Israel Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.5 Billion |

| Market Size (2026) | USD 0.52 Billion |

| Market Size (2031) | USD 0.64 Billion |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Israel Corrugated Packaging Market Analysis by Mordor Intelligence

The Israel corrugated packaging market size is expected to increase from USD 0.52 billion in 2026 to reach USD 0.64 billion by 2031, growing at a CAGR of 4.24% over 2026-2031. Solid retail demand, regulatory support for recycled content, and the rapid expansion of e-commerce and quick-commerce platforms underpin volume growth. Brand owners are favoring thinner flutes and digitally printed graphics that speed shelf replenishment and lift visual impact, while converters prioritize feedstock security amid volatile kraft-pulp prices. Government grants for new sorting facilities tighten the loop between household collection and mill recycling, progressively displacing virgin imports. At the same time, food processors and fresh-produce exporters maintain a structural need for high-performance, moisture-resistant grades that preserve cold-chain integrity.

Key Report Takeaways

- By material type, the recycled linerboard segment captured 51.78% of the Israel corrugated packaging market share in 2025.

- By flute type, the Israel corrugated packaging market size for e flute is projected to grow at an 5.44% CAGR through 2031.

- By packaging type, the regular slotted containers segment captured 43.38% of the Israel corrugated packaging market share in 2025.

- By wall type, the Israel corrugated packaging market size for triple-wall is projected to grow at an 5.31% CAGR through 2031.

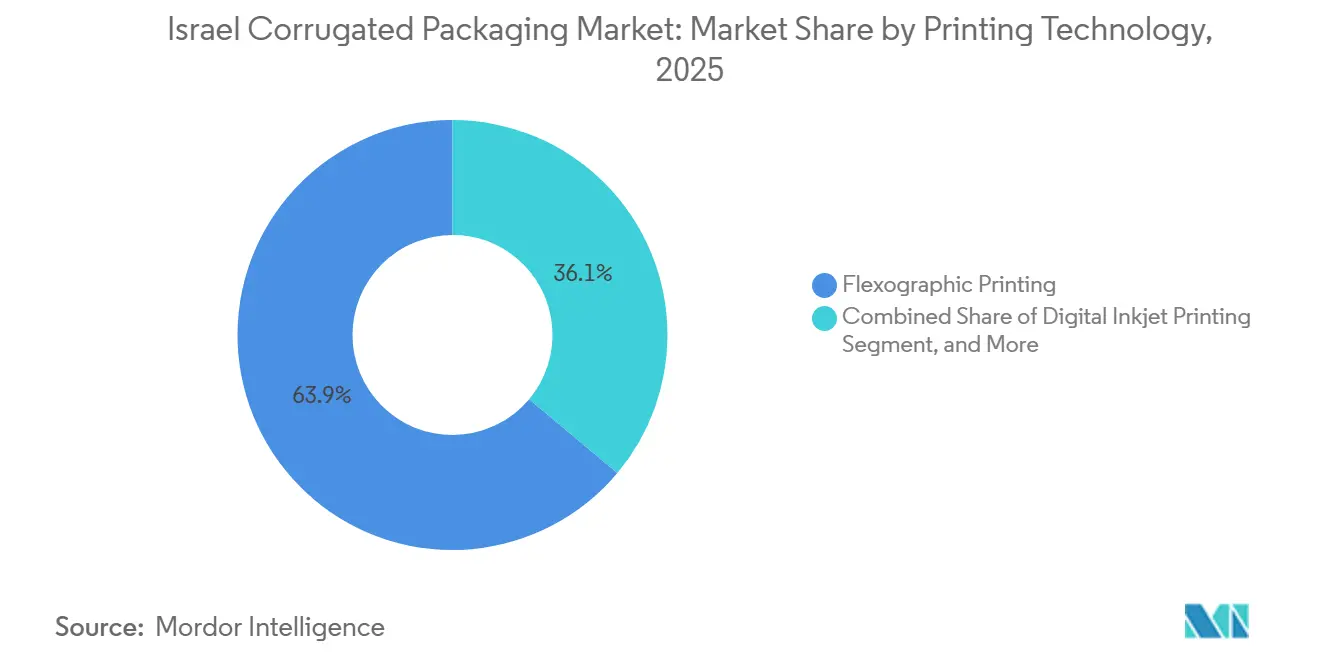

- By printing technology, the flexographic printing segment captured 63.91% of the Israel corrugated packaging market share in 2025.

- By end-user industry, the Israel corrugated packaging market size for e-commerce fulfillment centers is projected to grow at an 4.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Israel Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Penetration of E-Commerce and Quick-Commerce Channels | +1.2% | National, concentrated in Tel Aviv, Jerusalem, Haifa metropolitan areas | Medium term (2-4 years) |

| Expansion of Israel's Fresh Produce Export Corrugate Standards | +0.9% | National, with export hubs near Ashdod and Haifa ports | Long term (≥ 4 years) |

| Brand Owners' Shift Toward High-Graphic Retail-Ready Packs | +0.8% | National, led by major retail chains in urban centers | Short term (≤ 2 years) |

| Government Packaging Waste Targets Boosting Recycled Content | +0.7% | National | Medium term (2-4 years) |

| Start-Up Adoption of Molded-Fiber Hybrid Liners | +0.3% | National, early adoption in Tel Aviv tech corridor | Long term (≥ 4 years) |

| Defense Cold-Chain Corrugates for Biologics and UAV Parts | +0.2% | National, concentrated near defense manufacturing zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Penetration of E-Commerce and Quick-Commerce Channels

Online retail platforms continue to reorder packaging specifications, demanding smaller footprints that cut dimensional-weight fees and withstand high-velocity last-mile delivery. Order fragmentation drives converters toward short-run setups, making digital inkjet lines and E or F flute builds essential for meeting surge demand without excess inventory. Quick-commerce operators in Tel Aviv, Jerusalem, and Haifa are further tightening delivery windows, encouraging light yet crush-resistant formats that preserve product aesthetics upon arrival. Grocery baskets now lean toward single-serve SKUs, shaping a rising need for die-cut custom boxes capable of high-graphic treatments and variable-data printing. Converters who can synchronize design portals with fulfillment software secure repeat business by reducing lead times to under 7 days.

Expansion Of Israel's Fresh Produce Export Corrugate Standards

Citrus, avocado, and vegetable shippers must meet European moisture-barrier metrics and ventilated-pack benchmarks, driving demand for wax-alternative coatings and micro-perforated liners that extend shelf life without condensation. As exporters seek documented recycled-content shares aligned with EU directives, domestic mills increase blending ratios of recovered fiber to maintain certification pathways. Hubs at Ashdod and Haifa coordinate cold-chain corridors that integrate smart sensors and humidity cushions, placing a premium value on structural consistency across multi-temperature legs. Over time, semi-chemical fluting gains share within pallet-grade boxes, balancing rigidity and reduced basis weight to mitigate airfreight charges.

Brand Owners Shift Toward High-Graphic Retail-Ready Packs

Food and beverage manufacturers replace plain brown transit cartons with shelf-ready formats that travel directly from distribution centers to store aisles. Digital inkjet presses now achieve litho-laminated quality at speeds beyond 9,000 m² hr-¹, allowing seasonal artwork changes without flexo plate delays. Retail chains award contracts to converters that guarantee eight-color resolution and water-based inks approved for indirect food contact. As shelf facings shrink, marketing teams rely on vivid imagery and QR codes to trigger mobile engagement, moving packaging from a protective cost to a conversion tool. The pivot lifts average square-meter printing revenues and justifies capital expenditure for single-pass presses.

Government Packaging Waste Targets Boosting Recycled Content

Legislative amendments to the Packaging Law require producers to finance take-back systems, compelling converters to lift recycled-fiber incorporation toward the ministry’s 51% recycling aim for 2030.[1]TMIR Packaging Recycling Corporation, “The Packaging Law,” TMIR.ORG.IL Municipal grants worth ILS 3.99 billion (USD 1.05 billion) fund new sorting lines that increase recovered fiber availability, yet the rollout also reduces landfill capacity and pushes gate fees higher for low-grade waste. Mills equipped with de-inking and coarse-screen circuits secure stable feedstock, while kraft-import-dependent converters face cost risk as virgin pulp attracts carbon surcharges. End-markets reward compliance labels, allowing recycled linerboard to command a sustainable-premium even when grammage drops.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Imported Kraft Pulp Prices | -0.6% | National, affecting all converters reliant on virgin fiber imports | Short term (≤ 2 years) |

| Supply Uncertainty of Natural Gas for Paper Mills | -0.4% | National, concentrated at Hadera Paper mill operations | Medium term (2-4 years) |

| Labor Shortages in Skilled Flexo Press Operators | -0.3% | National, acute in industrial zones near Lod, Petah Tikva | Medium term (2-4 years) |

| Export Container Congestion at Ashdod and Haifa Ports | -0.3% | National, affecting import-export logistics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility In Imported Kraft Pulp Prices

Spot kraft quotes move sharply with freight-rate swings and exchange-rate shifts, and converters under fixed-price sales contracts struggle to recover costs inside a 60-90 day lag. Smaller plants without hedging instruments absorb margin hits that delay machinery upgrades or force production pauses. Price spikes also intensify substitution toward recovered linerboard, yet moisture-critical export boxes still demand virgin top liners, preserving exposure. When pulp surges converge with shekel depreciation, converters raise minimum order sizes to dilute risk, inadvertently squeezing small- and medium-sized brand owners on working-capital cycles.

Supply Uncertainty of Natural Gas for Paper Mills

Israel’s single domestic mill relies on continuous natural-gas flow for steam generation, and any pipeline maintenance or geopolitical disruption requires a rapid switch to diesel backup, which raises energy costs per tonne. Output curtailments ripple down to converters awaiting linerboard deliveries, lengthening lead times beyond contractual service-level agreements. Importers attempt to bridge gaps, but container congestion at Ashdod and Haifa constrains arrival schedules, leaving pockets of linerboard scarcity that push spot prices higher. To ease exposure, several converters maintain stock buffers equal to three weeks of demand, tying up capital that could be used to fund digital-press installations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Regulatory Tailwinds Elevate Recycled Linerboard Share

Recycled grades accounted for 51.78% of demand in 2025, a position underpinned by producer-responsibility quotas and TMIR enforcement that reward high post-consumer content. The Israel corrugated packaging market size for semi-chemical fluting is set to expand the fastest, reaching brand owners that need pallet-strength boxes without heavyweight kraft tops. Virgin Kraft retains relevance in humid produce lanes, yet its proportion slips as domestic collection networks scale and mills perfect strength-enhancement chemistries.

Hadera Paper expanded from roughly 160,000 tpa to 320,000 tpa capacity following Machine 8’s startup, enabling the mill to supply recycled linerboard at a USD 100 tons premium to base grades while still shielding converters from pulp volatility.[2]Gur Ben David, “The Current Paper Production Network,” Hadera Paper Group, SEC.GOV The closed-loop model, in which the Amnir unit harvests curbside fiber and feeds it back to Machine 8, raises national recovery rates and aligns with the ministry’s 2030 strategy.

By Flute Type: B Flute Dominance with E Flute Momentum

B flute delivered 41.57% of 2025 volume, reflecting its adaptability across produce trays, RSCs, and mid-strength die-cuts. E flute demand races ahead at 5.44% CAGR through 2031 as converters cater to shelf-ready and e-commerce parcels that value thinner profiles and reduced void space. The Israel corrugated packaging market share advantage of B flute erodes slightly as retailers benchmark lighter formats to optimize truck fill.

E flute’s acceleration pairs naturally with single-pass inkjet lines, since the reduced caliper shortens drying distance and cuts ink loading. F flute lingers in luxury cosmetics where tactile finesse outweighs cost premiums, and A/C flutes maintain niches in industrial cushioning. Converters calibrate corrugator gaps more frequently as order runs shrink, raising changeover counts from two to four per shift in plants serving quick-commerce hubs.

By Packaging Type: Regular Slotted Containers Anchor Volume, Custom Boxes Surge

Regular slotted containers comprised 43.38% of the Israel corrugated packaging market size in 2025, serving baseline logistics for food processors and beverage distributors. Custom die-cut boxes grow fastest at a 5.49% CAGR to 2031, as omnichannel retailers require SKU-specific dimensions that eliminate dunnage and reduce return damage. Folding cartons and POP displays round out secondary shelf-marketing tools in high-frequency grocery lanes.

Digital workflows shorten artwork approval loops, enabling converters to pivot from master die-cuts to micro-runs inside 24 hours. Grocery retailers co-design auto-lock bottoms and crash-lock trays to boost replenishment speed, while premium confectioners embed foil layers or water-based barrier coatings to protect organoleptic properties. Die-cut capacity utilization now exceeds 78% in leading plants, opening investment cycles for additional flatbed plotters.

By Wall Type: Single-Wall Preference, Triple-Wall Expansion

Single-wall designs covered 57.34% demand during 2025, balancing price and stacking safety for most ambient products. Triple-wall boxes will post a 5.31% CAGR as defense contractors and biologics shippers require thermal insulation and vibration dampening on airfreight legs. Double-wall maintains a foothold for export-grade produce that needs above-average burst strength without weight penalties. Double-wall serves export packaging for fresh produce and processed foods, meeting international shipping standards without incurring the weight penalties of triple-wall construction.

Defense programs procure validated ISTA 7D-compliant cartons embedding phase-change gel packs, pushing triple-wall symmetry beyond the conventional 5-5-5 flute count. Pharmaceutical distributors adopt similar builds for cell-gene therapies that cannot withstand excursions above 30 °C. Energy cost sensitivity remains lower in this niche because payload value dwarfs packaging expense. Single-face corrugated remains a niche segment, limited to protective wrapping and cushioning applications within larger shipments.

By Printing Technology: Flexo Scale Meets Inkjet Agility

Flexographic presses held 63.91% share in 2025 by exploiting long-run economies and plate amortization. Digital inkjet units grow at 5.36% CAGR, catalyzed by retail-ready demand for four-color process images and SKU-level coding. Litho-lamination remains relevant in cosmetics and duty-free spirits, while screen printing serves a defensive role for small-batch tactical inventory. The Israel corrugated packaging industry is increasingly pursuing hybrid lines that pre-print liners via inkjet before the slotter-folder-gluer stages, halving makeready times and reducing jacket waste.

Converters running two-shift flexo cycles repurpose older machines to aqueous-only inks, allocating complex work to inkjet bays. Plate recyclers experience lower volumes as short runs migrate away from photopolymer. Other printing technologies, including UV flexo and hybrid systems, remain in early adoption phases among larger converters seeking to bridge the cost-quality gap between traditional flexo and digital inkjet.

By End-User Industry: Produce Dominance, E-Commerce Lift

Fresh food and produce remained core, accounting for 27.39% of volume in 2025, driven by Israel’s export corridors to Europe and the Gulf. E-commerce fulfillment will advance at 4.85% CAGR, leveraging E flute parcels, void-fill wraps, and branded opening experiences. Processed foods and beverages continue steady uptake of RSCs, while electronics and defense components edge toward triple-wall for fragile loads.

Online grocery operators integrate algorithmic box-right-sizing software, steering converters toward modular footprints that iterate weekly with SKU catalog changes. Cosmetics brands import litho-laminated cartons, yet a local pivot toward digital cold-foil units is underway to localize lead times. Pharmaceutical lines invest in tamper-evident print features and humidity sensors embedded inside fluting webs for biologics.

Geography Analysis

The coastal economic triangle spanning Tel Aviv, Haifa, and Ashdod accounts for the majority of the Israel corrugated packaging market size because it co-locates food processors, export container ports, and last-mile dark stores. Converters near these hubs benefit from reduced drayage costs and the ability to dispatch pallets same day. Legislative pilots that mandate source separation roll out first in metropolitan councils, generating higher post-consumer fiber capture and creating a local feedstock pool for nearby mills.[3]Ministry of Environmental Protection, “Waste Facts and Figures,” GOV.IL

Northern agricultural districts, including the Galilee and Jezreel valleys, consume high volumes of moisture-barrier boxes for citrus and vegetable exports. Producers here favor Hadera-sourced recycled linerboard blended with kraft topsheets to satisfy EU phytosanitary entry rules. Dedicated reefer corridors connect packing houses to Haifa Port, ensuring sub-four-hour transit from harvest to vessel, a factor that drives tight procurement timetables and high OTIF penalties for converters.

Southern regions around Beersheba and the Negev Defense Technological Cluster represent emerging demand nodes for triple-wall cold-chain corrugates supporting UAV electronics and biologics. Lower population density elongates distribution chains, raising compression resistance requirements and bolstering single-weight ratios, yet the absolute volume remains smaller than the coastal belt. Energy-intensive paper conversion in this area hinges on solar co-generation schemes that partially offset natural-gas uncertainty.

Competitive Landscape

Israel’s corrugated sector exhibits moderate concentration, anchored by Hadera Paper’s integrated presence that spans waste-paper collection, recycled linerboard production, and box conversion. The company’s Machine 8 line, optimized for post-consumer inputs, reduces reliance on kraft imports and offers a recycled premium that resonates with TMIR compliance certificates. Downstream, Carmel Container Systems leverages the same-network supply to lock in service contracts with top FMCG accounts, cutting lead times below the market average of 7 days.

Mid-sized converters, many family-owned, differentiate through proximity, custom die-cut expertise, and bilingual design services aimed at export-oriented fresh-produce growers. These players must navigate pulp-price swings without the hedge of integrated mills, prompting alliances that pool linerboard procurement to improve bargaining leverage. The Israel corrugated packaging market repeatedly witnesses tactical investments in digital inkjet lines, with least-cost capital sourced from state-backed green-technology funds that recognize the benefits of recycled content.

Tadbik exemplifies a diversification model, blending labels, shrink sleeves, and corrugated sleeves within a single portfolio to cross-sell into food, personal care, and RFID-enabled packaging.[4]Tadbik, “About Tadbik,” TADBIK.COM Start-ups housed in Tel Aviv accelerators pilot molded-fiber hybrid liners that pair plant-based cushioning with thin corrugated outers, targeting carbon-neutral online brands willing to pay 20% premiums. Logistics snarls at Ashdod and Haifa motivate converters to pre-book slots two months ahead, encouraging local sourcing and elevating Hadera’s strategic importance as a domestic board provider.

Israel Corrugated Packaging Industry Leaders

Klinger Packaging Ltd.

Ducart Packaging Industries Ltd.

al-ahlia boxes industry co

Best Carton Ltd

Yamaton Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Israel’s Ministry of Environmental Protection outlined new waste-market regulations that will reshape producer-responsibility costs and open collection contracts to competitive tenders.

- December 2025: The ministry inaugurated an advanced waste-recycling facility with a USD 1.52 million investment, boosting household paper and cardboard sorting capacity.

- December 2025: ILS 154 million (USD 40 million) was earmarked for northern community waste-management infrastructure, including fiber-sorting lines linked to corrugated feedstock streams.

- September 2025: USDA’s Exporter Guide Annual recorded USD 21 billion domestic food retail sales and highlighted rising demand for premium, single-portion products that lean on high-graphic corrugated.

Israel Corrugated Packaging Market Report Scope

The Israel corrugated packaging market is defined as the industrial sector involved in the production and conversion of fiber-based packaging materials, consisting of a fluted corrugated medium bonded between flat linerboards. This market encompasses various structural grades, including single-wall, double-wall, and triple-wall boards, designed to provide high-performance protective solutions for domestic distribution and international transit.

The Israel Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material Type | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current value of the Israel corrugated packaging market?

The Israel corrugated packaging market size stands at USD 0.52 billion in 2026 and is projected to reach USD 0.64 billion by 2031.

Which flute type is growing the fastest?

E flute shows the highest momentum, advancing at a 5.44% CAGR through 2031 as retailers favor slim, high-graphic shelf-ready formats.

How is government policy influencing material choices?

Producer-responsibility mandates and a 51% recycling target for 2030 are driving converters to increase recycled linerboard content and invest in upgraded sorting capacity.

Why are digital inkjet presses gaining share?

Brand owners want short-run, high-graphic packaging that can switch artwork frequently, and digital inkjet eliminates plate costs while meeting tight lead times.

Which end-user segment is expanding the quickest?

E-commerce fulfillment centers are the fastest-growing users, registering a 4.85% CAGR as online and quick-commerce models proliferate across urban Israel.

What risks do converters face from energy supply?

Intermittent natural-gas availability can force mills to burn costlier diesel, squeezing margins and potentially delaying linerboard deliveries to box plants.

Page last updated on: