United States LED Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

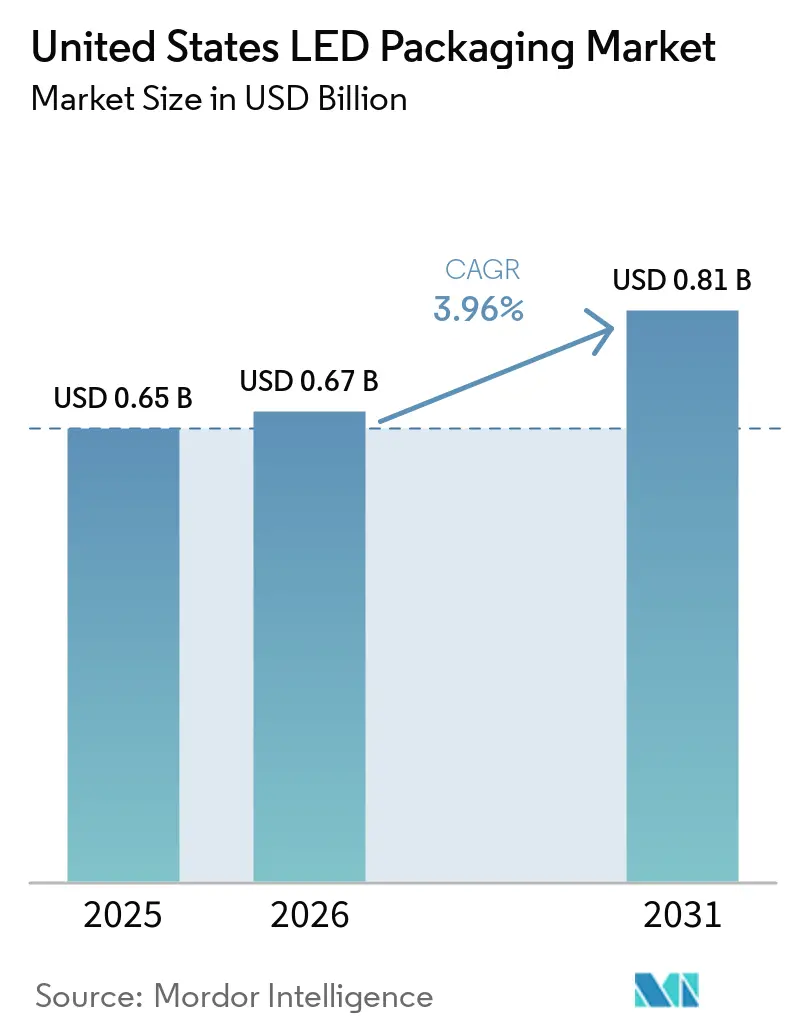

| Base Year Market Size (2025) | USD 0.65 Billion |

| Market Size (2026) | USD 0.67 Billion |

| Market Size (2031) | USD 0.81 Billion |

| Growth Rate (2026 - 2031) | 3.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States LED Packaging Market Analysis by Mordor Intelligence

The United States LED packaging market size was valued at USD 0.65 billion in 2025 and estimated to grow from USD 0.67 billion in 2026 to reach USD 0.81 billion by 2031, at a CAGR of 3.96% during the forecast period 2026-2031. A mature domestic supply base, higher lamp-efficacy mandates, and application-specific innovations are sustaining demand even as unit volumes plateau. Continued tightening of U.S. energy-efficiency rules is shifting product design toward higher-power packages that deliver more lumens per component while maintaining color quality and thermal reliability. Automotive OEMs are accelerating the move to pixelated headlights, driver-monitoring modules, and short-range LiDAR, which favor compact chip scale packages and ceramic substrates. Horticulture lighting growth in vertical farms and greenhouses is spurring interest in tunable spectra and UV-enhanced modules, reinforcing investment in rare-earth phosphors and advanced encapsulants. At the same time, on-shoring incentives under the CHIPS for America program are encouraging pilot-line construction for fan-out wafer-level processing and glass-core substrates, positioning U.S. manufacturers to reduce import dependence for critical materials and tooling.

Key Report Takeaways

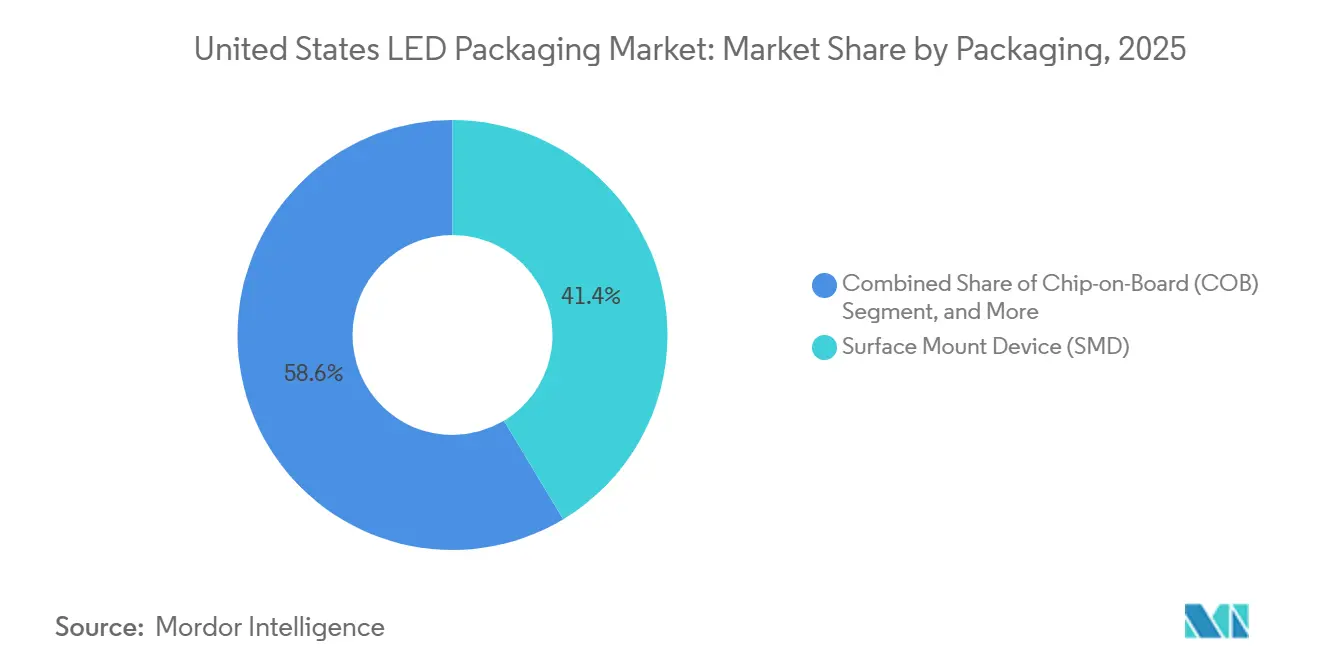

- By packaging architecture, surface-mount device packages led with a 41.38% revenue share of the United States LED packaging Market in 2025, while chip-scale packages are projected to expand at a 4.44% CAGR to 2031.

- By power class, mid-power packages accounted for 36.83% of the United States LED packaging market size in 2025, whereas high-power packages are advancing at a 4.21% CAGR through 2031.

- By emission type, visible LED packages dominated with 88.47% shipment share in 2025, yet ultraviolet LED packages are poised to grow at a 4.39% CAGR over the same period.

- By material chemistry, substrates accounted for 32.68% of the United States LED packaging market share in 2025, while phosphors and coatings are set to grow at a 4.27% CAGR through 2031.

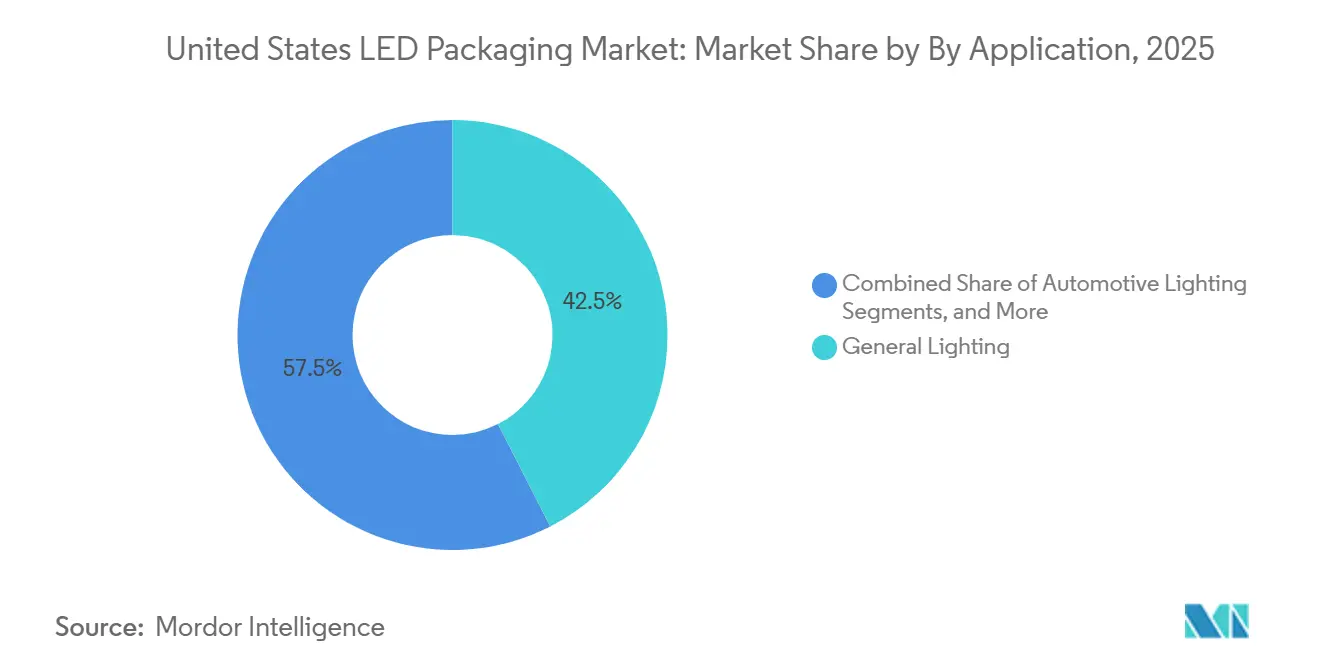

- By application, general lighting accounted for 42.49% of 2025 revenue, but automotive lighting is forecast to register the fastest 4.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States LED Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Mini-LED Backlight Adoption | +1.2% | National, California and Texas hubs | Medium term (2-4 years) |

| Tightening U.S. Energy-Efficiency Norms | +1.0% | National | Long term (≥ 4 years) |

| Rapid Automotive LED Growth in ADAS Sensors | +0.9% | Michigan and California automotive corridors | Medium term (2-4 years) |

| Expansion of Horticulture Lighting | +0.5% | California, Arizona, Texas, Colorado | Medium term (2-4 years) |

| On-shoring Incentives for Semiconductor Packaging | +0.3% | Arizona, California, Georgia pilot sites | Long term (≥ 4 years) |

| Silicon Photonics Integrated Packaging Breakthroughs | +0.1% | California and Massachusetts photonics clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge In Mini-LED Backlight Adoption

Samsung and LG introduced RGB Mini-LED televisions featuring more than 1,000 dimming zones, tripling the LED count versus legacy edge-lit designs. The finer pitch demands chip scale packages under 1 mm², automated pick-and-place tools exceeding 100,000 units per hour, and enhanced thermal vias to keep junction temperatures below 85 °C, preserving color stability over product lifetimes.[1]Samsung Electronics America, “Samsung Expands 2026 TV Lineup,” news.samsung.com Supply-chain learning curves have lowered average Mini-LED TV prices by nearly 30% over the past year, moving the technology from premium to mid-tier segments. For LED packagers, the architecture lifts revenue per panel because discrete red, green, and blue dies replace white LEDs plus quantum-dot films. Demand is strongest in consumer electronics assembly hubs in California and Texas, where rapid design cycles favor domestic suppliers capable of short lead times. The shift also stimulates investment in low-warpage metal-core printed circuit boards that dissipate hotspot heat in high-pixel-density arrays.

Tightening U.S. Energy-Efficiency Norms For Solid-State Lighting

The U.S. Department of Energy finalized a rule in April 2024 that raises general service lamp efficacy to roughly 120 lm W⁻¹ by July 2028, effectively eliminating most non-LED technologies.[2]U.S. Department of Energy, “Energy Conservation Standards for General Service Lamps,” federalregister.gov LED packagers must therefore improve phosphor conversion efficiency and adopt low-thermal-resistance flip-chip designs that sustain high drive currents without color shift. Integrated lamps must now meet power-factor thresholds of 0.7 or higher, linking package thermal design with electronic driver performance. High-CRI and color-tunable products face steeper optimization trade-offs, prompting segmented product lines that separate compliance-focused models from premium human-centric lighting offerings. Over the long term, the rule supports a steady baseline of replacement demand, cushioning the LED packaging market against cyclical swings in new-construction spending.

Rapid Automotive LED Penetration In ADAS Sensors

Automakers are embedding infrared 940 nm emitters for driver-monitoring cameras, gesture recognition, and short-range LiDAR to meet upcoming European driver-distraction regulations. Automotive-qualified packages endure junction temperatures up to 125 °C and 1,000 thermal cycles per AEC-Q102 standards, favoring ceramic substrates and gold-tin eutectic die attach. ams OSRAM’s pixelated EVIYOS 2.0 device combines 25,600 controllable pixels within 40 mm², integrating illumination with depth-of-flight sensing in a single unit. Domestic capacity is emerging: Lumentum committed hundreds of millions of dollars to a Greensboro, North Carolina facility that will process indium phosphide lasers adaptable to automotive modules, with ramp-up targeted for 2028. The convergence of lighting and sensing is redefining package design around high-density interconnects and real-time thermal management.

Expansion Of Horticulture Lighting In Controlled-Environment Farming

Vertical farms and greenhouses are upgrading to multi-channel LED fixtures that deliver photosynthetic photon efficacy above 3.0 µmol J⁻¹ while allowing spectral tuning across blue, red, far-red, and UV wavelengths to optimize crop traits. The DesignLights Consortium’s horticultural v4.0 requirements tightened efficacy thresholds, prompting packagers to document photon flux and thermal performance at operating temperatures rather than ambient test points. University of Missouri extension guidance highlights the need for close-proximity mounting within 15 cm of plant canopies, remote driver placement, and IP65-rated enclosures, all of which influence package footprint, coating selection, and connector design. Growers evaluate total cost of ownership over 50,000-hour lifetimes, rewarding LED suppliers that can certify lumen maintenance and spectral stability and integrate with climate-control software. These dynamics boost demand for high-power packages with ceramic substrates and UV-stable encapsulants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capex for Advanced Packaging Lines | -0.7% | National, especially small and mid-sized firms | Short term (≤ 2 years) |

| IP Litigation Risks Around Flip-Chip Processes | -0.5% | Automotive and high-power segments | Medium term (2-4 years) |

| Volatility in Rare-Earth Phosphor Supply | -0.4% | All color-converted LED packages | Medium term (2-4 years) |

| Thermal-Management Challenges at Ultra-High Power Levels | -0.3% | Automotive, horticulture, outdoor infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capex For Advanced Packaging Lines

Setting up flip-chip bonding, chip scale package assembly, and automated optical inspection requires investments of USD 30 million to USD 80 million per site. Tool lead times often exceed 12 months, and only a handful of global vendors supply eutectic die-attach ovens, wafer-level phosphor coaters, and sub-0.2 mm pick-and-place systems. Although the CHIPS for America program awarded USD 1.4 billion for advanced-packaging pilot lines, first commercial volumes will serve high-margin microelectronics long before LED products. Many regional packagers therefore outsource critical steps to subcontractors in East Asia, incurring logistics costs and exposure to tariff swings. Access to affordable capital remains the primary barrier for smaller U.S. entrants wishing to target high-reliability automotive or horticulture niches.

IP Litigation Risks Around Flip-Chip Processes

Everlight filed U.S. lawsuits in February 2026 against both Lumileds and Seoul Semiconductor, alleging infringement of U.S. Patent 7,554,126 covering electrode-ratio optimization in flip-chip packages.[3]Everlight Electronics Co., Ltd., “LED Patent Infringement Lawsuit Against Lumileds,” en.everlight.com Previous European decisions forced product recalls where Seoul’s WICOP technology was involved, demonstrating that injunctions can disrupt supply chains quickly. Licensing negotiations can add 5%-15% to bill-of-materials costs and delay launches by six to twelve months while freedom-to-operate analyses proceed. Large players mitigate exposure through cross-licensing, such as the broad October 2025 agreement between Nichia and ams OSRAM, but smaller firms without deep patent portfolios remain vulnerable. Higher insurance premiums and legal reserves further squeeze margins in already cost-competitive segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Architecture: Compact Designs Propel CSP Uptake

Chip scale packages account for the fastest growth trajectory, expanding at a 4.44% CAGR, as television makers and automotive OEMs demand sub-millimeter footprints that reduce optical losses and simplify assembly. Surface mount device formats still delivered the largest 41.38% LED packaging market share in 2025, supported by broad availability and well-established pick-and-place infrastructure.

The migration toward fine-pitch Mini-LED backlights and pixelated headlights is elevating interest in flip-chip architectures that eliminate top-side electrodes, trimming junction-to-case thermal resistance by up to 40%. Meanwhile, chip-on-board modules retain relevance in commercial downlights and horticulture fixtures where continuous high flux and uniform color output matter. Dual in-line and through-hole packages persist in retrofit signage but face erosion as automated surface-mount processes dominate. Integrated matrix device and glass-on-board concepts within the LED packaging market are emerging to co-package driver ICs, thermal spreaders, and optics for highly integrated displays, signaling a convergence of semiconductor and printed-circuit manufacturing disciplines.

By Power Class: High-Power Designs Capture New Regulatory Demand

Mid-power devices held 36.83% of the United States LED packaging market in 2025 value because they satisfy typical A-lamp and troffer requirements at modest cost, yet tightening efficacy rules favor consolidation into fewer, brighter packages. High-power modules (1-3 W) are therefore projected to outpace the overall LED packaging market size with a 4.21% CAGR, fueled by street-lighting retrofits, horticulture luminaires, and adaptive automotive beams that require sustained luminous flux.

Ultra-high-power units above 3 W confront thermal flux densities near 85 W cm⁻², compelling adoption of aluminum-nitride ceramics, vapor-chamber heat spreaders, and active cooling strategies. At the opposite end, low-power indicators lose relevance in general service lamps as minimum lumen thresholds rise. Rising drive currents are also directing R&D dollars toward high-reliability silver-sintered die attach and high-thermal-conductivity phosphor-silicone composites, maintaining performance even when junctions surpass 100 °C during automotive or horticultural duty cycles.

By Emission Type: UV Expansion Diversifies Revenue Streams

Visible LED packages dominated 88.47% of shipments of the United States LED packaging market in 2025in 2025, but ultraviolet devices show the strongest velocity, advancing at 4.39% a year on sterilization and resin-curing demand. UVA modules tuned near 365 nm enable rapid adhesive curing in electronics and automotive assembly lines, while UVC chips in the 260-280 nm band support water disinfection without mercury.

Package design must accommodate quartz windows or UV-stable silicones, as standard epoxies yellow under high-energy photons. Infrared emitters, particularly 830-940 nm VCSELs, are rising within driver-monitoring cameras and smartphone facial-recognition sensors, creating crossover opportunities for LED packaging industry players already supplying automotive headlamp arrays. These shifts reduce revenue dependence on traditional visible-light categories and encourage investment in specialized encapsulants, bond wires, and optical filters.

By Material Chemistry: Phosphor Innovation Enhances Spectral Control

Substrates led with 32.68% of LED packaging market share in 2025, reflecting sapphire, silicon, and ceramic wafers that anchor die and funnel heat. Nonetheless, phosphors and coatings record the highest 4.27% growth rate through 2031, driven by narrow-band red and green compositions that unlock BT.2020 and DCI-P3 color gamut compliance in premium displays.

Rare-earth volatility remains a core risk, as europium and terbium processing is heavily concentrated in China, prompting supply-chain dual-sourcing strategies and recycled phosphor initiatives. Encapsulation materials are shifting toward high-refractive-index silicones (n≈1.6) that raise light extraction by up to 15% while resisting photothermal degradation. In die-attach, gold-tin eutectic remains the benchmark for high-power reliability, although silver-sintered pastes are gaining acceptance because they eliminate voiding risk and match coefficient-of-thermal-expansion better than solders.

By Application: Automotive Lighting Outpaces General Illumination

General lighting remained the largest end-use at 42.49% of the United States LED packaging market in 2025, but its growth moderates as replacement cycles lengthen and efficacy gains plateau. Automotive lighting, by contrast, is forecast to grow at a 4.16% CAGR, propelled by adaptive driving beams, projection-based communication, and the fusion of illumination with perception sensors.

Display and backlighting demand is diversifying from edge-lit white LEDs toward dense RGB Mini-LED grids, multiplying per-panel die counts and boosting revenue per square inch. Consumer electronics drive ultra-thin form factors and under-display sensor integration, rewarding package designs under 0.5 mm z-height. Industrial and specialty niches, including UV curing, machine vision, and medical diagnostics, favor hermetic sealing and ceramic substrates, maintaining premium margins despite modest volumes within the broader LED packaging market.

Geography Analysis

California, Texas, and Arizona anchor the nation’s largest concentration of LED packaging facilities, benefitting from proximity to consumer-electronics contract manufacturers, abundant engineering talent, and established semiconductor infrastructure. The CHIPS for America program’s pilot lines in Arizona and California are expected to lower substrate costs and accelerate adoption of fan-out wafer-level processes by late-decade.

Michigan, Ohio, and surrounding Great Lakes states experience strong pull-through from automotive OEMs integrating matrix headlamps, driver-monitoring systems, and short-range LiDAR modules. Regulatory alignment with forthcoming European distraction-warning mandates is already influencing domestic component specifications, elevating demand for AEC-Q102-qualified infrared packages.

Vertical-farm clusters in California, Colorado, and Arizona lead U.S. adoption of high-efficacy horticultural fixtures, intensifying local sourcing of high-power LED modules and phosphor blends tailored for specific crop spectra. Meanwhile, photonics research corridors in Massachusetts and New York advance silicon-photonics integration and quantum-dot hybrids, although commercial packaging volume largely remains concentrated in the Southwest and West Coast.

Competitive Landscape

Global leaders such as Nichia, ams OSRAM, Lumileds, and Seoul Semiconductor control sizeable share through vertically integrated epitaxy, phosphor synthesis, and module assembly. Nichia and ams OSRAM’s 2025 cross-license covering thousands of nitride-based inventions reduces litigation risk for customers sourcing matrix headlamps and automotive interior modules. ams OSRAM confirmed the number-one ranking in TrendForce’s 2025 packaged-LED list and reported 7% year-on-year growth in its core semiconductor portfolio.

Domestic mid-tier players such as Bridgelux and Luminus Devices carve out niches in high-CRI architectural downlights and UV-C disinfection, leveraging rapid prototyping services and application engineering support to offset scale disadvantages. Cree LED’s 2026 launch of turnkey Level-2 PCB assemblies aims to streamline fixture manufacturer supply chains and capture more value upstream.

IP litigation remains a strategic lever: Everlight’s twin lawsuits against Lumileds and Seoul Semiconductor heighten uncertainty for producers lacking expansive patent portfolios. Simultaneously, the sector is investing in advanced thermal management, such as aluminum-nitride substrates and vapor-chamber integration, to unlock ultra-high-power horticulture and automotive opportunities. These technology races sustain moderate consolidation while leaving room for specialized entrants targeting emerging spectrally tuned or hybrid photonic-sensor applications across the LED packaging market.

United States LED Packaging Industry Leaders

Wolfspeed Inc.

Lumileds Holding B.V.

Osram Opto Semiconductors GmbH

Nichia Corporation

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lumentum committed hundreds of millions of dollars to acquire and equip a 240,000 sq ft Greensboro, North Carolina site for indium-phosphide laser and photonic product manufacturing, with more than 400 jobs planned and ramp-up targeted for 2028.

- March 2026: Bridgelux expanded its flexible linear portfolio with Thrive, F90, and RGBW strips delivering up to 160 lm W⁻¹ and CRI 98, rated IP68 for architectural installs.

- February 2026: Everlight sued Seoul Semiconductor in the Eastern District of Texas alleging infringement of flip-chip packaging patent 7,554,126.

- February 2026: Everlight filed a separate infringement action against Lumileds in Delaware over the same patent covering flip-chip electrode structures.

United States LED Packaging Market Report Scope

The United States LED Packaging Market Report is Segmented by Packaging Architecture (Surface Mount Device, Chip-on-Board, Chip Scale Package, Flip-Chip LED Packages, Dual In-line Package, Others), Power Class (Low Power, Mid Power, High Power, Ultra-High Power), Emission Type (Visible LED Packages, Infrared LED Packages, Ultraviolet LED Packages), Material Chemistry (Substrates, Encapsulation, Bonding/Die-Attach, Phosphors/Coatings), and Application (General Lighting, Automotive Lighting, Display and Backlighting, Consumer Electronics, Industrial and Specialty). The Market Forecasts are Provided in Terms of Value (USD).

| Surface Mount Device (SMD) |

| Chip-on-Board (COB) |

| Chip Scale Package (CSP) |

| Flip-Chip LED Packages |

| Dual In-line Package (DIP / Through-hole) |

| Others – IMD, GOB, Mini-LED Display Packaging |

| Low Power (Less Than 0.5 W) |

| Mid Power (0.5 to 1 W) |

| High Power (1 to 3 W) |

| Ultra-High Power (More Than 3 W) |

| Visible LED Packages |

| Infrared (IR) LED Packages |

| Ultraviolet (UV) LED Packages |

| Substrates |

| Encapsulation |

| Bonding / Die-Attach |

| Phosphors / Coatings |

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Consumer Electronics |

| Industrial and Specialty |

| By Packaging Architecture | Surface Mount Device (SMD) |

| Chip-on-Board (COB) | |

| Chip Scale Package (CSP) | |

| Flip-Chip LED Packages | |

| Dual In-line Package (DIP / Through-hole) | |

| Others – IMD, GOB, Mini-LED Display Packaging | |

| By Power Class | Low Power (Less Than 0.5 W) |

| Mid Power (0.5 to 1 W) | |

| High Power (1 to 3 W) | |

| Ultra-High Power (More Than 3 W) | |

| By Emission Type | Visible LED Packages |

| Infrared (IR) LED Packages | |

| Ultraviolet (UV) LED Packages | |

| By Material Chemistry | Substrates |

| Encapsulation | |

| Bonding / Die-Attach | |

| Phosphors / Coatings | |

| By Application | General Lighting |

| Automotive Lighting | |

| Display and Backlighting | |

| Consumer Electronics | |

| Industrial and Specialty |

Key Questions Answered in the Report

What is the current value of the United States LED packaging market?

The LED packaging market size stood at USD 0.65 billion in 2025 and is projected to reach USD 0.81 billion by 2031.

Which packaging architecture is growing the fastest?

Chip scale packages are forecast at a 4.44% CAGR through 2031, driven by Mini-LED backlights and pixelated automotive headlamps.

How will U.S. energy-efficiency rules influence package design?

The 2028 efficacy mandate of roughly 120 lm W⁻¹ is pushing manufacturers toward high-power, flip-chip architectures that maximize lumen output while controlling junction temperature.

Why are UV LED packages gaining traction?

Mercury-free sterilization, water treatment, and industrial curing processes favor UVC and UVA LEDs, which are projected to expand at a 4.39% CAGR.

What are the main barriers for new domestic entrants?

High capital expenditure for advanced packaging lines, often USD 30 million to USD 80 million, and exposure to patent litigation around flip-chip designs remain significant hurdles.

Which end-use segment will contribute the most incremental growth?

Automotive lighting is expected to deliver the highest incremental revenue through 2031, benefiting from adaptive beam, driver-monitoring, and LiDAR integration.

Page last updated on: