Automotive Chassis Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

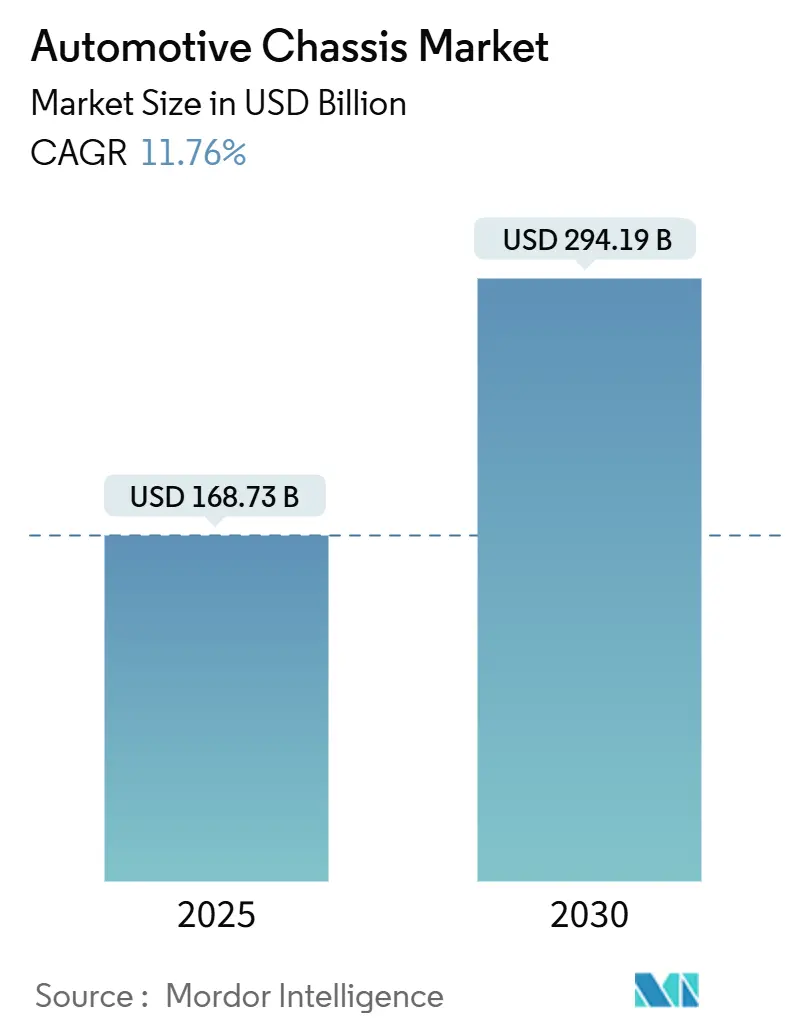

| Market Size (2025) | USD 168.73 Billion |

| Market Size (2030) | USD 294.19 Billion |

| Growth Rate (2025 - 2030) | 11.76% CAGR |

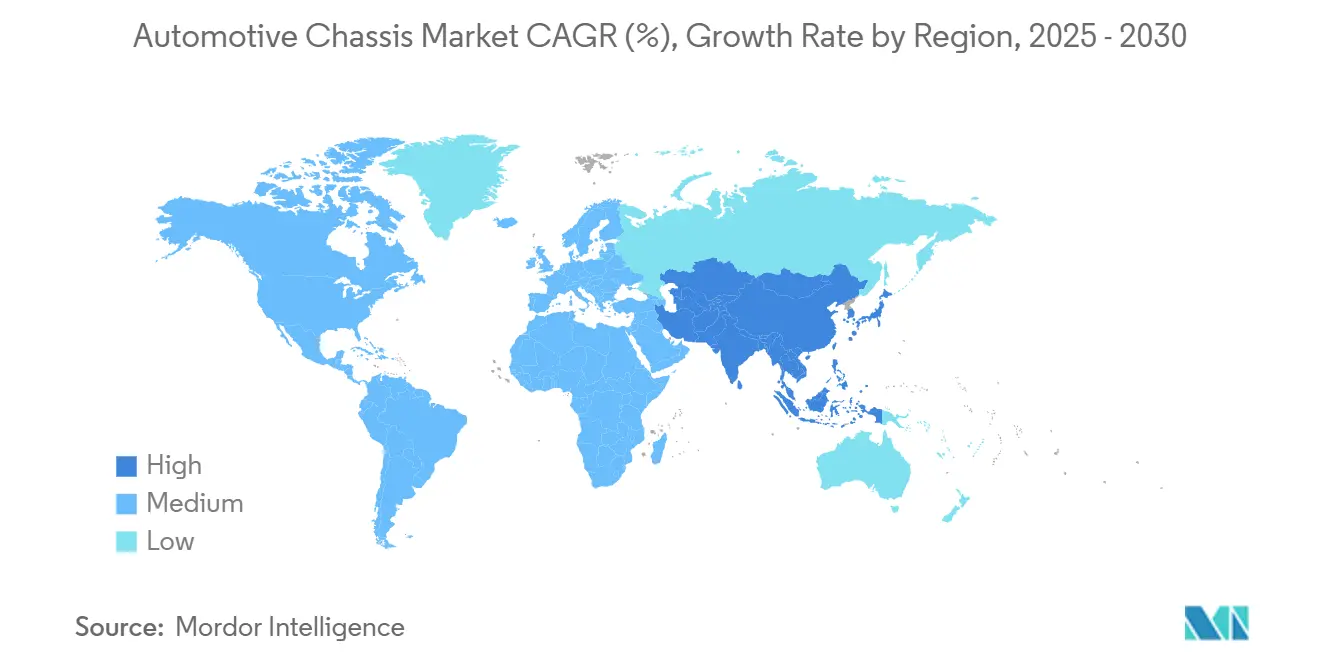

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

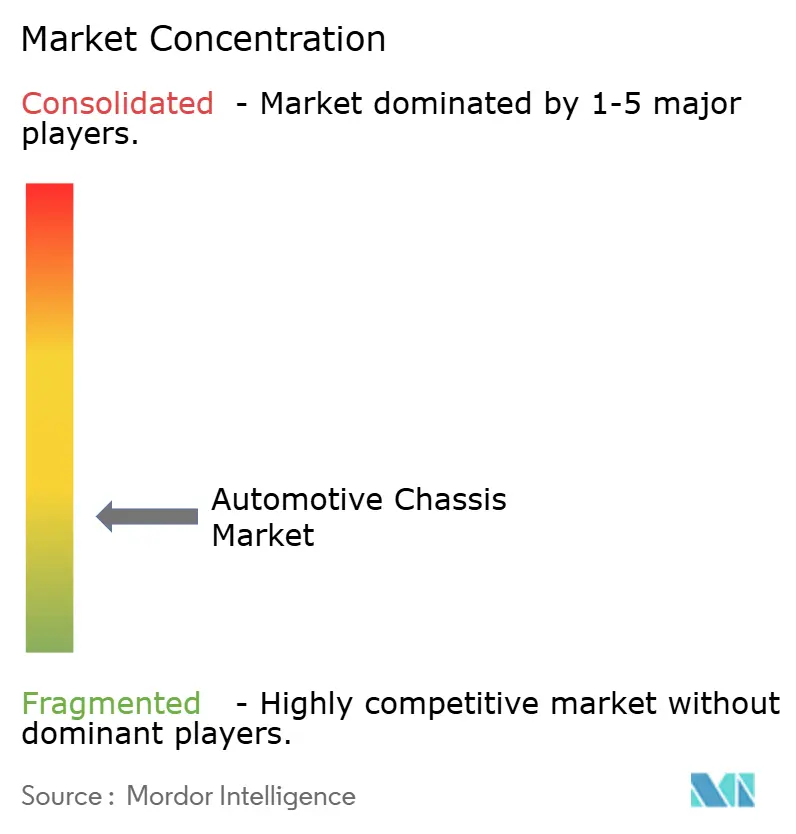

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Chassis Market Analysis by Mordor Intelligence

The automotive chassis market stood at USD 168.73 billion in 2025 and is forecast to climb to USD 294.19 billion by 2030, advancing at an 11.76% CAGR. This sustained expansion reflects three converging trends: regulatory zero-emission targets that accelerate battery-electric adoption, lightweighting imperatives that favour advanced materials, and safety mandates that reward integrated skateboard platforms. Major automakers are committing large-scale capital to single-piece castings that replace welded sub-assemblies, while suppliers are racing to secure cobalt-free battery packs that double as load-bearing members. Autonomous pod concepts and coastal-region corrosion challenges broaden the design envelope and create aftermarket upgrade opportunities.

Key Report Takeaways

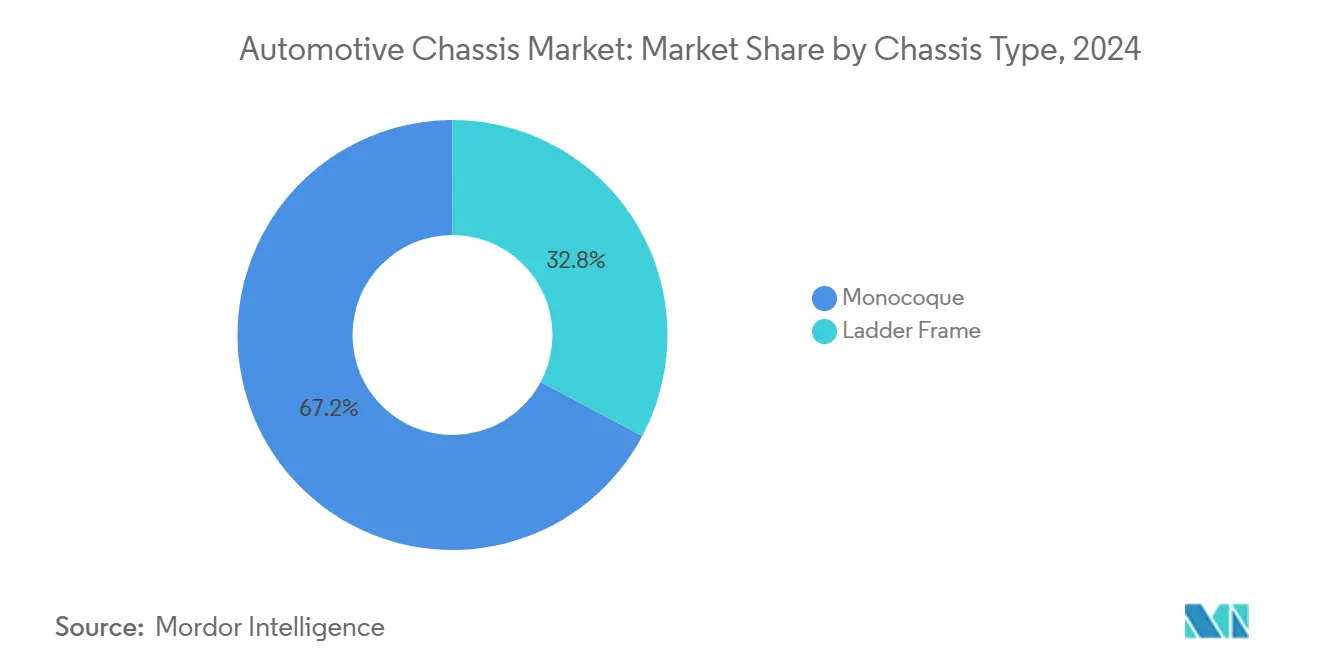

- By chassis type, monocoque designs accounted for a 67.22% share of the automotive chassis market in 2024, whereas ladder-frame platforms are poised for the highest 13.23% CAGR over the forecast horizon.

- By material type, steel dominated the automotive chassis market, with a 65.28% share in 2024, while carbon-fibre composites are projected to post the strongest 16.62% CAGR through 2030.

- By vehicle type, passenger cars held a 60.71% share of the automotive chassis market in 2024 and are forecast to expand at an 11.92% CAGR to 2030.

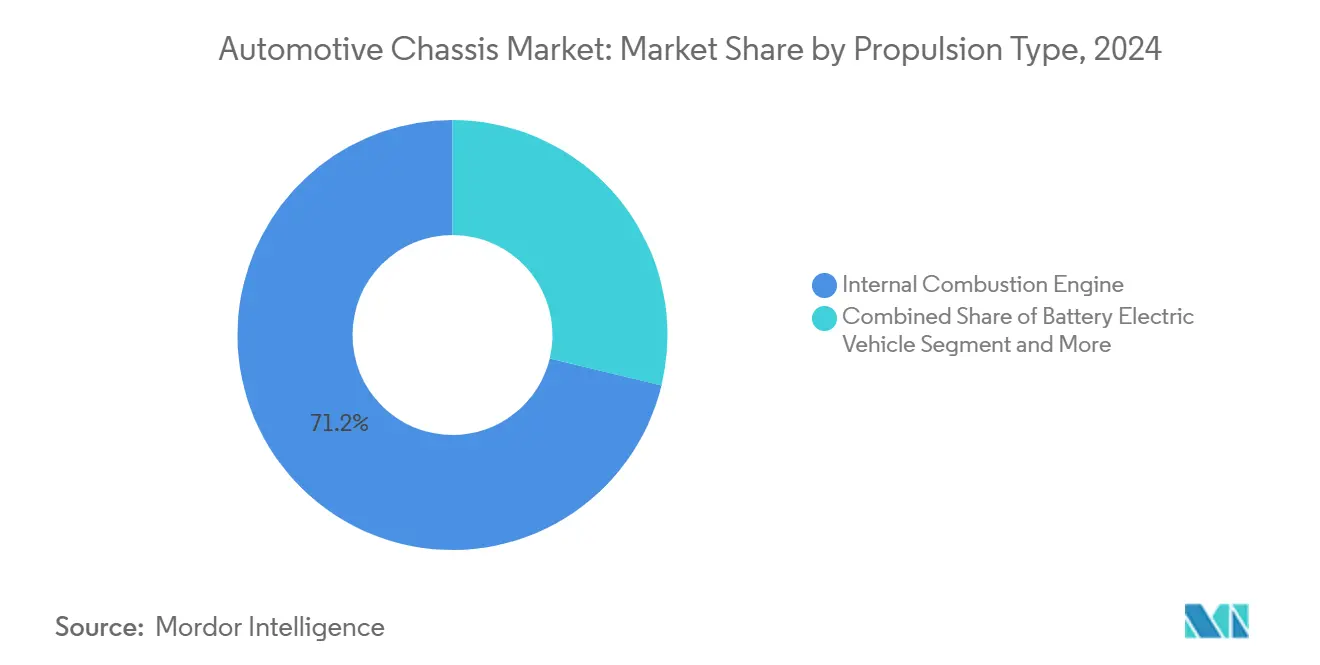

- By propulsion type, internal combustion engines retained 71.23% share of the automotive chassis market in 2024, while battery-electric vehicles registered the fastest 18.27% CAGR projected through 2030.

- By sales channel, OEM deliveries commanded an 84.41% share of the automotive chassis market in 2024, yet the aftermarket segment is set to grow at a 11.97% CAGR up to 2030.

- By geography, Asia-Pacific led with 48.37% automotive chassis market share in 2024 and is expected to log the quickest 11.82% CAGR during the forecast period.

Global Automotive Chassis Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Boom Driving Platform/Skateboard Chassis | +3.2% | Asia-Pacific core; spill-over to North America and Europe | Short term (≤ 2 years) |

| Lightweighting for Fuel Economy and Range Goals | +2.8% | Global; early gains in Europe, China, California | Medium term (2-4 years) |

| Megacasting and Structural Packs Unlocking New Value | +2.1% | China, Germany, United States | Medium term (2-4 years) |

| Stricter Crash Norms Raising Material Complexity | +1.9% | North America and Europe | Long term (≥ 4 years) |

| Coastal Corrosion Demand Boosting Coated Frames | +0.9% | Asia-Pacific and Gulf states | Medium term (2-4 years) |

| Flat-Floor Chassis Needed for Autonomous Pods | +0.7% | Urban centers worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging EV Production Driving Skateboard/Platform Chassis

Integrated skateboard frames now bundle battery, motor, steering, and telematics into a self-contained module that can cut vehicle development time by 18 months. U POWER Tech’s modular UP VAN chassis recently earned European WVTA certification, giving Chinese tier-1 suppliers direct access to EU fleets[1]“UP VAN Achieves WVTA Certification,”, U POWER Tech, upowertech.com. CATL’s cell-to-chassis “Bedrock” concept deletes the traditional enclosure and claims higher crash energy absorption than steel under-body trays. The skateboard shift reallocates margin from body-in-white to battery-pack producers and forces legacy suppliers to pivot toward thermal, sealing, and software domains.

Megacasting and Structural Battery Packs Creating New Value Pools

Tesla's pioneering gigacasting method has transformed vehicle manufacturing, streamlining the car body structure. By substituting numerous individual parts with just two sizable aluminium castings, Tesla has sped up production and cut costs. This innovation has led to its widespread adoption throughout the automotive sector.

Chinese automakers, including BYD, Tesla, and NIO, are at the forefront of integrated chassis technology, positioning China as a leader in electric vehicle (EV) production. Their leadership has enabled China to outpace Europe in adopting this advanced architecture.

Tightening Crash-Safety Norms Elevating Material Complexity

IIHS pedestrian-protection updates and NHTSA’s evolving FMVSS series drive multi-material cockpit cages that combine boron steel pillars with aluminium crush-boxes [2]“Pedestrian Protection Test Updates,”, IIHS, iihs.org. Fresher regulations require 25–35% additional frontal energy absorption versus 2020 baselines, pushing OEMs toward tailor-welded blanks and 4-layer laminate floorpans that resist battery intrusion [3]“FMVSS Regulatory Docket,”, NHTSA, nhtsa.gov. Speciality players such as Pierce Manufacturing are applying military-grade cataphoresis E-coats to chassis destined for emergency vehicles operating in corrosive environments. Hybrid joining processes—laser-assisted riveting, mixed-material adhesives, and friction-stir welding—have become mandatory skill sets for tier-1 suppliers, cementing high entry barriers for new entrants.

Coastal-Region Corrosion-Resistance Demand Boosting Coated Frames

In coastal and high-humidity regions, salt-laden air accelerates vehicle frame corrosion. Manufacturers now use advanced protective coatings to extend lifespans and reduce warranty claims. Schmitz Cargobull hot-dip galvanises semitrailer frames post-roll forming, offering long-term rust-through warranties. MOOG and HÖRMANN Automotive enhance durability with cathodic-dip primers and powder topcoats for harsh environments like the Gulf states.

IGL’s Aegis kit for 4×4 enthusiasts in the aftermarket features a self-healing polymer that seals minor surface damage, ensuring quick protection and low maintenance. Though premium coatings raise initial costs, they reduce repairs in corrosive climates, emphasising lifecycle value and regional customisation.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CapEx for Composite/Multi-Material Production | -2.1% | Worldwide; smaller suppliers disadvantaged | Medium term (2-4 years) |

| Raw Material Price Swings (Steel, Aluminum, CFRP) | -1.8% | Global; import-dependent regions most exposed | Short term (≤ 2 years) |

| EV Weight Pressuring GVWR and Fleet Economics | -1.2% | North America and Europe commercial fleets | Medium term (2-4 years) |

| Skilled Labor Shortage in Advanced Bonding Techniques | -0.9% | North America core; spill-over to Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Steel, Aluminum, CFRP)

Amidst significant price swings in steel and aluminium markets, the automotive sector is reshaping its sourcing strategies. These fluctuations have disrupted quarterly procurement plans and complicated cost forecasting. In response, manufacturers are increasingly turning to financial hedging tools. Notably, there's a surge in demand for forward contracts, especially among auto forging suppliers, underscoring their heightened sensitivity to commodity price shocks.

Skilled-Labour Shortages in Advanced Joining/Bonding

Advanced vehicle production grapples with labour shortages, especially in specialised welding and bonding roles. In response, OEMs are aggressively turning to automation. While this move helps sustain production levels, it simultaneously escalates capital expenditures and brings new challenges, notably cybersecurity and system integration. This transition highlights the increasing importance of workforce development in tandem with technological investments.

Segment Analysis

By Chassis Type: Monocoque Dominance Drives Integration

Monocoque frames accounted for 67.22% of 2024 revenue, reflecting OEM preference for single-shell bodies that integrate battery trays and crumple zones. This dominance equated to the largest slice of the automotive chassis market share for the year. Ladder frames, although niche, are projected to score the fastest 13.23% CAGR as electric pickups and off-road SUVs gain traction. The automotive chassis market size tied to ladder platforms will scale rapidly as repairability and modular cargo beds outweigh efficiency penalties.

Monocoque integration lowers parts count, simplifies sealing, and helps pass new IIHS small-overlap crash tests, yet it complicates collision repair. Ladder frames preserve ease of body swaps and appeal to fleet upfitters such as INEOS Automotive, whose Grenadier Quartermaster exposes 1.5 m of rear frame rails for box conversions. Future composite ladder variants may blend glass fibre rails with aluminium cross-members to cut 80 kg in Class 3 trucks, closing the mass gap with monocoques while retaining modularity.

By Material Type: Steel Resilience Meets Carbon-Fiber Innovation

Steel supplied 65.28% of chassis revenue in 2024, due to affordable high-strength recipes, cementing the segment’s largest automotive chassis market share. Aluminium occupies most premium EV platforms, while carbon fibre composites expand at a 16.62% CAGR as cost curves bend downward. The automotive chassis market size attributable to carbon fibre remains modest but rising as track-legal supercars and top-tier SUVs adopt woven tubs.

Magnesium remains an X-factor: semi-solid wheels and subframes shed double-digit kilograms, yet galvanic corrosion hurdles restrict OEM take-up. Material road maps centre on mixed-metal knuckles, fibre-reinforced battery enclosures, and overmolded polypropylene ribs that distribute impact loads.

By Vehicle Type: Passenger-Car Electrification Leads Transformation

Passenger cars captured 60.71% of 2024 revenue and will widen share on an 11.92% CAGR run-rate as compact crossovers transition to battery-electric skateboard frames. Light commercial vans surf e-commerce demand but confront payload penalties described earlier. The automotive chassis market size tied to passenger cars consequently dwarfs other categories, positioning them as test beds for megacasting and structural packs.

Commercial chassis innovation trails but is accelerating: Ford’s E-Transit integrates an under-floor battery that doubles as a torsion beam, while BrightDrop’s Zevo platform exploits dual 400 V motor units to simplify driveshaft packaging. Bus and coach frames add stainless-steel reinforcements around rooftop hydrogen tanks, foreshadowing later adoption of hollow-section composites. Across classes, crash-energy management and thermal-runaway containment dictate geometry choices more than legacy engine-mount considerations

By Propulsion Type: ICE Dominance Faces EV Disruption

Internal combustion layouts held 71.23% of 2024 revenue, yet battery-electric chassis volumes are rising at an 18.27% CAGR, compelling suppliers to redesign cross-members around 400–800 V packs. The automotive chassis market size associated with BEV platforms is predicted to double by the decade’s close. Hybrids and plug-ins provide interim volume but complicate packaging because exhaust paths compete with battery tunnels.

BEV chassis delete fuel-tank saddles, freeing designers to adopt flat-floor cabins or add structural battery stiffness. Fuel-cell skateboards demand crush-proof hydrogen tubes and ballistic protection, pushing metal-matrix composites to centre stage. Suppliers must juggle divergent R&D timetables: ICE volumes remain necessary for cash flow, yet BEV contracts dictate future viability.

By Sales Channel: OEM Integration Dominates Value Chain

OEM supply lines generated 84.41% of 2024 sales, underscoring the embedded nature of chassis co-development in vehicle programs. The aftermarket, while smaller, grows at a 11.97% CAGR as ageing fleets require replacement control arms, bushings, and electronic dampers. Performance enthusiasts seek coil-over kits and tubular sub-frames to compensate for EV weight, broadening the aftermarket scope.

OEM contracts favour suppliers that bundle hardware with software calibration; ZF’s chassis-control ECU pairs with adaptive ride modules to secure multiyear volume. Aftermarket innovators such as Dorman are scaling 400-m² drive-shaft plants to serve 15-year-old pickup models. Channel bifurcation will continue, with OEMs absorbing high-tech content and aftermarket players targeting niche upgrades and conversions.

Geography Analysis

Asia-Pacific produced 48.37% in 2024 and is set to log an 11.82% CAGR through 2030. The automotive chassis market in China is growing, reflecting BYD and NIO’s vertical integration push. Government rebates accelerate megacasting adoption, while provincial grants subsidise casting-sand recycling that trims per-kilogram costs.

North America ranks second in value as Tesla, GM, and Ford embed single-piece rear structures into crossover rollouts. The region’s average aluminium content per vehicle is growing, and Detroit plants are ordering 9,000-ton presses that match Fremont’s throughput. Canada’s magnesium-sheet pilot line demonstrates regional material diversification. U.S. IIHS and FMVSS updates reinforce multi-material crash cages, steering demand toward mixed-metal joining expertise.

Europe couples engineering services depth with stringent emission ceilings. Germany’s Tier-1 cluster around Baden-Württemberg leads in steer-by-wire and steel-aluminium tailor-welded blanks. The UK’s M-LightEn consortium underlines circular economy priorities, while Italy’s supercar valley anchors carbon-fibre know-how. Middle East and Africa remain emergent, with GCC bus makers specifying full-galvanized frames to handle 45 °C ambient operation and 3% road salt content. Latin America shows patchy electrification; Brazil’s new ProMovE program extends tax credits to aluminum-intensive chassis.

Competitive Landscape

The automotive supplier landscape shows moderate concentration, with a handful of major players—ZF, Magna, Continental, Aisin, and Gestamp—commanding over half of OEM sourcing volume. ZF’s 2024 Foxconn venture folds 3,800 employees and USD 4.7 billion revenue into a chassis-module entity that benefits from Taiwan’s semiconductor logistics [4]“Foxconn Joint Venture Press Release,”, ZF, zf.com. Magna’s eBeam axle launch targets 3-ton pickups and captures Ford and GM contracts, while Continental’s Advanced Lateral Dynamics platform couples brake-by-wire with 48 V roll stabilisation.

Disrupters tilt the playing field. Tesla internalises gigacasting and structural packs, shrinking the sourcing scope for external cross-members. Chinese entrants such as U POWER Tech license skateboard tool-kits that let mid-tier OEMs skip five-year platform cycles. Schaeffler pivots to mechatronics, signing rear-wheel-steer deals that multiply content per vehicle.

Strategic plays revolve around capital scale and software integration. Honda’s USD 1 billion megacasting retrofit lands a 2026 production start, echoing Volvo’s Swedish line that will cast complete front tubs. Gestamp funds an in-house scrap-melting circuit to hedge aluminium volatility. Suppliers without die-casting muscles woo clients through mini-casting for low-volume exotics or hybrid laminates that avoid 9,000-ton presses.

Automotive Chassis Industry Leaders

ZF Friedrichshafen AG

Magna International Inc.

Benteler International AG

Hyundai Mobis Co., Ltd.

Gestamp Automoción S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Constellium SE joined 'Project M-LightEn,' an initiative to develop ultra-lightweight, sustainable vehicle chassis structures. The Gordon Murray Group leads the project, with support from Innovate UK and the Advanced Propulsion Centre.

- April 2024: ZF Friedrichshafen AG and Hon Hai Technology Group (Foxconn) have established a joint venture focusing on passenger car chassis systems. The partnership structure consists of Foxconn acquiring a 50% stake in ZF Chassis Modules GmbH, creating an equal ownership arrangement between the two companies.

Global Automotive Chassis Market Report Scope

| Ladder Frame |

| Monocoque |

| Steel |

| Aluminum Alloy |

| Carbon Fiber Composite |

| Others |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (MHCVs) |

| Buses and Coaches |

| Internal Combustion Engine |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid EV (PHEV) |

| Hybrid EV (HEV) |

| Fuel-Cell EV (FCEV) |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Chassis Type | Ladder Frame | |

| Monocoque | ||

| By Material Type | Steel | |

| Aluminum Alloy | ||

| Carbon Fiber Composite | ||

| Others | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Medium and Heavy Commercial Vehicles (MHCVs) | ||

| Buses and Coaches | ||

| By Propulsion Type | Internal Combustion Engine | |

| Battery Electric Vehicle (BEV) | ||

| Plug-in Hybrid EV (PHEV) | ||

| Hybrid EV (HEV) | ||

| Fuel-Cell EV (FCEV) | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the automotive chassis market in 2030?

The market is forecast to reach USD 294.19 billion by 2030, reflecting an 11.76% CAGR.

Which region leads global chassis revenue?

Asia-Pacific held a 48.37% share in 2024, driven by China’s integrated casting capacity and India’s commercial-vehicle output.

How fast are battery-electric chassis volumes growing?

Battery-electric platforms are scaling at an 18.27% CAGR through 2030, outpacing every other propulsion type.

Which material shows the highest growth rate?

Carbon-fiber composites are expanding at a 16.62% CAGR as premium EVs and motorsport programs adopt ultralight tubs.

What challenge limits EV adoption in commercial fleets?

Heavy battery packs push gross-vehicle-weight ratings to regulatory limits, eroding payload capacity and hurting fleet economics.

Page last updated on: