Antioxidants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.83 Billion |

| Market Size (2031) | USD 6.36 Billion |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

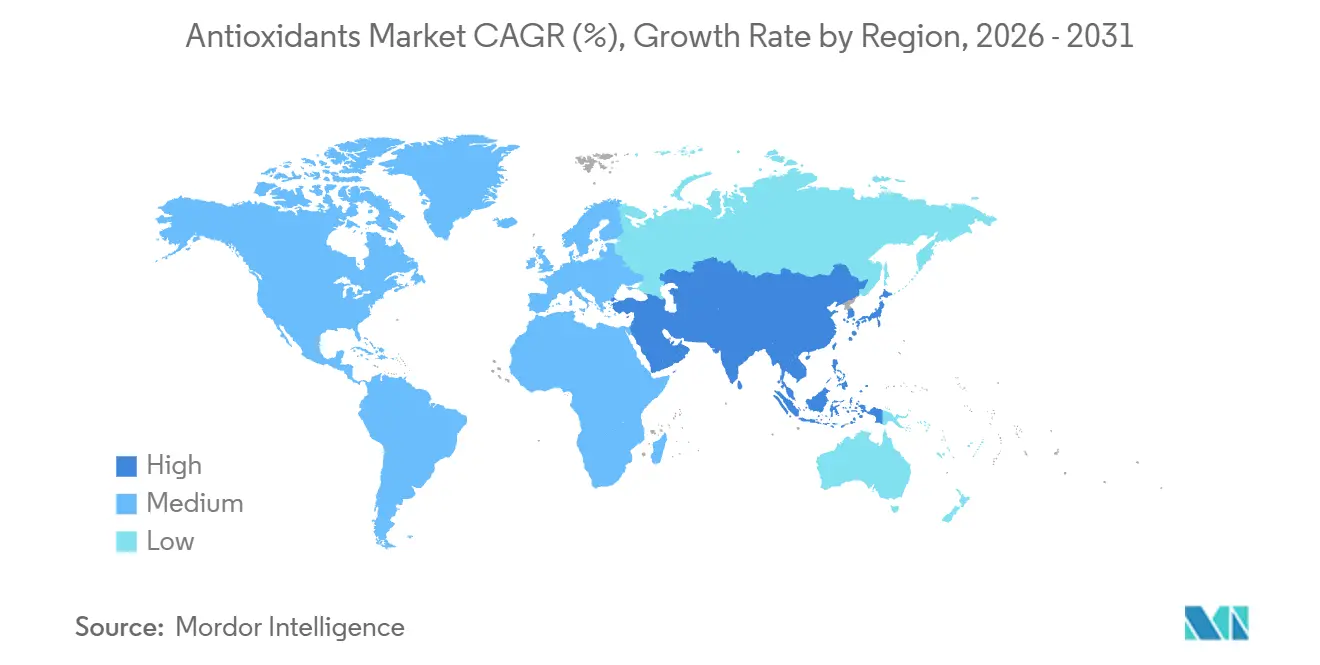

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antioxidants Market Analysis by Mordor Intelligence

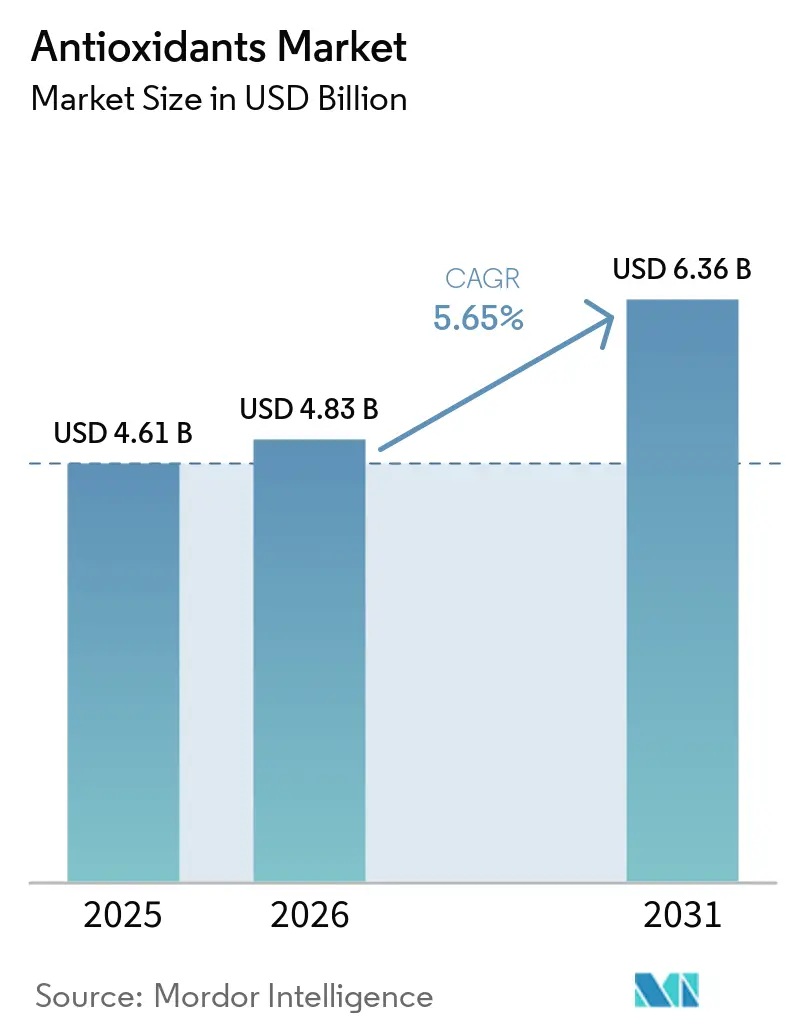

The antioxidants market, valued at USD 4.61 billion in 2025, is expected to grow to USD 4.83 billion in 2026 and reach USD 6.36 billion by 2031, with a 5.65% CAGR from 2026 to 2031. Demand spans food and beverage preservation, polymer stabilization, pharmaceuticals, and personal care, reflecting broad growth despite varying end-use trends. A key shift is the move from synthetic to natural formulations, driven by stricter U.S. food chemical reviews and Europe’s additive reevaluation. North America led the market in 2025, while Asia-Pacific is set for faster growth through 2031, highlighting reliance on mature consumption centers alongside Asia’s rising manufacturing capacity. Competition includes chemical suppliers, natural ingredient specialists, and Asian additive producers. Rianlon’s Malaysia project illustrates capacity expansion near global customers. Challenges like feedstock volatility (rosemary, green tea, tocopherol) and scrutiny of synthetic additives push suppliers to focus on traceable sourcing, regulatory compliance, and performance.

Key Report Takeaways

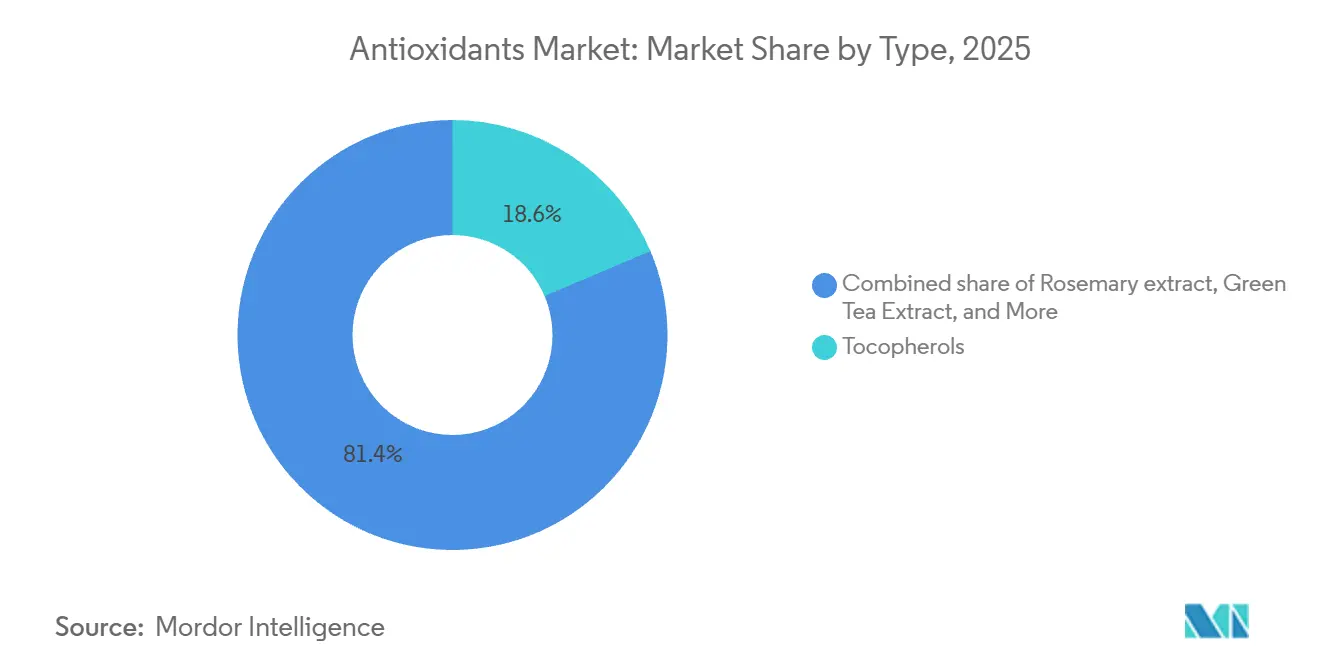

- By type, Tocopherols led with 18.62% revenue share in 2025, while Green Tea Extract is forecast to expand at a 6.8% CAGR through 2031.

- By nature, Natural Antioxidants held 43.25% share in 2025, while Synthetic Antioxidants recorded the highest projected CAGR at 7.3% through 2031.

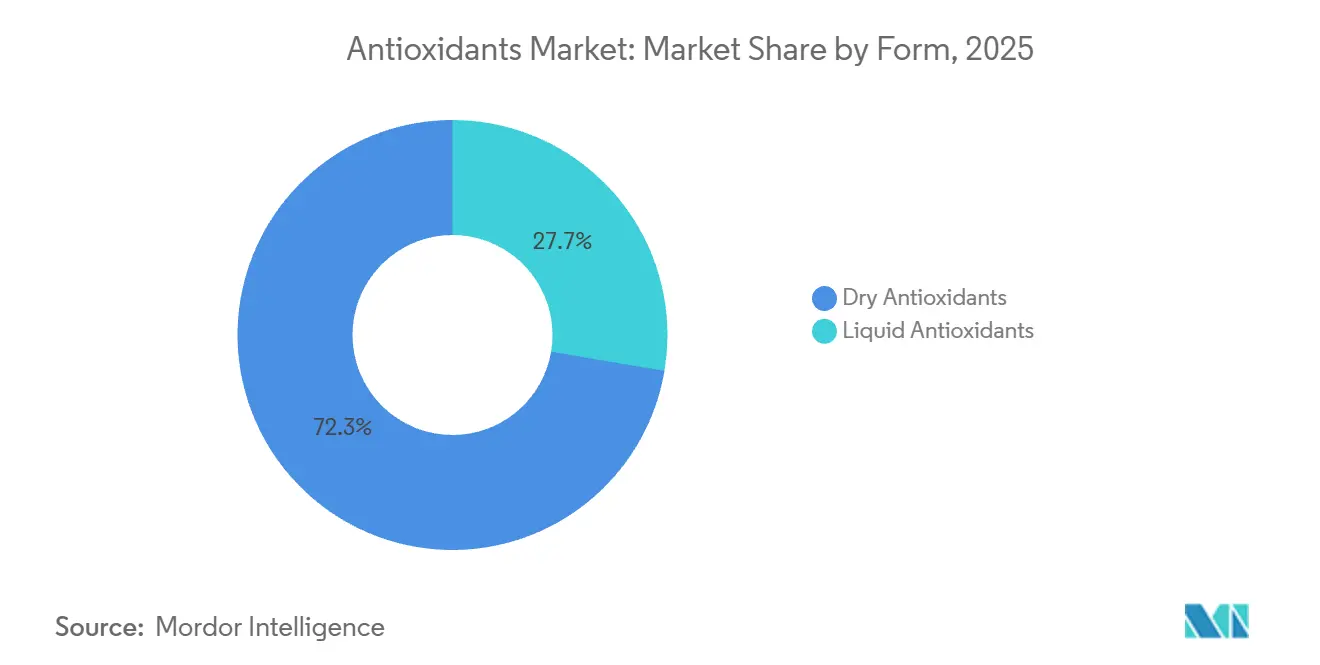

- By form, Dry Antioxidants accounted for 72.33% share in 2025, while Liquid Antioxidants are advancing at a 6.3% CAGR through 2031.

- By application, Plastic Additives accounted for a 40.45% share of the antioxidants market size in 2025, while Pharmaceuticals and Personal Care Products are forecast to grow at a 6.8% CAGR through 2031.

- By geography, North America held 33.37% of the antioxidants market share in 2025, while Asia-Pacific recorded the highest projected CAGR at 7.8% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Antioxidants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Natural Antioxidants | +1.1% | Global, with highest momentum in North America and Europe | Short term (≤ 2 years) |

| Rising Health Awareness Among Consumers | +0.9% | Global, with early gains in China, India, and Southeast Asia | Medium term (2-4 years) |

| Expansion of Functional Foods and Beverages | +0.8% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Clean-Label Ingredient Preference | +0.7% | North America and EU, with spill-over to APAC | Short term (≤ 2 years) |

| Rising Use in Nutraceuticals and Dietary Supplements | +0.6% | North America, Western Europe, Japan, Australia | Medium term (2-4 years) |

| Rising Use in Processed Foods to Prevent Oxidation | +0.5% | Global, fastest adoption in APAC emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Natural Antioxidants

The antioxidants market is shifting towards plant-based solutions in food, cosmetics, and nutraceuticals, driven by consumer demand and reformulation needs. Regulatory actions, such as the FDA's safety reassessment of BHA in February 2026 under its post-market review framework, are accelerating this trend[1]Source: U.S. Food and Drug Administration, “FDA Launches Assessment of BHA, a Common Food Chemical Preservative”, hhs.gov. Buyers are moving to natural alternatives ahead of potential restrictions. Kemin’s 2025 expansion of its rosemary-based OLESSENCE platform highlights the rising importance of vertical control, from crop development to finished ingredients, alongside formulation quality. However, the shift is uneven, with scalable ingredients offering stable supply and proven performance growing faster than niche extracts. Suppliers that ensure traceable sourcing, consistent extraction, and application support are better positioned to maintain margins in the antioxidants market.

Expansion of Functional Foods and Beverages

Functional foods and beverages are paving a wider path for antioxidants into daily consumption. Once primarily used to extend shelf life, antioxidants in these products are now increasingly associated with health, wellness, and active ingredient prominence. Research published in Discover Applied Sciences in 2025 highlighted that blends of plant-derived antioxidants, particularly combinations of polyphenols and vitamin C, exhibited a stronger ability to scavenge free radicals than individual compounds. This finding bolsters product formats that harness the synergy of multiple ingredients, allowing suppliers to provide more than just a single raw material. The strongest demand is for natural antioxidants that seamlessly integrate into beverages, supplements, and beauty products, minimizing the need for extensive reformulation. Furthermore, in the antioxidants market, this trend is enhancing the value of technical support, particularly in areas like blending, solubility, and aligning product claims.

Clean-Label Ingredient Preference

In many packaged food and beverage categories, consumers now prioritize clean-label preferences, directly impacting the antioxidants market. In 2025, Ingredion highlighted that 56% of global consumers were ready to pay a premium for products featuring recognizable ingredients. Furthermore, 38% of new food and beverage launches in the U.S. and Canada boasted a clean-label claim. This shift diminishes the acceptance of synthetic antioxidants, even in the absence of formal bans. The European Commission's agricultural and food policy framework is bolstering sustainable ingredient systems, fortifying the base for botanical antioxidants in Europe. As clean-label standards evolve, buyers increasingly demand traceability, certification, and proof of sourcing. This trend positions suppliers in the antioxidants market, especially those with robust agricultural ties and documentation, at a competitive advantage.

Rising Use in Processed Foods to Prevent Oxidation

As processed food demand surges, so does the need for antioxidants, primarily due to the vulnerabilities of extended supply chains to oxidative damage. Oxidation directly leads to issues like rancidity, flavor loss, and color changes, all of which can deter repeat purchases, challenge retailer acceptance, and increase waste. A 2025 study in Discover Food spotlighted encapsulation methods that bolster oxidative stability in edible oils, underscoring the industry's push for enhanced antioxidant efficacy during storage and processing. This need is amplified in markets where storage conditions and transport quality fluctuate by location and product type. Consequently, the demand for antioxidants is not just limited to oils and fats; it's expanding into snacks, baked goods, and ready-to-eat meals. In this landscape, suppliers in the antioxidants market who can prolong shelf life while adhering to clean-label standards are carving out a significant niche in high-demand food sectors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Compliances | -0.5% | North America and EU, with growing impact in APAC | Medium term (2-4 years) |

| Concerns Over Synthetic Antioxidant Safety | -0.3% | North America, EU, increasingly South Korea and Japan | Short term (≤ 2 years) |

| Competition from Alternative Preservation Methods | -0.3% | Global, strongest in EU and North America | Long term (≥ 4 years) |

| Consumer Skepticism Toward Isolated Antioxidant Supplements | -0.2% | North America, Northern Europe, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Compliances

Compliance pressures are increasing in the antioxidants market, especially for synthetic ingredients used in food applications. The FDA's February 2026 reassessment of BHA highlights a more active post-market approach in the U.S. State-level restrictions on BHA in school food settings are creating inconsistent regulations within the U.S. market, complicating sourcing and formulation decisions. In Europe, the ongoing re-evaluation of food additives is putting more scrutiny on ingredients without strong safety documentation. These regulatory challenges raise documentation costs, delay commercialization, and slow adoption for smaller suppliers. Larger companies, however, manage these challenges more effectively due to their regulatory teams, established files, and global customer networks.

Consumer Skepticism Toward Isolated Antioxidant Supplements

The antioxidants market also faces a demand-side limit in nutraceutical applications when consumers question isolated supplement formats. Interest in wellness products remains healthy, but buyers are becoming more selective about what they expect from single-ingredient antioxidant products. That creates a mismatch between broad demand for health-support products and lower confidence in disease-prevention style positioning for isolated supplements. Value is shifting toward blended products, food-linked formats, and daily maintenance messages that feel more practical for consumers. This change does not remove demand from the antioxidants market, but it does alter where that demand lands inside the category. Suppliers that can help customers adjust product framing, formulation, and end-use positioning are more insulated than those tied to narrow efficacy narratives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Tocopherols Anchor Cross-Sector Demand

Tocopherols captured 18.62% of the antioxidants market in 2025, which kept them as the largest type by revenue. Their lead comes from broad use across food preservation, dietary supplements, cosmetics, animal nutrition, and polymer stabilization. They offer a combination of nutritional relevance and oxidation control that reduces the need for multiple inputs in one formula. That balance keeps tocopherols central to the antioxidants industry where buyers want familiar ingredients without giving up performance. Their position is also supported by wide compatibility across different delivery formats and processing systems.

Green Tea Extract is the fastest-growing type in the antioxidants market, with a projected CAGR of 6.8% from 2026 to 2031. Growth comes from its use across functional beverages, pharmaceuticals, personal care, and dietary supplements. It benefits from demand where formulators want a visible bioactive ingredient and not only a background stabilizer. This gives Green Tea Extract a stronger role in premium products than in purely cost-driven formulations. Other types such as rosemary extract, ascorbic acid, BHA, BHT, and erythorbic acid remain important because each one still fits a specific processing need, label goal, or cost profile.

By Nature: Natural Antioxidants Lead, Industrial Demand Propels Synthetics

In 2025, Natural Antioxidants held a 43.25% share of the antioxidants market, maintaining their value-based lead. Consumers' preference for plant-based ingredients drives demand across food, personal care, and nutraceutical sectors. Europe's ongoing food additive re-evaluation has increased scrutiny on certain ingredients, indirectly favoring natural alternatives with clearer regulatory support. Within this segment, demand is uneven; tocopherols, rosemary extract, and ascorbic acid see higher reformulation demand than smaller botanicals. Suppliers with integrated agricultural sourcing and extraction capabilities are well-positioned to benefit from these market shifts.

Synthetic Antioxidants are the fastest-growing segment in the antioxidants market, with a projected CAGR of 7.25% from 2026 to 2031. This growth is mainly fueled by industrial applications like polymer stabilization, rubber processing, and fuel and lubricant systems, where natural substitutes are limited. In April 2026, BASF announced a price hike of up to 25% on antioxidants and related additives for plastic applications, reflecting strong industrial demand despite cost pressures. The segment also thrives in areas where heat resistance, long service life, and process stability outweigh clean-label concerns. While compliance demands remain high, experienced producers with technical expertise and completed regulatory work maintain a competitive edge.

By Form: Dry Variants Dominate, Liquid Innovation Expands Addressable Applications

In 2025, dry antioxidants captured a commanding 72.33% share of the antioxidants market, establishing themselves as the clear frontrunner. Their edge stems from advantages like easier handling, enhanced storage stability, precise dosing, and reduced logistics complexity. Such benefits are crucial in large-scale operations, be it bakery, confectionery, snacks, feed, or polymer processing, where automated dry blending is the norm. Furthermore, dry formats are ideal for applications demanding uniform distribution without the risk of moisture addition or viscosity alteration. This operational convenience cements the position of dry products at the forefront of the antioxidants market.

Liquid antioxidants are emerging as the fastest-growing segment in the antioxidants arena, boasting a CAGR of 6.34% projected from 2026 to 2031. Their uptake is surging in sectors like beverages, ready meals, edible oils, and personal care, where achieving uniform dispersion is paramount. Research highlighted in Discover Food showcases encapsulation techniques that shield plant polyphenols from heat, oxygen, and pH challenges, broadening the applicability of liquid antioxidant systems. Moreover, liquid formats seamlessly integrate with creams, serums, oral liquids, and emulsions, unlike powders. This compatibility paves the way for liquid antioxidants to penetrate premium formulations, where both processing simplicity and effective bioactive delivery are crucial.

By Application: Plastic Additives Dominate, Pharmaceuticals and Personal Care Accelerate

In 2025, plastic additives commanded a dominant 40.45% share of the antioxidants market, solidifying their position as the leading application segment. This dominance underscores the polymer sector's reliance on antioxidants for ensuring thermal stability, oxidative protection, and color retention, both during processing and in end-use. A 2025 study in Macromolecular Materials and Engineering highlighted the pivotal role of antioxidants in plastics, emphasizing their significance in maintaining processability and enhancing material performance. The demand for antioxidants is further bolstered by the use of recycled polymers, as these necessitate fresh antioxidant loading for re-stabilization after prior processing cycles. This interplay solidifies plastic additives as a cornerstone for the antioxidants industry.

Pharmaceuticals and personal care products are emerging as the fastest-growing segment in the antioxidants market, boasting a projected CAGR of 6.82% from 2026 to 2031. In this arena, antioxidants are increasingly featured as prominent active ingredients in serums, creams, oral products, and beauty enhancers. The segment gains traction as brands emphasize antioxidants for anti-aging, daily wellness, and scientific formulation benefits, rather than merely for preservation. Moreover, it outpaces certain food categories, thanks to shorter product cycles and heightened brand differentiation. Meanwhile, the fuel and lubricant sector remains a crucial player, as oxidation control is vital for ensuring extended service life and optimal performance in formulations.

Geography Analysis

In 2025, North America held a 33.37% share of the antioxidants market, maintaining its position as the leading regional segment. The region benefits from a strong processed food industry, high supplement demand, and growing adoption of clean-label products. The FDA's February 2026 reevaluation of BHA increased reformulation pressures on food manufacturers and highlighted the need for alternative ingredients. State-level BHA restrictions further shortened planning timelines for some buyers, increasing urgency in sourcing decisions. Mexico supports the region as both a consumption hub and production center, reflected in BASF's expansion of aminic antioxidant capacity in Puebla.

Asia-Pacific is the fastest-growing region in the antioxidants market, with a projected CAGR of 7.79% from 2026 to 2031. China drives growth with its use of antioxidants in food preservation, plastics, pharmaceuticals, personal care, and fuel and lubricants. India is expanding due to rising packaged food demand and growing nutraceutical consumption, supported by familiarity with botanical ingredients. Japan, South Korea, Australia, and Singapore contribute to premium demand for pharmaceutical and cosmetic-grade antioxidants. In 2026, Rianlon's manufacturing and R&D project in Johor, Malaysia, highlights Asia-Pacific's growing role as a production hub, beyond being just a demand center[2]Source: Malaysian Investment Development Authority, “Rianlon Malaysia Breaks Ground on RM1.27 Billion R&D and Manufacturing Base in Johor”, mida.gov.my .

Europe remains the second-largest region in the antioxidants market, supported by its established food processing, polymer, and pharmaceutical industries. Growth in the region is driven by food additive reevaluations and policies promoting sustainable agricultural practices, which strengthen the use of botanical raw materials. South America, led by Brazil and Argentina, is growing through food exports, industrialization, and soy-linked tocopherol supply. The Middle East and Africa, though smaller in market value, see steady demand from packaged food retail, tourism-related food services, and livestock applications.

Competitive Landscape

The antioxidants market is moderately consolidated, with a few global manufacturers dominating while regional suppliers focus on niche applications. Key players like BASF SE, Koninklijke DSM N.V., Archer Daniels Midland Company, Kemin Industries, Inc., and International Flavors and Fragrances Inc. use their broad product ranges, global sourcing, advanced research, and strong industry ties to serve diverse customer needs across food, beverage, dietary supplements, animal nutrition, and personal care sectors. Their ability to supply both natural and synthetic antioxidants supports their wide market reach.

Competition centers on innovation, clean-label products, and demand for natural antioxidants. Manufacturers are investing in plant-based solutions from fruits, vegetables, herbs, and spices to meet consumer preferences. They are also improving antioxidant efficacy, stability, and functionality using advanced technologies. In the nutraceutical and functional food sectors, regulatory compliance, traceability, and validated health benefits are key differentiators.

Strategic acquisitions, partnerships, and portfolio expansions are helping companies strengthen their positions and enter high-growth areas. Leading players focus on customized solutions for food preservation, dietary supplements, animal feed, cosmetics, and pharmaceuticals. Large multinationals benefit from economies of scale and distribution networks, while niche suppliers compete with targeted innovations. As demand for health-focused, clean-label, and shelf-life-enhancing ingredients grows, companies are increasing investments in product development, sustainability, and supply chain improvements to maintain their edge.

Antioxidants Industry Leaders

BASF SE

Koninklijke DSM N.V.

Archer Daniels Midland Company

Kemin Industries, Inc.

International Flavors and Fragrances Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: BASF SE expanded global production capacities for both standard and NOR HALS light stabilizers and antioxidant systems for plastics, targeting rising demand for durability in outdoor, agricultural film, and UV-exposed polymer applications. The expansion supports BASF's NOR HALS platform, which addresses stricter weatherability standards across automotive, construction, and plasticulture sectors.

- March 2026: Biesterfeld SE expanded its distribution agreement with Songwon, adding the Baltic States, Bulgaria, Bosnia-Herzegovina, Croatia, Kosovo, North Macedonia, Montenegro, Serbia, Slovenia, Ukraine, and Romania to the coverage of Songwon's SONGNOX CS antioxidant product lines, extending Songwon's European market reach across Southeast Europe.

- January 2026: Rianlon Corporation invested USD 285 million in research and development (R&D) and established a manufacturing base in Johor, Malaysia. This facility marks the company's first major integrated site outside of China, focusing on the production of polymer antioxidant additives and lubricant additives for both the Southeast Asian and global markets.

Global Antioxidants Market Report Scope

| Tocopherols |

| Rosemary extract |

| Green Tea Extract |

| Butylated hydroxyanisole (BHA) |

| Butylated hydroxytoluene (BHT) |

| Erythorbic acid and Derivatives |

| Ascorbic acid |

| Others |

| Natural Antioxidants |

| Synthetic Antioxidants |

| Dry Antioxidants |

| Liquid Antioxidants |

| Food and Beverage |

| Pharmaceuticals and Personal Care Products |

| Fuel and Lubricant |

| Plastic Additives |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Tocopherols | |

| Rosemary extract | ||

| Green Tea Extract | ||

| Butylated hydroxyanisole (BHA) | ||

| Butylated hydroxytoluene (BHT) | ||

| Erythorbic acid and Derivatives | ||

| Ascorbic acid | ||

| Others | ||

| By Nature | Natural Antioxidants | |

| Synthetic Antioxidants | ||

| By Form | Dry Antioxidants | |

| Liquid Antioxidants | ||

| By Application | Food and Beverage | |

| Pharmaceuticals and Personal Care Products | ||

| Fuel and Lubricant | ||

| Plastic Additives | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of the antioxidants market by 2031?

The antioxidants market is forecast to reach USD 6.36 billion by 2031, up from USD 4.83 billion in 2026, at a 5.65% CAGR over 2026-2031.

Which region leads antioxidants demand today?

North America led in 2025 with a 33.37% share, supported by processed food demand, supplement use, and faster reformulation activity.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to grow at 7.79% CAGR through 2031, driven mainly by China and India across food, plastics, and health-related applications.

What is the biggest product type in antioxidants?

Tocopherols was the leading type in 2025 with 18.62% share due to wide use across food, supplements, cosmetics, and polymer stabilization.

Page last updated on: