Truck Refrigeration Unit Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 12.78 Billion |

| Market Size (2030) | USD 16.23 Billion |

| Growth Rate (2025 - 2030) | 4.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

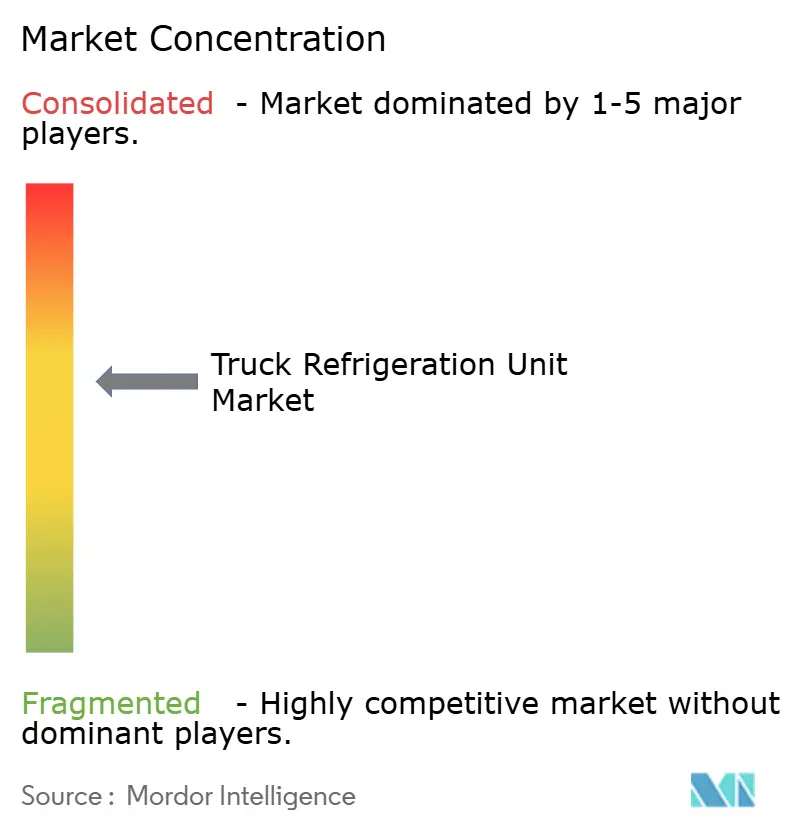

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Truck Refrigeration Unit Market Analysis by Mordor Intelligence

The truck refrigeration unit market size stood at USD 12.78 billion in 2025 and is projected to reach USD 16.23 billion by 2030, and is expected to expand at a 4.89% CAGR during the forecast period (2025-2030). Growing demand for temperature-controlled logistics, strict emission rules, and accelerating electrification of commercial vehicles are steering the industry toward engine-free and hybrid systems. Fleet operators view electric transport refrigeration units (eTRUs) as a long-term hedge against diesel price volatility, while shore-power infrastructure at ports reduces operating costs and local emissions. Advances in battery energy density, predictive-maintenance telematics, and integrated power management are improving the total cost of ownership, widening the appeal of high-voltage solutions in both developed and emerging economies. Asia-Pacific leads new unit installations, but North America’s policy momentum catalyzes the fastest technology transition.[1]“Transport Refrigeration Unit,” California Air Resources Board, arb.ca.gov

Key Report Takeaways

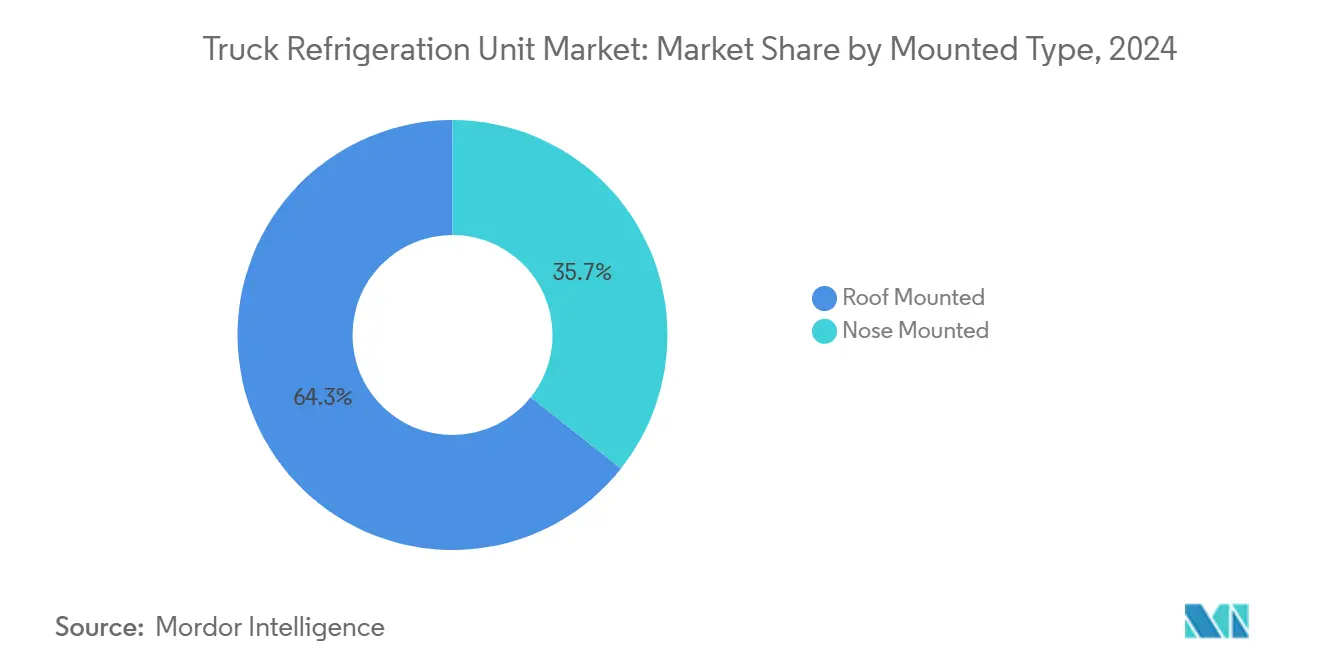

- By mounted type, roof-mounted systems held 64.33% of the truck refrigeration unit market share in 2024 and are forecasted to grow at a 7.31% CAGR during the forecast period (2025-2030).

- By vehicle type, light commercial vehicles accounted for a 53.12% share of the truck refrigeration unit market in 2024, while trailers are expected to register a 5.92% CAGR during the forecast period (2025-2030).

- By temperature mode, single-temperature systems captured a 69.46% share of the truck refrigeration unit market in 2024; multi-temperature units are expected to be on track for a 7.49% CAGR during the forecast period (2025-2030).

- By power source, engine-powered units dominated with a 78.65% share of the truck refrigeration unit market in 2024, whereas the independent electric platforms segment is expected to grow at an 8.89% CAGR during the forecast period (2025-2030).

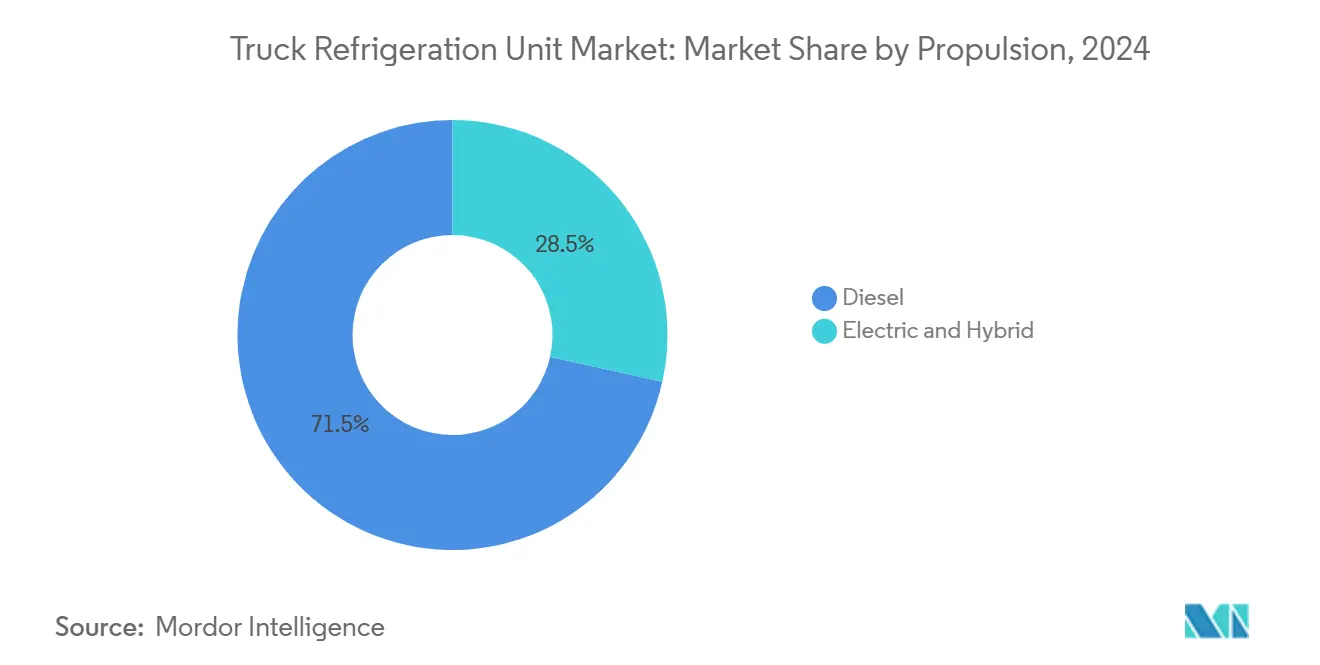

- Diesel remained the mainstream choice for propulsion, with a 71.51% share of the truck refrigeration unit market in 2024. Yet, the electric and hybrid units segment is expected to grow at a 13.48% CAGR during the forecast period (2025-2030).

- By end-use industry, food and beverage led with a 62.31% share of the truck refrigeration unit market in 2024; healthcare logistics is expected to climb at an 8.98% CAGR during the forecast period (2025-2030).

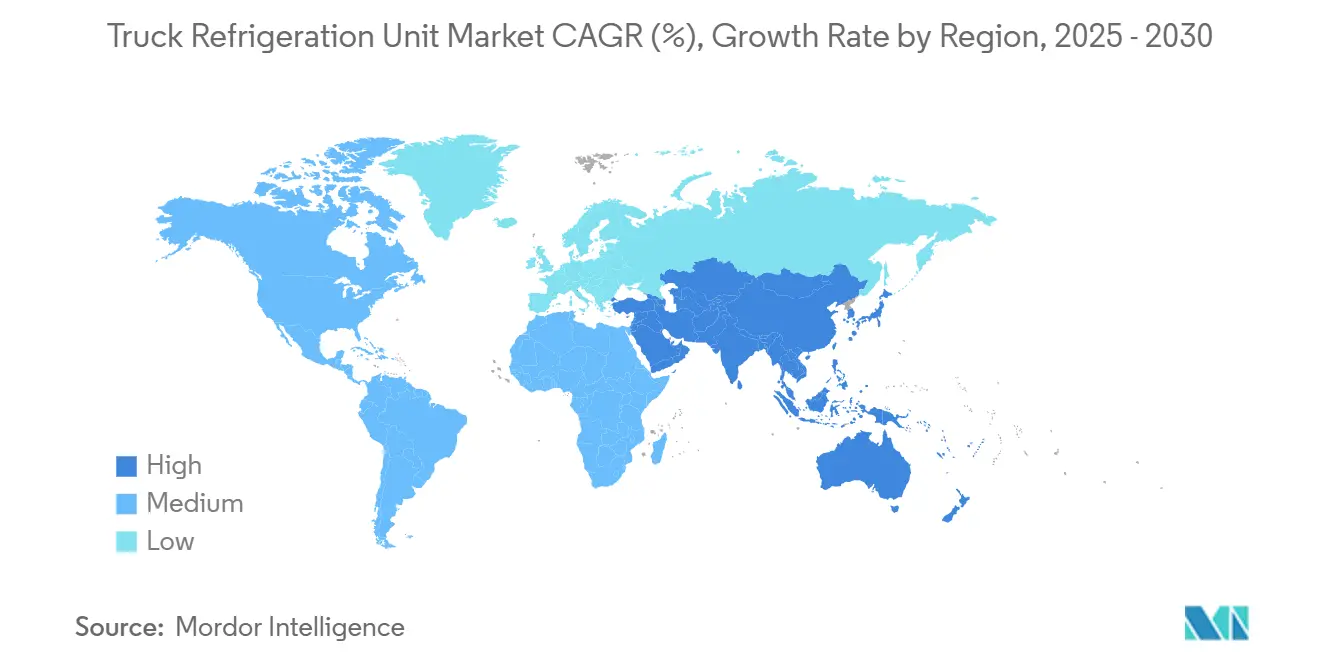

- By geography, Asia-Pacific captured 38.82% of the truck refrigeration unit market size in 2024 and is forecasted to grow at a 5.13% CAGR during the forecast period (2025-2030).

Global Truck Refrigeration Unit Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-chain Expansion | +1.3% | Global, with early gains in Asia-Pacific, South America | Medium term (2-4 years) |

| Emission Mandates | +1.1% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Micro-fulfilment Boom | +0.8% | Global urban centers, concentrated in North America, Europe | Short term (≤ 2 years) |

| Shore-power Infrastructure | +0.6% | North America, Northern Europe ports | Medium term (2-4 years) |

| Predictive-maintenance Telematics | +0.4% | Global, led by North America and Europe | Medium term (2-4 years) |

| EV-purchase Incentives | +0.3% | North America, EU, selective APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cold-chain Expansion for Perishables

Demand for fresh produce, frozen foods, and temperature-sensitive pharmaceuticals is expanding global cold-chain capacity, especially in Asia-Pacific and Latin America. Governments are funding distribution hubs and reefer fleet upgrades to cut food loss and meet food-safety norms. Pharmaceutical firms require validated temperature mapping, pushing fleets to adopt multi-temperature and ultra-low-temperature configurations. Retailers in fast-growing urban regions prefer flexible cargo zones to consolidate outbound routes. Rising e-grocery penetration further supports high-utilization refrigerated delivery trucks capable of meeting stringent time-temperature integrity standards.

Regulatory Emission Mandates

California has set a global benchmark for sustainability with its Transport Refrigeration Unit regulation, mandating fleets in the state to transition to zero-emission units by a specified timeline. Several other states in the United States are contemplating similar regulations following California's lead. Meanwhile, the European Union's overhaul of the F-Gas regulation pushes operators away from high-GWP refrigerants. These regulations push the demand for fuel for electric systems that utilize low-GWP refrigerants and battery-electric drives. In light of these developments, manufacturers are hastening their product development efforts, rolling out solutions that meld electric compressors, DC-DC converters, and cutting-edge telematics to ensure compliance with diverse regulatory standards.

Urban Micro-fulfillment Boom

E-commerce grocery platforms and convenience retailers favor small, quiet, and highly maneuverable refrigerated vans for same-day delivery. Electric TRUs integrated into Class 1-4 chassis meet urban noise ordinances and zero-emission zones, reducing local pollutants. Compact vans can access curb-side loading bays and below-grade parking facilities where larger trucks face restrictions. High delivery density increases daily door-counts, amplifying the value of predictive maintenance to avoid unplanned downtime. Consequently, unit volumes for light commercial vehicles continue to outpace traditional heavy-duty fleets.

Shore-power Infrastructure Adoption

Distribution hubs and ports are installing plug-in points so reefers can draw grid power when stationary, cutting diesel usage and operating costs. Electric transport refrigeration units, on average, incur lower hourly energy costs than their diesel counterparts, leading to substantial long-term operational savings. Utility incentive schemes lower installation costs, accelerating the adoption of shore-power-ready designs. Operators also gain carbon-credit benefits and quieter loading-dock environments. Plug-in functionality compensates battery range limits, making electric units viable for longer dwell times.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Of E/hybrid TRUs | -0.9% | Global, most acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Grid Capacity Constraints | -0.7% | North America, selective EU regions, emerging markets | Medium term (2-4 years) |

| Payload Loss from Battery Weight | -0.5% | Global, particularly impacting long-haul operations | Medium term (2-4 years) |

| Technician Skill-gap | -0.3% | Global, concentrated in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Electric/Hybrid TRUs

Electric systems, while environmentally friendly, come with a hefty price tag, especially when compared to their diesel counterparts. This financial hurdle is particularly pronounced for smaller carriers in emerging markets. The elevated acquisition costs can be attributed to several factors: the pricing of batteries, the expense of power electronics, and the procurement of low-GWP refrigerants. Although leasing options offer a way to spread these costs over time, many financial institutions approach cautiously, primarily due to the absence of established benchmarks for residual value. Moreover, external pressures like component tariffs and disruptions in the supply chain further inflate landed costs, posing challenges for buyers sensitive to pricing. Despite the total cost of ownership eventually tipping in favor of electric units over the long haul, the daunting upfront investment remains a significant barrier to swift adoption.

Utility-grid Capacity Constraints

Charging multiple electric transport refrigeration units (eTRUs) at a single depot often strains local distribution transformers, leading to lengthy grid upgrades. Before installation, facility managers navigate utility approvals, engineering assessments, and secure capital funding. In regions with aging infrastructure, upgrade costs often fall on end-users, undermining the financial case for adoption. While portable battery-buffer systems can alleviate peak loads, they add expense and complexity. Consequently, limited grid readiness poses a significant barrier to widespread eTRU deployment, even with strong interest from fleets.

Segment Analysis

By Mounted Type: Roof-mounted Systems Drive Market Leadership

Roof-mounted units accounted for a commanding 64.33% of the truck refrigeration unit market share in 2024, reflecting operators’ preference for designs that do not encroach on usable cargo space. Their elevated placement enhances aerodynamics, improving fuel economy and helping fleets meet tightening emission limits. Service technicians value quick access from the trailer roofline, which shortens maintenance windows and maximizes asset uptime. Trailer builders increasingly offer standardized roof-mount brackets, reducing installation labor and ensuring consistent weight distribution. These factors underpin a projected 7.31% CAGR for roof-mounted systems through 2030.

Competitive positioning inside the truck refrigeration unit market favors suppliers able to balance airflow capacity with low-profile housings that minimize drag. Technology upgrades, such as composite mounting frames and vibration-dampening pads, address past durability concerns on rough roads. In long-haul applications, improved condensers and variable-speed fans help roof-mounted models hold set-points while drawing less power, supporting future hybrid and battery-electric trucks. Nose-mounted units retain niche roles on vehicles with rooftop obstructions, yet their lower cooling output constrains adoption on large boxes. As electric drive trains spread, roof-mounted architectures remain compatible because they operate independently of any front-wall clearance constraints.

By Vehicle Type: Light Commercial Vehicles Lead Urban Transformation

Light commercial vehicles captured 53.12% of the truck refrigeration unit market in 2024, owing to surging demand for same-day grocery and meal-kit delivery. Their compact footprints let drivers navigate dense city streets and satisfy curb-side loading bans on heavier trucks. Urban zero-emission zones further accelerate interest in lightweight vans that pair small battery packs with engineless refrigeration units. High drop densities generate more door-open cycles, so thermal-efficient doors and rapid-pull-down evaporators have become critical design differentiators. Consequently, OEMs now pre-install refrigeration wiring harnesses to speed up aftermarket upfits.

Medium and heavy-duty trucks still dominate long-haul lanes, but trailers are forecast to post a healthy 5.92% CAGR as intermodal hubs expand cross-dock operations. Trailer-based reefers detach from tractors during maintenance or regulatory checks, keeping perishable freight moving and reducing downtime. Fleets also value the ability to pre-cool trailers on shore power, a practice that lowers diesel consumption and aligns with emission mandates. Growth in Latin American produce exports and North American big-box retail replenishment supports rising trailer volumes. In contrast, rigid heavy trucks are seeing slower growth because route consolidation favors modular trailer swaps.

By Temperature Mode: Single-temperature Dominates Despite Multi-temperature Growth

Single-temperature systems held 69.46% of the truck refrigeration unit market size in 2024, meeting the needs of dedicated frozen or chilled routes with lower capital outlays versus multi-zone units. Their simpler control architecture reduces failure points, important for small carriers lacking advanced maintenance capabilities. Fuel economy remains attractive because a single evaporator and compressor cycle draws less power than multi-zone counterparts. These advantages explain why many fleet operators keep single-temperature trucks on high-frequency store replenishment loops. However, rising mixed-load demand is challenging this status quo.

Multi-temperature systems are projected to log a robust 7.49% CAGR through 2030 as retailers pursue inventory consolidation strategies. Flexible bulkheads and independent evaporators let one vehicle haul frozen, chilled, and ambient products together, cutting total fleet size and empty-backhaul miles. Advances in lightweight insulating partitions mitigate payload penalties, while smart controllers balance compressor duty cycles to curb energy use. Supermarkets running micro-fulfillment hubs rely on these units to support rapid order picking across diverse product categories. Improved zone-temperature logging also aids compliance with food-safety and pharmaceutical transport protocols.

By Power Source: Engine-powered Systems Face Transition Pressure

Engine-powered units commanded 78.65% of 2024 revenue, largely because they operate independently of vehicle electrical systems and remain reliable on routes with limited charging infrastructure. Their self-contained diesel engines supply consistent refrigeration even when the truck idles, an asset for unrestricted dwell times at distribution centers. Yet these auxiliary engines fall under stricter emission standards, obliging manufacturers to add diesel particulate filters and selective catalytic reduction hardware. Extra after-treatment raises acquisition cost and maintenance complexity, narrowing the historical cost advantage. Regulatory scrutiny is therefore driving fleets to explore alternative power sources.

Independent electric platforms are predicted to expand at an 8.89% CAGR, leveraging modular battery packs and shore-power compatibility to displace diesel engines. Many depots now install plug-in posts, letting units pre-cool trailers on grid electricity at one-third the hourly energy cost of diesel. Software-enabled power management synchronizes battery charging with route schedules, extending range without oversizing packs. Hybrid configurations that blend battery and engine power act as transitional solutions for fleets not yet ready for full electrification. Over time, falling battery prices and wider charging coverage are expected to erode the dominance of engine-powered systems in the truck refrigeration unit market.

By Propulsion: Electric and Hybrid Solutions Accelerate Market Transformation

Diesel remained the mainstream propulsion choice with a 71.51% share in 2024, anchored by a vast installed base and proven long-range capability. Operators appreciate diesel’s high energy density and quick refueling, which sustain cold chains on multi-day trips. Nevertheless, diesel faces mounting policy headwinds and rising fuel taxes that erode its cost leadership. OEMs respond with cleaner engines using low-GWP refrigerants, yet this only postpones inevitable electrification. The industry, therefore, views diesel as a bridge technology rather than a long-term solution.

Electric and hybrid TRUs are surging at a 13.48% CAGR, buoyed by California’s 2029 zero-emission deadline and similar European city mandates. Full-electric models integrate with battery-electric trucks, eliminating duplicate engines and simplifying service regimes. Hybrids maintain a small diesel backup to safeguard temperature control on exceptionally long routes, easing range-anxiety concerns for early adopters. Noise reductions from electric compressors permit nighttime deliveries, raising asset utilization and improving return on investment. As battery pack prices decline, total cost of ownership projections increasingly favor electric propulsion, accelerating the retirement of diesel-only fleets.

By End-use Industry: Food and Beverage Leadership with Healthcare Acceleration

Food and beverage logistics generated 62.31% of the truck refrigeration unit market revenue in 2024, reflecting continuous restocking rhythms across grocery, restaurant, and convenience channels. Frequent route cycles translate to higher unit-hour utilization, prompting fleets to prioritize reliability and rapid pull-down performance. Seasonal produce surges and holiday demand spikes encourage operators to maintain excess refrigerated capacity, sustaining steady unit replacement. Retailers’ commitment to reducing spoilage and extending shelf life reinforces the dominance of food-centric applications. Synchronization with warehouse automation further boosts demand for precise temperature control.

Healthcare consignments remain smaller in volume but are forecast to post an 8.98% CAGR due to rising biologics and vaccine shipments that demand tight temperature tolerances. Pharmaceutical guidelines require real-time temperature logging and redundant power safeguards, driving uptake of high-specification electric or hybrid units. Cold-chain validation protocols also favor telematics-enabled reefers that provide tamper-proof data trails for regulatory audits. Growth of contract manufacturing in Asia and expanded clinical-trial networks in Latin America enlarge cross-border pharma flows, strengthening long-haul healthcare demand. Chemical, floral, and electronic segments add incremental volume, yet food and healthcare will continue to define specification roadmaps for future TRU innovations.

Geography Analysis

Asia-Pacific dominated the truck refrigeration unit market with 38.82% revenue share of the truck refrigeration unit in 2024 and is expected to expand at a 5.13% CAGR through 2030. Rapid urbanization and rising middle-class incomes spur growth in e-grocery and quick-service restaurants, boosting demand for refrigerated light vehicles. Domestic manufacturers in China and India supply cost-effective units, while Japan and South Korea contribute high-spec designs leveraging automotive electronics expertise. Government food-safety campaigns and burgeoning pharmaceutical exports reinforce sustained investment in cold-chain fleets.

North America ranked second in 2024 unit shipments, yet leads the regulatory push toward zero-emission solutions. The region’s 3.92% CAGR masks robust replacement demand triggered by the California zero-emission timeline, influencing fleets operating across state lines. Canadian provinces support hybrid-electric adoption through emission-reduction funds, and Mexico’s near-shoring boom fuels new assembly plants that supply both diesel and electric TRUs to regional fleets. U.S. utility programs co-fund charging infrastructure, lowering barriers for small carriers.

Europe recorded a 3.54% CAGR forecast, reflecting market maturity and strict refrigerant regulations rather than high unit growth. The European Union’s F-Gas revisions accelerate uptake of low-GWP refrigerants and CO₂ trans-critical systems[2] “Cold Hard Facts 4,” Department of Climate Change, Energy, the Environment and Water, climatechange.gov.au. Western Europe emphasizes eTRU deployment in urban low-emission zones, while Eastern European members invest in modern cold-chain fleets to align with EU food-safety rules. Innovation focuses on refrigerant recovery services and circular-economy design principles to maximize component reuse.

Competitive Landscape

The Truck Refrigeration Unit Market exhibits moderate concentration, indicating substantial opportunities for technological disruption and market entry by innovative players. Incumbents Carrier Transicold and Thermo King leverage global service networks and OEM chassis partnerships to safeguard share while launching fully electric product lines. DENSO integrates automotive HVAC know-how into compact eTRUs for light vehicles, tapping synergies with electrified vans.

Three competitive archetypes are emerging. First, diversified incumbents hedge bets across diesel, hybrid, and all-electric models supported by telematics subscriptions that create stickier customer relationships. Second, specialist electric entrants package high-voltage refrigeration with battery-electric truck platforms, promising factory-integrated solutions and simplified after-sales support. Third, cost-competitive Asian manufacturers scale production to serve domestic demand and target price-sensitive export markets.

Strategic priorities revolve around modular architectures allowing rapid technology swaps, integrated power-train management that optimizes vehicle and refrigeration loads, and predictive maintenance to boost fleet uptime. Intellectual-property battles now focus on battery thermal-management patents and low-GWP refrigerant circuit designs. Overall, technological migration toward zero-emission and connected units is redrawing competitive boundaries, creating entry windows for agile innovators.

Truck Refrigeration Unit Industry Leaders

Carrier Transicold

Thermo King

DENSO Corporation

Hwasung Thermo

Dongin Thermo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Carrier Transicold debuted its all-electric Pulsor eCool at the REFCOLD exhibition in New Delhi, broadening its emission-free portfolio.

- July 2025: Carrier Transicold added Supra HE 11 MT and HE 13 MT models, offering higher capacity and multi-temperature flexibility.

- June 2025: IRS Eastern and Carrier Transicold launched the Philippines’ first all-electric truck refrigeration unit to meet growing sustainability goals.

- April 2025: Thermo King opened its LEGEND trailer refrigeration unit production line in Wujiang, China, to serve the Asia-Pacific market.

Global Truck Refrigeration Unit Market Report Scope

| Roof Mounted |

| Nose Mounted |

| Light Commercial Vehicle |

| Medium and Heavy-Duty Truck |

| Trailers |

| Single Temperature |

| Multi Temperature |

| Engine-Powered |

| Independent |

| Diesel |

| Electric and Hybrid |

| Healthcare |

| Food and Beverage |

| Chemical |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Mounted Type | Roof Mounted | |

| Nose Mounted | ||

| By Vehicle Type | Light Commercial Vehicle | |

| Medium and Heavy-Duty Truck | ||

| Trailers | ||

| By Temperature Mode | Single Temperature | |

| Multi Temperature | ||

| By Power Source | Engine-Powered | |

| Independent | ||

| By Propulsion | Diesel | |

| Electric and Hybrid | ||

| By End-Use Industry | Healthcare | |

| Food and Beverage | ||

| Chemical | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What CAGR is expected for the truck refrigeration unit market between 2025 and 2030?

The market is projected to grow at a 4.89% CAGR, rising from USD 12.78 billion in 2025 to USD 16.23 billion by 2030.

Which mounted configuration leads current demand?

Roof-mounted refrigeration units command a 64.35% share owing to aerodynamic efficiency and easier maintenance access.

How fast are electric and hybrid TRUs growing?

Electric and hybrid propulsion systems are set to register a 13.48% CAGR, the fastest among all powertrain categories.

Why is Asia-Pacific the largest regional market?

Rapid urbanization, expanding cold-chain infrastructure, and cost-competitive regional manufacturing give Asia-Pacific a 38.82% share.

What regulatory change most affects North American fleets?

California’s mandate requiring all truck refrigeration units to be zero-emission by 2029 is driving nationwide equipment replacement.

Page last updated on: