China Herbicide Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

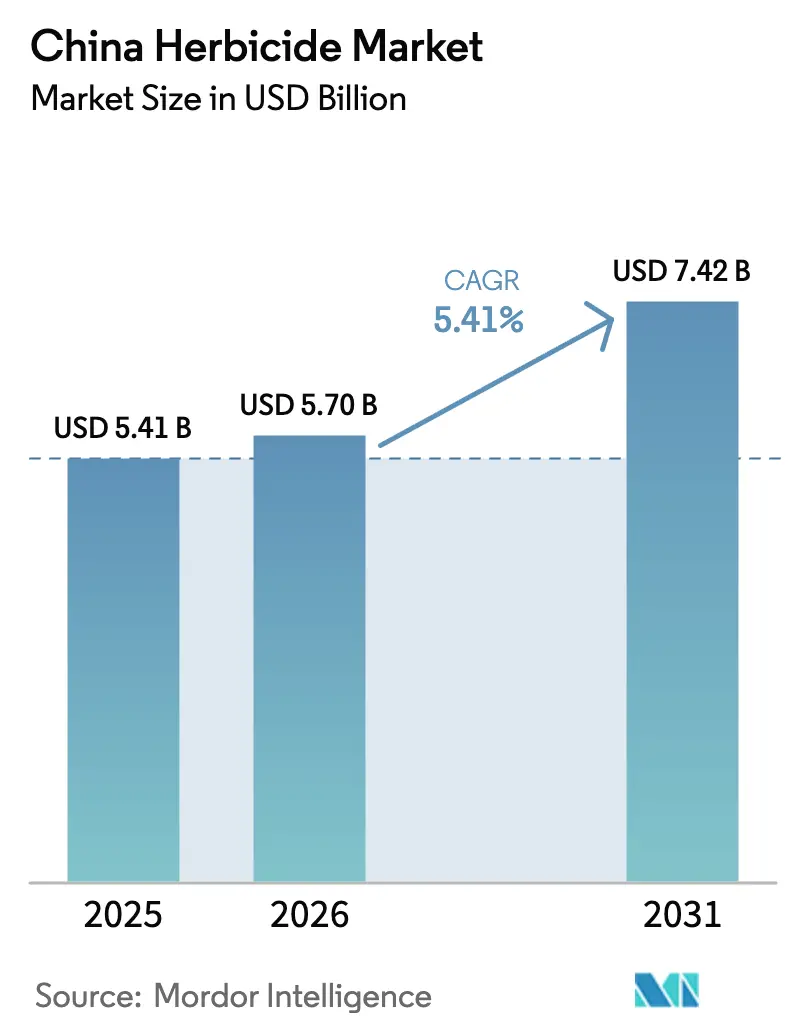

| Base Year Market Size (2025) | USD 5.41 Billion |

| Market Size (2026) | USD 5.7 Billion |

| Market Size (2031) | USD 7.42 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

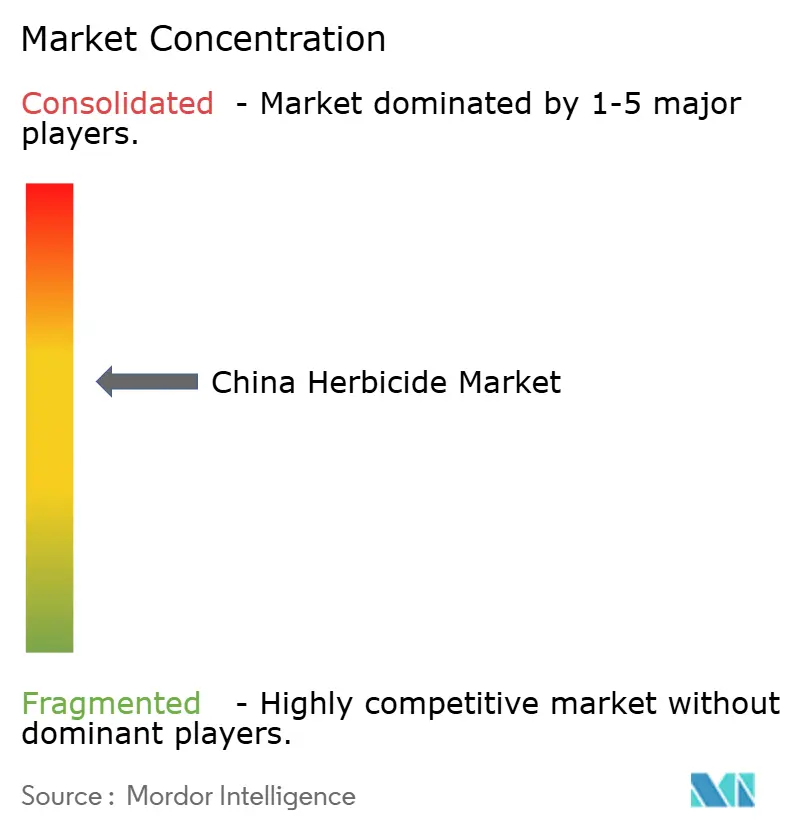

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Herbicide Market Analysis by Mordor Intelligence

The China herbicide market size is expected to grow from USD 5.41 billion in 2025 to USD 5.7 billion in 2026 and is forecast to reach USD 7.42 billion by 2031 at 5.41% CAGR over 2026-2031. Government grain-security mandates, rural mechanization, and expanding specialty-crop acreage underpin steady demand even as environmental oversight intensifies. Subsidy programs that link weed-control spending to yield metrics make herbicides a non-discretionary input for commercial growers. Domestic producers benefit from 20-30 % manufacturing cost advantages that sustain a leading export position, while upgraded “Two High” rules remove legacy actives and channel farmers toward premium, compliant formulations. Digital ag platforms are reshaping last-mile distribution, enabling prescription-based recommendations and data-driven cross-selling that lift average spend per hectare.

Key Report Takeaways

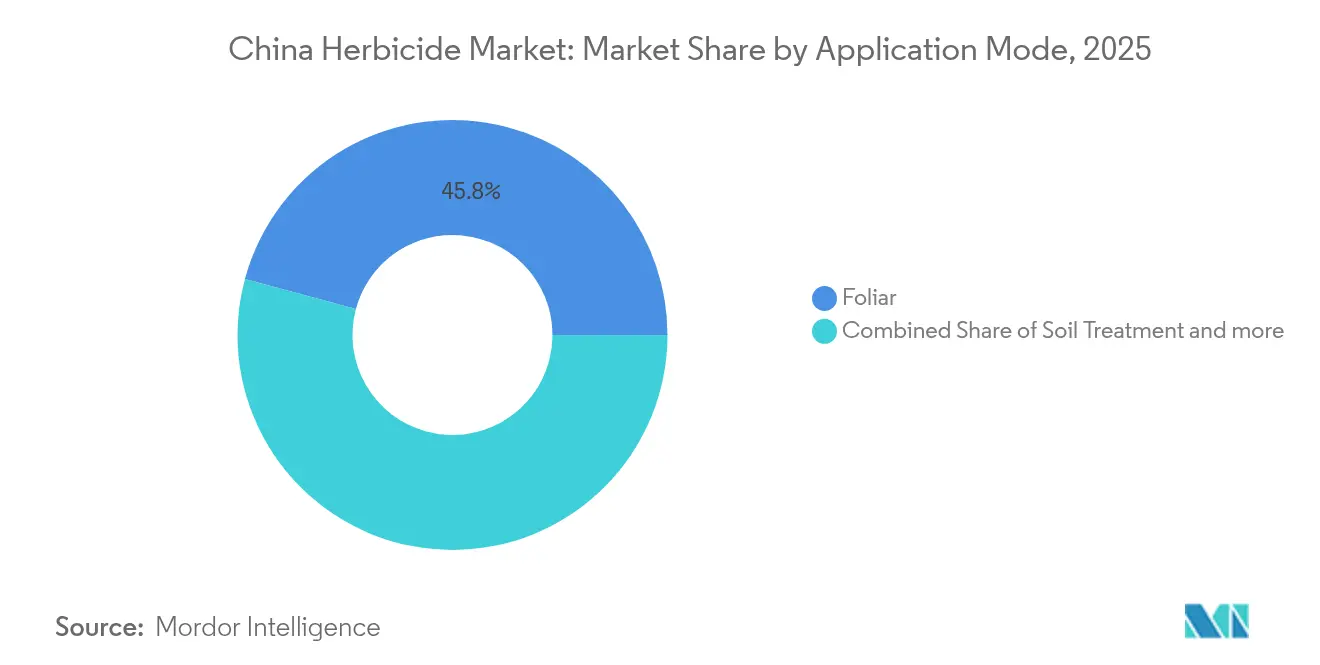

- By application mode, foliar applications commanded 45.80% of the China herbicide market share in 2025, whereas soil treatment is projected to expand at a 5.78% CAGR through 2031.

- By crop type, grains and cereals accounted for 51.45% of the China herbicide market size in 2025, while fruits and vegetables are poised for a 5.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Herbicide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government grain-security programs escalating weed-control spend | +1.2% | National, concentrated in major grain provinces | Medium term (2-4 years) |

| Shift toward post-emergence selective chemistries for labor savings | +0.9% | National, strongest in labor-scarce regions | Short term (≤ 2 years) |

| Expansion of glyphosate-tolerant GM soybean acreage in Heilongjiang | +0.8% | Heilongjiang province, potential national expansion | Long term (≥ 4 years) |

| Domestic production cost advantage driving export demand | +0.7% | Manufacturing hubs in Jiangsu, Zhejiang, and Shandong | Medium term (2-4 years) |

| Digital ag platforms accelerating prescription herbicide sales | +0.6% | Eastern provinces, expanding westward | Short term (≤ 2 years) |

| R&D push for drift-reduction formulations backed by subsidies | +0.5% | National priority in environmentally sensitive areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Grain-Security Programs Escalating Weed-Control Spend

China's food security imperatives create structural demand growth for herbicides through direct government intervention and subsidy mechanisms that prioritize agricultural productivity over cost optimization. The Central Document No. 1 for 2024 explicitly mandates provincial governments to achieve grain self-sufficiency targets, with herbicide application subsidies tied to yield performance metrics rather than environmental considerations. This policy framework creates inelastic demand patterns where farmers prioritize weed control effectiveness over price sensitivity, benefiting premium herbicide formulations and integrated crop protection systems. The government's commitment to maintaining 95% grain self-sufficiency by 2030 necessitates productivity gains on existing arable land, making herbicides essential tools for achieving yield targets without expanding cultivation areas[1]Source: State Council of the People’s Republic of China, “Central Document No. 1 of 2024,” gov.cn .

Shift Toward Post-Emergence Selective Chemistries for Labor Savings

Rural labor scarcity drives fundamental changes in herbicide application timing and chemistry selection, with post-emergence selective products gaining market share through operational convenience and reduced labor requirements. China's rural workforce declined by 15.8 million people between 2019 and 2024, creating acute labor shortages during critical agricultural seasons that favor herbicide solutions requiring fewer application windows. Post-emergence herbicides eliminate the need for precise pre-planting timing and reduce total field operations, making them particularly attractive for aging farm operators and mechanized operations. The trend accelerates the adoption of sulfonylurea and HPPD inhibitor chemistries that offer broad-spectrum weed control with single applications, despite higher per-hectare costs compared to traditional pre-emergence programs.

Expansion of Glyphosate-Tolerant GM Soybean Acreage in Heilongjiang

The Ministry of Agriculture's extension of glyphosate-tolerant soybean trials through 2025 signals likely commercial approval that would fundamentally alter herbicide usage patterns in China's largest soybean-producing region. Heilongjiang province accounts for approximately 40% of China's soybean production, with current herbicide programs relying on complex tank-mix applications and multiple active ingredients to achieve adequate weed control without crop injury. GM soybean approval would simplify weed management to single-active glyphosate applications, potentially reducing total herbicide costs by 25-30% while improving weed control efficacy. The regulatory approval process reflects broader Chinese agricultural policy balancing food security objectives against environmental and trade considerations, with glyphosate tolerance technology offering clear productivity advantages despite public health concerns.

Domestic Production Cost Advantage Driving Export Demand

China's herbicide manufacturing sector leverages integrated chemical production capabilities and favorable regulatory environments to maintain 20-30% cost advantages over international competitors, enabling aggressive export market expansion. Domestic glyphosate production costs average USD 2,800-3,200 per metric ton compared to USD 4,000-4,500 for equivalent international production, creating sustainable competitive advantages in global commodity herbicide markets. The cost structure benefits from vertical integration across the petrochemical value chain, with major producers controlling upstream intermediates and downstream formulation capabilities that reduce supply chain risks and margin volatility. Export demand growth accelerates as international crop protection companies source active ingredients from Chinese manufacturers to maintain competitive pricing in their home markets, creating stable long-term demand that supports domestic capacity expansion and technology investment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent MEE re-registration tightening active-ingredient approvals | -0.8% | National regulatory framework | Long term (≥ 4 years) |

| Periodic raw-material shortages | -0.6% | Manufacturing centers in Jiangsu, Zhejiang | Short term (≤ 2 years) |

| Rising multi-herbicide-resistant weed populations | -0.5% | Intensive cropping regions nationwide | Medium term (2-4 years) |

| Land-consolidation pace lowering smallholder demand growth | -0.4% | Rural areas undergoing mechanization | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent MEE Re-registration Tightening Active-Ingredient Approvals

The Ministry of Ecology and Environment's enhanced re-registration requirements create substantial barriers to market entry and product portfolio expansion, constraining industry growth through reduced active ingredient availability and increased compliance costs. The 2024 implementation of revised "Two High" environmental policies eliminated 18 legacy active ingredients from commercial use, while new registration requirements demand comprehensive environmental fate studies and risk assessments that can cost USD 500,000-1,000,000 per active ingredient [2]Source: Ministry of Ecology and Environment, “Two High Policy Guidelines,” mee.gov.cn. These regulatory changes disproportionately affect smaller manufacturers lacking resources for extensive regulatory submissions, while benefiting established companies with existing registration portfolios and regulatory expertise. The approval timeline for new active ingredients extends to 3-5 years under current procedures, creating market entry barriers that protect incumbent positions but limit innovation adoption and competitive intensity.

Periodic Raw-Material Shortages

Supply chain vulnerabilities for critical herbicide intermediates create recurring production disruptions and margin volatility that constrain market growth through unpredictable cost structures and capacity limitations. Environmental enforcement campaigns in major chemical production regions, particularly Jiangsu province, result in periodic facility shutdowns that reduce intermediate availability and spike raw material prices by 30-50% during shortage periods. Para-cresol shortages particularly affect 2,4-D production, while chlor-alkali supply constraints impact glyphosate manufacturing, creating cascading effects across herbicide product categories. The cyclical nature of these disruptions, typically occurring during environmental inspection periods in Q2 and Q4, creates planning challenges for herbicide manufacturers and distributive pressure throughout the supply chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Mode: Foliar Applications Dominate Usage

Foliar applications command 45.80% market share in 2025, reflecting China's preference for post-emergence weed control strategies that align with labor availability and mechanization capabilities across diverse farming systems. The dominance stems from operational flexibility that allows farmers to assess weed pressure before making treatment decisions, reducing herbicide waste and optimizing application timing based on weather conditions and crop development stages.Foliar herbicide application represents the second-largest segment, offering precise targeting as foliar herbicides directly contact weed foliage. This method is particularly valued for its flexibility in application timing and effectiveness in post-emergence weed control.

Soil treatment methods demonstrate the strongest growth trajectory at 5.78% CAGR through 2031, driven by increasing adoption of pre-emergence programs in mechanized grain production systems where precise planting schedules enable consistent soil application timing. Chemigation applications remain limited to specialized crops and regions with advanced irrigation infrastructure, while Fumigation methods serve niche applications in high-value vegetable production. The growth differential between application modes reflects broader agricultural modernization trends, with Soil Treatment adoption accelerating in regions implementing precision agriculture technologies and standardized cropping systems. Digital agriculture platforms increasingly provide soil application recommendations based on weather forecasting and soil moisture monitoring, reducing application risks and improving herbicide efficacy .

By Crop Type: Grains Drive Volume, Specialty Crops Fuel Growth

Grains and cereals represent 51.45% of herbicide demand in 2025, underpinning market stability through consistent, large-scale applications across China's primary food production systems. This segment benefits from government grain security policies that prioritize yield maximization and provide direct subsidies for crop protection inputs, creating price-inelastic demand patterns that support premium herbicide adoption. The segment's dominance can be attributed to the critical importance of these crops in China's food security strategy and the substantial challenges posed by weed infestations in grain cultivation. Common weeds affecting these crops include barnyard grass, wild oats, green foxtail, and various broadleaf weeds such as purslane and pigweed, necessitating consistent contact herbicide application.

Fruits and vegetables emerge as the fastest-growing segment at 5.56% CAGR through 2031, reflecting dietary diversification trends and export market development that justify higher per-hectare herbicide investments for quality and yield optimization. Pulses and Oilseeds maintain steady demand growth driven by protein crop expansion and cooking oil consumption increases, while Commercial Crops, including cotton, face regional variations based on textile industry dynamics and international trade policies. This accelerated growth is driven by China's position as the world's largest producer of fruits and vegetables, with a per capita consumption rate that exceeds the global average by 1.5 times. The expansion of cultivation areas for fruits and vegetables, coupled with increasing demand for fresh produce, has intensified the need for effective weed management solutions.

Geography Analysis

China's herbicide market exhibits significant regional variation driven by crop patterns, mechanization levels, and economic development that create distinct opportunities and challenges across major agricultural provinces. Heilongjiang province leads consumption through extensive grain production and early adoption of mechanized application systems, with soybean and corn crops driving demand for selective herbicides and precision application technologies.

Regional development patterns reflect China's agricultural modernization priorities and environmental protection requirements that influence herbicide usage patterns and regulatory compliance standards. Eastern provinces demonstrate higher adoption rates for premium formulations and precision application technologies, supported by greater economic resources and technical expertise that justify investments in advanced crop protection systems. Central grain-producing regions focus on cost-effective herbicide programs that maximize yield per unit input cost, creating opportunities for generic manufacturers and commodity formulations.

Environmental regulations vary significantly across provinces based on ecological sensitivity and industrial development priorities, creating complex compliance requirements that favor manufacturers with comprehensive regulatory expertise and flexible production capabilities. The Yangtze River Economic Belt faces stricter environmental controls that limit certain herbicide applications and favor reduced-risk formulations, while northeastern provinces prioritize agricultural productivity and maintain more flexible application guidelines.

Competitive Landscape

The Chinese herbicide market exhibits a moderate, consolidated mix of domestic manufacturing giants and global agrochemical conglomerates, with local players holding significant market share. Companies like NUTRICHEM CO., LTD., Bayer AG, UPL Limited, Corteva Agriscience, and FMC Corporation are maintaining their presence through technological superiority and established brand reputation. The market structure shows moderate consolidation, with the top players controlling a substantial portion of the market share, while numerous smaller players compete in specialized segments and regional markets.

The market is witnessing active merger and acquisition activities as companies seek to strengthen their position and expand their product offerings. Global players are particularly interested in acquiring Chinese companies to gain access to local manufacturing capabilities and distribution networks. Local companies are also pursuing strategic acquisitions to enhance their technological capabilities and expand their international presence. This consolidation trend is reshaping the competitive landscape, leading to the emergence of stronger, more integrated players with enhanced capabilities across the value chain.

For incumbent companies to maintain and increase their market share, focusing on technological innovation and sustainable product development is crucial. Market leaders are investing in developing new active ingredients and improved formulations that offer better efficacy while meeting stringent environmental standards. Building strong relationships with farmers through technical support and integrated pest management solutions is becoming increasingly important. Companies are also strengthening their supply chain resilience and expanding their distribution networks to ensure consistent product availability and market coverage.

China Herbicide Industry Leaders

NUTRICHEM CO., LTD.

Bayer AG

UPL Limited

Corteva Agriscience

FMC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Syngenta Group China announced CNY 1.2 billion (USD 167 million) investment in advanced herbicide formulation facilities in Jiangsu province, targeting nano-encapsulation and controlled-release technologies for premium crop protection applications. The investment addresses growing demand for environmentally compatible herbicide formulations and positions Syngenta to compete in high-margin specialty segments while maintaining manufacturing cost advantages through integrated production capabilities.

- January 2023: Bayer formed a new partnership with Oerth Bio to enhance crop protection technology and create more eco-friendly crop protection solutions.

- January 2022: In the Chinese region of Ningxia, Rainbow opened a new R&D Center, which has strengthened its R&D capabilities to develop new pesticides.

China Herbicide Market Report Scope

Chemigation, Foliar, Fumigation, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type.| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

| Commercial Crops |

| Fruits & Vegetables |

| Grains & Cereals |

| Pulses & Oilseeds |

| Turf & Ornamental |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits & Vegetables | |

| Grains & Cereals | |

| Pulses & Oilseeds | |

| Turf & Ornamental |

Market Definition

- Function - Herbicides are chemicals used to control or prevent weeds from preventing crop growth and yield loss.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms