Europe White LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.55 Billion |

| Market Size (2026) | USD 1.59 Billion |

| Market Size (2031) | USD 1.88 Billion |

| Growth Rate (2026 - 2031) | 3.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe White LED Package Market Analysis by Mordor Intelligence

The Europe White LED Package market size is projected to be USD 1.55 billion in 2025, USD 1.59 billion in 2026, and reach USD 1.88 billion by 2031, growing at a CAGR of 3.36% from 2026 to 2031. Replacement cycles in municipal and commercial lighting, regulatory mandates on energy efficiency, and rising electricity tariffs sustain volume growth, yet expanded manufacturing capacity keeps average selling prices subdued. Automotive original equipment manufacturers continue shifting to pixelated LED arrays, which cascades demand for high-power chip-scale packages and flip-chip formats. Meanwhile, vertical-farming operators are emerging as a niche customer set that values precise spectrum control and can absorb premium pricing. Competitive tension stems from Asian entrants pricing mid-power surface-mount devices below USD 0.50, prompting established European suppliers to focus on application-specific modules that combine drivers, optics, and thermal substrates.

Key Report Takeaways

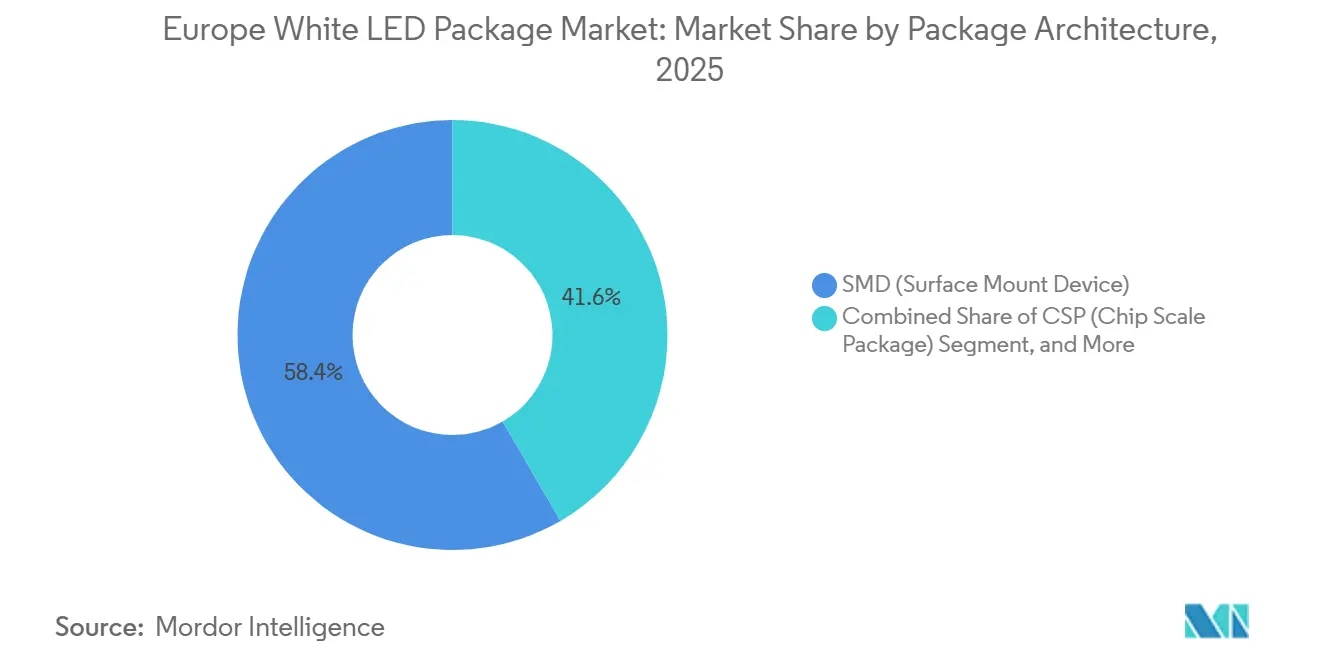

- By package architecture, surface-mount device packages led with 58.38% of the Europe White LED Package market share in 2025. Chip-scale packages are forecast to expand at a 3.88% CAGR through 2031.

- By power class, mid-power devices accounted for 42.73% of the Europe White LED Package market in 2025, while high-power devices are projected to grow at a 3.95% CAGR between 2026 and 2031.

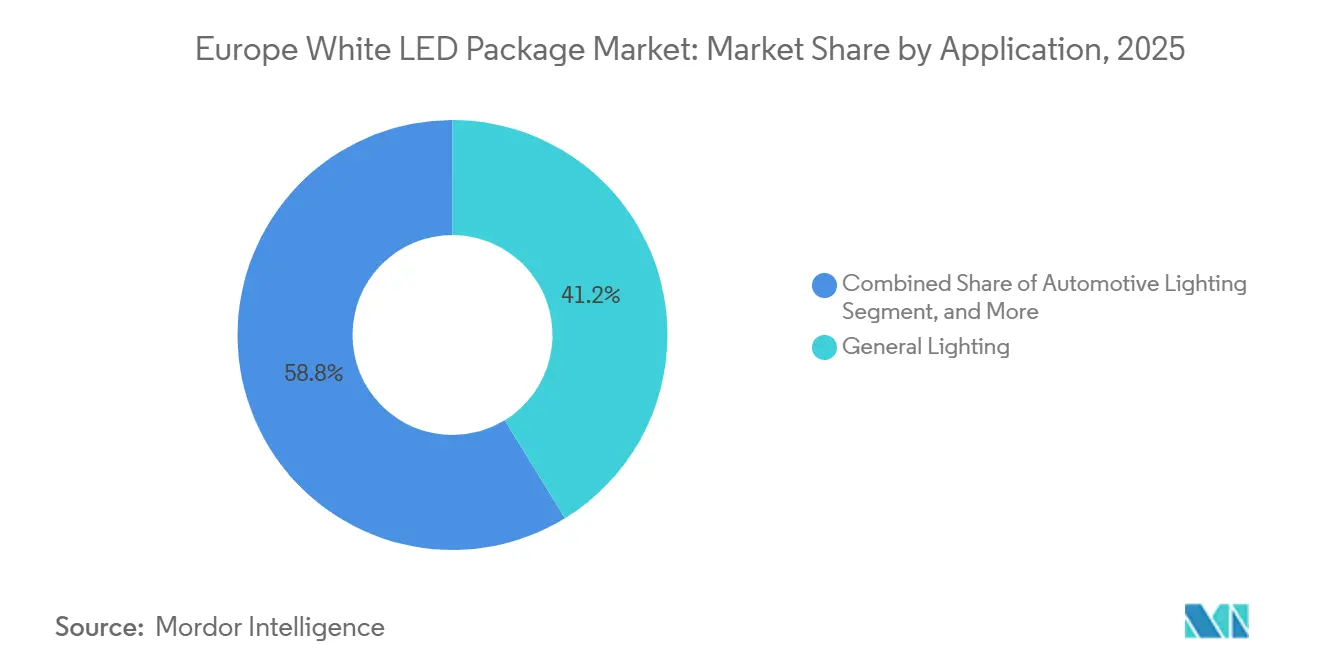

- By application, general lighting accounted for 41.23% of revenue in 2025; automotive lighting is advancing at a 3.72% CAGR through 2031.

- By geography, Germany accounted for 27.64% of 2025 revenue, whereas France is positioned for the fastest growth at a 3.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe White LED Package Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy Efficiency Regulations Tightening Across EU | +1.1% | EU-wide, strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| Declining LED Package Costs Due to Economies of Scale | +0.8% | Global, with EU price-sensitive segments (general lighting, mid-power SMD) | Short term (≤ 2 years) |

| Accelerated Adoption in Automotive Adaptive Headlamps | +0.7% | Germany, France, UK (OEM hubs and Tier-1 suppliers) | Medium term (2-4 years) |

| Rising Electricity Costs Driving Commercial Retrofit Acceleration | +0.5% | EU-wide, most acute in Germany, UK, France, Netherlands | Short term (≤ 2 years) |

| EU RoHS Phase-Out of Mercury-Based Back-Lights | +0.4% | EU-wide, concentrated in display and backlighting segments | Short term (≤ 2 years) |

| Expansion of Vertical Farming Using White LEDs | +0.3% | Netherlands, France, UK (controlled-environment agriculture clusters) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy Efficiency Regulations Tightening Across the EU

The Energy Efficiency Directive 2023/1791/EU compels member states to reduce final energy consumption by 11.7% by 2030, while the Ecodesign Regulation 2019/2020 bans non-directional lamps with a luminous efficacy below 85 lumens per watt, pushing public agencies to specify LED retrofits in every new tender.[1]European Commission, “Directive (EU) 2023/1791 on Energy Efficiency,” europa.eu Municipalities treat lighting as critical infrastructure: Paris signed a EUR 700 million contract in 2025 to replace 70,000 luminaires with connected LED systems that promise 240 GWh in savings over 10 years. Similar performance-based concessions in Mulhouse and Reading involve installing remote-management nodes that require high-efficiency packages and traceable component bills. These regulatory mandates sustain baseline volumes even as unit prices fall, because every non-compliant lamp removed drives direct package demand. Suppliers with LM-80 files and reparability documentation meet tender prerequisites more easily, translating compliance expertise into higher bid-win ratios.

Declining LED Package Costs Due to Economies Of Scale

Asian wafer fabs running 150 mm and 200 mm lines have lowered mid-power SMD prices by 8-12% annually since 2023, enabling European retrofit projects to achieve 2-year paybacks at electricity tariffs above EUR 0.15/kWh. Lumileds answered with its LUXEON Altilon SMD-A, a pick-and-place-optimized package that reduces the assembly cycle time by 18% while maintaining 0.2 V forward-voltage consistency across bins, helping OEMs squeeze costs without sacrificing reliability.[2]Lumileds, “LUXEON Altilon SMD-A Product Brochure,” lumileds.com Lower landed costs accelerate adoption in troffers and panel lights, expanding the addressable volume for package vendors even as gross margins compress. The price curve also widens the performance gap between commodity mid-power and premium chip-scale or flip-chip options, allowing suppliers to segment portfolios and defend margin in high-power niches. Consequently, economies of scale both democratize basic lighting and finance R&D for specialty architectures.

Accelerated Adoption of Automotive Adaptive Headlamps

UN ECE Regulation 123 authorizes glare-free high beams, prompting European OEMs to integrate micro-LED arrays with more than 1,000 pixels per headlamp and to require packages that sustain 150 °C junction temperatures. Nichia’s µPLS Mini, unveiled at ISAL 2025, embeds more than 3,000 addressable pixels and an Infineon driver ASIC that halves idle power in urban driving, illustrating how wafer-level phosphor and flip-chip techniques converge inside a single module.[3]Nichia Corporation, “µPLS Mini Technical Datasheet,” nichia.com Audi’s 2025 Q3 launch validated this architecture in series production, prompting Hella and Marelli to accelerate similar programs. Adaptive headlamps command premium pricing, so package vendors offset general-lighting margin squeeze by capturing value in each vehicle sold. Germany hosts most Tier-1 qualification labs, keeping procurement local and reinforcing regional demand resilience.

EU RoHS Phase-Out of Mercury-Based Backlights

RoHS Annex III exemptions for mercury in cold-cathode fluorescent lamps began expiring in 2024, forcing automotive and industrial display makers to adopt LED edge-lit and direct-lit architectures. Osram’s OSLON Compact RM, released in 2025, delivers 28 lm at 65 mA in a 2.0 × 1.25 mm footprint with ±2-step MacAdam binning, enabling local dimming zones that raise contrast by up to 40% in cockpit clusters. Display integrators now insist on electrostatic-discharge protection and automotive AEC-Q102 approval, creating high-entry hurdles for low-cost rivals. The sunset of mercury lamps also triggers a secondary replacement wave in legacy retail signage, widening the total addressable market for mid-power and mini-LED packages. Compliance deadlines, therefore, convert regulatory risk into a steady stream of retrofit orders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commoditization-Driven Price Pressure | -0.6% | EU-wide, most acute in general lighting and mid-power SMD segments | Short term (≤ 2 years) |

| Supply Chain Volatility for Rare-Earth Phosphors | -0.4% | Global, affecting all white LED packages; EU lacks domestic refining capacity | Medium term (2-4 years) |

| EU Ecodesign Reparability Rules Limiting CSP Uptake | -0.3% | EU-wide, concentrated in general lighting and low-cost luminaire segments | Medium term (2-4 years) |

| Extended Replacement Cycles in Mature LED Installations | -0.2% | EU-wide, particularly in early-adopter markets (Germany, UK, Scandinavia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commoditization-Driven Price Pressure

Second-tier Asian manufacturers offer sub-USD 0.50 mid-power packages, prompting European luminaire OEMs to dual-source and negotiate bulk discounts that erode supplier loyalty. In retrofit bulbs and tubes, buyers judge LEDs as interchangeable, so even established brands must shave margins to keep per-lumen costs competitive. Some mid-tier European assemblers have exited commodity bins, reallocating R&D toward automotive or horticultural segments where technical barriers curb direct price fights. The squeeze is most acute in public tenders that award on the lowest bid, leaving little room for premium positioning unless lifetime or warranty clauses carry measurable penalties. Persistent price deflation, therefore, drags on overall revenue growth despite steady unit shipments.

Supply Chain Volatility for Rare-Earth Phosphors

China imposed 2025 export quotas on europium and yttrium oxides, elevating phosphor costs for European packagers by up to 18% and reducing the color-rendering index from 90+ to 80-85 when blends are reformulated. Osram’s Premstätten expansion includes in-house phosphor synthesis and a pilot recycling line designed to cut external dependency, but industrywide recycling remains uneconomic without policy incentives. Many vendors now hold six-month inventories, tying up working capital and complicating just-in-time production models. Lower europium content hampers premium retail and medical lighting that demands high color fidelity, potentially ceding market share to RGB or dual-blue architectures. Until alternative phosphor sources or recycling reaches scale, raw-material volatility will linger as a headwind on margins and design flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Package Architecture: Compact Formats Advance in Premium Lighting

Surface-mount device packages captured 58.38% of the Europe White LED Package market share in 2025, retaining leadership because their plastic housing, proven pick-and-place compatibility, and field-serviceable design align with the European Union’s reparability rules. Municipal street-lighting concessions and commercial ceiling-panel retrofits continue to specify SMD formats, providing assemblers with predictable volumes and helping luminaire makers keep warranty claims below contract thresholds. Mid-cycle product updates, such as automated optical inspection markers and tighter binning tolerances, improve quality without disrupting established production flows. The broad installed base also underpins secondary demand for spare parts, keeping SMD revenues resilient even as unit prices decline each year.

Chip-scale packages are on a faster growth curve, advancing at a 3.88% CAGR through 2031 as automotive adaptive headlamps and micro-LED backplanes favor sub-0.5 millimeter profiles and high thermal conductivity. Eliminating the molded housing drops thermal resistance by roughly 20%, enabling tighter pixel spacing and higher drive currents without lumen sag. European Tier-1 suppliers integrate wafer-level phosphor, driver ASICs, and aluminum nitride substrates, turning the compact form factor into a single-sourced module with defensible pricing. Flip-chip and chip-on-board formats fill adjacent niches—flip-chip in high-current daytime running lamps, chip-on-board in industrial high-bays—highlighting how architecture choice now tracks end-use performance targets rather than one-size-fits-all cost metrics.

By Power Class: High-Power Devices Lead Premium Performance

Mid-power LEDs accounted for a sizeable share of the Europe White LED Package market, with 42.73% in 2025, as linear tubes, troffers, and retrofit bulbs still dominate volume. Typical drive currents of 150-350 mA keep junction temperatures below 100 °C, so aluminum-clad boards and simple plastic optics remain adequate, supporting the sub-USD 0.50 price points demanded by public tenders. Assembly lines already calibrated for these devices achieve high throughput, enabling manufacturers to offset steady year-on-year price erosion with incremental productivity gains. As energy tariffs rise, facility managers keep specifying mid-power retrofits because two-year paybacks remain achievable even after incentive programs taper.

High-power packages above 1 W are the growth engine, expanding at a 3.95% CAGR to 2031 as adaptive headlamps, industrial high-bays, and sports-arena floodlights need lumen densities topping 19,500 lumens per fixture. These parts run at junction temperatures near 150 °C, so copper-core boards, low-thermal-resistance die attach, and ceramic lenses become mandatory. Flip-chip and CSP constructions dominate the class, spreading current uniformly and eliminating wire-bond shading that can distort sophisticated beam patterns. Automotive customers also demand AEC-Q102 qualification cycles that screen out early-life failures, giving established suppliers with in-house reliability labs an edge over low-cost rivals. The higher bill-of-materials cost is absorbed by premium vehicle trims and energy-service contracts that monetize long-lumen maintenance.

By Application: Automotive Lighting Surges While General Lighting Holds Scale

General lighting accounted for 41.23% of 2025 revenue, driven by ongoing municipal streetlight concessions that bundle luminaires, remote management nodes, and long-term maintenance guarantees. Multiyear contracts in cities such as Paris, Mulhouse, and Reading lock in thousands of fixture call-offs per quarter, smoothing production planning for LED package vendors. Because these projects prioritize lumen-per-watt and reparability, SMD mid-power devices remain the reference specification, and pricing competitions center on per-lumen cost rather than exotic features. Energy-savings performance clauses reinforce consistent demand because replacement cycles have now moved from pilot deployments to full network rollouts.

Automotive lighting is growing faster at a 3.72% CAGR through 2031, fueled by European original-equipment makers integrating matrix arrays that support glare-free high-beam and dynamic welcome animations. Pixel counts exceed 1,000 per headlamp, so package suppliers that combine high-power dies with on-board driver ICs capture the design wins. The performance premium shields pricing: one micro-LED headlamp set can embed more semiconductor content than an entire interior lamp suite. Beyond passenger cars, heavy-duty trucks and two-wheelers are increasingly adopting adaptive beams to meet evolving safety rules, widening the addressable market. Display backlighting and horticultural lighting add smaller but higher-margin pockets, proving that differentiated spectral output or binning precision can carve profitable niches even within a maturing industry.

Geography Analysis

Germany accounted for 27.64% of the Europe White LED Package market share in 2025, reflecting the concentration of Tier-1 lighting suppliers and automotive OEM design centers. Local production of high-power chip-scale and flip-chip devices supports adaptive headlamp programs at Audi, BMW, and Mercedes, which in turn stabilizes quarterly call-offs for premium packages. Municipal retrofit activity adds a second demand layer as cities such as Rutesheim and Stuttgart replace sodium streetlights with connected LED systems, guaranteeing baseline volume even when vehicle output cycles soften. Contract specifications in these tenders favor surface-mount mid-power formats that allow field repairs and comply with Ecodesign rules, so German assemblers maintain balanced product portfolios that cover both automotive and general lighting channels.

France is poised for the quickest advance, expanding at a 3.78% CAGR through 2031 on the back of ambitious carbon-reduction targets set under the Loi Climat et Résilience. Paris closed a EUR 700 million public lighting concession in 2025, and Mulhouse began a 14,000-luminaire overhaul in early 2026, creating multiyear procurement pipelines for mid-power and high-power packages. Regional cities, including Le Puy-en-Velay and Vienne, have replicated this model, demonstrating that digital remote-management clauses and presence-detection sensors are now baseline requirements. These contracts bundle luminaires, drivers, and telematics, channeling a larger share of project value toward integrated modules rather than discrete LEDs. Suppliers that can certify remote-monitoring interfaces under EU cybersecurity guidelines gain additional leverage when bidding for follow-up maintenance services.

The United Kingdom, the Netherlands, Belgium, and Scandinavia deliver steady, incremental demand, driven by council-funded streetlight conversions and early vertical-farming trials. West Sussex, Reading, and Slough collectively committed more than GBP 40 million to LED upgrades between 2025 and 2026, filling order books for commodity mid-power devices. Dutch horticulture clusters purchase high-efficacy white packages with far-red enhancement, while Nordic logistics operators retrofit high-bay fixtures that require lumen outputs above 19,500 lumens. Rest-of-Europe customers remain fragmented, yet their procurement often references German and French technical standards, which indirectly harmonize product specifications across the region. As a result, suppliers that certify once for the stringent markets can cost-effectively serve the broader bloc, lifting utilization rates without major redesigns.

Competitive Landscape

The competitive field shows moderate concentration, with Signify, Osram Opto Semiconductors, Lumileds, Nichia, and Samsung jointly controlling about 55-60% of revenue, while dozens of Asian foundries contest the remainder on price. Signify focuses on application-specific growth, supplying horticultural modules to Planet Farms in Italy, where photosynthetic photon efficacy and spectrum tuning justify premium margins. Osram is investing EUR 567 million in Premstätten production to add micro-LED and mini-LED capacity and an on-site phosphor recycling line, a hedge against rare-earth volatility and a bid to secure long-term contracts with European automotive OEMs. Nichia opened its Automotive Innovation Center in Aachen to provide rapid prototyping and qualification support, thereby strengthening ties with Tier-1 headlamp suppliers and accelerating design-in cycles for pixelated light sources.

Lumileds targets general lighting commoditization with the LUXEON Altilon SMD-A series, an automation-ready package that reduces pick-and-place time by 18% and helps luminaire makers defend margins in price-sensitive bids. Samsung leverages back-end scale in Korea to press mid-power prices below USD 0.50 while still meeting LM-80 and TM-21 lifetime claims, positioning the brand as a low-risk alternative to lesser-known Asian vendors. Danish start-up LED iBond prototypes chip-on-board modules with embedded thermal sensors for greenhouse retrofits, showing how specialized features can carve defensible footholds even for small entrants. Competitive pressure has driven many European mid-tier assemblers to exit commodity bins and instead bundle LEDs with drivers, optics, and control boards, lifting average selling prices per luminaire and reducing exposure to single-component price swings.

Certification regimes shape market entry dynamics. Automotive customers mandate AEC-Q102 stress tests, municipal projects insist on ENEC safety marks, and commercial buyers increasingly request Environmental Product Declarations. Vendors with in-house labs shortcut approval timelines and lock in preferred supplier status, reinforcing scale advantages. Intellectual property around wafer-level phosphor deposition and integrated driver ASICs further raises barriers, because infringement risks deter price-only challengers from cloning advanced architectures. The net effect is a stable top tier that continues to expand through specialization, while cost competition intensifies in the long tail of general lighting, where functionality is largely standardized.

Europe White LED Package Industry Leaders

Osram Opto Semiconductors GmbH

Lumileds Holding B.V.

Nichia Europe B.V.

Samsung Electronics Co., Ltd.

Seoul Semiconductor Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Nichia hosted an Innovation Gallery in Frankfurt during Light + Building week, highlighting cross-technology integration across automotive, medical, horticultural, and laser portfolios.

- March 2026: Mulhouse, France, commenced a EUR 24 million (USD 26 million) 15-year contract to replace 14,000 luminaires with LED fixtures, achieving a first-year public-lighting energy reduction of 75%.

- February 2026: Cree LED launched the OptiLamp module series with integrated driver and thermal management, compliant with Ecodesign reparability rules for commercial retrofits.

- December 2025: Le Puy-en-Velay, France, approved a six-year plan to finalize its municipal LED transition after halving annual lighting spend during the initial contract term.

Europe White LED Package Market Report Scope

The Europe White LED Package Market Report is Segmented by Package Architecture (SMD (Surface Mount Device), COB (Chip-on-Board), CSP (Chip Scale Package), Flip-Chip LED Packages), Power Class (Low Power (Below 0.5 W), Mid Power (0.5-1 W), High Power (Above 1 W)), Application (General Lighting, Automotive Lighting, Display and Backlighting, Specialty/Niche), and Country (United Kingdom, Germany, France, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| SMD (Surface Mount Device) |

| COB (Chip-on-Board) |

| CSP (Chip Scale Package) |

| Flip-Chip LED Packages |

| Low Power (Below 0.5 W) |

| Mid Power (0.5-1 W) |

| High Power (Above 1 W) |

| General Lighting |

| Automotive Lighting |

| Display AND Backlighting |

| Specialty / Niche |

| United Kingdom |

| Germany |

| France |

| Rest of Europe |

| By Package Architecture | SMD (Surface Mount Device) |

| COB (Chip-on-Board) | |

| CSP (Chip Scale Package) | |

| Flip-Chip LED Packages | |

| By Power Class | Low Power (Below 0.5 W) |

| Mid Power (0.5-1 W) | |

| High Power (Above 1 W) | |

| By Application | General Lighting |

| Automotive Lighting | |

| Display AND Backlighting | |

| Specialty / Niche | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe White LED Package market by 2031?

The market is forecast to reach USD 1.88 billion by 2031.

Which package architecture holds the largest share today?

Surface-mount device packages led with 58.38% share in 2025.

Which application is growing the fastest to 2031?

Automotive lighting is advancing at a 3.72% CAGR through 2031.

Why are high-power packages gaining traction?

Adaptive automotive headlamps and industrial high-bay retrofits demand lumen density above 19,500 lumens per fixture, favoring >1 W devices.

Which EU country is expected to post the quickest growth?

France is projected to expand at a 3.78% CAGR thanks to aggressive municipal streetlight conversions.

How are suppliers addressing rare-earth supply risks?

Leading vendors are stockpiling phosphor inventories and investing in recycling infrastructure to recover europium and yttrium from end-of-life LEDs.

Page last updated on: