Herbicide Safeners Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

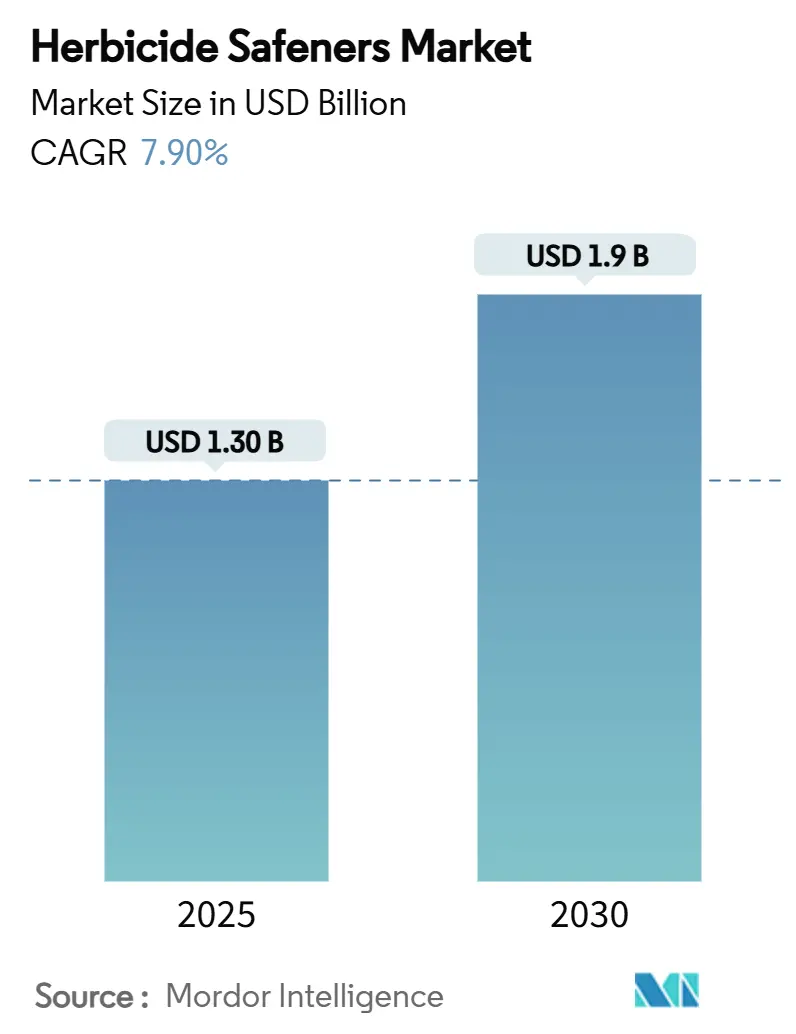

| Market Size (2025) | USD 1.30 Billion |

| Market Size (2030) | USD 1.9 Billion |

| Growth Rate (2025 - 2030) | 7.90% CAGR |

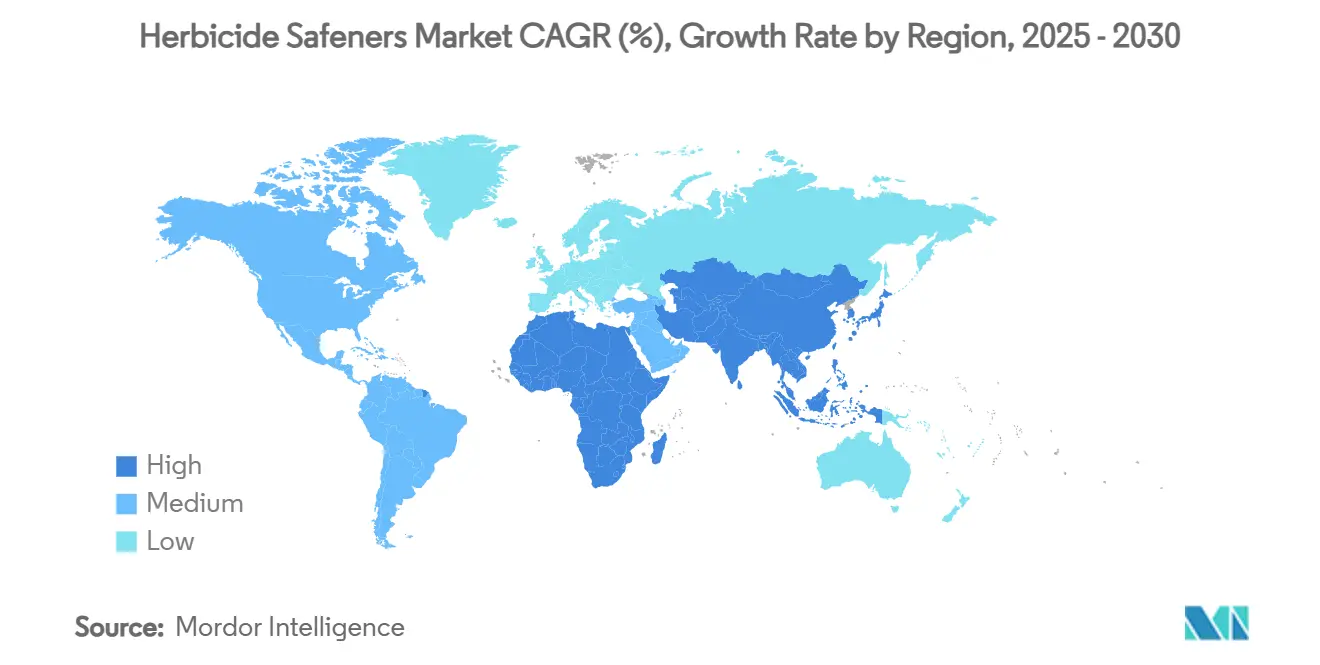

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Herbicide Safeners Market Analysis by Mordor Intelligence

The herbicide safeners market size reached USD 1.3 billion in 2025 and is projected to grow at a CAGR of 7.9% to USD 1.9 billion by 2030. The market expansion is attributed to increasing herbicide-resistant weed populations, regulations promoting precise input usage, and growing adoption of stacked-trait genetically modified crops. Herbicide safeners have become essential components of sustainable weed management programs, enabling farmers to utilize multiple herbicide modes of action while maintaining crop protection. While North America remains the primary market, the Asia-Pacific region is emerging as a significant demand center due to the modernization of agricultural practices. Companies are implementing supply-chain diversification, digital agriculture integration, and patent-protected formulation development to maintain profitability while adhering to environmental regulations.

Key Report Takeaways

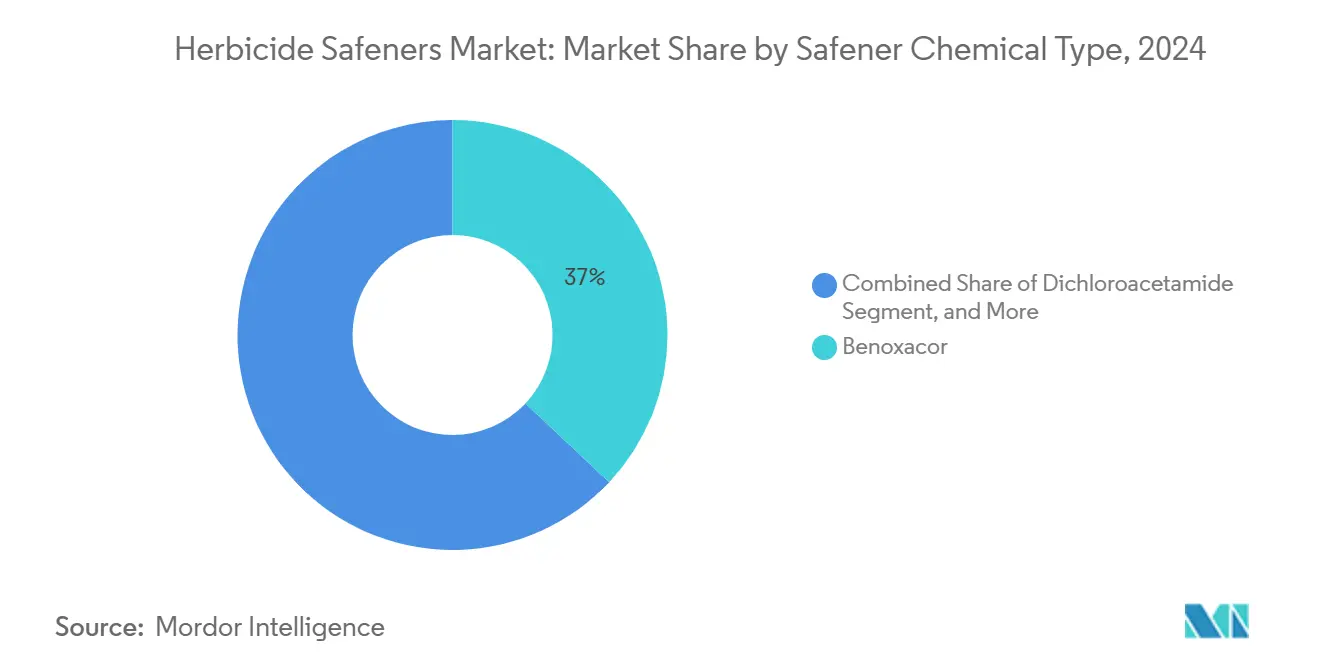

- By safener chemical type, benoxacor retained 37% of the herbicide safener market share in 2024, aryloxyacetic acids led growth at a 10.8% CAGR through 2030.

- By application timing, pre-emergence applications accounted for a 51% share of the herbicide safener market size in 2024, and post-emergence options posted the fastest CAGR of 9.1% from 2024 to 2030.

- By herbicide selectivity, selective herbicides held a 71% revenue share in 2024, while the non-selective segment is anticipated to advance at a 10.0% CAGR through 2030.

- By mode of application, foliar spray accounted for a 48% share of the herbicide safener market in 2024, while seed treatment registered the fastest CAGR of 9.4% from 2024 to 2030.

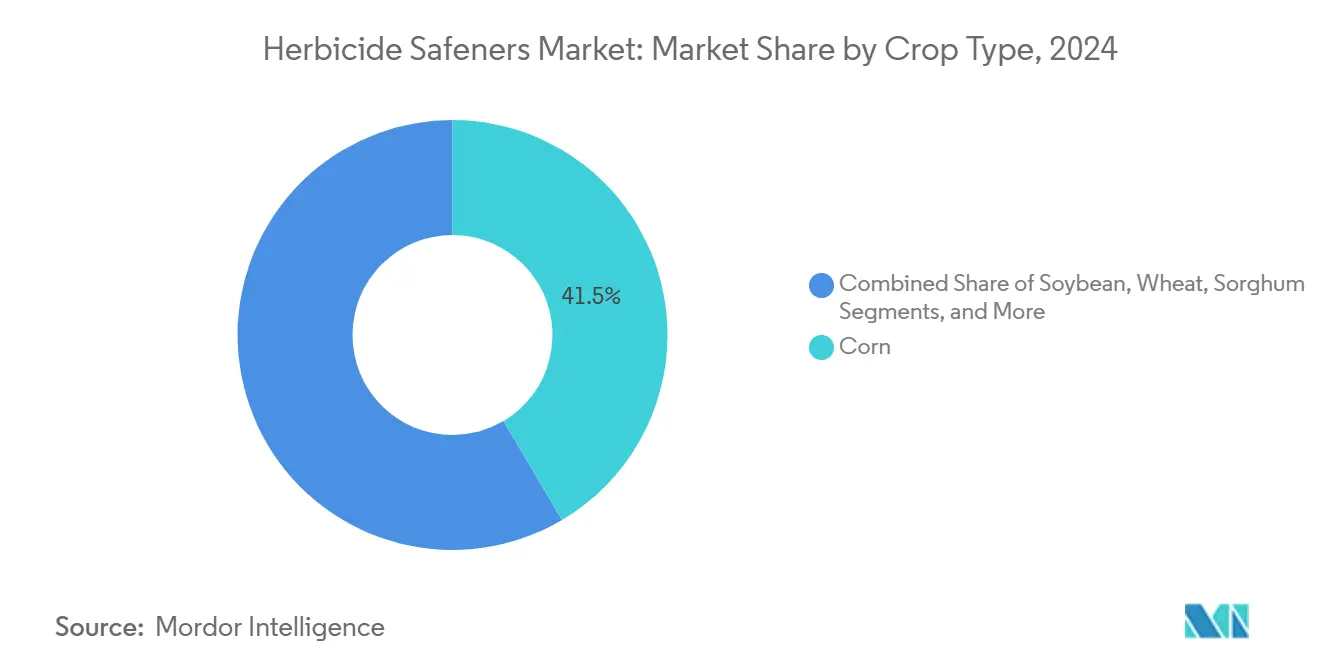

- By crop type, corn accounts for 41.5% of the herbicide safener market in 2024. The soybean segment is projected to grow at the highest CAGR of 10.2% through 2030.

- By geography, North America led with 34.9% revenue in 2024, while Asia-Pacific is poised for the quickest 8.9% CAGR through 2030.

- BASF SE, Syngenta Group, Corteva Agriscience, Bayer AG, and FMC Corporation collectively controlled 63% of global revenue in 2024, signaling moderate consolidation.

Global Herbicide Safeners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated herbicide rotation to mitigate resistance | +1.8% | North America and Brazil | Medium term (2-4 years) |

| Expansion of seed-applied safener formulations | +1.5% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Regulatory pressure favoring lower-dose herbicides | +1.2% | Europe and North America | Long term (≥ 4 years) |

| Growth of stacked-trait GM crops requiring broad-spectrum weed control | +1.4% | North America, and Asia-Pacific | Medium term (2-4 years) |

| Rising adoption of conservation tillage systems | +1.0% | Global | Long term (≥ 4 years) |

| Digital agronomy platforms enabling precise dosing | +0.9% | North America, and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Herbicide Rotation to Mitigate Resistance

Global cases of herbicide resistance exceed 530 and continue to increase, compelling growers to use multiple herbicide classes within a single growing season. Safener-enhanced herbicide rotation programs enable switching between chloroacetamides, Acetolactate Synthase (ALS) Inhibitors, Hydroxyphenylpyruvate Dioxygenase (HPPD) Inhibitors, and Protoporphyrinogen Oxidase (PPO) Inhibitors without damaging crops. FMC Corporation's tetrafluoropropylidene-based Dodhylex active, launched in 2025, demonstrates how combining new modes of action with specific safeners extends product effectiveness and improves weed control economics. These advances primarily benefit North American corn and Brazilian soybean production systems, where herbicide resistance has a significant impact on profitability.

Expansion of Seed-Applied Safener Formulations

The use of seed treatments with safeners is growing due to farmers' preference for precise, low-volume applications. The U.S. Environmental Protection Agency's 2024 spray-drift regulations encourage application methods that minimize off-target movement.[1] U.S. Environmental Protection Agency, “Herbicide Strategy Framework,” epa.gov Polymer coatings and encapsulation technologies improve the release profiles of safeners, providing corn and sorghum with protection against chloroacetamide injury throughout the growing season. Studies demonstrate that these treatments reduce chemical inputs by up to 75% compared to broadcast sprays while maintaining crop yields.[2]American Society of Agricultural and Biological Engineers, “Precision Application Reduces Chemical Loads,” asabe.org

Regulatory Pressure Favoring Lower-dose Herbicides

Regulatory frameworks from the Environmental Protection Agency and European authorities prioritize herbicides that maintain effectiveness while reducing the concentrations of active ingredients. BASF SE's Liberty ULTRA herbicide, which received approval from the Environmental Protection Agency in 2024, reduces glufosinate application rates by 50% through its safener technology and formulation. Companies that demonstrate equivalent weed control with lower application rates can obtain regulatory approvals and establish premium market positions.

Growth of Stacked-trait GM Crops Requiring Broad-spectrum Weed Control

Bayer's Vyconic soybeans exhibit tolerance to five modes of action of herbicides, which increases the complexity of selectivity requirements. The multi-trait systems require sophisticated safener combinations to protect crops from multiple herbicide chemistries. Strategic partnerships between companies, such as Corteva and BASF SE's collaboration on soybean trait stacks, demonstrate the commercial advantages of controlling both traits and their corresponding safeners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited safener registration outside major row crops | −1.5% | Specialty-crop regions | Medium term (2-4 years) |

| High Research and Development costs versus narrow molecule life cycles | −1.2% | Global | Long term (≥ 4 years) |

| Supply-chain dependency on a few specialty intermediaries | −0.8% | Asia-Pacific concentration | Short term (≤ 2 years) |

| Potential ecotoxicity concerns for aquatic organisms | −0.7% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Safener Registration Outside Major Row Crops

According to Environmental Protection Agency data, registering a new safener-crop combination requires investments of several million dollars, which companies rarely pursue for specialty vegetables or orchard crops.[3]U.S. Environmental Protection Agency, “Pesticide Registration Cost Estimates,” epa.gov This high cost often deters innovation and limits the development of safer options tailored to these crops. Although Argentina simplified its equivalency regulations in 2024 to shorten approval timelines, specialty crop growers still face limited access to labeled safener options, which significantly constrains their ability to maximize potential revenue from high-value crops. The lack of sufficient safener options also impacts the overall productivity and profitability of these growers, as they are unable to fully protect their crops from herbicide damage.

High Research and Development Costs Versus Narrow Molecule Life Cycles

The development and commercialization of a new safener demands an investment of over USD 100 million and approximately 10 years of laboratory and field research. This extensive process involves multiple stages, including discovery, formulation, regulatory approvals, and large-scale field trials, all of which contribute to the high costs and lengthy timelines associated with developing new herbicides. BASF SE's decision to cease glufosinate production in Europe by 2024 highlights the financial challenges faced by manufacturers, as shrinking profit margins and rising generic competition limit the recovery of research and development costs prior to patent expiration. These challenges are further exacerbated by the increasing regulatory requirements and the need for sustainable and environmentally friendly solutions, which add complexity and expense to the development process.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Safener Chemical Type: Rising Aryloxyacetic Acid Uptake Bolsters Innovation Pipeline

Benoxacor holds a 37% market share in the herbicide safeners market in 2024, supported by its established track record of crop selectivity in corn and sorghum programs that rely heavily on chloroacetamide herbicides. Its market leadership stems from its versatility in both tank-mix applications and seed treatments. Aryloxyacetic acids, including isoxadifen-ethyl, are experiencing growth at a 10.8% CAGR due to their effectiveness in protecting cereals against Acetolactate Synthase (ALS) Inhibitors and 4-Hydroxyphenylpyruvate Dioxygenase (HPPD) herbicides. The regulatory approval of Corteva Agriscience's cloquintocet-mexyl demonstrates how adaptable regulations enable expanded use across multiple active ingredients.

The increasing occurrence of herbicide-resistant weeds drives the need for innovative safener molecules. Research efforts concentrate on developing compounds compatible with new herbicide modes of action, such as tetflupyrolimet. These market dynamics indicate an expanding range of chemical types in the herbicide safener market during the forecast period, even as benoxacor maintains its significant market position.

By Application Timing: Post-Emergence Momentum Complements Pre-Season Foundation

Pre-emergence applications accounted for 51% of the herbicide safeners market size in 2024, primarily due to their established efficacy and standardized planting schedules. The increasing variability in climate patterns and non-uniform weed emergence are driving the demand for post-emergence applications, which are experiencing growth at a 9.1% CAGR. FMC Corporation's Cadet herbicide demonstrates the efficacy of post-emergence solutions, providing comprehensive velvetleaf control at minimal application rates when initial treatments prove insufficient.

The implementation of real-time field monitoring systems integrated with precision application equipment facilitates targeted post-emergence treatments in specific areas, eliminating the need for whole-field applications. This methodology enables the herbicide safener market to enhance value while maintaining reduced active ingredient volumes, in compliance with environmental regulations.

By Herbicide Selectivity: Non-Selective Segment Accelerates on Conservation Tillage

Selective herbicides constitute 71% of market revenue, driven by the established use of chloroacetamides and 4-Hydroxyphenylpyruvate Dioxygenase (HPPD) in row crops. Non-selective herbicide applications, traditionally limited to burn-down treatments, are experiencing growth at a 10.0% CAGR. Sumitomo Chemical Co., Ltd.'s Rapidicil exemplifies this market evolution through its proprietary safener technology, which enables foliar application in no-till soybeans without compromising seedling integrity.

The expansion of non-selective herbicides correlates with the increased adoption of conservation tillage practices, particularly in South American soybean production regions. As agricultural operations transition from mechanical plowing to chemical-based weed control, the herbicide safener market must develop protective solutions that facilitate flexible crop rotation systems.

By Crop Type: Soybeans Narrow the Gap on Corn Leadership

Corn constitutes 41.5% of the herbicide safeners market size in 2024. The crop's significant presence in the United States, Brazil, and China, combined with its susceptibility to chloroacetamide herbicide injury, maintains consistent demand. The soybean segment is projected to grow at 10.2% annually, driven by the implementation of multi-herbicide tolerance traits, including Vyconic, which requires advanced safener solutions. The expansion of soybean cultivation in South America, alongside the prevalent adoption of conservation tillage practices, increases the requirement for chemical protection.

Wheat, rice, and sorghum maintain stable safener consumption through established agricultural practices in Europe and Asia. While cotton comprises a smaller market share, it demonstrates growth potential due to new herbicide developments addressing resistant pigweed species. This diversified crop distribution in the herbicide safener market protects against individual crop market fluctuations.

By Mode of Application: Seed-Treatment Surge Challenges Foliar Orthodoxy

Foliar sprays accounted for a 48% market share in 2024, attributed to widespread sprayer availability and efficient tank-mix operations. The seed treatment segment demonstrates a CAGR of 9.4%, indicating agricultural producers' increasing adoption of single-pass applications with reduced drift potential. The implementation of variable-rate seeding technology enables precise adjustment of protective coatings by field zone, optimizing safener application costs while ensuring enhanced protection in low-organic-matter soils.

Soil treatments maintain specific applications, particularly in conservation tillage systems, where residual herbicides present phytotoxicity concerns. The combination of artificial intelligence-based prescription systems with controlled-release granular formulations is anticipated to increase the adoption of soil treatments, generating additional growth opportunities in the herbicide safener market.

Geography Analysis

North America accounts for 34.9% of the herbicide safeners market revenue in 2024, driven by extensive corn and soybean rotation practices that require consistent safener use. The Environmental Protection Agency's clear registration procedures and widespread adoption of precision agriculture technologies facilitate faster commercialization. The market also benefits from Canadian wheat and canola farmers who use safeners to expand herbicide options in areas with resistance issues, while Mexico's growing large-scale grain operations create additional demand.

The Asia-Pacific region is projected to grow at an 8.9% CAGR through 2030, leading all regions. China's herbicide usage represents over 98% of total pesticide volume, indicating significant market potential beyond current multinational suppliers such as Bayer AG. India's expanding agrochemical manufacturing capacity, backed by government incentives, improves regional supply chain efficiency. The market further benefits from Australia's extensive grain production and Southeast Asian rice cultivation, which require water-compatible safeners for flooded field applications.

Europe maintains market growth while adhering to strict environmental regulations and steady grain demand. German manufacturers utilize local chemical production capabilities to develop low-dose, safener-enhanced HPPD solutions, while French agricultural cooperatives implement AI-guided application systems to maintain productivity under EU Farm-to-Fork pesticide reduction requirements. In South America, Brazil's expanding soy-corn double-cropping systems drive safener demand, with no-till farming exceeding 35 million hectares. The African and Middle Eastern regions show future growth potential as agricultural mechanization advances and spray infrastructure develops.

Competitive Landscape

The herbicide safeners market demonstrates moderate concentration, with BASF SE, Syngenta Group, Corteva Agriscience, Bayer AG, and FMC Corporation collectively accounting for approximately 63% of market revenue in 2024. BASF maintains its market leadership through extensive chemistry coverage and the 2024 EPA registration of Liberty ULTRA, which combines glufosinate-P with an enhanced safener package to achieve efficacy at half the standard rate. Syngenta strengthens its market position by integrating its Enogen corn hybrids with chemistry and trait-based solutions to enhance customer retention.

Corteva Agriscience expands its market presence through trait-safener co-development initiatives, while FMC Corporation distinguishes itself with novel modes of action, including Dodhylex. Mid-tier companies, including UPL, Nufarm, and Sumitomo, focus on regional formulations and specialty crop segments. Industry partnerships are increasing, as demonstrated by the FMC-Bayer Isoflex collaboration and Aarti Industries' long-term intermediate supply agreements, which address cost inflation and raw material security. Emerging companies such as Greeneye Technology are transforming the market by reducing herbicide usage by approximately 90% through AI vision technology, potentially affecting safener demand through modified application economics.

Research and development partnerships, integration of digital platforms, and shifts in manufacturing locations will influence the herbicide safener market's competitive landscape. Companies that successfully combine patent-protected molecules with data-driven management tools will establish market leadership in the coming decade.

Herbicide Safeners Industry Leaders

BASF SE

Corteva Agriscience

Bayer AG

FMC Corporation

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Syngenta introduced metproxybicyclone, a new herbicide chemical subclass for weed control. The development of metproxybicyclone follows Syngenta's "Safer by Design" approach for sustainable crop protection.

- February 2025: FMC Corporation produced its first commercial batch of Dodhylex active (tetflupyrolimet), a pre-emergence and early post-emergence herbicide with a herbicide safener for broad rice applications globally.

- July 2024: The U.S. Environmental Protection Agency (EPA) strengthened pesticide spray-drift regulations, which increased the demand for seed and soil delivery methods. The EPA's revised pesticide regulations made herbicide application more complex and risk-sensitive, driving the increased use of herbicide safeners.

Global Herbicide Safeners Market Report Scope

| Benoxacor |

| Dichloroacetamide |

| Furilazole |

| Aryloxyacetic Acids |

| Others (Cyprosulfamid, Mefenpyr-diethyl, Fenclorim, and Fluxofenim) |

| Pre-emergence |

| Post-emergence |

| Selective Herbicides |

| Non-selective Herbicides |

| Corn |

| Soybean |

| Wheat |

| Sorghum |

| Rice |

| Cotton |

| Others (Sugarcane, Sugarbeet, Potato, Onion, Citrus, and Cocoa) |

| Foliar Spray |

| Soil Treatment |

| Seed Treatment |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Safener Chemical Type | Benoxacor | |

| Dichloroacetamide | ||

| Furilazole | ||

| Aryloxyacetic Acids | ||

| Others (Cyprosulfamid, Mefenpyr-diethyl, Fenclorim, and Fluxofenim) | ||

| By Application Time | Pre-emergence | |

| Post-emergence | ||

| By Herbicide Selectivity | Selective Herbicides | |

| Non-selective Herbicides | ||

| By Crop Type | Corn | |

| Soybean | ||

| Wheat | ||

| Sorghum | ||

| Rice | ||

| Cotton | ||

| Others (Sugarcane, Sugarbeet, Potato, Onion, Citrus, and Cocoa) | ||

| By Mode of Application | Foliar Spray | |

| Soil Treatment | ||

| Seed Treatment | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the herbicide safener market?

The herbicide safener market size stood at USD 1.3 billion in 2025 and is projected to reach USD 1.9 billion by 2030.

Why are safeners important for stacked-trait GM crops?

Multi-trait crops tolerate several herbicide classes, and tailored safeners prevent phytotoxicity when growers rotate or combine these chemistries within a single season.

Which region is growing fastest in safener demand?

Asia-Pacific is projected to expand at an 8.9 % CAGR to 2030 as China and India intensify herbicide use and modernize weed-control practices.

How concentrated is the competitive landscape?

The top five companies control 63 % of global revenue, indicating moderate consolidation but still leaving room for mid-tier entrants and innovative start-ups.

What are the main challenges facing new safener development?

High Research and Development costs, complex registration requirements for specialty crops, and supply-chain dependence on limited intermediates all dampen ROI for novel molecules.

Page last updated on: