Automotive AC Compressor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

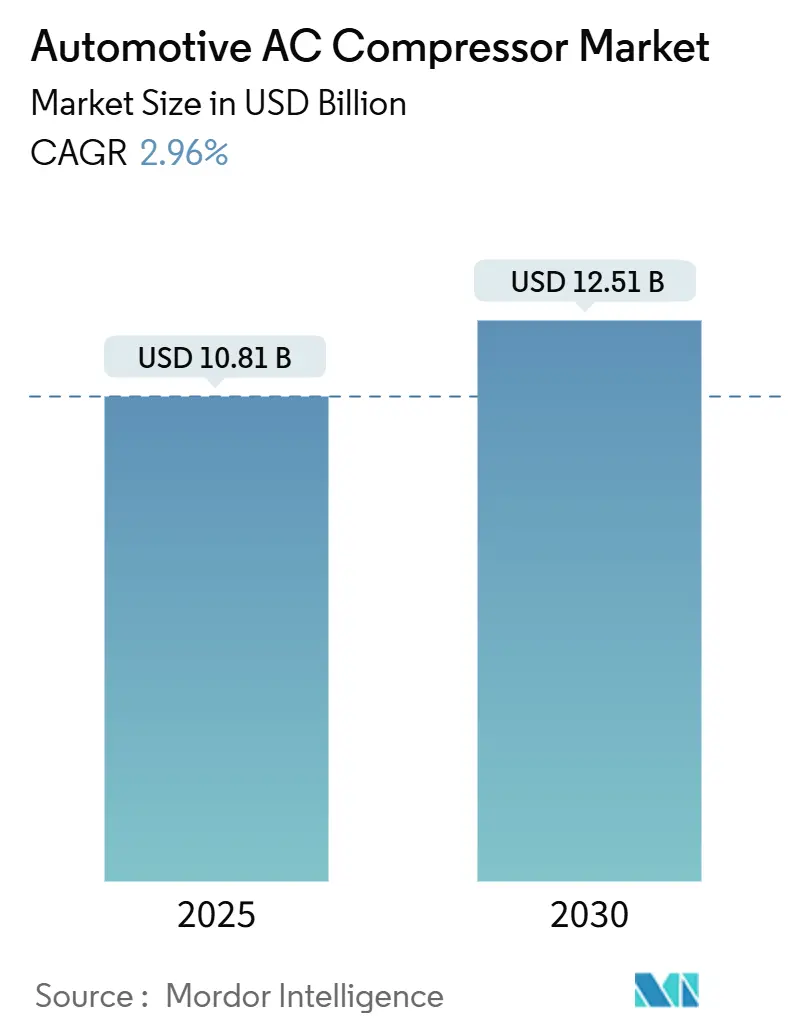

| Market Size (2025) | USD 10.81 Billion |

| Market Size (2030) | USD 12.51 Billion |

| Growth Rate (2025 - 2030) | 2.96% CAGR |

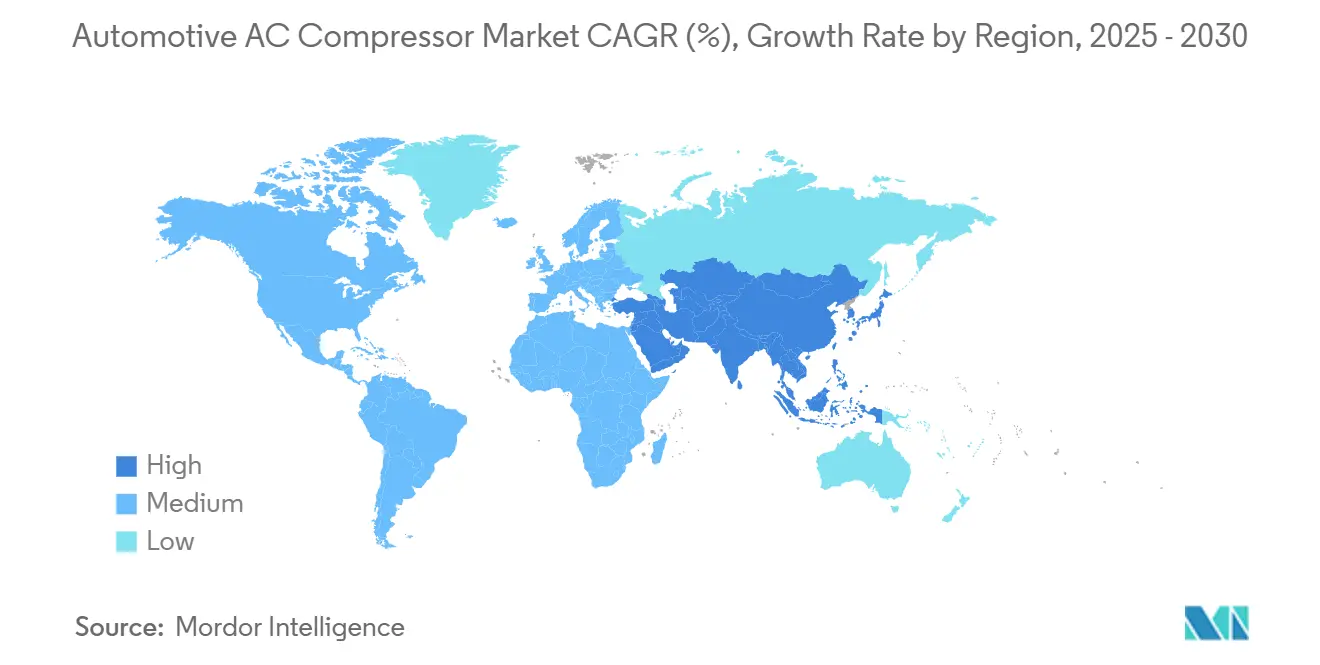

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

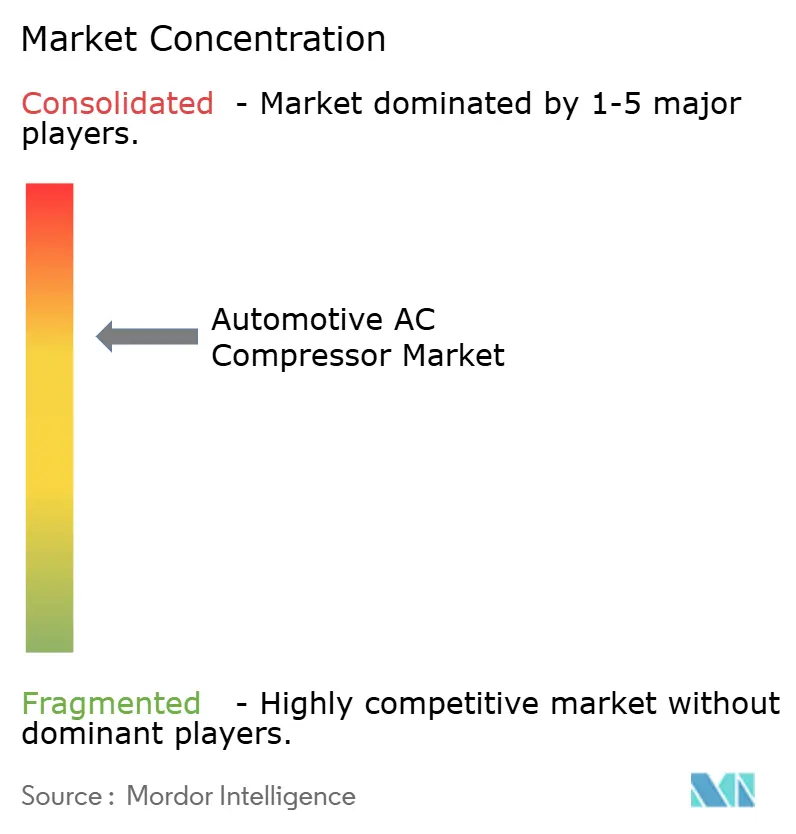

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive AC Compressor Market Analysis by Mordor Intelligence

The Automotive AC compressor market size stands at USD 10.81 billion in 2025 and is set to reach USD 12.51 billion by 2030, translating to a steady 2.96% CAGR. This headline growth hides a sharp technological pivot as electric-driven architectures displace belt-driven systems, a shift propelled by electrification mandates and the thermal complexity of battery electric vehicles (BEVs). Cooler cabin expectations, stricter fuel-efficiency rules and evolving refrigerant regulations collectively raise the performance bar, pushing variable-displacement and heat-pump-ready compressors from niche options into mainstream specifications. Suppliers that marry mechanical know-how with power-electronics competence capture premium margins, while those tied to legacy belt technology confront commoditization risks. At the same time, supply-chain fragility around rare-earth magnets and power semiconductors injects cost volatility, encouraging regional sourcing and materials innovation as strategic countermeasures.

Key Report Takeaways

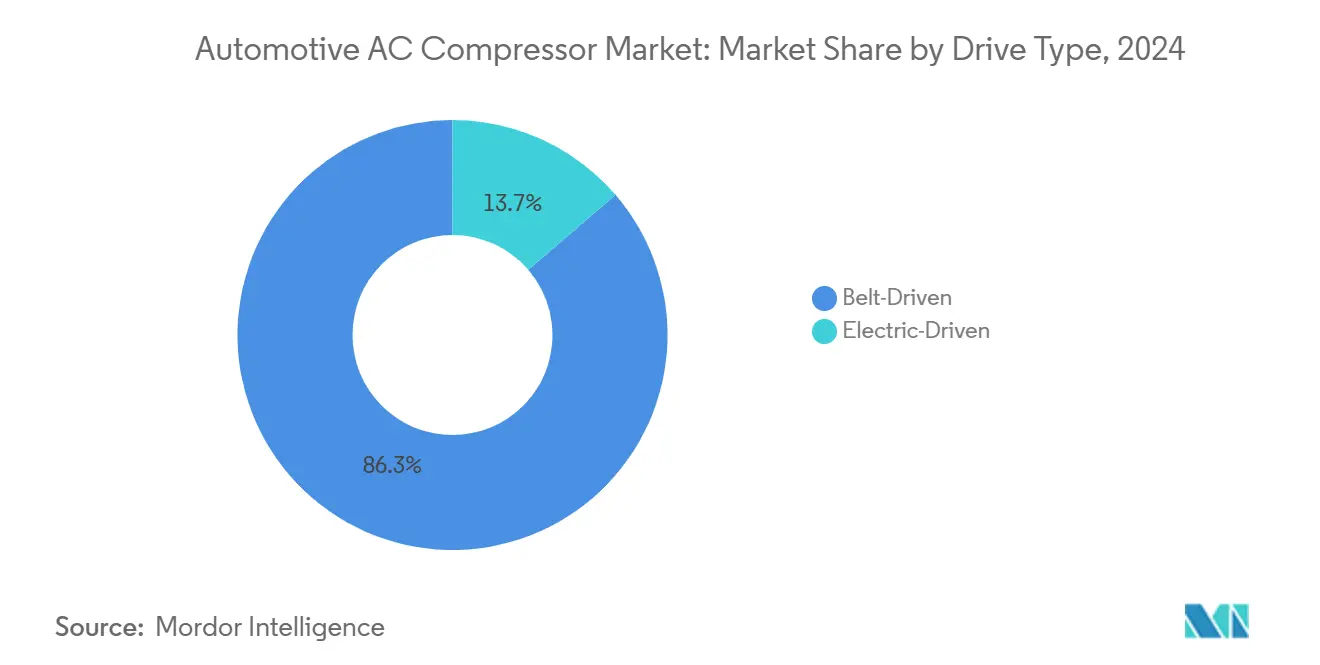

- By drive type, belt-driven units held 86.33% of the Automotive AC compressor market share in 2024, though electric-driven compressors posted the fastest expansion at a 4.22% CAGR through 2030.

- By design type, reciprocating products commanded 65.16% of the Automotive AC compressor market share in 2024, whereas rotary technology is on course for the highest 4.84% CAGR over the same horizon.

- By vehicle type, passenger cars contributed 72.44% of the Automotive AC compressor market share in 2024 and delivered the leading 3.16% CAGR to 2030.

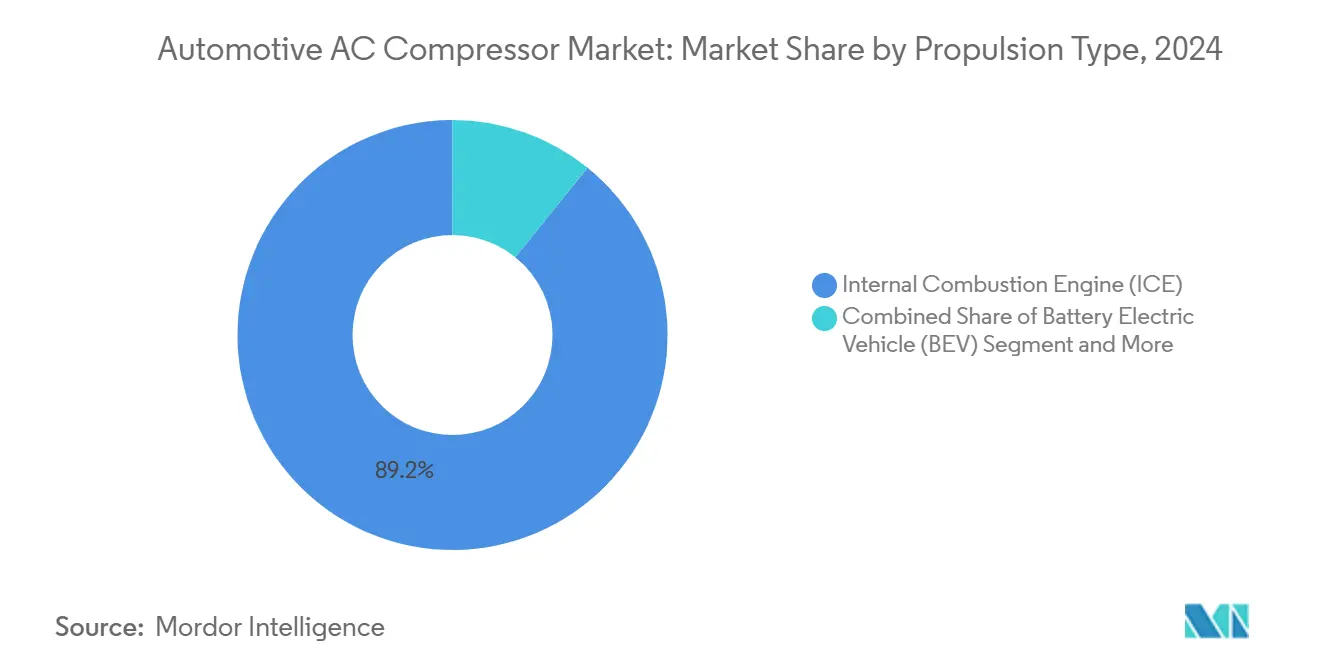

- By propulsion type, ICE platforms still represented 89.17% of the Automotive AC compressor market share in 2024, yet BEVs will accelerate at a 5.27% CAGR as electrification scales.

- By distribution channel, OEM integration accounted for 83.11% of the Automotive AC compressor market share in 2024 shipments and is forecast to register a 3.44% CAGR, reinforcing its dominance over aftermarket sales.

- By geography, Asia-Pacific controlled 47.25% of the Automotive AC compressor market share in 2024 and will widen its lead with a 3.68% CAGR through 2030.

Global Automotive AC Compressor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EV Adoption Drives E-Compressors | +0.8% | Global, led by China and EU | Long term (≥ 4 years) |

| Fuel Efficiency, CO2 Rules Impact Units | +0.6% | North America and EU, expanding to Asia-Pacific | Medium term (2–4 years) |

| Emerging Economies Boost Production | +0.5% | Asia-Pacific core, spill-over to South America | Medium term (2–4 years) |

| Consumers Seek Better Cabin Comfort | +0.4% | Global, strongest in developed markets | Short term (≤ 2 years) |

| EV Thermal Management Lifts Compressor Value | +0.3% | Global EV markets | Long term (≥ 4 years) |

| 48V Mild Hybrids Enable E-Compressors | +0.2% | Europe and North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid EV Adoption Driving Demand for Electric-Driven Compressors

Electrification eliminates belt-driven accessories, elevating the electric compressor from option to necessity in BEV thermal loops. Oil-less centrifugal and scroll architectures enable continuous operation during DC fast-charging, stabilizing cell temperatures and trimming charge times. Heat-pump compatibility broadens seasonal operating envelopes and reduces cabin-heating energy draw. Early rollout in China and the EU validates commercial readiness, with unit-volume projections outpacing overall auto output as mandates intensify.

Fuel-Efficiency / CO₂ Rules Spurring High-Efficiency and Variable-Displacement Units

Regulatory CO₂ ceilings spur OEM adoption of variable-capacity mechanisms that cut parasitic load under partial cooling demand. Scroll and swash-plate designs dominate premium installations, while refined reciprocating units satisfy cost-conscious tiers. Integrated inverters and sensor feedback loops further optimize duty cycles, aligning with EU F-Gas rules that phase in ultra-low-GWP refrigerants. Suppliers with turnkey system engineering win platform awards as automakers compress launch timelines.

Rising Global Vehicle Production in Emerging Economies

Production upswings in India, Brazil, and Southeast Asia expand addressable unit volumes for compressor vendors. Local governments push supplier localization to trim logistics overheads and foreign-exchange exposure. Multinationals launching greenfield plants speed technology diffusion and foster regional supply-chain depth. Price-sensitive buyers favor proven reciprocating formats, pressuring cost structures yet securing long-run baseline demand. Gradual migration to higher-efficiency units is anticipated once regulatory thresholds tighten.

Consumer Preference for Enhanced Cabin Comfort and HVAC Penetration

Air conditioning has transitioned from an optional extra to a baseline expectation across vehicle classes, including entry-level models in emerging markets. Multi-zone HVAC and air-quality filtration raise capacity and control requirements, rewarding compressors with rapid response and fine modulation capabilities. SUV interior growth burdens cooling loads, accelerating the retirement of on-off cycling units. Autonomous-driving roadmaps also elevate interior experience as a design focal point, further boosting advanced compressor content.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electric Compressors' High Costs | -0.4% | Global, most acute in price-sensitive markets | Short term (≤ 2 years) |

| Low-GWP Regulations Increase Redesign Costs | -0.3% | North America and EU, expanding globally | Medium term (2–4 years) |

| Long Service Life Affects Aftermarket | -0.2% | Global, strongest in mature markets | Long term (≥ 4 years) |

| Supply Chain Risks For Materials | -0.1% | Global, concentrated in China supply base | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost and Engineering Complexity of Electric Compressors

Electric compressor systems currently price at two to three times equivalent belt units, complicating adoption in cost-sensitive segments. Integration into high-voltage powertrains necessitates extensive electrical validation, stretching development calendars and budgets. Suppliers must pair motor control firmware with thermal algorithms, a cross-disciplinary skill set not universally available. As learning curves flatten and scale improves, cost gaps are predicted to narrow, but affordability remains a near-term hurdle for value models.

Stringent Low-GWP Refrigerant Regulations Raising Redesign Costs

The EU F-Gas Regulation 2024/573 accelerates phasedown schedules, obliging platform changes to ultra-low-GWP refrigerants such as R-474A [1]“Regulation (EU) 2024/573 on Fluorinated Greenhouse Gases,” European Commission, europa.eu. Fresh sealing compounds, lubricants, and heat-exchanger geometries are mandatory, eroding the reuse of legacy tooling. Certification rules also require specialized technician training, inflating compliance overheads across the service chain. Dual-inventory management for old and new refrigerant systems strains working capital until fleet turnover stabilizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drive Type: Electric Units Gain Despite Belt Dominance

Belt-driven compressors retained 86.33% of the Automotive AC compressor market share in 2024, supported by entrenched ICE architectures and attractive unit economics. Though smaller in absolute volume, electric-driven alternatives are expanding at a 4.22% CAGR, carving footholds in BEVs, mild hybrids, and premium vehicles requiring precise load control. Independent operating capability during vehicle charging or at idle elevates thermal comfort without fuel use, a key selling point in stricter emissions zones.

The Automotive AC compressor market size for electric variants is projected to grow significantly in 2030 as cost curves descend and integrated inverter packaging becomes standard. OEM procurement strategies increasingly bundle electric compressors with broader thermal modules, boosting system revenue while shortening development cycles for new EV platforms. Conversely, belt technology faces pricing pressure and limited innovation runway, prompting incumbent suppliers to redeploy mechanical prowess toward hybrid and heavy-duty niches where belts retain relevance.

By Design Type: Rotary Technology Advances on Efficiency Gains

Reciprocating designs delivered 65.16% of the Automotive AC compressor market share in 2024 thanks to proven reliability, low tooling cost, and broad service networks. Rotary formats, scroll, vane, and centrifugal post a robust 4.84% CAGR, driven by smoother operation, superior volumetric efficiency, and better compatibility with inverter control. In the Automotive AC compressor market, rotary adoption aligns strongly with variable-capacity demand, reinforcing its future outlook.

Efficiency improvements reach double-digit percentages at partial load, directly aiding Corporate Average Fuel Economy compliance. Suppliers mitigate former durability concerns through enhanced tip-seal materials and refined oil-circuit topologies. Manufacturing complexity and tighter tolerances keep entry barriers high, preserving price premiums relative to piston units. Nevertheless, as high-volume EV programs adopt scroll types, economies of scale should reduce cost deltas.

By Vehicle Type: Passenger Cars Set the Volume Tone

Passenger cars accounted for 72.44% of the Automotive AC compressor market share in 2024, reflecting global light-vehicle dominance. This category registers a 3.16% CAGR, buoyed by comfort-oriented feature uptake and broader electrification timelines relative to commercial fleets. The Automotive AC compressor market share in passenger cars is expected to remain higher through 2030, even as e-commerce growth lifts demand in light commercial vehicles (LCVs).

LCV adoption of electric compressors is rising as last-mile delivery operators seek idle-free HVAC during urban stops, although unit volume remains comparatively modest. Medium and heavy trucks emphasize durability and serviceability, keeping reciprocating units relevant despite incremental interest in electric scrolls for auxiliary cabins. Divergent duty cycles underpin product differentiation: long-haul rigs prioritize field repairability, while urban vans value rapid cabin cool-down and reduced noise.

By Propulsion Type: BEV Platforms Drive Innovation Push

ICE vehicles still dominated the automotive AC compressor market, with 89.17% of the share in 2024, but BEVs recorded the highest 5.27% CAGR. Heat-pump operation, reversible refrigerant flow, and CO₂ compatibility shape BEV compressor specifications, demanding mechanical and control sophistication. Automakers pursuing region-wide zero-emission targets embed electric units early in development to avoid expensive redesigns later.

The Automotive AC compressor market size attributable to BEV applications is on pace to grow significantly between 2025 and 2030 as battery costs fall and model variety widens. Hybrid and plug-in hybrid platforms require dual-mode capability, letting a single compressor function under belt or electric input, an engineering challenge that only a handful of suppliers have mastered. Fuel-cell electric vehicles add stack-cooling duties, creating niche opportunities for high-purity, oil-free centrifugal designs.

By Distribution Channel: OEM Integration Dominates Value Chain

OEM channels delivered 83.11% of the Automotive AC compressor market share in 2024 and outpaced aftermarket growth at a 3.44% CAGR. Vehicle thermal architecture complexity forces early supplier involvement, often two to three years before start-of-production. Tier-one suppliers deepen collaboration through co-located design hubs and simulation sharing, cementing long-term sourcing agreements.

Aftermarket penetration remains muted as electric compressors integrate power electronics and proprietary diagnostics, limiting viable third-party replacements. Remanufacturing fills a sustainability niche, yet total addressable volumes stay modest given extended compressor life. The Automotive AC compressor industry sees OEM relationships as strategic assets, with contract renewals typically spanning full vehicle generations, protecting revenue predictability for leading vendors.

Geography Analysis

Asia-Pacific generated 47.25% of the Automotive AC compressor market share in 2024 and is forecast to expand at a 3.68% CAGR, anchored by China’s vast production scale and proactive electric-mobility subsidies. Government incentives such as China’s NEV credits and India’s Faster Adoption and Manufacturing of Hybrid and Electric vehicles (FAME) program accelerate OEM platform launches, lifting compressor unit demand [2]“FAME II Scheme Notification,” Ministry of Heavy Industries, Government of India, heavyindustries.gov.in. Local suppliers capitalize on shorter supply lines, while global players invest in joint ventures to secure market share and comply with localization quotas. Cost-sensitive consumers across Southeast Asia still favor conventional reciprocating units, but policy momentum and urban air-quality concerns gradually tilt demand toward efficient electric architectures.

North America follows with high-content vehicles and stringent Corporate Average Fuel Economy (CAFE) standards that make variable-displacement technologies mainstream. U.S. electric pickup launches deploy large-frame electric compressors to handle cabin and battery thermal loads, broadening product mix. Due to regulatory-driven technology adoption, Europe exhibits slower total-vehicle growth yet commands outsized revenue per unit. The revised EU F-Gas schedule triggers early transition to ultra-low-GWP refrigerants, creating pull for next-generation compressors compliant with new sealing and lubricant standards.

South America and the Middle East & Africa present emerging pockets where macroeconomic cycles influence automotive output. Brazilian automakers reintroduce idle-stop systems requiring improved belt-driven compressors with lower drag. Gulf Cooperation Council countries, with year-round high temperatures, specify larger displacement units, yet purchase decisions remain price-led, delaying wide adoption of inverter-controlled electric compressors.

Competitive Landscape

Technology convergence between mechanics, electronics, and thermodynamics reshapes the competitive field. The market shows evidence of high concentration, while belt-driven segments are fragmented among regional producers. Incumbent giants such as DENSO and Hanon Systems leverage scale and multi-product portfolios to cross-subsidize R&D, accelerating integrated compressor–pump module launches. Automakers reward these capabilities with multi-year sourcing contracts that span multiple vehicle platforms.

Strategic acquisitions reinforce vertical integration. Hankook & Company’s majority stake purchase in Hanon Systems in 2024 demonstrates investors’ belief that thermal-management know-how will gain strategic value as electrification intensifies [3]“Acquisition of Hanon Systems Press Release,” Hankook & Company, hankooktire.com. Compressor specialists partner with semiconductor firms to secure inverter supply and co-develop gate-driver algorithms tuned for compressor operating envelopes. Meanwhile, power-electronics newcomers enter the Automotive AC compressor market through joint ventures, bringing advanced PCB design and wide-bandgap device expertise.

Differentiation increasingly hinges on refrigerant flexibility and embedded analytics. Compressors capable of seamless R-1234yf to R-474A transition offer OEMs reduced platform complexity. Edge-compute modules track vibration signatures, predicting bearing wear and enabling warranty-cost reduction for automakers. Compliance with automotive cybersecurity and functional-safety standards further raises entry barriers for latecomers. Environmental stewardship, codified through ISO 14001 and carbon-neutral programs, also sways nomination decisions, making sustainable manufacturing a competitive lever.

Automotive AC Compressor Industry Leaders

Denso Corporation

Hanon Systems

Valeo SA

Sanden Holdings Corporation

MAHLE GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: GSF Car Parts introduced 335 Lucas-branded remanufactured air-conditioning compressors to support rising seasonal demand across passenger cars and LCVs.

- May 2024: BORG Automotive Reman expanded its catalog with a new compressor reference serving eight Dacia models, broadening coverage for independent repairers.

Global Automotive AC Compressor Market Report Scope

| Belt-Driven |

| Electric-Driven |

| Reciprocating Type |

| Rotary Type |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (MHCVs) |

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of APAC | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Drive Type | Belt-Driven | |

| Electric-Driven | ||

| By Design Type | Reciprocating Type | |

| Rotary Type | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Medium and Heavy Commercial Vehicles (MHCVs) | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Battery Electric Vehicle (BEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of APAC | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Automotive AC compressor market by 2030?

The sector is forecast to reach USD 12.51 billion by 2030 on a 2.96% CAGR trajectory.

Which compressor drive type is growing fastest?

Electric-driven units are advancing at a 4.22% CAGR as BEVs and mild hybrids proliferate.

How will low-GWP refrigerant rules affect suppliers?

Compliance forces costly redesigns of seals, lubricants and heat exchangers, but it also accelerates replacement demand for outdated units.

Which region leads global demand?

Asia-Pacific commands nearly half of worldwide revenue, fueled by large-scale vehicle production and proactive electrification policies.

Page last updated on: