Russia Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.72 Billion |

| Market Size (2026) | USD 6.89 Billion |

| Market Size (2031) | USD 7.61 Billion |

| Growth Rate (2026 - 2031) | 2.01% CAGR |

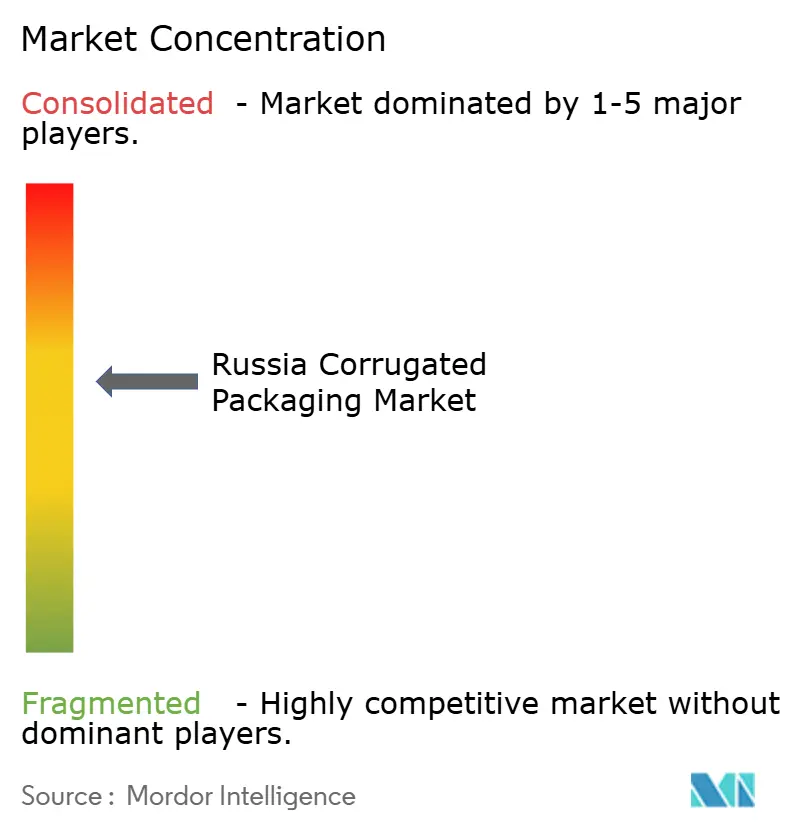

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Corrugated Packaging Market Analysis by Mordor Intelligence

The Russia corrugated market size is projected to be USD 6.72 billion in 2025, USD 6.89 billion in 2026, and reach USD 7.61 billion by 2031, growing at a CAGR of 2.01% from 2026 to 2031. E-commerce consolidation, regulatory pressure for recyclability, and expanding virgin-fiber capacity are reshaping cost structures even as macro headwinds, such as a potential 20-30% contraction in forestry output, threaten raw-material stability. Russia’s two dominant online marketplaces funnel more than 65% of total parcel flow through a handful of fulfillment hubs, concentrating demand for standardized shipping boxes yet fragmenting average lot sizes. At the same time, recycled linerboard maintains cost leadership but faces a domestic OCC ceiling that intensifies price swings whenever export bans or currency shocks hit import channels. Producers are investing in digital inkjet presses, robotics, and wastewater upgrades to capture premium food, cosmetics, and pharma contracts while meeting Best Available Techniques rules for emissions.

Key Report Takeaways

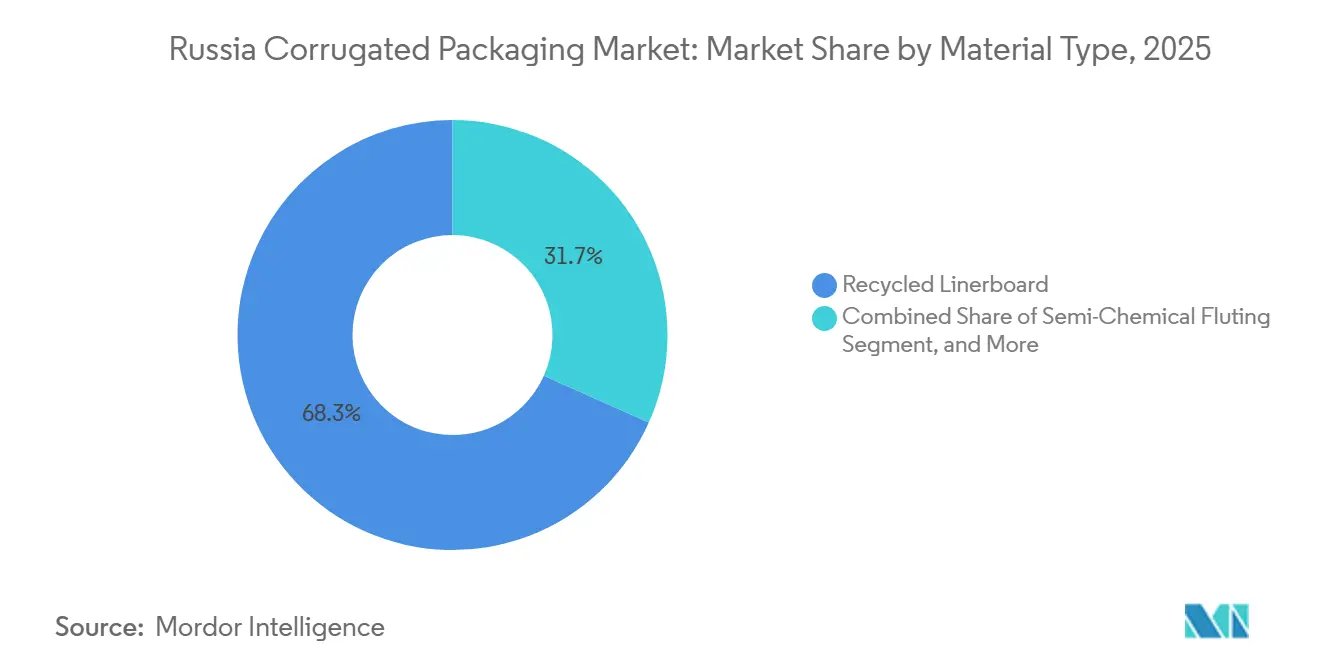

- By material type, the recycled linerboard segment captured 68.32% of the Russia corrugated packaging market share in 2025.

- By flute type, the Russia corrugated packaging market size for e-flute is projected to grow at a 3.79% CAGR through 2031.

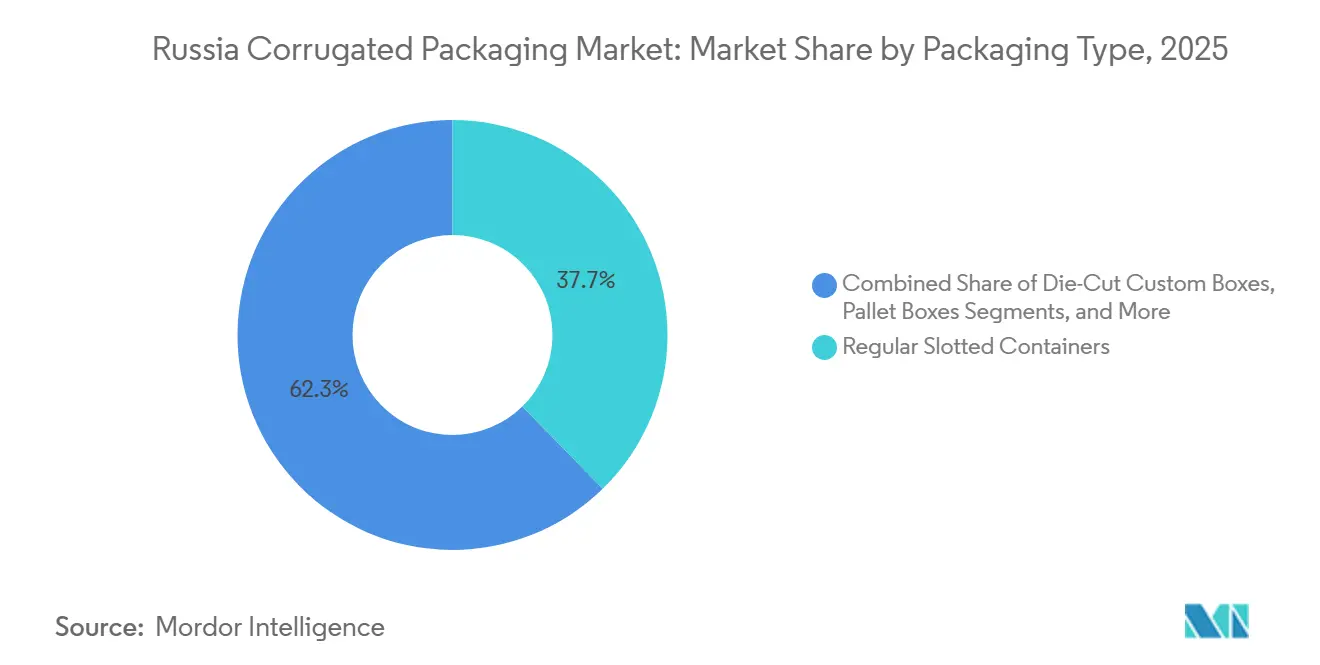

- By packaging type, the regular slotted containers segment captured 37.69% of the Russia corrugated packaging market share in 2025.

- By wall type, the Russia corrugated packaging market size for single-wall is projected to grow at a 3.86% CAGR through 2031.

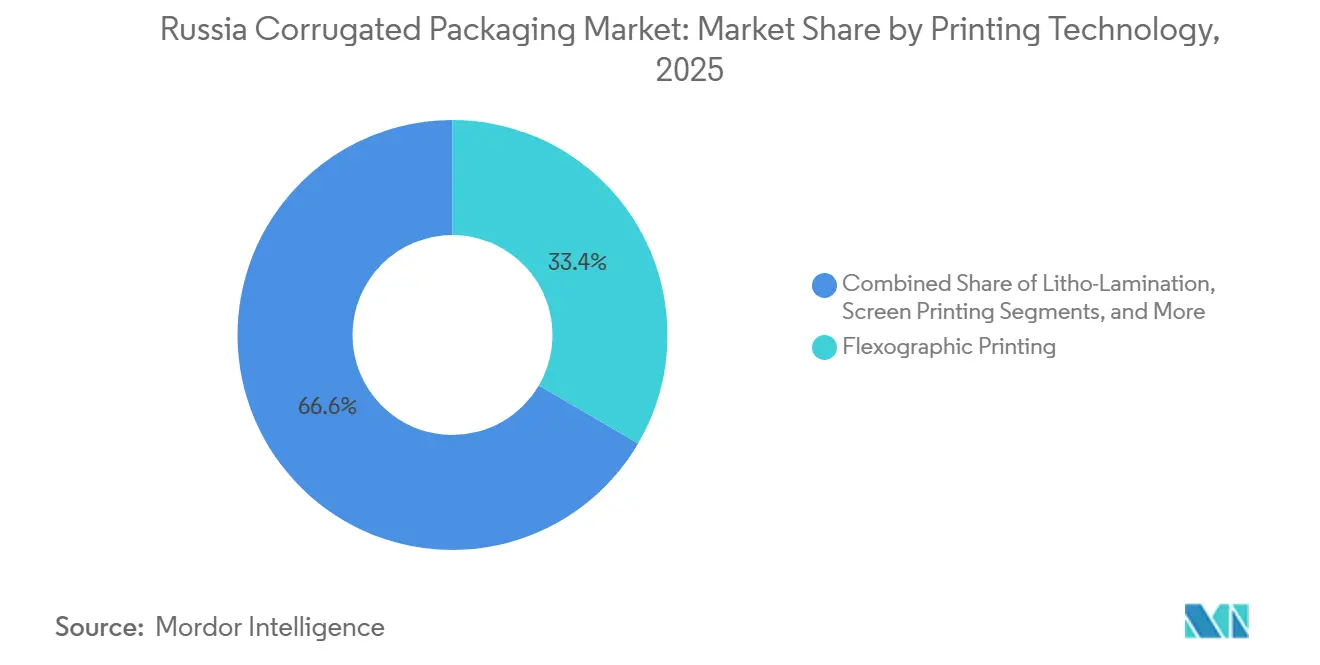

- By printing technology, the flexographic printing segment captured 33.41% of the Russia corrugated packaging market share in 2025.

- By end-user industry, the Russia corrugated packaging market size for e-commerce fulfillment centers is projected to grow at a 3.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Russia Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-Commerce Logistics Acceleration | +0.8% | Nationwide hubs in Moscow, St. Petersburg, and regional centers | Short term (≤ 2 years) |

| Growth in Processed Food and Beverage Exports | +0.5% | Southern Russia export corridors to China, Turkey, Central Asia | Medium term (2-4 years) |

| Regulatory Shift Toward Recyclable Packaging | +0.4% | Nationwide, stricter in major cities and ecologically sensitive provinces | Long term (≥ 4 years) |

| Expansion of Domestic Kraftliner Capacity | +0.3% | Irkutsk, Adygea, Tver, Tula | Medium term (2-4 years) |

| Digital Inkjet Customization Demand | +0.2% | Moscow, Yekaterinburg, Saratov, Novosibirsk | Short term (≤ 2 years) |

| Cold-Chain Export Growth | +0.1% | Southern and Far East export gateways | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce Logistics Acceleration

Russia’s online retail generated 8.3 billion orders and RUB 13.4 trillion (USD 142 billion) in 2025, with two marketplaces capturing nearly four-fifths of parcels. Centralized hubs are now pressuring packaging vendors to deliver lighter, right-sized cartons that cut dimensional-weight fees. Demand therefore tilts toward E flute and microflute boards that lower shipping costs while supporting vivid branding. Although parcel volume keeps growing, order values fell 5%, pressuring converters to supply cost-efficient designs without sacrificing protective integrity. Slowing marketplace growth is shifting focus from sheer volume to lean fulfillment, rewarding suppliers that embed data-driven sizing algorithms and easy-print customization.

Growth in Processed Food and Beverage Exports

Southern agribusiness corridors expanded processed output in double digits, pivoting export lanes from Europe toward China, Turkey, and Central Asia. Longer hauls and harsher climates increase the need for moisture-resistant double-wall cartons. Government backing for fish canning, dairy, and potato processing has spurred the development of regional converting plants with high-speed tray lines. Yet concentrated exposure to a handful of destinations raises geopolitical risk, pushing packagers to certify materials under multiple customs regimes and adopt modular box designs that accept variable pallet footprints.

Regulatory Shift Toward Recyclable Packaging

Amendments to Federal Law 89-FZ lift environmental levies by roughly 20% and set a target of 100% packaging recycling by 2027. Corrugated board qualifies as an approved recycling stream, granting converters levy relief if they meet utilization quotas. Firms therefore strip out plastic windows, switch to water-based inks, and publish recycling mass balances. Yet Russia’s waste-paper capture plateaued at 4 million tonnes, so compliance hinges on scaling separate-collection and sorting infrastructure, which regulators expect industry to co-finance via Extended Producer Responsibility fees.

Expansion of Domestic Kraftliner Capacity

The 600,000-tonne Ust-Ilimsk mill and other greenfield lines promise to ease virgin-fiber deficits and stabilize liner prices. New machines deploy energy-saving drives and closed-loop water loops that lower operating costs and emissions, letting integrated giants undercut spot imports. However, upstream logging has hit a four-year low, and financing costs remain elevated at a 21% policy rate, risking schedule slippage that could delay price relief for converters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycled Paper Price Volatility | -0.4% | Nationwide, acute in Central and Northwestern districts reliant on imported OCC | Short term (≤ 2 years) |

| Competition from Returnable Plastic Crates | -0.2% | Fresh-produce chains in southern Russia and urban distribution routes | Medium term (2-4 years) |

| Water-Scarcity Constraints on Mills | -0.1% | Pulp‐producing regions with aging hydraulic systems | Long term (≥ 4 years) |

| Dependence on Imported Virgin Fibre | -0.1% | National converters making premium kraftliner and specialty boards | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recycled Paper Price Volatility

Domestic OCC recovery already runs at 88%, so any demand spike quickly forces imports. European OCC costs hover near half the Russian price, tempting spot buyers but exposing them to ruble swings.[1]Recycling Today staff, “Mixed Paper, OCC End Year on Downward Trend,” recyclingtoday.com Converters therefore juggle higher safety stocks and hedge contracts, yet margin squeeze persists because retailers resist surcharges. Broadening EPR coverage to lower-grade papers is critical, but infrastructure roll-out lags.

Competition from Returnable Plastic Crates

Large grocers are piloting reusable plastic crates for short‐haul produce runs. Crates outlast cartons over 20-plus cycles and stack efficiently, but they require costly washbacks and reverse logistics. Corrugated remains preferred where routes are fragmented or transnational, and where retailers value on-pack graphics for brand storytelling. Box suppliers need life-cycle data to demonstrate carbon parity and to promote quick-collapse designs that minimize back-haul voids.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Linerboard Dominates but Nears Collection Limits

Recycled linerboard captured 68.32% of the Russia corrugated market share in 2025 as brands prioritized levy-free, circular substrates. The Russia corrugated market size for this grade is projected to expand at a 3.62% CAGR, even though OCC recovery hovers at 88%. Producers curb volatility by diversifying bale supply through European spot cargoes, yet currency swings can erase savings. Virgin Kraftliner sustains premium niches such as pharma and cosmetics, where purity and print gloss command higher margins. Mill expansions in Irkutsk and Arkhangelsk will lift domestic virgin output by over 1 million tonnes by 2027, but forestry headwinds may temper ambitions.

Corrugating medium and semi-chemical fluting fill structural roles in double-wall boards for grain, timber, and appliance shipments. Specialty coatings that repel condensation are gaining favor among fish exporters, yet volumes stay niche. Second-generation OCC sorting lines and AI-based quality scanners promise yield boosts without new collection tonnage. EPR cash flows are earmarked for bin deployments in mid-sized cities, potentially raising feedstock by 0.4 million tonnes if targets hold. Until then, recycled linerboard profitability hinges on agile spot buying and tighter energy management. Virgin producers meanwhile market low-basis-weight kraftliner to offset cost premiums and to break into e-commerce formats that formerly defaulted to recycled liners.

By Flute Type: E Flute Wins as Parcel Weight Shrinks

B flute held 35.92% of 2025 tonnage thanks to robust performance in vegetables and household staples. Yet parcels are slimming, and E flute’s micro-profile reduces dimensional fees, letting online sellers shave shipping costs. The Russia corrugated market for E flute is therefore poised for a 3.79% CAGR, comfortably above the headline rate. Printers exploit its smooth surface for high-definition brand imagery, critical for cosmetics and nutraceuticals. C and A flutes defend heavy loads like furniture and machinery, but grow modestly as product redesigns squeeze excess weight. F flute, scarcely 1 mm thick, emerges in luxury confectionery and gifting.

Converters increasingly laminate B + E flute combinations to balance cushioning and volumetric efficiency. Digital die-cut tables streamline microflute blanking and trimming set-up costs for small-batch runs. However, thinner calipers risk crush failures in long rail hauls across Siberia, so sellers often specify reinforced corner posts or integrated pulp inserts. As average order values continue to contract, flute selection calculus will pivot more on freight math than on static lab tests.

By Packaging Type: Regular Slotted Containers Remain Workhorse

Regular slotted containers retained a 37.69% share in 2025 and are expanding fastest at a 4.17% CAGR as automated erecting lines push throughput in grocery and electronics hubs. Their universal blank optimizes knife changeovers, reinforcing dominance in high-volume e-commerce flows. Die-cut custom boxes woo craft brewers and SME exporters that seek shelf pop and storytelling real estate. Folding cartons blur lines between paperboard and micro-fluted corrugated, allowing producers to court pharma contracts that demand tamper-evident seals and insert partitions.

Point-of-purchase displays and pallet boxes represent niche volume but punch above their weight in terms of value, leveraging high-impact graphics at product launches. Robotic pick-and-place systems now assemble RSCs in 0.8 seconds, shrinking labor footprints. Yet as levy schedules reward weight reduction, some platforms experiment with mailers that integrate molded pulp pads, substituting bulky void-fill. The Russian corrugated market, therefore, bifurcates into cost-optimized generic shells and richly printed lifestyle packs, compelling converters to operate both mega-volume flexo assets and nimble digital lines.

By Wall Type: Single-Wall Retains Sweet Spot for Cost and Strength

Single-wall boards held a 42.67% share and are forecast to grow at a 3.86% CAGR, serving 1-5 kg parcels that dominate marketplace traffic. Enhancements to starch-based adhesives and cross-linking resins increase compression strength, enabling encroachment into double-wall turf without material penalties. Double-wall persists for white goods and outbound rail to Central Asia, where vibration warrants extra cushioning. Triple-wall displaces plywood crates for industrial pumps and power-train modules but remains a niche.

Single-face webs thrive as inner wraps and void fill across the Russian corrugated market, protecting fragile SKUs without resorting to plastic bubbles. Integrated plants now run real-time edge-crush testing to validate downgauging, saving up to 8% fiber per square meter. Yet insurers often mandate double-wall for export insurance, limiting substitution. Expect insurers to adopt performance-based rather than construction-based criteria, unleashing further single-wall penetration.

By Printing Technology: Digital Inkjet Bridges Customization Gap

Flexographic presses accounted for 33.41% of impressions in 2025, churning out millions of identical pizza and detergent cartons at two-digit cents each. Digital inkjet, posting a 3.67% CAGR, addresses the Russia corrugated market’s hunger for small promotional runs and regional language variants. Single-pass aqueous systems hit 9,000 m²-h with food-safe inks, meeting retailer mandates for indirect food contact.

Litho-laminated sheets continue to dress up perfume and chocolate boxes, though cost pressure could cede share to high-density four-color inkjet. Screen and hybrid methods occupy decorative niches such as metallic accents and Braille varnish. Aging machinery, averaging 12 years, hampers throughput. State export benefits now cover up to 30% of capex on domestically assembled digital presses, nudging converters toward modernization. Plants installing inline quality cameras report 40% fewer remakes and faster root-cause analytics.

By End-User Industry: E-Commerce Fulfillment Sets the Pace

Fresh food and produce still led volume in 2025, yet e-commerce fulfillment centers top the growth league at 3.53% CAGR. Marketplace sellers demand auto-lock bottoms and tear-strip openings that enhance consumer unboxing. Processed foods, beverages, and confectionery account for over one-third of secondary packaging spend, using wax-resistant coatings and high-impact flexo to survive cold storage.

Electrical appliances lean on double-wall cartons with vibration pads, while pharmaceuticals standardize micro-flute inserts that comply with GOST 17768-90. Craft breweries, niche cosmetics, and home-grown electronics brands collectively push converters toward micro-run agility as they vie for online shelf space. The Russia corrugated market thus experiences a tilt from low-SKU mass production toward high-mix, data-driven scheduling, rewarding ERP-enabled factories that can switch jobs with sub-30-minute downtime.

Geography Analysis

The Central and Northwestern districts account for more than 60% of the Russian corrugated market, leveraging their proximity to the distribution hubs of Moscow and St. Petersburg. Plants in Podolsk, Istra, and Leningrad Oblast feed mega-fulfillment centers that dispatch millions of parcels daily. Siberia’s Irkutsk cluster, anchored by Ust-Ilimsk, exports virgin kraftliner to China but battles rail congestion east of Lake Baikal. Southern regions Adygea, Krasnodar, and Rostov are rising fast as agribusiness packaging demand and regional incentives lure fresh capacity.

Adygea’s Kartontara-2 and planned paper mill could transform the republic into the South’s biggest corrugated node, trimming freight costs for fruit and vegetable growers shipping to Black Sea ports. Bashkortostan’s new Dobry Karton site fills a geographic gap in the Urals, offering two-day delivery to Yekaterinburg and Chelyabinsk.[2]WhatWood editors, “SFT Group Launches New Kartontara-2 Plant,” whatwood.ru Tula and Tver expansions cluster near the M-11 and North-South corridors, exploiting motorway upgrades that cut transit time to Baltic docks.

Far East ports eye freezer cargo to Japan and South Korea, demanding moisture-proof cartons. Yet distant mills face high backhaul voids because westbound container traffic remains light. Policy grants on rail tariffs and forwarding services partially offset the imbalance, but many exporters still trans-ship via St. Petersburg. Differences in regional enforcement of EPR fees also shape competitive positioning. Urban prefectures already audit recycling declarations, whereas rural oblasts lag, offering temporary reprieve on levy hikes.

Competitive Landscape

With the top-20 players holding under 30% share, the Russian corrugated market remains structurally fragmented, though greenfield projects are accelerating consolidation. Integrated giants such as Ilim Group, Segezha Group, and SFT Group leverage captive fiber supply to offset OCC volatility and to guarantee chain-of-custody compliance sought by multinational FMCG buyers. Ilim’s 600,000-tonne kraftliner machine anchors a USD 1.3 billion complex that feeds both domestic converters and Chinese importers.[3]PaperAge newsroom, “Ilim Group Nearing Start-Up of New Kraftliner Machine,” paperage.com SFT Group’s multi-site Seven Winds upgrades boost flexo capacity by 40%, enabling quick-turn color runs for regional grocers.

Emerging challengers like L-Pak and Dobry Karton tap Industrial Development Fund loans and special economic-zone tax holidays to install automated corrugators, robotic palletizers, and inline digital presses. Their strategy revolves around servicing craft breweries, SMEs, and marketplace merchants that big mills often underserve. Technology vendors, including Gofro-Technologies and RussKom, demo modular folding-gluing lines and cut-on-demand plotters at RosUpack, sparking a race to shorten order-to-ship cycles.

Environmental compliance is an arena for differentiation. Syktyvkar Forest Industry Complex runs biomass boilers to cut GHG intensity to 0.3 tCO₂e t-¹, giving its cartonboard a lower carbon footprint badge attractive to export‐minded converters.[4]Sustainability journal, Nadezhda Shmeleva et al., “Open Environmental Collaborations,” eipc.center Mills lagging on BAT retrofits face steeper permit fees and inspection risk, nudging them to partner with Chinese EPC firms offering turnkey bleach-plant revamps under sanctions-evading payment structures.

Russia Corrugated Packaging Industry Leaders

JSC Ilim Group

Arkhangelsk Pulp and Paper Mill

JSC Solikamskbumprom

Segezha Group

JSC SLPK

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Dobry Karton opened a Bashkortostan corrugated plant for RUB 1.2 billion (USD 15.6 million), adding 70 million m² of annual capacity.

- June 2025: Gofro-Technologies showcased robotic palletizing with Shinko SA-619 FT at RosUpack 2025.

- March 2025: Ilim Group’s Ust-Ilimsk kraftliner mill hit 600,000 tons y-¹ design rate.

- March 2025: MarketPrint deployed a G!Digital SC600 inkjet press in Moscow.

Russia Corrugated Packaging Market Report Scope

The Russia corrugated packaging market is the sector responsible for manufacturing and converting paperboard into fluted containers and protective materials, including single-face, single-wall, double-wall, and triple-wall configurations. This industry serves as a critical infrastructure for domestic logistics, providing essential transport and retail-ready packaging solutions that are recyclable and increasingly favored over plastic alternatives. Furthermore, the study covers the regulatory impact of federal plastic-ban roadmaps and the import-substitution drive, alongside a competitive assessment of the newly restructured local manufacturing landscape.

The Russia Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material Type | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current Russia corrugated market size and its expected growth?

The Russia corrugated market size stands at USD 6.89 billion in 2026 and is projected to reach USD 7.61 billion by 2031, expanding at a 2.01% CAGR over 2026-2031.

Which segment leads the Russia corrugated market by material?

Recycled linerboard leads, holding 68.32% market share in 2025, driven by cost savings and EPR incentives.

Why is E flute gaining popularity among Russian converters?

E flute’s thin profile lowers parcel dimensional weight, aligns with e-commerce shipping fees, and supports high-resolution digital printing that boosts brand visibility.

How are regulations influencing packaging design in Russia?

Extended Producer Responsibility laws raise recycling targets and levies, prompting converters to adopt mono-material corrugated designs and water-based inks to avoid penalties.

Which regions are emerging as growth hotspots for corrugated production?

Southern territories such as Adygea, Krasnodar, and Bashkortostan are drawing new mills to serve agribusiness exports and cut logistics costs.

What technologies are Russian plants adopting to stay competitive?

Investments focus on single-pass digital inkjet presses, robotic palletizers, real-time quality sensors, and BAT-compliant wastewater systems to boost agility and sustainability.

Page last updated on: