Aquatic Herbicides Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.05 Billion |

| Market Size (2031) | USD 1.62 Billion |

| Growth Rate (2026 - 2031) | 9.00% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aquatic Herbicides Market Analysis by Mordor Intelligence

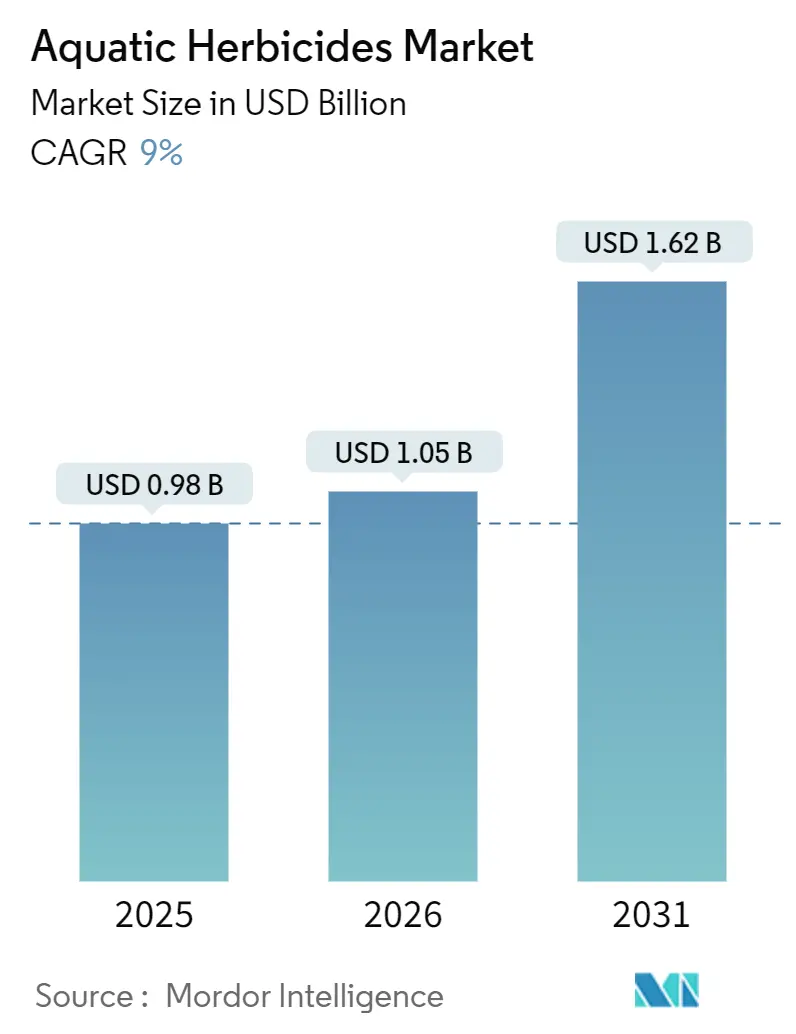

The aquatic herbicides market is projected to grow from USD 0.98 billion in 2025 to USD 1.05 billion in 2026, and is forecast to reach USD 1.62 billion by 2031, marking a 9% CAGR from 2026 to 2031. This growth is driven by increasing invasive-weed outbreaks in hydropower reservoirs, expanding aquaculture acreage in the Asia-Pacific, and expedited approvals for reduced-risk actives. Utilities and irrigation districts prefer chemical control methods, as mechanical harvesting is both capital-intensive and labor-restricted. Formulators are introducing controlled-release granules and chelation carriers, which not only extend efficacy but also comply with stringent toxicology regulations, allowing them to command premium prices. Concurrently, advancements in digital bathymetry and drone-assisted spraying are reducing treatment costs per hectare and enabling submerged injections in deeper reservoirs. As generic suppliers ramp up glyphosate and diquat production, competitive intensity heightens, pushing innovators to stand out with novel action modes, service-centric business models, and ecosystem-focused metrics.

Key Report Takeaways

- By product type, glyphosate captured the largest 42.5% market share for aquatic herbicides in 2025, while imazamox is projected to post the fastest 11.2% CAGR from 2026 to 2031.

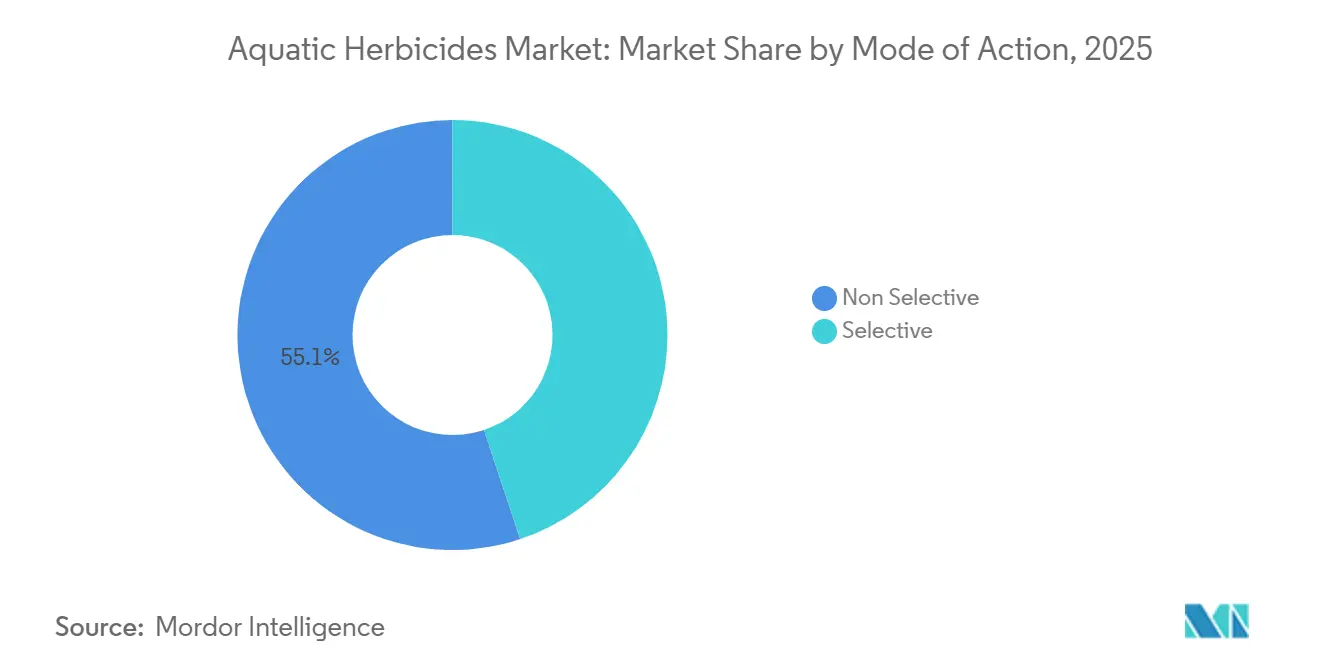

- By mode of action, non-selective actives commanded the largest 55.1% market share for aquatic herbicides in 2025, whereas the selective chemistry is anticipated to log the fastest 9.4% CAGR from 2026 to 2031.

- By application method, foliar treatment held the largest 47% market share for aquatic herbicides in 2025, and submersed injection is forecast to achieve the fastest 10.5% CAGR from 2026 to 2031.

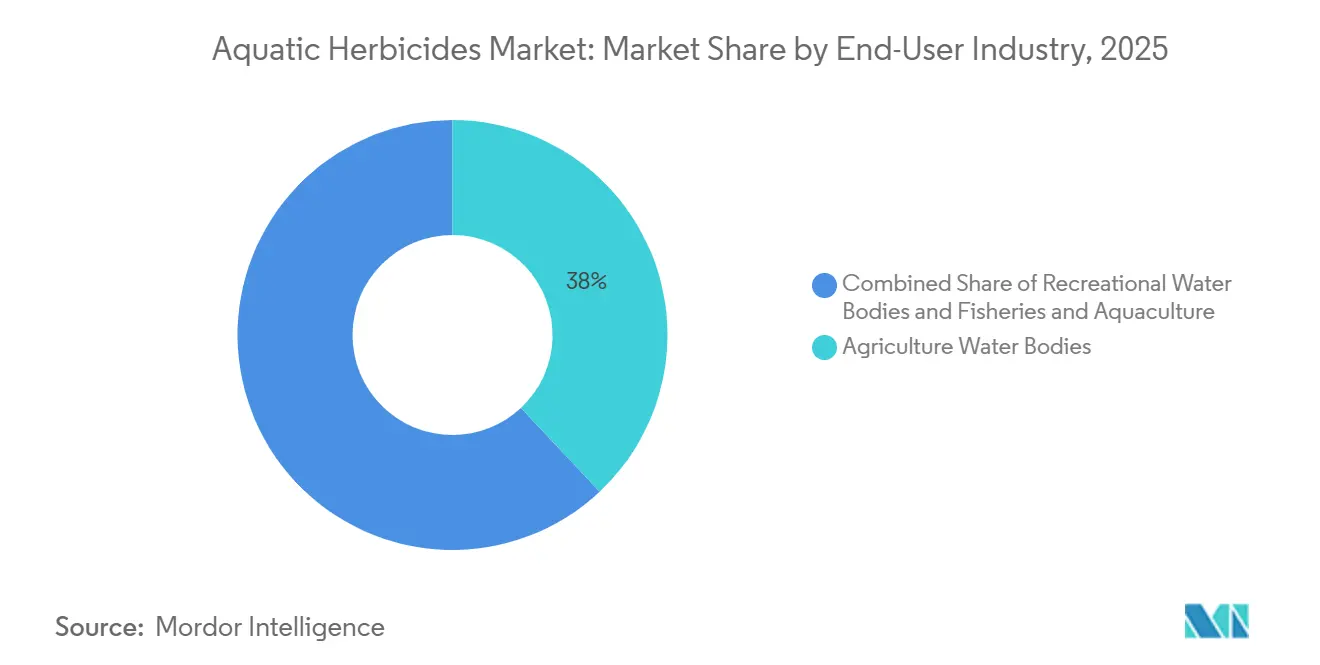

- By end-user industry, agricultural water bodies accounted for the largest 38% market share of aquatic herbicides in 2025, while the fisheries and aquaculture segment is set to grow at the fastest 9.8% CAGR from 2026 to 2031.

- By formulation, liquid concentrates held the largest 46% market share for aquatic herbicides in 2025, while the granular/pelletized is projected to register the fastest 12.1% CAGR from 2026 to 2031.

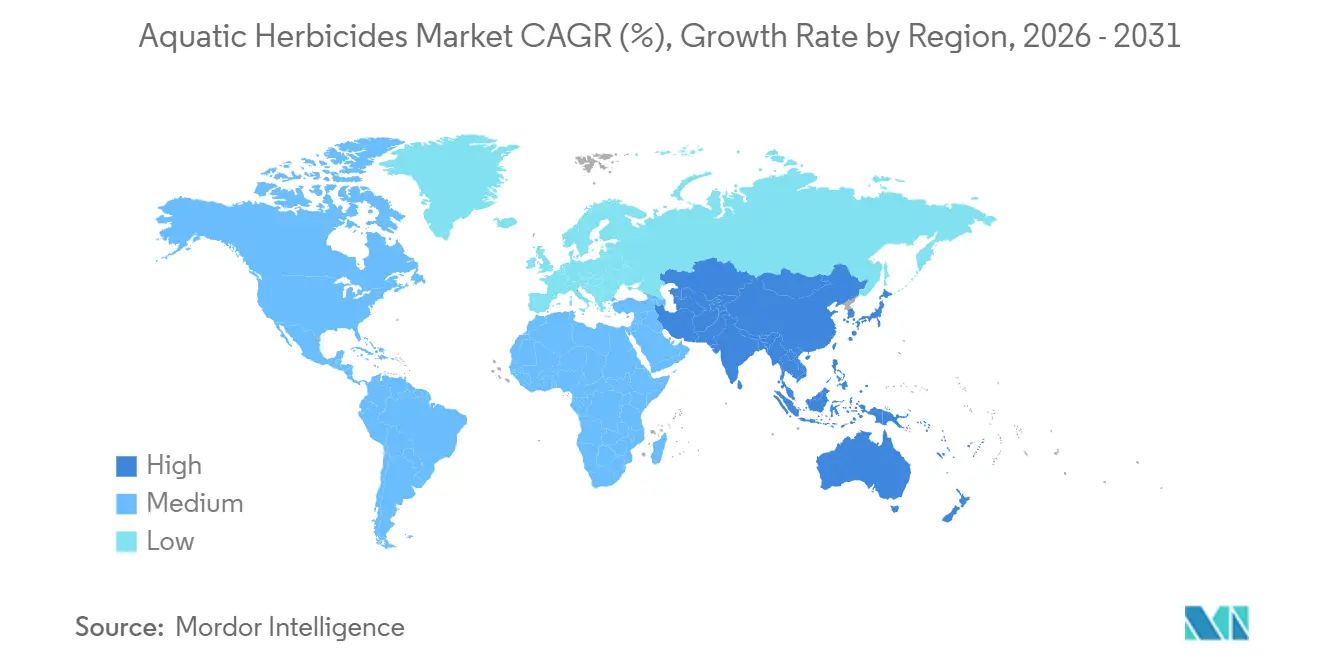

- By geography, North America represented the largest 35% market share for aquatic herbicides in 2025, and Asia-Pacific market is projected to post the fastest 9.5% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aquatic Herbicides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Invasive-weed outbreaks in hydropower reservoirs | +1.8% | Global, acute in Sub-Saharan Africa, South Asia, and South America | Medium term (2-4 years) |

| Faster permitting of reduced-risk actives | +1.5% | North America and Europe, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Eco-tourism and blue-economy funding for lake restoration | +1.2% | North America and Europe, early gains in coastal Southeast Asia | Medium term (2-4 years) |

| Aquaculture acreage expansion driving demand | +2.0% | Asia-Pacific core, secondary in South America and Middle East | Long term (≥ 4 years) |

| Digital bathymetry and drone spraying cutting costs | +1.3% | North America and Europe, pilots in China and Australia | Short term (≤ 2 years) |

| Bio-based chelation carriers improving copper-herbicide efficacy | +1.0% | Global, research and development hubs in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Invasive-Weed Outbreaks In Hydropower Reservoirs

Invasive macrophytes are obstructing turbine intakes and reducing capacity at hydropower assets in emerging regions. For instance, water-hyacinth mats have caused significant operational challenges, prompting the adoption of continuous herbicide programs and mechanical removal. Federal funding initiatives highlight the growing recognition of the threat invasive species pose to power generation and recreation. Operators are shifting from reactive measures to proactive strategies, such as basin-wide mapping, early-detection surveillance, and whole-lake herbicide treatments. This shift is driving demand for efficient chemical solutions and precision delivery systems.

Faster Permitting Of Reduced-Risk Actives

In 2024, the United States Environmental Protection Agency (EPA) approved glufosinate-P for aquatic use, marking the first phosphinic-acid option for submersed treatments [1]Source: United States Environmental Protection Agency, “Glufosinate-P Registration for Aquatic Use,” epa.gov . FMC Corporation intends to introduce Dodhylex in 2026. Harmonized exposure modeling and toxicology endpoints in Europe and North America are expediting approvals, benefiting molecules with selective toxicity and rapid degradation. These advancements are fostering innovation while also increasing competition in premium, compliance-sensitive market segments, where adherence to stringent regulations is critical for market entry and sustainability.

Eco-Tourism And Blue-Economy Funding For Lake Restoration

The National Oceanic and Atmospheric Administration allocated substantial funding for aquatic habitat restoration in 2024–2025. This includes USD 20 million for community-based projects and up to USD 100 million for large-scale habitat restoration initiatives, aimed at supporting ecosystem rehabilitation and improving water quality. In Europe, the EUROLakes project employs real-time sensors, predictive models, and precision dosing to protect water quality essential for tourism. These programs emphasize metrics like clarity, dissolved oxygen, and biodiversity, encouraging herbicide vendors to meet ecological standards.

Aquaculture Acreage Expansion Driving Demand

According to the Food and Agriculture Organization, global aquaculture production reached 94.4 million metric tons in 2022, indicating ongoing growth in farmed aquatic systems worldwide. This expansion has been driven by the establishment of new aquaculture ponds, reservoirs, and coastal farming zones, particularly in the Asia-Pacific and South America regions. In these areas, vegetation control is critical to maintaining oxygen balance and preventing habitat disruption. As aquaculture acreage increases, operators are increasingly utilizing aquatic herbicides to manage excessive plant growth, enhance water circulation, and support higher stocking densities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent toxicological re-registration | -1.2% | North America and Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Price compression from generic glyphosate and diquat oversupply | -1.5% | Global, intense in Asia-Pacific and South America | Short term (≤ 2 years) |

| Preference for mechanical harvesting in recreation lakes | -0.8% | North America and Europe, niche in emerging markets | Medium term (2-4 years) |

| Activist litigation delaying permits | -0.6% | North America and Europe, isolated in Australia and New Zealand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Toxicological Re-Registration

In 2025, the United States Environmental Protection Agency (EPA) updated its Aquatic Life Benchmarks, incorporating revised toxicity thresholds for numerous pesticide active ingredients based on updated ecological risk assessments. Concurrently, the European Food Safety Authority (EFSA) continues to enforce stringent requirements for endocrine disruption and ecotoxicological data under European Union pesticide regulations. These regulations often mandate higher-tier and long-term studies on aquatic species. The evolving regulatory standards have increased data requirements, extended approval timelines, and raised compliance costs for manufacturers, creating significant entry barriers and contributing to supply constraints.

Price Compression From Generic Glyphosate And Diquat Oversupply

The oversupply of generic herbicides has resulted in significant price compression within the aquatic herbicides market, adversely impacting overall profitability. A surge in production capacity and inventory accumulation led to a sharp decline in glyphosate prices. Market reports indicate a 64% drop in global glyphosate prices by early 2025 compared to previous peak levels, driven by oversupply and weak downstream demand [2]Source: Echemi, “Glyphosate Prices Drop by 64%, Major Changes in the Agricultural Input Market,” echemi.com . The increased availability of low-cost generics has heightened competition, compelling manufacturers to operate with tighter margins and restricting price recovery, despite stable demand from the aquaculture and water management sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Selectivity Premiums Sustain Imazamox Uptake

Glyphosate generated the largest 42.5% market share for aquatic herbicides in 2025, while imazamox is projected to log the fastest 11.2% CAGR from 2026 to 2031, pointing to progressive portfolio realignment. Data shows that imazamox can effectively control aquatic weeds at submerged rates of 500 parts per billion and foliar rates of 32 fluid ounces per acre [3]Source: University of Florida IFAS Extension, “Imazamox Efficacy and Application Rates,” edis.ifas.ufl.edu . Investors in aquaculture are gravitating towards imazamox, willing to pay a 30%-50% premium over traditional actives to protect their high-value fish and crustaceans. While triclopyr and 2,4-D cater to specific woody shoreline needs, diquat is facing margin pressures due to an influx of generic alternatives.

Looking ahead, formulators are increasingly combining reduced-risk actives with adjuvants, enhancing uptake efficiency and extending environmental application windows. As the demand for selective molecules rises, distributors are reshaping their inventories to meet tightening residue tolerances. FMC Corporation's upcoming launch of Dodhylex in 2026, a new mode-of-action chemistry, is poised to challenge glyphosate's market dominance. In summary, the aquatic herbicides market is gradually shifting its focus from volume to value, emphasizing high-selectivity actives.

By Mode of Action: Aquaculture Demand Shifts Mix Toward Selective Chemistry

Non-selective herbicides maintained the largest 55.1% market share for the aquatic herbicides in 2025, yet selective formulas will advance at the fastest 9.4% CAGR from 2026 to 2031. Selective options suit integrated rice-fish-vegetable wetlands in Bangladesh, where farmers need to protect both rice seedlings and stock. Regulatory regimes in North America reward selectivity with Reduced Risk designations, accelerating label clearance and shortening market entry.

Conversely, in South America, hydropower and irrigation districts continue to favor non-selective herbicides. Their goal is to optimize conveyance capacity while minimizing costs per hectare. To address the evolving market dynamics, vendors are introducing split-application programs. These combine a lower-rate non-selective knockdown with a subsequent selective application, striking a balance between efficacy, cost, and ecological considerations. Such innovative hybrid strategies ensure that while the market for aquatic herbicides expands its selective offerings, non-selective chemistry remains pertinent.

By Application Method: Submersed Injection Benefits from Precision Mapping

Foliar spray accounted for the largest 47% market share for the aquatic herbicides market in 2025. Submersed injection market size is primed for the fastest 10.5% CAGR from 2026 to 2031 as deep reservoirs adopt bathymetry-guided treatment plans. The University of Florida Extension guides the construction of weighted trailing-hose systems designed to maintain herbicide contact with submerged vegetation for longer durations. This approach enhances herbicide uptake efficiency and reduces the need for frequent reapplications.

Drone platforms are now extending their reach to steep-banked lakes, enabling precise micro-dosing while maintaining compliance with buffer zones near potable water intakes. Suppliers are increasingly bundling herbicide sales with advanced data services, which include weed-density heatmaps and compliance documentation to streamline operations. As these integrated solutions continue to scale, the adoption of submerged injection methods is projected to grow significantly. However, foliar techniques will remain indispensable for effectively managing emergent weeds and drawdown applications, ensuring comprehensive weed control across diverse aquatic environments.

By End-User Industry: Fisheries and Aquaculture Expand Rapidly

Agricultural waters bodies represented the largest 38% market share for the aquatic herbicides in 2025, buoyed by the vast irrigation footprint in Asia-Pacific and North America. Fisheries and aquaculture, however, exhibit the fastest 9.8% CAGR from 2026 to 2031, propelled by intensive shrimp and tilapia systems that now supply the majority of global volume. Selective chemistry adoption here is rapid because residue thresholds can dictate export eligibility.

While the recreational sector grows slowly, its loyalty lies with reduced-risk or low-odor formulations that help maintain property values and align with environmental preferences. Hydropower operators, aiming for swift biomass knockdown to ensure turbine efficiency and prevent operational disruptions, uphold a steady demand for broad-spectrum products. Additionally, the rising global demand for protein and the increasing emphasis on ecological certification are driving the aquatic herbicides industry toward innovative solutions that balance effectiveness with the safety of aquatic ecosystems, ensuring compliance with environmental standards and market needs.

By Formulation: Controlled-Release Granules Accelerate

Liquid concentrates retained the largest 46% market share for aquatic herbicides in 2025, favored for ease of storage and compatibility with legacy equipment. The granular/pelletized granules market size will post the fastest 12.1% CAGR from 2026 to 2031 because bio-based carriers like lignin nanoparticles demonstrate sustained release and reduced leaching. Encapsulation also minimizes peak water concentrations, an attribute prized by regulators and lakefront stakeholders focused on residue optics.

These formulations offer extended activity periods and reduced application frequency, particularly valuable in remote locations where repeated treatments are logistically challenging. Water-soluble concentrates and emulsifiable concentrates serve specialized applications where rapid dissolution or enhanced penetration is required, while tablet and compressed briquette formulations provide convenient dosing for smaller-scale applications. The development of biodegradable polymer carriers is enhancing granular formulation performance while addressing environmental persistence concerns that have historically limited adoption in sensitive aquatic environments.

Geography Analysis

In 2025, North America held the largest market share of 35% in the aquatic herbicides market, driven by robust regulatory frameworks and public funding initiatives. The Great Lakes Restoration Initiative has seen cumulative investments exceeding USD 4 billion, with additional funding provided under the Bipartisan Infrastructure Law for ecosystem restoration. State-level programs further bolster demand. Additionally, the approval of newer herbicide actives, such as florpyrauxifen-benzyl, by the United States Environmental Protection Agency reflects a shift toward more selective and environmentally compliant chemistries.

From 2026 to 2031, the Asia-Pacific region is projected to experience the fastest growth in the aquatic herbicides market, with a CAGR of 9.5%. This growth is attributed to the expansion of aquaculture and water infrastructure. According to the Food and Agriculture Organization, Asia accounts for over 85% of global aquaculture production, with significant contributions from China, India, Indonesia, and Vietnam. The prevalence of invasive aquatic weeds, such as water hyacinth, negatively impacts productivity, increasing the reliance on herbicides. Furthermore, China's strong domestic production of glyphosate and diquat enhances cost competitiveness, although regulatory fragmentation across the region poses challenges for smaller market players.

Europe, South America, the Middle East, and Africa exhibit diverse market dynamics influenced by regulatory and investment trends. In Europe, the European Food Safety Authority enforces stringent pesticide approval protocols, including assessments for endocrine disruption, which can delay the commercialization of new active ingredients. In Brazil, aquatic weed management practices vary by application. Chemical herbicides are commonly used in irrigation canals, while mechanical removal is preferred in environmentally sensitive areas. In Africa and the Middle East, increasing investments in hydropower and water infrastructure, supported by institutions such as the World Bank, are driving the adoption of integrated aquatic vegetation management approaches that combine herbicides with monitoring systems.

Competitive Landscape

In 2025, the market is moderately concentrated, with five major players including Syngenta AG, BASF SE, UPL Limited, Corteva Inc., and Nufarm Limited. SePRO Corporation, leveraging the Reduced Risk status of florpyrauxifen-benzyl, has secured multi-year contracts with utilities and conservation agencies, strengthening its position in the market. FMC Corporation is preparing to introduce its Dodhylex modal chemistry in 2026, marking a strategic focus on patent-protected niches that provide resistance-management benefits and cater to evolving market demands.

Generic producers from China and Indonesia, including Hebang Biotech, Rainbow Agro, and Yonon, are making significant investments in glyphosate and diquat production. These efforts are driving down global price floors, creating competitive pressure on innovators to shift their focus toward advanced formulation technologies, stewardship services, and digital monitoring platforms to maintain their market positions. Research and development investments are increasingly shifting toward bio-based carriers, with peer-reviewed studies on lignin nanoparticle encapsulation paving the way for a premium relaunch of legacy active ingredients, offering enhanced performance and sustainability benefits.

Regional specialists are differentiating themselves by bundling herbicides with localized expertise and rapid response teams, enabling them to address specific regional challenges effectively. This approach is gaining traction among mid-sized lake associations that prioritize agility and tailored solutions over brand recognition.Technology partnerships are transforming service offerings and operational efficiencies. For example, a contract with the United States Army Corps of Engineers highlights the value of GPS-guided submerged rigs, which streamline workflows by integrating bathymetric scans, application logs, and post-treatment efficacy audits. These advanced tools improve precision and effectiveness in aquatic applications.

Aquatic Herbicides Industry Leaders

Syngenta AG

BASF SE

UPL Limited

Nufarm Limited

Corteva Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: SePRO Corporation acquired Earth Science Laboratories to expand its portfolio in water treatment and aquatic ecosystem management, strengthening solutions for invasive weeds, algae, and water quality across lakes and reservoirs.

- December 2022: FMC Corporation entered into a strategic collaboration with Micropep Technology to explore aquatic applications of its herbicide technologies, focusing on sustainable weed control in water-intensive agricultural systems.

- July 2021: BASF SE Canada launched Habitat Aqua herbicide, specifically approved for use in aquatic environments, targeting invasive species such as phragmites and knotweeds in lakes, rivers, and wetlands.

Global Aquatic Herbicides Market Report Scope

Aquatic herbicides control unwanted aquatic plants, algae, and invasive weeds in water bodies like lakes, ponds, rivers, and canals. They maintain water quality, support ecosystems, and ensure efficient water use for irrigation, aquaculture, and recreation. The aquatic herbicides market report is segmented by product type (glyphosate, 2,4-d, imazamox, imazapyr, triclopyr, and diquat), by mode of action (selective herbicides and non-selective herbicides), by application method (foliar application and submersed application), by end-user industry (agricultural water bodies, recreational water bodies, and fisheries and aquaculture), by formulation (liquid concentrates, granular/pellet, tablet/cake, water-soluble powders, and emulsifiable concentrates), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Glyphosate |

| 2,4-D |

| Imazamox |

| Imazapyr |

| Triclopyr |

| Diquat |

| Selective Herbicides |

| Non-Selective Herbicides |

| Foliar Application |

| Submersed Injection |

| Agricultural Water Bodies |

| Recreational Water Bodies |

| Fisheries and Aquaculture |

| Liquid Concentrates |

| Granular/Pelletized |

| Tablet/Compressed Briquettes |

| Water Soluble Concentrates |

| Emulsifiable Concentrates |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Glyphosate | |

| 2,4-D | ||

| Imazamox | ||

| Imazapyr | ||

| Triclopyr | ||

| Diquat | ||

| By Mode of Action | Selective Herbicides | |

| Non-Selective Herbicides | ||

| By Application Method | Foliar Application | |

| Submersed Injection | ||

| By End-User Industry | Agricultural Water Bodies | |

| Recreational Water Bodies | ||

| Fisheries and Aquaculture | ||

| By Formulation | Liquid Concentrates | |

| Granular/Pelletized | ||

| Tablet/Compressed Briquettes | ||

| Water Soluble Concentrates | ||

| Emulsifiable Concentrates | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will aquatic herbicide spending be by 2031?

The aquatic herbicides market size is forecast at USD 1.62 billion by 2031, expanding from USD 1.05 billion in 2026.

Which product type now leads global revenue?

Glyphosate retained the largest 42.5% aquatic herbicides market share in 2025 due to broad-spectrum performance and low cost.

What segment is growing fastest through 2031?

Imazamox is projected to deliver the fastest 11.2% CAGR from 2026-2031 within product types, driven by selective requirements in fisheries and aquaculture.

Which region shows strongest future growth momentum?

Asia-Pacific is projected to record the fastest 9.5% CAGR from 2026-2031, reflecting rapid aquaculture expansion and escalating invasive-weed pressure in irrigation canals.

Page last updated on: