Automotive HVAC Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

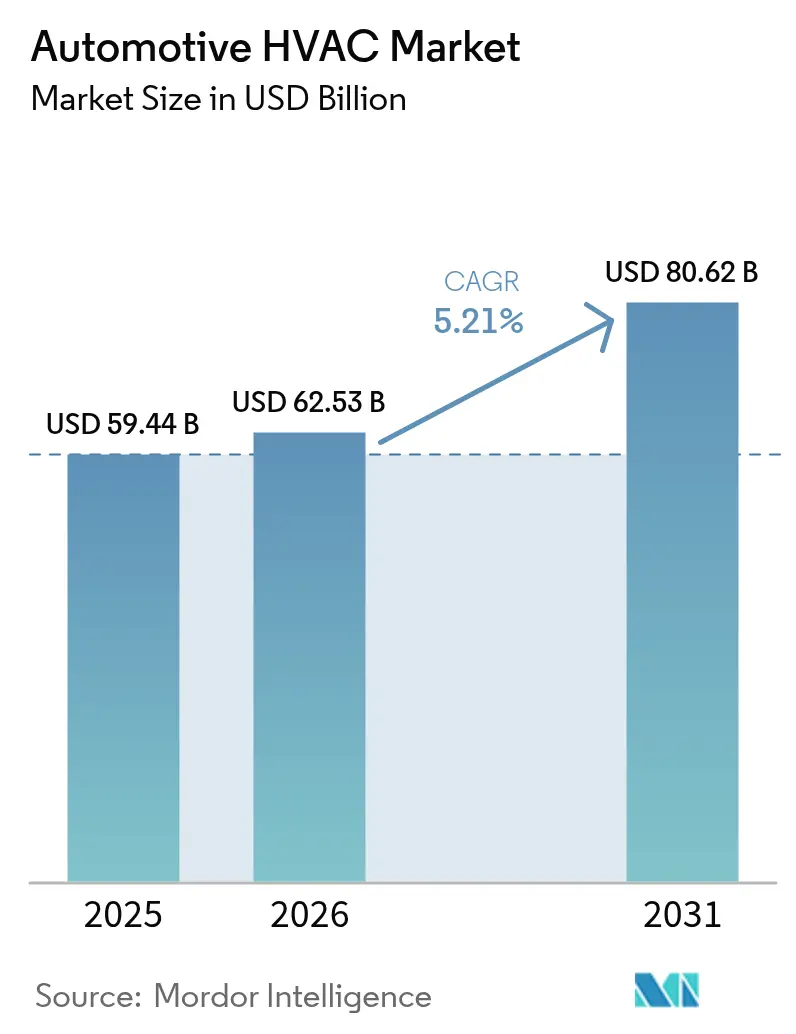

| Market Size (2026) | USD 62.53 Billion |

| Market Size (2031) | USD 80.62 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive HVAC Market Analysis by Mordor Intelligence

The automotive HVAC market size was valued at USD 59.44 billion in 2025 and estimated to grow from USD 62.53 billion in 2026 to reach USD 80.62 billion by 2031, at a CAGR of 5.21% during the forecast period (2026-2031). This steady expansion reflects the sector’s transition toward electrified powertrains, stricter comfort regulations, and rising consumer expectations. Asia-Pacific remains the principal manufacturing hub, and its tightening emissions rules spur continuous upgrades of thermal-management technology. Meanwhile, automatic climate-control systems enter mass-market vehicle lines, compressing the price premium that once confined them to luxury models. Component suppliers differentiate through electronic control, advanced filtration, and low-GWP refrigerant compatibility, repositioning HVAC from an auxiliary comfort module to a critical enabler of vehicle electrification.

Key Report Takeaways

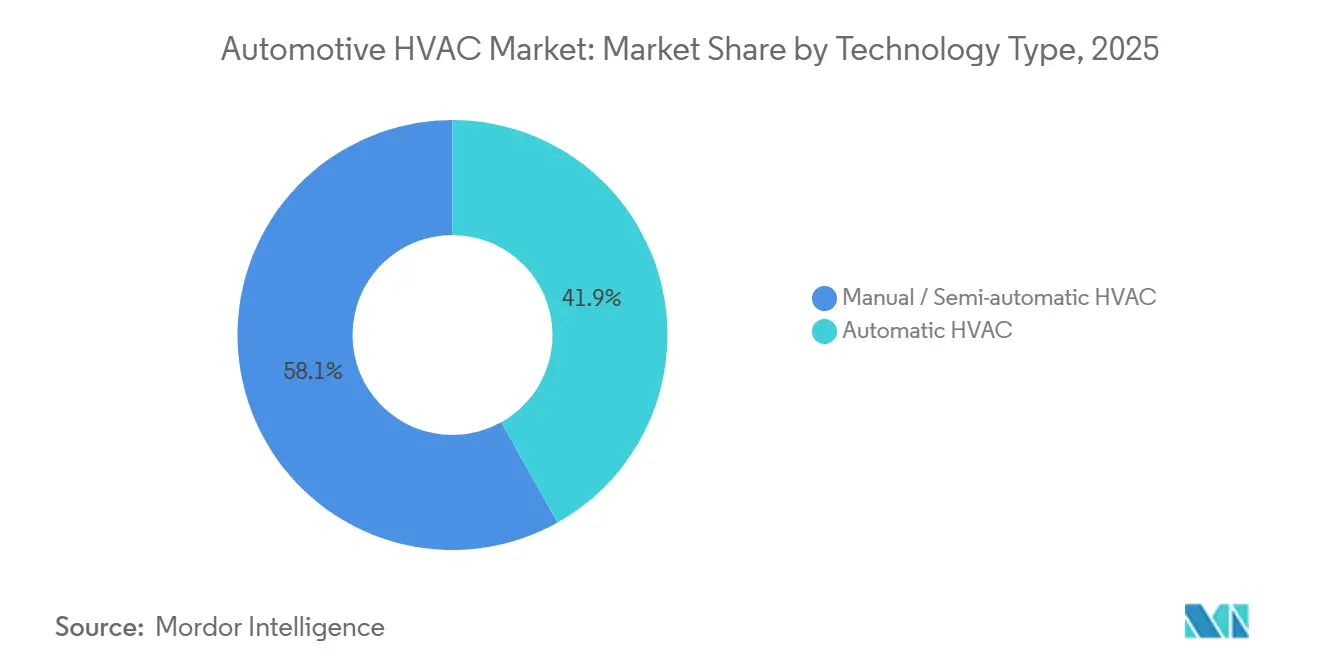

- By technology type, manual and semi-automatic systems led with 58.12% of the automotive HVAC market share in 2025, while automatic systems recorded the highest 9.25% CAGR through 2031.

- By vehicle type, passenger cars captured 79.62% of the automotive HVAC market share in 2025, whereas buses and coaches are set to grow at a 6.55% CAGR through 2031.

- By component, compressors held 32.10% of the automotive HVAC market share in 2025; electronic and sensor suites are advancing at a 6.78% CAGR to 2031.

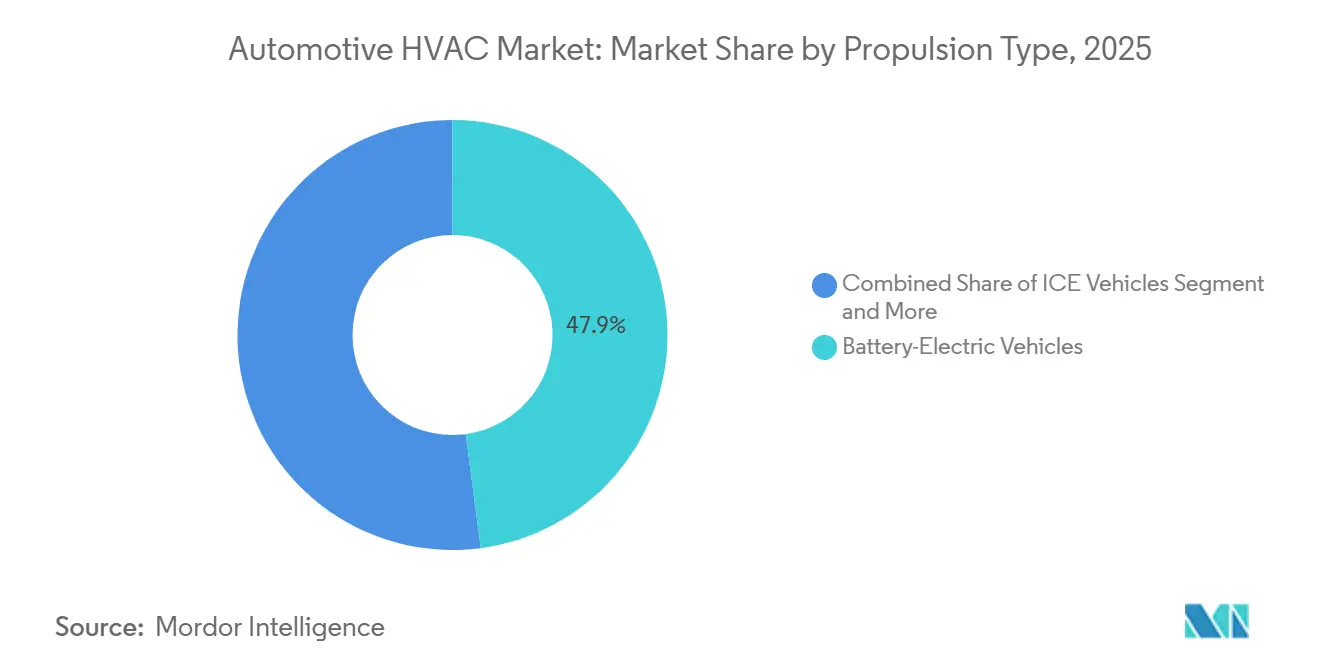

- By propulsion type, battery-electric vehicles commanded a 47.90% of the automotive HVAC market share in 2025 and are expanding at a 9.65% CAGR through 2031.

- By sales channel, OEM factory-fit installations accounted for 82.05% of the automotive HVAC market share in 2025, whereas the aftermarket is progressing at a 6.05% CAGR through 2031.

- By geography, Asia-Pacific dominated with 48.55% of the automotive HVAC market share in 2025; the region continues to post a 5.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive HVAC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HVAC Efficiency for EV Heat-Pumps | +1.5% | China, EU, North America | Long term (≥ 4 years) |

| Demand for Automatic Climate-Control | +1.2% | Global, premium uptake in North America and Europe | Medium term (2-4 years) |

| Focus on Cabin Air Quality | +0.9% | Global, regulation led by EU and North America | Short term (≤ 2 years) |

| Safety and Comfort Regulations | +0.8% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Ride-Hailing Fleet Retrofit Demand | +0.6% | Urban centers globally, APAC concentration | Medium term (2-4 years) |

| AI Predictive Zonal Climate Control | +0.4% | Premium segments in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

HVAC Efficiency Requirements for EV Heat-Pump Systems

BEV adoption turns HVAC into a range-critical subsystem. Heat pumps that achieve a coefficient of performance above 3.0 at –10 °C can save up to 11 kWh during a 300 km winter drive, mitigating the 40% range penalty seen with resistive heaters. Automakers integrate coolant loops among battery, power electronics, and cabin to harvest waste heat, prompting suppliers to deliver multi-port valves and inverter-driven compressors tuned for low-temperature vapor injection. Regulatory incentives that reward vehicle efficiency, such as China’s MIIT credits, incentivize OEMs to specify premium HVAC even for entry-segment EVs.

Demand for Automatic Climate-Control Comfort

Consumer preference for automatic systems intensifies as vehicles migrate to connected architectures that enable remote pre-conditioning, voice commands, and user-profile learning. Precise temperature maintenance reduces driver fatigue and distraction, aligning with safety priorities as SUVs with larger cabin volumes proliferate. OEMs bundle automatic HVAC with infotainment packages to lift average transaction prices, and falling sensor costs encourage deployment in compact models. Uptake accelerates in emerging economies where rising incomes elevate comfort expectations. In BEVs, automatic control also orchestrates energy-efficient cabin warming strategies that preserve battery state of charge during urban commutes.

Post-Pandemic Focus on Cabin Air-Quality and Filtration

Legislators now treat in-cab filtration as an occupational-health requirement rather than an optional comfort feature. Standards across the EU and parts of North America mandate removal efficiencies for PM 2.5 and VOC concentrations below 0.3 mg m-³. Suppliers respond with dual-layer filters embedded with activated-carbon media and UV-C sterilization modules compatible with R1234yf refrigerant flow paths [1]“Dual-Layer Cabin Air-Quality Solutions,” Valeo, valeo.com. Automakers market these upgrades as wellness solutions, strengthening brand differentiation and enabling subscription models for filter replenishment.

Safety and Comfort Regulations in Emerging Markets

Governments leverage HVAC mandates to combat driver heat stress, productivity loss, and accident rates. India will require air-conditioned cabins in all medium and heavy-duty trucks from October 2025, opening a retrofit opportunity for the legacy fleet. Comparable initiatives surface across Southeast Asia as regulators reconcile climate adaptation with supply-chain resilience. Compliance hinges on systems meeting IS14618:2022 performance criteria, pushing procurement toward certified suppliers and stimulating demand for retrofit kits that match restricted engine-power envelopes.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Cost and Complexity for HVAC | –0.7% | Price-sensitive markets in APAC and South America | Medium term (2-4 years) |

| HVAC Load Cutting EV Range | –0.6% | EV-focused markets globally | Long term (≥ 4 years) |

| Costly Low-GWP Refrigerant Transition | –0.5% | Global, compliance pressure in the EU and North America | Short term (≤ 2 years) |

| Technician Shortage for New Refrigerants | –0.4% | Global, acute in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Unit Cost and Complexity for Automatic HVAC

Electronic expansion valves, stepper-motor actuators, and multi-sensor clusters elevate bill-of-materials cost by up to 50% relative to manual systems, limiting penetration in entry-segment hatchbacks. Service networks require diagnostic scan tools and technician retraining, further inflating lifecycle expense. Semiconductor shortages introduce procurement volatility, encouraging OEMs in Brazil and Indonesia to delay standardization of automatic climate control despite consumer interest.

HVAC Load Cutting EV Driving-Range Targets

Extreme-climate markets such as Canada and Norway report significant range attrition when resistive cabin heating is engaged. Fleet purchasers may postpone BEV acquisition until heat-pump supply stabilizes, tempering growth in cold-weather regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Type: Automatic Systems Drive Premium Adoption

Automatic systems capture incremental share as sensor prices fall and OEMs exploit telematics platforms to deliver comfort subscriptions. In 2025, manual and semi-automatic solutions still dominated with a 58.12% of the automotive HVAC market share in 2025. However, automatic setups will expand at a 9.25% CAGR through 2031, adding nearly USD 16.8 billion in incremental value. AI-based learning profiles elevate the user experience, while integration with battery preconditioning benefits BEVs.

Standardizing single-zone automatic control in C-segment cars compresses the cost gap relative to manual rotary dials. In premium models, dual- and tri-zone configurations underpin add-on pricing. Suppliers that mastered in-house algorithm development now cross-sell software consultancy, while legacy mechanical firms partner with microcontroller specialists to stay competitive.

By Vehicle Type: Commercial Segments Accelerate Adoption

Passenger cars account for 79.62% of the automotive HVAC market share in 2025, yet buses and coaches will outpace at a 6.55% CAGR to 2031 as governments legislate passenger comfort mandates. Ride-sharing minibus services favor roof-mounted units with integrated HEPA filtration to win municipal contracts.

Light commercial vehicles serving last-mile logistics adopt auxiliary electric air-conditioning to allow engine-off parcel drops, reducing idling penalties in low-emission zones. Medium and heavy trucks in India, Indonesia, and Mexico shift toward factory-fit AC to comply with new safety rules, enlarging volume for robust compressor designs that tolerate dusty duty cycles.

By Component: Electronics Enable Smart Thermal Management

Compressors maintained a 32.10% of the automotive HVAC market share in 2025 as variable-speed scroll designs became mainstream. Yet electronic and sensor suites will climb at 6.78% CAGR, reflecting demand for cabin-air-quality sensing, humidity detection, and zonal occupancy mapping.

Electronic expansion valves raise efficiency by modulating refrigerant flow in response to high-resolution pressure feedback. Integrated control units consolidate HVAC logic onto the vehicle’s domain controller, reducing wiring harness length and boosting cybersecurity requirements. Suppliers with software over-the-air capabilities generate annuity revenue by selling energy-optimization updates, altering the traditional once-per-vehicle sales model.

By Propulsion Type: Battery-Electric Vehicles Lead Innovation

Battery-electric vehicles (BEVs) already had 47.90% of the automotive HVAC market share in 2025 due to their intrinsic reliance on sophisticated thermal control. They will grow the fastest, at 9.65% CAGR through 2031. System architectures couple cabin conditioning with battery thermal management to extend cell longevity and charging performance.

Hybrids and plug-in hybrids use dual-source heat systems that prioritize electric compressors but revert to engine coolant under high load. ICE vehicles remain relevant in regions with limited charging infrastructure, but their share erodes as regulatory tailwinds favor zero-emission transport. Suppliers with early-stage heat-pump patents capture disproportionate design wins in global EV platforms.

By Sales Channel: Aftermarket Growth Reflects Service Complexity

OEM factory installations captured 82.05% of the automotive HVAC market share in 2025, mirroring the need for precise calibration and system integration at the assembly line. Still, the aftermarket is projected to register a 6.05% CAGR, buoyed by ride-hailing retrofits, low-GWP refrigerant conversions, and mandatory AC installations in aging truck fleets.

Distribution consolidates around networks that can finance R1234yf service machines and remote-diagnostic portals. Component makers bundle training memberships with compressor kits, creating sticky revenue while safeguarding correct installation. Independent garages partner with parts retailers that offer cloud-based repair manuals and refrigerant tracking tools, heightening professionalism across the service ecosystem.

Geography Analysis

Asia-Pacific commanded 48.55% of the automotive HVAC market share in 2025 and is set to maintain the lead with a 5.55% CAGR through 2031. China’s 2025 NEV sales quota compels local OEMs to adopt integrated heat-pump modules that operate efficiently in -20 °C northern winters. India’s blanket AC mandate for heavy trucks fuels bulk orders for rugged compressors built to tolerate high vibration. Japan and South Korea export high-precision electronic expansion valves, reinforcing the region’s value-chain completeness.

North America reflects a mature yet technologically progressive market. Pickup trucks and SUVs require high-capacity condensers to serve large cabin volumes, and frigid climates in Canada and the northern United States validate the performance of cold-weather heat pumps. Mitsubishi Electric’s USD 143.5 million retrofit of its Kentucky plant for variable-speed compressor lines underscores the region’s strategic focus on domestically sourced HVAC for EV applications.

Europe enforces the most aggressive low-GWP refrigerant timeline, accelerating the adoption of R1234yf and pushing suppliers toward natural refrigerant R744 prototypes for post-2030 compliance. Urban bus electrification programs in Germany and France stipulate energy-efficient heat-pump systems to meet tender requirements. ISO 13043:2011 sets performance benchmarks that ripple through supplier quality management systems, ensuring system integrity across the continent.

Competitive Landscape

Key players like Denso, Valeo, Hanon Systems, and MAHLE dominate the automotive HVAC market, capitalizing on established OEM relationships and their own vertically integrated compressor lines to secure a significant market share. Differentiation revolves around system-level software, extreme-temperature heat-pump efficiency, and filtration efficacy. Hankook & Company’s acquisition of Hanon Systems strengthens its competence in integrated thermal management and secures access to European EV programs [3]“Acquisition of Hanon Systems,” Hankook & Company Group, hankook.com.

Patents cluster around multifunctional thermal modules and predictive diagnostics. Sanhua Automotive scales rapidly in China, bundling heat pump, expansion valve, and electronic control to supply domestic NEV champions. European suppliers invest in cybersecurity certification to safeguard connected HVAC controllers, while North American players co-develop over-the-air energy-optimization algorithms with infotainment-system integrators.

Price competition abates as OEMs prioritize efficiency gains that unlock higher real-world EV range. The transition to low-GWP refrigerants, requiring redesigned heat exchangers, increases switching costs and thus entrenches incumbent platforms. Tier-1 suppliers with global service footprints assist automakers in technician training and refrigerant recycling, further deepening customer lock-in.

Automotive HVAC Industry Leaders

Denso Corporation

Valeo Group

Hanon Systems Co., Ltd.

MAHLE GmbH

Sanden Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Valeo secured a contract to supply its Dual-Layer HVAC system to a major Chinese automaker, aiming to enhance cabin comfort while reducing emissions.

- July 2025: DRiV, a Tenneco division, introduced Wagner HVAC components—including radiators, condensers, and blower motors—to the United States and Canadian aftermarket channels.

- December 2024: Mitsubishi Electric announced a USD 143.5 million investment to retrofit its United States plant for variable-speed compressors, with production slated for 2027.

Global Automotive HVAC Market Report Scope

Heating, ventilation, and air conditioning (HVAC) is the technology used to maintain the vehicle's internal climate. It helps maintain the interior temperature (hot/cold) and thus provides comfort for onboard passengers.

The Automotive HVAC Market is segmented by Technology Type (Manual/Semi-Automatic and Automatic), Vehicle Type (Passenger Cars and Commercial Vehicles), and Geography (North America, Europe, Asia-Pacific, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Manual / Semi-automatic HVAC |

| Automatic HVAC |

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Medium and Heavy Commercial Vehicles |

| Buses and Coaches |

| Compressor |

| Condenser |

| Evaporator |

| Expansion Valve / Orifice Tube |

| Receiver-Dryer and Accumulator |

| Electronic and Sensor Suite |

| ICE Vehicles |

| Hybrid and Plug-in Hybrid Vehicles |

| Battery-Electric Vehicles |

| OEM Factory-Fit |

| Aftermarket Retro-Fit and Service |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology Type | Manual / Semi-automatic HVAC | |

| Automatic HVAC | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCV) | ||

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| By Component | Compressor | |

| Condenser | ||

| Evaporator | ||

| Expansion Valve / Orifice Tube | ||

| Receiver-Dryer and Accumulator | ||

| Electronic and Sensor Suite | ||

| By Propulsion Type | ICE Vehicles | |

| Hybrid and Plug-in Hybrid Vehicles | ||

| Battery-Electric Vehicles | ||

| By Sales Channel | OEM Factory-Fit | |

| Aftermarket Retro-Fit and Service | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the automotive HVAC market by 2031?

The market is expected to reach USD 80.62 billion by 2031, growing at a 5.21% CAGR from 2026.

Which vehicle propulsion type drives the fastest HVAC growth?

Battery-electric vehicles lead with a 9.65% CAGR, reflecting their need for energy-efficient heat-pump systems.

Why are automatic HVAC systems gaining popularity in emerging economies?

Falling sensor prices and consumer premiumization trends make automatic climate control more affordable, while regulations increasingly favor comfort and safety.

Which region dominates the automotive HVAC market?

Asia-Pacific holds 48.55% of global revenue and maintains leadership through large-scale vehicle production and stringent emissions policies.

Page last updated on: