Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

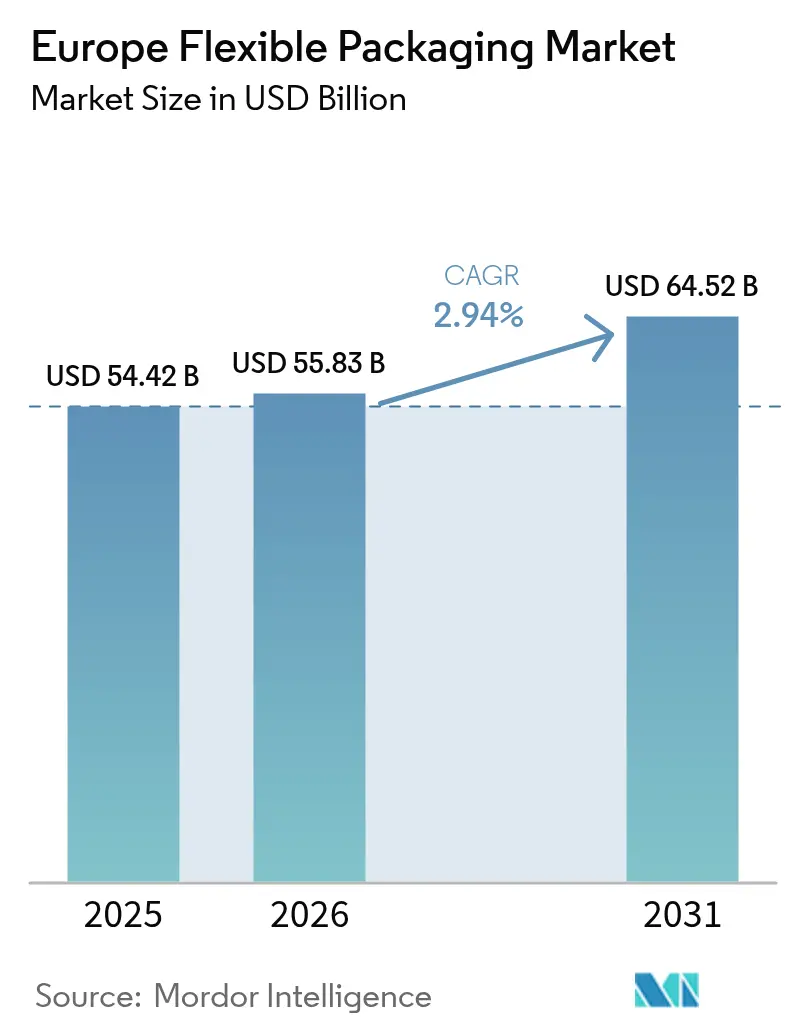

| Base Year Market Size (2025) | USD 54.42 Billion |

| Market Size (2026) | USD 55.83 Billion |

| Market Size (2031) | USD 64.52 Billion |

| Growth Rate (2026 - 2031) | 2.94% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Flexible Packaging Market Analysis by Mordor Intelligence

The Europe flexible packaging market size size was valued at USD 54.42 billion in 2025 and is estimated to grow from USD 55.83 billion in 2026 to reach USD 64.52 billion by 2031, at a CAGR of 2.94% during the forecast period (2026-2031). Rising circular-economy regulations, e-commerce parcel growth, and a consumer tilt toward lighter, portion-controlled packs are reshaping the competitive playbook. Brand owners are accelerating a shift from complex multi-layer laminates to recyclable mono-materials, even though barrier performance can suffer, while converters add digital-printing lines to serve the surge in short-run regional SKUs. Germany’s early compliance with stringent recyclability targets is setting technical benchmarks that the rest of the region is expected to follow, creating first-mover advantages for suppliers of HD-printing, solvent-free lamination, and chemical-recycling feedstocks. Acquisitive multinationals are widening the capability gap by funding line conversions that many mid-tier rivals cannot finance, opening a consolidation window in high-margin niches such as recyclable high-barrier retort pouches.

Key Report Takeaways

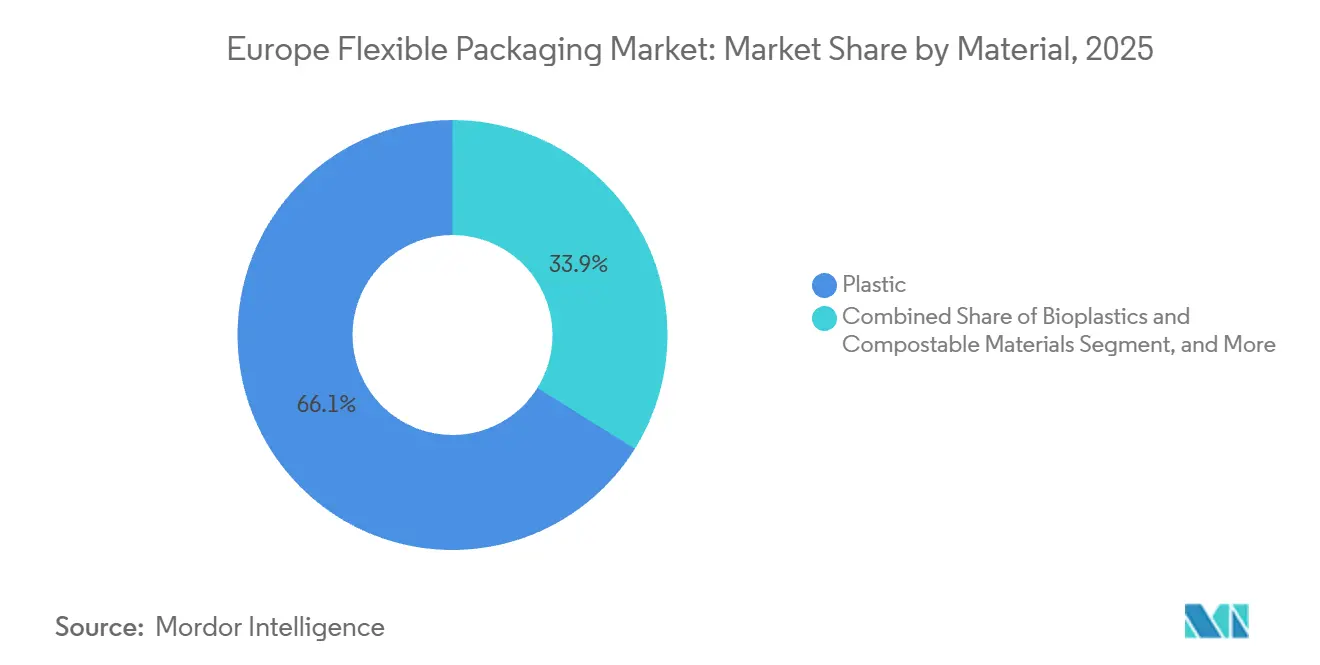

- By material, plastics dominated with 66.12% of market share in 2025, while bioplastics are forecast to expand at a 4.21% CAGR to 2031.

- By product format, bags and pouches led with 46.63% of market share in 2025; sachets and stick packs are projected to advance at a 3.45% CAGR through 2031.

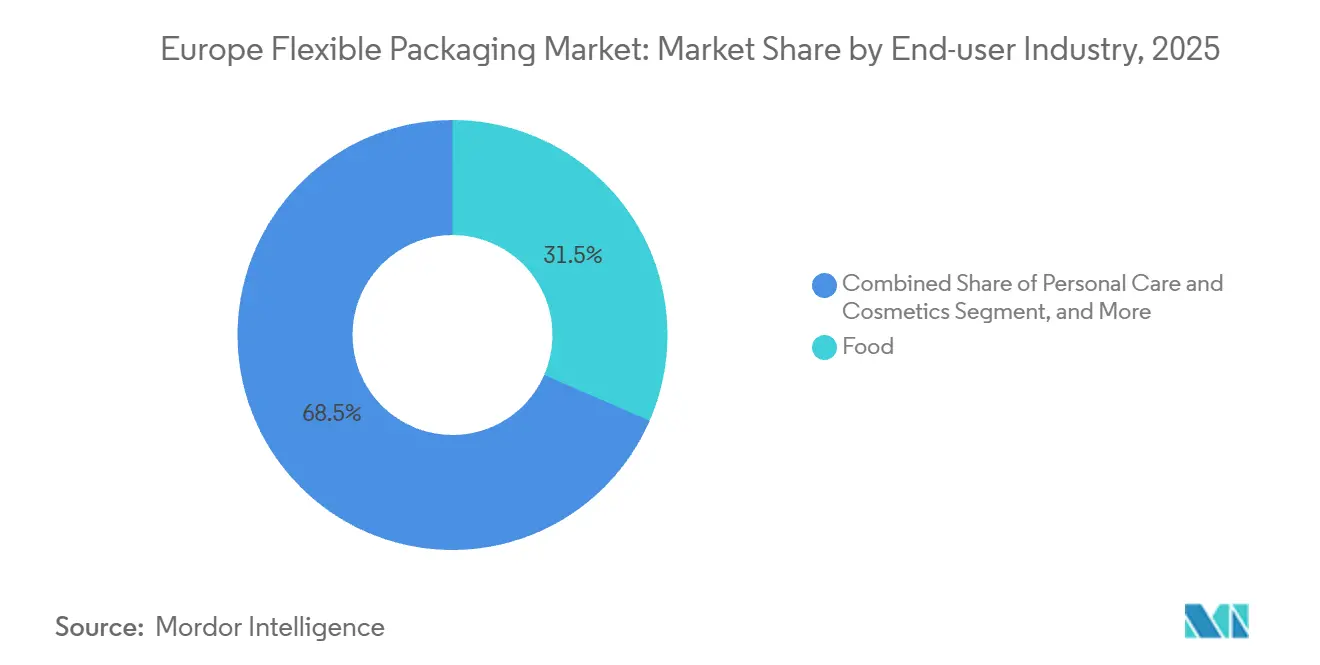

- By end-user, food captured 31.53% of the share in 2025, whereas personal care and cosmetics are expected to grow at a 3.59% CAGR to 2031.

- By printing technology, flexography retained 42.72% of the market share in 2025, and digital printing is on track for the fastest 3.88% CAGR to 2031.

- By geography, Germany held 21.12% of the Europe flexible packaging market share in 2025, while Spain is set to record the highest 4.13% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Demand for Recyclable Mono-Material Films Driven by EU Circular Economy Targets | +0.9% | EU-27, with early adoption in Germany, France, and Benelux | Medium term (2-4 years) |

| Accelerated Growth of E-Commerce Elevating Demand for Flexible Mailer and Protective Formats in Europe | +0.7% | Pan-European, strongest in UK, Germany, and Nordic markets | Short term (≤ 2 years) |

| Consumer Shift Toward Convenience and Portion-Control Products Boosting Flexible Pouch Adoption | +0.5% | Western Europe, urban centers in Spain, Italy, and France | Medium term (2-4 years) |

| Technological Advances in High-Barrier Co-Extrusion Enhancing Shelf-Life for Ready Meals | +0.3% | Germany, UK, France, with spillover to Central Europe | Long term (≥ 4 years) |

| Rising Penetration of Digital and Hybrid Printing Enabling Short Runs and Mass Personalization | +0.2% | Western Europe, premium segments in Italy, France, and UK | Medium term (2-4 years) |

| Rapid Expansion of the European Pet-Food Industry Using Retort and Stand-Up Pouches | +0.3% | Germany, UK, France, and Nordic markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Demand for Recyclable Mono-Material Films Driven by EU Circular-Economy Targets

Europe’s recyclability-by-design mandate is dismantling the long-running cost advantage of mixed-polymer laminates. Converters are engineering single-polyethylene or single-polypropylene films that integrate oxygen and moisture barriers through specialty tie layers and ultra-thin EVOH cores, thereby complying with the Packaging and Packaging Waste Regulation, which requires 30% post-consumer resin in flexible packs by 2030. Mechanical-recycling constraints force many converters to blend downgraded PCR with virgin resin, raising material cost and driving innovation toward solvent-based delamination and chemical-recycling alliances. Extended Producer Responsibility fees now vary with recyclability scores, adding up to EUR 0.80 (USD 0.90) per kilogram for non-recyclable films in France’s CITEO system, a direct hit to brand-owner budgets. The European Chemicals Agency’s looming PFAS ban, effective 2026, further tightens material choices by eliminating a class of grease-resistant coatings.[1]European Chemicals Agency, “Restriction Proposal for Per- and Polyfluoroalkyl Substances in Food Contact Materials,” ECHA.EUROPA.EU The result is a synchronized rush toward mono-material platforms despite unresolved trade-offs in barrier performance.

Accelerated Growth of E-Commerce Elevating Demand for Flexible Mailers and Protective Formats in Europe

Parcel volumes topped 87 billion in 2024, and flexible mailers are displacing corrugated boxes wherever dimensional-weight rules punish oversized packaging. The European Parliament capped empty space at 40% for e-commerce parcels by 2026, effectively steering retailers toward thinner, form-fitting mailers. Automated fulfillment lines that dispense custom-sized pouches reduce warehouse storage by up to 20% and lower carrier surcharges linked to volumetric weight. Yet, the same regulation compels reusability or recyclability, forcing a design compromise: durability for reverse logistics versus compatibility with polyethylene film streams. Germany’s 2025 VerpackG amendment requires online retailers to fund take-back schemes, adding EUR 0.05-0.10 (USD 0.06-0.11) per mailer, a cost that nudges some merchants toward coated-paper solutions despite higher moisture-barrier challenges.

Consumer Shift Toward Convenience and Portion-Control Products Boosting Flexible-Pouch Adoption

Europe’s shrinking household sizes and urban lifestyles are fueling single-serve sales. Ready meal, snack, and even pet-food brands prefer pouches that provide shelf-life parity with rigid packs at 30-40% lower weight, translating into meaningful freight savings. Portion control resonates with inflation-sensitive shoppers who seek to minimize food waste, although aggregate pack-to-product ratios can rise. Stand-up retort pouches now replace cans in premium pet-food ranges, slicing transport emissions by 60% while adding merchandising appeal through high-resolution flexographic graphics. Policymakers are scrutinizing the sustainability upside, and draft EU eco-design rules under consultation in 2025 could impose minimum fill-weight thresholds. Brands therefore juggle the marketing value of convenience against the risk of future under-fill penalties.

Technological Advances in High-Barrier Co-Extrusion Enhancing Shelf-Life for Ready Meals

Next-generation co-extrusion lines achieve oxygen-transmission rates below 1 cm³/m²/day, tripling shelf-life for ready meals and deli meats without refrigeration. Typical structures combine an EVOH micro-layer with polyethylene outer skins, yet EVOH levels above 5% jeopardize recyclability in mono-PE streams. Dutch and German pilot plants now demonstrate solvent-based delamination that retrieves clean EVOH and polyethylene fractions, though long-run economics hinge on achieving about 10,000 tonnes per year of feedstock. Brand owners also test plasma-deposited silica and nano-clay barrier coatings that nearly match EVOH but at a 20-30% premium. Early adopters in Germany and the UK see the cost outweighed by extended shelf-life, reduced cold-chain dependence, and lower food-waste liabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU Plastics and Packaging-Waste Regulations Increasing Compliance Costs | -0.6% | EU-27, with highest impact in France, Germany, and Netherlands | Short term (≤ 2 years) |

| Limited Recycling Infrastructure for Multi-Layer Films Hampering Circularity Goals | -0.4% | Southern and Eastern Europe, infrastructure gaps in Spain, Italy, Poland | Medium term (2-4 years) |

| Volatile Polyolefin and Aluminum-Foil Prices Post-Energy Crisis Impacting Margins | -0.3% | Pan-European, with acute pressure in energy-intensive Germany and Italy | Short term (≤ 2 years) |

| Competitive Pressure from Rigid Recyclable Alternatives Among Sustainability-Minded Brands | -0.2% | Western Europe, premium segments in UK, Germany, and Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent EU Plastics and Packaging-Waste Regulations Increasing Compliance Costs

More than 20 national EPR schemes now impose differentiated fees based on pack design, and converters must fund recyclability lab tests, migration studies, and cross-border registrations that can total USD 100,000 per plant each year. France’s AGEC law adds blockchain-level traceability for recycled content, raising material premiums by USD 0.02-0.05 per kilogram.[2]France Ministry of Ecological Transition, “Anti-Waste Law for a Circular Economy,” ECOLOGIE.GOUV.FR Small converters are diverting capital from growth projects just to keep SKUs compliant. In parallel, Germany’s updated VerpackG enforces a 65% recycling target for plastics by 2025, a level that flexible films cannot meet today, thereby exposing converters to penalty fees or market exits. Some firms relocate production to lower-fee jurisdictions, but the European Commission plans a harmonized fee model by 2027 that will close such loopholes.

Limited Recycling Infrastructure for Multi-Layer Films Hampering Circularity Goals

Europe generated over 4.5 million tonnes of flexible-packaging waste in 2024, yet only about 1.2 million tonnes entered mechanical-recycling plants. Optical sorters still struggle to distinguish polyethylene from polypropylene films, producing PCR with unstable melt-flow indices that rarely meet food-contact thresholds. Chemical-recycling capacity remains below 100,000 tonnes per year, and regulatory approval of pyrolysis oils is slowed by concerns over polycyclic aromatic hydrocarbons. Collection economics remain unfavorable in rural regions where film density is too low for curbside pickup. Until infrastructure scales, converters must either down-cycle waste into low-value applications or pay incineration fees, both of which undermine the EU’s 2030 recyclability target.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Mono-Material Shift Challenges Barrier Performance

Plastics represented 66.12% of market share in 2025, confirming that virgin and recycled polyolefins still anchor the Europe flexible packaging market. Yet, bioplastics are poised for the fastest 4.21% CAGR as brand owners hedge against future fossil-based bans. Polylactic acid films find a niche in bakery liners where short shelf-life tolerates limited barrier properties, while cast polypropylene remains the default sealant layer even as converters trial pure-PP laminates to meet recyclability rules. Paper-based laminates are rebounding in dry goods, though the Europe flexible packaging market size for coated paper remains modest because plastic liners exceeding 2% by weight disqualify most packs from paper-mill streams. Aluminum foil retains critical roles in pharmaceutical blister and coffee applications where near-zero oxygen transmission is non-negotiable.

The mono-material pivot accelerates demand for specialty tie-layer resins that bond EVOH micro-layers to polyethylene without compromising seal strength. Polymer suppliers are marketing compatibilizers that claim to preserve optical clarity and drop-test performance, yet converters report a learning curve that increases scrap rates during early production. Brands accept these inefficiencies to secure “designed for recycling” logos that ease EPR fees and bolster corporate-sustainability disclosures. Despite high interest in compostables, industrial-scale composting infrastructure remains rare outside Italy and Austria, meaning most PLA or starch blends still end in landfill or incineration. Until consumer-collection systems mature, polyolefins are expected to dominate the Europe flexible packaging market share for at least the next five years.

By Product Type: E-Commerce Reshapes the Format Hierarchy

Bags and pouches held 46.63% of the market share in 2025, benefiting from stand-up formats that replace rigid tubs in baby food, ready meals, and household cleaners. Europe flexible packaging market size linked to sachets and stick packs is forecast to rise at a 3.45% CAGR through 2031 thanks to pharmaceutical unit-dose demand and single-serve coffee innovations. Films and wraps remain a bulk-volume workhorse in palletizing and silage, but margin compression is acute as resin-price swings transfer directly to commoditized contracts. Correspondingly, converters are steering investments toward higher-value mailers with multi-layer cushioning and printable zones for reverse-logistics labels.

Mailers illustrate the trade-off between operational efficiency and regulatory compliance. A 60-gram-per-square-meter co-extruded mailer can cut shipping costs by 40% compared with a small corrugated box, yet PPWR’s draft rules favor reusability, forcing retailers to trial thicker, returnable pouches embossed with QR codes for tracking. Pilot programs in the Nordics show 30% consumer return rates, insufficient to justify higher unit costs without deposit incentives. Paper mailers laminated with water-based barriers gain favor in humid climates where uncoated kraft fails, even though mixed-material construction complicates recycling. Converters that can deliver a certified recyclable PE mailer compatible with automated pack-in-bag systems are likely to seize profitable share over the forecast period.

By End-User Industry: Premiumization Drives Personal-Care Surge

Food applications contributed 31.53% of market share in 2025, but pricing pressure from private-label retailers limits margin upside, pushing converters to lightweight structures and adopt solvent-free lamination to save energy. Personal-care and cosmetics is forecast to expand at a 3.59% CAGR, propelled by luxury brands swapping glass jars for high-barrier pouches that weigh 70% less and tout lower carbon footprints. The Europe flexible packaging market size serving beverage pouches also edges higher as spouted pouches displace small PET bottles in on-the-go juices.

Healthcare packaging maintains stringent requirements. Aluminum-foil blister packs still dominate moisture-sensitive tablets, and regulatory dossiers add 12-18 months to any material substitution, entrenching incumbent suppliers. Pet food illustrates how category dynamics intersect; premium wet formulas now rely on retort pouches that cut transport costs but remain non-recyclable under current PPWR definitions, putting pressure on converters to commercialize aluminum-free retort structures. Agriculture’s low-margin pallet wrap and greenhouse film segment continues to migrate toward lower-cost Eastern European plants, where labor and energy savings offset higher logistics outlays to Western consumer markets.

By Printing Technology: Digital Gains Despite Ink-Compliance Hurdles

Flexography commanded 42.72% of market share in 2025 owing to its versatility and drop-in water-based ink upgrades that meet VOC limits without plant overhauls. Digital printing, however, is projected to chart a 3.88% CAGR as brands demand 500-unit trial runs and seasonal graphics. The Europe flexible packaging market share for rotogravure remains sticky in ultra-long confectionery and tobacco runs, but cylinder lead times and upfront costs deter new SKUs.

Hybrid lines that print a common brand background flexographically before digitally adding language variants offer an attractive compromise. Ink suppliers are racing to certify food-contact digital sets under EFSA rules that require full toxicology, but the color gamut remains narrower than analog inks. Converters that crack the compliance puzzle stand to attract premium beverage and baby-food brands craving photorealistic imagery combined with serialized QR codes for traceability. As these investments spread, digital’s share is expected to accelerate after 2028 when early adopters validate full-speed productivity on 1 m wide inkjet lines.

Geography Analysis

Germany delivered 21.12% of market share in 2025, leveraging its dense manufacturing base and high packaged-goods consumption. Elevated energy costs after the 2024 gas-price shock squeezed film-extrusion margins, yet the country’s stringent VerpackG law pushed converters to upgrade lines early, turning compliance into a future export advantage.[3]Germany Federal Ministry for the Environment, “Packaging Act (VerpackG) Amendment,” BMUV.DE Spain represents the fastest 4.13% CAGR through 2031, underpinned by Mediterranean food exporters that prize lightweight, oxygen-barrier pouches for olive oil and canned seafood bound for North America and Asia. Madrid and Catalonia also host expanding e-commerce hubs, boosting demand for PE mailers and air-cushion films.

The United Kingdom’s dual-regulation environment complicates operations for companies selling in both the UK and the EU blocs. Separate inventory streams for REACH-compliant and UKCA-marked films raise working-capital needs, though some converters offset the burden by centralizing digital printing in UK plants that serve pan-European limited editions. France and Italy, long centers of luxury and pharmaceutical packaging, continue to command high-barrier co-extrusion and deep-tone gravure capacity. France’s AGEC law is spurring fast adoption of chemical-recycling pilots, while Italy leverages its robust industrial-composting network to attract PLA and starch-blend trials.

Nordic countries boast collection rates above 80% for flexible films, validating deposit-return schemes that other EU states may replicate. Eastern Europe remains a cost-competitive production basin; Poland and Czechia lure investment with lower wages and proximity to German OEMs, but shortages of skilled process engineers are emerging. Benelux nations act as a testing ground for closed-loop pilots because of dense populations and advanced sortation infrastructure, making them ideal markets for launch of mono-PE snack bags with 30% PCR content. These regional nuances create a patchwork of opportunities and regulatory hurdles that shape converter investment plans across the continent.

Regulatory Landscape

The regulatory framework for flexible packaging in Europe is tightening under the Packaging and Packaging Waste Regulation, Regulation (EU) 2025/40 (PPWR). PPWR entered into force on 11 February 2025 and applies from 12 August 2026, replacing Directive 94/62/EC. It introduces directly applicable, EU-wide requirements for packaging sustainability, labeling, and lifecycle obligations, which raises the compliance bar for flexible formats using multi-layer or composite structures.

EU food contact materials rules are also evolving through amendments to Regulation (EU) No 10/2011 and related implementing measures. Commission Regulation (EU) 2026/245 (published 2 February 2026) updates Annex I substance authorizations for plastic food contact materials, while Commission Regulation (EU) 2026/250 (published 2 February 2026) sets transitional provisions related to Bisphenol A restrictions, with timelines extending to 20 July 2026 and 20 January 2028 for specific applications. Commission Regulation (EU) 2025/351 further updates manufacturing and quality control requirements, with transition allowances extending to 16 September 2026 for existing stock. In 2026, the European Commission also issued a PPWR guidance document (OJ C series, C/2026/3084) to support consistent interpretation as companies prepare for the August 2026 applicability date.

Value Chain Analysis

The Europe flexible packaging value chain spans resin, paper, and aluminum suppliers, additive, ink, coating, and adhesive formulators, and film extruders and substrate producers. Converters, including printing, laminating, pouching, and bag-making specialists, sit between brand owners and retailers, and upstream and downstream ties extend to collection, sorting, recyclers, and producer responsibility organizations that manage EPR obligations.

Industry coordination platforms such as CEFLEX (a consortium with over 180 member companies and organizations) and Flexible Packaging Europe (representing over 80 companies operating at more than 350 sites and accounting for nearly 90% of European flexible packaging sales) help align design-for-recycling guidance, test methods, and implementation positions across the chain. With PPWR applying from 12 August 2026, the value chain is being reorganized around recyclability-by-design, verified food-contact compliance, and traceability for recycled content. That increases dependencies on specialty materials such as tie layers, barrier coatings, and compliant inks, on qualified testing and certification capacity, and on access to recycling outputs suitable for flexible packaging applications where multilayer structures face limited mechanical recycling routes. To reduce friction from uneven national implementation and improve readiness, value-chain groups have expanded implementation support activities, including a legislative dashboard developed by Stichting CEFLEX in 2026 to help stakeholders navigate PPWR and related secondary measures.

Competitive Landscape

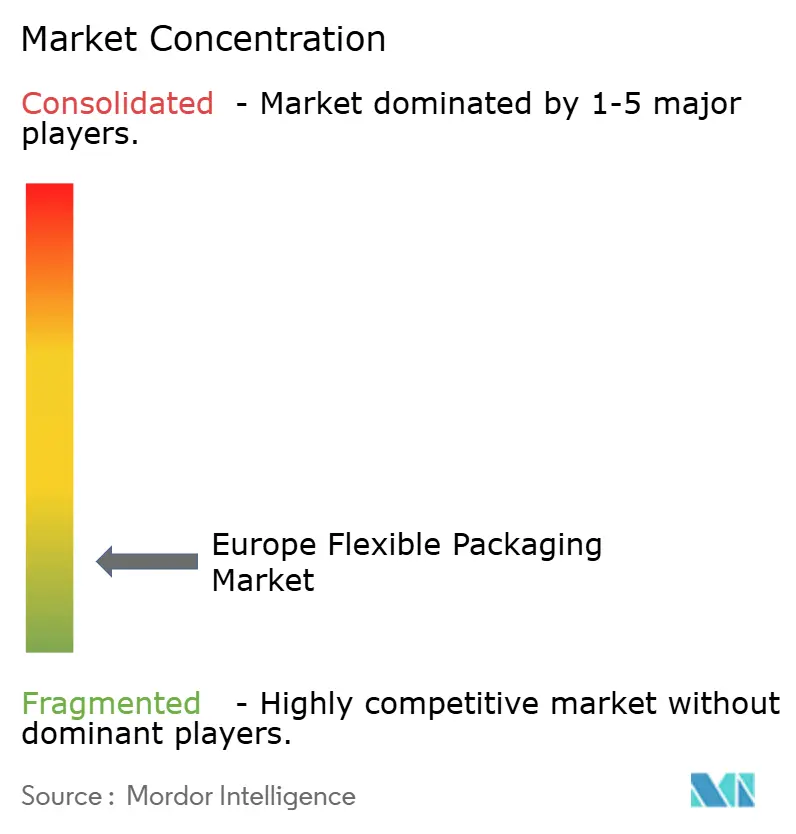

The Europe flexible packaging market features fragmentation. Scale leaders such as Amcor, Mondi, and Huhtamaki absorb PPWR compliance costs by spreading capital upgrades across multi-country footprints and leveraging global resin-purchasing power. Private-equity funds remain active consolidators, targeting sub-USD 100 million converters that specialize in pet-food retort pouches, pharma clean-room laminates, or digital-print on-demand services.

Product innovation focuses on recyclable high-barrier films and certified carbon-neutral supply chains. Mondi’s grease-resistant paper line and Huhtamaki’s mono-PP retort pouch show how multinationals use proprietary tie-layer chemistries and pilot-scale recycling loops to lock in early adopter customers. Smaller specialists defend share by offering rapid artwork changeovers, multilingual regulatory support, and low-volume order flexibility. Resin volatility since 2024 has squeezed margins, yet converters with surcharge pass-through clauses or backward-integrated recycling capacity weather volatility better than price-takers.

Strategic partnerships with chemical-recycling firms, such as Sealed Air’s 20,000-tonne off-take from Eastman’s molecular-recycling plant, create closed-loop narratives that resonate with consumer-packaged-goods majors. Digital-print pure-plays like ePac expand regionally to supply local craft-food entrepreneurs seeking 48-hour turnaround. As pan-European EPR fee harmonization draws near, the ability to guarantee certified recyclability is evolving from a marketing edge into a ticket-to-play for every participant in the Europe flexible packaging market.

Europe Flexible Packaging Industry Leaders

Amcor PLC

Mondi Group

Huhtamaki Oyj

Constantia Flexibles GmbH

Wipak Oy

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

PPWR, Regulation (EU) 2025/40, entering application on 12 August 2026 is sharpening whitespace around recycle-ready high-barrier structures that preserve functionality while meeting design-for-recycling requirements. Converter investments visible in 2026 point to active commercialization pathways: Amcor added a new production line at its Lugo di Vicenza, Italy site for high-barrier recycle-ready films used across food, beverage, pet food, and healthcare, and also announced a multi-million-euro printing-line investment at Hardenberg, Netherlands to lift industrial film capacity by up to 6,000 tonnes annually. Taken together, these moves show where buyers are allocating spend now, particularly for barrier performance without aluminum foil laminates, faster SKU changeovers, and compliant materials for regulated end uses.

Recycled-content sourcing and compatible processing remain a second opportunity area, since regulatory targets and EPR differentiation are shifting procurement toward verified, fit-for-purpose PCR for flexible applications. At the same time, capability-building through acquisitions and equipment upgrades continues to widen the gap between scale players and mid-tier converters, especially in niche substrates such as cast polypropylene (CPP), and in converting and printing assets that support high-spec formats. Coveris acquisition of GEFO in Germany in June 2026 to expand CPP extrusion capability, along with incremental manufacturing investments in Poland for printing and bag-making equipment, illustrates continued restructuring toward more integrated film supply and higher-value applications such as medical, retort, and lidding, where performance and compliance constraints limit substitution.

Recent Industry Developments

- June 2026: Coveris acquired GEFO Folienbetrieb GmbH in Germany to expand its cast polypropylene (CPP) film production capabilities for applications including medical, retort, and lidding. The deal strengthens Coveris control over CPP extrusion and supports development of higher-performance structures aligned with recyclability and barrier requirements across regulated end uses.

- April 2026: Amcor announced a multi-million-euro investment in a new flexographic printing line at its Hardenberg, Netherlands facility to increase printing capacity by up to 6,000 tonnes per year for industrial and agricultural films. The added capacity is aimed at faster turnaround and higher-volume output for film-based applications as customers adjust specifications and labeling to meet tightening EU packaging rules.

- June 2024: Coveris acquired HADEPOL FLEXO to expand its flexible paper and film packaging footprint in Central and Eastern Europe. The acquisition broadened manufacturing capabilities and regional reach, supporting supply resilience and a wider product offering for customers shifting formats and materials in response to sustainability and compliance pressures.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Europe flexible packaging market covers the value of flexible packs sold for use across end users in Europe, including common film, pouch, bag, and wrap style formats made from plastic, paper, foil, or mixed structures.

Scope exclusions: We exclude rigid packaging formats and packaging machinery, and we also exclude logistics services that sit outside the packaging sale.

Segmentation Overview

- By Material

- Plastics

- Polyethylene (PE)

- Biaxially Oriented Polypropylene (BOPP)

- Cast Polypropylene (CPP)

- Other Plastics

- Paper

- Metal Foil

- Bioplastics and Compostable Materials

- Plastics

- By Product Type

- Bags and Pouches

- Films and Wraps

- Sachets and Stick Packs

- Other Product Types

- BY End-user Industry

- Food

- Baked Goods

- Snacks

- Meat, Poultry and Seafood

- Confectionery

- Pet Food

- Other Food Products

- Beverage

- Healthcare and Pharmaceutical

- Personal Care and Cosmetics

- Agriculture

- Other End-Use Industries

- Food

- By Printing Technology

- Flexography

- Rotogravure

- Digital Printing

- Other Printing Technologies

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, build the initial demand indicators, and pressure test the numbers at a country level. We relied on public, non paywalled sources such as Eurostat production and trade series, UN Comtrade customs data, European Commission policy updates on packaging and waste, and OECD macro indicators that influence packaged goods demand.

To keep assumptions realistic, we also reviewed converter and material supplier annual reports, investor presentations, sustainability disclosures, and reputable packaging press to track capacity additions, material shifts (for example mono material moves), and end user packaging changes. Where needed, paid subscriptions for company financials, patent databases, and shipment level trade views were used to clarify revenue exposure, innovation activity, and cross border flows. These examples are indicative only, and many other sources were also referred to for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work was used to close gaps that desk sources cannot address cleanly, especially on price realization, product mix shifts, and how quickly sustainability targets translate into firm purchasing decisions. We interviewed packaging converters, raw material participants, brand owners, and channel partners across major European markets, then ran follow up checks to align assumptions on volumes, margins, and substitution between materials.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 18% | |

| Mid tier: 55% | Functional/Unit leaders: 26% | |

| Smaller Players: 20% | Managers: 56% |

Market-Sizing & Forecasting

Sizing was built using a top down and bottom up approach, where the starting point was reconstructed from Europe level packaging demand signals and then distributed by country using production, trade, and consumption proxies. Once that demand pool was in place, selective bottom up checks were added, such as sampled converter revenue exposure, packaging material consumption patterns, and price per unit ranges, which were then used to adjust totals when large gaps showed up.

Key inputs that influenced the model included flexible packaging penetration in major end uses (food, beverages, home care, and health), shifts toward recyclable structures, lightweighting trends, resin and foil price movement, and changes in retail and e commerce packing formats. Because market drivers move together, scenario analysis was used for forecasting, with base, conservative, and upside paths tied to variables like packaged food output, policy timing, and material price pass through discussed during interviews. When bottom up information was not available for smaller countries, we used ratio based allocation anchored to trade and packaged goods indicators, and then rechecked the implied per capita use for outliers.

Data Validation & Update Cycle

Validation was done through multiple steps so the final number stays consistent with real world signals. Model outputs were compared against independent indicators like packaging production indexes, import export directionality, and country level demand splits that surfaced in interviews, and then large variances were reviewed again before sign off.

If an unusual move is seen, such as a sudden material price swing or a regulation change that affects a major end user group, we re contact sources to confirm whether the shift is structural or short term. Reports are refreshed annually, and interim updates are added when material events occur, followed by a final pre delivery check so clients receive an updated view at the time of release.

Mordor Intelligence's Europe Flexible Packaging Market Market Size Compared With Other Published Estimates

Published market sizes for Europe flexible packaging do not always match because each study draws the boundary differently and also picks a different base year and price logic. In practice, differences show up when one estimate treats flexible packaging as only plastic films, or when value is built from shipment revenue versus consumption value inside Europe.

By tracking packaged goods output, net trade signals, and converter price realization, Mordor Intelligence keeps the Europe total tied to a defined consumption pool, and it is then rechecked with country level plausibility tests before finalization.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 54.42 B (2025) | |

| Global Consultancy A | USD 55.87 B (2023) | Uses a 2023 revenue base and a different time cut for currency and pricing, which can lift or lower value when resin pass through timing changes across countries. |

| Regional Consultancy B | USD 36.41 B (2024) | Appears to apply a narrower included scope and may exclude some mixed material flexible structures or parts of non food demand, which compresses the total versus a broader flexible pack definition. |

The spread mainly comes from scope boundaries and year of measurement, and then from how price changes are treated across materials and countries. When the market is anchored to clear demand signals and cross checked with country patterns, the result stays easier to reproduce and explain for planning decisions.

Key Questions Answered in the Report

What is the projected compound annual growth rate for Europe’s flexible-packaging sector between 2026 and 2031?

The market is forecast to expand at a 2.94% CAGR during the 2026-2031 period.

Which material group is expected to record the quickest expansion?

Bioplastics and other compostable materials are set to grow the fastest, at a 4.21% CAGR through 2031.

Why are mono-material polyethylene and polypropylene films rapidly replacing multi-layer laminates?

EU recyclability mandates effective by 2030 require packaging to enter existing recycling streams, so brand owners are shifting to single-polymer structures that meet those rules while avoiding costly EPR fees.

Which national market is anticipated to post the strongest growth through 2031?

Spain is projected to lead regional gains with a 4.13% CAGR, driven by Mediterranean food exports and expanded e-commerce logistics.

How is digital printing reshaping supply-chain strategy for converters?

Digital and hybrid presses eliminate plate costs, enabling profitable runs as low as 500 units and allowing brands to launch multi-language or limited-edition SKUs on short notice.

What makes recyclable high-barrier retort pouches a key white-space opportunity?

Current aluminum-foil structures face regulatory obsolescence, so converters that deliver mono-polymer pouches offering 121 °C sterilization performance can capture share from pet-food and ready-meal brands seeking compliant alternatives.

Page last updated on: