Automotive Active Purge Pump Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 0.72 Billion |

| Market Size (2030) | USD 0.76 Billion |

| Growth Rate (2025 - 2030) | 1.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Active Purge Pump Market Analysis by Mordor Intelligence

The automotive active purge pump market size stood at USD 0.71 billion in 2024 and is projected to advance to USD 0.76 billion by 2030, registering a 1.09% CAGR during the forecast period. This modest trajectory reflects a tug-of-war between tightening evaporative-emission rules and the steady rise of battery-electric vehicles. Demand concentrates where turbocharged gasoline direct-injection engines and hybrid powertrains create low manifold vacuum, making engine-driven purge valves ineffective. At the same time, software-defined vehicle platforms now harvest sensor data to schedule purge events when fuel vapor concentration, ambient temperature, and engine load meet optimal conditions, improving fuel economy and cutting warranty claims. On the supply side, brushless DC motors dominate current designs, yet rare-earth magnet shortages are nudging suppliers to explore switched-reluctance options that lessen dependence on neodymium.

Key Report Takeaways

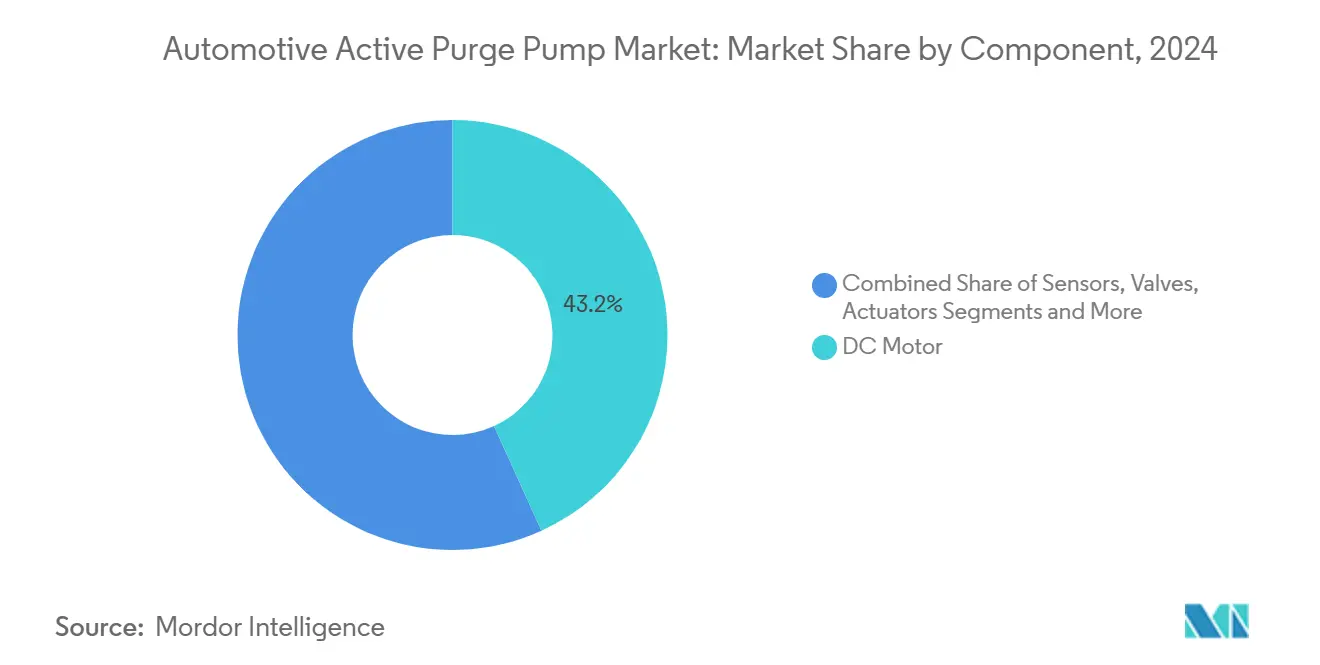

- By component, DC motors led with 43.15% of the automotive active purge pump market share in 2024, while sensors are poised for the fastest climb at a 2.25% CAGR through 2030.

- By material type, non-metal pumps captured 60.18% of the automotive active purge pump market share in 2024, and is forecast to post the highest 1.52% CAGR to 2030.

- By manufacturing process, vacuum forming captured 48.33% of the automotive active purge pump market share in 2024, whereas injection molding is forecast to post the highest 3.55% CAGR to 2030.

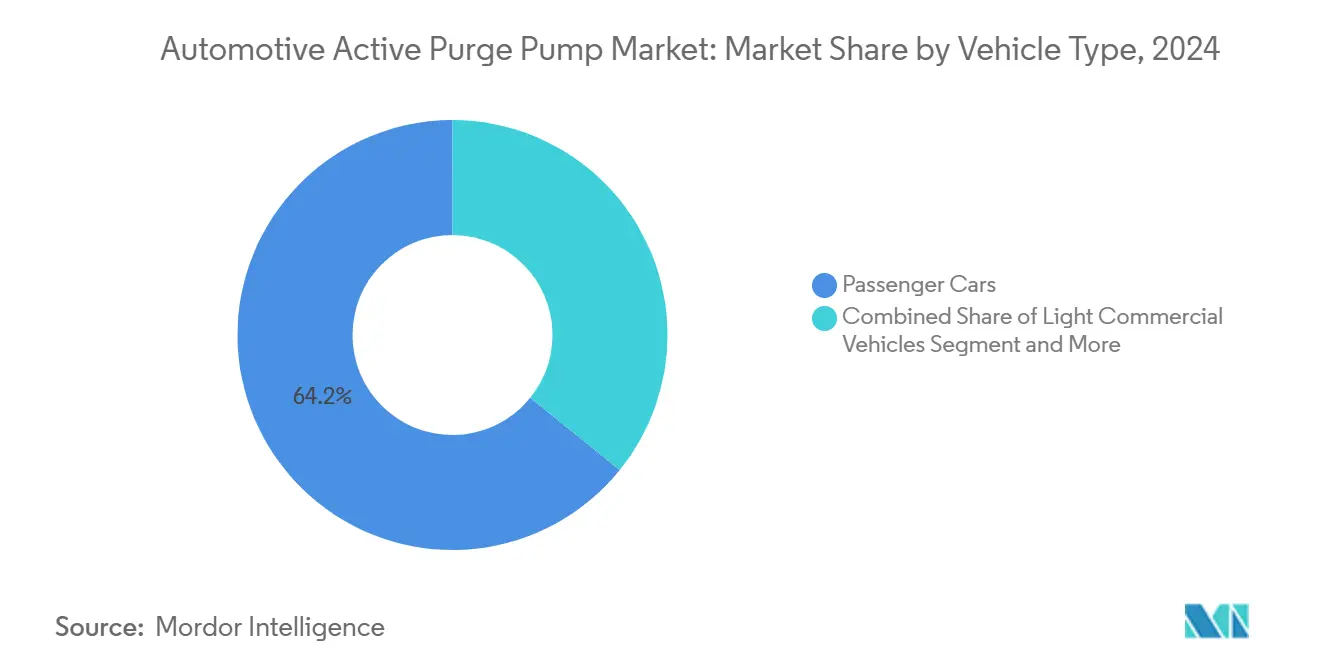

- By vehicle type, passenger cars captured 64.22% of the automotive active purge pump market share in 2024, whereas medium and heavy commercial vehicles are forecast to post the highest 1.94% CAGR to 2030.

- By distribution channel, OEM captured 72.44% of the automotive active purge pump market share in 2024, whereas the aftermarket is forecast to post the highest 3.12% CAGR to 2030.

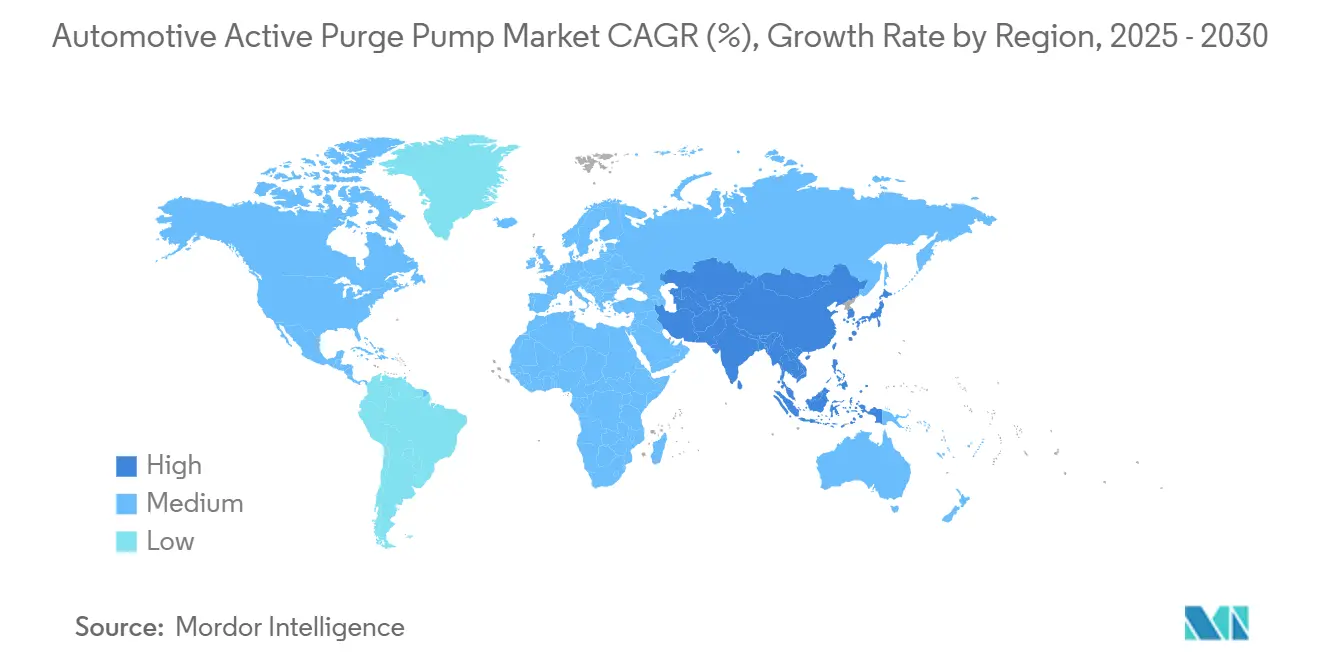

- By geography, Europe commanded 35.81% of the automotive active purge pump market in 2024, and Asia-Pacific is set to expand at a 2.85% CAGR to 2030.

Global Automotive Active Purge Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Evaporative-Emission Regulations Tighten | +0.4% | North America, Europe | Medium term (2–4 years) |

| Turbo/GDI Active Purge Required | +0.3% | Global premium segments | Long term (≥ 4 years) |

| Asia-Mena Vehicle Output Grows | +0.2% | Asia-Pacific core, spill-over to MENA | Medium term (2–4 years) |

| PHEV Pressurized Fuel Tanks | +0.2% | Electrified markets | Short term (≤ 2 years) |

| Predictive Diagnostics Via Software | +0.1% | Global premium markets | Long term (≥ 4 years) |

| Multi-Function Pumps Lower System Costs | +0.1% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Stricter Evaporative-Emission Regulations (EPA Tier-3, Euro 6e etc.)

Regulators in the United States and European Union moved leak-detection thresholds from 0.04 inches to 0.02 inches, a change that passive purge valves cannot satisfy. Active purge pumps sustain precise flow and run self-diagnostics during key-off events, giving OEMs a robust compliance path that avoids hefty penalties for non-conformance [1]“Active Purge Pump Generation IV,” Continental AG, continental.com. European programs such as Euro 6e reinforce the need for continuous monitoring, anchoring steady demand for pump-based systems in new passenger vehicles.

Turbo/GDI Engines Create Low-Vacuum Need for Active Purge

Modern downsized engines operate with pressurized intakes under boost, leaving no manifold vacuum to draw vapor from the charcoal canister. Active purge pumps, therefore, step in to move fuel vapor at any load point and preserve drivability. Continental’s patent shows centrifugal impellers that spin beyond 50,000 rpm to keep flow independent of engine vacuum, enabling tighter packaging and significant volume reduction versus older gear pumps.

Passenger-Vehicle Production Growth in Asia and MENA

China and India ramp up production to meet rising middle-class demand, and stricter export requirements mirror European and U.S. emission levels. Denso and other Tier-1s add local pump lines to hit domestic content mandates while avoiding logistics risk. Growing assembly in Thailand, Indonesia, and Vietnam provides spill-over demand, cushioning revenue even as Europe nears saturation.

Pressurized Fuel Tanks in PHEVs Demand Active Purge Pumps

Pressurized fuel tanks in plug-in hybrid electric vehicles stay sealed for long stretches when the vehicle runs on battery power, causing vapor pressure to build to levels that passive valves cannot relieve. Active purge pumps evacuate the tank at controlled intervals, preventing pressure spikes that could trigger warning lights or fuel-door release faults. During engine-off periods, the pump also supports self-diagnostic leak tests that regulators require, ensuring compliance without restarting the engine. As PHEV volumes rise, OEM engineering teams specify compact brushless pumps that integrate pressure sensors to shorten plumbing runs and cut component count.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BEV Penetration Ends Purge Pumps | -0.3% | Global premium segments | Long term (≥ 4 years) |

| Higher Materials Than Passive Valves | -0.2% | Global | Short term (≤ 2 years) |

| Rare-Earth Magnet Shortages | -0.1% | Asia-Pacific | Medium term (2–4 years) |

| Sealed Fuel Systems Bypass Pumps | -0.1% | Early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

BEV Penetration Eliminates Need for Purge Pumps

Battery electric vehicles store no liquid fuel, so they require neither charcoal canisters nor purge pumps; each BEV sale therefore subtracts one full system from the addressable market. Europe’s 2035 internal-combustion ban and China’s New Energy Vehicle quotas formalize a decade-long demand slide that suppliers must plan into capacity forecasts [2]“EU Agrees to End Sales of New Combustion-Engine Cars by 2035,” European Commission, europa.eu. Automakers that once bought 2–3 million active purge pumps per year are shifting capital toward thermal management modules instead, redirecting R&D resources and tooling budgets. Service demand from the legacy ICE fleet tempers the near-term impact, yet OE fitment volumes will contract in line with BEV share growth. Suppliers with balanced portfolios across ICE and electric fluid systems will manage the transition better than single-product specialists.

Higher BOM Cost vs. Passive EVAP Valves

An active purge assembly adds a motor, controller, and pressure sensor, raising per-vehicle cost compared to a passive valve, a delta that pressures entry-level models. Emerging economies where Stage-2 evaporative rules still apply allow passive systems, letting automakers avoid the premium while remaining compliant. Even in regulated markets, procurement teams negotiate aggressive cost downs that squeeze supplier margins and can delay new pump launches. Tier-1s respond with multi-function modules and high-cavitation injection molding to trim plastic mass and reduce assembly labor, yet the gap with passive hardware remains material. Adoption, therefore, concentrates on segments where turbocharged engines and on-board diagnostics justify the extra spend.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: DC motors retain scale while sensors accelerate

DC motors delivered 43.15% of the automotive active purge pump market in 2024, a leadership anchored by proven reliability in harsh under-hood environments. Continental’s compact 12-V brushless design weighs 120 g yet spins 50,000 rpm, matching purge flow targets for 3.0 L turbo applications while slashing power draw. Sensors will rise fastest at 2.25% CAGR to 2030, reflecting regulatory insistence on real-time leak checks. Pressure transducers feeding closed-loop controllers now detect leaks down to 0.02 inches, satisfying CARB’s enhanced protocols. Actuators and valves keep a steady call rate as they gate flow during diagnostic modes, whereas canister components inch lower as multi-function pump modules integrate charcoal volumes.

DC motors are also vulnerable to rare-earth pricing swings that influence OEM sourcing. Sensor suppliers see cross-functional leverage by reusing MEMS dies from TPMS and EGR programs, lowering incremental cost per channel. Over the forecast, sensor revenue will narrow the gap with motor revenue even if overall volume growth remains flat. The emerging switch to Ethernet-based architectures, with higher bandwidth for diagnostic data, strengthens the business case for advanced sensors inside the automotive active purge pump market.

By Material Type: Polymers dominate and accelerate cost wins

Non-metal housings accounted for 60.18% of the automotive active purge pump market in 2024, propelled by glass-filled nylon that resists fuel and cuts weight. Suppliers target a 1.52% CAGR by moving from machined aluminum to injection-molded PA66 in end-plates, trimming 30% expense at equal burst pressure. Metal still anchors motor stators and magnet carriers, preserving rigidity where tolerances fall below 30 µm. Hybrid polymer-metal assemblies advance as over-molded copper windings drop assembly steps by welding leads inside the mold.

Cost comparison studies show that polymer replacement can save USD 1.1 per unit, a vital lever for automakers who chase every gram of CO2 compliance. Regulatory durability cycles, 15 years or 150,000 mi, demand chemical stability. New aliphatic polyketones and PPS blends now achieve near-zero permeation, ensuring the automotive active purge pump market meets evaporative limits without a metal penalty.

By Manufacturing Process: Injection molding surges on automation payback

Vacuum forming maintained 48.33% of the automotive active purge pump market in 2024, serving small-batch programs and late-cycle engineering changes. Yet injection molding is slated for a 3.55% CAGR as all-electric presses minimize scrap and raise cavity counts, driving down cost per part. Multi-shot molding bonds elastomer seals directly onto housings, erasing two downstream steps and removing manual insertion labor.

OEMs now mandate traceable molding parameters logged to the cloud. Suppliers running 4.0 data loops flagged a 14-ppm defect rate against 65 ppm on vacuum-formed lots. Cost modeling indicates full amortization of a 1,500-t press at 300,000 units a year within three years, making injection molding the default for high-volume C-segment platforms in the automotive active purge pump market.

By Vehicle Type: Passenger cars stay dominant despite commercial momentum

Passenger cars represented 64.22% of the automotive active purge pump market in 2024, driven by high annual unit builds and the turbo adoption curve. Regulatory tests first cover the light-duty class, guaranteeing purge suppliers' base volume. Medium and heavy commercial trucks will log the strongest 1.94% CAGR through 2030 because fleet operators adopt advanced emission controls to secure urban operating permits. In the United States, Phase 2 greenhouse-gas rules increase purge-system complexity in Class 6–8 rigs, lifting ASPs.

Buses in China and India amplify this rise because city administrations restrict evaporative VOCs near depots, triggering retrofit programs. Even so, the automotive active purge pump market size in buses remains low, so passenger car dominance prevails over time.

By Distribution Channel: OEM integration leads, aftermarket growth follows

OEM channels captured 72.44% of the automotive active purge pump market in 2024, since purge calibration occurs during powertrain certification, leaving little scope for third-party substitution. Warranty liability also keeps automakers tied closely to Tier-1s. The aftermarket will climb at a 3.12% CAGR as the production cohort ages into its first purge system replacements from 2027 onward. Continental already released 700 pump part numbers, doubling catalog coverage to a notable share of the North American vehicle parc.

Independent garages gain diagnostic capability through low-cost smoke machines and OBD enhancements that pinpoint small evap leaks, building confidence to install aftermarket kits. Europe's rising average vehicle age is expected to grow by 2030, supporting steady service demand within the automotive active purge pump market.

Geography Analysis

Europe held 35.81% of the automotive active purge pump market in 2024, buttressed by Euro 6e evaporative rules and the region’s turbo-gasoline penetration. France mandates canister computer-controlled purge for new type approvals, cementing demand. Germany’s premium OEMs deploy multi-function pump modules that combine purge, tank-pressure sensing, and onboard refueling vapor recovery, boosting average selling price.

Asia-Pacific will post the quickest 2.85% CAGR, with China representing a significant share of the regional total in 2024. Stricter China VII regulations, effective in the coming years, draft leak thresholds akin to Euro 6e, aligning domestic requirements with export standards. India’s Bharat Stage VII proposal mirrors this trend. Regional suppliers that leverage local resin and motor sourcing offset cost pressure and enhance competitiveness.

North America remains a solid third pillar given EPA Tier-3 rules and the popularity of large fuel tanks in pickup trucks, which amplify vapor loads. California’s Advanced Clean Cars II keeps hybrid residual demand alive through 2030, cushioning volume. Latin America and the Middle East trail but gain impetus from investments in local vehicle assembly facilities in Brazil and Saudi Arabia, respectively, both of which import best-in-class emission hardware to reach Euro-aligned norms.

Competitive Landscape

The market shows moderate concentration. Continental, Bosch, and Denso together control a significant position, leveraging extensive EVAP portfolios and global manufacturing footprints. Continental’s Gen IV pump packs motor, diagnostics, and leak-detection sensor into a 380 g housing and won nominations on two German luxury platforms launching in 2026. Bosch focuses on energy-optimized motors that cut current draw by 22%, a feature valued by plug-in hybrid makers. Denso localizes production in India and Thailand to meet automaker sourcing mandates.

Second-tier players such as Mahle and GMB Korea focus on regional OEMs and late-cycle model refreshes where price sensitivity is acute. GMB Korea localized magnets and motor laminations in 2025, eliminating import duty and shaving lead times for Hyundai and Kia programs [3]“Localization of Active Purge Pump,” GMB Korea Co. Ltd., gmbkorea.co.kr.

Start-ups explore switched-reluctance motors to sidestep rare-earth exposure, though noise and torque ripple still limit adoption. Over the long haul, suppliers aim to pivot hardware knowledge toward thermal-fluid management modules that serve both ICE and BEV architectures, preparing for eventual contraction in the automotive active purge pump market.

Automotive Active Purge Pump Industry Leaders

Continental AG

Robert Bosch GmbH

Denso Corporation

Schaeffler Group

Johnson Electric Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: GMB Korea localized the active purge pump for hybrid vehicles, marking Korea’s first domestic development of the component.

- August 2023: Vitesco Technologies partnered with Cebi Group to co-develop washer and purge modules for future Euro-7 programs

Global Automotive Active Purge Pump Market Report Scope

| DC Motor |

| Sensors |

| Actuators |

| Valves |

| Vapor Canister |

| Metal |

| Non-Metal |

| Cutting |

| Vacuum Forming |

| Injection Molding |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (MHCVs) |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Component | DC Motor | |

| Sensors | ||

| Actuators | ||

| Valves | ||

| Vapor Canister | ||

| By Material Type | Metal | |

| Non-Metal | ||

| By Manufacturing Process | Cutting | |

| Vacuum Forming | ||

| Injection Molding | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Medium and Heavy Commercial Vehicles (MHCVs) | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the automotive active purge pump market in 2025?

The automotive active purge pump market size is USD 0.72 billion in 2025, continuing on a path toward USD 0.76 billion by 2030.

Which region grows fastest through 2030?

Asia-Pacific posts the highest 2.85% CAGR, lifted by China’s and India’s stricter emission norms and rising vehicle builds.

What component leads revenue today?

DC motors account for 43.15% revenue because they provide the core actuation needed for precise vapor flow control.

Which manufacturing process gains share?

Injection molding grows at 3.55% CAGR as suppliers automate high-volume production and integrate multiple functions into single housings.

Page last updated on: