Algaecides Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.79 Billion |

| Market Size (2031) | USD 4.38 Billion |

| Growth Rate (2026 - 2031) | 9.40% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

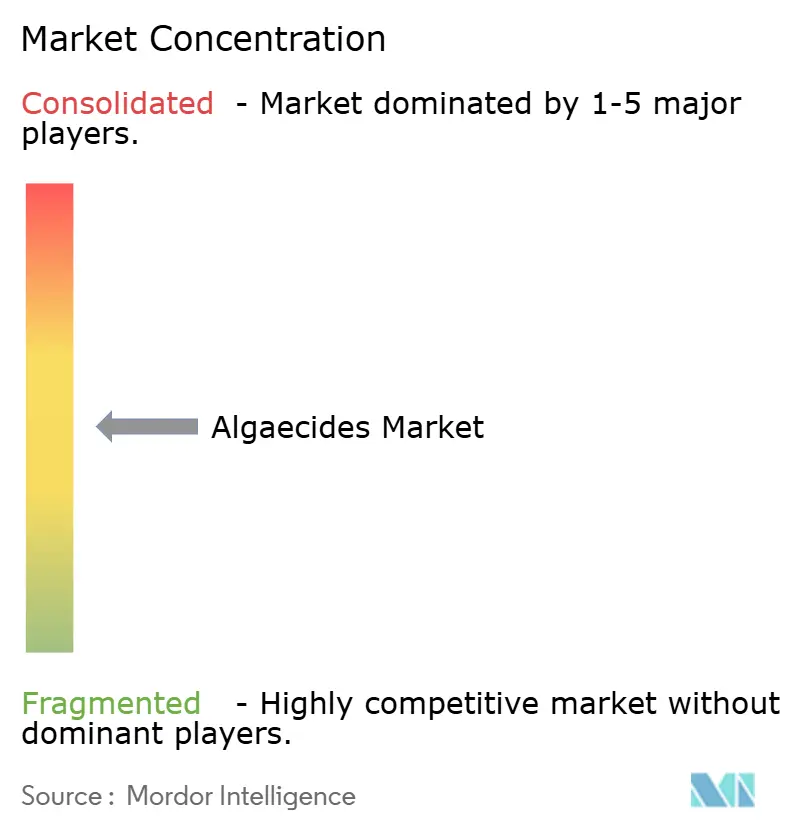

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Algaecides Market Analysis by Mordor Intelligence

The algaecides market size is projected to grow from USD 2.59 billion in 2025 to USD 2.79 billion in 2026 and reach USD 4.38 billion by 2031, registering a CAGR of 9.4% during 2026-2031. Increasing eutrophication is driving irrigators and aquaculture operators to implement year-round algae-control programs to maintain emitter flow rates and dissolved oxygen stability. Copper price fluctuations, exceeding USD 13,000 per metric ton in early 2026, have prompted formulators to mitigate exposure by incorporating peroxide and quaternary ammonium products, thereby expanding the competitive landscape. Regulatory bodies, such as those in California and the European Commission, are imposing stricter copper-discharge limits, boosting demand for products that comply with Total Maximum Daily Load and Industrial Emissions Directive standards[1]Source: Majde Nouri, “Copper Prices Technical Outlook: Copper surge to record highs,” CFI, cfi.trade. North America dominates market revenue due to extensive irrigation networks and stringent Environmental Protection Agency regulations, while the Asia-Pacific region exhibits the fastest growth, driven by recirculating aquaculture systems that reduce water usage by up to 99% while still requiring consistent algae control.

Key Report Takeaways

- By type, copper-based algaecides held the largest 38% of the Algaecides market share in 2025, while peroxide-based market size is forecast to grow at the fastest 9.8% CAGR from 2026 to 2031.

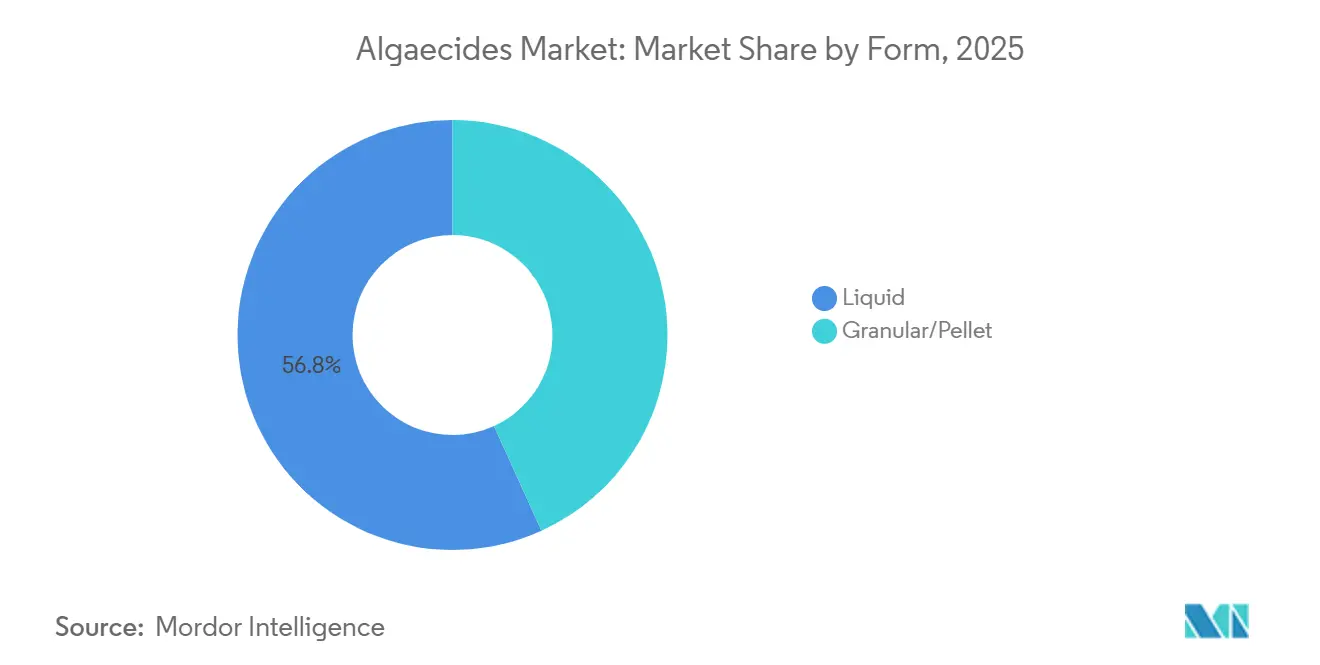

- By form, liquid captured the largest 56.8% of the Algaecides market share in 2025, and the granular/pellet formats market size is set to rise at the fastest 10.7% CAGR from 2026 to 2031.

- By application, irrigation water treatment led the largest 33.5% market share of the Algaecides market in 2025, and the aquaculture ponds and raceways market size is advancing at the fastest 10.5% CAGR from 2026 to 2031.

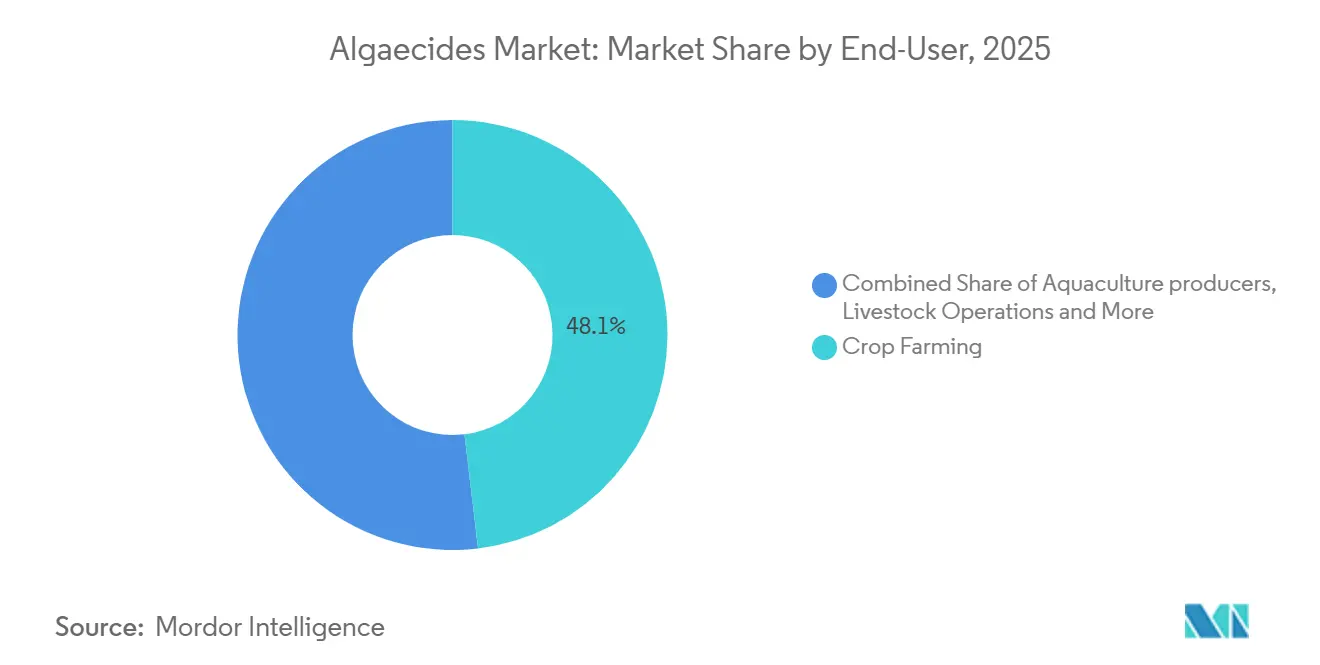

- By end user, crop farming accounted for the largest 48.1% of the Algaecides market share in 2025, whereas the aquaculture producers market is on track for the fastest 9.4% CAGR from 2026 to 2031.

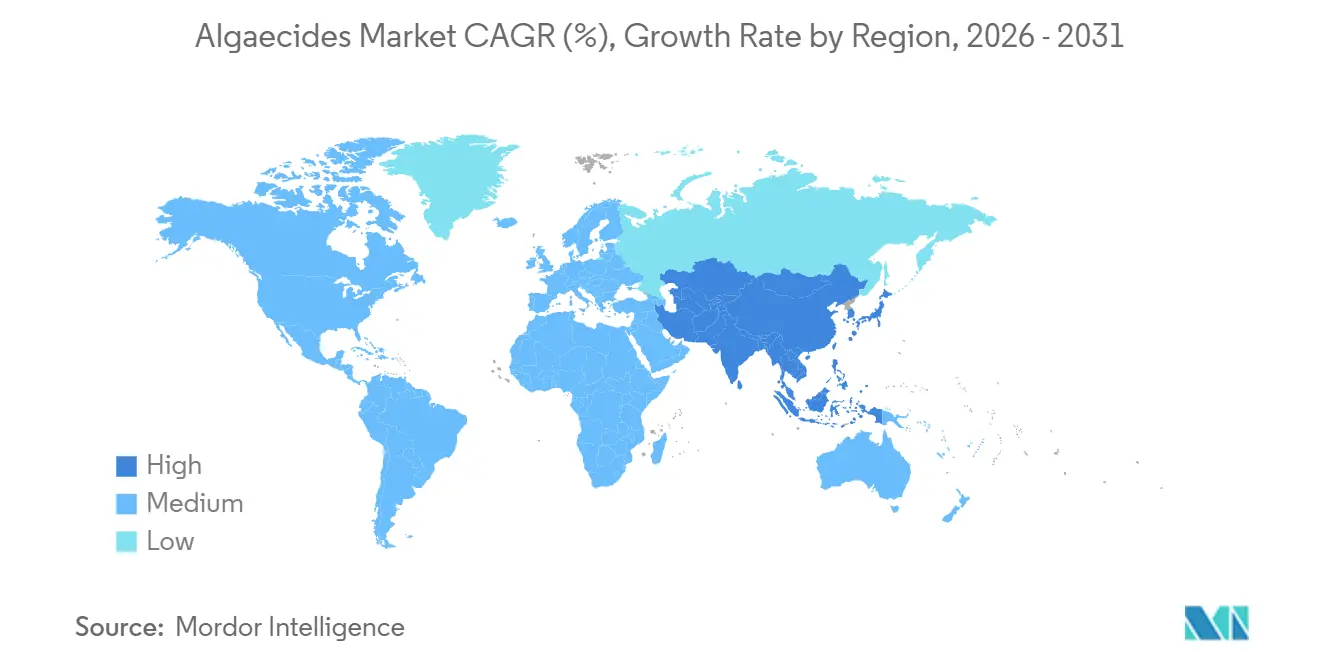

- By geography, North America commanded the largest 43.7% market share in 2025, whereas the Asia-Pacific market size is projected to grow at the fastest 8.5% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Algaecides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating micro-algae blooms in irrigation reservoirs | +1.8% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Expansion of closed-loop aquaculture systems (RAS) | +2.1% | Asia-Pacific core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Rise in copper price hedging driving alternative chemistries | +1.5% | Global | Short term (≤ 2 years) |

| Legalization of non-food cash crops demands clear water quality | +0.9% | North America and South America | Medium term (2-4 years) |

| Integration of algaecide dosing with precision fertigation systems | +1.3% | North America and Europe | Medium term (2-4 years) |

| Insurance rebates for farms with proactive algae-control protocols | +0.6% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Micro-Algae Blooms in Irrigation Reservoirs

Intense heat waves and increased nutrient runoff have created optimal growth conditions for cyanobacteria in reservoirs supplying micro and drip irrigation systems. The Environmental Protection Agency's remote-sensing tools now provide near-real-time bloom alerts for 2,192 lakes. As a result, many growers are transitioning from seasonal shock treatments to full-season maintenance programs that utilize fast-acting algaecides with multi-mode activity. According to California’s 2025 Central Valley survey, eutrophic conditions were identified in nearly half of the monitored lakes, prompting the introduction of new county cost-share grants for copper-free chemistries. Formulators indicate that demand is highest in areas where specialty crops rely on recycled water and require emitter flow to remain within a 2% variance. These agronomic and regulatory changes are shifting algae management from an emergency response to a routine operational expense.

Expansion of Closed-Loop Aquaculture Systems (RAS)

Land-based farms utilizing recirculating aquaculture systems (RAS) recycle up to 99% of process water. However, these closed systems also retain nitrogen and carbon, which contribute to persistent algal mat formation. A 2025 review in Bioresource Technology Reports highlighted that microalgae biofilters can remove up to 90% of dissolved nutrients. Despite this, operators continue to use algaecides to maintain clear raceways and sensors. Shrimp and salmon producers in countries such as China, India, and Ecuador are expanding facilities designed for stocking densities exceeding 100 kilograms per cubic meter, increasing the risk of oxygen depletion if algal blooms are not controlled. Capital lenders mandate documented water-quality protocols before releasing funds, embedding chemical budgets into project financial plans. This structural connection between financing, biosecurity, and daily operations positions RAS growth as a consistent volume driver for the algaecides market.

Rise in Copper Price Hedging Driving Alternative Chemistries

London Metal Exchange three-month copper futures exceeded USD 13,000 per metric ton in early 2026, leading to significant fluctuations in raw material costs for traditional algaecide concentrates. In response, dealers secured forward contracts and increased inventories of peroxide and quaternary ammonium, which provide more stable input costs. These alternatives are also easier to register in watersheds with copper Total Maximum Daily Load (TMDL) restrictions, offering distributors an additional incentive to promote them. Early adopters include large seed companies conducting on-farm irrigation tests, where avoiding regulatory delays associated with copper is critical. As a result, ongoing volatility in base-metal markets functions less as a temporary cost challenge and more as a structural driver for portfolio diversification.

Legalization of Non-Food Cash Crops Demands Clear Water Quality

The cultivation of cannabis and hemp is expanding in states that mandate documented water-quality plans as part of the licensing process. This has created a niche, high-margin demand for Organic Materials Review Institute (OMRI)-listed algaecides. Research from Oregon State University indicates that hemp achieves optimal performance at 80% evapotranspiration. However, over-irrigation promotes biofilm growth, which reduces cannabinoid extraction yields. To address this, growers use peroxide-based blends to maintain clear irrigation lines. In states like California and Colorado, compliance audits by state inspectors often include reviews of water-treatment logs, making algae control an essential operational expense. Given the premium retail pricing of these crops, producers are willing to invest in residue-free inputs to protect their brand value. This intersection of regulatory requirements, agronomic practices, and consumer pricing supports consistent adoption of copper-free solutions among licensed producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of UV and ultrasonic algae-control devices | -1.2% | Global, early uptake in Europe and North America | Medium term (2-4 years) |

| Copper discharge limits in Europe and California are tightening | -1.6% | Europe, California, spill-over to other United States states | Short term (≤ 2 years) |

| Growing consumer push for chemical-free produce labels | -0.8% | North America and Europe | Medium term (2-4 years) |

| Volatility in raw-material availability for peroxide formulations | -0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adoption of UV and Ultrasonic Algae-Control Devices

Non-chemical solutions, such as ultraviolet irradiation and ultrasonic resonance, are attractive to operators adhering to strict discharge permits. However, their capital costs often exceed USD 50,000 for commercial-scale applications. For instance, Hydro Synergy installations in New Zealand salmon farms reduced net fouling within 45 days and lowered manual cleaning costs. Despite these benefits, their performance is influenced by water clarity and flow rates. In areas with high turbidity, ultrasonic energy dissipates rapidly, prompting many users to maintain liquid algaecides as a backup. The return on investment for these devices improves primarily in scenarios where labor costs are high or permit fees impose penalties for chemical discharge. These limitations have slowed the adoption of such devices in broad-acre irrigation and open reservoirs, thereby moderating their overall impact on the algaecides market.

Copper Discharge Limits in Europe and California are Tightening

Regulatory agencies are enforcing stricter copper discharge thresholds, limiting the use of copper-based algaecides and increasing compliance requirements for applicators. The United States Environmental Protection Agency (EPA) has established aquatic life protection criteria, capping chronic copper concentrations in water at 3.1 µg/L to mitigate long-term toxicity to aquatic organisms [2]Source: United States Environmental Protection Agency, “Aquatic Life Water Quality Criteria for Copper,” epa.gov. These limits are being progressively adopted and tightened at state and regional levels, particularly for sensitive water bodies. As compliance standards become more stringent, users are required to reduce copper usage and transition to alternative chemistries, leading to increased formulation complexity and operational challenges within the algaecides market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Copper Holds Ground as Peroxide Accelerates

Copper-based algaecides accounted for the largest 38% of the algaecides market share in 2025, primarily due to their broad-spectrum control at a cost suitable for large irrigated farms. Their dominance continues to influence the overall algaecides market, favoring traditional chemistry, even as California and the European Commission implement stricter discharge limits. Chelated copper complexes and slow-release granules enhance residual activity, enabling applicators to comply with stricter water-quality regulations without requiring significant changes to existing equipment. Larger distributors are bundling copper concentrates with herbicides and insecticides, leveraging procurement contracts that favor established active ingredients.

The algaecides market size for peroxide is projected to grow at the fastest CAGR of 9.8% from 2026 to 2031. Their inclusion in the Organic Materials Review Institute (OMRI) listings and copper-free residue profiles enables these formulations to penetrate specialty crops, golf courses, and recirculating aquaculture systems, where discharge permits limit the use of metals. Quaternary ammonium and endothall products cater to niche applications, such as ponds and hatcheries, requiring rapid knockdown with low mammalian toxicity. Suppliers focusing on stabilizing peroxide for extended shelf life and prolonged contact time are projected to increase margins, driving incremental market growth within premium price segments.

By Form: Liquids Dominate, Granular Solutions Gain Momentum

Liquid accounted for the largest 56.8% of the market share for the projected 2025 revenue due to its seamless flow through fertigation pumps and inline injectors, enabling growers to adjust dosage rates in real time via smartphones. The compatibility of this format with precision controllers allows large orchards and greenhouse complexes to synchronize algae control with nutrient schedules, reducing waste and labor. Additionally, liquids disperse quickly in raceways, a critical factor for super-intensive shrimp farms that cannot tolerate dissolved oxygen dips lasting more than a few minutes. The preference for concentrate drums, which require less shelf space compared to bags or pellets, is further supported by tight inventory turnover at dealer warehouses.

The algaecides market size for granular/pellet is growing at the fastest CAGR of 10.7% from 2026 to 2031, driven by adoption among homeowners’ associations, turf managers, and municipal lake crews due to their ease of broadcasting. Slow-release coatings provide controlled release of active ingredients over several weeks, reducing the frequency of site visits and minimizing insurance liabilities associated with tanker handling. Encapsulated copper granules also help lower peak effluent concentrations, enabling operators to meet Total Maximum Daily Load (TMDL) limits without compromising efficacy. Additionally, formulators are testing effervescent tablets that dissolve upon contact, combining the convenience of granular formulations with the rapid action of liquids, which could unlock new opportunities in the mid-size reservoir segment of the algaecides market.

By Application: Surface Water Leads while Aquaculture Surges

In 2025, irrigation water treatment accounted for the largest 33.5% market share for the algaecides market, encompassing canals, reservoirs, and municipal water sources where filamentous blooms disrupt downstream applications. State pesticide permits mandate pre- and post-treatment monitoring, prompting applicators to prefer well-documented product labels that streamline compliance processes. The adoption of integrated sensor platforms enables agencies to initiate dosing based on chlorophyll thresholds, reducing chemical usage and improving public transparency. This approach ensures that this high-visibility segment remains within regulatory boundaries.

The algaecides market size for aquaculture ponds and raceways is projected to exhibit the fastest growth, with a CAGR of 10.5% from 2026 to 2031. Recirculating aquaculture systems concentrate nutrients, leading to plankton blooms. Operators prioritize rapid and predictable suppression to meet export residue limits and maintain dissolved oxygen levels within strict parameters, even at higher costs. Additionally, livestock drinking water, ornamental ponds, and runoff ditches experience episodic demand surges during heat waves or following fertilizer applications, when nutrient influx triggers blooms. These varied applications contribute to the diversification of the algaecides market across different climates and budgetary constraints, mitigating the impact of downturns in any single segment.

By End User: Crop Farming Commands Volume, Aquaculture Drives Growth

In 2025, crop farming accounted for the largest 48.1% of the market share for the algaecides market, primarily due to the challenges posed by long conveyance lines and the tendency of drip emitters to clog quickly in warm, nutrient-rich water. Commodity producers prioritize low-cost active ingredients and negotiate truckload pricing, which establishes the baseline size of the Algaecides market. Their emphasis on maintaining flow rather than achieving full sterilization sustains the relevance of copper, even during price fluctuations. Additionally, precision dosing minimizes residues that could damage high-value crops such as strawberries and lettuce.

The algaecides market size for aquaculture producers is projected to grow at the fastest 9.4% from 2026 to 2031, driven by inland shrimp and salmon facilities that cannot risk partial die-offs caused by cyanotoxin spikes. Livestock and turf managers contribute a smaller but consistent demand, often guided by veterinarians or golf-course superintendents who prioritize ease of handling and adherence to environmental stewardship certifications, such as Audubon Sanctuary standards. This diverse buyer base compels suppliers to offer multiple packaging sizes and technical service models, thereby expanding the commercial reach of the Algaecides market.

Geography Analysis

North America accounted for the largest 43.7% of the algaecides market share in 2025, primarily due to extensive irrigation systems spanning from California to Texas. These systems depend on reservoir storage, which warms rapidly during summer, fostering algal blooms that restrict emitter flow. The Environmental Protection Agency’s 2026 Pesticide General Permit requires compliance with the Biotic Ligand Model, encouraging growers to adopt precision injectors that adjust copper levels based on water hardness and pH readings. In Canada, salmon and trout hatcheries in British Columbia are experimenting with hydrogen-peroxide pulses to clear raceways without leaving residues. Meanwhile, municipal lake districts in the Great Lakes region are deploying ultrasonic rafts to meet public demand for chemical-free recreational waters.

The Asia-Pacific region is advancing at a fastest CAGR of 8.5% from 2026 to 2031, driven by China’s target of achieving 1.55 million metric tons of shrimp production and India’s increasing inland carp farming systems. Super-intensive biofloc tanks and recirculating systems are reducing freshwater usage but concentrating nutrients, which sustain continuous algal blooms, making algaecide application a routine part of aquaculture management. Regulatory frameworks in the region remain inconsistent. For instance, China imposes limits on copper residues in edible tissues, while India’s Coastal Aquaculture Authority reviews chemical usage during license renewals. This regulatory environment provides larger multinational companies with comprehensive dossiers an advantage in obtaining local approvals.

Europe, South America, the Middle East, and Africa collectively account for the remaining market share, each influenced by distinct factors. In Europe, the Industrial Emissions Directive imposes stricter controls on copper discharge, leading to increased adoption of peroxide in Dutch greenhouse canals and Norwegian smolt hatcheries. In South America, Ecuador’s shrimp ponds, producing 1.49 million metric tons annually, predominantly use conventional copper due to its low monitoring costs [3]Source: Aquaculture Magazine, “Global Scenario of Shrimp Industry: Present Status and Future Prospects,” aquaculturemag.com. However, processors exporting to the United States often employ peroxide flushes before harvest to meet buyer audit requirements.

Competitive Landscape

The algaecides market is moderately concentrated, with five key companies, including BASF SE, FMC Corporation, UPL Limited, Nufarm Limited, and SePRO Corporation, holding a notable share of copper and peroxide registrations worldwide in 2025. Despite this, their combined market share is moderate, preventing the market from being categorized as an oligopoly. This creates opportunities for regional specialists to succeed. SePRO Corporation's acquisition of Green Eyes in 2025 has strengthened its position in niche segments such as golf course and lake management.

Smaller companies, including BioSafe Systems and Innovative Water Care, are focusing on stabilized peroxide and quaternary ammonium blends that offer shorter worker reentry intervals. These innovations have enabled them to capture market share in high-margin specialty crops. Meanwhile, device manufacturers like Hydro Synergy and LG Sonic are promoting ultrasonic raft systems that eliminate chemical discharge, positioning their products as environmentally sustainable solutions. These systems, which require significant capital investment, rely on strong after-sales support.

Regulatory compliance has emerged as a key differentiator in the algaecides market. The Environmental Protection Agency’s electronic reporting requirements under the 2026 Pesticide General Permit compel suppliers to provide tools such as dosing calculators and sample log templates to avoid product substitution. In Europe, the accelerated re-registration process under the Industrial Emissions Directive benefits companies capable of financing multiyear dossier updates and toxicology reviews. Additionally, price volatility in copper and peroxide feedstocks gives an advantage to formulators with diversified procurement strategies, ensuring their priority placement.

Algaecides Industry Leaders

BASF SE

UPL Limited

Nufarm Limited

SePRO Corporation

BioSafe Systems, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SePRO Corporation has acquired Green Eyes LLC to enhance its capabilities in aquatic and lake management solutions. This acquisition adds slow-release copper granule technologies to SePRO Corporation’s product portfolio, improving its offerings for algae and invasive species control, especially in golf course water features.

- June 2024: BioSafe Systems, LLC collaborated with Veolia Water Operations to deploy GreenClean Liquid 5.0, a fast-acting algaecide, for reservoir treatment. This proactive approach effectively reduced cyanobacteria levels and enhanced water quality, showcasing its efficacy in large-scale water systems.

Global Algaecides Market Report Scope

Algaecides are substances designed to control, prevent, or eliminate algae growth in water systems, including lakes, ponds, irrigation channels, and industrial water bodies. They function by disrupting algal cell processes or altering growth conditions, thereby maintaining water quality, preventing oxygen depletion, and ensuring safe usage in agriculture, aquaculture, and recreational settings. The algaecides market report is segmented by type (copper-based, quaternary ammonium compounds, peroxide-based, and other types), by form (liquid, and granular/pellet), by application (irrigation water treatment, aquaculture ponds and raceways, livestock drinking water, ornamental and golf course ponds, and field runoff ditches), by end user (crop farming, aquaculture producers, livestock operations, and turf and ornamental growers), and by geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The market forecasts are provided in terms of value (USD).

| Copper-based |

| Quaternary Ammonium Compounds |

| Peroxide-based |

| Other Types |

| Liquid |

| Granular/Pellet |

| Irrigation Water Treatment |

| Aquaculture Ponds and Raceways |

| Livestock Drinking Water |

| Ornamental and Golf Course Ponds |

| Field Runoff Ditches |

| Crop Farming |

| Aquaculture Producers |

| Livestock Operations |

| Turf and Ornamental Growers |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Italy | |

| United Kingdom | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Type | Copper-based | |

| Quaternary Ammonium Compounds | ||

| Peroxide-based | ||

| Other Types | ||

| By Form | Liquid | |

| Granular/Pellet | ||

| By Application | Irrigation Water Treatment | |

| Aquaculture Ponds and Raceways | ||

| Livestock Drinking Water | ||

| Ornamental and Golf Course Ponds | ||

| Field Runoff Ditches | ||

| By End User | Crop Farming | |

| Aquaculture Producers | ||

| Livestock Operations | ||

| Turf and Ornamental Growers | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| United Kingdom | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the market size and forecast growth rate for the algaecides market from 2026 to 2031?

The algaecides market size is projected to grow from USD 2.79 billion in 2026 and reach USD 4.38 billion by 2031, registering a CAGR of 9.4% during 2026-2031.

Which product type is expanding fastest inside the market?

Peroxide-based formulations are growing at a 9.8% CAGR through 2031, driven by copper-discharge limits.

Why is Asia-Pacific the fastest-growing regional segment?

Rapid adoption of recirculating aquaculture systems and biofloc technologies concentrates nutrients that require constant algae control, lifting regional demand.

How are regulators influencing product choice in North America?

Environmental Protection Agency Biotic Ligand Model rules cap copper discharge, so many users integrate precision injectors and shift toward peroxide blends.

What technologies outside chemicals are challenging traditional algaecides?

Ultraviolet irradiation and ultrasonic resonance units offer residue-free control, especially where discharge permits are strictly required.

Page last updated on: