Asia-Pacific LED Module Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

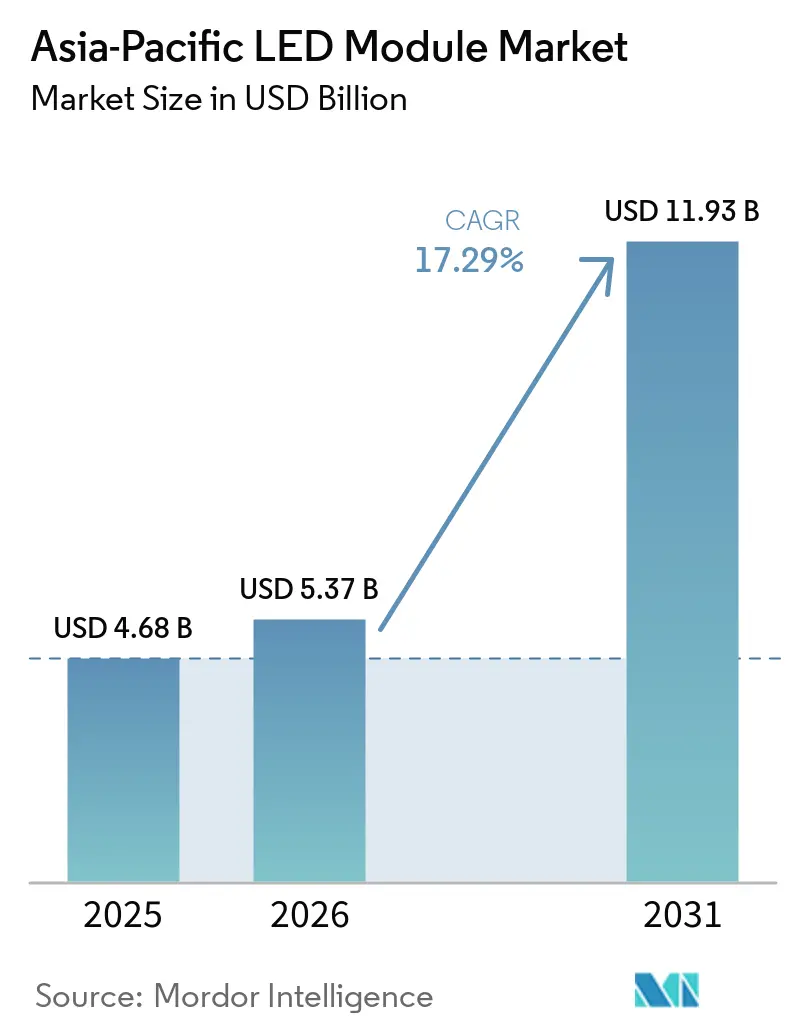

| Base Year Market Size (2025) | USD 4.68 Billion |

| Market Size (2026) | USD 5.37 Billion |

| Market Size (2031) | USD 11.93 Billion |

| Growth Rate (2026 - 2031) | 17.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific LED Module Market Analysis by Mordor Intelligence

The Asia-Pacific LED module market size is expected to increase from USD 4.68 billion in 2025 to USD 5.37 billion in 2026 and reach USD 11.93 billion by 2031, growing at a CAGR of 17.29% over 2026-2031. This upward trajectory is stimulated by regulatory bans on fluorescent lamps, double-digit cost erosion in high-power LED packages, and the mass-market rollout of mini-LED backlighting for premium televisions and automotive cockpits. Falling rare-earth phosphor supply security, especially after China’s 2025 export controls, is nudging customers toward phosphor-lean blue-pump architectures, while government incentives under China’s 14th Five-Year Plan and India’s Production Linked Incentive (PLI) program are localizing upstream chip and module capacity. Competition is intensifying as Chinese chipmakers absorb struggling Western assets, most notably San’an Optoelectronics’ pending acquisition of Lumileds, and as mid-tier brands weaponize proprietary no-wire packaging, pick-and-place automation, and spectrum-tuning software to defend margins in smart, automotive, and horticulture niches.

Key Report Takeaways

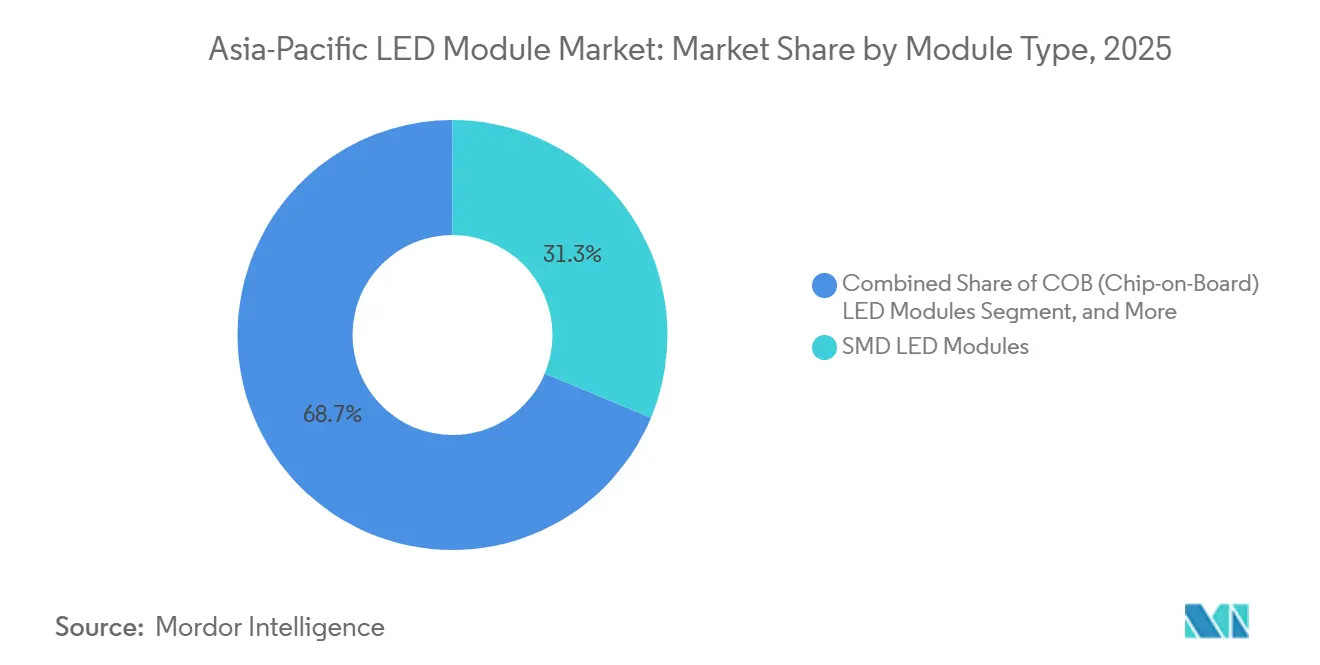

- By module type, surface mount device (SMD) packages led with 31.29% of the Asia-Pacific LED module market share in 2025, while backlight modules are projected to post a 17.73% CAGR through 2031.

- By application, general lighting accounted for 44.68% of the Asia-Pacific LED module market size in 2025, whereas display and backlighting are advancing at a 17.58% CAGR toward 2031.

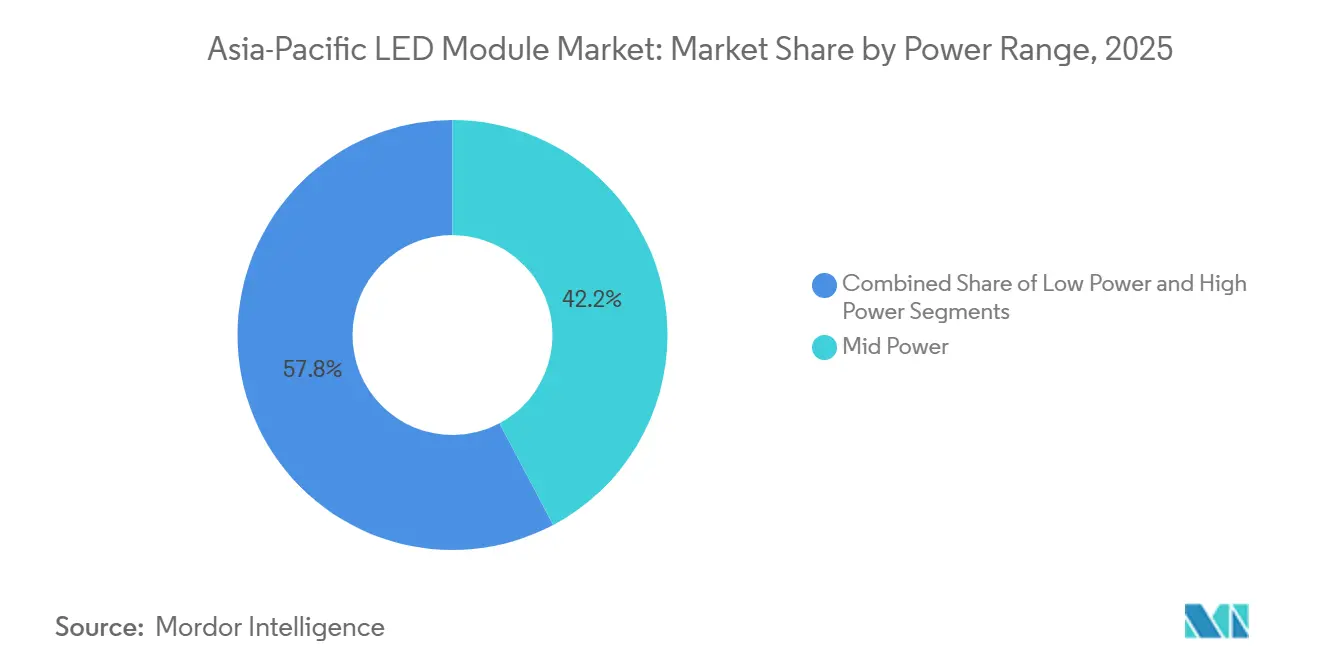

- By power range, mid-power modules accounted for 42.23% of 2025 revenue, and high-power modules are forecast to expand at a 18.05% CAGR between 2026 and 2031.

- By form factor, rigid boards held 82.18% shipment share in 2025, yet flexible modules are set to grow at an 18.11% CAGR through 2031.

- China captured 50.56% of 2025 regional revenue, while India is slated to be the fastest-growing geography, with a projected 17.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific LED Module Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerating Phase-Out of Fluorescent Lighting Mandates | +3.2% | China, Japan, India, Australia | Short term (≤ 2 years) |

| Rapid Decline in High-Power LED Cost per Lumen | +4.1% | Global (largest in China, India) | Medium term (2–4 years) |

| Expansion of Smart Lighting Ecosystems in Commercial Buildings | +2.8% | China, India, Singapore, Australia | Medium term (2–4 years) |

| Surge in Mini-LED Backlighting for High-End Displays | +3.5% | China, South Korea, Taiwan, Japan | Short term (≤ 2 years) |

| Localization Incentives Under China’s Five-Year Plan | +2.1% | China, spillover to Southeast Asia | Long term (≥ 4 years) |

| Growing VC Funding for Horticulture-Specific LED Modules | +1.2% | China, Japan, Australia, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Decline in High-Power LED Cost per Lumen

Wafer-scale yields jumping from 25% to 75% pushed package cost per kilolumen down by 95% between 2003 and 2020. Recent chip-on-board (COB) portfolio upgrades lifted luminous flux 5-8% at unchanged prices, further shrinking dollar per lumen metrics. These savings unlock use cases once blocked by payback hurdles, such as 100,000-lumen stadium floods and 3.0 µmol J⁻¹ horticulture fixtures. Chinese chip fabs drove module-level cost drops near 40% in 2025 on sub-P1.0 fine-pitch displays, hitting 99.99% die-transfer yields. Legacy suppliers must now pivot toward adaptive driving beam headlamps or micro-LED cinema screens to escape price wars.

Expansion of Smart Lighting Ecosystems in Commercial Buildings

Asia-Pacific building-automation investments are expanding at double-digit rates, and smart lighting sits at the heart of occupancy sensing and daylight harvesting strategies. Demonstrated energy savings of 40-60% in wired or wireless retrofits have convinced property owners in Singapore, Shanghai, and Mumbai to specify controllable Asia-Pacific LED module market SKUs. Municipal pilots like Taoyuan’s 6,000-pole project validate large-scale deployments using DALI-2 and Bluetooth mesh. Module vendors embedding radios and sensors enjoy a systems-level premium while partnering with building-management integrators to guarantee compliance with India’s code requirements.[1]Baogaobox Research, “Smart Lighting and Building Automation,” baogaobox.com

Surge in Mini-LED Backlighting for High-End Displays

Mini-LED televisions topped 20 million units shown at the 2026 CES, and China supplied over half that volume. Brands now deliver >2,000 nit peak brightness and >1,000,000:1 contrast through thousands of local-dimming zones. Automotive shipments for instrument clusters and head-up displays more than doubled between 2023 and 2025, escalating die counts per vehicle cockpit. Production lines embrace automated 10 µm pick-and-place tools reaching 99.9995% yield, the economic break-even for screens surpassing 10 million pixels.[2]LEDinside, “Mini-LED TV Shipments,” ledinside.com

Accelerating Phase-Out of Fluorescent Lighting Mandates

Mandatory phase-outs of compact and linear fluorescent lamps are compressing replacement cycles, channeling budgets toward linear Asia-Pacific LED module market solutions. China’s 2025 export curbs on rare-earth phosphors elevated legacy lamp prices, making LED retrofits cost-competitive even for price-sensitive facilities. Japan has mapped a 2027 cut-off for compact fluorescents and 2030 for linear tubes, while India’s building code forces LEDs in new commercial projects larger than 1,000 m². Australia mirrors United Nations Regulation 128 for automotive lighting, removing halogen options from new vehicles. Suppliers are bundling driver electronics and thermally optimized boards, so retrofit crews can finish installs without rewiring ballasts or enlarging cut-outs.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Persistent Thermal Management Challenges in High-Power Modules | -1.8% | Global, acute in Southeast Asia, India | Medium term (2–4 years) |

| Supply-Chain Concentration of Key Phosphor Materials | -1.5% | Global, highest in China-linked chains | Short term (≤ 2 years) |

| Stringent Automotive EMC Compliance Costs | -0.9% | China, Japan, South Korea, India | Medium term (2–4 years) |

| Plateauing Retrofit Demand in Tier-1 Cities | -1.1% | China, Japan, Singapore, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Concentration of Key Phosphor Materials

China refines more than 80% of global lanthanum, yttrium, europium, and cerium feedstock, and its October 2025 export license mechanism extends lead times by 45 days. Phosphor powders jumped 30% in late 2025, trimming gross margin by up to three points for buyers lacking long contracts. Inventories have ballooned to 90-120 days, locking working capital and heightening obsolescence risk if RGB COB stacks mature. Mining projects in Australia and Vietnam will not materially diversify supply before 2028.

Persistent Thermal Management Challenges in High-Power Modules

Junction temperatures beyond 125 °C cut luminous efficacy by up to 15% and shift correlated color temperature by 500-1,000 K after 10,000 hours. Uncooled 50 W COB assemblies hit 142 °C in <1 minute, forcing designers to add vapor-chamber spreaders, liquid cold plates, or thermoelectric coolers that raise bill-of-materials (BoM) by USD 15-25 each. Hot, humid climates in Southeast Asia further degrade natural convection, requiring heavier aluminum extrusions that inflate transport costs. Ceramic substrates with >200 W m⁻¹ K⁻¹ conductivity triple printed-circuit expense but remain indispensable for adaptive driving beam modules.[3]OFweek, “Thermal Runaway in High-Power COB Arrays,” ofweek.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Module Type: SMD Volume Leadership, COB Niches Scale

SMD boards captured 31.29% of the Asia-Pacific LED module market share in 2025, supported by mass-manufactured troffers, downlights, and strip fixtures. Shipment trends confirm that the Asia-Pacific LED module market remains anchored in SMD architectures, which accounted for one-third of 2025 regional revenue. SMD arrays dissipate heat across multiple junctions, tolerate automated high-speed placement exceeding 50,000 components per hour, and meet efficacy targets up to 181 lm W⁻¹ without active cooling. The Asia-Pacific LED module market size, attributed to backlight modules, is expanding fastest, propelled by mini-LED television orders and double-digit growth in automotive cockpits. Chip-on-board entries, although still a minority, offer flux densities up to 8,000 lumens from a single emitter, ideal for museum spots, adaptive headlamps, and cinema projection.

Competitive positioning is diverging. SMD providers face commodity erosion as new Chinese entrants match performance at lower costs, whereas COB specialists shield margins through proprietary ceramic substrates and reflective coatings. Linear replacement boards remain resilient in commercial retrofits, while flexible strips migrate toward ambient lighting and curved signage duties. Suppliers that invest in no-wire interconnects and high-thermal conductivity composites are winning design-ins for next-generation automotive arrays.

By Application: Backlighting Momentum Tops General Lighting

General lighting still supplied 44.68% of 2025 demand across residential, commercial, and industrial premises, but its growth decelerates as household penetration in tier-1 cities surpasses 60%. The Asia-Pacific LED module market share weighted to display backlighting is climbing at a 17.58% CAGR, reflecting premium television diffusion and instrument-cluster upgrades in electric vehicles. Industrial buyers pursue high-bay modules with >140 lm W⁻¹ efficacy and 100,000-hour lifetimes to curb maintenance at 10-m ceiling heights. Automotive lighting expands briskly thanks to pixelated headlamps and animated exterior signals that require millisecond response times.

Smart-ready commercial luminaires bundle Bluetooth mesh or Zigbee radios, tilting the specification in favor of vendors with embedded driver and sensing know-how. Fine-pitch digital signage drops below P1.0 mm, allowing outdoor billboards and in-store kiosks to rival LCD video walls in perceived resolution. Module makers differentiating through optical films and spectrum-tuning algorithms can lock in sticky revenues as retailers demand high color rendering for merchandise illumination.

By Power Range: High-Power Modules Accelerate

Mid-power assemblies spanning 5-30 W retained a 42.23% share during 2025, propelled by cost-effective downlights and troffers. However, the Asia-Pacific LED module market size for high-power designs above 30 W is projected to rise at an 18.05% CAGR, addressing stadium fixtures, port aprons, and adaptive headlamp arrays. Low-power segments <5 W plateau as smartphones and wearables migrate to micro-LEDs and organic light-emitters. The thermal headroom gap keeps high-power boards reliant on advanced substrates, but premium automotive and horticulture use cases justify higher BoM and price points.

Module vendors with graphene pads, vapor-chamber plates, or ceramic composites secure the bulk of design wins in high-heat environments. Conversely, mid-power producers exploit aluminum heat sinks to satisfy rebate programs targeting efficacy above 120 lm W⁻¹. Price competition below 5 W remains intense, pushing differentiation toward lead times and private-label custom colors.

By Form Factor: Flexible Boards Unlock Curved Installations

Rigid printed-circuit assemblies made up 82.18% of 2025 shipments on account of robustness, simpler tooling, and lower costs. The Asia-Pacific LED module market expects flexible boards to outpace all other forms at an 18.11% CAGR, driven by ambient strips that wrap automotive interiors and immersive retail façades. Polyimide substrates <0.2 mm thick survive 10 mm bend radii without solder-joint cracking, while roll-to-roll production is narrowing the price delta with rigid boards to 25-30%.

Flexible pioneers offer pixel pitches from P0.9 to P5.0 at 600-1,000 nit brightness, suitable for indoor curved video walls. Automakers increasingly specify color-changing cabin accents integrated into dashboards and door lines, positioning module vendors with conformal-coating expertise to capture higher margins. Rigid specialists will need optical films or spectrum-tuning add-ons to defend their share in commoditized flat-panel backlighting.

Geography Analysis

China remained the powerhouse of the Asia-Pacific LED module market in 2025, controlling 50.56% of turnover through fully integrated ecosystems across the Yangtze River Delta, Pearl River Delta, and Chengdu-Chongqing corridors. Provincial subsidies, land grants, and tax holidays kept capital expenditures flowing into chip and module fabs. Mini-LED backlight revenue grew from CNY 19.0 billion (USD 2.68 billion) in 2023 to CNY 30 billion (USD 4.18 billion) in 2025, underscoring China’s grip on display-grade modules. The October 2025 rare-earth export license regime further tightened Beijing’s leverage over phosphor supply and encouraged overseas buyers to accelerate LED conversions to sidestep fluorescent scarcity.

India is forecast to be the fastest-growing Asia-Pacific LED module market, expanding at a 17.84% CAGR through 2031. The PLI scheme disbursed INR 28,748 crore (USD 344 million) in incentives by February 2026, catalyzing local investment from Ikio Solutions, Lumax Industries, and others. The Energy Conservation Building Code locks LEDs into all new commercial builds over 1,000 m², guaranteeing mid-power board demand. Global brands that lack Indian production must partner or license technology to clear localization thresholds.

Japan exhibits a mature but profitable profile, with >70% penetration in general lighting by 2025 and a pivot toward automotive, horticulture, and micro-LED wearables. Conformance with European fluorescent phase-outs will push linear module upgrades in office and transport infrastructure. South Korea leads mini-LED and micro-LED panel innovation via Samsung Display and LG Display, while Taiwan supplies chips through Epistar and Everlight. Southeast Asian nations, notably Vietnam, are capturing assembly offshoring as Seoul Semiconductor and OMINSU form alliances for global export.

Competitive Landscape

The Asia-Pacific LED module market shows moderate fragmentation, with the top five suppliers holding 35.87% of 2025 revenue. Consolidation is gathering pace: San’an Optoelectronics intends to close a USD 239 million purchase of Lumileds in Q1 2026, vaulting the Chinese firm into automotive supply chains and an extensive cross-licensing club. Seoul Semiconductor narrowed its global gap with ams OSRAM to one percentage point in 2024 by leaning on WICOP no-wire packages and >18,000 patents. ams OSRAM divested its Entertainment and Industry Lamps unit to Ushio for EUR 114 million (USD 128 million) in March 2026, freeing cash for digital photonics.

Competitive levers pivot on intellectual property, automation, and niche spectrum science. Vendors owning pick-and-place lines that handle 10 µm chips at 99.9995% yield can undercut rivals in mini-LED backlights. Horticultural-module start-ups raise venture funding to develop spectrum algorithms, creating white-space opportunities. Automotive pixelated headlamps and adaptive beam modules demand ASIC-grade EMC compliance, steering contracts toward suppliers with in-house anechoic labs. Chinese display makers like BOE and TCL Huaxing are internalizing module production to secure capacity, pressuring independents to specialize or merge.

Asia-Pacific LED Module Industry Leaders

Nichia Corporation

Samsung Electronics Co., Ltd.

Seoul Semiconductor Co., Ltd.

LG Innotek Co., Ltd.

Cree LED (SGH Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: ams OSRAM completed the sale of its Entertainment and Industry Lamps unit to Ushio for EUR 114 million (USD 128 million) on a cash- and debt-free basis, bolstering balance-sheet deleveraging and sharpening focus on digital photonics.

- January 2026: Bloemteknik raised GBP 2.5 million (USD 3.2 million) to scale spectrum-tunable horticulture fixtures and deploy more than 25,000 units worldwide.

- Jan 2026: LG Innotek won a CES innovation award for its Ultra Thin Pixel Lighting Module, slated for mass production in H2 2027 for curved automotive interiors and retail façades.

- August 2025: San’an Optoelectronics and Inari Amertron agreed to acquire Lumileds for USD 239 million, granting access to automotive customers and global patents.

Asia-Pacific LED Module Market Report Scope

An LED Module is a pre-assembled, integrated lighting component consisting of one or more light-emitting diodes (LEDs) mounted on a printed circuit board or substrate, along with essential electrical and thermal management elements such as current-limiting circuitry and heat-dissipation structures, designed to operate as a functional light source when incorporated into a luminaire and powered by an appropriate electrical supply.

The Asia-Pacific LED Module Market Report is Segmented by Module Type (COB, SMD, Linear, Backlight, High-Power, and Other Module Types), Application (General Lighting, Automotive, Display and Backlighting, Signage, and Other Applications), Power Range (Low, Mid, and High), and Form Factor (Rigid, and Flexible), and Country (China, Japan, India and Rest of Asia- Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| COB (Chip-on-Board) LED Modules |

| SMD LED Modules |

| Linear LED Modules |

| LED Backlight Modules |

| High-Power LED Modules |

| Others, Module Type |

| General Lighting | Residential |

| Commercial | |

| Industrial | |

| Automotive Lighting | |

| Display and Backlighting | |

| Signage and Advertising | |

| Others, Application |

| Low Power (less than or equal to 5 W) |

| Mid Power (greater than 5 W to less than or equal to 30 W) |

| High Power (greater than 30 W) |

| Rigid LED Modules |

| Flexible LED Modules |

| China |

| Japan |

| India |

| Rest of Asia-Pacific |

| By Module Type | COB (Chip-on-Board) LED Modules | |

| SMD LED Modules | ||

| Linear LED Modules | ||

| LED Backlight Modules | ||

| High-Power LED Modules | ||

| Others, Module Type | ||

| By Application | General Lighting | Residential |

| Commercial | ||

| Industrial | ||

| Automotive Lighting | ||

| Display and Backlighting | ||

| Signage and Advertising | ||

| Others, Application | ||

| By Power Range | Low Power (less than or equal to 5 W) | |

| Mid Power (greater than 5 W to less than or equal to 30 W) | ||

| High Power (greater than 30 W) | ||

| By Form Factor | Rigid LED Modules | |

| Flexible LED Modules | ||

| By Geography | China | |

| Japan | ||

| India | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large will Asia-Pacific demand for LED modules be by 2031?

The Asia-Pacific LED module market is forecast to reach USD 11.93 billion by 2031, up from USD 5.37 billion in 2026.

Which module type holds the top revenue position today?

SMD boards dominate, supplying 30-35% of 2025 shipments because of mass-production economics and broad design compatibility.

Why is India the fastest-growing country?

India’s PLI incentives and mandatory LED codes in new commercial buildings are propelling a projected 17.84% CAGR through 2031.

What is driving mini-LED backlighting adoption?

The shift to local dimming zones above 1,000, brightness levels >2,000 nits, and cost-competitive yields near 99.9995% are accelerating mini-LED demand.

Page last updated on: