Automotive Wiper Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

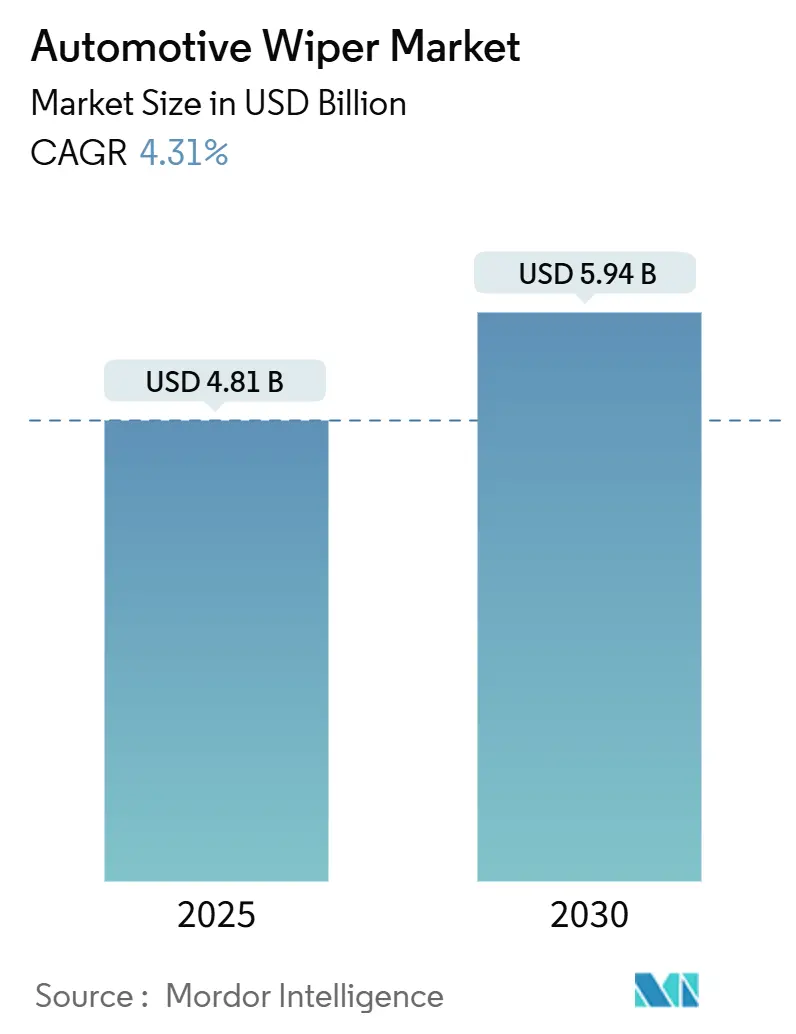

| Market Size (2025) | USD 4.81 Billion |

| Market Size (2030) | USD 5.94 Billion |

| Growth Rate (2025 - 2030) | 4.31% CAGR |

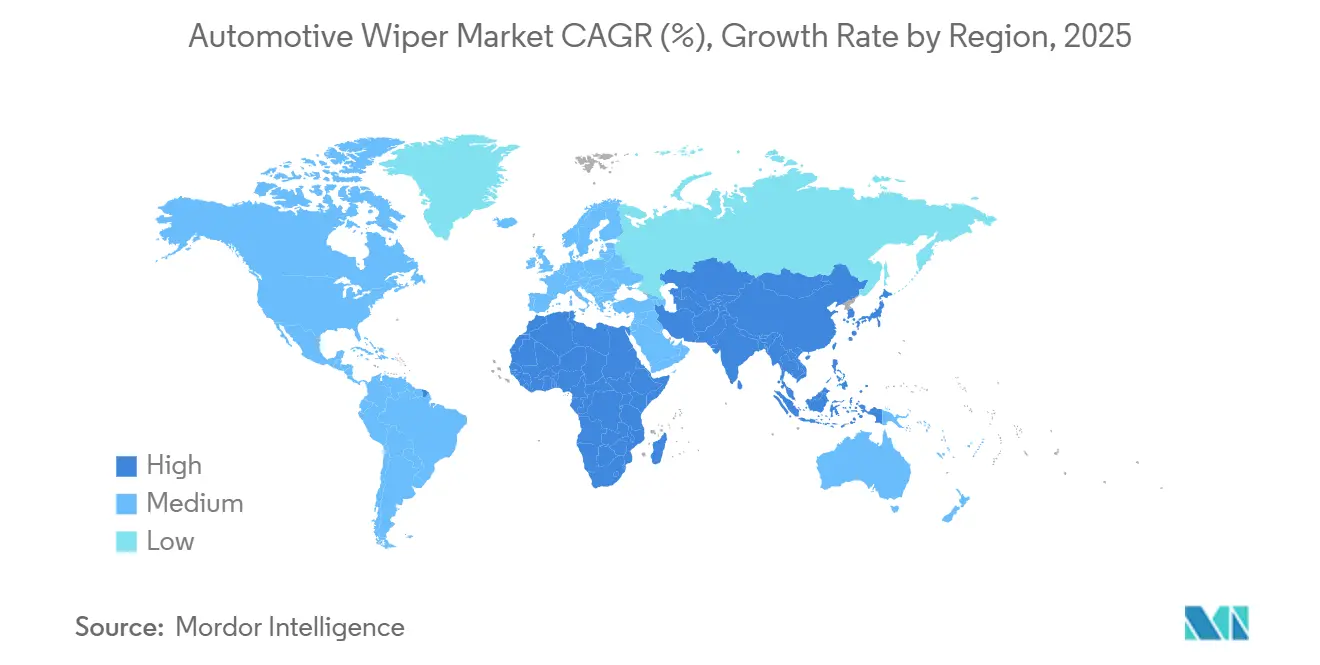

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Wiper Market Analysis by Mordor Intelligence

The automotive wiper market size stood at USD 4.81 billion in 2025 and is forecast to expand at a 4.31% CAGR to USD 5.94 billion by 2030. This trajectory reflects rising fitment rates of sensor-integrated wiping solutions, enforcement of camera-cleaning regulations, and engineering refinements that lower electrical draw for battery-electric platforms. The automotive wiper market is also benefiting from stronger replacement demand as weather volatility accelerates blade wear cycles, while aftermarket digitization widens access to premium products. Traditional bracket designs still dominate volumes, yet beam technology is advancing quickly as premium trims emphasize wind-lift resistance and rain-sensing activation. On the supply side, mid-tier manufacturers are forming joint ventures with motor specialists to secure brushless DC capability and hedge rare-earth magnet risk.

Key Report Takeaways

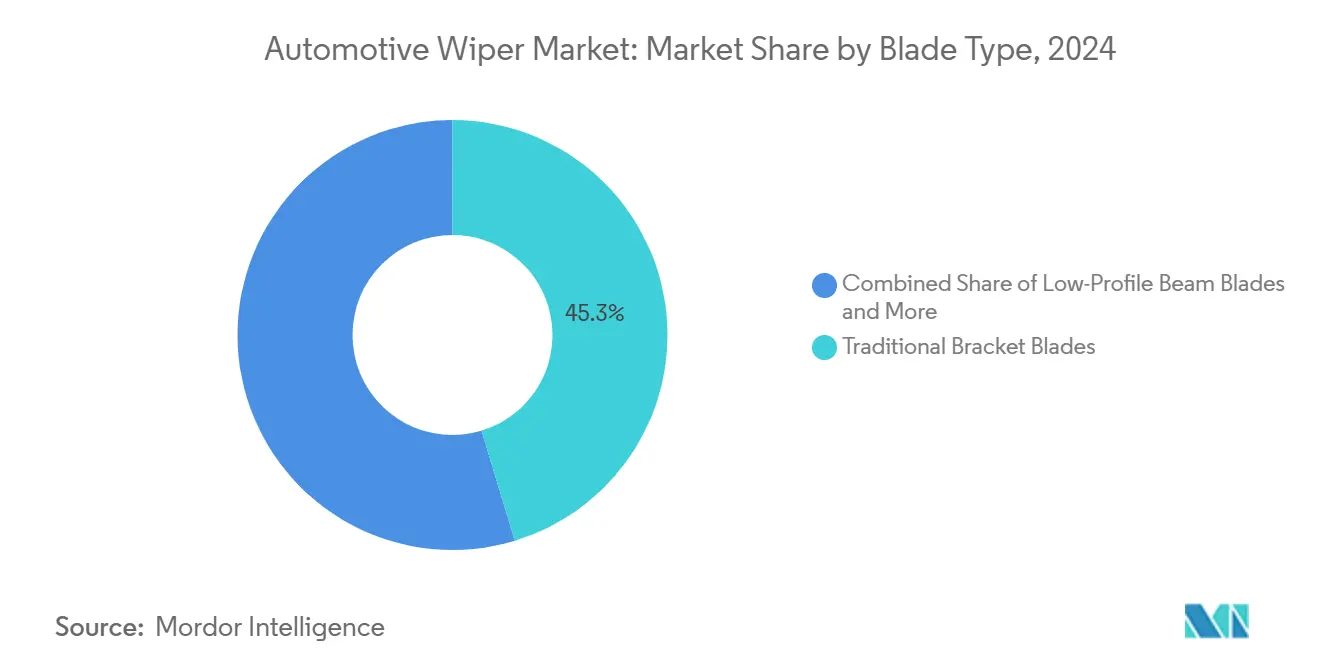

- By blade type, traditional bracket blades led with 45.32% of the automotive wiper market share in 2024, whereas beam blades are advancing at a 7.84% CAGR through 2030.

- By application type, windshields led the automotive wiper market with 70.06% of the market share in 2024, whereas headlights accounted for 8.53%.

- By vehicle type, passenger vehicles dominated the automotive wiper market with 60.41% of the market share in 2024, while BEVs captured 9.47%.

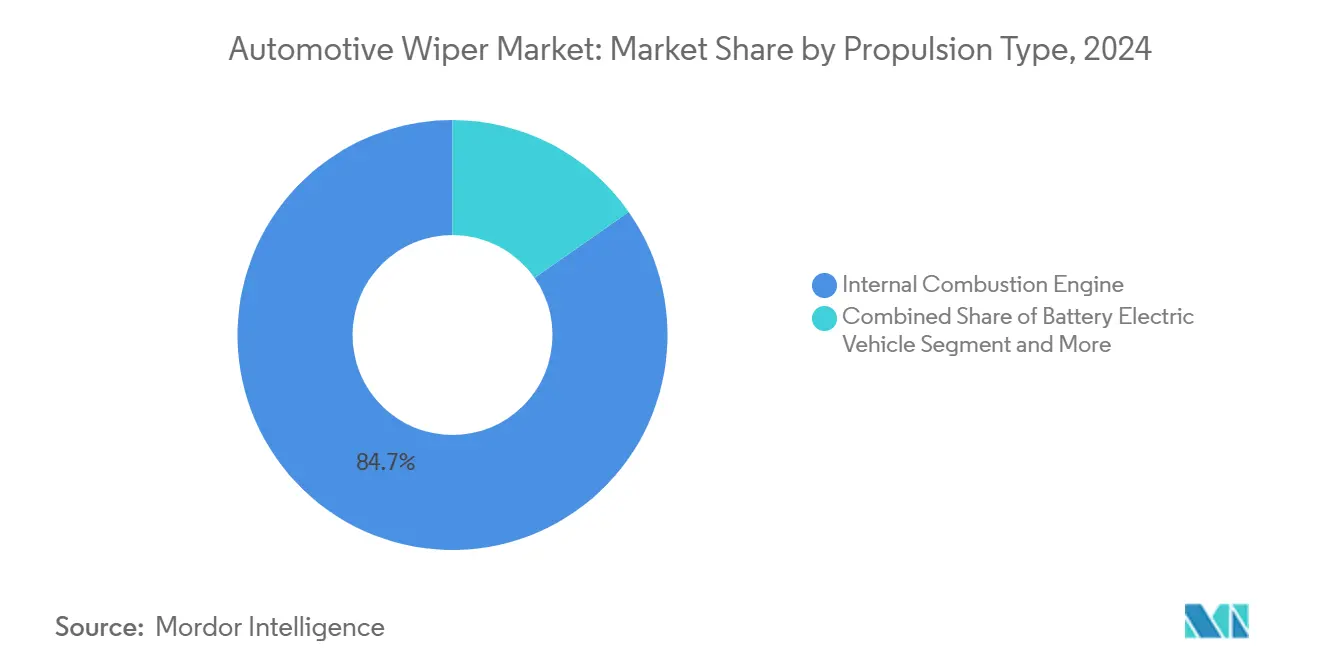

- By propulsion type, ICE vehicles held the largest share of the automotive wiper market at 84.73% in 2024, whereas BEVs represented 11.21%.

- By distribution channel, the aftermarket commanded 58.24% of the automotive wiper market size in 2024, and online aftermarket sales are growing at a 7.05% CAGR to 2030.

- By geography, Asia-Pacific captured a 44.92% revenue share in 2024; the Middle East and Africa region is projected to post the fastest 6.27% CAGR to 2030.

Global Automotive Wiper Market Trends and Insights

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rear-Wiper Fitment Surge in Compact SUVs and Crossovers | +0.8% | North America and Europe core, global uptake | Medium term (2–4 years) |

| Rain-Sensing Beam Blades Adopted in Premium Trims | +0.7% | North America and EU, rising in Asia-Pacific | Medium term (2–4 years) |

| ADAS Camera-Cleaning Compliance Regulations (EU 2026) | +0.6% | EU core, spill-over to global OEM specs | Short term (≤ 2 years) |

| EV-Specific Low-Power Wiper Motors for Range Gain | +0.5% | China and EU early, global long-term | Long term (≥ 4 years) |

| Cloud-Based Predictive-Maintenance Algorithms for Fleets | +0.3% | North America and EU commercial fleets | Long term (≥ 4 years) |

| India’s 2025 ISI Mandatory Winter-Blade-Durability Norm | +0.2% | India national, possible Asia-Pacific echo | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rear-Wiper Fitment Surge in Compact SUVs and Crossovers

The proliferation of compact SUVs and crossovers is driving unprecedented demand for rear wiper systems, as these vehicle architectures inherently require enhanced rear visibility due to their upright tailgate designs. This trend accelerated in 2024 when Hyundai added rear wipers to its Ioniq 5 in the 2025 model year update, responding to customer feedback about visibility challenges during adverse weather conditions. Conversely, some premium manufacturers like Porsche are monetizing rear wiper demand by offering it as a USD 370 option on the Macan EV, creating new revenue streams while testing consumer willingness to pay for previously standard features[1]"Porsche Charges Extra for the Macan EV's Rear Wiper," Edmunds, edmunds.com.. The compact SUV segment's continued expansion, particularly in emerging markets where these vehicles offer optimal urban maneuverability, ensures sustained rear wiper demand growth. Fleet operators increasingly specify rear wipers as mandatory equipment for commercial compact SUVs operating in diverse weather conditions, further solidifying this trend's impact on market dynamics.

Rain-Sensing Beam Blades Adopted in Premium Trims

Premium vehicle manufacturers are rapidly integrating rain-sensing beam blade systems as standard equipment, driven by consumer expectations for automated convenience features and superior wiping performance. Bosch's ENVISION wiper system exemplifies this trend, incorporating NightFocus technology that fuses base connector and blade into a single-core construction for uniform stability, while ClearMax 365 flexible dual synthetic rubber blend extends operational life under extreme weather conditions[2]"ENVISION™ Windshield Wipers for Sharper Night Visibility," boschautoparts.com.. The technology's appeal extends beyond convenience to safety, as rain-sensing systems activate within milliseconds of moisture detection, providing a faster response than manual activation during sudden weather changes. Beam blades' aerodynamic design reduces wind lift at highway speeds while maintaining consistent pressure distribution across the windshield surface, addressing performance limitations of traditional bracket systems. This premium positioning creates margin expansion opportunities for manufacturers while establishing technology differentiation that gradually filters down to volume segments, accelerating overall market adoption of advanced wiper technologies.

ADAS Camera Cleaning Compliance Regulations (EU 2026)

The European Union's General Safety Regulation (GSR2) mandates comprehensive ADAS systems for new vehicles by July 2026, creating unprecedented demand for camera cleaning solutions that maintain sensor functionality under all weather conditions. EU Regulation 2019/2144 specifically requires windscreen washing systems capable of cleaning vision zones A and B to specified performance standards, with zone A requiring 80% de-icing within 20 minutes and 90% demisting within 10 minutes. Forward-facing cameras mounted behind windshields near rearview mirrors demand precise alignment and unobstructed views, as even 1-degree misalignment can produce 1-foot detection offset at 100 yards, potentially causing pedestrian detection failures. This regulatory framework extends beyond Europe through global OEM standardization, as manufacturers adopt unified specifications across markets to achieve economies of scale. The compliance requirements create new technical specifications for wiper blade materials, washer fluid formulations, and nozzle positioning to ensure optimal camera performance while maintaining traditional visibility functions.

EV-Specific Low-Power Wiper Motors for Range Gain

Electric vehicle manufacturers are developing specialized low-power wiper motor systems to maximize driving range, as every watt of auxiliary power consumption directly impacts vehicle efficiency and customer satisfaction. Current wiper systems consume approximately 100 watts during operation, translating to roughly 9 meters of range reduction per hour of use, creating engineering incentives for power optimization. Brushless DC (BLDC) motor adoption is accelerating in EV applications, offering superior efficiency and precise speed control compared to traditional brush motors, though rare earth magnet shortages present supply chain challenges for widespread implementation. Mitsuba's reversing wiper system demonstrates advanced engineering approaches, using model-based development to create controllers that dynamically adjust motor angle for wind pressure compensation while enabling compact integration that improves aerodynamics. The system entered production with monthly shipments of 20,000-30,000 units, indicating commercial viability of sophisticated wiper motor technologies. These developments position EV-optimized wiper systems as a competitive differentiator in the expanding electric vehicle market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rubber-Compound Price Volatility | -0.7% | Global, with highest impact in cost-sensitive Asia-Pacific markets | Short term (≤ 2 years) |

| Counterfeit Blades in Price-Sensitive Markets | -0.4% | Asia-Pacific core, expanding to Latin America and Africa | Medium term (2–4 years) |

| Autonomous-Vehicle Optical Coatings Reducing Blade Need | -0.3% | North America and EU premium segments | Long term (≥ 4 years) |

| Shortage of Rare-Earth Magnets for BLDC Wiper Motors | -0.2% | Global, with supply chain concentrated in China | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rubber-Compound Price Volatility

Natural rubber price fluctuations significantly impact wiper blade manufacturing costs, with 2024 experiencing particularly acute supply chain disruptions due to weather-related production shortfalls in key growing regions. The automotive rubber compounds market faces additional pressure from competing demand in electric vehicle tire production, where specialized formulations command premium pricing and divert supply from traditional applications. Manufacturers must balance cost management with performance requirements, as inferior rubber compounds rapidly degrade under environmental stresses like ozone exposure and temperature cycling, leading to premature blade failure and customer dissatisfaction. This volatility forces wiper manufacturers to implement dynamic pricing strategies and explore alternative synthetic rubber formulations, though these substitutes often compromise performance characteristics essential for premium applications. The cost pressures particularly impact aftermarket segments where price sensitivity limits manufacturers' ability to pass through raw material increases, compressing margins and potentially driving consolidation among smaller suppliers.

Counterfeit Blades in Price-Sensitive Markets

Counterfeit wiper blades represent a growing threat across Southeast Asian markets, where substandard products undermine both safety and legitimate manufacturer revenues through deceptive packaging and distribution channels. These counterfeit products typically use inferior rubber compounds and inadequate metal components that fail prematurely, creating safety hazards during critical weather conditions while damaging windshield surfaces through poor contact pressure distribution. The proliferation of online marketplaces has facilitated counterfeit distribution, making it increasingly difficult for consumers to distinguish authentic products from sophisticated replicas that mimic legitimate brand packaging and documentation. Regulatory enforcement remains inconsistent across affected regions, allowing counterfeit operations to persist despite periodic crackdowns by authorities and industry associations. This market distortion particularly impacts aftermarket channels where price competition intensifies, forcing legitimate manufacturers to invest in anti-counterfeiting technologies and consumer education programs that increase operational costs while potentially reducing market share in price-sensitive segments.

Segment Analysis

By Blade Type: Beam Technology Gains Premium Traction

Traditional bracket blades maintained 45.32% market share in 2024, reflecting their cost-effectiveness and broad compatibility across vehicle platforms, while beam blades are experiencing rapid adoption at 7.84% CAGR (2025-2030) as manufacturers integrate advanced aerodynamic designs. Hybrid blades occupy the middle ground, combining bracket system durability with beam blade performance characteristics, appealing to consumers seeking enhanced performance without premium pricing. The shift toward beam blades accelerates in premium vehicle segments where manufacturers prioritize superior wiping performance and reduced wind noise, with Valeo's beam blade technology claiming coverage for 9 million European vehicles through its hybrid range[3]"Valeo Silencio™ Wiper Blades," valeoservice.com..

EU Regulation 2021/535 mandates specific performance standards for wiper systems, requiring coverage of 98% of vision zone A and 80% of vision zone B, driving manufacturers toward beam blade designs that provide more consistent pressure distribution across curved windshield surfaces. Traditional bracket systems remain dominant in cost-sensitive markets and commercial vehicle applications where durability and serviceability outweigh performance considerations. The technology evolution reflects broader automotive trends toward integrated systems that support ADAS functionality while maintaining traditional visibility requirements under diverse environmental conditions.

By Application Type: Headlight Cleaning Drives Innovation

Windshield wipers command 70.06% market share in 2024, representing the core application that defines market dynamics and technological development priorities. Headlight wipers are experiencing the fastest growth at 8.53% CAGR (2025-2030), driven by regulatory requirements for camera and sensor cleaning in ADAS-equipped vehicles. Rear wipers occupy a specialized niche that varies significantly by vehicle architecture, with compact SUVs and crossovers driving increased fitment rates as manufacturers respond to customer demands for enhanced rear visibility.

The headlight wiper segment's growth trajectory reflects the convergence of lighting technology and autonomous driving requirements, where LED and laser headlight systems require consistent cleaning to maintain optimal performance. UN Regulation No. 45 establishes technical requirements for headlamp cleaners, creating standardized performance benchmarks that drive system development. Windshield applications continue evolving through integration with washer fluid systems that incorporate specialized formulations designed to avoid optical distortion on ADAS camera lenses. Rear wiper applications face market pressure from aerodynamic optimization efforts, though safety considerations and consumer preferences maintain demand across most vehicle segments.

By Vehicle Type: Commercial Segments Embrace Durability

Passenger vehicles dominate with 60.41% market share in 2024, driven by global automotive production volumes and replacement market demand across diverse geographic regions. Light commercial vehicles and medium/heavy commercial vehicles collectively represent significant growth opportunities as fleet operators prioritize system reliability and maintenance optimization. The commercial vehicle segments demand enhanced durability specifications that withstand intensive operating conditions while minimizing maintenance intervals and operational disruptions.

Fleet applications increasingly specify predictive maintenance capabilities that integrate with vehicle telematics systems, enabling centralized monitoring and optimized replacement scheduling across vehicle populations. DENSO's comprehensive R&D capabilities, spanning 59 global centers with 19,000 engineers, support the development of commercial-grade wiper systems that meet stringent durability requirements. Passenger vehicle applications drive technological innovation through premium feature integration, while commercial segments focus on total cost of ownership optimization through extended service intervals and simplified maintenance procedures. The segmentation reflects broader automotive industry trends toward application-specific engineering that balances performance, durability, and cost considerations.

By Propulsion Type: Electric Platforms Reshape Requirements

Internal combustion engine vehicles maintain 84.73% market share in 2024, though battery electric vehicles are experiencing accelerated growth at 11.21% CAGR (2025-2030) as manufacturers optimize auxiliary systems for energy efficiency. Hybrid electric vehicles and plug-in hybrid electric vehicles represent transitional technologies that bridge conventional and electric architectures while maintaining traditional wiper system requirements. Fuel cell electric vehicles remain a niche segment with specialized requirements for cold-weather operation and system integration.

The electric vehicle transition creates new engineering challenges for wiper system design, particularly power consumption optimization and integration with regenerative braking systems that affect electrical load management. Mitsuba's reversing wiper system development demonstrates the sophisticated engineering required for EV applications, using model-based design to optimize power consumption while maintaining performance standards. Battery electric vehicles demand specialized motor controllers that minimize parasitic losses while providing precise speed control for varying weather conditions. The propulsion type segmentation increasingly influences wiper system specifications as manufacturers balance performance requirements with energy efficiency mandates across diverse vehicle platforms.

By Distribution Channel: Digital Transformation Accelerates

The aftermarket channel commands 58.24% market share in 2024, reflecting the replacement-driven nature of wiper blade consumption and the importance of distribution network reach. Online aftermarket sales are expanding at a 7.05% CAGR (2025-2030) as consumers embrace e-commerce platforms for automotive maintenance products. OEM channels maintain significant influence through original equipment specifications that establish performance benchmarks and brand preferences among consumers and service providers.

Vertu Motors' acquisition of Wiper Blades for GBP 3.5 million (USD 4.2 million) in 2022 exemplifies the consolidation trend in aftermarket distribution, where established automotive retailers expand digital capabilities through strategic acquisitions. The digital transformation enables enhanced customer experience through vehicle-specific fitment guidance and simplified ordering processes that reduce installation errors. Traditional brick-and-mortar distribution maintains importance for commercial fleet applications where technical support and bulk ordering capabilities provide value beyond product availability. The channel evolution reflects broader retail trends toward omnichannel strategies that combine digital convenience with traditional service capabilities.

Geography Analysis

Asia-Pacific leads the global automotive wiper market with a The 44.92% share in 2024, driven by robust automotive production across China, India, Japan, and South Korea, while also benefiting from expanding vehicle ownership in emerging economies throughout the region. The region's dominance reflects both manufacturing scale and growing domestic demand, as rising disposable incomes drive vehicle purchases across diverse market segments. China's position as the world's largest automotive market creates substantial OEM demand, while India's growing automotive sector benefits from government initiatives promoting domestic manufacturing and quality standards. Japan and South Korea contribute advanced technology development through companies like DENSO and Mitsuba, whose engineering capabilities support global wiper system innovation.

The Middle East and Africa represents the fastest-growing regional market at 6.27% CAGR (2025-2030), driven by expanding automotive infrastructure and increasing vehicle imports across Gulf Cooperation Council countries and emerging African markets. The region's growth trajectory reflects improving economic conditions and urbanization trends that drive vehicle adoption, though market development remains constrained by infrastructure limitations and import dependencies. Harsh environmental conditions across much of the region create demand for specialized wiper systems capable of handling sand, dust, and extreme temperatures, creating opportunities for manufacturers offering enhanced durability specifications.

North America and Europe maintain significant market positions through premium vehicle segments and advanced technology adoption, with regulatory frameworks like the EU's GSR2 driving innovation in ADAS-integrated wiper systems. European markets particularly benefit from stringent safety regulations that mandate enhanced windscreen cleaning capabilities, creating demand for sophisticated wiper technologies that support camera and sensor functionality. South America represents a developing market with growth potential constrained by economic volatility and currency fluctuations that impact automotive production and consumer purchasing power, though Brazil's automotive sector provides a foundation for regional market development.

Competitive Landscape

The automotive wiper market exhibits moderate consolidation with established players leveraging technological innovation and global manufacturing scale to maintain competitive positions. Valeo's claim as the worldwide leader in wiper systems, supported by 191 production sites and 59 R&D centers, demonstrates the importance of global reach and engineering capabilities in this market. Competition intensifies through technology differentiation, where companies like Bosch integrate advanced features such as NightFocus technology and ClearMax 365 rubber compounds to command premium pricing in aftermarket channels. The market structure enables both large-scale manufacturers and specialized suppliers to coexist, with companies like TRICO maintaining strong positions through product innovation and strategic partnerships despite industry consolidation pressures.

White-space opportunities emerge in predictive maintenance integration and EV-optimized systems, where traditional wiper manufacturers can leverage IoT connectivity and energy efficiency expertise to capture emerging market segments. DENSO's comprehensive approach to semiconductor integration and Factory-IoT implementation across 130 plants positions the company to capitalize on connected vehicle trends that extend beyond traditional wiper functionality.

Emerging disruptors focus on specialized applications such as autonomous vehicle sensor cleaning and aftermarket digital distribution, where established players may lack agility or domain expertise. The competitive landscape continues evolving through strategic acquisitions, technology partnerships, and geographic expansion as companies position themselves for the transition toward electrified and autonomous vehicle platforms.

Automotive Wiper Industry Leaders

-

Robert Bosch GmbH

-

Valeo SA

-

DENSO Corporation

-

Trico Products Corp.

-

Mitsuba Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Edmunds reported on Porsche's decision to offer rear wipers as a USD 370 option on the Macan EV, highlighting industry trends toward monetizing previously standard features while addressing customer demands for enhanced rear visibility in adverse weather conditions.

- September 2024: Bosch announced comprehensive commercial vehicle strategy reorganization, pooling system development and product management under a new business unit led by Jan-Oliver Röhrl, with implications for centralized wiper system development across truck and off-highway applications. The restructuring supports Bosch's target of EUR 80 billion Mobility sales by 2029 while addressing the shift toward software-defined vehicle architectures that require integrated wiper system connectivity.

Global Automotive Wiper Market Report Scope

| Traditional Bracket Blades |

| Low-Profile Beam Blades |

| Hybrid Blades |

| Windshield Wipers |

| Rear Wipers |

| Headlight Wipers |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Internal Combustion Engine |

| Battery Electric Vehicle |

| Hybrid Electric Vehicle |

| Plug-In Hybrid Electric Vehicle |

| Fuel Cell Electric Vehicle |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Blade Type | Traditional Bracket Blades | |

| Low-Profile Beam Blades | ||

| Hybrid Blades | ||

| By Application Type | Windshield Wipers | |

| Rear Wipers | ||

| Headlight Wipers | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Propulsion Type | Internal Combustion Engine | |

| Battery Electric Vehicle | ||

| Hybrid Electric Vehicle | ||

| Plug-In Hybrid Electric Vehicle | ||

| Fuel Cell Electric Vehicle | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Which blade type is growing fastest within global demand?

Beam blades are advancing at a 7.84% CAGR as premium vehicles adopt rain-sensing technology.

How large is Asia-Pacific’s share of worldwide sales?

Asia-Pacific held 44.92% of 2024 revenue, making it the largest regional contributor.

Why are low-power wiper motors important for electric vehicles?

They cut auxiliary draw by up to 30 watts, helping maximize driving range and supporting OEM efficiency targets.

Which distribution channel will show the highest growth to 2030?

Online aftermarket platforms are expanding at 7.05% CAGR as consumers shift to e-commerce for maintenance parts.

Page last updated on: