Asia-Pacific Automotive LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

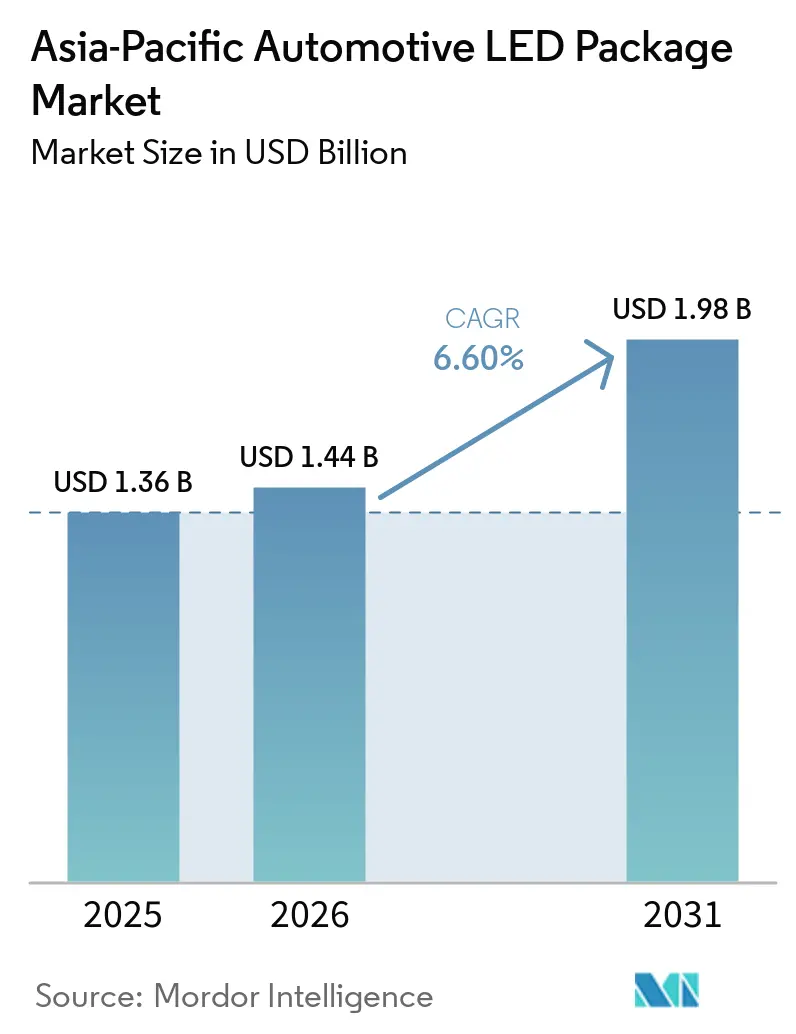

| Base Year Market Size (2025) | USD 1.36 Billion |

| Market Size (2026) | USD 1.44 Billion |

| Market Size (2031) | USD 1.98 Billion |

| Growth Rate (2026 - 2031) | 6.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Automotive LED Package Market Analysis by Mordor Intelligence

The Asia-Pacific automotive LED package market size is expected to grow from USD 1.36 billion in 2025 to USD 1.44 billion in 2026 and is forecast to reach USD 1.98 billion by 2031 at a 6.60% CAGR over 2026-2031. Structural demand is shifting from basic illumination toward intelligent, pixel-addressable lighting that embeds sensing, data communication, and adaptive beam control within a single compact package. China leads adoption thanks to large-scale new-energy vehicle output and aggressive in-country epitaxy investment, while India’s production-linked incentives and safety regulations make it the fastest-growing geography. Automakers are migrating from surface-mount to chip-scale formats to achieve ultra-slim headlamp profiles, reduced drag, and distinctive brand signatures. Competitive intensity is rising as Japanese and Korean incumbents defend share against vertically integrated Chinese suppliers that leverage lower epitaxial costs and shorter supply chains to price aggressively.

Key Report Takeaways

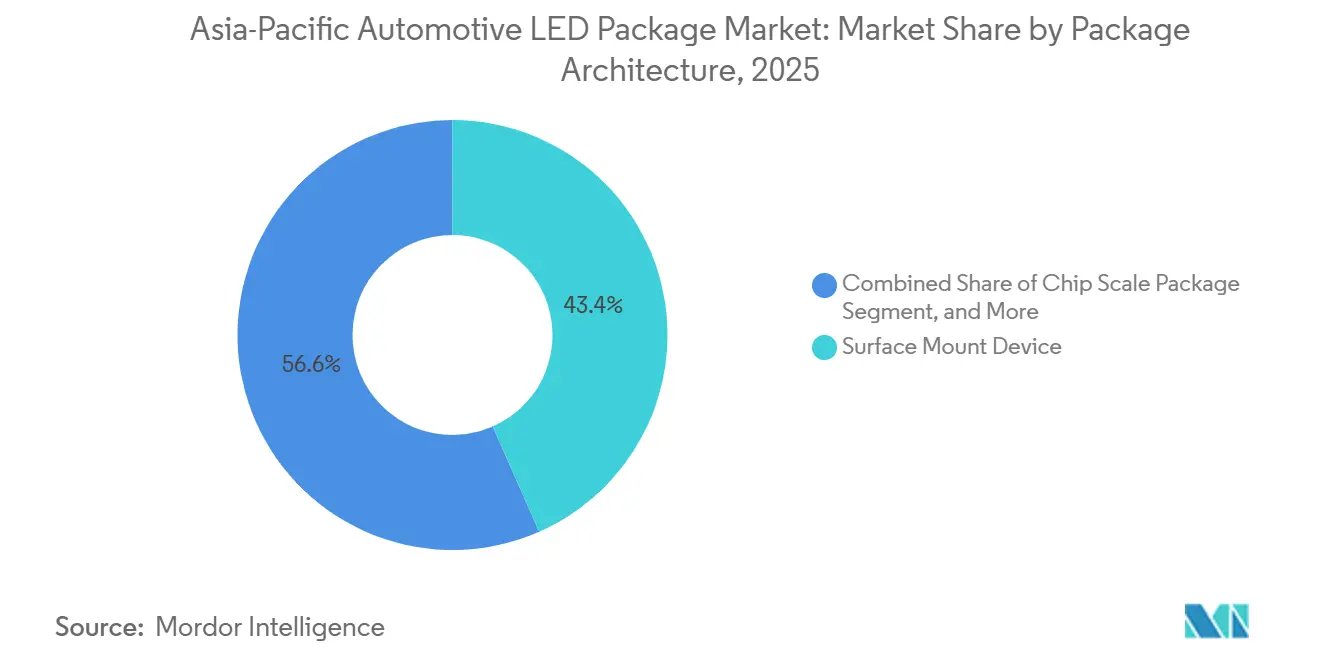

- By package architecture, surface-mount device formats led with 43.39% revenue share in 2025; chip-scale packages are forecast to expand at a 7.06% CAGR to 2031.

- By power class, high-power packages above 1 watt captured 57.89% of the Asia-Pacific automotive LED package market size in 2025 and will advance at a 6.97% CAGR.

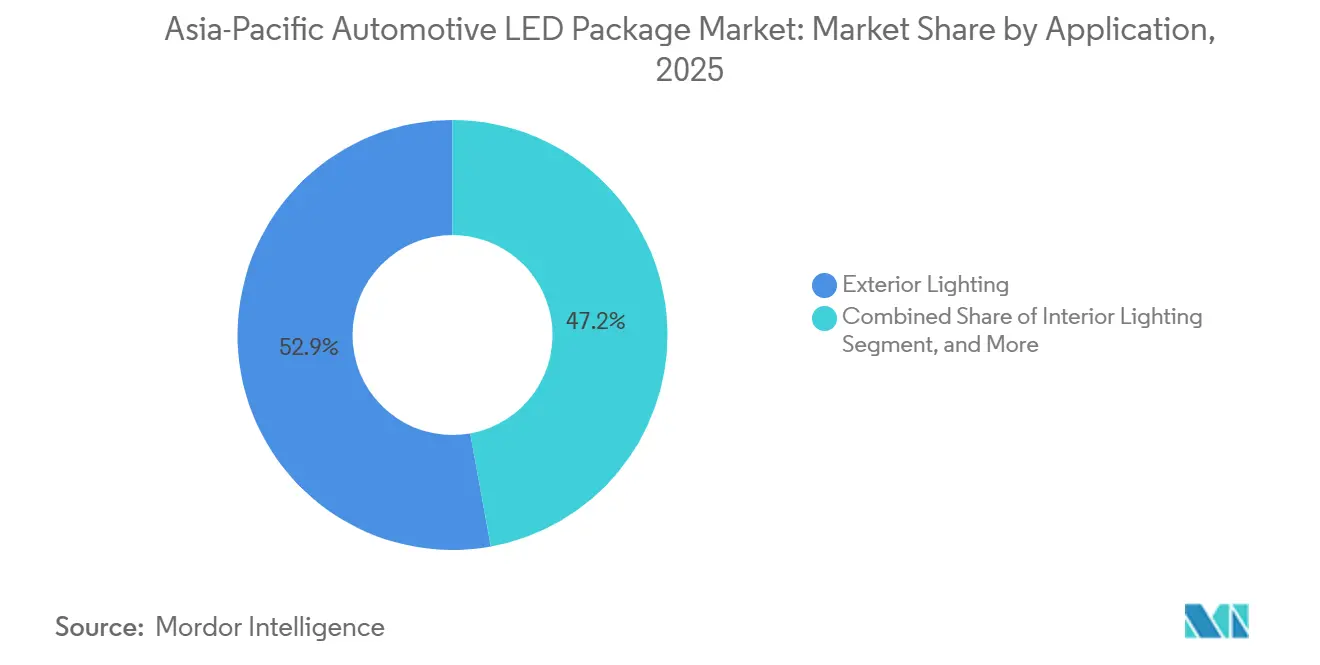

- By application, exterior lighting commanded 52.85% share of the Asia-Pacific automotive LED package market size in 2025, whereas interior lighting is poised for a 7.11% CAGR.

- By vehicle type, passenger cars represented 73.49% of 2025 volume and are set to grow at a 6.89% CAGR through 2031.

- By geography, China held 54.49% of the Asia-Pacific automotive LED package market share in 2025, while India is projected to record the highest 6.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Automotive LED Package Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for energy-efficient automotive lighting | +1.2% | Global, strongest in China, Japan, South Korea | Medium term (2-4 years) |

| Growing penetration of LED headlamps in passenger vehicles | +1.4% | China, India, Southeast Asia | Short term (≤ 2 years) |

| Stringent automotive lighting safety regulations | +0.9% | China, India, ASEAN | Long term (≥ 4 years) |

| Rapid expansion of electric vehicle production in Asia-Pacific | +1.5% | China dominant, India emerging | Medium term (2-4 years) |

| Localized supply chains reducing LED package costs in ASEAN | +0.8% | Thailand, Vietnam, Malaysia, spillover to India | Medium term (2-4 years) |

| Integration of smart pixel LED arrays for ADAS | +1.0% | China, Japan, South Korea, premium India and ASEAN | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Energy-Efficient Automotive Lighting

Electric vehicle programs across Asia-Pacific center on maximizing range, so every watt shaved from lighting subsystems translates directly into extra driving kilometers. China’s 12.86 million new-energy vehicles built in 2024 created a large installed base that values LED packages delivering 30-50% lower power draw than halogens, translating to 5-10 kilometer range gains in compact battery-electric cars.[1]Office of Energy Efficiency and Renewable Energy, “Solid-State Lighting 2022 Research Roadmap,” energy.gov Hybrid platforms also benefit when alternator load falls, improving fuel-economy scores used for subsidy qualification in India and Thailand. Efficacy gains projected by the U.S. Department of Energy, reaching 249 lumens per watt by 2035, underpin future package roadmaps. Reliability advantages, with lifetimes of 25,000-50,000 hours compared with 1,000-2,000 hours for halogens, cut warranty risk for fleet operators in Southeast Asia where service networks are sparse.

Growing Penetration of LED Headlamps in Passenger Vehicles

Packaged LED cost fell below USD 0.50 per kilolumen in 2025, allowing automakers to list LED headlamps as standard equipment on mid-tier sedans and sport-utility vehicles. Seoul Semiconductor’s WICOP chip-scale devices underpin more than 100 passenger models, validating cost targets for mass production. India’s Bharat NCAP protocol attaches higher safety scores to daytime-running-lamp equipped cars, nudging OEMs toward full LED headlamp-DRL bundles. China’s passenger car production exceeded 20 million units in 2024, with LED headlamp penetration crossing 60% as domestic suppliers matched Japanese peers on luminance and thermal performance while pricing 20-30% below incumbent quotes.[2] Bureau of Indian Standards, “Automotive Headlamp Performance Regulations,” bis.gov.in

Stringent Automotive Lighting Safety Regulations

China’s GB 4599-2021 and GB 25991-2021 raise photometric thresholds that halogens struggle to meet cost-effectively. India’s AIS-034 and subsequent AIS-145 DRL mandate create a regulatory floor for LED fitment beginning in 2025. Thailand, Vietnam, and Singapore have adopted UNECE R48, R7, R87, R112, and R128, enabling harmonized beam-pattern requirements and driving OEMs to specify multi-chip LED arrays that deliver precise cutoff lines and glare control.[3]Ministry of Road Transport and Highways, “AIS-145 Revision for Daytime Running Lamps,” morth.nic.in

Rapid Expansion of Electric Vehicle Production in Asia-Pacific

China’s dominance, responsible for roughly 60% of global EV sales, yields the largest regional addressable market for high-reliability LED packages. India’s 2.36 million EV units sold in 2025 include 1.28 million two-wheelers and witness 85% year-over-year passenger-car growth. EV interiors feature 50-100 RGB LEDs for mood, navigation, and ADAS alerts, expanding demand for mid-power devices. China’s January 2026 export licensing for new-energy vehicles signals policy support for domestic value retention, spurring LED suppliers to add in-country lines that now feed export programs across Asia-Pacific.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial cost compared to halogen solutions | -0.6% | India, Southeast Asia price-sensitive segments, China entry models | Short term (≤ 2 years) |

| Thermal management challenges in high-power LED packages | -0.5% | Global, acute in tropical Southeast Asia, Southern China, India | Medium term (2-4 years) |

| Volatility in automotive sales due to macroeconomic uncertainties | -0.4% | China purchase-tax impact, India interest-rate sensitivity, ASEAN exports | Short term (≤ 2 years) |

| Patent litigation risks limiting new entrant innovation | -0.3% | Japan, South Korea, Taiwan, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Cost Compared to Halogen Solutions

Entry-level cars in India and cost-sensitive ASEAN markets still rely on halogen assemblies costing USD 5-8 each, whereas a basic LED headlamp bill of materials sits in the USD 15-25 range. For compact sedans retailing at roughly USD 10,000-12,000, the extra USD 10 per lamp materially erodes automaker margin. Although mid-power surface-mount LED prices are now under USD 0.50 per kilolumen, drivers, heat sinks, and optics push full-system cost three-to-four times higher than halogen. Two-wheel EVs, despite energy-efficiency gains, continue opting for single-chip LEDs or halogens because unit economics dominate purchase decisions.

Thermal Management Challenges in High-Power LED Packages

High-power packages exceeding 1 watt can push junction temperatures past 120 °C, forcing designers to specify metal-core PCBs, heat pipes, or active fans that add USD 5-8 to each headlamp. Ambient temperatures above 35 °C in Southeast Asia and Southern China worsen degradation and drive overspecification or reduced life targets. ams OSRAM’s OSLON Compact RM achieves 209 Mcd m-2 at 1 ampere with 4.62 K W-1 thermal resistance but still needs active cooling in dense matrix arrays. Ceramic package innovations reduce thermal impedance yet remain confined to premium models due to process complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Package Architecture: Chip-Scale Migration Underpins Slim Headlamp Styling

Surface-mount devices captured 43.39% of the Asia-Pacific automotive LED package market share in 2025, maintaining leadership in rear lamps, license-plate illumination, and dome lights where proven reliability and entrenched supply chains matter most. Yet chip-scale packages, expanding at a 7.06% CAGR, are redefining headlamp styling by trimming total optical height to as low as 10 millimeters. Seoul Semiconductor’s WICOP structure bonds the bare die directly to the circuit board, eliminating substrates and ceramic frames. The Asia-Pacific automotive LED package market size attached to chip-scale devices is set to accelerate as OEMs in China and Japan seek razor-thin lamp designs that lower drag and enable distinct daytime signatures.

Flip-chip formats ride the same trend, leveraging gold-pad bonding to improve thermal conductivity and current spreading for adaptive driving beam arrays. Patent crossfire is intensifying; Everlight’s February 2026 U.S. filing against Seoul Semiconductor alleges infringement on flip-chip electrode geometry, signaling legal friction as CSP demand grows. Chip-on-board remains a niche for auxiliary spot lamps in commercial vehicles where clustering multiple dies on a single aluminum substrate gives high lumen density. Combined, these dynamics indicate that chip-scale and flip-chip will keep eroding legacy SMD share as local Chinese suppliers scale wafer-level packaging lines.

By Power Class: High-Power Devices Fuel Matrix Headlamp Adoption

High-power packages above 1 watt delivered 57.89% of 2025 revenue, mirroring rapid uptake of adaptive driving beam systems that require 200-plus cd mm-2 luminance for glare-free high beam. The Asia-Pacific automotive LED package market size attributable to this class will expand alongside pixelated headlights entering mid-tier sedans by 2028. Mid-power devices fill daytime running lamp and interior RGB roles where thermal constraints are modest. Low-power indicators are commoditizing as Chinese vendors quote sub-USD 0.10 per part, squeezing margins and prompting consolidation.

Nichia’s µPLS micro-LED light engine shows the trajectory: 16,384 high-power micro-LEDs, each at 50-100 mW, combine for over 1,000 lumens while enabling road-surface projections. Regulatory glare-control requirements in GB 4599-2021 and UNECE R112 push OEMs toward such arrays. Mid-power RGB usage is surging in electric-vehicle cabins where 50-100 addressable LEDs handle mood, navigation, and state-of-charge alerts. The high-power segment will continue to dominate value as each vehicle adds 100-300 pixels for smart headlights.

By Application: Interior Lighting Outpaces Exterior as Personalization Takes Hold

Exterior lighting retained 52.85% revenue share in 2025, anchored by headlamps and rear lamps that carry higher power budgets and regulatory complexity. Yet interior lighting is on track for a 7.11% CAGR to 2031, the fastest pace in the Asia-Pacific automotive LED package market. Premium electric cars now integrate multi-zone RGB ambient systems with 50-100 addressable LEDs per cabin, offering dynamic color shifts tied to ADAS notifications.

Sensing and infrared functions add a parallel revenue stream as driver-monitoring and night-vision cameras embed 850-940 nm emitters alongside visible LEDs. Refond Optoelectronics’ interactive grille and taillight modules demonstrate cross-function packaging that merges communication, safety, and styling. Exterior growth moderates because LED penetration already exceeds 70% in China and Japan, but adaptive matrix systems and grille lighting will keep value high. Interior expansion is passenger-vehicle focused, while commercial fleets remain cost-cautious.

By Vehicle Type: Passenger Cars Anchor Volume and Feature Innovation

Passenger vehicles delivered 73.49% of units in 2025, and their Asia-Pacific automotive LED package market share will climb as LED headlamps move from premium to standard trim levels. New-energy cars built in China surpass 40% share of production, each featuring multiple adaptive lighting elements that inflate LED content per unit. Commercial vehicles lag because fleet buyers prioritize total cost of ownership and longer service intervals that delay technology refresh.

Two- and three-wheel EVs in India, while sizeable, mostly utilize single-chip LEDs, highlighting cost sensitivity. Nonetheless, as production-linked incentives compress system pricing, LED technology will filter into light-duty trucks for safety-critical lamps. Passenger sedans and crossovers remain the innovation sandbox for pixel-level headlights and multi-zone ambient lighting that magnify package demand per vehicle.

Geography Analysis

China’s outsized 54.49% share reflects its unmatched scale in both new-energy vehicle production and vertically integrated LED manufacture. Facilities such as LEKIN Semiconductor’s USD 735 million Suzhou campus can supply five million vehicles a year, while refinement of domestic GB standards accelerates LED replacement of halogens and HID lamps. The government’s export-license framework effective January 2026 further cements domestic value capture and incentivizes in-country assembly by global tier-ones.

India is on a rapid ascent with a 6.83% CAGR, underpinned by generous production-linked incentives that target 75-80% local value-addition by the 2028-2029 fiscal year. Electric-vehicle penetration reached 8% in 2025, and AIS-145 daytime-running-lamp rules, together with Bharat NCAP safety scores, are embedding LED lighting as a default even in mid-tier cars. Localization is forecast to cut the price gap between LED and halogen headlamps from four-times to under two-times within three years, catalyzing adoption in compact and entry models.

Japan, South Korea, and the key ASEAN economies round out the remaining share. Japan exports advanced micro-LED and CSP technology, South Korea pivots toward high-value AP modules following Samsung’s commodity exit, and ASEAN forms a hub-and-spoke network with Thailand assembling finished vehicles, Vietnam hosting low-cost packaging lines, and Malaysia providing OSRAM’s global supply. Harmonized UNECE regulations across ASEAN enable single-architecture lamp designs, accelerating LED inclusion across multiple markets.

Competitive Landscape

Market concentration sits in the moderate range; the top five suppliers control roughly half of 2025 revenue, but share is fluid as price pressure intensifies. Samsung’s withdrawal reshuffled the order book, giving Seoul Semiconductor a sudden volume boost while opening space for Chinese challengers that pair low-cost epitaxy with AEC-Q102 certification. Vertical integration is the dominant strategic lever, exemplified by Sanan Optoelectronics absorbing Lumileds to trim chip costs 30% and lock in captive package demand.

Nichia and ams OSRAM protect premium niches through expansive patent estates and continuous micro-LED innovation, launching 16,384-pixel and 25,600-pixel arrays already deployed in German and Chinese luxury models. Patent enforcement remains vigorous; Everlight’s U.S. case against Seoul Semiconductor in February 2026 underscores ongoing IP battles that could reshape access to flip-chip architectures. Licensing remains essential, with cross-licensing deals serving as passports into high-value segments without protracted litigation.

Emerging players such as Refond Optoelectronics, MLS, and Ennostar aim to leapfrog via chip-scale and adaptive-matrix platforms while leveraging Chinese government subsidies and Southeast Asian cost bases. Qualification to AEC-Q102, photometric compliance under UNECE R112, and proven thermal cycling are minimal gateways, yet brand reputation and proven field reliability still favor incumbents in high-liability headlamp programs. Overall, rivalry will intensify as matrix headlamps migrate into mid-priced vehicles and per-car LED content continues to climb.

Asia-Pacific Automotive LED Package Industry Leaders

Nichia Corporation

OSRAM GmbH (Ams-OSRAM AG)

Seoul Semiconductor Co., Ltd.

Lumileds Holding B.V.

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Everlight Electronics filed a U.S. patent infringement suit against Seoul Semiconductor covering WICOP HF Series flip-chip processes.

- January 2026: LG Innotek committed KRW 100 billion (USD 67.9 million) to expand its Gwangju site for automotive application-processor modules, completion by Dec 2026.

- November 2025: ams OSRAM introduced OSLON Compact RM, a 0.5 mm² high-current chip rated at 209 Mcd m-2 for ultra-slim headlamps.

- August 2025: Sanan Optoelectronics closed the USD 239 million Lumileds acquisition, securing 30% epitaxial cost savings.

Asia-Pacific Automotive LED Package Market Report Scope

The Asia-Pacific Automotive LED Package Market Report is Segmented by Package Architecture (SMD, CSP, Flip-Chip LED Packages, COB), Power Class (Low Power <0.5 W, Mid Power 0.5-1 W, High Power >1 W), Application (Exterior Lighting, Interior Lighting, Sensing/IR Applications, Others), Vehicle Type (Passenger Vehicles, Commercial Vehicles), and Geography (China, Japan, India, Southeast Asia, Rest of Asia-Pacific). Market Forecasts are Provided in Terms of Value (USD).

| SMD (Surface Mount Device) |

| CSP (Chip Scale Package) |

| Flip-Chip LED Packages |

| COB (Chip-On-Board) |

| Low Power ( Less Than 0.5 W) |

| Mid Power (0.5 to 1 W) |

| High Power (More Than 1 W) |

| Exterior Lighting |

| Interior Lighting |

| Sensing / IR Applications |

| Others - Applications |

| Passenger Vehicles |

| Commercial Vehicles |

| China |

| Japan |

| India |

| Southeast Asia |

| Rest Of Asia-Pacific |

| By Package Architecture | SMD (Surface Mount Device) |

| CSP (Chip Scale Package) | |

| Flip-Chip LED Packages | |

| COB (Chip-On-Board) | |

| By Power Class | Low Power ( Less Than 0.5 W) |

| Mid Power (0.5 to 1 W) | |

| High Power (More Than 1 W) | |

| By Application | Exterior Lighting |

| Interior Lighting | |

| Sensing / IR Applications | |

| Others - Applications | |

| By Vehicle Type | Passenger Vehicles |

| Commercial Vehicles | |

| By Country | China |

| Japan | |

| India | |

| Southeast Asia | |

| Rest Of Asia-Pacific |

Key Questions Answered in the Report

How fast is the Asia-Pacific automotive LED package market expected to expand through 2031?

It is projected to rise from USD 1.44 billion in 2026 to USD 1.98 billion by 2031, registering a 6.60% CAGR.

Which country contributes the largest share of regional demand?

China accounted for 54.49% of 2025 revenue due to its large new-energy vehicle output and domestic LED capacity.

Why are chip-scale packages gaining traction in headlamps?

They allow optical heights under 10 millimeters, lower aerodynamic drag, and deliver higher luminance-per-area versus traditional SMDs.

What restrains LED adoption in entry-level vehicles?

Higher system cost relative to halogen assemblies and added thermal-management hardware can raise bill-of-materials three-to-four times.

Which application segment is growing the fastest?

Interior ambient lighting, driven by multi-zone RGB systems in electric vehicles, is forecast for a 7.11% CAGR.

How are suppliers responding to rising price pressure?

Many pursue vertical integration, such as Sanan’s Lumileds acquisition, to cut epitaxy costs and keep packages AEC-Q102 qualified.

Page last updated on: