India Herbicide Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

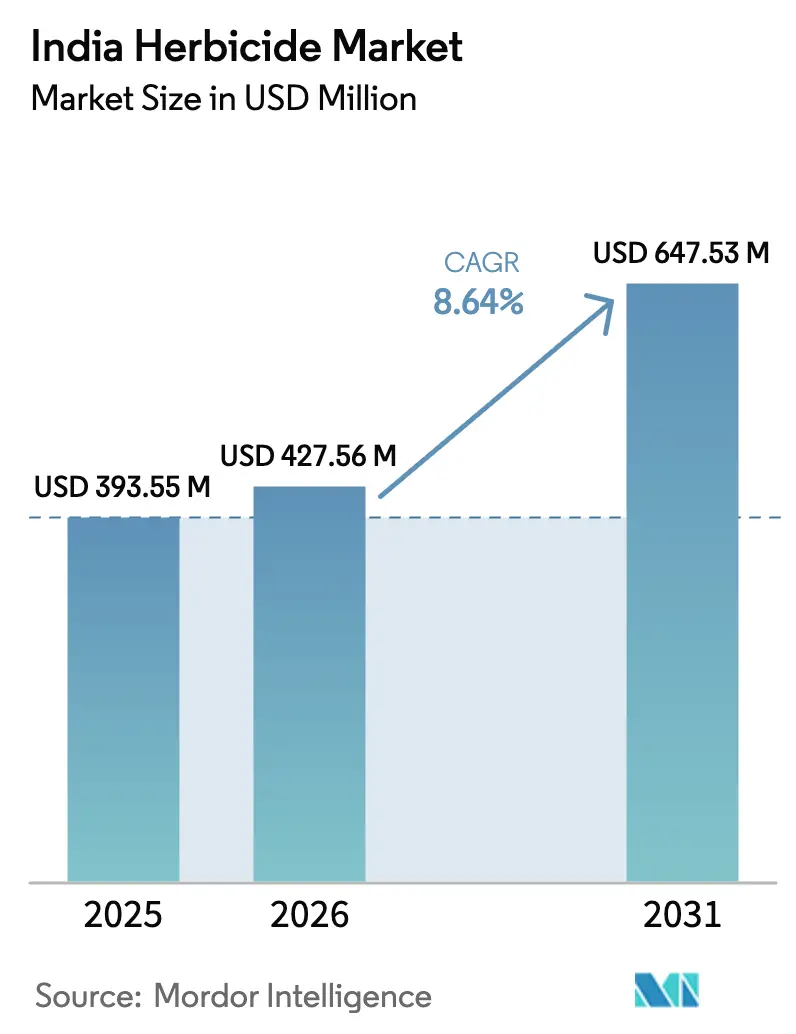

| Base Year Market Size (2025) | USD 393.55 Million |

| Market Size (2026) | USD 427.56 Million |

| Market Size (2031) | USD 647.53 Million |

| Growth Rate (2026 - 2031) | 8.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Herbicide Market Analysis by Mordor Intelligence

The India herbicide market size was valued at USD 393.55 million in 2025 and estimated to grow from USD 427.56 million in 2026 to reach USD 647.53 million by 2031, at a CAGR of 8.64% during the forecast period (2026-2031). This strong trajectory reflects a lasting shift toward chemical weed control as farm labor costs continue to rise, government subsidy structures reward precision spraying, and herbicide-tolerant cotton varieties gain ground. Major multinational suppliers are deepening distribution partnerships to secure volume growth, while domestic formulators concentrate on low-cost offerings that fit small-holder budgets. The regulatory environment under the Central Insecticides Board and Registration Committee (CIBRC) is simultaneously promoting innovation through new active ingredient approvals and constraining older actives through tighter re-registration norms. Drone-enabled precision application, climate-linked weed-pressure spikes, and a policy push for mechanization collectively create a platform for sustained demand across cereals, pulses, and high-value commercial crops.

Key Report Takeaways

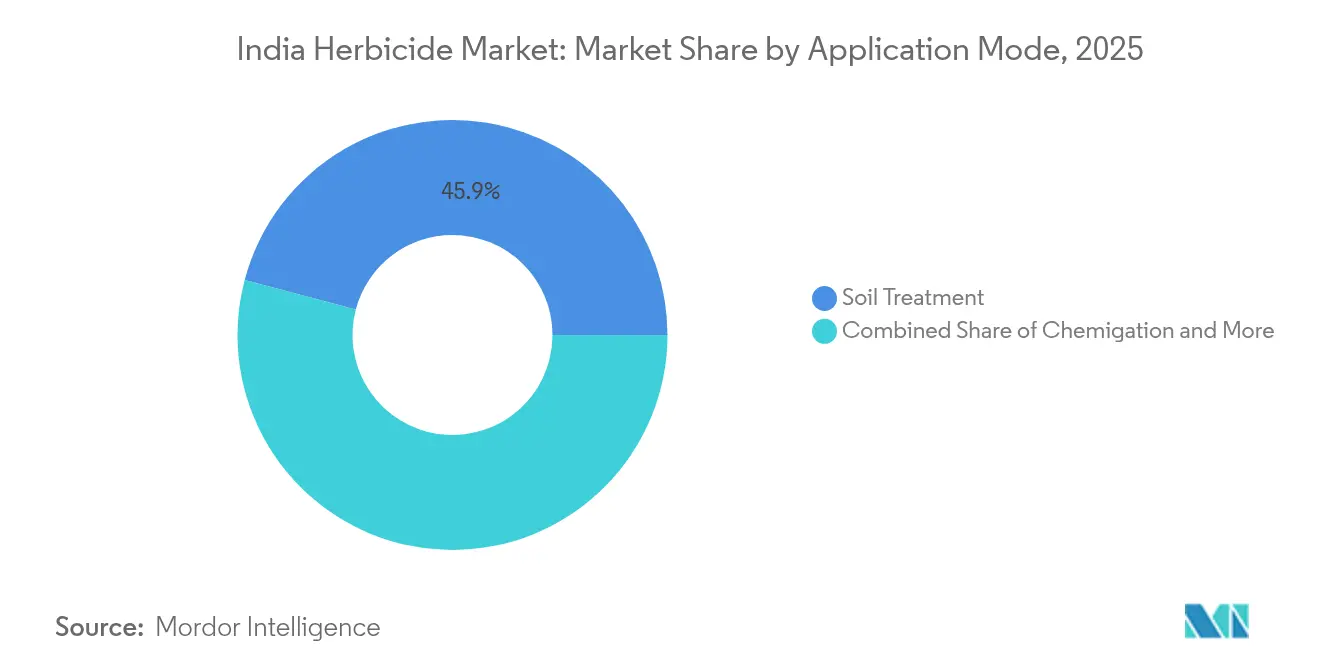

- By application mode, soil treatment led with a 45.88% revenue of the India herbicide market share in 2025, while the same mode is forecast to expand at a 8.91% CAGR through 2031.

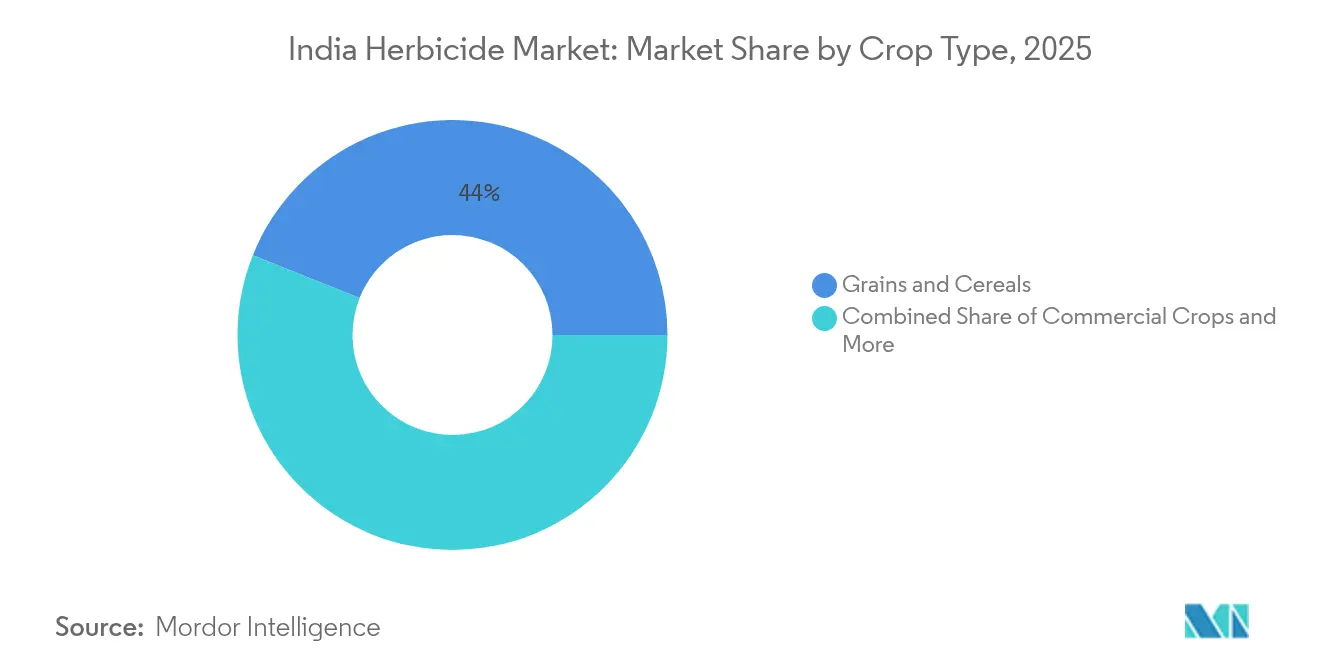

- By crop type, grains and cereals accounted for a 43.95% share of the India herbicide market size in 2025, and commercial crops are advancing at a 9.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Herbicide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread herbicide resistance in weeds | +1.8% | Punjab, Haryana, Maharashtra, and Gujarat | Medium term (2-4 years) |

| Government subsidy reforms favoring post-emergence actives | +1.5% | National, with early gains in Punjab, Haryana, and Uttar Pradesh | Short term (≤ 2 years) |

| Expansion of herbicide-tolerant cotton acreage | +1.2% | Maharashtra, Gujarat, Telangana, and Karnataka | Medium term (2-4 years) |

| Surge in farm-labor costs pushing chemical weed control | +2.1% | Punjab, Haryana, Uttar Pradesh, and Maharashtra | Short term (≤ 2 years) |

| Climate-induced weed-pressure spikes | +1.0% | National, with a higher impact in Northern states | Long term (≥ 4 years) |

| Drone-enabled precision spraying adoption | +0.9% | Punjab, Haryana, Maharashtra, and Gujarat | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Widespread Herbicide Resistance in Weeds

Rising resistance to glyphosate, 2,4-D, and ALS inhibitors is prompting farmers to switch to premium pre-mixes and rotation programs that command higher per-hectare spending. State field trials confirm multiple-site resistance in Phalaris minor and Amaranthus palmeri, pushing demand for newer chemistries cleared by the CIBRC[1]Source: PubMed Central, “Pesticide Pollution in India: Environmental and Health Risks,” pmc.ncbi.nlm.nih.gov. The strongest uptake is visible in Punjab and Haryana wheat-rice systems, where growers now front-load soil-applied herbicides to prevent resistant-weed establishment. Multinational suppliers are capitalizing by bundling resistance-management education with product launches, while domestic formulators pursue generic mixtures to retain price-sensitive customers.

Government Subsidy Reforms Favoring Post-Emergence Actives

Under the National Mission for Sustainable Agriculture, subsidies have shifted toward precision application equipment and post-emergence formulations with lower environmental persistence. In fiscal 2024-25, the Ministry of Agriculture and Farmers Welfare allocated funds to programs that include drone demonstrations for weed control[2]Source: Ministry of Agriculture and Farmers Welfare, “National Mission for Sustainable Agriculture Guidelines,” pib.gov.in. The realignment narrows the cost gap between labor and chemical solutions, accelerating adoption in small and medium holdings across northern irrigated belts. Companies offering drone-ready SC formulations benefit most, as policy incentives cushion the capital cost for service providers.

Expansion of Herbicide-Tolerant Cotton Acreage

Herbicide-tolerant (HT) cotton now covers an estimated 17% of India’s total cotton area, unlocking season-long over-the-top spraying opportunities. Maharashtra and Gujarat growers report up to 25% labor-cost savings after switching to HT seeds paired with broad-spectrum actives. Seed companies forecast additional HT launches pending state biosafety clearances, and CIBRC fast-tracks complementary herbicides with proven crop safety data. As a result, the India herbicide market size for commercial crops is projected to rise faster than that for cereals during 2025-30.

Surge in Farm-Labor Costs Pushing Chemical Weed Control

Daily agricultural wages rose by double digits in several states during 2024, driven by urban migration and higher alternative-sector earnings. Labor scarcity has made manual weeding economically untenable for Punjab’s paddy growers, who now rely on pre-mix soil treatments that reduce field passes and water use. Extension agencies and ag-fintech platforms are reinforcing this transition by offering input credit linked to herbicide packages, deepening chemical weed-management penetration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter registration norms for legacy actives | -1.3% | National, with a higher impact on older formulations | Medium term (2-4 years) |

| Growing counterfeit product circulation | -0.8% | Rural areas across all states, particularly Bihar, Uttar Pradesh | Short term (≤ 2 years) |

| Small-holder fragmentation limiting large-pack sales | -1.1% | National, with a higher impact in Eastern states | Long term (≥ 4 years) |

| Cultural preference for manual weeding in eastern states | -0.6% | West Bengal, Bihar, Odisha, Assam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Registration Norms for Legacy Actives

The Central Insecticides Board and Registration Committee's enhanced scrutiny of existing herbicide registrations creates significant compliance costs and market access barriers that constrain growth in established product categories. The regulatory tightening particularly affects older active ingredients that lack comprehensive environmental fate and toxicology data required under current registration standards, forcing manufacturers to invest in expensive data generation or face product withdrawals. This regulatory evolution reflects India's alignment with international pesticide safety standards and responds to growing environmental and health concerns documented in peer-reviewed research.

Growing Counterfeit Product Circulation

Counterfeit herbicide circulation represents a persistent market distortion that undermines legitimate product sales while creating farmer dissatisfaction with chemical weed control effectiveness. The problem is particularly acute in rural distribution channels where regulatory oversight is limited and price-sensitive farmers may unknowingly purchase substandard products that deliver poor weed control results. This quality control challenge damages the reputation of herbicide technology among farmers who experience crop losses or inadequate weed suppression from counterfeit products, potentially slowing the transition from manual to chemical weed management methods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Mode: Soil Treatment Dominates Pre-Planting Strategies

Soil treatment captured 45.88% of India herbicide market share in 2025 and is projected to expand at a 8.91% CAGR through 2031. The India herbicide market size linked to soil-applied pre-emergence programs is rising fastest in direct-seeded rice and zero-till wheat systems, where single-pass incorporation saves irrigation and labor. Multinational suppliers have introduced new granules that release actives gradually, reducing leaching in light soils and commanding premium prices. Uptake is highest in Punjab and Haryana, aided by state subsidies for zero-till seeders that synchronize herbicide and sowing operations.

Foliar spraying holds the second-largest share, driven by post-emergence needs in cotton and soybeans. Drone services are expanding foliar reach in small holdings where tractor booms remain uneconomical. Chemigation and fumigation together contribute a minor share, but chemigation shows double-digit growth in high-value horticulture clusters of Maharashtra and Gujarat due to water-soluble formulations that maximize fertigation. Companies targeting chemigation co-promote inline filters and injectors to ensure application precision and reduce clogging incidents.

By Crop Type: Commercial Crops Drive Premium Herbicide Adoption

Grains and cereals commanded 43.95% of India herbicide market size in 2025, with rice and wheat dominating volume sales. Yet commercial crops are forecast to post the highest 9.02% CAGR, led by HT cotton acreage and plantation crops such as sugarcane that favor multiple in-season applications. As cotton farmers embrace over-the-top sprays, average spending per hectare surpasses that in cereal fields, widening revenue contribution. Sugarcane growers in Uttar Pradesh now integrate pre-emergence soil treatments with directed post-emergence sprays, doubling herbicide outlays compared with 2023.

Pulses and oilseeds exhibit steady, mid-single-digit growth, constrained by growers’ lower risk appetite in rain-fed tracts. Fruits and vegetables form a niche with the rising adoption of selective actives that meet export-market residue limits. Turf and ornamental remains the smallest slice due to limited urban landscaping budgets, but public-sector park authorities in tier-one cities are trialing low-drift SC formulations to comply with pollution-control norms.

Geography Analysis

Northern India leads the India herbicide market, with Punjab and Haryana collectively accounting for a disproportionate share given their cultivated area. These states benefit from mechanization, direct-seeded rice uptake, and high labor costs that push herbicide substitution. The India herbicide market share within the north is further buoyed by state incentives for drone spraying, including service-rate reimbursements covering up to 50% of per-hectare fees.

Western states Maharashtra and Gujarat rank second in demand, driven by HT cotton, irrigated horticulture, and chemigation-ready infrastructure. Gujarat’s micro-irrigation program covers more than 2.2 million hectares, creating a ready base for water-soluble herbicide sales. Precision-ag service companies in Pune and Ahmedabad run subscription models that bundle satellite weed mapping with variable-rate spraying, locking in product demand for premium actives.

Eastern and Northeastern states remain under-penetrated but represent future growth engines. Manual weeding still dominates in West Bengal and Bihar, yet rising wages and migration trends are eroding the cost advantage. Government extension officers report that demonstration plots using soil-applied pendimethalin achieved 15-20% higher paddy yields, stimulating farmer interest. Assam’s flood-prone fields are testing granular formulations that resist wash-off, potentially widening herbicide applicability in high-rainfall zones.

Competitive Landscape

The India herbicide market exhibits moderate concentration with multinational corporations leveraging technical expertise and established distribution networks to maintain market leadership against cost-competitive domestic players. Market dynamics favor companies that can navigate complex regulatory requirements under the Central Insecticides Board while developing products tailored to India's diverse cropping systems and farm sizes. The competitive environment is increasingly shaped by technology adoption, with companies investing in drone-compatible formulations and precision application systems to differentiate their offerings.

UPL Limited's joint venture with Aarti Industries exemplifies the strategic partnerships emerging to combine manufacturing capabilities with market access, while Dhanuka Agritech's acquisition of Bayer's select herbicide products demonstrates consolidation opportunities in specialized market segments. Dhanuka’s January 2025 acquisition of select Bayer brands strengthened its presence in monocot-selective segments. Multinationals are investing in in-country data generation to secure re-registration of legacy blockbusters, while domestic firms allocate R&D budgets toward drone-optimized SC formulations.

Emerging disruptors include domestic companies focusing on generic versions of off-patent herbicides and specialized formulation companies developing region-specific products for resistant weed management. The use of technology to win market share is evident in companies' investments in digital agriculture platforms that provide farmers with application timing recommendations and weed identification services, creating customer loyalty beyond product performance alone.

India Herbicide Industry Leaders

Bayer AG

Corteva Agriscience

FMC Corporation

PI Industries

UPL Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: PI Industries reported successful commercialization of pyroxasulfone manufacturing following patent expiry, positioning the company to capture market share in the pre-emergence herbicide segment previously dominated by imported products.

- May 2024: UPL Limited announced a joint venture with Aarti Industries to establish integrated herbicide manufacturing capabilities, combining UPL's global market access with Aarti's chemical synthesis expertise to reduce import dependence for key active ingredients.

- January 2023: Bayer formed a new partnership with Oerth Bio to enhance crop protection technology and create more eco-friendly crop protection solutions.

India Herbicide Market Report Scope

Chemigation, Foliar, Fumigation, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type.| Chemigation |

| Foliar |

| Fumigation |

| Soil Treatment |

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental |

Market Definition

- Function - Herbicides are chemicals used to control or prevent weeds from preventing crop growth and yield loss.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms