Asia-Pacific White LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

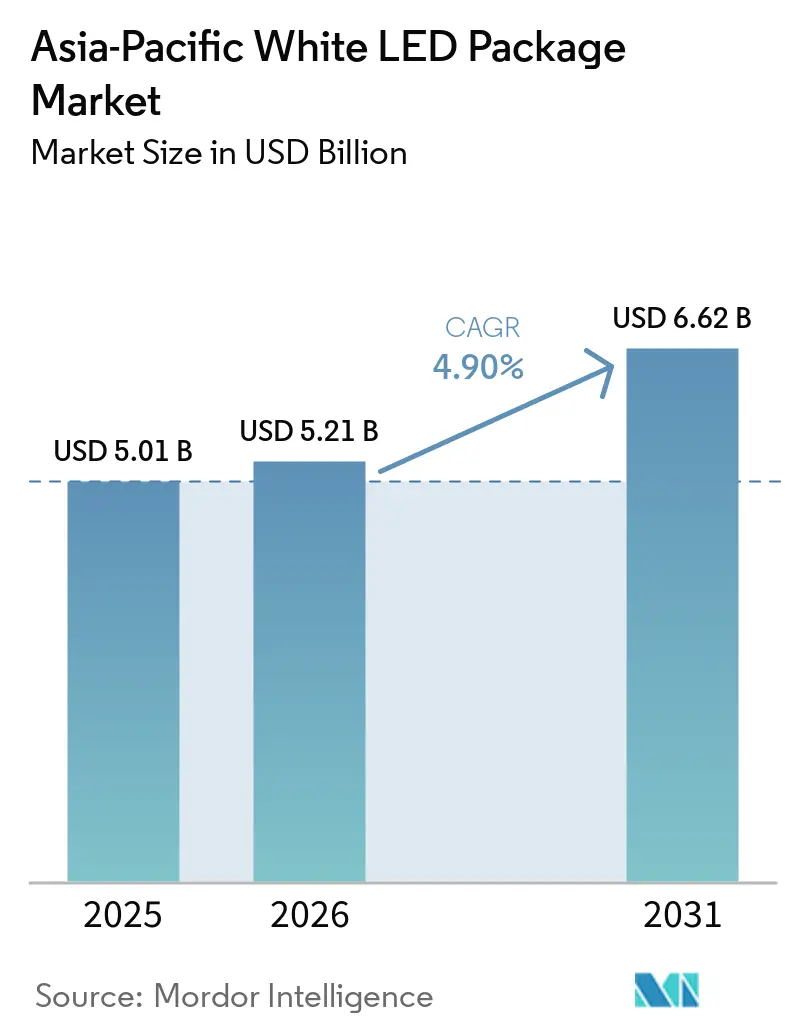

| Base Year Market Size (2025) | USD 5.01 Billion |

| Market Size (2026) | USD 5.21 Billion |

| Market Size (2031) | USD 6.62 Billion |

| Growth Rate (2026 - 2031) | 4.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific White LED Package Market Analysis by Mordor Intelligence

The Asia-Pacific white LED package market size is expected to grow from USD 5.01 billion in 2025 to USD 5.21 billion in 2026 and is forecast to reach USD 6.62 billion by 2031 at a 4.9% CAGR over 2026-2031. Continued policy support for solid-state lighting, rising mini-LED backlighting adoption in consumer electronics, and rapid electric-vehicle (EV) charging-station build-outs reinforce a steady demand baseline even as patent disputes inject near-term supply risk. Advances in wafer-level chip-scale packaging compress thermal resistance, trim die footprint, and unlock incremental margin in automotive daytime running lamps and direct-view displays. China dominates the Asia-Pacific white LED package market on the strength of fully integrated sapphire, phosphor, and back-end assembly clusters, yet Southeast Asian and Indian capacity additions are eroding that concentration as OEMs diversify tariff exposure. Currency and rare-earth volatility remain watchpoints, but most tier-one suppliers now hedge europium and terbium oxide requirements for up to 24 months, dampening price shocks.

Key Report Takeaways

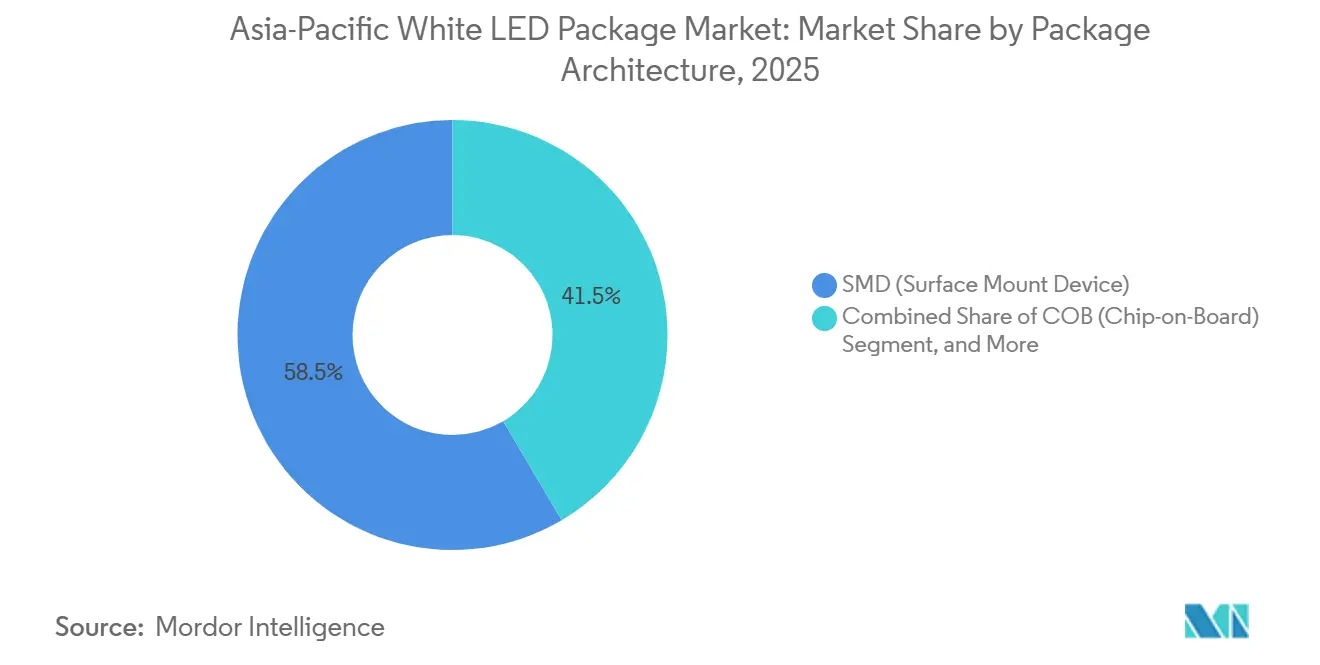

- By package architecture, surface-mount device (SMD) formats held 58.48% of the Asia-Pacific white LED package market share in 2025, while chip-scale packages (CSP) are projected to expand at a 5.49% CAGR through 2031.

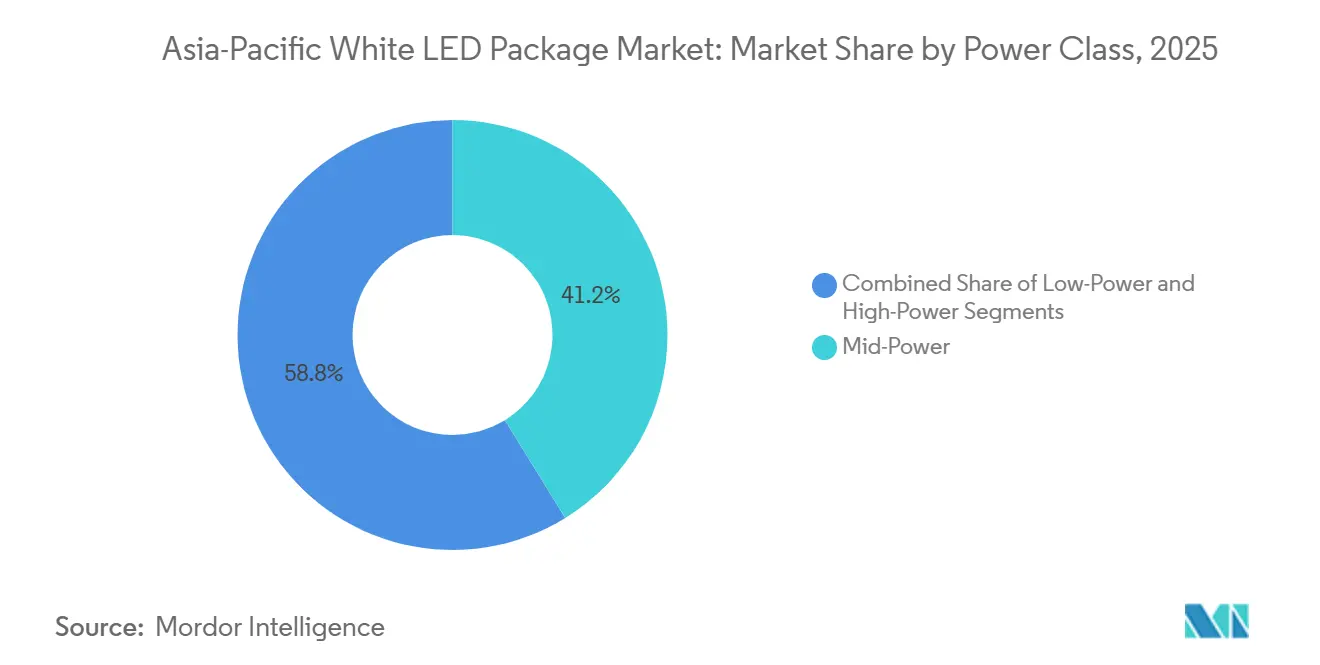

- By power class, mid-power devices between 0.5 W and 1 W captured 41.22% of the Asia-Pacific white LED package market size in 2025, whereas high-power packages above 1 W are advancing at a 5.55% CAGR to 2031.

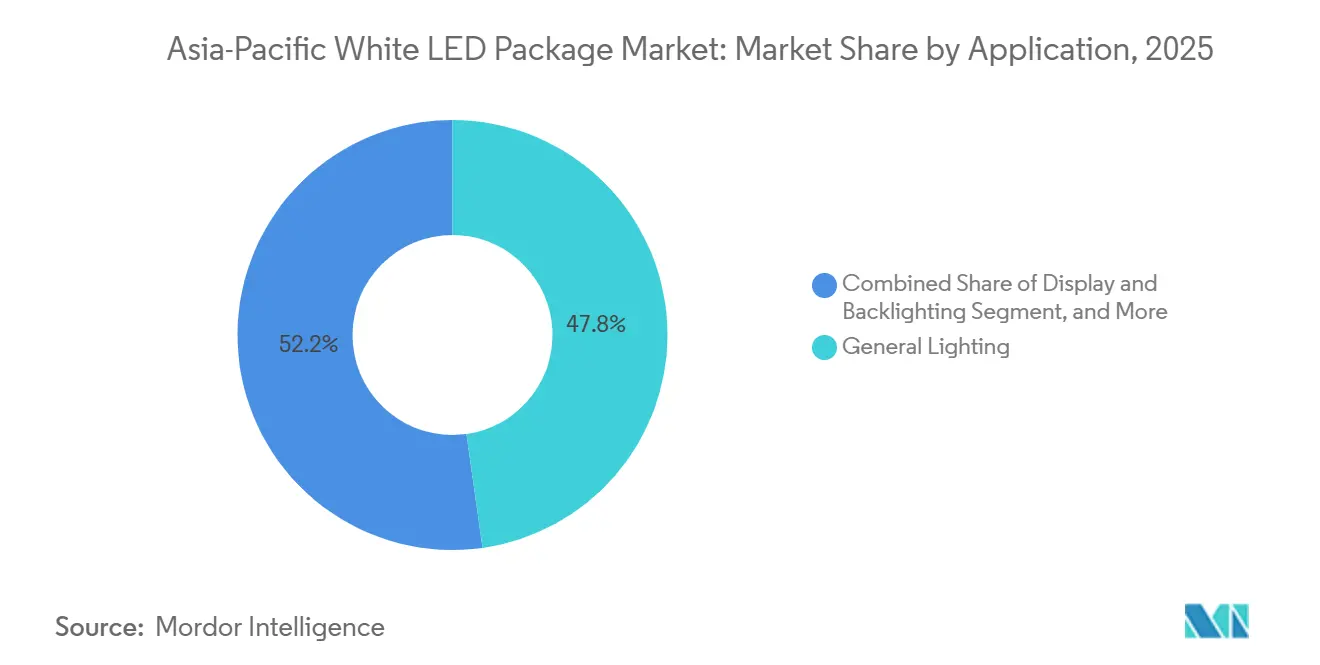

- By application, general lighting led with a 47.78% revenue share in 2025, yet automotive lighting is the fastest-growing use-case, accelerating at a 5.84% CAGR to 2031.

- By geography, China accounted for 53.49% of Asia-Pacific revenue in 2025, but India is the standout growth engine, with a 5.68% CAGR projected through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific White LED Package Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Mini and Micro-LED Backlighting Demand in Smart TVs | +1.2% | China, Japan, South Korea, spillover to Southeast Asia | Medium term (2-4 years) |

| Aggressive SSL Incentive Programs Across Southeast Asia | +0.9% | Thailand, Vietnam, Indonesia, Philippines | Short term (≤ 2 years) |

| Rapid Build-out of EV Charging-Station Lighting Networks | +0.8% | China tier-two cities, India metros, ASEAN capitals | Medium term (2-4 years) |

| Cost Downsizing via Wafer-Level CSP Adoption | +0.7% | Global, led by Taiwan and mainland China fab clusters | Long term (≥ 4 years) |

| Proliferation of UV-Free Health-Oriented Lighting in Japan | +0.4% | Japan residential and healthcare segments | Long term (≥ 4 years) |

| Mandatory Energy-Efficiency Labelling in India and China | +0.6% | India nationwide, China urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Mini And Micro-LED Backlighting Demand In Smart TVs

Premium television brands introduced RGB mini-LED sets at the January 2026 Consumer Electronics Show, demonstrating zone counts as high as 43,000 and peak brightness above 4,000 nits. Eliminating quantum-dot films trims the bill of materials by 15% once die yields stabilize, redirecting savings toward higher-value chip-scale packages. Guangdong and Jiangsu panel assemblers are installing placement tools with sub-5 µm accuracy to manage the tighter pitch, favoring LED suppliers that co-locate back-end assembly within 50 km of module plants. As sub-100 µm die enters volume production, the Asia-Pacific white LED package market migrates from commodity SMD to high-power wafer-level CSP capable of dissipating 3 W mm-2. The trend lifts luminance requirements, driving upstream demand for advanced phosphor blends that maintain color-point stability at elevated current densities.

Aggressive SSL Incentive Programs Across Southeast Asia

Thailand extended double corporate-tax deductions for LED retrofits through 2028, Indonesia preserved its 30% national energy-savings target, and Vietnam plans an Asian Development Bank-backed efficiency framework.[1]Ministry of Energy Thailand, “Extended Tax Deduction for Energy Efficiency,” thaigov.go.th These incentives compress lighting payback periods to below 18 months, catalyzing public-sector procurement that prioritizes efficacy over color rendering or lifetime. As municipal buyers standardize on 100 lm/W thresholds, mid-power SMD suppliers face accelerated commoditization. The Asia-Pacific white LED package market therefore sees a volume swell in entry-level devices even as value pools migrate to premium automotive and display niches. Policy momentum is strongest in the commercial high-bay and roadway categories, locking in a multi-year demand base for 2835- and 3030-footprint footprints fabricated in Thai and Vietnamese export-processing zones.

Rapid Build-Out Of EV Charging-Station Lighting Networks

Chengdu retrofitted more than 600 streetlight poles with 7 kW Level 2 chargers in April 2026, cutting the installed cost 40% relative to standalone posts.[2]China Daily, “Chengdu Installs Combined Lighting and EV Charging Poles,” chinadaily.com.cn Delhi and Bengaluru issued similar tenders early 2026, specifying IP66 packages rated for 50,000 h at 95 °C junction temperature. The dual-use approach distributes power infrastructure without grid-upgrade delays, boosting demand for high-power flip-chip LEDs that maintain lumen maintenance under elevated ambient heat. As other tier-two Chinese and Indian cities replicate the model, the Asia-Pacific white LED package market pivots toward CSPs and chip-on-board (COB) platforms optimized for thermal dissipation. By integrating lighting and charging, municipalities unlock new revenue streams, enabling premium pricing that offsets phosphor-cost inflation.

Cost Downsizing Via Wafer-Level CSP Adoption

Fan-out wafer-level packaging eliminates wire-bonds and reduces footprint up to 60% while achieving thermal resistance below 8 K W-1. Taiwan Semiconductor Manufacturing Company and Advanced Semiconductor Engineering each expanded fan-out lines in 2025-2026, pursuing automotive and monitor backlight orders that exceed the 10 million-unit monthly crossover for cost parity. As yields climb beyond 98%, CSPs begin displacing SMD incumbents in mid-power ranges where price elasticity once precluded the use of premium substrates. The Asia-Pacific white LED package market, therefore, captures manufacturing learning curves that lower per-lumen cost and improve reliability, accelerating OEM qualification cycles in adaptive-beam headlamps and gaming monitors.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent IP Litigation Over Flip-Chip Architectures | -0.6% | Global, concentrated in North American and European venues | Short term (≤ 2 years) |

| Thermal Management Challenges Above 3 W Power Class | -0.5% | Automotive and specialty lighting segments across Asia-Pacific | Medium term (2-4 years) |

| Supply Tightness of High CRI Phosphors | -0.4% | China, Japan, South Korea phosphor chains | Medium term (2-4 years) |

| Rising Mini-LED Die Cost Due to Sapphire Substrate Inflation | -0.3% | Global, acute in China and Taiwan fab operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent IP Litigation Over Flip-Chip Architectures

Everlight Electronics lodged patent claims against Lumileds and Seoul Semiconductor in February 2026, citing infringement of U.S. Patent 7,554,126 covering direct-bond flip-chip methods. Injunction risk and escalating legal expenses deter tier-two assemblers from investing in flip-chip tooling, consolidating capacity among vertically integrated giants. OEMs now negotiate indemnification clauses that add 3-5% to contract prices, tempering adoption velocity even where thermal benefits are clear. The Asia-Pacific white LED package market thus experiences a short-term drag on high-power CSP penetration, although incumbent suppliers leverage the dispute to justify premium pricing on authenticated packages.

Thermal Management Challenges Above 3 W Power Class

Automotive headlamps running above 3 W per package encounter junction temperatures approaching 115 °C, where phosphor degradation accelerates and lumen output halves.[3]LEDs Magazine, “Thermal Runaway in High-Power LEDs,” ledsmagazine.com Insulated metal-substrate boards mitigate heat but add USD 0.15-0.40 per package, pressuring margins in cost-sensitive exterior-lighting bids. Advanced substrates such as copper-tungsten composites enhance thermal conductivity but remain confined to aerospace budgets. Until interface materials exceed 10 W m-1 K-1 at automotive price points, high-power adoption in mass-market sedans may lag. The Asia-Pacific white LED package market, therefore, balances performance gains against system-level economics, capping high-power share growth despite rising EV volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Package Architecture: Wafer-Level Formats Challenge SMD Incumbency

Surface-mount device packages captured 58.48% of the Asia-Pacific white LED package market share in 2025, reflecting entrenched adoption in retrofit bulbs and tubes. Wafer-level CSP formats are expanding at a 5.49% CAGR and, by 2031, are expected to shoulder a sizeable portion of automotive headlamp and premium display orders. The Asia-Pacific white LED package market size tied to CSP technology is projected to rise steadily as OEMs seek smaller footprints, higher drive currents, and lower thermal resistance. Margin pressure, however, remains acute in SMD lines where Shenzhen and Dongguan contract factories quote assembly at USD 0.02 per device, undercutting legacy brands by 40%.

High-bay and stadium operators still favor chip-on-board arrays for punchy lumen outputs, while flip-chip packages dominate premium automotive daytime running lamps despite pending litigation. Over the forecast horizon, economics favor CSP lines once monthly volumes top 10 million units, pulling SMD incumbents into retrofit niches or prompting technology upgrades. Suppliers with fan-out expertise gain leverage as television panel makers compress product cycles and demand co-located assembly to meet just-in-time inventory goals. Consequently, the Asia-Pacific white LED package market aligns capital spending with wafer-level processes that promise both cost and performance advantages.

By Power Class: High-Power Segments Outpace Mid-Power Commoditization

Mid-power LEDs between 0.5 W and 1 W controlled 41.22% of the Asia-Pacific white LED package market size in 2025, thanks to price-sensitive general-lighting retrofits. Nevertheless, high-power packages above 1 W are growing 5.55% annually, propelled by adaptive-beam automotive lamps that need more than 1,000 lumens per emitter. The Asia-Pacific white LED package market value associated with these high-power devices is climbing faster than volume because ceramic and metal-core substrates command premiums.

Chinese suppliers routinely post efficacies above 180 lm W-1 for mid-power nodes at USD 0.05 each, eroding branded margins, while low-power indicators below 0.5 W ride the smart-home wave with standby currents under 10 µA. Automotive specifications require junction temperatures below 95 °C and lifetimes beyond 50,000 h, driving substrate spend to USD 0.30-0.60 per unit. Meanwhile, China’s GB/T 31831-2025 efficacy ratchet, effective April 2026, pressures obsolete mid-power offerings and nudges demand toward CSP devices delivering improved light extraction. Overall, the Asia-Pacific white LED package market positions high-power formats as the clear value-creation frontier despite thermal engineering headwinds.

By Application: Automotive Lighting Outpaces General Illumination

General lighting remained the largest slice of the Asia-Pacific white LED package market at 47.78% in 2025, yet automotive lighting is the velocity leader with a 5.84% CAGR to 2031. Electric-vehicle programs bundle LED headlamps, daytime running lamps, and interior mood lighting as baseline equipment, increasing per-car diode counts. Display backlighting re-accelerated in 2025-2026 when mini-LED televisions shipped in volume, drawing sub-100 µm die with stringent binning requirements. Specialty verticals such as horticulture and medical lighting gain from spectral-tuning features that command higher ASPs.

Municipal retrofits integrating EV chargers, such as Chengdu’s 600 dual-use poles, illustrate how general-illumination infrastructure can generate incremental revenue while mitigating the need for transformer upgrades. In displays, Samsung and peers unveiled panels with up to 43,000 local-dimming zones, a design that multiplies LED demand per set several-fold. Across segments, the Asia-Pacific white LED package market delivers differentiated value propositions, cost efficiency in general lighting, performance leadership in automotive, contrast enhancement in displays, and biological efficacy in horticulture. Suppliers balance portfolio mix to hedge against price compression in commoditized channels while capitalizing on high-margin niches.

Geography Analysis

China generated 53.49% of the Asia-Pacific white LED package market revenue in 2025, leveraging cradle-to-grave supply integration from sapphire boules to final packaging. State funds totaling CNY 150 billion (USD 21.3 billion) channeled into compound-semiconductor fabs between 2024-2026 strengthen domestic control over critical inputs. Nevertheless, U.S. tariffs doubling to 50% in 2025 pushed OEMs to diversify assembly footprints toward Thailand, Vietnam, and Malaysia, where final testing circumvents elevated duties. India, aided by Bureau of Energy Efficiency star labeling ratchets and state procurement mandates, is tracking a 5.68% CAGR as utility-funded streetlight conversions accelerate.

Japan remains a premium pocket where CRI > 95 and flicker-free drivers hold sway in residential and healthcare settings. The 2026 rise of human-centric lighting that syncs correlated color temperature with circadian cycles further lifts unit ASPs. Southeast Asian markets, seeded by Asian Development Bank energy-efficiency loans, deploy double-tax deductions that cut retrofit payback to well under two years. Australia and New Zealand contribute a single-digit share yet punch above their weight in per-capita LED spend, driven by utility subsidies aimed at deferring grid upgrades.

China’s forthcoming GB 30255-2026 standard widens scope to spotlights and smart lamps by September 2027, locking in efficiency and standby limits that will obsolete under-performing imports. Simultaneously, San’an Optoelectronics’ silicon-carbide expansion to 16,000 6-inch and 1,000 8-inch wafers monthly positions China as both LED and power-device powerhouse. Over the forecast horizon, cross-border supply-chain shifts may trim China’s share 2-3 percentage points, but absolute sales continue to rise as the Asia-Pacific white LED package market itself expands.

Competitive Landscape

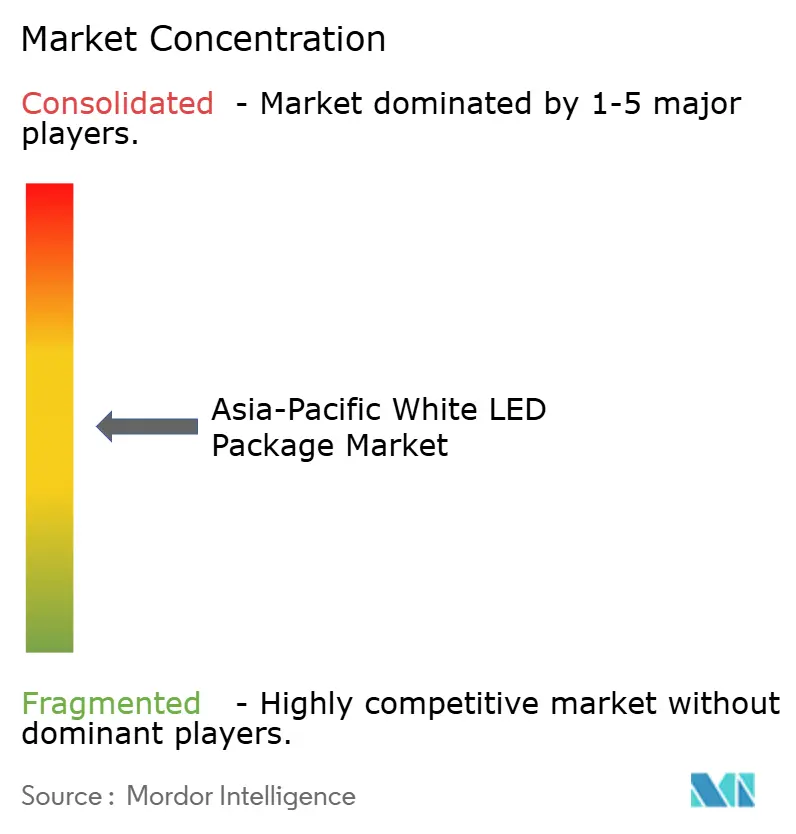

The Asia-Pacific white LED package market exhibits moderate concentration, with the top five suppliers accounting for roughly half of 2025 revenue, leaving a long tail of more than 50 contract assemblers. Incumbents defend share with broad patent estates around flip-chip bonding, narrow-band phosphors, and wafer-level fan-out processes, yet Shenzhen and Dongguan newcomers slash SMD pricing by up to 40%. Everlight’s February 2026 suits against Lumileds and Seoul Semiconductor highlight the stakes, as proven IP provides the last bulwark against cost-driven erosion.

Differentiation increasingly hinges on high-power thermal performance and ultra-tight color binning that support HDR displays. LG Innotek’s plan to double substrate capacity by the second half of 2027 targets flip-chip ball-grid arrays for automotive radar and RF system-in-package applications, yielding cross-segment synergies. Advanced Semiconductor Engineering’s NT$ 17.6 billion (USD 550 million) K18B plant, coming online in 2028, will specialize in fan-out wafer-level lines that shrink the footprint 60%, reinforcing long-term CSP economics.

Niche players such as Refond Optoelectronics and Hongli Zhihui secure potassium-fluorosilicate red-phosphor licenses to serve high-CRI markets without infringing legacy portfolios. Fabless design houses outsource EPI and dicing but keep phosphor coating in-house, shortening development cycles and reducing capex. As mini-LED backlighting scales, suppliers with die-attach accuracy below 5 µm and thermal resistance under 5 K W-1 gain pricing power, reinforcing a two-tier structure where scale players chase volume while specialists harvest margin in demanding automotive, horticulture, and display segments.

Asia-Pacific White LED Package Industry Leaders

Nichia Corporation

Samsung Electronics Co. Ltd.

Seoul Semiconductor Co. Ltd.

Everlight Electronics Co. Ltd.

Lumileds Holding B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Chengdu commissioned 600 streetlight poles integrating 7 kW EV chargers, cutting per-unit installation cost 40% compared with standalone posts.

- March 2026: China’s GB/T 31831-2025 efficacy standard entered force, lifting minimum efficacy to 105 lm W-1 for non-directional LED lamps.

- February 2026: Everlight Electronics filed patent-infringement lawsuits against Lumileds and Seoul Semiconductor, asserting violations of U.S. Patent 7,554,126 related to flip-chip bonding.

- January 2026: Samsung Electronics, LG Electronics, Hisense, and TCL debuted RGB mini-LED televisions with up to 43,000 dimming zones and 4,000 nits peak brightness at CES 2026.

Asia-Pacific White LED Package Market Report Scope

The Asia-Pacific White LED Package Market refers to the market encompassing the design, development, and production of white LED packages.

The Asia-Pacific White LED Package Market Report is Segmented by Package Architecture (SMD, COB, CSP, and Flip-Chip LED Packages), Power Class (Low Power, Mid Power, and High Power), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty), and Country (China, Japan, India, Southeast Asia, and the rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| SMD (Surface Mount Device) |

| COB (Chip-on-Board) |

| CSP (Chip Scale Package) |

| Flip-Chip LED Packages |

| Low Power (Less than 0.5 W) |

| Mid Power (0.5 -1 W) |

| High Power (More than 1 W) |

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Specialty / Niche |

| China |

| Japan |

| India |

| Southeast Asia |

| Rest of Asia-Pacific |

| By Package Architecture | SMD (Surface Mount Device) |

| COB (Chip-on-Board) | |

| CSP (Chip Scale Package) | |

| Flip-Chip LED Packages | |

| By Power Class | Low Power (Less than 0.5 W) |

| Mid Power (0.5 -1 W) | |

| High Power (More than 1 W) | |

| By Application | General Lighting |

| Automotive Lighting | |

| Display and Backlighting | |

| Specialty / Niche | |

| By Country | China |

| Japan | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia -acific white LED package market in revenue terms today?

It reached USD 5.21 billion in 2026 and is forecast to climb to USD 6.62 billion by 2031.

What CAGR is expected for Asia-Pacific white LED packages through 2031?

The market is projected to expand at a 4.9% CAGR over 2026-2031.

Which package architecture is growing fastest?

Wafer-level chip-scale packages are the fastest-growing format, advancing at a 5.49% CAGR.

Why is automotive lighting outperforming general illumination?

EV production bundles adaptive headlamps and daytime running lamps as standard equipment, boosting high-power LED demand.

Which country is anticipated to post the strongest growth?

India is on track for a 5.68% CAGR through 2031, driven by mandatory efficiency labeling and public-sector procurement mandates.

Page last updated on: