Natural Food Preservatives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.01 Billion |

| Market Size (2031) | USD 2.76 Billion |

| Growth Rate (2026 - 2031) | 6.53% CAGR |

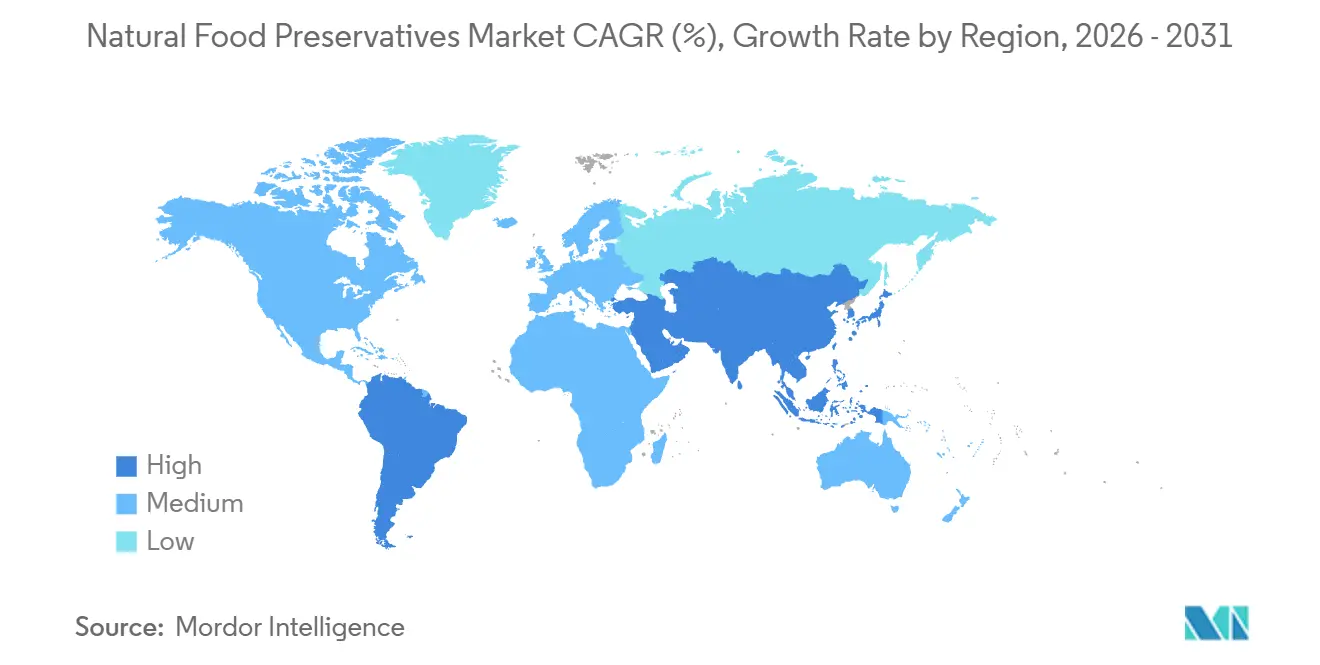

| Fastest Growing Market | South America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Natural Food Preservatives Market Analysis by Mordor Intelligence

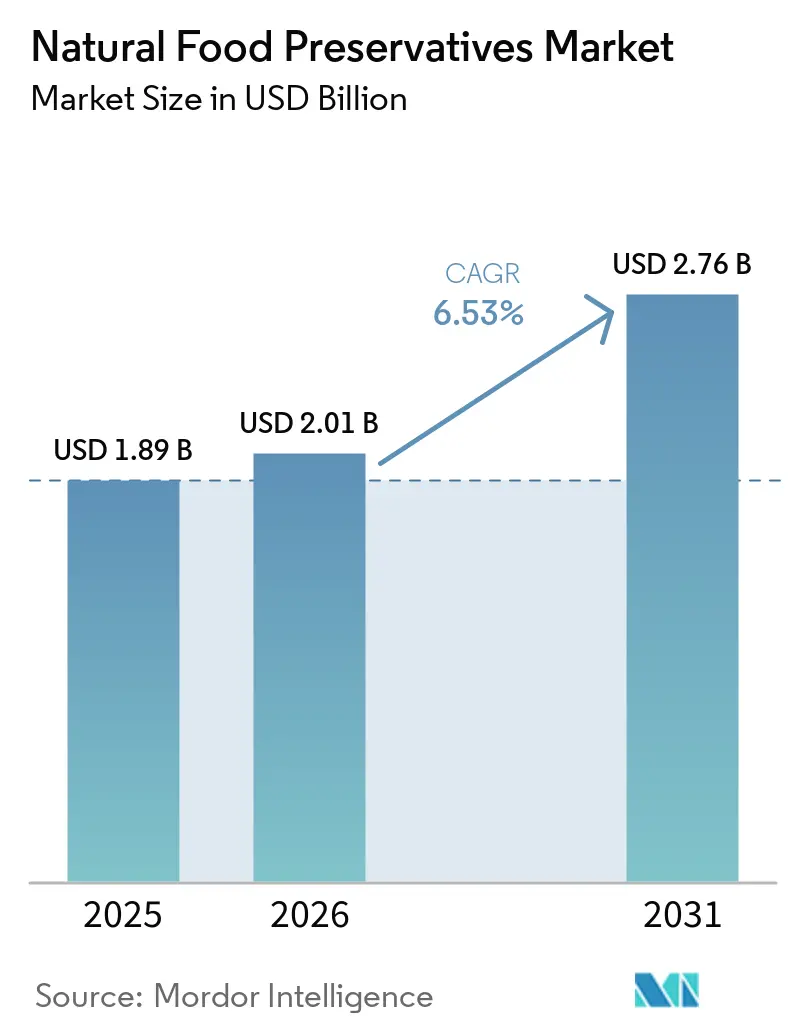

The natural food preservatives market size is projected to expand from USD 1.89 billion in 2025 and USD 2.01 billion in 2026 to USD 2.76 billion by 2031, registering a CAGR of 6.5% between 2026 to 2031. Food manufacturers are replacing synthetic antioxidants and antimicrobials with plant-based, fermentation, and microbial alternatives to meet clean-label demands. In the U.S., the FDA's 2026 Human Foods Program prioritizes reducing petroleum-based additives and fast-tracking natural alternatives, driving reformulation in packaged foods. Retailer rules now require private-label clean-label standards, influencing supplier approvals early. Organic food sales in the U.S. reached USD 70.1 billion in 2025, increasing demand for preservative systems that meet strict ingredient and certification standards. Competition now favors suppliers with regulatory compliance, organic compatibility, stable sourcing, and scalable fermentation or botanical extraction capabilities.

Key Report Takeaways

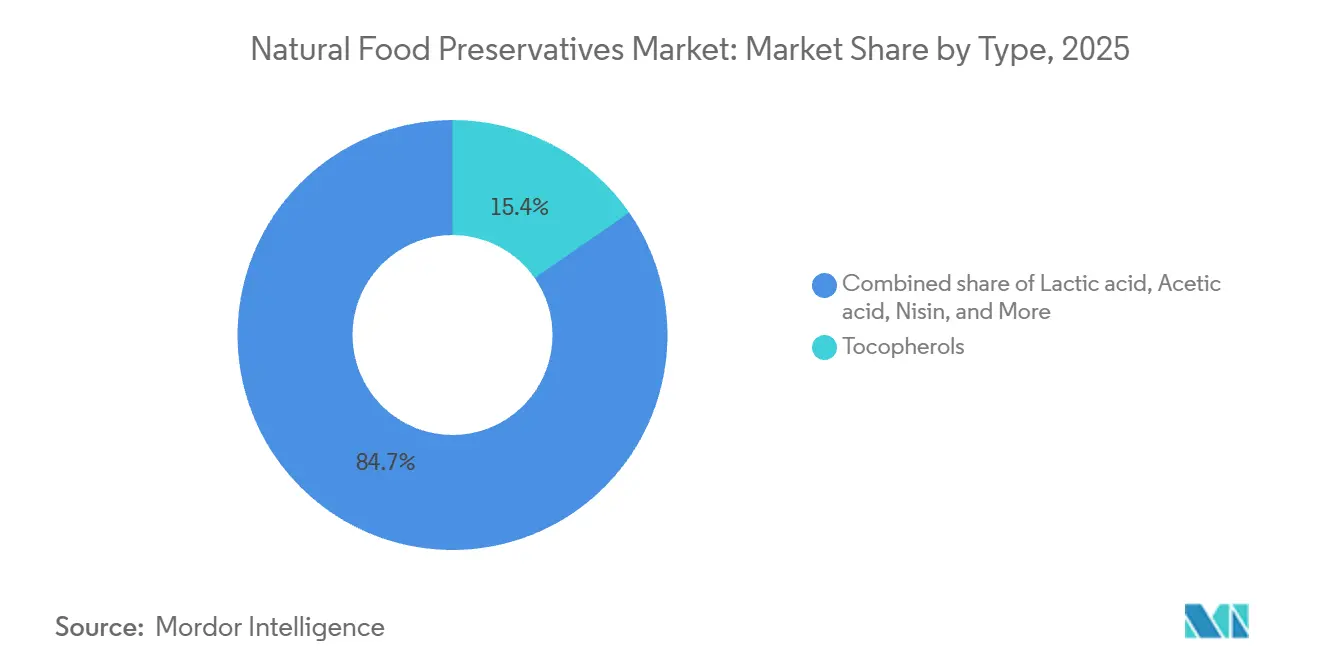

- By type, tocopherols held 15.4% share in 2025, while lactic acid is projected to expand at 8.5% CAGR through 2031.

- By function, antioxidants accounted for 58.1% of the natural food preservatives market size in 2025, while antimicrobials are forecast to grow at 7.7% CAGR through 2031.

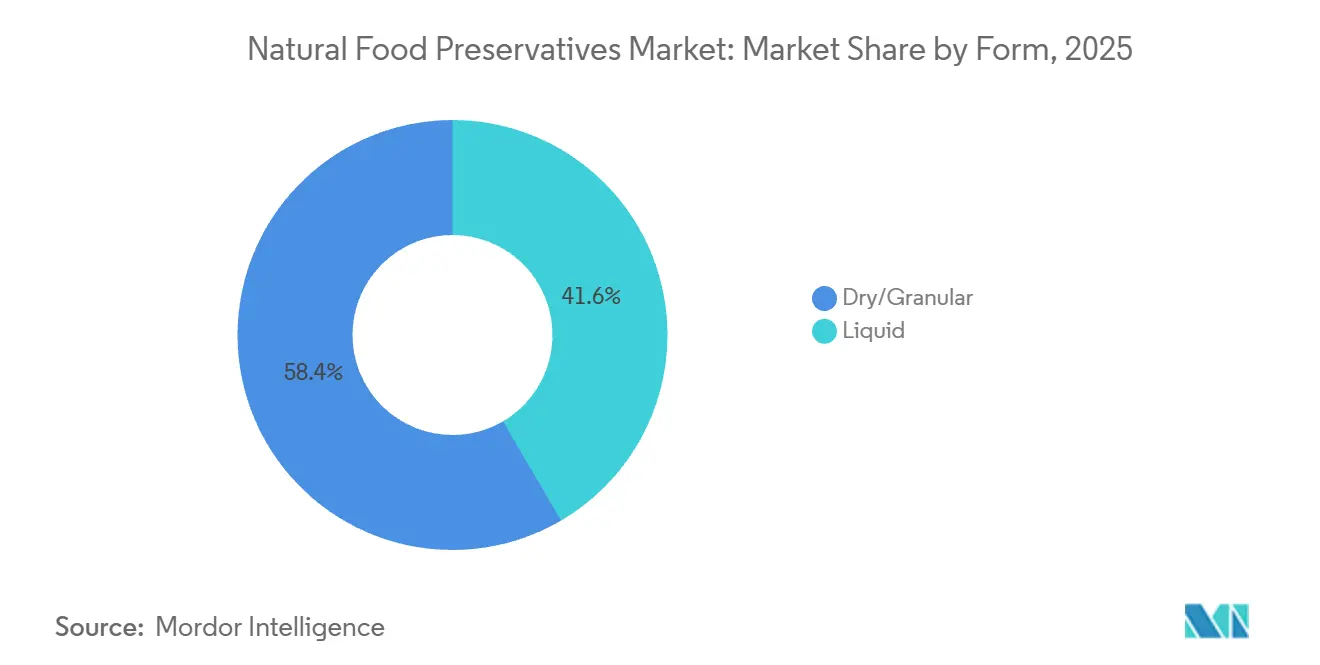

- By form, dry and granular products held 58.4% share in 2025, while liquid formats are projected to grow at 7.8% CAGR through 2031.

- By application, meat and meat alternatives accounted for 24.5% of the natural food preservatives market size in 2025, while snacks and cereals are forecast to expand at 9.3% CAGR through 2031.

- By geography, North America held 35.8% of the natural food preservatives market share in 2025, while South America is set to advance at 7.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Natural Food Preservatives Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Health Consciousness And Clean-Label Movement | +1.7% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Innovation In Natural Preservation Technologies | +1.2% | Global | Medium term (2-4 years) |

| Expansion Of The Organic And Natural Food Industry | +1.0% | North America, Europe, APAC | Medium term (2-4 years) |

| Increasing Consumption Of Processed And Convenience Foods | +1.1% | Asia-Pacific, South America, MEA | Short term (≤ 2 years) |

| Sustainability And Eco-Friendly Sourcing Trends | +0.7% | Europe, North America | Medium term (2-4 years) |

| Demand For Gluten-Free And Allergen-Free Preservatives | +0.5% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Health Consciousness and Clean-Label Movement

In the natural food preservatives market, clean-label demand has emerged as a dominant trend, driven by a unified push from retailers, regulators, and consumers alike. EU Regulation 1169/2011 mandates the disclosure of additives on food labels, enhancing the visibility of preservative choices at the point of sale and increasing the costs associated with synthetic systems[1]Source: European Union, “Regulation (EU) No 1169/2011 on the Provision of Food Information to Consumers”, eur-lex.europa.eu. Meanwhile, in the U.S., the FDA's 2026 priority agenda lends direct policy support to the evaluation of natural alternatives, steering away from petroleum-based additives. This confluence of regulations and consumer preferences has led food manufacturers to be as responsive to procurement rules as they are to market demands. A notable shift occurs when a leading retailer eliminates synthetic preservatives from its private-label standards; this decision triggers a ripple effect, exerting reformulation pressure on contract manufacturers, ingredient suppliers, and branded food companies simultaneously.

Innovation in Natural Preservation Technologies

Technology is narrowing the performance gap that once limited the natural food preservatives market to premium uses. Research published by the Royal Society of Chemistry in 2026 shows that natural extract and biopolymer-based antimicrobial packaging systems can reduce spoilage and extend shelf life, especially when paired with broader preservation tools. Springer Nature also reported in 2026 that AI-assisted delivery optimization is improving the way essential oil bio-preservatives are applied across different food matrices. These advances matter because they shift natural preservation from a narrow ingredient conversation to a platform and process conversation. Suppliers with strength in precision fermentation, encapsulation, and formulation control are therefore building positions that are harder for commodity producers to copy.

Expansion of the Organic and Natural Food Industry

As organic food sales surge, they're driving heightened demand in the natural food preservatives market. It's no longer just about cleaner labels; there's a growing emphasis on ingredient systems that adhere to certification standards. In 2025, U.S. organic food sales hit USD 70.1 billion, marking a robust 6.9% growth, outpacing the broader food market[2]Source: Organic Trade Association, “U.S. Organic Marketplace Achieved Significant Growth in 2025”, ota.com. The Food and Agriculture Organization reported over 350,000 organic producers in Latin America as of 2024, underscoring the region's significance as a deepening source of certified agricultural supply. This is crucial: not all naturally derived preservatives qualify for organic formulations, narrowing the pool of eligible suppliers. Consequently, companies providing organic-compatible and traceable preservation systems are poised for stronger pricing power and more stable customer ties.

Increasing Consumption of Processed and Convenience Foods

Emerging economies are increasingly turning to natural food preservatives, not just for premium clean-label packaging, but for broader applications. According to USDA data, India's demand for packaged food is set to hit USD 175 billion by 2030, bolstered by supportive policy measures for local processing[3]Source: USDA Foreign Agricultural Service, “Food Processing Ingredients Annual, India”, apps.fas.usda.gov. In several of these markets, the combination of elevated ambient temperatures and underdeveloped cold chains elevates shelf-life control from a mere branding choice to a critical food safety necessity. An FAO analysis highlights that a prolonged shelf life is a pivotal commercial attribute in ultra-processed foods, underscoring the importance of preservation performance in manufacturing economics. This trend steers demand towards solutions that harmonize label standards with microbiological reliability in genuine distribution scenarios. Consequently, the natural food preservatives market is poised for growth, especially in value segments where purchasing decisions hinge on waste reduction and regulatory compliance, alongside consumer perception.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Production And Processing Costs | -0.9% | Global | Short term (≤ 2 years) |

| Limited Shelf Life And Efficacy Compared To Synthetic Preservatives | -0.8% | Global | Medium term (2-4 years) |

| Supply Chain Volatility And Raw Material Availability | -0.7% | Asia-Pacific, South America, MEA | Medium term (2-4 years) |

| Stringent Regulatory Approval And Compliance Hurdles | -0.5% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Production and Processing Costs

Cost remains the clearest short-term brake on the natural food preservatives market, especially in price-sensitive food categories. Fermentation processes need controlled infrastructure, while botanical extracts require standardized active-compound levels and stronger quality checks to deliver repeatable performance. That burden is more visible in developing markets, where synthetic preservatives can still cost far less on a functional basis in mass-volume products. The gap does narrow when multinational food companies evaluate sustainability and broader cost of ownership, but that shift is gradual rather than immediate. For now, premium products, export-oriented lines, and categories with strict label standards are still the easiest places for natural systems to win.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Production And Processing Costs | -0.9% | Global | Short term (≤ 2 years) |

| Limited Shelf Life And Efficacy Compared To Synthetic Preservatives | -0.8% | Global | Medium term (2-4 years) |

| Supply Chain Volatility And Raw Material Availability | -0.7% | Asia-Pacific, South America, MEA | Medium term (2-4 years) |

| Stringent Regulatory Approval And Compliance Hurdles | -0.5% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Shelf Life and Efficacy Compared to Synthetic Preservatives

The natural food preservatives market also faces a technical ceiling in applications that need very broad antimicrobial action or long shelf stability under harsh processing conditions. Natural preservatives are often more sensitive to heat, light, and pH, which can complicate direct replacement of synthetic systems in extended-shelf-life foods. Research published by Springer Nature in 2025 found that single-agent natural antimicrobials often require higher minimum inhibitory concentrations than synthetic alternatives, which can raise cost and create sensory trade-offs at effective doses. This is why many food companies move toward multi-hurdle strategies that combine more than one preservative mechanism rather than relying on a single natural input. That approach improves performance, but it also adds formulation work and slows broad penetration in lower-value applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Tocopherols Lead While Lactic Acid Accelerates

In 2025, tocopherols held 15.4% of the natural food preservatives market, making them the top ingredient type. Their dominance stems from their use in edible oils, processed meats, bakery items, and snacks, where oxidation control is essential for shelf life. Tocopherols also serve as Vitamin E-related components, offering a "cleaner label" profile. This dual role helps suppliers replace BHA and BHT with familiar alternatives. Other ingredients play specific roles in the market. Rosemary extract and ascorbic acid aid oxidation control, while buffered vinegar and acetic acid provide antimicrobial benefits in meats and baked goods. Green tea extract is gaining traction in premium and functional foods, combining polyphenol benefits with preservation.

Lactic acid is the fastest-growing ingredient, with an 8.5% CAGR through 2031, driven by the adoption of fermentation-based preservation in food safety programs. A 2025 Frontiers in Microbiology study highlighted lactic acid bacteria's role in reducing meat spoilage, supporting its use in premium proteins. A 2026 study showed cell-free extracts from these bacteria effectively combat dairy contaminants. Galactic’s 2025 Impact Report emphasized its focus on circular economy goals to meet rising lactic acid demand. Broad GRAS acceptance in the U.S. further ensures its scalability for food applications.

By Function: Antioxidants Hold the Core, Antimicrobials Expand Faster

Antioxidants held 58.1% of the natural food preservatives market size in 2025, which reflects their central role in foods where rancidity is the first shelf-life problem to address. Mixed tocopherols and rosemary extract remain the main natural antioxidant systems in oils, snacks, meats, and related packaged foods. Their progress has been supported by retailer efforts to remove synthetic antioxidants from private-label formulas and by wider regulatory attention on synthetic additive exposure. ADM reinforced that direction in January 2026 by announcing a USD 26 million investment in its Erlanger, Kentucky facility to support growing reformulation demand in food and beverage applications.

Antimicrobials are projected to grow at 7.7% CAGR through 2031, making them the faster-moving functional segment in the natural food preservatives market. Growth is strongest in meat, dairy, and ready-meal applications where pathogen control is as important as label simplification. Nisin and natamycin already hold established roles in dairy and cheese, while bacteriocin-based systems and fermentate solutions are extending into produce and protein applications. Research from the Universidad de Zaragoza in 2025 showed that lactic acid bacteria cell-free supernatants preserved fresh-cut produce for up to 12 days while maintaining quality and sensory properties. This functional expansion suggests that natural antimicrobial demand is no longer confined to traditional dairy niches.

By Form: Dry Formats Stay Dominant While Liquids Gain Use Cases

Dry and granular formats held 58.4% of the natural food preservatives market size in 2025, which kept them ahead of liquid products in industrial food processing. Their lead comes from better storage stability, cleaner handling in bulk manufacturing, and easier dosing in powder blending systems used across bakery, snack, and seasoning lines. Dry preservatives also avoid the water activity complications that can arise when liquid inputs are added to moisture-sensitive foods. Kemin’s NaturCEASE Dry shows how suppliers are combining buffered vinegar and plant extracts in a dry format to serve processed meat applications that need both clean-label positioning and operational ease.

Liquid forms are expected to grow at 7.8% CAGR through 2031, making them the faster-rising format in the natural food preservatives market. Demand is being lifted by beverages, dairy, and fresh produce applications where inline dosing and homogeneous distribution matter more than dry handling convenience. Continuous-flow production in modern beverage and dairy plants is a strong fit for liquid preservatives with defined concentration and reproducible activity. Encapsulated liquid systems also offer a premium path, because they can protect active compounds during processing and release them later when conditions are more favorable. That combination should keep liquid formats gaining share even while dry products remain the larger base.

By Application: Processed Meats Lead Volume While Snacks and Cereals Grow Fastest

In 2025, meat and alternatives led the natural food preservatives market, comprising 24.5% of its size. Protein-rich, moisture-heavy foods like meats face microbial spoilage and lipid oxidation, requiring multiple preservation methods. Suppliers offering integrated systems benefit, as performance testing, sensory balance, and regulatory compliance are critical. Plant-based meats, with unique moisture and fat systems, demand tailored preservation solutions, creating opportunities for customized formulations. Research in 2026 by Springer Nature highlighted Lactiplantibacillus plantarum bacteriocins in beef, supporting lactic acid bacteria as bio-preservatives in protein applications.

Snacks and cereals are projected to grow at a 9.3% CAGR through 2031, making them the fastest-growing segment in the natural food preservatives market. Growth stems from clean-label snacking, cereal reformulations, and reduced artificial additives in retail. High-oil snacks drive demand for tocopherols and rosemary extract. Private-label programs adopting "no artificial preservatives" expand natural preservative use to larger stock-keeping units. This application mix balances steady demand with growth opportunities. Bakery relies on fermentation-based mold inhibitors and buffered acids, while dairy uses nisin and natamycin for clean-label positioning. Sauces, dressings, and condiments offer reformulation potential, replacing synthetic systems with natural acids and antioxidants. Growth is strongest where shelf-life risks and label pressures are high.

Geography Analysis

In 2025, North America held a 35.8% share of the natural food preservatives market, leading globally. This dominance stems from a strong packaged food industry, significant private-label influence, and a wide range of organic and clean-label brands. In the U.S., the FDA's 2026 agenda promotes a faster shift to natural alternatives, driving reformulations in major food categories. Additionally, U.S. organic food sales reached USD 70.1 billion in 2025, boosting demand for preservative systems that meet strict ingredient and certification standards.

Europe is the second-largest market for natural food preservatives, with Germany, France, and the U.K. as key food processing hubs. EU labeling rules requiring full additive disclosure enhance ingredient transparency, making synthetic preservatives more noticeable to buyers and retailers. This regulatory framework is driving a shift toward cleaner-label antioxidant and antimicrobial systems in packaged foods. Poland, Belgium, and the Netherlands strengthen manufacturing, especially as mid-tier processors adjust formulations to meet retailer demands. Asia-Pacific is emerging as a major growth region, driven by China's urban packaged food demand, India's modernization of food processing, and South Korea's focus on ingredient innovation. USDA data projects India's packaged food demand to reach USD 175 billion by 2030, highlighting a growing need for shelf-life solutions in local manufacturing.

South America is expected to grow at a 7.5% CAGR through 2031, making it the fastest-growing region in the natural food preservatives market. Brazil leads this growth, with USDA data reporting food processing revenue of USD 248 billion in 2025 and annual growth of 8%. While Argentina, Colombia, Chile, and Peru are smaller markets, premium retail expansion and export-oriented processing are increasing interest in cleaner preservation systems. In the Middle East and Africa, urban markets like South Africa, Saudi Arabia, and the UAE are adopting natural food preservatives due to modern retail growth. However, cost and infrastructure challenges limit broader market penetration.

Competitive Landscape

The Natural Food Preservatives Market is moderately consolidated, with a few multinational ingredient companies holding a significant share of global revenue. Companies like Cargill, Incorporated, Kerry Group plc, Koninklijke DSM N.V., Kemin Industries, Inc., and Corbion leverage extensive product portfolios, strong distribution networks, and advanced research to meet growing demand for clean-label, naturally derived ingredients. Their integrated preservation solutions across food and beverage categories strengthen their market positions.

Corbion and Kemin Industries lead with expertise in natural preservation technologies, including fermentation-derived ingredients, organic acids, plant extracts, and antimicrobial solutions. Kerry Group combines preservation with flavor and quality enhancement through its broad taste and nutrition portfolio. Cargill supports manufacturers with natural alternatives to synthetic preservatives, while DSM focuses on science-based solutions to improve food safety, shelf life, and stability.

Competition centers on innovation, clean-label product development, and meeting regulatory and consumer demands. Leading companies invest in R&D, partnerships, and product launches to expand offerings and strengthen their presence. Emerging suppliers and niche manufacturers add competitive intensity by providing specialized solutions, maintaining the market’s moderately consolidated structure.

Natural Food Preservatives Industry Leaders

Cargill, Incorporated

Kerry Group plc

Koninklijke DSM N.V.

Kemin Industries, Inc.

Corbion

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: IFF expanded its Latin American footprint by transforming the Arroyito site in Argentina into its first full fermentation-based enzyme production hub in the region, and opened a new application laboratory in Brazil, enhancing regional supply chain resilience for fermentation-derived food and beverage ingredients.

- January 2026: ADM announced a USD 26 million investment in its Erlanger, Kentucky facility to expand capabilities in response to growing food and beverage reformulation demand, building on a USD 15 million investment at the same site in 2025 that expanded the Customer Creation and Innovation Center.

- October 2025: IFF and BASF announced a strategic collaboration to co-develop next-generation enzyme technologies and biobased polymer innovations, combining BASF's chemical engineering expertise with IFF's biotechnology capabilities to develop sustainable, high-performance ingredient solutions.

Global Natural Food Preservatives Market Report Scope

| Tocopherols |

| Rosemary extract |

| Lactic acid |

| Acetic acid |

| Nisin |

| Natamycin |

| Green Tea Extract |

| Citric acid |

| Ascorbic acid |

| Buffered Vinegar |

| Others |

| Antimicrobials |

| Antioxidants |

| Dry/Granular |

| Liquid |

| Bakery |

| Confectionery |

| Dairy and Dairy Alternatives |

| Beverages |

| Meat and Meat Alternatives |

| Snacks and Cereals |

| Sauces, Dressings, and Condiments |

| Fats and Oil |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Tocopherols | |

| Rosemary extract | ||

| Lactic acid | ||

| Acetic acid | ||

| Nisin | ||

| Natamycin | ||

| Green Tea Extract | ||

| Citric acid | ||

| Ascorbic acid | ||

| Buffered Vinegar | ||

| Others | ||

| By Function | Antimicrobials | |

| Antioxidants | ||

| By Form | Dry/Granular | |

| Liquid | ||

| By Application | Bakery | |

| Confectionery | ||

| Dairy and Dairy Alternatives | ||

| Beverages | ||

| Meat and Meat Alternatives | ||

| Snacks and Cereals | ||

| Sauces, Dressings, and Condiments | ||

| Fats and Oil | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 outlook for natural food preservatives?

The natural food preservatives market is projected to reach USD 2.76 billion by 2031 from USD 2.01 billion in 2026, growing at a 6.53% CAGR over 2026 to 2031.

Which region currently leads demand?

North America led with 35.76% share in 2025, supported by large packaged food volumes, retailer clean-label mandates, and strong organic food demand.

Which ingredient type is growing the fastest?

Lactic acid is the fastest-growing ingredient type with an 8.48% CAGR through 2031, supported by wider acceptance of fermentation-based food safety solutions.

Which application is expanding the quickest?

Snacks and cereals are projected to grow at 9.31% CAGR through 2031 as mainstream brands remove artificial preservatives and reformulate higher-oil snack products.

Page last updated on: