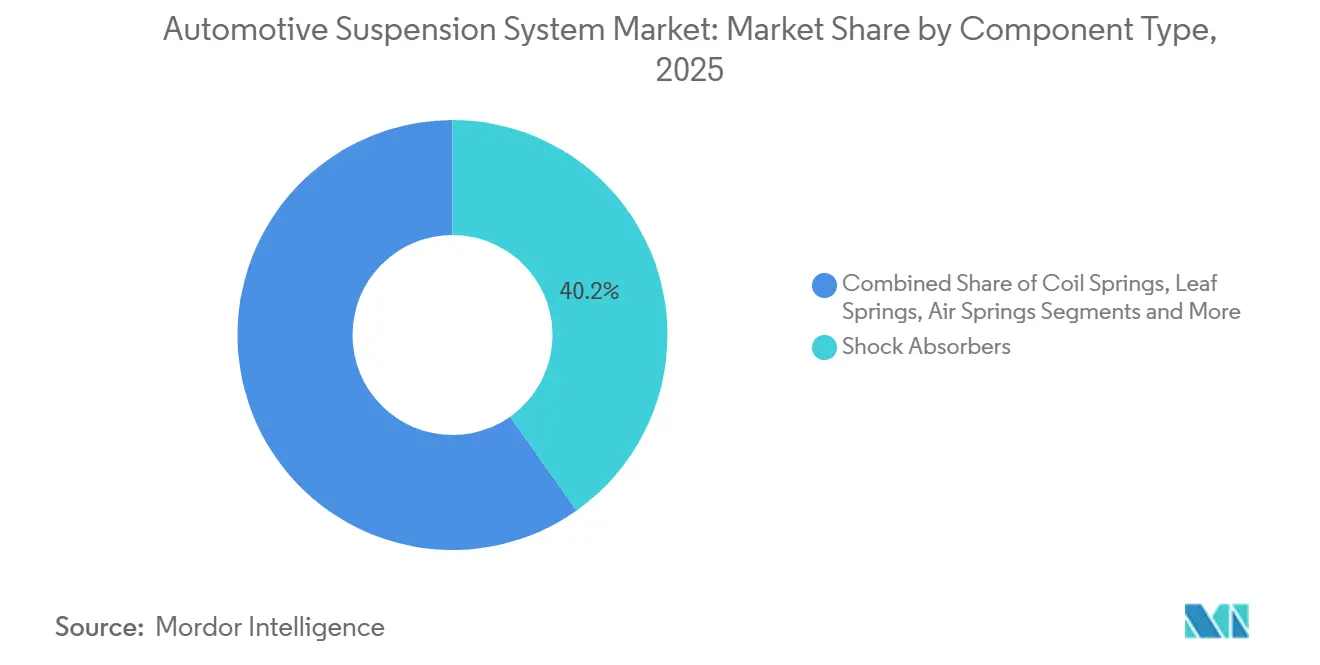

- By component type, shock absorbers held 40.21% of the automotive suspension system market share in 2025, while electronic control units and sensors are projected to expand at a 9.22% CAGR through 2031.

- By suspension system type, passive systems accounted for 64.32% of the automotive suspension systems market share in 2025; semi-active systems are forecast to grow at an 8.74% CAGR through 2031.

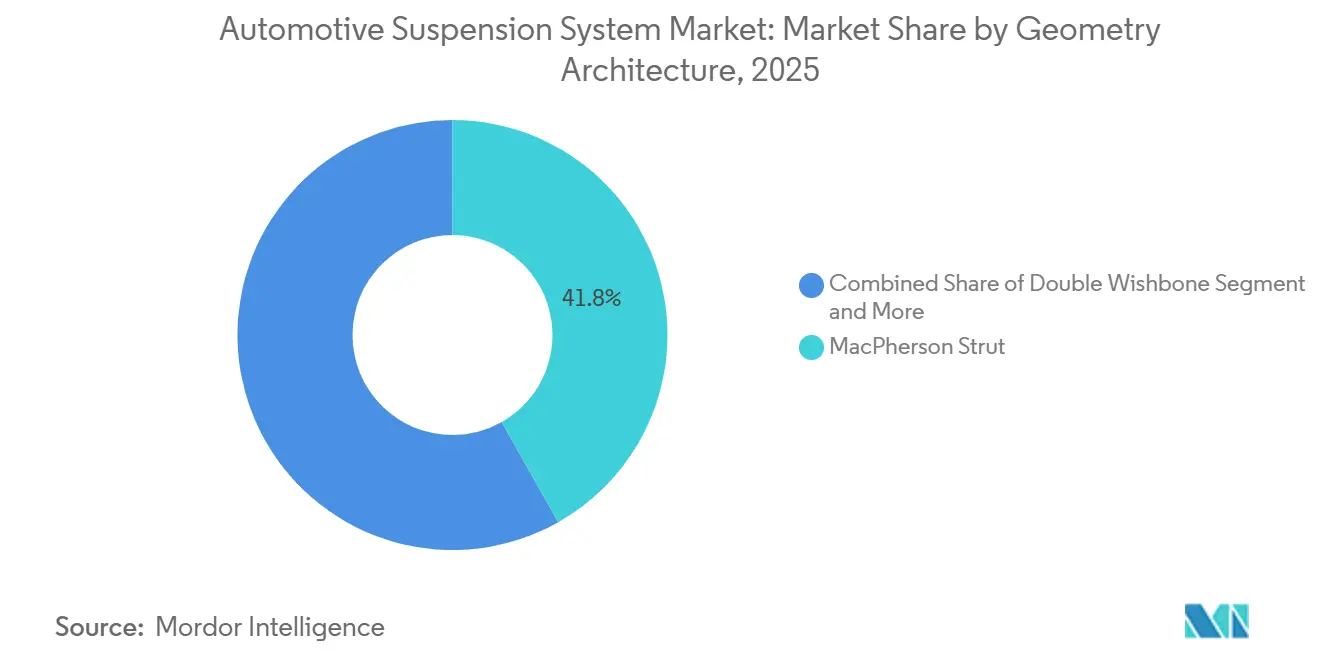

- By geometry, MacPherson strut layouts dominated the automotive suspension systems market, accounting for a 41.82% share in 2025; multi-link architectures are projected to grow at an 8.08% CAGR over the forecast period.

- By vehicle type, passenger cars accounted for 58.92% of the automotive suspension system market share in 2025. Additionally, electric passenger vehicles are expected to advance at a 10.71% CAGR during 2026–2031.

- By sales channel, OEM shipments accounted for 73.44% of the automotive suspension system market share in 2025, and the aftermarket segment is expected to grow at a 7.64% CAGR through 2031.

- By propulsion, ICE vehicles comprised 85.23% of the automotive suspension system market share in 2025, while electric and hybrid vehicles are projected to register a 14.89% CAGR through 2031.

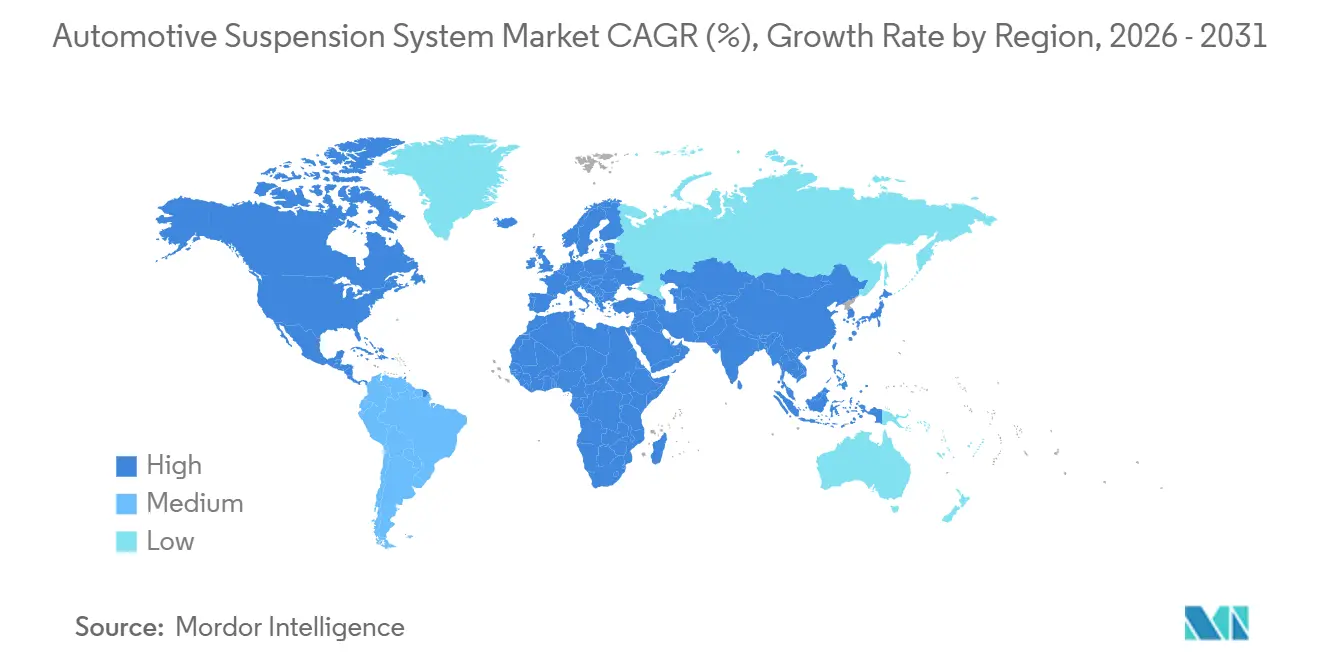

- By geography, the Asia-Pacific region led with 48.96% of the automotive suspension system market share in 2025, and the Middle East and Africa are anticipated to post the fastest regional growth at a 7.65% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Suspension System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification-Driven Chassis Redesign | +1.8% | Asia-Pacific core (China, South Korea), spill-over to North America and Europe | Long term (≥4 years) |

| ADAS-Linked Chassis Safety Push | +1.3% | Europe (UN R171, EU 2019/2144), North America (NHTSA NCAP updates) | Short term (≤2 years) |

| Rising Demand for Ride Comfort & Handling | +1.2% | Global, with premium-segment concentration in North America, Europe, and China | Medium term (2–4 years) |

| Rapid SUV & Premium Sales in Emerging Markets | +0.9% | India, Southeast Asia, Middle East | Medium term (2–4 years) |

| OTA Upgrades Unlock Active Suspension | +0.7% | North America, Europe, China (premium OEMs) | Short term (≤2 years) |

| 3D-Printed Composite Parts Cut Tooling Costs | +0.3% | North America (prototyping hubs), Europe (motorsport-derived applications) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Electrification-Driven Lightweight Adaptive Suspensions

Mahindra's BE 6e SUV, equipped with die-cast aluminum lower arms, enhances isolation indices on India's rugged roads. ZF's sMOTION, integrating air springs with active anti-roll bars, reduces mass compared to traditional steel coil counterparts, allowing electric vehicles to regain lost driving range. The European Commission's LEVA program has endorsed a 3D-printed thermoplastic composite arm, which is lighter than its forged steel counterpart and meets ECE crash standards. Toyota's bZ4X, using finite element analysis, has achieved weight reduction through a hollow stabilizer bar. Following this trend, Hendrickson's PRIMAAX EX has successfully reduced axle weight in electric delivery vans, a move that commercial fleets have echoed.

Regulatory Push for ADAS-Linked Chassis Safety

In Europe, UN R171 mandates lane-keeping and subtly advocates semi-active damping, as passive systems struggle to stabilize lateral loads within a crucial time window [1]“Regulation No. 171,” United Nations Economic Commission for Europe, unece.org. Continental observed a significant reduction in lane-departure incidents with the installation of electronically controlled dampers. The EU regulation 2019/2144 emphasizes the importance of stable tire contact during emergency braking. In response, ZF’s sMOTION technology pre-compresses the dampers before autonomous braking is activated. Meanwhile, NHTSA's 2025 initiative aims to certify automatic emergency braking systems for higher speeds, thereby amplifying the U.S. market's appetite for active safety features. Additionally, ISO 26262 has designated suspension ECUs as safety-critical, a move that extends development cycles but also underscores the importance of certified suppliers.

Increasing Demand for Enhanced Ride Comfort and Handling

Genesis introduced downloadable damping maps on its GV60, allowing buyers to subscribe to the "Dynamic Plus" package, turning suspension tuning into a software revenue stream [2]“GV60 Software Revenues,” Hyundai Motor Company, hyundai.com. Continental's MK C2 controller integrates ABS data with suspension-stroke feedback to enhance aquaplaning response and improve wet stopping performance [3]“MK C2 Technical Release,” Continental AG, continental.com. BMW's Neue Klasse RFQ requires advanced Ethernet links to enable predictive damping algorithms to utilize camera feeds in real-time. Consequently, multi-link rear setups, offering independent toe and camber control, are replacing traditional torsion beams in battery-heavy sedans, aligning performance goals with luxury-segment standards.

Rapid SUV and Premium-Vehicle Sales in Emerging Economies

India has experienced a significant rise in SUV registrations, with a notable increase in the adoption of independent rear suspension. Tata's Harrier facelift transitioned to a multi-link geometry, reducing body roll while meeting ground clearance requirements. In Saudi Arabia, a major venture with Lucid is set to assemble air-suspended sedans annually, enhancing regional capacity for Continental and ZF modules. In the Gulf, luxury models increasingly rely on air springs, as high ambient temperatures can cause steel coils to sag. In Southeast Asia, the premium segment has grown, supported by local assembly initiatives of BMW and Mercedes-Benz vehicles featuring adaptive damping, which helps avoid tariffs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Smart Suspension | -0.9% | Global, acute in price-sensitive segments (India, Southeast Asia, Latin America) | Medium term (2–4 years) |

| Reliability Issues in Harsh Conditions | -0.6% | Middle East, Africa, Rural India, Northern North America | Long term (≥4 years) |

| Cybersecurity and Safety Compliance Burden | -0.4% | Europe (UN R155, ISO 26262), North America (NHTSA cybersecurity framework) | Short term (≤2 years) |

| MR-Fluid and Sensor Supply Bottlenecks | -0.4% | Global, concentrated supplier base (China, Japan, U.S.) | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Upfront and Lifecycle Cost of Smart Suspension Architectures

Volkswagen, facing higher vehicle build costs due to semi-active hardware, has limited adaptive damping to higher-priced Tiguan trims. This strategic move safeguards the company's margins. While air-spring compressors require replacement after a certain distance, overshadowing the lifetime costs of coil springs, India sees a higher failure rate in semi-active dampers within a specific distance. The issue arises from solenoid valves clogging with ferrous dust. In contrast, passive units report a significantly lower failure rate. Although subscription pricing eases entry costs, only a small percentage of price-sensitive buyers continue paying after the free trial period.

Reliability and Maintenance Challenges in Harsh Conditions

Magnetorheological dampers experience a significant reduction in lifespan when ambient temperatures exceed a threshold, primarily due to accelerated seal wear caused by fluid oxidation. ZF issued a recall for sMOTION units in Canada and Scandinavia, responding to cracked air-spring bellows at extremely low temperatures. Following a notable failure rate of suspension ECUs in Southeast Asia—attributed to salt-fog ingress—Toyota enhanced the bZ4X connector seals to a higher standard. The challenge is further exacerbated by a shortage of diagnostic tools, with only a small percentage of independent workshops in India equipped to recalibrate semi-active dampers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Sensors and Control Units Accelerate Value Creation

The automotive suspension system market for electronic control units and sensors is expanding at a 9.22% CAGR through 2031, driven by the 8–12 accelerometers and multiple ride-height sensors required per vehicle. Shock absorbers still accounted for 40.21% of 2025 revenue, but monotube upgrades, priced at USD 55–75, are holding their value even as volumes shift toward adaptive variants. Changes in the mix now prioritize monotube heat-dissipation efficiency, a key requirement for regenerative-braking duty cycles in electric vehicles (EVs). While shipments of coil and leaf springs remained stable, air-spring modules for Class 8 trucks have increased their share of North American axles.

Innovations on the horizon include thermoplastic-elastomer bushings, which maintain consistent stiffness across a wide temperature range, leading to a significant reduction in NVH complaints. Magnetorheological engine mounts, which utilize the same MR fluid as dampers, are isolating powertrain shocks in hybrids. This development is set to increase the content per vehicle for suppliers like Parker. Chinese monotube suppliers have captured a notable share of Asia-Pacific absorber revenue by pricing themselves lower than their Japanese counterparts, while adhering to GB/T 21510 quality standards.

By Suspension System Type: Semi-Active Solutions Bridge Cost and Performance

Passive designs accounted for 64.32% of the automotive suspension system market share in 2025, but are ceding share as semi-active content rises due to volume-driven cost reductions; Ford's decision to standardize continuously controlled damping across all F-150 Lightning models underscores a significant trend. The growing adoption of semi-active systems, with a CAGR of 8.74%, is elevating the role of electronic components in the automotive suspension market, while proprietary control algorithms further solidify supplier dominance. While active hydraulically driven systems hold a smaller share of the market, they're finding a niche in luxury EVs. For instance, in the Mercedes-Benz EQS, cabin tilt control effectively reduces perceived lateral forces.

Price sensitivity keeps passive systems in the sub-USD 25,000 market segment, especially given the steep ISO 26262 validation costs for electronics. Torsion beams, which constitute a significant portion of the global compact-car output, are facing a shift. This is mainly due to EU lane-keeping mandates that are pushing for the replacement of these setups with independent systems. There's a notable regional disparity: Europe shows higher adoption rates for semi-active systems than Asia-Pacific, highlighting differing consumer valuations of automotive refinement.

By Vehicle Type: Electrified Passenger Cars Impose New Design Constraints

Passenger cars accounted for 58.92% of the automotive suspension system market share in 2025, driven by the growth of electric variants at a 10.71% CAGR through 2031, as OEMs integrate adaptive damping to compensate for battery height and center-of-gravity shifts. Light commercial vehicles are transitioning from leaf springs to multi-link coils to comply with pedestrian safety regulations. Ford's Transit Custom has successfully improved unladen ride comfort. While heavy trucks represent a smaller share of units sold, they account for a significant share of component value. This is mainly due to Class 8 air-spring modules, which are engineered to support heavy axle loads.

Price segmentation in the market is distinctly defined. Vehicles in the lower price range predominantly feature passive MacPherson struts. For those in the mid-range, semi-active systems have become the norm. Meanwhile, premium cars are equipped with advanced active hydraulics. To compensate for a higher center of gravity compared to internal combustion engine sedans, EV sedans like Hyundai's Ioniq 6 have stiffer anti-roll bars. Furthermore, commercial vans are now incorporating air-leveling systems to optimize aerodynamics across varying payloads, as demonstrated by the improved drag performance of Mercedes-Benz's eSprinter.

By Geometry/Architecture: Multi-Link Assemblies Climb the Adoption Curve

MacPherson struts captured 41.82% of the automotive suspension system market share in 2025, thanks to integrated strut-tower packaging that saves up to USD 28 per corner. Yet, multi-link setups are expanding at an 8.08% CAGR through 2031, because they decouple toe and camber. Take Audi's e-tron GT, for instance, which showcases a negative camber under lateral load. While double-wishbones have long been a premium feature, they're ceding ground to optimized multi-links. These multi-links not only cut the ball-joint count but also reduce assembly time and warranty risks.

Entry-level cars still favor torsion beams, prioritizing cost over dynamic finesse. Yet, Hyundai's Elantra N opts for a multi-link rear suspension, ensuring it meets stability benchmarks. With platform electrification, the shift from traditional longitudinal powertrains to batteries offers newfound layout flexibility.

By Sales Channel: Digital Aftermarket Unlocks New Revenue Pools

OEM lines retained 73.44% of the automotive suspension system market share in 2025, as vertically integrated plants, such as ZF’s in-house line at Volkswagen Zwickau, shaved logistics costs. The aftermarket, however, is growing at a 7.64% CAGR due to vehicle aging in North America and Europe, where the average fleet age has reached 12.6 years. Online platforms report significant growth in coil-overs, underscoring the strength of digital sales.

Remanufactured semi-active dampers are gaining traction: a suspension system refurbishes units at a lower cost than the original price while still delivering high performance. Meanwhile, a company is pioneering a hybrid approach with its OTA unlocks, charging a monthly fee for adaptive damping, all without the need to ship hardware, thus carving out a new service revenue stream.

By Propulsion: Battery-Electric Vehicles Catalyze Specialization

In 2025, internal combustion engine vehicles commanded a dominant 85.23% share of the automotive suspension system market. Meanwhile, electrified vehicles, equipped with 400–700 kg battery packs, are turning to specialized damping solutions. The demand for electric and hybrid cars is set to grow at an impressive 14.89% CAGR, extending through 2031. Highlighting this trend, BYD's Seal employs frequency-selective dampers to counteract low-frequency body movements caused by the battery's weight. This is paired with a dual-motor torque vectoring system for superior roll control. Similarly, Tesla's revamped Model 3 features a cutting-edge air suspension that not only lowers the ride height but also boosts range by minimizing drag.

Hybrid systems introduce distinct challenges: Toyota's Crown Hybrid uses MR-fluid engine mounts that can stiffen rapidly to mitigate vibrations during engine start-stop. Given that regenerative braking significantly increases damper compression cycles, there's a need for upgraded seals and fluids. While internal combustion engine (ICE) programs continue to lead in volume, they undergo less frequent geometric redesigns; for instance, Ford's Mustang retains the MacPherson layout, making only minor adjustments to the spring rate.

Geography Analysis

The Asia-Pacific region accounted for 48.96% of the automotive suspension system market share in 2025, as China's light-vehicle production saw local OEMs, such as BYD, equipping their Seal sedans with adaptive dampers. In India, a booming SUV market led Tata to implement multi-link rear axles, which reduced body roll and aligned with benchmarks set by the Hyundai Tucson. To reduce unit labor costs, Japanese suppliers relocated absorber production to Thailand and Vietnam, resulting in a drop in Japan’s regional share. Highlighting the push for localization, Hyundai Mobis inaugurated a plant in Indonesia, aiming to produce suspension modules annually.

North America and Europe accounted for a significant portion of the turnover, with a noticeable tilt towards semi-active content. Ford’s F-150 Lightning set a precedent by making adaptive damping standard, achieving full penetration across its sales. ZF’s production line in Germany successfully delivered sMOTION units for BMW and Mercedes-Benz. Europe's lane-keeping regulations have driven the adoption of semi-active installations. Meanwhile, North America's aftermarket experienced a revenue boost, driven by the surge in e-commerce demand for adjustable coilovers. In Canada, frigid winters are prompting pickup buyers to opt for air-springs, ensuring optimal ground clearance.

The Middle East and Africa, although they held a smaller share of the 2025 volume, are pacing the global growth chart at a 7.65% CAGR through 2031. Saudi Arabia's Lucid joint venture plans to produce air-suspended cars annually, establishing new regional supply chains for Continental and ZF. In the UAE, luxury car demand skews heavily towards adaptive damping systems, a move aimed at combating the sweltering desert heat. While South Africa's power supply challenges led to a dip in car production, a weaker rand bolstered exports to Europe, seeing an uptick. In response to Egypt's high import tariffs, Tenneco is setting up a damper plant in the Suez zone. South America accounted for a small market share, with Argentina witnessing a surge after lifting caps on component imports.

Competitive Landscape

Market dynamics are evolving, distinguishing between vertically integrated Tier-1s, specialized actuator experts, and regionally-focused suppliers driven by cost. ZF and Continental dominate the semi-active revenue landscape. They achieve this by incorporating suspension ECUs with brake and stability functions into domain controllers, effectively reducing wiring mass. ZF’s sMOTION, now a standard feature in BMW and Mercedes-Benz models, utilizes crowd-sourced maps and high-rate sensor streams to pre-load dampers ahead of potholes, resulting in a significant reduction in vertical acceleration. Meanwhile, Multimatic’s TrueActive hydraulic actuators, capable of delivering high roll control in milliseconds, have found a niche with Aston Martin in the hypercar segment, where their unit cost is deemed negligible.

Chinese suppliers are reshaping the pricing landscape. BWI’s semi-active damper undercuts Continental's offering while boasting the prestigious ISO 26262 ASIL-D certification, making it a preferred choice for mid-tier EVs. In a strategic move, Continental invested significantly to acquire a majority stake in Jingwei Hirain to leverage its patent portfolio. Meanwhile, newcomers like Divergent Technologies, leveraging additive manufacturing, are revolutionizing the industry by reducing prototyping cycles with their 3D-printed suspension nodes, hinting at quicker hardware rollouts. Schaeffler’s innovative 48-volt ball-screw actuators not only promise substantial energy efficiency over traditional hydraulic pumps but also eliminate the need for the fluid reservoir found in older active-roll systems.

Automotive Suspension System Industry Leaders

ZF Friedrichshafen AG

Continental AG

Tenneco Inc.

KYB Corporation

Hitachi Astemo Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Tenneco finalized the sale of Öhlins Racing to Brembo for USD 405 million, combining performance braking and adaptive damping solutions for premium models.

- January 2025: Sona Comstar invested USD 4 million in ClearMotion to accelerate the commercial rollout of its proactive suspension technology.

- October 2024: Ams OSRAM showcased high-resolution position sensors critical for steer-by-wire and active suspension integration.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the automotive suspension system market as the value of all factory-installed and replacement assemblies, springs, dampers, linkages, bushings, sensors, and electronic control units that connect road wheels to the chassis across passenger cars, light and heavy commercial vehicles, and battery-electric models manufactured or sold in 2025. These assemblies are counted at ex-factory or retail invoice prices, depending on the sales channel we capture.

Scope does not include two-wheelers, motorsport, or purely aftermarket performance upgrade kits.

Segmentation Overview

- By Component Type

- Coil Springs

- Leaf Springs

- Air Springs

- Shock Absorbers

- Stabilizer / Anti-roll Bars

- Suspension Arms & Links

- Electronic Control Units and Sensors

- Other Components

- By Suspension System Type

- Passive Suspension

- Semi-Active Suspension

- Active Suspension

- By Geometry /Architecture

- MacPherson Strut

- Double Wishbone

- Multi-Link

- Torsion Beam / Twist Beam

- Other Geometries

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- By Sales Channel

- Original Equipment Manufacturer (OEM)

- Aftermarket

- By Propulsion

- Internal-Combustion-Engine Vehicles

- Electric & Hybrid Vehicles

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Aisa-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Turkey

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed tier-one engineering heads, chassis consultants, and regional parts distributors in Asia, Europe, and North America. Their inputs validated replacement cycles, semi-active penetration, and the price premiums OEMs pay for electronically controlled setups.

Desk Research

We screened open-source datasets such as UN Comtrade suspension part codes, OICA vehicle production tables, national vehicle-parc statistics, and SAE Mobility technical papers, which clarified material cost curves. Company 10-Ks and quarterly filings revealed average component revenue per vehicle, while regulatory portals (NHTSA, ACEA) signposted mandates shaping technology adoption. Paid repositories, D&B Hoovers for supplier financials and Dow Jones Factiva for news flow, provided hard numbers on plant capacity and pricing. Many other publications were also reviewed to round out context.

A second desktop pass matched association shipment tallies with region-level fitment rates gleaned from press releases and patent filings, letting us map average suspension content per vehicle class.

Market-Sizing & Forecasting

A blended top-down build converts 2025 vehicle production and parc data into potential suspension demand pools, which are then adjusted by modeled replacement intervals and aftermarket capture ratios. Bottom-up cross-checks, sampled OEM purchase prices multiplied by supplier volumes, fine-tune totals. Key variables include units per vehicle, semi-active uptake, electric vehicle share, regional mileage, and raw material trends. Forecasts to 2030 rely on multivariate regression linked to these drivers and scenario bands that primary respondents reviewed.

Data Validation & Update Cycle

Outputs pass a two-step peer review, variance thresholds trigger re-checks, and every figure is reconciled against new registrations and trade flows before annual refresh. Interim updates follow recalls or major regulatory shifts.

Why Mordor's Automotive Suspension System Market Baseline Commands Reliability

Published estimates often diverge because providers select different product mixes, ignore retrofit volumes, or freeze currency at outdated rates. By capturing both OEM fit and genuine aftermarket sales, while updating FX each quarter, our baseline stays current and complete.

Key gap drivers include narrower vehicle coverage, omission of electronic modules, optimistic ASP curves, and infrequent refresh cadences seen elsewhere.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 142.92 B (2025) | Mordor Intelligence | - |

| USD 46.6 B (2024) | Regional Consultancy A | Excludes aftermarket and heavy vehicles |

| USD 47.25 B (2024) | Global Consultancy B | Counts mechanical parts only; static FX |

| USD 53.10 B (2024) | Trade Journal C | Uses limited Asia sample; omits electronic content |

These contrasts show that Mordor's disciplined scoping, variable tracking, and yearly refresh deliver the most balanced, transparent baseline for decision-makers.

Key Questions Answered in the Report

What is the projected value of the automotive suspension system market in 2031?

The market is forecast to reach USD 204.46 billion by 2031.

How fast is the automotive suspension system market growing?

It is expanding at a 6.15% compound annual growth rate between 2026 and 2031.

Which suspension system type is gaining share the fastest?

Semi-active systems are advancing at an 8.74% CAGR through 2031.

How are electrification trends influencing suspension design?

Battery-electric vehicles require lighter adaptive components to offset pack mass and integrate real-time damping with energy-management software.

Page last updated on: