Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

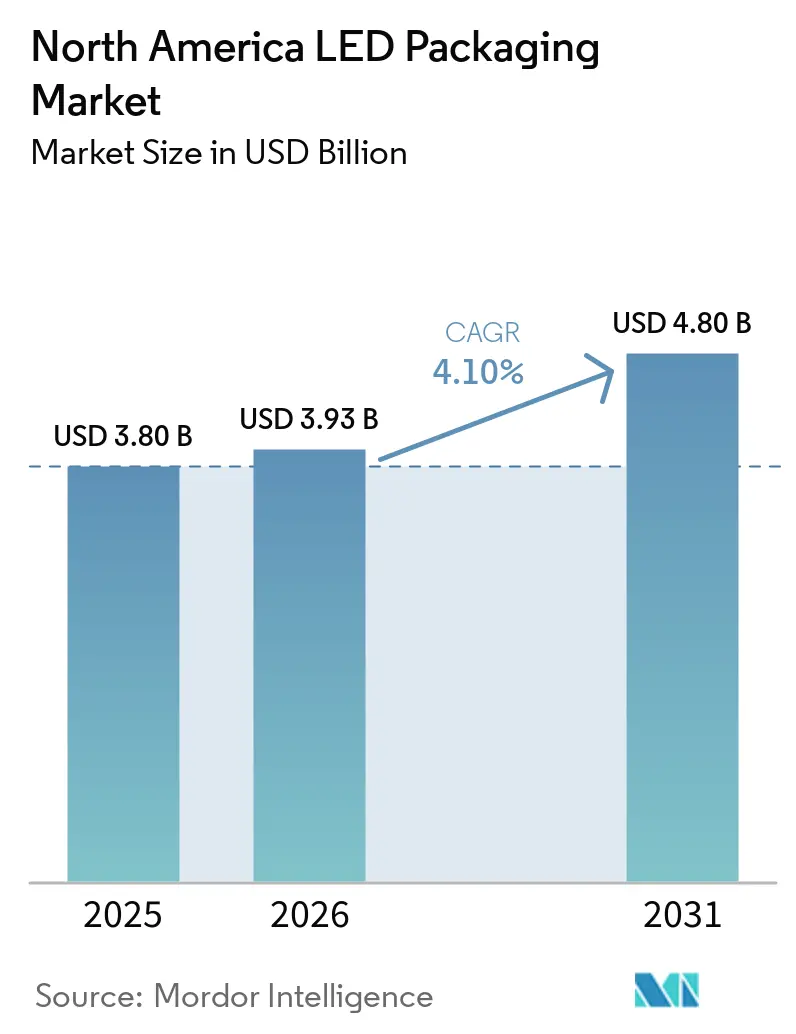

| Base Year Market Size (2025) | USD 3.80 Billion |

| Market Size (2026) | USD 3.93 Billion |

| Market Size (2031) | USD 4.80 Billion |

| Growth Rate (2026 - 2031) | 4.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America LED Packaging Market Analysis by Mordor Intelligence

The North America LED Packaging market size is projected to expand from USD 3.80 billion in 2025 and USD 3.93 billion in 2026 to USD 4.80 billion by 2031, registering a CAGR of 4.10% between 2026 to 2031. Demand is shifting from commoditized surface-mount devices toward higher-value chip-scale, flip-chip, and chip-on-board architectures that command healthier margins. Federal incentives under the CHIPS and Science Act are catalyzing domestic investments in advanced packaging lines, while municipal-level energy-efficiency mandates sustain retrofit activity in general lighting. Automotive headlamp suppliers are adopting matrix-LED modules that rely on robust thermal pathways and pixel-level control, and display manufacturers are ramping mini-LED backlight volumes for televisions and monitors. Persistent rare-earth supply risks and price erosion in standard SMD packages motivate regional producers to climb the value chain rather than compete head-to-head with large Asian contract assemblers.

Key Report Takeaways

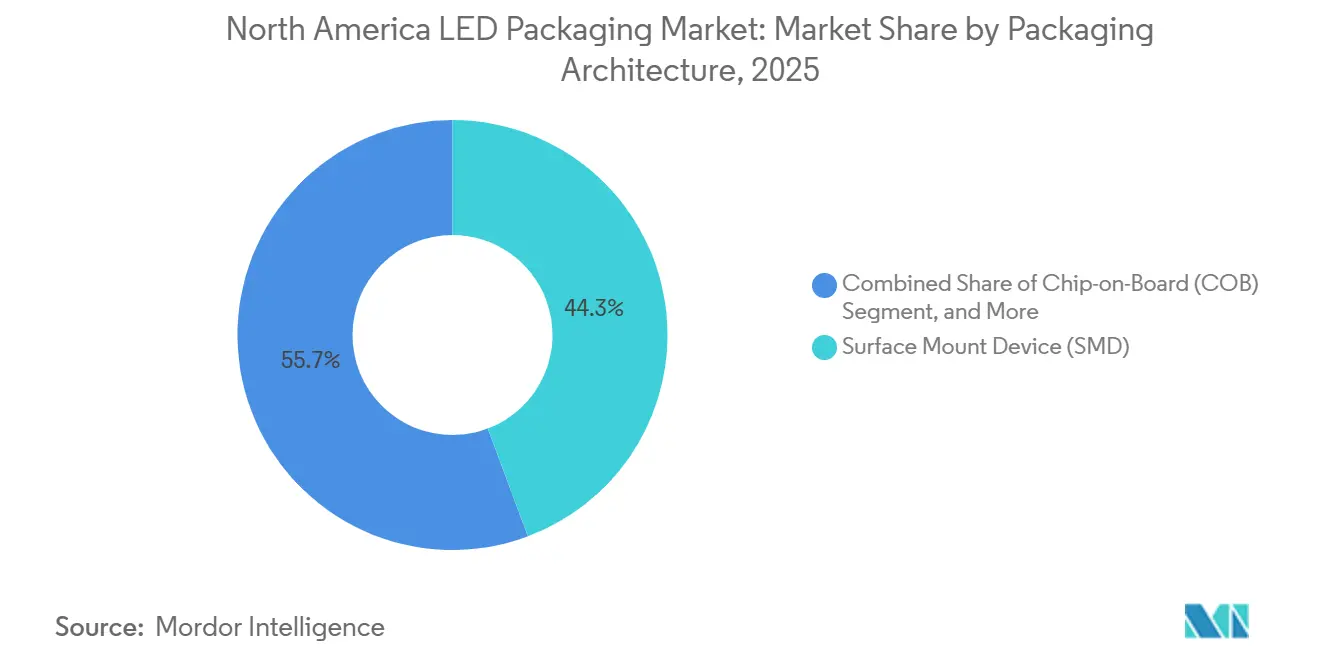

- By packaging architecture, surface-mount devices led with 44.28% of North America LED Packaging market share in 2025, while chip-scale packages are forecast to advance at a 4.68% CAGR through 2031.

- By power class, mid-power packages accounted for 39.18% share of the North America LED Packaging market size in 2025 and high-power packages are projected to grow at a 4.99% CAGR to 2031.

- By emission type, visible-wavelength LEDs dominated with 85.19% of 2025 shipments, whereas ultraviolet packages are set to expand at a 4.78% CAGR during 2026-2031.

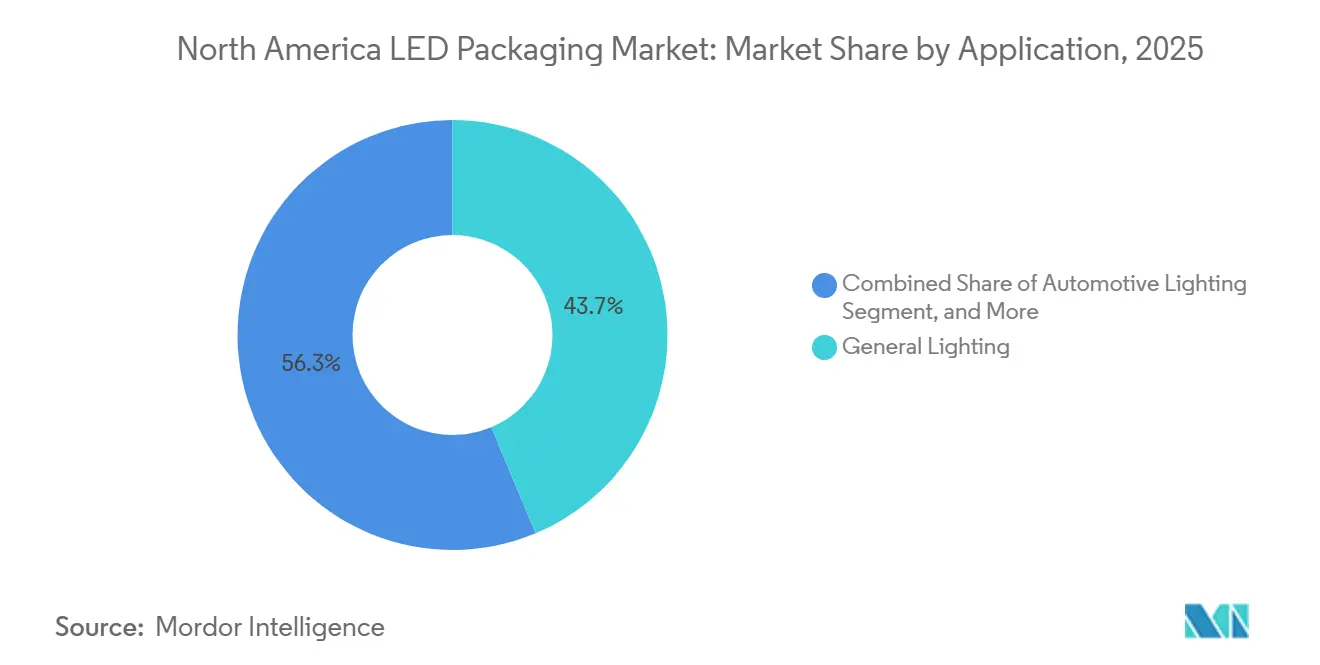

- By application, general lighting retained 43.68% revenue share in 2025, but automotive lighting is the fastest-growing segment at a 5.18% CAGR to 2031.

- By geography, the United States commanded 87.48% of regional revenue in 2025; Canada is expected to post a 5.06% CAGR through 2031 on the back of energy-efficiency mandates and cross-border automotive supply agreements.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America LED Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Mini-LED Backlighting Demand | +1.2% | United States And Canada, Spillover To Mexican Display-Assembly Hubs | Medium Term (2–4 Years) |

| Automotive Headlamp Shift To Matrix LED | +1.5% | United States, Canada, Mexico Automotive Corridors | Long Term (≥ 4 Years) |

| U.S. CHIPS Act Incentives For Domestic LED Supply Chain | +0.9% | United States Funding Zones | Short Term (≤ 2 Years) |

| Rapid Adoption Of CSP In High-Lumen Outdoor Fixtures | +0.8% | Municipal And Commercial Outdoor Retrofits Across North America | Medium Term (2–4 Years) |

| Integration Of UV-C LEDs In HVAC For Pathogen Control | +0.6% | Commercial Real Estate And Healthcare Facilities In United States And Canada | Short Term (≤ 2 Years) |

| Emerging Micro-LED Use In AR/VR Wearables | +0.4% | U.S. Technology Clusters | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Surge In Mini-LED Backlighting Demand

Television and monitor brands unveiled more than 20 million mini-LED backlit units at the January 2026 Consumer Electronics Show, underscoring rapid adoption of dense LED matrices that deliver in-panel local dimming exceeding 10,000 zones per display. Mini-LEDs use dies as small as 100-200 µm placed on pitches below 0.5 mm, so North American packagers are re-tooling with sub-10 µm-accuracy pick-and-place systems capable of high-throughput bonding. Bridgelux reported its CSP2727 family now accounts for roughly 30% of the company’s continental CSP shipments as display integrators migrate to chip-scale designs.[1]Bridgelux Inc., “CSP2727 Series Product Brief,” bridgelux.com Energy Star 9.0 limits, effective January 2025, tightened on-mode power for screens larger than 65 inches, and mini-LED’s ability to dim unused zones by more than 99% helps manufacturers stay compliant without lowering peak brightness. The architectural shift also favors chip-on-board (COB) modules that eliminate lead frames, reduce package height under 1 mm, and improve thermal spreading. As component counts balloon, backend optical calibration emerges as a bottleneck, spurring interest in automated photometric testing stations that can process entire backlight panels in under 60 seconds.

Automotive Headlamp Shift To Matrix LED

Adaptive-driving-beam systems gained U.S. regulatory clearance under FMVSS 108 in 2022, and original equipment manufacturers quickly accelerated matrix headlamp rollouts. Tesla integrated matrix headlights into the 2025 Model Y, and Rivian activated the feature via over-the-air update in August 2024 for its R1T and R1S trucks. ams OSRAM’s EVIYOS 3.0 chip, launched at CES 2026, packs 25,600 individually addressable pixels to create high-resolution light carpets that adapt to traffic and project navigation prompts onto pavement.[2]ams OSRAM, “EVIYOS 3.0 Intelligent Headlight Launch Presentation,” ams-osram.com These modules require flip-chip packages rated for junction temperatures above 125 °C, as well as optical coatings that hold color temperature within ±200 K from −40 °C to +105 °C. ISO 26262 functional-safety rules published in 2024 force redundant die architectures and real-time fault detection, adding up to 20% in bill-of-material cost but ensuring fail-silent behavior. As regulations harmonize across Canada and Mexico, tier-one lighting suppliers are localizing assembly in North America to minimize logistics overhead and currency-exchange exposure.

U.S. CHIPS Act Incentives For Domestic LED Supply Chain

The CHIPS and Science Act assigned USD 52.7 billion to strengthen U.S. semiconductor capacity, including USD 39 billion for manufacturing subsidies that explicitly mention advanced packaging. In December 2025, XLight secured USD 150 million to prototype extreme-ultraviolet lithography tooling with carve-outs for heterogeneous LED modules. Analysts expect domestic advanced-packaging floor space to quadruple by 2030, compressing custom LED module lead times to 6-8 weeks from today’s 12-16 weeks. The 25% investment tax credit that accompanies the law applies to pick-and-place, die-attach, and wire-bond assets, lowering cash payback periods for North American contract packagers that upgrade from legacy SMD lines to CSP and flip-chip capable tooling. A domestic-content clause, climbing from 55% in 2025 to 75% by 2029, is triggering reshoring moves by substrate and phosphor suppliers even though U.S. utility and labor costs remain higher than Asia-Pacific benchmarks.

Rapid Adoption Of CSP In High-Lumen Outdoor Fixtures

Chip-scale packages dispense with bulky plastic housings, bonding the die directly to ceramic or metal-core boards and slashing thermal resistance by up to 40%. Municipal street-light tenders in California and Texas now routinely specify CSP modules so fixture designers can reduce reflector depth 20-25% and cut pole wind-loading. Bridgelux CSPs hit 150-209 lm/W in 2025 lab tests, enabling 10 W/cm² power densities without active cooling. Reflow durability improves because the omission of plastic eliminates delamination risk at 260 °C peak temperatures. IES TM-21-20 projections show silicone-encapsulated CSPs depreciating less than 5% after 50,000 h in accelerated thermal cycling, satisfying L95 targets for high-bay warehouses. As utilities shift maintenance contracts to performance-based models, lower fixture weight and longer lumen maintenance translate directly into life-cycle savings that strengthen the CSP value proposition.

Restraints Impact Analysis*

| Restraint | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Erosion Pressuring Gross Margins | -1.1% | United States Commodity SMD Lines | Short Term (≤ 2 Years) |

| Thermal-Management Challenges Beyond 3 W Packages | -0.7% | Automotive And Industrial High-Power Applications Across United States And Canada | Medium Term (2–4 Years) |

| Dependence On Asia-Pacific Contract Packaging | -0.5% | Mid-Power And Low-Cost SMD Supply Chains | Long Term (≥ 4 Years) |

| Supply Risk Of Rare-Earth Phosphors | -0.9% | United States And Canada Phosphor Fabrication | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Price Erosion Pressuring Gross Margins

Average selling prices for commodity mid-power SMD LEDs fell 8-12% year-over-year in 2025 as Asian contract assemblers ran at utilization rates above 90% and flooded the market with excess output. North American players saw gross margins compress by 200-300 basis points, forcing manufacturing consolidation and accelerated depreciation of legacy pick-and-place assets. Migrating to CSP and flip-chip designs partially offsets the squeeze because lead-frame and plastic encapsulation costs disappear, but new die-attach tools priced at USD 2-3 million each are beyond reach for many regional specialists. Industry chatter suggests a new wave of mergers and asset sales is likely over the next 18 months, especially among firms lacking proprietary phosphors or optical coatings that can defend premium ASPs.

Thermal-Management Challenges Beyond 3 W Packages

Packages running above 3 W generate junction temperatures that can top 150 °C, and phosphor conversion drops nearly 1% for every 3 °C rise according to IEEE-published data.[3]IEEE, “Thermal Degradation of Phosphor-Converted White LEDs,” ieee.org Conventional silicone pads conduct only 3-5 W/m-K, inadequate for ultra-high-power modules needing more than 10 W/m-K pathways to stay below 105 °C. Chip-on-board arrays bonded to copper cores help, but void-free die attach across 50-plus die grids requires vacuum reflow ovens and X-ray inspection that lift manufacturing cost 25-30%. The U.S. Department of Energy is funding research into phase-change materials and vapor-chamber spreaders thin enough to fit inside sub-2 mm packages, yet commercial adoption remains two to three years away. Until next-generation thermal solutions scale, designers must throttle drive currents or accept shorter L70 lifetimes, both of which constrain adoption in mission-critical industrial and automotive settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Architecture: CSP Gains On SMD Incumbency

Surface-mount devices held 44.28% of 2025 revenue because they drop seamlessly into the vast installed base of pick-and-place assembly lines, yet chip-scale packages are forecast to outpace all rivals at a 4.68% CAGR through 2031. The North America LED Packaging market size for CSPs benefits from a 30-40% lower thermal resistance that lets outdoor fixture makers push drive currents without resorting to active cooling. In practice, streetscape engineers in Los Angeles and Toronto report fixture weight declines of up to 15% after switching to CSP boards that shrink reflector depth. Wire-bond-free flip-chip formats are also ascending in automotive headlamps where designers need 1,000 cd/mm² intensity and microsecond dimming. Meanwhile, legacy dual-in-line and through-hole packages have retreated to fewer than 3% of shipments as automated surface-mount lines become universal.

Second-generation CSPs further integrate transient-voltage suppression diodes and on-package thermistors, giving OEMs real-time health data for predictive maintenance. This functionality supports the trend toward lighting-as-a-service contracts in which fixture vendors guarantee lumen output over multi-year periods. Flip-chip makers are layering optical waveguides atop solder bumps to simplify assembly of adaptive-driving-beam pixels, a feature essential for automakers chasing top safety ratings. Chip-on-board suppliers, meanwhile, continue to dominate horticultural and stadium lighting thanks to their ability to spread 100 W across aluminum substrates without hotspot formation, though vapor-chamber hybrids are beginning to nibble at that niche.

By Power Class: High-Power Packages Driven By Automotive Demand

Mid-power LEDs between 0.5 W and 1 W controlled 39.18% of 2025 revenue as they remain the cheapest path to meet Energy Star lumen-per-dollar targets in retrofit bulbs and troffers. The high-power 1-3 W class is projected to chart a 4.99% CAGR, fueled by matrix headlamp arrays that need tightly binned, high-flux dies. The North America LED Packaging market share for high-power devices is set to climb as electric-vehicle platforms allocate larger electrical budgets to lighting than their internal-combustion predecessors. Low-power indicator parts hang on in wearables and dashboard icons where battery life trumps intensity, whereas ultra-high-power packages above 3 W are entering stadium floodlights and horticulture grow racks.

Thermal budgets separate winners from laggards. High-power dies demand vapor-chamber substrates or sintered copper bases to maintain junctions below 110 °C, yet those materials add 20-30% to BOM. Vendors that cannot solve heat extraction risk warranty claims when real-world duty cycles push modules past L70 in under 30,000 h. Tier-ones increasingly mandate thermal-impedance reports during sourcing, a shift that disadvantages commoditized mid-power lines but enhances the stickiness of specialized high-power suppliers.

By Emission Type: UV Packages Outpace Visible LEDs

Visible-light devices retained 85.19% of 2025 shipments across white, RGB, and amber bins, yet ultraviolet LEDs are slated for a 4.78% CAGR as HVAC integrators add UV-C arrays for pathogen reduction. Crystal IS launched Klaran emitters at 260-270 nm, and more than 50,000 modules entered U.S. and Canadian commercial buildings in 2025. Hospital trials show 99.9% viral inactivation when air flows past duct-mounted UV-C channels at 500 ft/min. Infrared packages serve driver-monitoring cameras and biometric sensors; ams OSRAM’s SFH 4735 delivers 1,200 mW/sr at 100 mA, enabling long-range time-of-flight modules. IEC 62471 classifies UV-C parts as Risk Group 2/3, and uneven enforcement across borders complicates commercialization, pushing suppliers to include interlock circuits and warning labels.

Interest in near-ultraviolet LEDs for water disinfection is also climbing because mercury lamps are headed for a 2027 global phase-out under the Minamata Convention. That dynamic accelerates demand for high-output 280-nm dies, though external quantum efficiency remains below 10%, so system designers often stack dozens of chips in parallel. Visible-light suppliers continue to chase broader color gamuts, using red KSF phosphors and quantum-dot films to stretch Rec. 2020 coverage in mini-LED backlights. As displays shift toward 10-bit color depth, the premium for tight wavelength bins widens, supporting healthy ASPs for top-tier visible emitters.

By Material Chemistry: Phosphor Revenue Leads Growth Despite Supply Risk

Substrates such as sapphire and silicon carbide took 34.79% of 2025 chemistry revenue, reflecting the cost of high-temperature epitaxy. Phosphors and coatings are heading for a 4.91% CAGR on the back of high-CRI retail lights and wide-gamut displays. China’s October 2025 expansion of rare-earth export controls, however, slashed U.S. yttrium imports by 95% within months. Spot prices for europium oxide jumped by triple digits, adding 5-10 cents per lumen to warm-white LEDs that rely on red phosphors. Some North American packagers switched sourcing to Australian miners, paying 30% premia but gaining compliance with domestic-content rules. Encapsulation is migrating from epoxy to silicone for better thermal stability above 150 °C, while die-attach teams increasingly specify silver sinter pastes that hit 150 W/m-K conductivity.

To hedge supply risk, Nichia unveiled mercury-free yttrium-aluminum-garnet phosphors that meet 90+ CRI without cadmium or lead, aligning with pending RoHS revisions. Quantum-dot film producers are prototyping cadmium-free indium-phosphide resins compatible with LED reflow profiles, a shift that could temper reliance on rare-earth reds. On substrates, 6-inch silicon carbide wafers are gaining favor for their low lattice mismatch and higher thermal conductivity, though tool sets remain expensive relative to sapphire.

By Application: Automotive Lighting Outpaces General Illumination

General illumination captured 43.68% of 2025 revenue across bulbs, troffers, and outdoor area lights, but automotive lighting is projected to clock a 5.18% CAGR as matrix, signature, and projection functions proliferate. Tesla and Rivian both rely on high-power flip-chips above 125 °C junction ratings, and premium German automakers are field-testing pixel counts above 30,000 per lamp for on-road guidance graphics. Display backlighting is migrating from edge-lit to direct-lit mini-LEDs with 10,000-plus dimming zones, a change that multiplies packaged-LED counts per panel by an order of magnitude. Consumer electronics retain a stable base of indicator and camera-flash LEDs, yet smartwatches and ear-wear are adopting infrared emitters for health metrics.

Industrial and horticultural niches remain attractive to packagers that can supply COB arrays with tuned spectra. Vertical farm trials in New York demonstrate 20-30% yield gains when far-red is blended with 660 nm red and 450 nm blue, a recipe only practical with high-density COB modules. UV curing in 3D-printing resins also drives incremental demand for 395 nm packages capable of 5-W/cm² irradiance without lens browning. Collectively these specialty applications lift average selling price and insulate suppliers from commodity price pressure.

Geography Analysis

North America remains the epicenter of advanced LED packaging in the Western Hemisphere. The United States generated 87.48% of regional revenue in 2025 owing to its vast installed lighting base, robust auto production, and concentration of display integrators. The North America LED Packaging market size in Canada is smaller but is expected to grow 5.06% CAGR through 2031 as Ottawa phases out inefficient lamps and Ontario’s auto plants localize LED headlamp assembly. Mexico’s tier-one suppliers feed U.S. final-assembly lines under the USMCA framework, leveraging proximity to Detroit and Tennessee EV hubs. Policy forces remain decisive: Washington’s CHIPS funding pushes substrate and phosphor plants to relocate stateside, while Canada’s Strategic Innovation Fund co-financed CAD 85 million (USD 63 million) for a gallium-nitride epi line in Montréal slated to pilot in late 2026

Canada’s market, though a fraction of U.S. scale, is expanding above the regional average. Provincial codes that outlaw incandescent and most halogen lamps after 2026 are driving LED adoption, while Québec and Ontario auto plants anchor demand for high-power flip-chip modules. Ottawa’s Strategic Innovation Fund co-investments in gallium-nitride epitaxy and UV-C disinfection research further stimulate local sourcing. Cross-border integration with U.S. tier-ones compresses lead times and aligns safety certification requirements, enabling Canadian packagers to compete for vehicle launch programs.

Mexico operates as a strategic manufacturing corridor. Its light-vehicle output exceeded 3.5 million units in 2025, and roof-line headlamp modules assembled in Chihuahua and Coahuila already meet FMVSS 108 photometrics for direct export to U.S. dealerships. The country’s cost advantage in manual assembly supports legacy SMD lines, but rising demand for CSP and flip-chip architectures is pushing EMS houses to invest in higher-precision die-attach equipment. Government policy is increasingly tied to USMCA content thresholds, nudging suppliers toward North American sourcing for phosphor powders and sapphire wafers.

Competitive Landscape

Market concentration is moderate, with the top five suppliers, Nichia, Cree LED, Samsung Electronics, ams OSRAM, and Lumileds, capturing roughly 55-60% of 2025 sales. Each is pivoting toward vertical integration to control substrates, phosphors, and driver ICs. San’an Optoelectronics’ USD 239 million acquisition of Lumileds in August 2025 extended San’an’s reach into North American auto and general lighting channels and buttressed its patent portfolio in phosphor-converted white LEDs.

Differentiation increasingly hinges on embedded intelligence. Cree LED’s February 2026 launch of OptiLamp modules adds on-die temperature, current, and luminance sensors that feed predictive-maintenance algorithms, delivering 10-15% energy savings in pilot warehouse deployments. OSRAM’s EVIYOS 3.0 pushes pixel density to 25,600 on one die, opening doors to road-projection graphics and advanced driver-assistance integration. Nichia’s mercury-free phosphor project positions the firm for upcoming global mercury bans while sustaining CRI above 90.

Start-ups expand niche frontiers. Rohinni’s printed micro-LED process hits 10,000 die placements per hour on flexible substrates, a capability that lures automotive interior and AR headset designers. Crystal IS maintains a stranglehold on aluminum-nitride UV-C dies that outperform sapphire competitors for disinfection tasks. Meanwhile, Taiwanese mid-tier players like Epistar and Everlight strategically license patents to avoid North American litigation, choosing to focus on cost-optimized commodity and signage SKUs.

Price competition remains fiercest in mid-power SMD categories, where Asian contractors undercut regional packagers by 15-20% on BOM. To escape the squeeze, North American firms concentrate on high-power, high-complexity modules that require proprietary thermal interfaces and tight optical tolerances unattractive to mass producers. Intellectual-property audits during sourcing show a rising premium on phosphor chemistry know-how and pixel-level current-steering circuits, assets that smaller assemblers often lack.

North America LED Packaging Industry Leaders

Nichia Corporation

Cree LED, Inc.

Samsung Electronics Co., Ltd.

ams-OSRAM AG

Lumileds Holding B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Cree LED introduced OptiLamp intelligent modules with embedded sensors for real-time lumen maintenance, achieving 10-15% energy savings in initial warehouse trials.

- January 2026: ams OSRAM unveiled EVIYOS 3.0, a 25,600-pixel flip-chip headlight die, and signed supply deals with two North American automakers for 2026 SOP.

- January 2026: JBD announced the Hummingbird II micro-LED projector exceeding 2 million nits for AR glasses, slated for H1 2026 commercial release.

- December 2025: The U.S. Department of Commerce awarded XLight USD 150 million in CHIPS funding to develop EUV tools and heterogeneous LED packaging research.

North America LED Packaging Market Report Scope

The North America LED Packaging Market Report is Segmented by Packaging Architecture (SMD, COB, CSP, Flip-Chip, DIP, Others), Power Class (Low, Mid, High, Ultra-High), Emission Type (Visible, Infrared, Ultraviolet), Material Chemistry (Substrates, Encapsulation, Bonding, Phosphors), Application (General Lighting, Automotive, Display, Consumer Electronics, Industrial), and Geography (United States, Canada, Mexico). Market Forecasts are Provided in Terms of Value (USD).

By Packaging Architecture

| Surface Mount Device (SMD) |

| Chip-on-Board (COB) |

| Chip Scale Package (CSP) |

| Flip-Chip LED Packages |

| Dual In-line Package (DIP / Through-hole) |

| Others, Packaging Architecture |

By Power Class

| Low Power (Less Than 0.5 W) |

| Mid Power (0.5 to 1 W) |

| High Power (1 to 3 W) |

| Ultra-High Power (More Than 3 W) |

By Emission Type

| Visible LED Packages |

| Infrared LED Packages |

| Ultraviolet LED Packages |

By Material Chemistry

| Substrates |

| Encapsulation |

| Bonding / Die-Attach |

| Phosphors / Coatings |

By Application

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Consumer Electronics |

| Industrial and Specialty |

By Country

| United States |

| Canada |

| Mexico |

| By Packaging Architecture | Surface Mount Device (SMD) |

| Chip-on-Board (COB) | |

| Chip Scale Package (CSP) | |

| Flip-Chip LED Packages | |

| Dual In-line Package (DIP / Through-hole) | |

| Others, Packaging Architecture | |

| By Power Class | Low Power (Less Than 0.5 W) |

| Mid Power (0.5 to 1 W) | |

| High Power (1 to 3 W) | |

| Ultra-High Power (More Than 3 W) | |

| By Emission Type | Visible LED Packages |

| Infrared LED Packages | |

| Ultraviolet LED Packages | |

| By Material Chemistry | Substrates |

| Encapsulation | |

| Bonding / Die-Attach | |

| Phosphors / Coatings | |

| By Application | General Lighting |

| Automotive Lighting | |

| Display and Backlighting | |

| Consumer Electronics | |

| Industrial and Specialty | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What Is The Current Value Of The North America LED Packaging Market And Its Forecast Growth Rate?

It Was Valued At USD 3.93 Billion In 2026 And Is Projected To Reach USD 4.80 Billion By 2031, Growing At A 4.10% CAGR.

Which Packaging Architecture Is Growing Fastest?

Chip-Scale Packages Are Forecast To Expand At 4.68% CAGR Through 2031 As Fixture Makers Exploit Their Compact Thermal Profile.

Why Are Automotive Manufacturers Driving Demand For High-Power LED Packages?

Adaptive-Beam Headlamps And Matrix Headlights Require Tightly Binned, High-Flux Dies Capable Of Pixel-Level Control, Pushing The 1–3 W Class Higher.

How Do CHIPS Act Incentives Affect Regional LED Supply Chains?

The Law Offers Subsidies And Tax Credits That Shorten Lead Times, Spur Capital Upgrades, And Encourage Phosphor And Substrate Reshoring To The United States.

What Supply Risks Surround Phosphor Materials?

China’s Rare-Earth Export Controls Reduced U.S. Yttrium Imports By 95%, Forcing Packagers To Secure Costlier Supplies From Other Countries And Accelerating Research Into Alternative Phosphors.

Page last updated on: